1. Introduction

The extended exponential–geometric (EEG) distribution was proposed by [

1] to analyze lifetime data. If the

Y random variable has the EEG distribution, then its probability density function (PDF) is given by

where

and

. This distribution provides decreasing or increasing hazard functions based on the values of its parameters, providing great flexibility of fit for real applications.

The importance of models with bounded support, particularly at unit intervals, is well established for modeling rates, indices, proportions, scores, etc. A wide range of distributions have been introduced and used in numerous different fields. The log-extended exponential–geometric (LEEG) distribution was introduced by [

2], applying the transformation

, where the random variable

Y follows the EEG distribution. The LEEG distribution is an alternative to the beta distribution and has applications in the populations of cities, the sizes of power outages, and the intensities of earthquakes. Ref. [

2] investigates some of the mathematical features of the LEEG distribution, such as moments and order statistics. Ref. [

3] discussed the Fisher information matrix of the LEEG distribution based on simple random sample, ranked set sample, median ranked set sample, and extreme ranked set sample. Ref. [

4] estimated the LEEG distribution parameters under simple random sampling and moving extremes ranked set sampling.

The PDF of the random variable

X following the LEEG distribution is of the form

and the corresponding cumulative distribution function (CDF) is

where

,

. It is worth noting that the specific situation

corresponds to the power function, which includes the uniform distribution for

. The PDF of the LEEG distribution is flexible and has a variety of asymmetic shapes, which make it attractive for statistical purposes. For more details on the LEEG distribution and its applications, see [

2,

4,

5,

6].

The

j-th moment of the LEEG distribution in Equation (

1) is given as (see [

2])

where

is the Lerch transcendent function of the form

which converges for any real number

if

z and

s are any complex numbers with either

or

and

, see [

7].

It is easy to see that (

1) and (

2) satisfy the following relationship:

where

The generalized order statistics (GOS) model is a model that contains many models of ordered random variables by selecting the parameters appropriately. Ref. [

8] introduced the concept of GOS as follows.

Let

be the parameters such that

. Then,

are the

n GOS, and their joint PDF is of the form

where

Many models of ordered random variables can be viewed as special instances of GOS. If and such that , then the model reduces to ordinary order statistics. For and such that , the model reduces to the k-th record values. Also, for , and where denotes the fixed number of failure of units to be observed, the model reduces to progressive Type-II censored order statistics. Here, we consider the following two cases:

Case 1: When

, the PDF of

is given by (Kamps and Cramer [

9])

and the joint PDF of

and

,

is given by [

9]

where

, and

Case 2: When

In this case, the PDF of

is given by (Kamps [

8])

and the joint PDF of

and

,

is given by (Kamps [

8])

where

and

.

The moments of ordered random schemes have garnered a lot of attention in recent years. Many authors studied the moments of GOS for various distributions. For example, see for some general forms of distribution [

9,

10,

11] and for some specific distributions [

12,

13,

14,

15,

16]. For more recent works, see [

17,

18,

19,

20]. However, to our knowledge, no attempt has yet been made to study the LEEG distribution based on GOS.The motivation for this paper is twofold: first, to derive the explicit expressions and recurrence relations for the single and product moments based on the GOS of the LEEG distribution; second, to obtain the best linear unbiased estimators (BLUEs) for the location and scale parameters based on progressively Type-II right censored order statistics.

The paper is organized as follows.

Section 2 and

Section 3 provide the explicit expressions and recurrence relations for the single and product moments of GOS from the LEEG distribution. In

Section 4, we compute the BLUEs for the location and scale parameters based on progressively Type-II right censored order statistics.

Section 5 includes a real example that is utilized to illustrate the findings obtained in the previous section.

4. BLUEs for Location-Scale LEEG Distribution

Suppose is a progressively Type-II right censored sample from a location-scale LEEG distribution with location parameter and scale parameter . Let , denote the corresponding progressively Type-II right censored sample from the standard distribution, and . Denote , as the mean vector, and as the variance–covariance matrix.

Then, the BLUE of the parameter

is given by

where

and

Moreover, the variances and covariances of these BLUEs are given by

and

See [

23,

24] for more details.

The coefficients of the BLUEs for

and

and the values Var

, Var

, and Cov

are displayed in

Table 5,

Table 6 and

Table 7 for sample size

and for different choices of

and progressive censoring schemes. The coefficients of the BLUEs

and

in

Table 5 and

Table 6 can be checked by the conditions

and

.

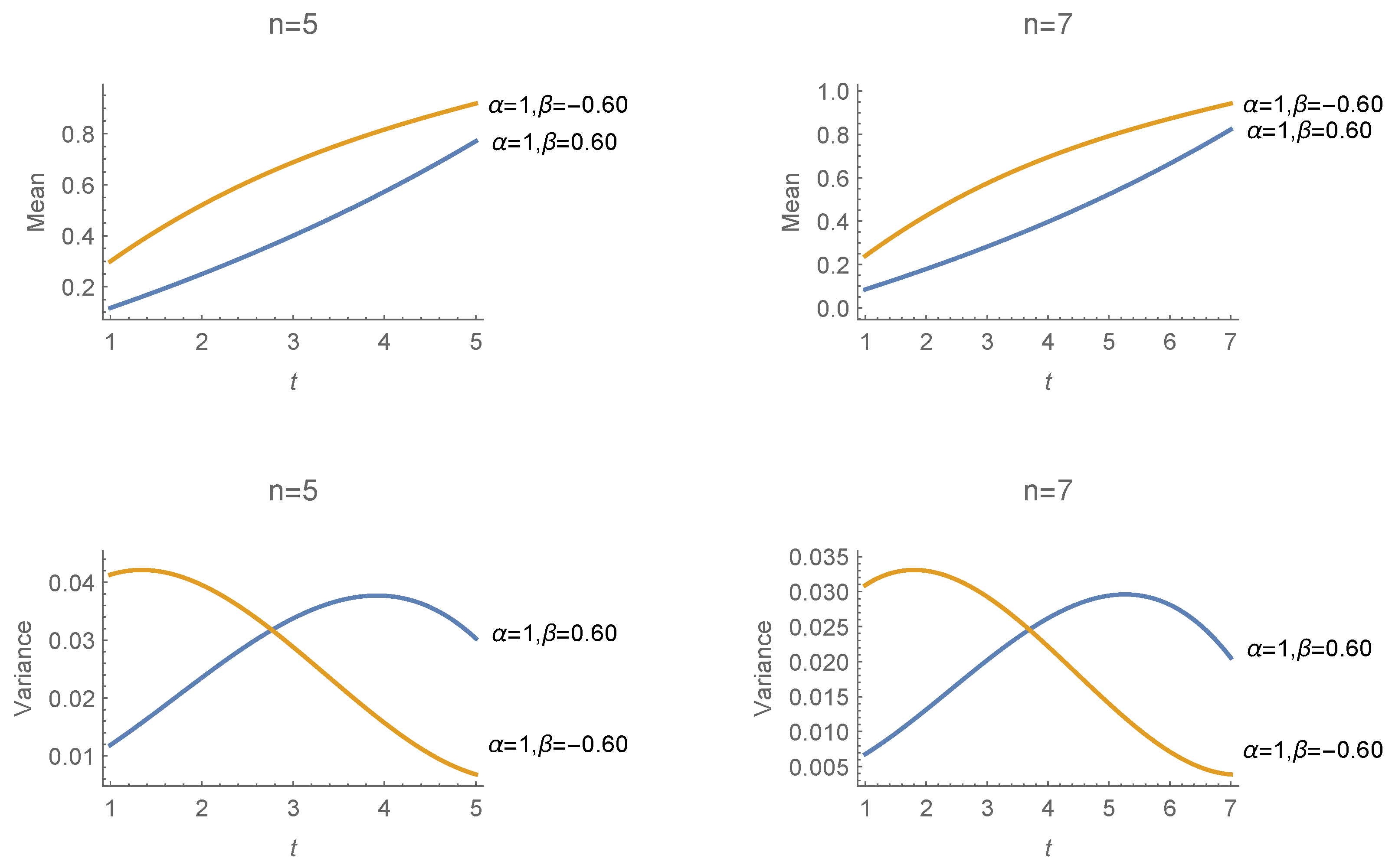

Table 5.

Coefficients for the BLUEs of for some selected progressive censoring schemes for the location-scale LEEG distribution with and .

Table 5.

Coefficients for the BLUEs of for some selected progressive censoring schemes for the location-scale LEEG distribution with and .

| | n | Scheme | Coefficients |

|---|

| −0.60 | 2 | 10 | | 1.35761 | −0.35761 | | | |

| −0.60 | 2 | 10 | | 2.21617 | −1.21617 | | | |

| 0.60 | 2 | 10 | | 1.15115 | −0.15115 | | | |

| 0.60 | 2 | 10 | | 1.93408 | −0.93408 | | | |

| −0.60 | 3 | 10 | | 1.267510 | 0.048873 | −0.316382 | | |

| −0.60 | 3 | 10 | | 1.622630 | 0.090463 | −0.713096 | | |

| 0.60 | 3 | 10 | | 1.084910 | 0.044168 | −0.129077 | | |

| 0.60 | 3 | 10 | | 1.465590 | −0.028833 | −0.436757 | | |

| −0.60 | 4 | 10 | | 1.233440 | 0.035801 | 0.051191 | −0.32043 | |

| −0.60 | 4 | 10 | | 1.424650 | 0.058870 | 0.071805 | −0.555328 | |

| 0.60 | 4 | 10 | | 1.079010 | −0.057814 | 0.147298 | −0.168491 | |

| 0.60 | 4 | 10 | | 1.309520 | −0.019550 | −0.018046 | −0.271927 | |

| −0.60 | 5 | 10 | | 1.212280 | 0.029705 | 0.040361 | 0.054430 | −0.336772 |

| −0.60 | 5 | 10 | | 1.324870 | 0.043549 | 0.053086 | 0.064140 | −0.485642 |

| 0.60 | 5 | 10 | | 1.154350 | −0.249614 | 0.081079 | 0.283290 | −0.269101 |

| 0.60 | 5 | 10 | | 1.231460 | −0.014845 | −0.013701 | −0.012619 | −0.190292 |

Table 6.

Coefficients for the BLUEs of for some selected progressive censoring schemes for the location-scale LEEG distribution with and .

Table 6.

Coefficients for the BLUEs of for some selected progressive censoring schemes for the location-scale LEEG distribution with and .

| | n | Scheme | Coefficients |

|---|

| −0.60 | 2 | 10 | | −1.93907 | 1.93907 | | | |

| −0.60 | 2 | 10 | | −6.59438 | 6.59438 | | | |

| 0.60 | 2 | 10 | | −2.48946 | 2.48946 | | | |

| 0.60 | 2 | 10 | | −15.3849 | 15.3849 | | | |

| −0.60 | 3 | 10 | | −1.50756 | −0.12082 | 1.62838 | | |

| −0.60 | 3 | 10 | | −3.43490 | −0.361011 | 3.79591 | | |

| 0.60 | 3 | 10 | | −1.88178 | 0.146175 | 1.73560 | | |

| 0.60 | 3 | 10 | | −7.63449 | 0.409117 | 7.22538 | | |

| −0.60 | 4 | 10 | | −1.37515 | −0.069004 | −0.100254 | 1.54441 | |

| −0.60 | 4 | 10 | | −2.41641 | −0.19848, | −0.241947 | 2.85684 | |

| 0.60 | 4 | 10 | | −1.86443 | 0.583966 | −0.312108 | 1.592570 | |

| 0.60 | 4 | 10 | | −5.02877 | 0.254115 | 0.234554 | 4.54010 | |

| −0.60 | 5 | 10 | | −1.310220 | −0.048427 | −0.066312 | −0.089994 | 1.514960 |

| −0.60 | 5 | 10 | | −1.927040 | −0.123346 | −0.150142 | −0.181194 | 2.381720 |

| 0.60 | 5 | 10 | | −2.310470 | 1.680380 | −0.497668 | −0.637334 | 1.765090 |

| 0.60 | 5 | 10 | | −3.706610 | 0.174442 | 0.160968 | 0.148230 | 3.222970 |

Table 7.

The values of Var, Var and Cov for some selected progressive censoring schemes for the location-scale LEEG distribution with and .

Table 7.

The values of Var, Var and Cov for some selected progressive censoring schemes for the location-scale LEEG distribution with and .

| | n | Scheme | | | |

|---|

| −0.60 | 2 | 10 | | 0.039000 | 0.234720 | −0.071469 |

| −0.60 | 2 | 10 | | 0.056385 | 0.691219 | −0.160697 |

| 0.60 | 2 | 10 | | 0.004760 | 0.423011 | −0.023590 |

| 0.60 | 2 | 10 | | 0.007123 | 0.924341 | −0.058274 |

| −0.60 | 3 | 10 | | 0.033814 | 0.094203 | −0.044520 |

| −0.60 | 3 | 10 | | 0.042320 | 0.292673 | −0.085827 |

| 0.60 | 3 | 10 | | 0.003466 | 0.159245 | −0.005680 |

| 0.60 | 3 | 10 | | 0.005344 | 0.437374 | −0.028838 |

| −0.60 | 4 | 10 | | 0.032441 | 0.060941 | −0.037824 |

| −0.60 | 4 | 10 | | 0.037611 | 0.168037 | −0.061599 |

| 0.60 | 4 | 10 | | 0.002489 | 0.072280 | 0.002225 |

| 0.60 | 4 | 10 | | 0.004751 | 0.272057 | −0.018936 |

| −0.60 | 5 | 10 | | 0.031844 | 0.048360 | −0.035150 |

| −0.60 | 5 | 10 | | 0.035224 | 0.110639 | −0.049896 |

| 0.60 | 5 | 10 | | 0.000822 | 0.012654 | 0.010497 |

| 0.60 | 5 | 10 | | 0.004454 | 0.186895 | −0.013908 |

5. Real Data Application

In this part, we consider a real data set as an application of the estimating method provided in this article. The data set is available in [

25] and consists of seventy-three observations on seven variables. Many authors analyzed these data; see [

26,

27,

28]. The data set’s description may be found in [

27].

Here, attention is on the variable FIRMCOST (divided by 100), which is a measure of the cost effectiveness of the firm’s risk management practices. A random sample of size ten is selected as follows: 0.002, 0.0036, 0.004, 0.0122, 0.0407, 0.0571, 0.0849, 0.1357, 0.1833, 0.2222. From the above data, we generate a progressively Type-II censored sample with

,

, and the censoring scheme

. The generated progressively Type-II censored sample is shown in

Table 8.

A simple plot of these censored values against the expected values given in

Table 3 for

and

shows a quite high correlation (i.e., a correlation coefficient of the order of 0.9743). Hence, we can assume that these data comes from the LEEG distribution with

and

.

Based on the progressively Type-II censored sample presented above, we find the BLUEs of and to be and , respectively, and their standard errors to be and .

{kind=link}