A Novel Algorithmic Forex Trade and Trend Analysis Framework Based on Deep Predictive Coding Network Optimized with Reptile Search Algorithm

,

,  and

and

Abstract

:1. Introduction

2. Literature Survey

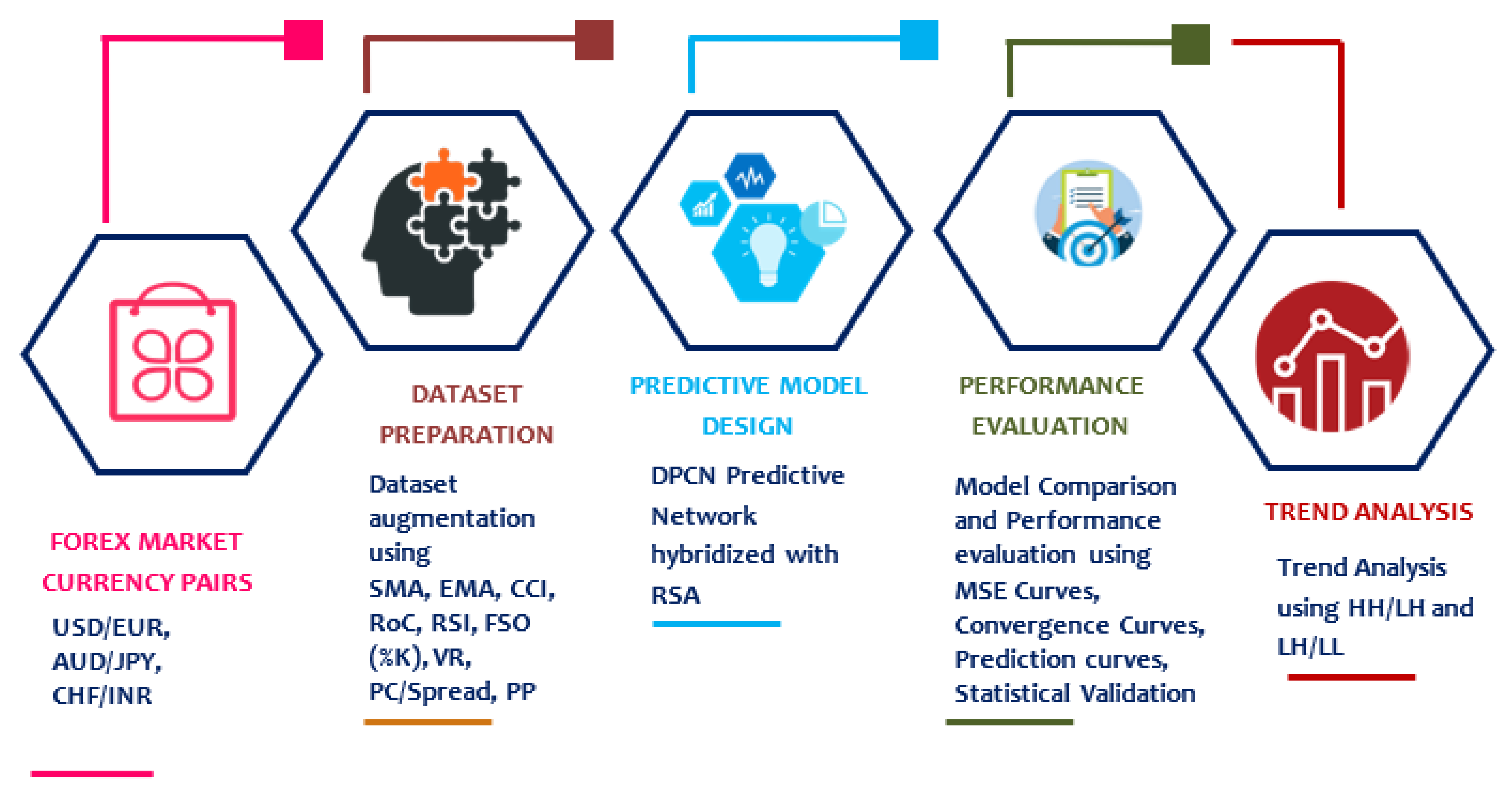

3. Materials and Methods

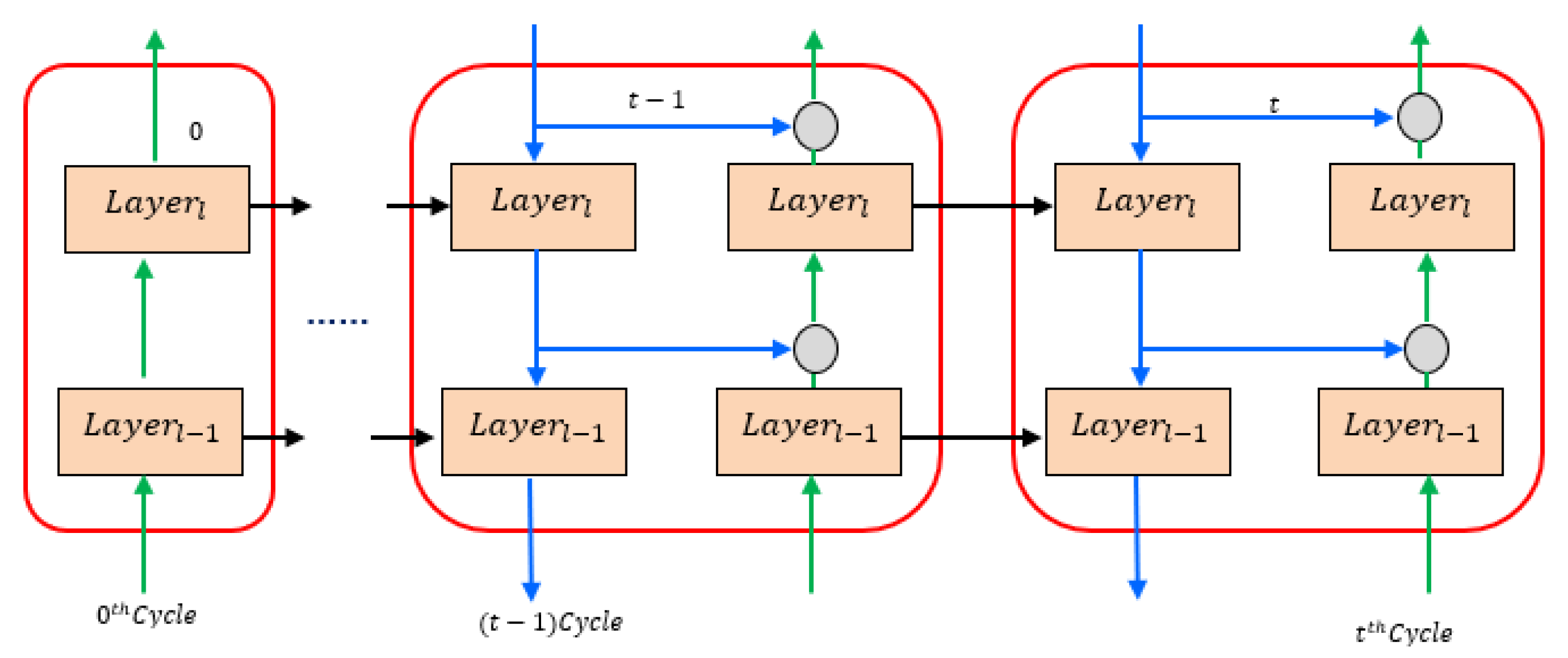

3.1. Architecture and Model Description of DPCN

3.2. RSA Optimization Strategy

- 1.

- Initialization Phase: In this phase, the process starts with a set of candidate solutions () generated stochastically to obtain the nearly optimum best solution at each iteration and is represented in Equation (10).where, is a randomly generated set of candidate solutions, is the candidate solutions, is dimension size of the given problem, represents the position of the solution and can be computed using Equation (11), where is a random value and , represents the lower and upper bound of the given problem.

- 2.

- Encircling Phase: This phase deals with the exploratory behavior or encircling of RSA with two movements of crocodiles, such as high walking and belly walking, which do not allow them to approach the target prey, and the exploration search discovers a wide search area due to this movement behavior of the crocodiles. This exploration through high and belly walking is only used to support other phases of operation, such as hunting or exploration. The RSA makes a change between exploration and exploitation in search phases based on various behaviors in four conditions by dividing the number of iterations into four parts. The objective of exploration or encircling is to obtain a better solution based on the movement, and searching is done on two conditions such as (i) for high walking and (ii) and for belly walking. The position updating is done using Equation (12) during the exploration phase.where, is position of the best obtained solution so far, rand is a random number between 0 and 1, is the current iteration number, maximum number of iterations is , represents the hunting operation of the position in the solution and is computed using Equation (13). The sensitive parameter is used to control the exploration accuracy (high walking) for encircling phase over the course of iterations, which is fixed equal to 0.1, the is a reduced function used to reduce the search space and is calculated using Equation (14), is the random number between [1 and CS] and the random position of the solution is denoted as . The evolutionary sense is a probability ratio considering values between [2 and −2] throughout the number of iterations and can be calculated using Equation (15).where, is a small value, is a random number between [1 to CS], 2 is a correlation value which gives a value between [2 and 0], is another random number between [−1 to 1]. The percentage difference between position of the best solution and position of the current solution is represented as and is calculated using Equation (16).where, denotes the average position of solution calculated using Equation (17), are the upper and lower bounds of position, controls the exploration accuracy i.e., difference between the candidate solutions for hunting co-operation and is fixed to 0.1.

- 3.

- Hunting Phase: This phase simulates crocodiles’ hunting strategy, such as coordination and cooperation, which allows them to target the prey quickly. These two phases obtain the near-optimal solution after several actions and establish the communication between them, and the RSA exploits those two main strategies based on Equation (18). The searching is based on hunting coordination conditioned on, otherwise the hunting coordination is done when .where, is position of the best obtained solution so far, are computed using Equation (13), Equation (16), and Equation (14), respectively, and is a very small value. The sensitive parameters and α are chosen carefully to produce a stochastic value at each iteration and it handles the exploration for all the iterations and is advantageous to overcome the local optima, particularly in last iteration. The computational complexity of RSA algorithm can be given as, where , and represent the number of iterations, number of solutions, and solution size, respectively.

3.3. Dataset Preparation and Augmentation

3.4. Parameters Used

3.5. Model Description and Proposed RSA-DPCN Algorithm

| Algorithm 1: RSA-DPCN forecasting model |

| Initialize the sensitive parameters [Controls the exploration accuracy for hunting cooperation and high walking for encircling phases over the course of iterations respectively and both are set to 0.1] Initialize decision variables Feed forward kernel size; Feedback kernel size; Up-sample scale factor; While: Meet termination condition Calculate MSE from DPCN model; Find minimum MSE for [Number of candidate solutions] Update ; [Hunting operator, Reduce function used to reduce the search space and Percentage Difference between the best obtained solution and current solution respectively] if then High Walking; else if Belly Walking; else if Hunting Co-ordination; else Hunting Co-operation; end if end for end while |

4. Experiments and Results

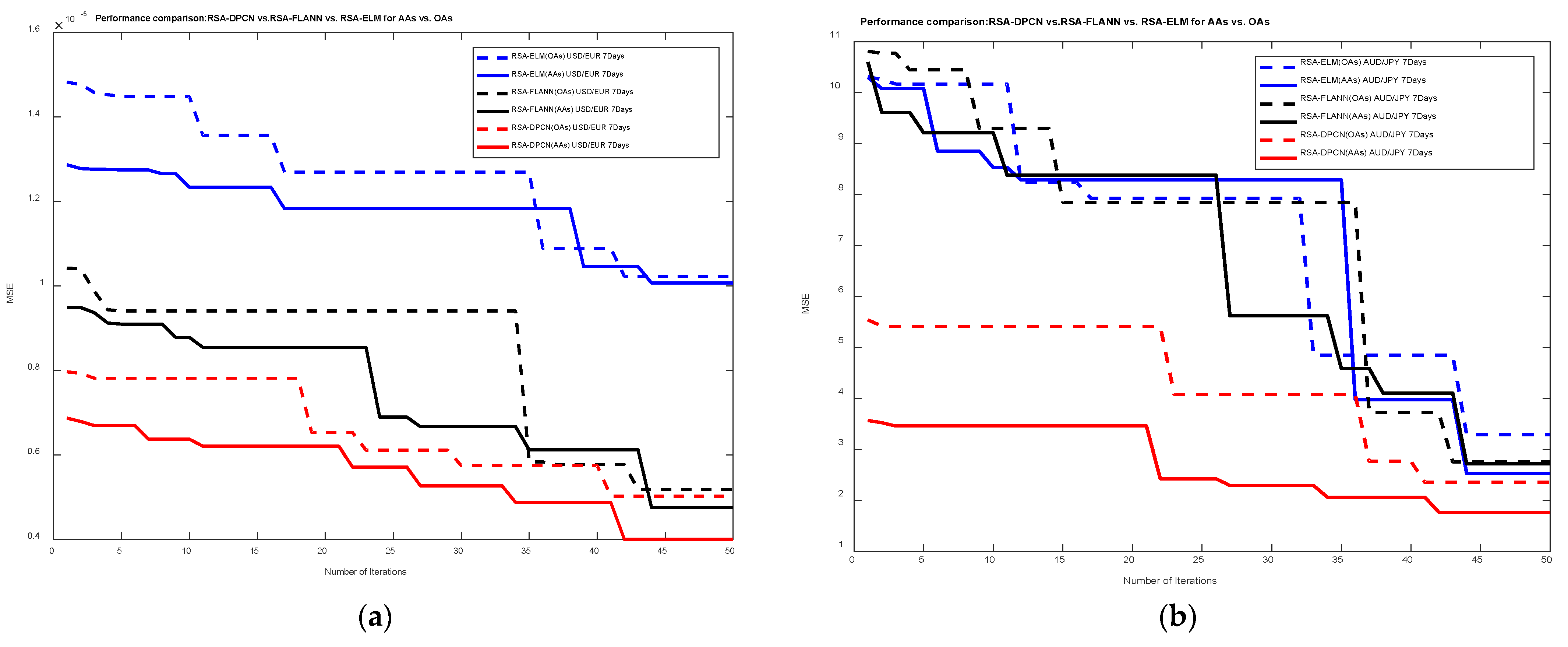

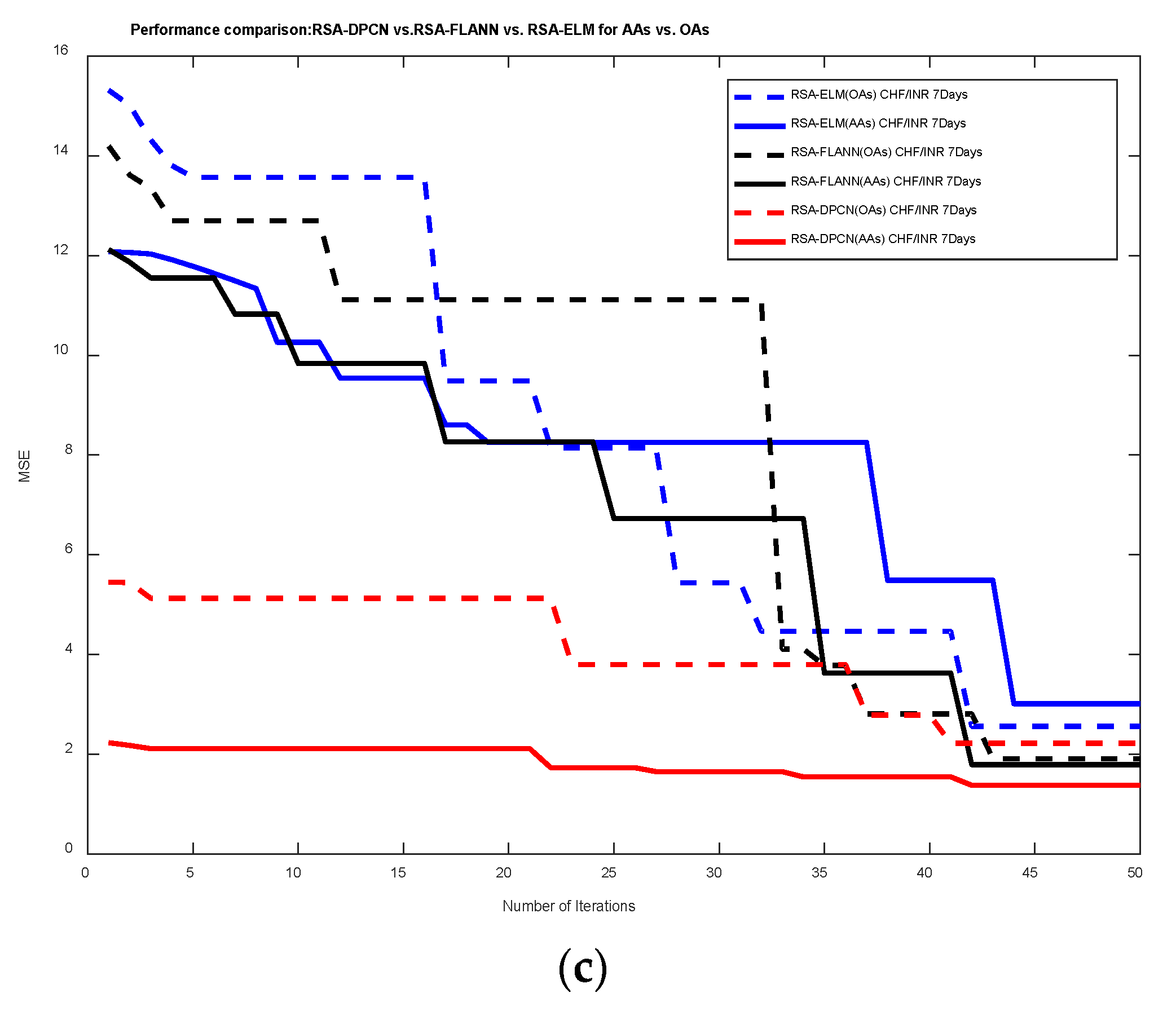

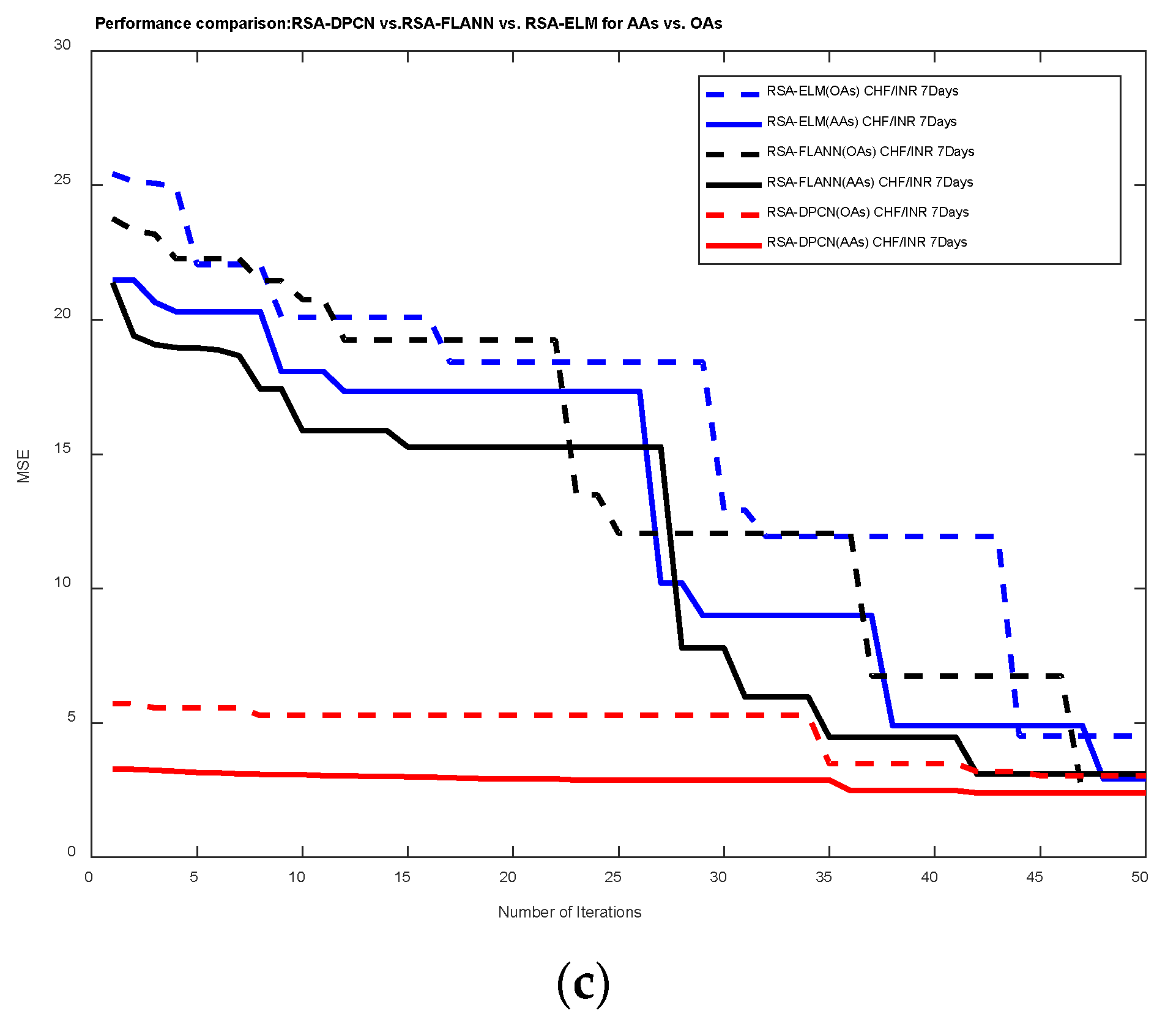

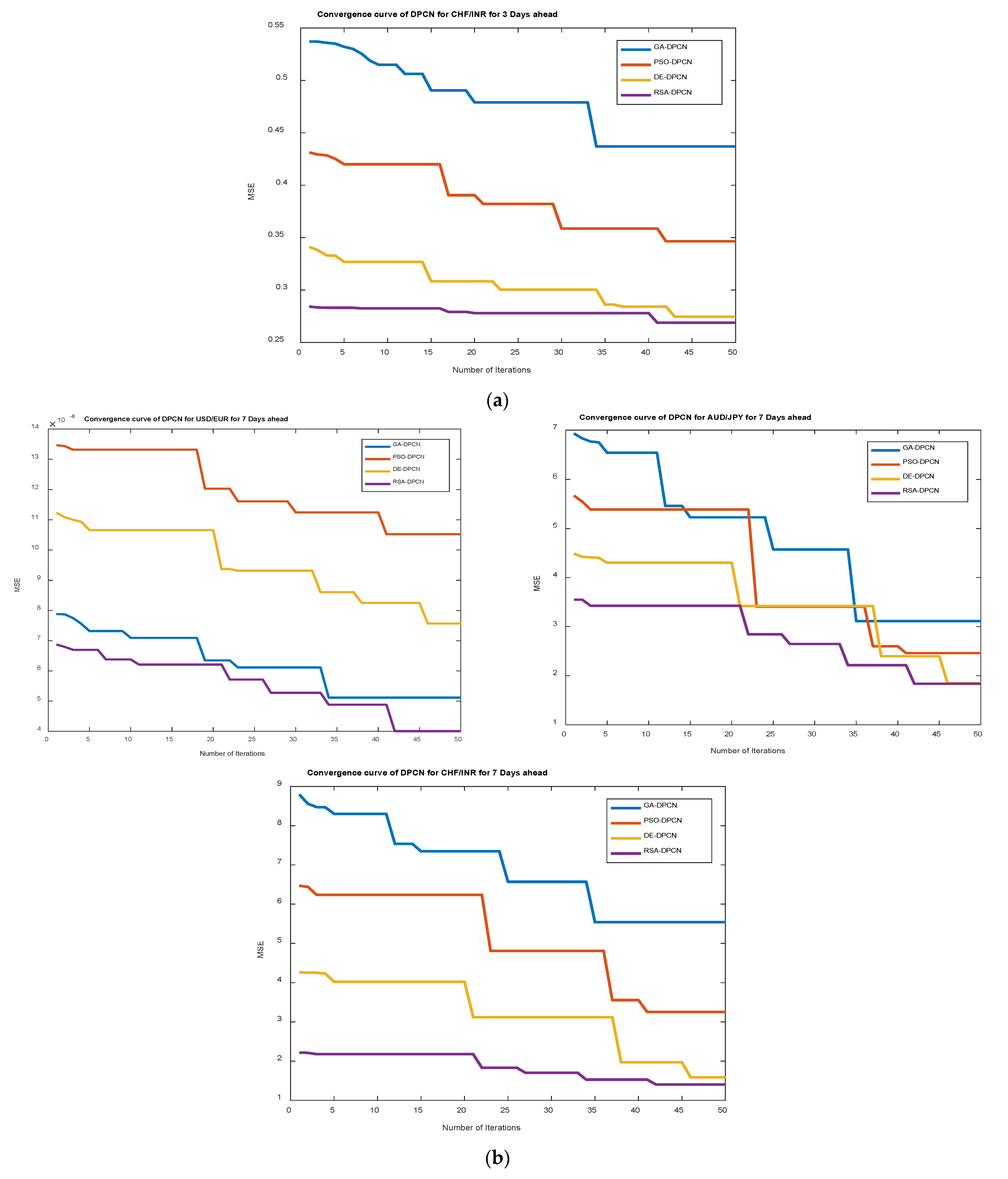

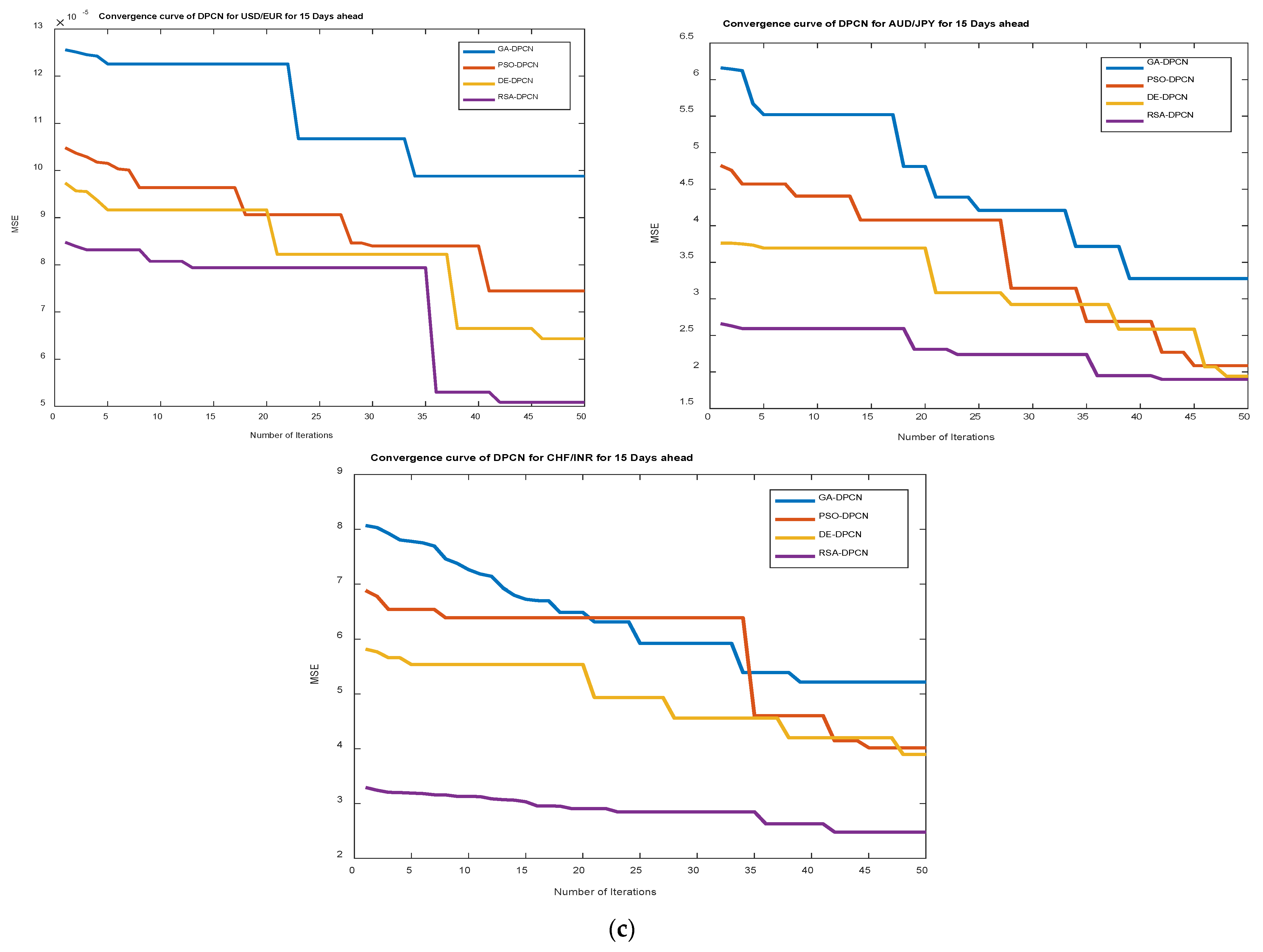

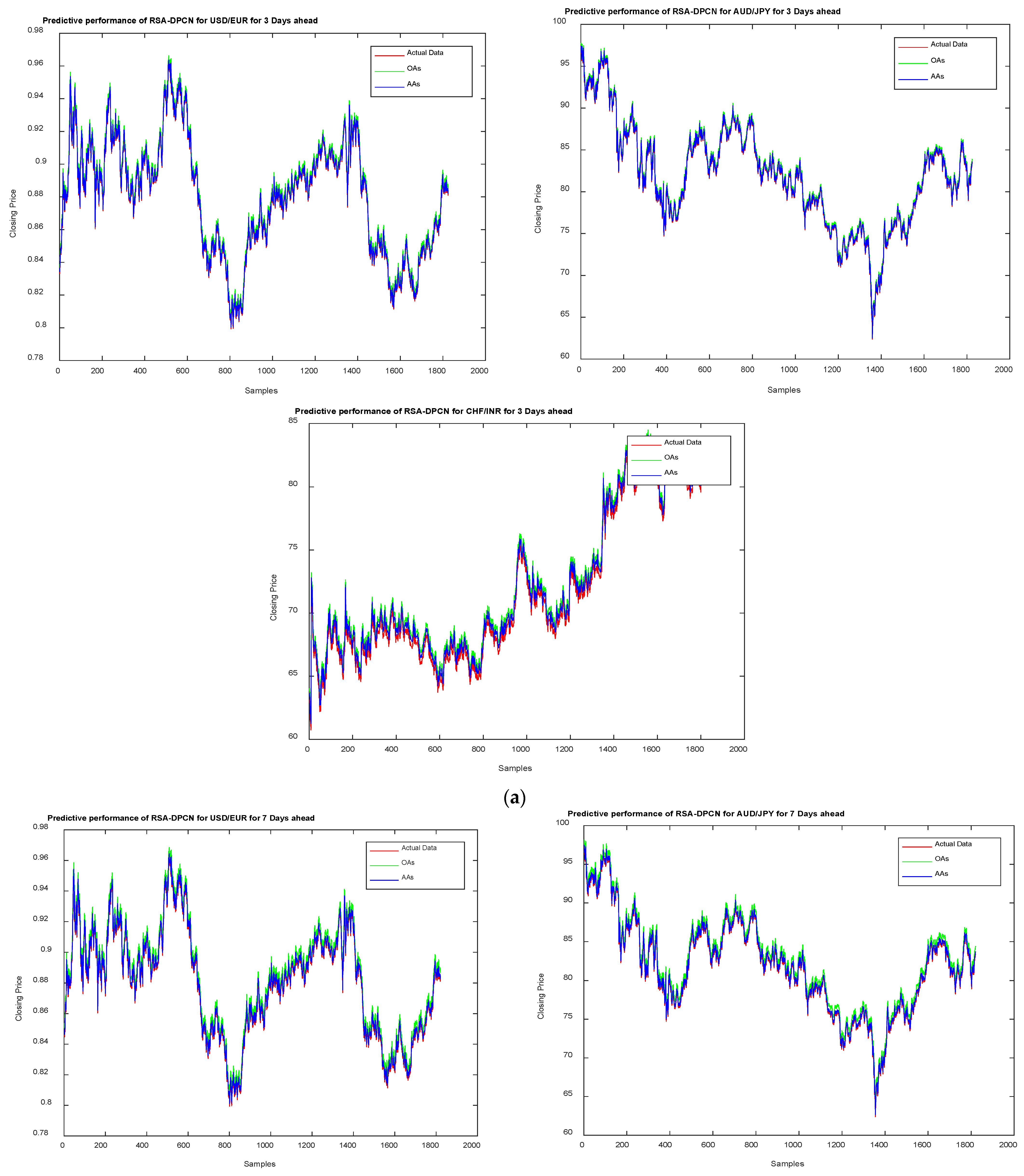

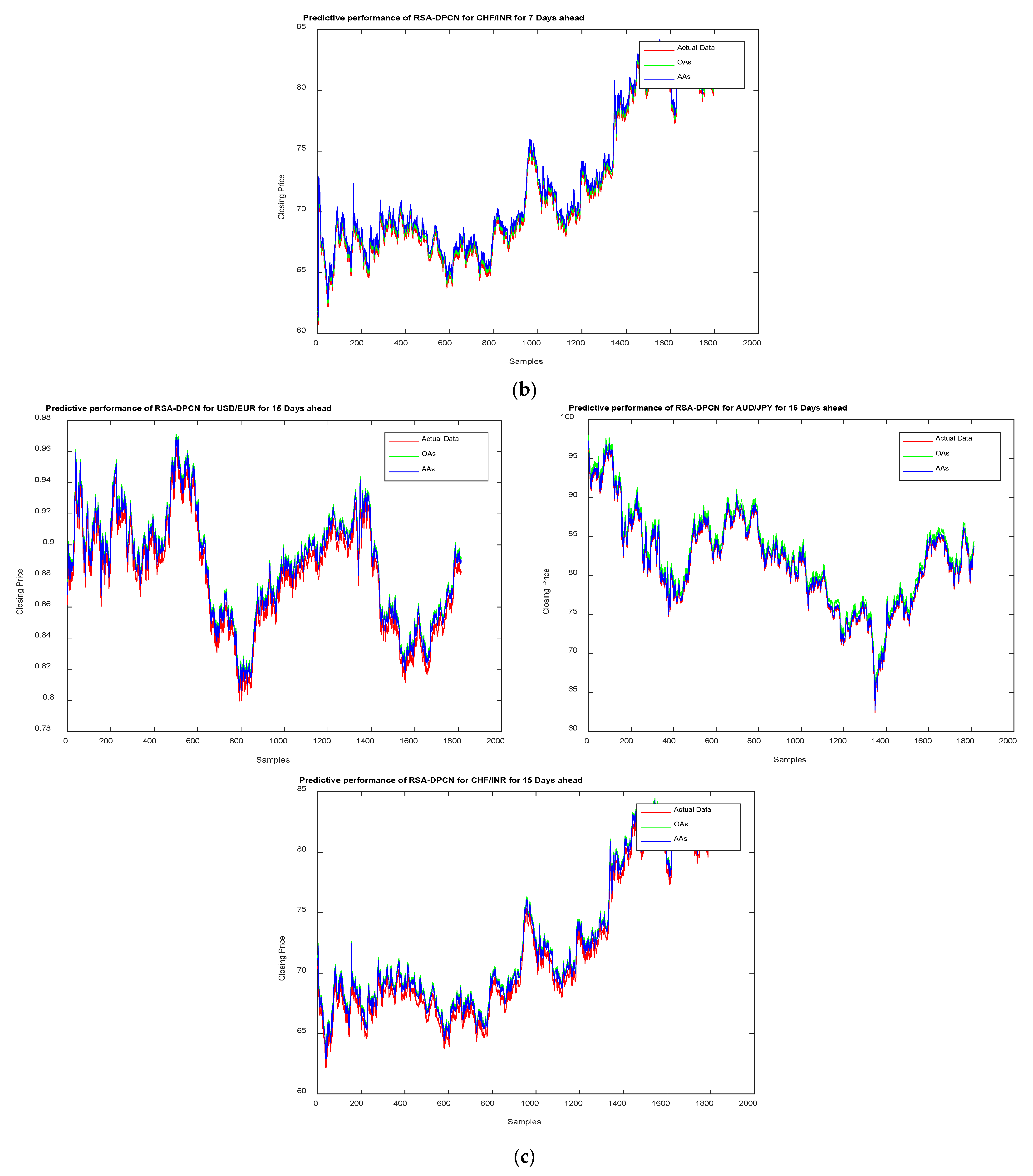

4.1. Phase #1: RSA-DPCN for FOREX Short-Term Trading

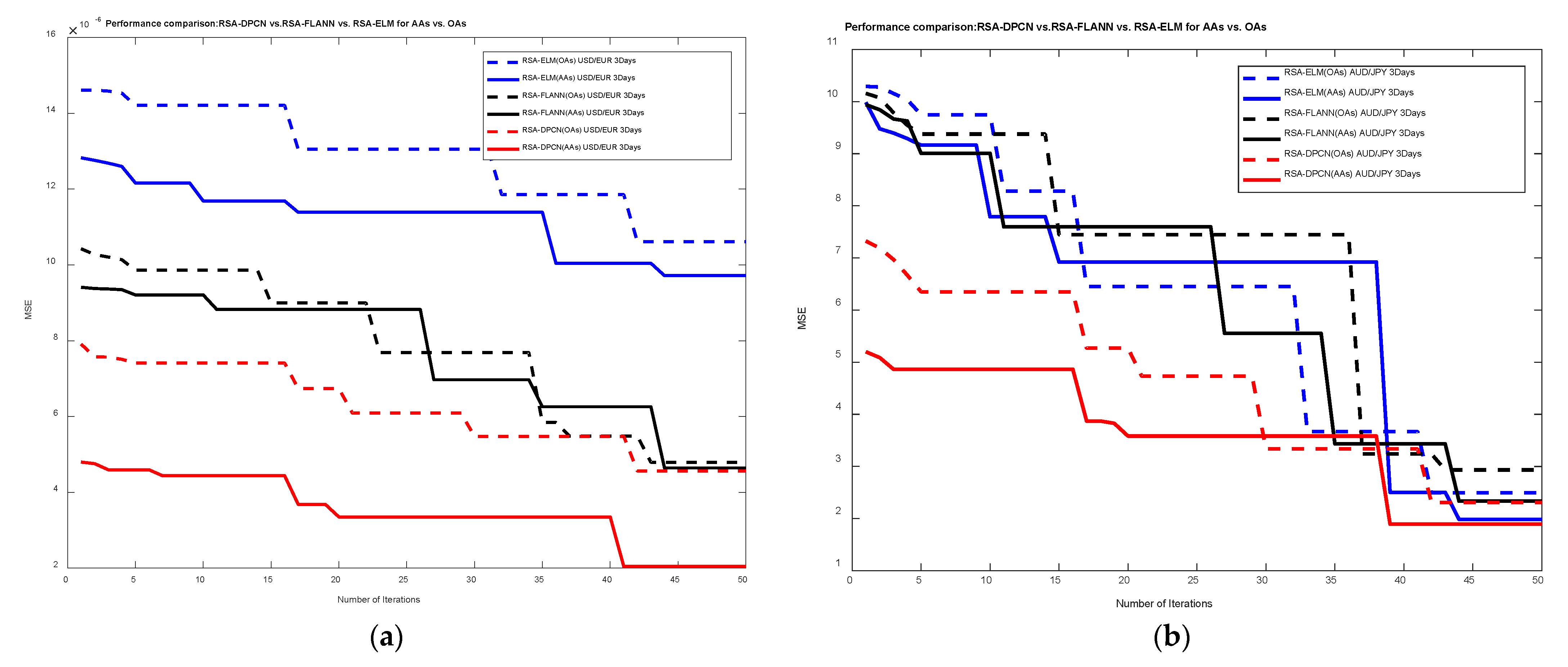

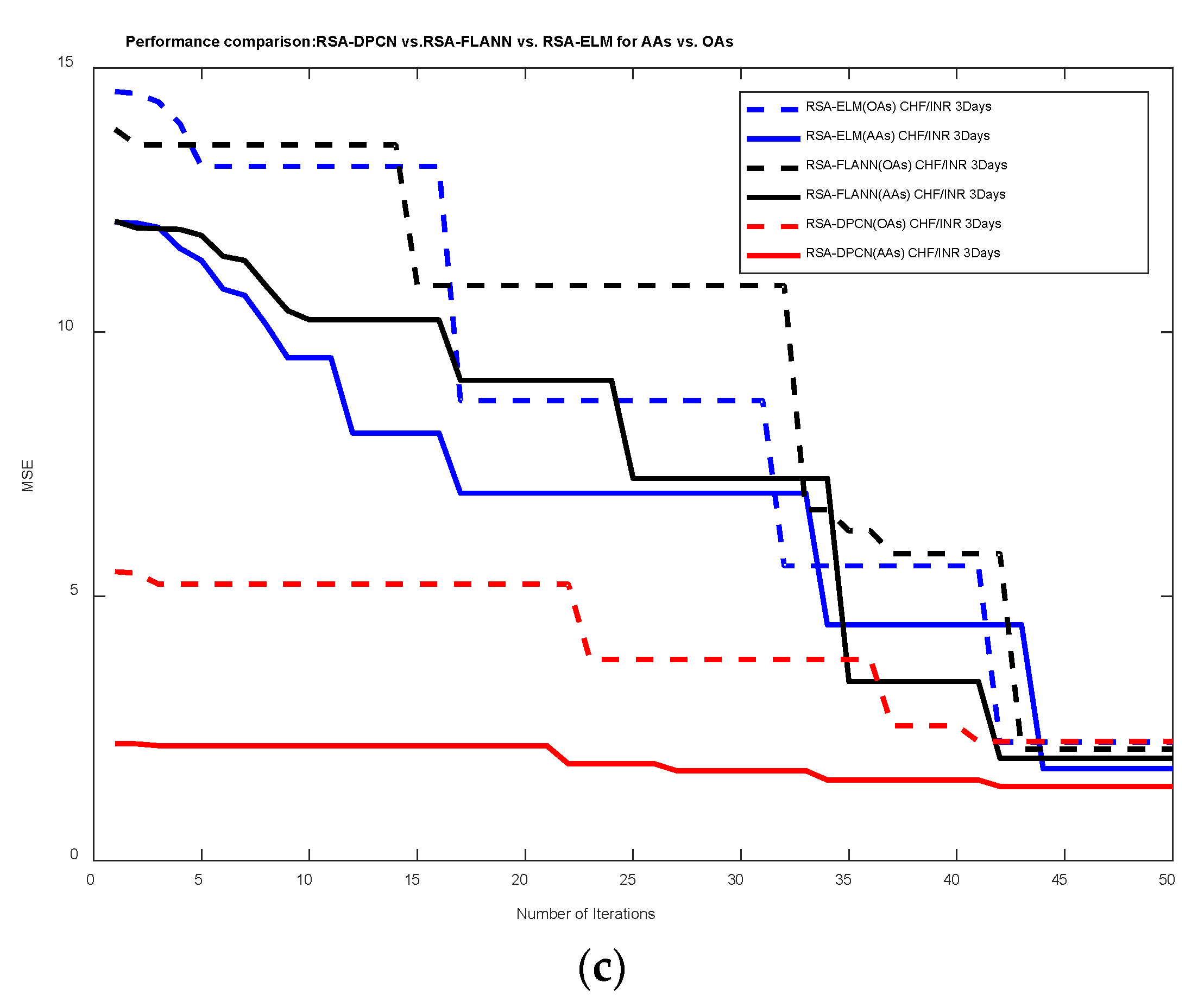

4.2. Performance Comparison and Validation of RSA-DPCN Forex Trading Model

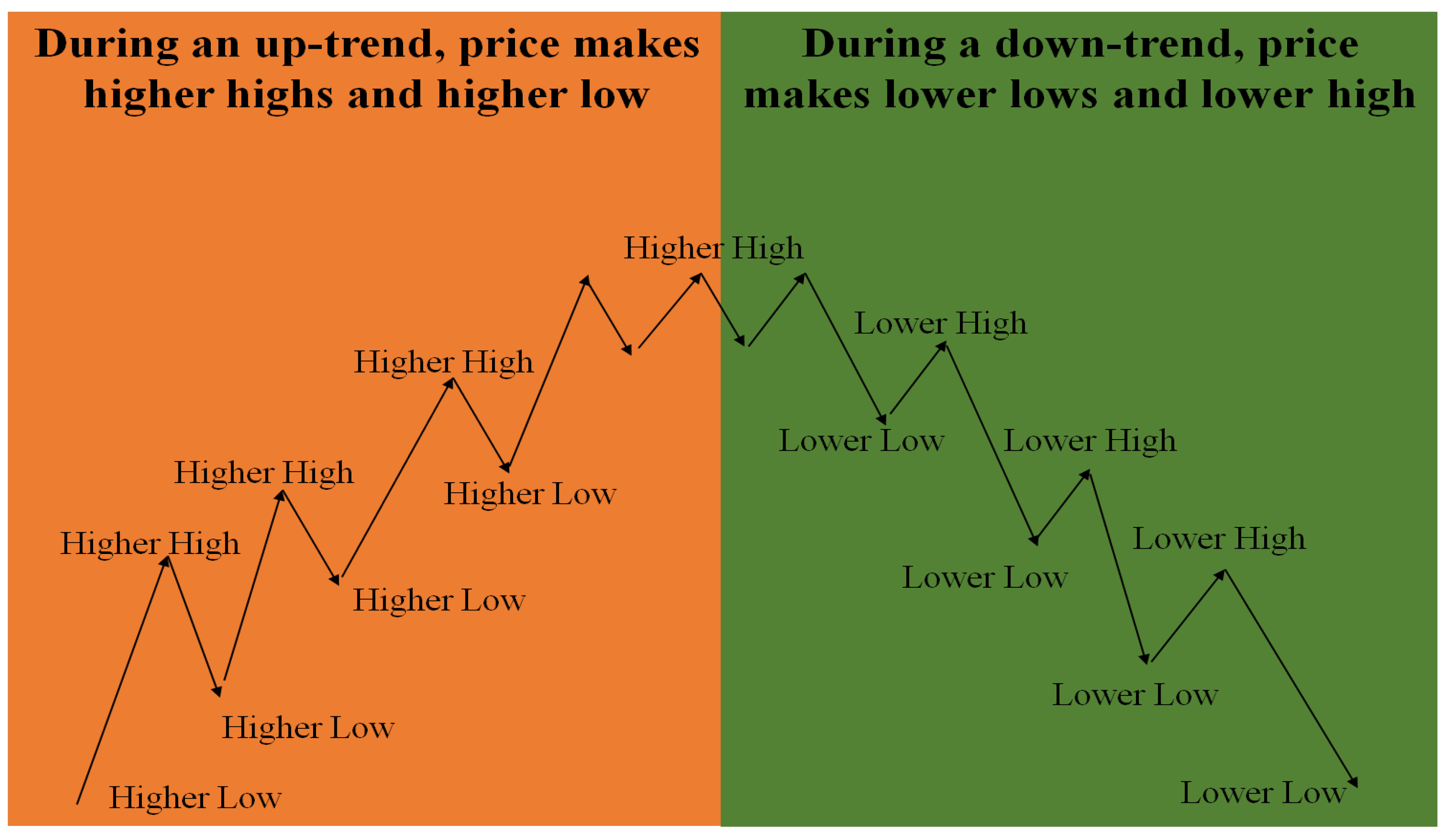

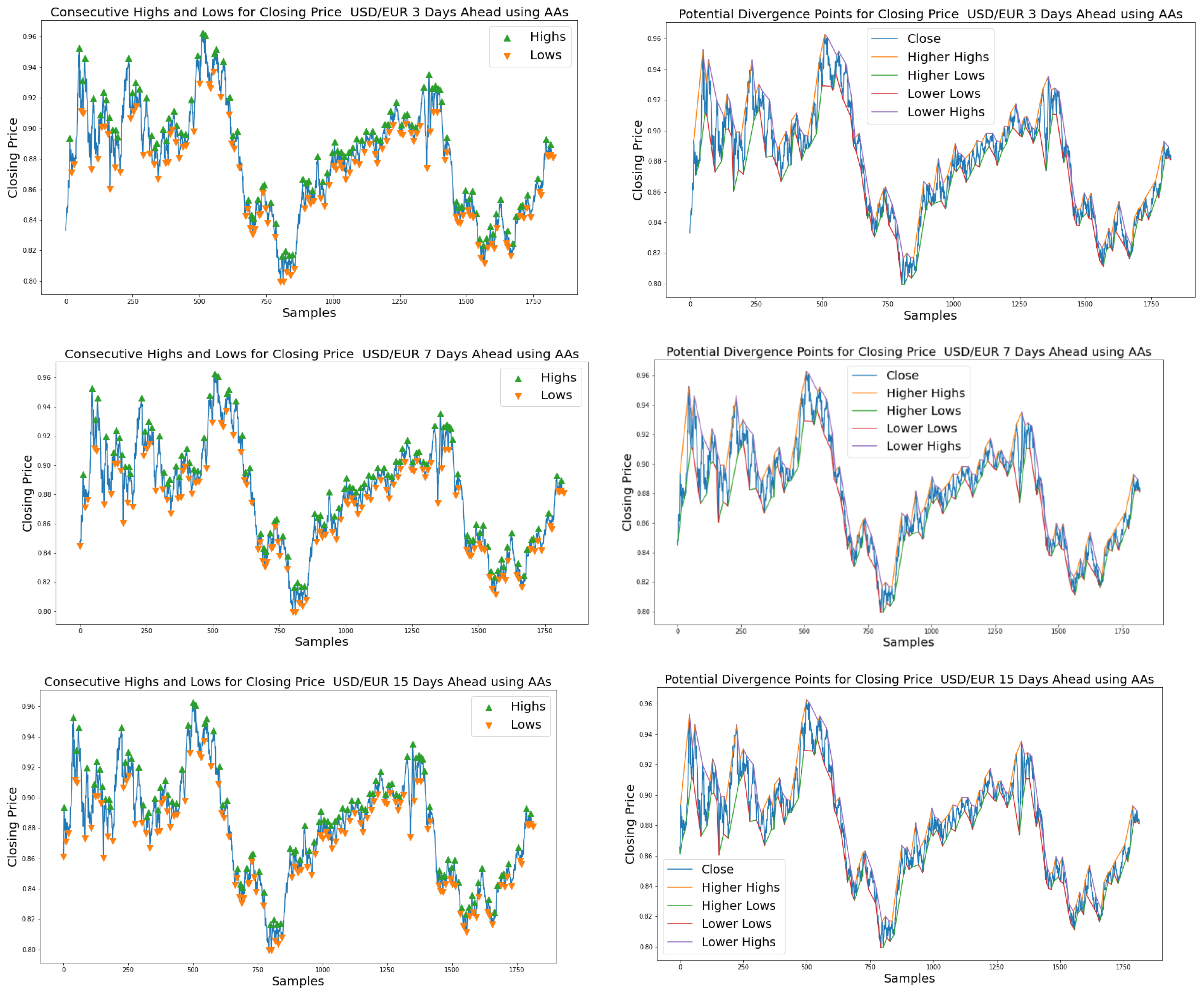

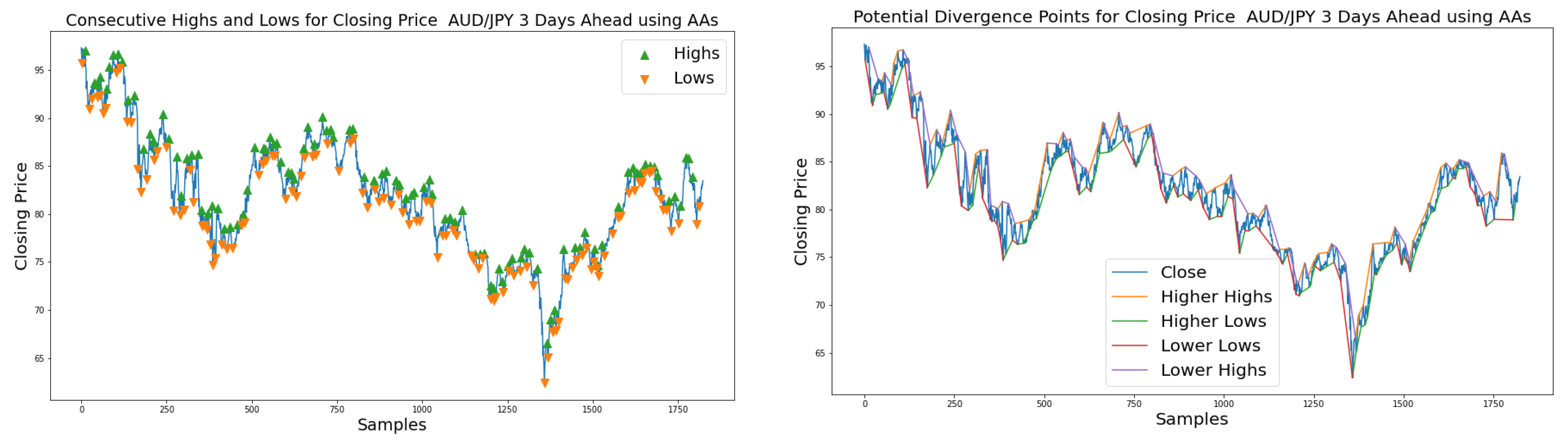

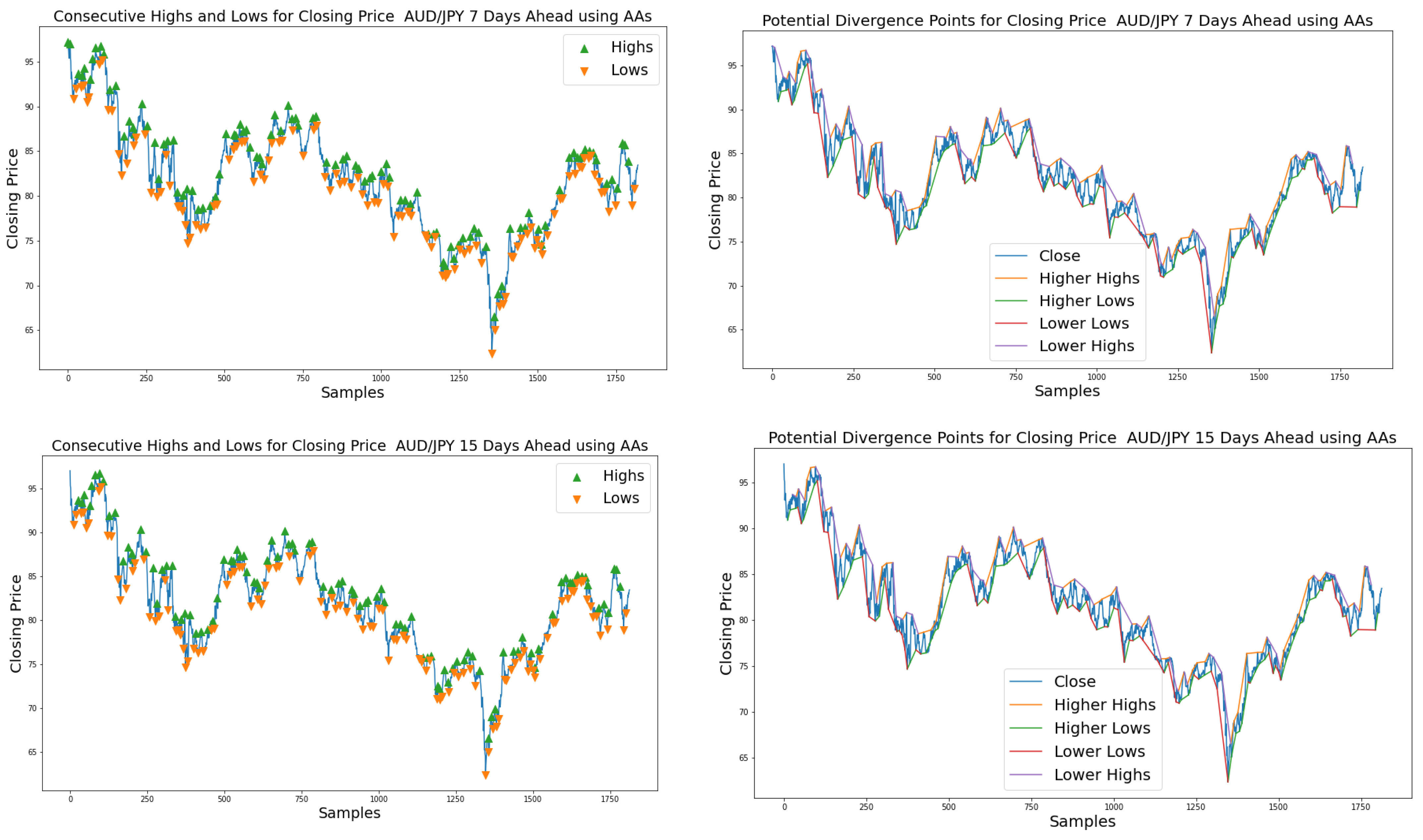

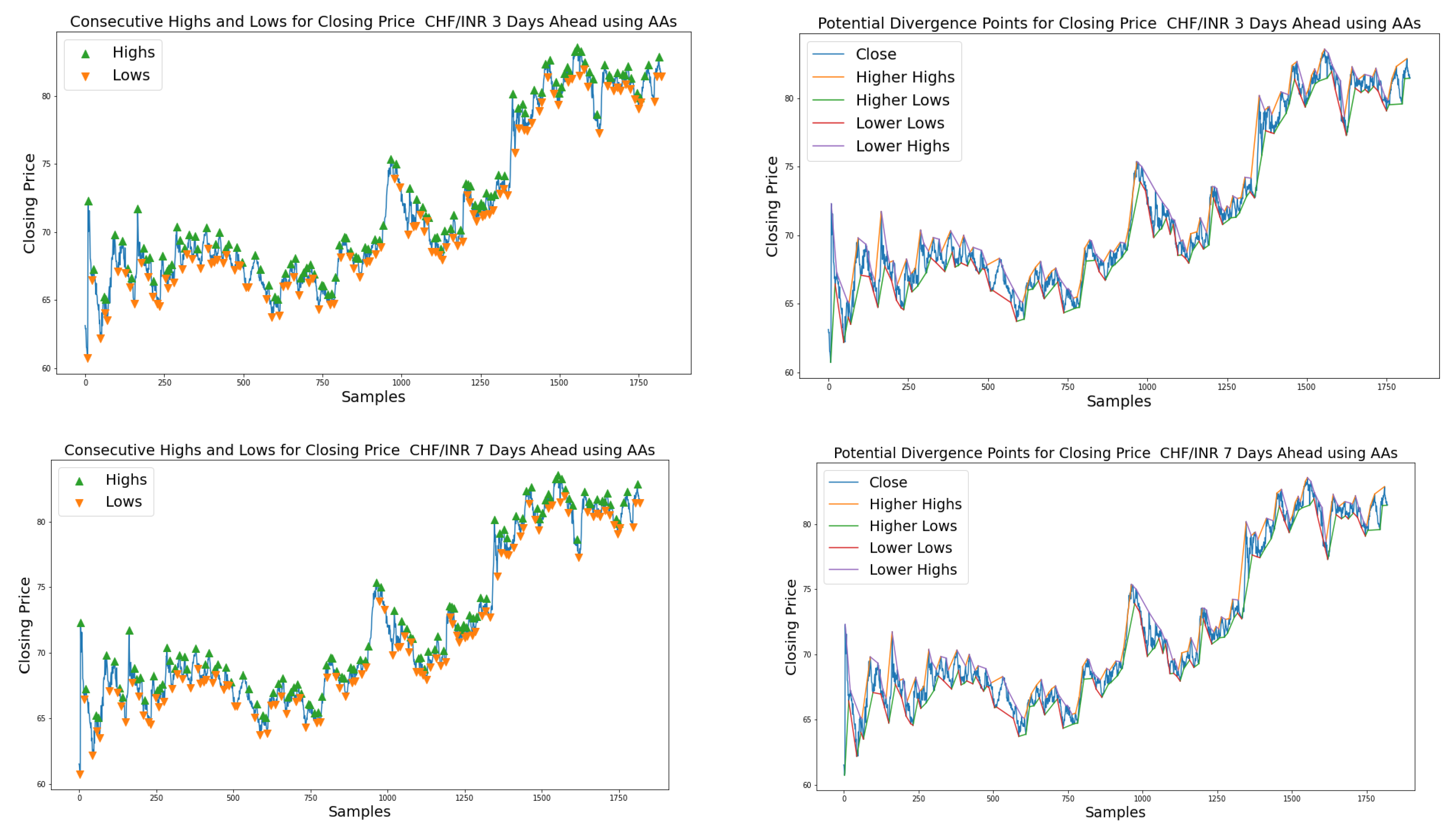

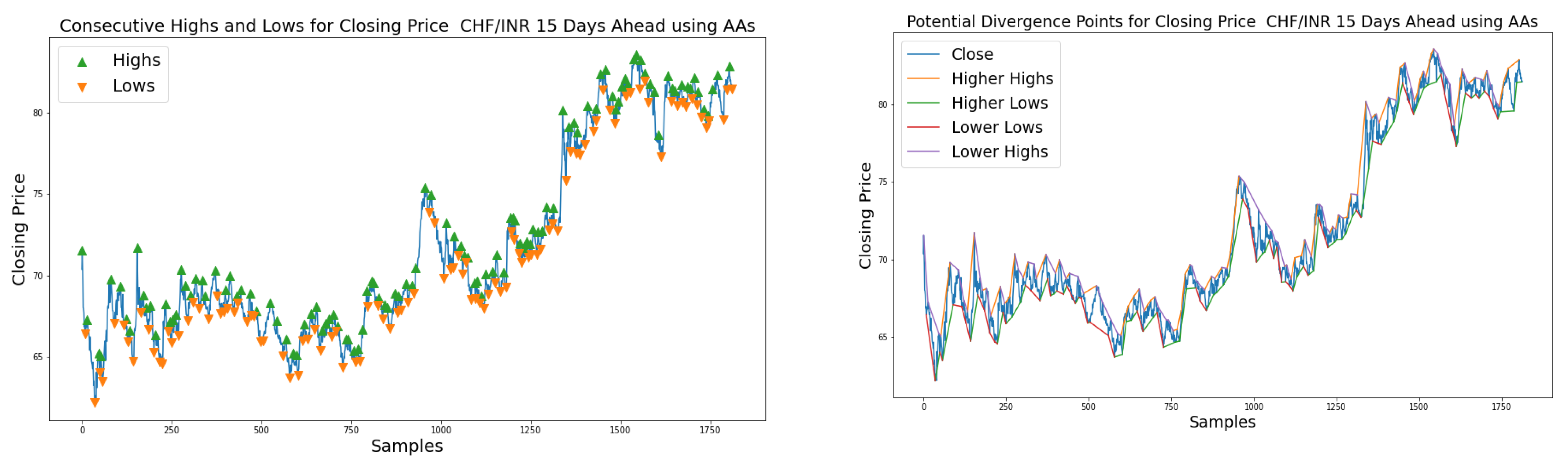

4.3. Phase #2: RSA-DPCN for FOREX Trend Analysis Using HHs/HLs and LHs/LLs

5. Conclusions and Future Scope

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Das, S.R.; Mishra, D.; Rout, M. A hybridized ELM-Jaya forecasting model for currency exchange prediction. J. King Saud Univ.—Comput. Inf. Sci. 2020, 32, 345–366. [Google Scholar] [CrossRef]

- Das, S.R.; Mishra, D.; Rout, M. An optimized feature reduction based currency forecasting model exploring the online sequential extreme learning machine and krill herd strategies. Phys. A Stat. Mech. Appl. 2019, 513, 339–370. [Google Scholar] [CrossRef]

- Sarangi, P.K.; Chawla, M.; Ghosh, P.; Singh, S.; Singh, P.K. FOREX trend analysis using machine learning techniques: INR vs USD currency exchange rate using ANN-GA hybrid approach. Mater. Today Proc. 2022, 49, 3170–3176. [Google Scholar] [CrossRef]

- Farimani, S.A.; Jahan, M.V.; Fard, A.M.; Tabbakh, S.R. Investigating the informativeness of technical indicators and news sentiment in financial market price prediction. Knowl.-Based Syst. 2022, 247, 108742. [Google Scholar] [CrossRef]

- Das, S.R.; Mishra, D.; Rout, M. A hybridized ELM using self-adaptive multi-population-based Jaya algorithm for currency exchange prediction: An empirical assessment. Neural Comput. Appl. 2019, 31, 7071–7094. [Google Scholar] [CrossRef]

- Nayak, R.K.; Mishra, D.; Rath, A.K. An optimized SVM-k-NN currency exchange forecasting model for Indian currency market. Neural Comput. Appl. 2019, 31, 995–3021. [Google Scholar] [CrossRef]

- Galeshchuk, S. Neural networks performance in exchange rate prediction. Neurocomputing 2016, 172, 446–452. [Google Scholar] [CrossRef]

- Ni, H.; Yin, H. Exchange rate prediction using hybrid neural networks and trading indicators. Neurocomputing 2009, 72, 2815–2823. [Google Scholar] [CrossRef]

- PradeepKumar, D.; Ravi, V. Soft computing hybrids for FOREX rate prediction: A comprehensive review. Comput. Oper. Res. 2018, 99, 262–284. [Google Scholar] [CrossRef]

- Carapuço, J.; Neves, R.; Horta, N. Reinforcement learning applied to Forex trading. Appl. Soft Comput. 2018, 73, 783–794. [Google Scholar] [CrossRef]

- Panda, M.M.; Panda, S.N.; Pattnaik, P.K. Multi currency exchange rate prediction using convolutional neural network. Mater. Today Proc. 2021. ISSN 2214-7853. [Google Scholar] [CrossRef]

- Sezer, O.B.; Gudelek, M.U.; Ozbayoglu, A.M. Financial time series forecasting with deep learning: A systematic literature review: 2005–2019. Appl. Soft Comput. 2020, 90, 106181. [Google Scholar] [CrossRef]

- Islam, M.S.; Hossain, E. Foreign exchange currency rate prediction using a GRU-LSTM hybrid network. Soft Comput. Lett. 2021, 3, 100009. [Google Scholar] [CrossRef]

- Juszczuk, P.; Kruś, L. Soft multicriteria computing supporting decisions on the Forex market. Appl. Soft Comput. 2020, 96, 106654. [Google Scholar] [CrossRef]

- Ahmed, S.; Hassan, S.U.; Aljohani, N.R.; Nawaz, R. FLF-LSTM: A novel prediction system using Forex Loss Function. Appl. Soft Comput. 2020, 97, 106780. [Google Scholar] [CrossRef]

- Pang, Z.; O’May, C.B.; Choksi, B.; VanRullen, R. Predictive coding feedback results in perceived illusory contours in a recurrent neural network. Neural Netw. 2021, 144, 164–175. [Google Scholar] [CrossRef] [PubMed]

- Mohan, A.; Luckey, A.; Weisz, N.; Vanneste, S. Predisposition to domain-wide maladaptive changes in predictive coding in auditory phantom perception. NeuroImage 2022, 248, 118813. [Google Scholar] [CrossRef]

- Wen, H.; Han, K.; Shi, J.; Zhang, Y.; Culurciello, E.; Liu, Z. Deep Predictive Coding Network for Object Recognition. In Proceedings of the 35th International Conference on Machine Learning (ICML 2018), Stockholmsmässan, Stockholm, Sweden, 10–15 July 2018; Volume 80, pp. 5266–5275. [Google Scholar]

- Dora, S.; Pennartz, C.; Bohte, S. A Deep Predictive Coding Network for Inferring Hierarchical Causes Underlying Sensory Inputs. In Artificial Neural Networks and Machine Learning—ICANN 2018; Kůrková, V., Manolopoulos, Y., Hammer, B., Iliadis, L., Maglogiannis, I., Eds.; Lecture Notes in Computer Science; Springer: Cham, Switzerland, 2018; Volume 11141. [Google Scholar]

- Sledge, I.J.; Principe, J.C. Faster Convergence in Deep-Predictive-Coding Networks to Learn Deeper Representations. IEEE Trans. Neural Netw. Learn. Systems 2021, 1–15. [Google Scholar] [CrossRef]

- Lotter, W.; Kreiman, G.; Cox, D. Deep Predictive Coding Networks for Video Prediction and Unsupervised Learning. arXiv 2016, arXiv:1605.08104. [Google Scholar]

- Wang, L.; Zeng, Y.; Chen, T. Back propagation neural network with adaptive differential evolution algorithm for time series forecasting. Expert Syst. Appl. 2015, 42, 855–863. [Google Scholar] [CrossRef]

- Rout, M.; Majhi, B.; Majhi, R.; Panda, G. Forecasting of currency exchange rates using an adaptive ARMA model with differential evolution based training. J. King Saud Univ.—Comput. Inf. Sci. 2014, 26, 7–18. [Google Scholar] [CrossRef]

- Chouikhi, N.; Ammar, B.; Rokbani, N.; Alimi, A.M. PSO-based analysis of Echo State Network parameters for time series forecasting. Appl. Soft Comput. 2017, 55, 211–225. [Google Scholar] [CrossRef]

- de Almeida, B.J.; Neves, R.F.; Horta, N. Combining Support Vector Machine with Genetic Algorithms to optimize investments in Forex markets with high leverage. Appl. Soft Comput. 2018, 64, 596–613. [Google Scholar] [CrossRef]

- Evans, C.; Pappas, K.; Xhafa, F. Utilizing artificial neural networks and genetic algorithms to build an algo-trading model for intra-day foreign exchange speculation. Math. Comput. Model. 2013, 58, 1249–1266. [Google Scholar] [CrossRef]

- Abualigah, L.; Abd Elaziz, M.; Sumari, P.; Geem, Z.W.; Gandomi, A.H. Reptile Search Algorithm (RSA): A nature-inspired meta-heuristic optimizer. Expert Syst. Appl. 2022, 191, 116158. [Google Scholar] [CrossRef]

- Güntürkün, O.; Stacho, M.; Ströckens, F. Chapter 8—The Brains of Reptiles and Birds. In Evolutionary Neuroscience, 2nd ed.; Jon, H.K., Ed.; Academic Press: Cambridge, MA, USA, 2020; pp. 159–212. [Google Scholar]

- Gibbons, P.M.; Tell, L.A. Problem Solving in Reptile Practice. J. Exot. Pet Med. 2009, 18, 202–212. [Google Scholar] [CrossRef]

- Das, S.R.; Mishra, D.; Rout, M. Stock market prediction using Firefly algorithm with evolutionary framework optimized feature reduction for OSELM method. Expert Syst. Appl. X 2019, 4, 100016. [Google Scholar] [CrossRef]

- Das, A.K.; Mishra, D.; Das, K.; Mallick, P.K.; Kumar, S.; Zymbler, M.; El-Sayed, H. Prophesying the Short-Term Dynamics of the Crude Oil Future Price by Adopting the Survival of the Fittest Principle of Improved Grey Optimization and Extreme Learning Machine. Mathematics 2022, 10, 1121. [Google Scholar] [CrossRef]

- Liu, M.; Luo, K.; Zhang, J.; Chen, S. A stock selection algorithm hybridizing grey wolf optimizer and support vector regression. Expert Syst. Appl. 2021, 179, 115078. [Google Scholar] [CrossRef]

- Yao, J.; Tan, C.L. A case study on using neural networks to perform technical forecasting of forex. Neurocomputing 2000, 34, 79–98. [Google Scholar] [CrossRef]

- Talebi, H.; Hoang, W.; Gavrilova, M.L. Multi-scale Foreign Exchange Rates Ensemble for Classification of Trends in Forex Market. Procedia Comput. Sci. 2014, 29, 2065–2075. [Google Scholar] [CrossRef]

- Fiorucci, J.A.; Silva, G.N.; Barboza, F. Reaction trend system with GARCH quantiles as action points. Expert Syst. Appl. 2022, 198, 116750. [Google Scholar] [CrossRef]

- Bartoš, E.; Pinčák, R. Identification of market trends with string and D2-brane maps. Phys. A Stat. Mech. Appl. 2017, 479, 57–70. [Google Scholar] [CrossRef]

- Sadeghi, A.; Daneshvar, A.; Zaj, M.M. Combined ensemble multi-class SVM and fuzzy NSGA-II for trend forecasting and trading in Forex markets. Expert Syst. Appl. 2021, 185, 115566. [Google Scholar] [CrossRef]

- Available online: https://in.investing.com/currencies/ (accessed on 1 January 2022).

- Panopoulou, E.; Souropanis, I. The role of technical indicators in exchange rate forecasting. J. Empir. Financ. 2019, 53, 197–221. [Google Scholar] [CrossRef]

- Dai, Z.; Zhu, H.; Kang, J. New technical indicators and stock returns predictability. Int. Rev. Econ. Financ. 2021, 71, 127–142. [Google Scholar] [CrossRef]

- Lee, S.W.; Kim, H.Y. Stock market forecasting with super-high dimensional time-series data using ConvLSTM, trend sampling, and specialized data augmentation. Expert Syst. Appl. 2020, 161, 113704. [Google Scholar] [CrossRef]

- Available online: https://forexbee.co/trend-analysis/ (accessed on 11 January 2022).

- Available online: https://www.incrediblecharts.com/technical/dow_theory_trends.php (accessed on 11 January 2022).

- Korczak, J.; Hernes, M. Performance Evaluation of Trading Strategies in Multi-Agent Systems—Case of A-Trader. In Proceedings of the 2018 Federated Conference on Computer Science and Information Systems (FedCSIS), Poznan, Poland, 9–12 September 2018; pp. 839–844. [Google Scholar]

- Otsu, T.; Taniguchi, G. Kolmogorov–Smirnov type test for generated variables. Econ. Lett. 2020, 195, 109401. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Datasets | Total Samples | Date Range | Data Range |

|---|---|---|---|

| USD/EUR | 1828 | 1 January 2015~1 January 2021 | 0.7969~0.9671 |

| AUD/JPY | 1828 | 59~98 | |

| CHF/INR | 1828 | 60~83 |

| Networks and Optimization Techniques | Parameters and Associated Values |

|---|---|

| FLANN | algorithm = ’autotuned’; target_precision = 0.7; build_weight = 0.01; memory_weight = 0; |

| ELM | Activation Function: Multiquadtratic |

| DPCN | Feebforward-Conv2D-Kernel Size-3; Feebback-Conv2D-Kernel Size-3 For prediction: Up sampling has been performed using PyTorch with various scaling factors. |

| GA | Number of Decision Variables = 3; Maximum Number of Iterations = 50 Population size = 10; Selection method-Roulette wheel |

| PSO | Number of Decision Variables = 3; Maximum Number of Iterations = 50 Number of Particles = 10; Inertia Weight = 1; Inertia Weight Damping Ratio = 0.99; Personal Learning Coefficient = 1.5; Global Learning Coefficient = 2.0 |

| DE | Number of Decision Variables = 3; Maximum Number of Iterations = 50 Crossover rate = 0.7; Mutation factor = 0.5; Number of Decision Variables = 3 |

| RSA | Maximum Number of Iterations = 50; Alpha = 0.1; Beta = 0.005 |

| Models | Currency Pairs | RMSE | MAPE | MAE | MSE | MARE | R2 | Theil’s U |

|---|---|---|---|---|---|---|---|---|

| GA-DPCN | USD/EUR | 0.0065 | 0.740271 | 0.0065 | 4.22 × 10−5 | 0.007403 | 0.964974 | 0.3958 |

| PSO-DPCN | 0.00308 | 0.350775 | 0.00308 | 9.49 × 10−6 | 0.003508 | 0.992136 | 0.1932 | |

| DE-DPCN | 0.002 | 0.227776 | 0.002 | 4 × 10−6 | 0.002278 | 0.996684 | 0.1923 | |

| RSA-DPCN | 0.001 | 0.113888 | 0.001 | 1 × 10−6 | 0.001139 | 0.999171 | 0.1919 | |

| GA-DPCN | AUD/JPY | 1.1885 | 1.462043 | 1.1885 | 1.412532 | 0.01462 | 0.961778 | 0.3215 |

| PSO-DPCN | 1.1788 | 1.45011 | 1.1788 | 1.389569 | 0.014501 | 0.962399 | 0.3158 | |

| DE-DPCN | 1.167 | 1.435594 | 1.167 | 1.361889 | 0.014356 | 0.963148 | 0.3115 | |

| RSA-DPCN | 1.148 | 1.412221 | 1.148 | 1.317904 | 0.014122 | 0.964338 | 0.2848 | |

| GA-DPCN | CHF/INR | 0.5885 | 0.826408 | 0.5885 | 0.346332 | 0.008264 | 0.989719 | 0.4181 |

| PSO-DPCN | 0.5788 | 0.812787 | 0.5788 | 0.335009 | 0.008128 | 0.990055 | 0.4142 | |

| DE-DPCN | 0.5167 | 0.725582 | 0.5167 | 0.266979 | 0.007256 | 0.992075 | 0.4156 | |

| RSA-DPCN | 0.5148 | 0.722914 | 0.5148 | 0.265019 | 0.007229 | 0.992133 | 0.3147 |

| Models | Currency Pairs | RMSE | MAPE | MAE | MSE | MARE | R2 | Theil’s U |

|---|---|---|---|---|---|---|---|---|

| GA-DPCN | USD/EUR | 0.00625 | 0.711727 | 0.00625 | 3.91 × 10−5 | 0.007117 | 0.967591 | 0.3868 |

| PSO-DPCN | 0.003087 | 0.351536 | 0.003087 | 9.53 × 10−6 | 0.003515 | 0.992094 | 0.2911 | |

| DE-DPCN | 0.0027 | 0.307466 | 0.0027 | 7.29 × 10−6 | 0.003075 | 0.993952 | 0.2593 | |

| RSA-DPCN | 0.0017 | 0.19359 | 0.0017 | 2.89 × 10−6 | 0.001936 | 0.997602 | 0.2124 | |

| GA-DPCN | AUD/JPY | 1.41985 | 1.747244 | 1.41985 | 2.015974 | 0.017472 | 0.944855 | 0.3242 |

| PSO-DPCN | 1.31888 | 1.622992 | 1.31888 | 1.739444 | 0.01623 | 0.952419 | 0.3168 | |

| DE-DPCN | 1.2697 | 1.562472 | 1.2697 | 1.612138 | 0.015625 | 0.955901 | 0.3154 | |

| RSA-DPCN | 1.258 | 1.548074 | 1.258 | 1.582564 | 0.015481 | 0.95671 | 0.2954 | |

| GA-DPCN | CHF/INR | 1.95885 | 2.749931 | 1.95885 | 3.837093 | 0.027499 | 0.885766 | 0.4487 |

| PSO-DPCN | 1.5788 | 2.216398 | 1.5788 | 2.492609 | 0.022164 | 0.925792 | 0.4444 | |

| DE-DPCN | 1.1667 | 1.637872 | 1.1667 | 1.361189 | 0.016379 | 0.959476 | 0.4251 | |

| RSA-DPCN | 1.1148 | 1.565012 | 1.1148 | 1.242779 | 0.01565 | 0.963001 | 0.3242 |

| Models | Currency Pairs | RMSE | MAPE | MAE | MSE | MARE | R2 | Theil’s U |

|---|---|---|---|---|---|---|---|---|

| GA-DPCN | USD/EUR | 0.00925 | 1.053217 | 0.00925 | 8.56 × 10−5 | 0.010532 | 0.929121 | 0.3879 |

| PSO-DPCN | 0.008087 | 0.920796 | 0.008087 | 6.54 × 10−5 | 0.009208 | 0.945823 | 0.2995 | |

| DE-DPCN | 0.0077 | 0.876732 | 0.0077 | 5.93 × 10−5 | 0.008767 | 0.950884 | 0.2784 | |

| RSA-DPCN | 0.0067 | 0.76287 | 0.0067 | 4.49 × 10−5 | 0.007629 | 0.962813 | 0.2615 | |

| GA-DPCN | AUD/JPY | 1.4985 | 1.845308 | 1.4985 | 2.245502 | 0.018453 | 0.937204 | 0.3249 |

| PSO-DPCN | 1.3888 | 1.71022 | 1.3888 | 1.928765 | 0.017102 | 0.946061 | 0.3287 | |

| DE-DPCN | 1.3697 | 1.686699 | 1.3697 | 1.876078 | 0.016867 | 0.947535 | 0.3241 | |

| RSA-DPCN | 1.298 | 1.598405 | 1.298 | 1.684804 | 0.015984 | 0.952884 | 0.2922 | |

| GA-DPCN | CHF/INR | 2.01885 | 2.832884 | 2.01885 | 4.075755 | 0.028329 | 0.878081 | 0.4491 |

| PSO-DPCN | 1.9788 | 2.776685 | 1.9788 | 3.915649 | 0.027767 | 0.88287 | 0.4318 | |

| DE-DPCN | 1.967 | 2.760127 | 1.967 | 3.869089 | 0.027601 | 0.884263 | 0.4122 | |

| RSA-DPCN | 1.5148 | 2.125593 | 1.5148 | 2.294619 | 0.021256 | 0.931361 | 0.3142 |

| Datasets | Model Pairs | Value | 03 Days | 07 Days | 15 Days |

|---|---|---|---|---|---|

| USD/EUR | RSA-DPCN vs. GA-DPCN | (p) | 1.8 × 10−6 | 7.85 × 10−5 | 0.027227 |

| (h) | 1 | 1 | 1 | ||

| RSA-DPCN vs. PSO-DPCN | (p) | 0.070596 | 0.228212 | 0.229598 | |

| (h) | 0 | 0 | 0 | ||

| RSA-DPCN vs. DE-DPCN | (p) | 0.384621 | 0.384953 | 0.386367 | |

| (h) | 0 | 0 | 0 | ||

| AUD/JPY | RSA-DPCN vs. GA-DPCN | (p) | 0.840559 | 0.419428 | 0.312933 |

| (h) | 0 | 0 | 0 | ||

| RSA-DPCN vs. PSO-DPCN | (p) | 0.878402 | 0.76134 | 0.647665 | |

| (h) | 0 | 0 | 0 | ||

| RSA-DPCN vs. DE-DPCN | (p) | 0.924807 | 0.953454 | 0.718191 | |

| (h) | 0 | 0 | 0 | ||

| CHF/INR | RSA-DPCN vs. GA-DPCN | (p) | 0.701395 | 1.15E-05 | (p)0.008726 |

| (h) | 0 | 1 | (h)1 | ||

| RSA-DPCN vs. PSO-DPCN | (p) | 0.739155 | 0.01578 | 0.015761 | |

| (h) | 0 | 1 | 1 | ||

| RSA-DPCN vs. DE-DPCN | (p) | 0.992113 | 0.78707 | 0.01862 | |

| (h) | 0 | 0 | 1 |

| Models | Currency Pairs | OAs | AAs | ||||

|---|---|---|---|---|---|---|---|

| 03 Days | 07 Days | 15 Days | 03 Days | 07 Days | 15 Days | ||

| GA-DPCN | USD/EUR | 960 | 943 | 915 | 1014 | 1001 | 986 |

| PSO-DPCN | 955 | 940 | 917 | 998 | 986 | 979 | |

| DE-DPCN | 964 | 942 | 921 | 1021 | 998 | 981 | |

| RSA-DPCN | 961 | 947 | 919 | 1002 | 999 | 985 | |

| GA-DPCN | AUD/JPY | 960 | 941 | 924 | 1012 | 999 | 986 |

| PSO-DPCN | 954 | 935 | 916 | 995 | 979 | 979 | |

| DE-DPCN | 952 | 942 | 923 | 1026 | 983 | 979 | |

| RSA-DPCN | 955 | 945 | 917 | 1008 | 999 | 982 | |

| GA-DPCN | HF/INR | 925 | 914 | 909 | 1017 | 1008 | 976 |

| PSO-DPCN | 931 | 924 | 917 | 989 | 981 | 972 | |

| DE-DPCN | 971 | 946 | 922 | 1015 | 993 | 969 | |

| RSA-DPCN | 958 | 947 | 920 | 1011 | 987 | 981 | |

| Predictive Days | Datasets OAs/AAs | USD/EUR | AUD/JPY | CHF/INR | |||

|---|---|---|---|---|---|---|---|

| No. of UP-Trends | No. of Down-Trends | No. of UP-Trends | No. of Down-Trends | No. of UP-Trends | No. of Down-Trends | ||

| 3 Days | OAs | 27 | 27 | 32 | 29 | 34 | 29 |

| AAs | 26 | 27 | 32 | 29 | 35 | 28 | |

| No. of mismatches observed | 1 | 0 | 0 | 0 | 1 | 1 | |

| 7 Days | OAs | 27 | 26 | 30 | 29 | 31 | 26 |

| AAs | 26 | 25 | 30 | 29 | 32 | 25 | |

| No. of mismatches observed | 1 | 1 | 0 | 0 | 1 | 1 | |

| 15 Days | OAs | 26 | 24 | 26 | 29 | 28 | 21 |

| AAs | 28 | 26 | 26 | 29 | 29 | 22 | |

| No. of mismatches observed | 1 | 2 | 0 | 0 | 1 | 1 | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Dash, S.; Sahu, P.K.; Mishra, D.; Mallick, P.K.; Sharma, B.; Zymbler, M.; Kumar, S. A Novel Algorithmic Forex Trade and Trend Analysis Framework Based on Deep Predictive Coding Network Optimized with Reptile Search Algorithm. Axioms 2022, 11, 396. https://doi.org/10.3390/axioms11080396

Dash S, Sahu PK, Mishra D, Mallick PK, Sharma B, Zymbler M, Kumar S. A Novel Algorithmic Forex Trade and Trend Analysis Framework Based on Deep Predictive Coding Network Optimized with Reptile Search Algorithm. Axioms. 2022; 11(8):396. https://doi.org/10.3390/axioms11080396

Chicago/Turabian StyleDash, Swaty, Pradip Kumar Sahu, Debahuti Mishra, Pradeep Kumar Mallick, Bharti Sharma, Mikhail Zymbler, and Sachin Kumar. 2022. "A Novel Algorithmic Forex Trade and Trend Analysis Framework Based on Deep Predictive Coding Network Optimized with Reptile Search Algorithm" Axioms 11, no. 8: 396. https://doi.org/10.3390/axioms11080396