Measurement of the Threatened Biodiversity Existence Value Output: Application of the Refined System of Environmental-Economic Accounting in the Pinus pinea Forests of Andalusia, Spain

Abstract

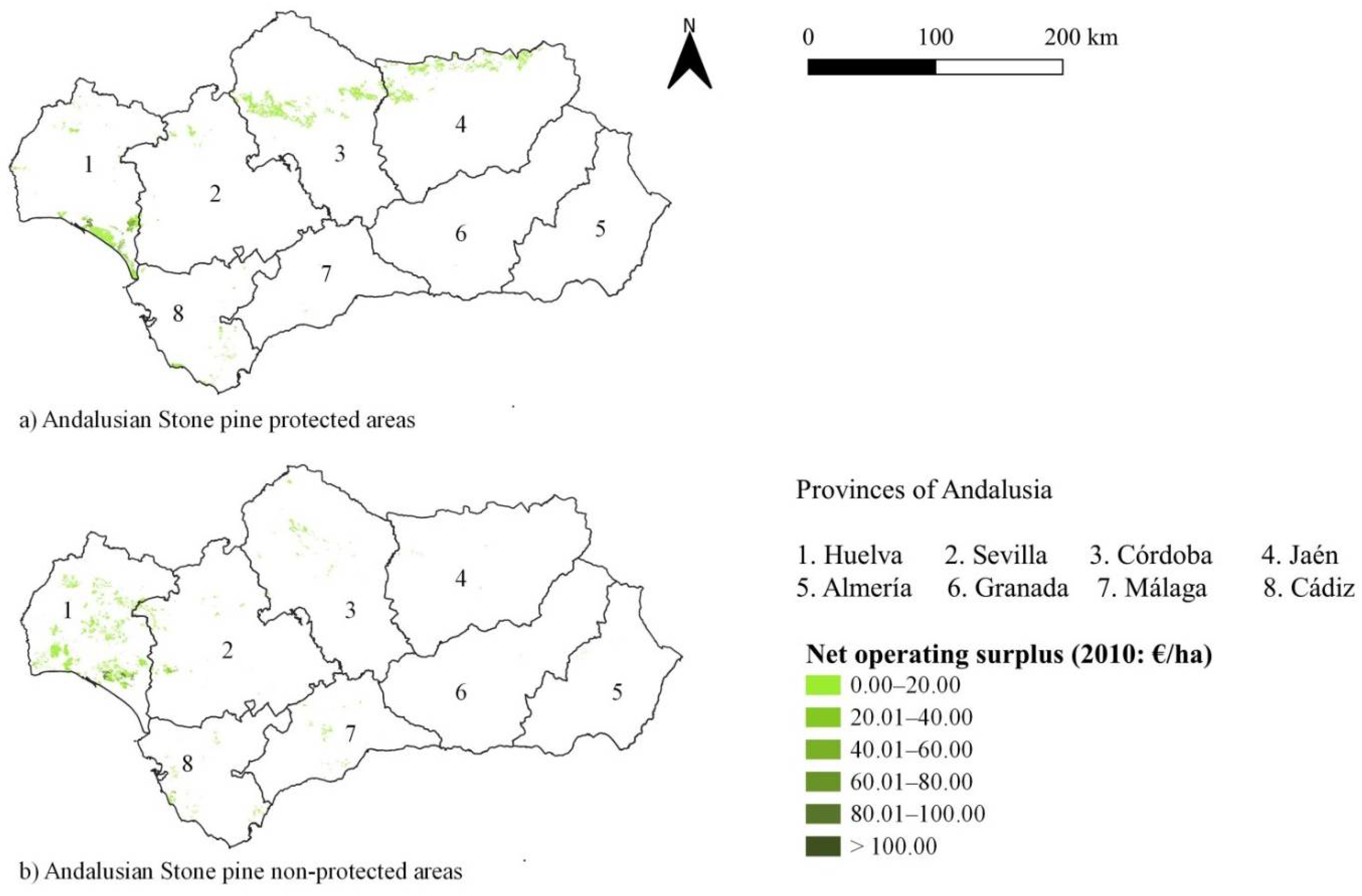

:1. Introduction

2. Concepts and Valuation Methods for Biodiversity Output Applied to the Pinus pinea Forests of Andalusia

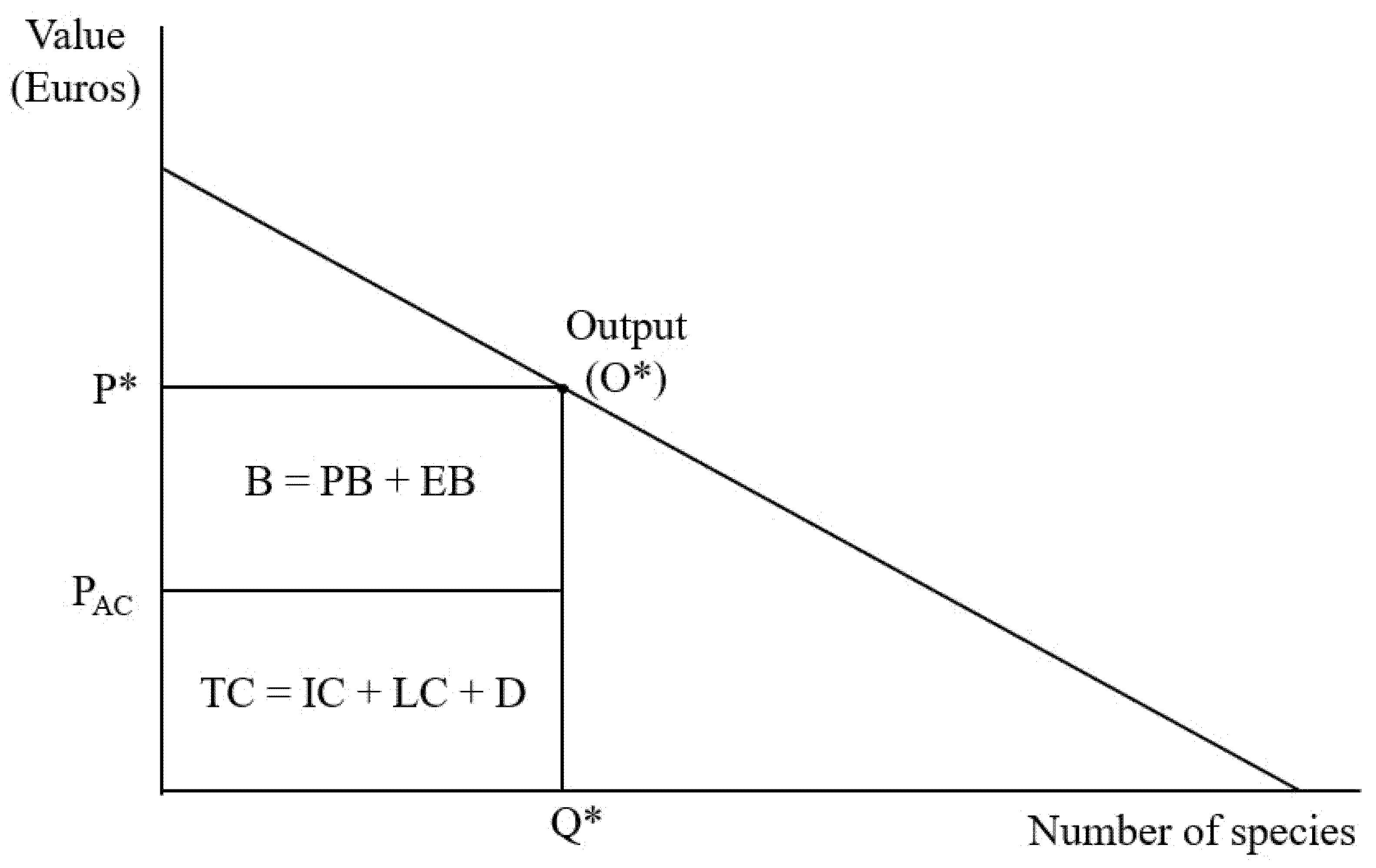

2.1. Concept of Transaction Price of Biodiversity Output

2.2. The Refined SEEA Output and Income Accounts for Threatened Biodiversity

3. Output and Net Value Added Results for Biodiversity in Pinus pinea Forests

3.1. Rationale of Public Management of the Pinus pinea Forests of Andalusia

3.2. Economic Results for Pinus pinea Biodiversity

4. Discussion of the Advances in Methods Applied and Estimated Results

4.1. The Omission of the Benefit of Biodiversity in the SEEA Guidelines

4.2. Uncertainty in the Estimation of the Threatened Biodiversity Demand

4.3. Towards the Management of Biodiversity Based on Economic-Environmental Accounting

5. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Class | Protected Areas (SPPAs) | Non-Protected Areas (SPNPAs) | ||

|---|---|---|---|---|

| (ha) | (%) | (ha) | (%) | |

| Without secondary species | 41,616 | 29.8 | 49,343 | 47.6 |

| Quercus ilex | 48,618 | 34.8 | 11,441 | 11.0 |

| Without tertiary species | 32,389 | 23.2 | 7315 | 7.1 |

| With tertiary species | 16,229 | 11.6 | 4126 | 4.0 |

| Quercus suber | 7242 | 5.2 | 9453 | 9.1 |

| Without tertiary species | 5058 | 3.6 | 5581 | 5.4 |

| With tertiary species | 2184 | 1.6 | 3871 | 3.7 |

| Quercus faginea | 1364 | 1.0 | 12 | 0.0 |

| Without tertiary species | 441 | 0.3 | 0.0 | |

| With tertiary species | 923 | 0.7 | 12 | 0.0 |

| Olea europaea | 3168 | 2.3 | 2029 | 2.0 |

| Without tertiary species | 1265 | 0.9 | 1359 | 1.3 |

| With tertiary species | 1902 | 1.4 | 671 | 0.6 |

| Pinus halepensis | 779 | 0.6 | 3446 | 3.3 |

| Without tertiary species | 475 | 0.3 | 1846 | 1.8 |

| With tertiary species | 305 | 0.2 | 1600 | 1.5 |

| Pinus pinaster | 17,195 | 12.3 | 3448 | 3.3 |

| Without tertiary species | 6935 | 5.0 | 1620 | 1.6 |

| With tertiary species | 10,260 | 7.3 | 1828 | 1.8 |

| Eucalyptus camaldulensis | 2415 | 1.7 | 5200 | 5.0 |

| Without tertiary species | 1394 | 1.0 | 4479 | 4.3 |

| With tertiary species | 1021 | 0.7 | 721 | 0.7 |

| Eucalyptus globulus | 2459 | 1.8 | 11,947 | 11.5 |

| Without tertiary species | 1924 | 1.4 | 9672 | 9.3 |

| With tertiary species | 535 | 0.4 | 2274 | 2.2 |

| Juniperus phoenicea | 5807 | 4.2 | 40 | 0.0 |

| Without tertiary species | 4837 | 3.5 | 40 | 0.0 |

| With tertiary species | 970 | 0.7 | 0.0 | |

| Juniperus oxycedrus | 828 | 0.6 | 97 | 0.1 |

| Without tertiary species | 418 | 0.3 | 43 | 0.0 |

| With tertiary species | 410 | 0.3 | 55 | 0.1 |

| Arbutus unedo | 978 | 0.7 | 609 | 0.6 |

| Without tertiary species | 423 | 0.3 | 269 | 0.3 |

| With tertiary species | 555 | 0.4 | 340 | 0.3 |

| Others | 7367 | 5.3 | 6657 | 6.4 |

| Total | 139,836 | 100.0 | 103,723 | 100.0 |

| Number | Species | Degree of Threat (*) | Unit Values of ACTsaAFAs by Single Species in Andalusian Forest Areas | Protected Areas (SPPAs) | Non-Protected Areas (SPNPAs) | ||

|---|---|---|---|---|---|---|---|

| Presence of the Threatened Species in Protected Areas (AsPAs,SP) | Values of ACTsSP by Species (SPPAs) | Presence of the Threatened Species in Non-Protected Areas (AsNPAs,SP) | Values of ACTsSP Per Species in Protected (SPPAs) and Non-Protected (SPNPAs) Areas of Andalusian Stone Pine | ||||

| (€/ha) | (ha) | (€) | (ha) | (€) | |||

| 1 | Abies pinsapo | EN | 15.0 | 2 | 30 | 0 | 0 |

| 2 | Aegypius monachus | EN | 2.2 | 16,905 | 38,684 | 5878 | 13,031 |

| 3 | Apus caffer | VU | 5.4 | 177 | 980 | 292 | 1593 |

| 4 | Aquila adalberti | CR | 0.3 | 83,521 | 31,365 | 19,440 | 5913 |

| 5 | Aquila chrysaetos | VU | 0.2 | 24,237 | 7690 | 2780 | 683 |

| 6 | Armeria velutina | VU | 3.2 | 27,862 | 90,411 | 14,766 | 46,861 |

| 7 | Baetica ustulata | VU | 1.0 | 4516 | 4950 | 900 | 923 |

| 8 | Bubo bubo | NT | 0.2 | 4749 | 1297 | 7234 | 1459 |

| 9 | Bufo calamita | LC | 0.1 | 5482 | 851 | 8081 | 677 |

| 10 | Canis lupus | CR | 0.4 | 73,680 | 39,652 | 1006 | 470 |

| 11 | Capreolus capreolus | VU | 0.7 | 26,858 | 22,084 | 3719 | 2792 |

| 12 | Caprimulgus europaeus | VU | 3.5 | 270 | 959 | 185 | 644 |

| 13 | Carduus myriacanthus. | VU | 37.6 | 291 | 10,953 | 54 | 2026 |

| 14 | Centaurea citricolor | EN | 76.8 | 318 | 24,439 | 0 | 0 |

| 15 | Chalcides bedriagai | NT | 0.3 | 3586 | 1312 | 6091 | 1794 |

| 16 | Ciconia nigra | EN | 0.7 | 10,270 | 8528 | 9669 | 7339 |

| 17 | Circaetus gallicus | NT | 0.2 | 5690 | 1933 | 5741 | 15,340 |

| 18 | Circus aeruginosus | EN | 1.9 | 2331 | 4642 | 3068 | 5892 |

| 19 | Circus pygargus | VU | 0.2 | 17 | 5 | 146 | 34 |

| 20 | Coluber hippocrepis | NT | 0.2 | 102 | 30 | 180 | 40 |

| 21 | Columba oenas | EN | 0.5 | 102 | 55 | 180 | 85 |

| 22 | Columba palumbus | LC | 0.1 | 6611 | 994 | 8550 | 675 |

| 23 | Coracias garrulous | NT | 0.1 | 583 | 108 | 767 | 88 |

| 24 | Coronella austriaca | EN | 5.6 | 10 | 57 | 0 | 0 |

| 25 | Corvus corone | LC | 0.1 | 1769 | 358 | 2067 | 271 |

| 26 | Corvus monedula | LC | 0.1 | 6611 | 1149 | 8550 | 875 |

| 27 | Culcita macrocarpa. | EN | 58.2 | 17 | 971 | 0 | 0 |

| 28 | Discoglossus galganoi | NT | 0.8 | 2563 | 2159 | 5580 | 4302 |

| 29 | Discoglossus jeanneae | NT | 1.4 | 1022 | 1513 | 940 | 1323 |

| 30 | Egretta garzetta | LC | 2.2 | 2936 | 6790 | 1855 | 4158 |

| 31 | Elanus caeruleus | VU | 0.1 | 4224 | 817 | 8076 | 985 |

| 32 | Eptesicus serotinus | NT | 4.1 | 1819 | 7702 | 1669 | 6951 |

| 33 | Erica andevalensis | EN | 3.1 | 573 | 1810 | 4692 | 14,487 |

| 34 | Euphydryas aurinia | LC | 1.4 | 80 | 115 | 637 | 878 |

| 35 | Falco naumanni | NT | 0.2 | 113 | 35 | 157 | 37 |

| 36 | Felis silvestris | NT | 0.1 | 3781 | 742 | 3486 | 436 |

| 37 | Festuca elegans | NT | 0.7 | 5249 | 3956 | 839 | 572 |

| 38 | Galerida theklae | NT | 0.1 | 6566 | 1533 | 8539 | 1383 |

| 39 | Gaudinia hispanica. | VU | 10.9 | 2313 | 25,426 | 2501 | 27,310 |

| 40 | Genetta genetta | NT | 0.1 | 75,021 | 12,870 | 49,541 | 4962 |

| 41 | Gyps fulvus | LC | 0.5 | 5741 | 3269 | 90 | 45 |

| 42 | Herpestes ichneumon | LC | 0.5 | 3973 | 2449 | 4268 | 2326 |

| 43 | Hieraaetus fasciatus | VU | 0.1 | 40,226 | 7242 | 8146 | 885 |

| 44 | Hieraaetus pennatus | LC | 0.1 | 139,596 | 32,908 | 103,588 | 17,025 |

| 45 | Hymenostemma pseudoanthemis | VU | 15.9 | 30 | 486 | 1067 | 17,026 |

| 46 | Hypsugo savii | NT | 0.5 | 610 | 349 | 0 | 0 |

| 47 | Linaria tursica | EN | 5.0 | 5289 | 27,108 | 470 | 2378 |

| 48 | Lucanus cervus | LC | 1087.2 | 0 | 0 | 0 | 0 |

| 49 | Lullula arborea | LC | 0.4 | 6566 | 3079 | 8539 | 3394 |

| 50 | Luscinia svecica | NT | 0.3 | 2689 | 1046 | 6216 | 1973 |

| 51 | Lynx pardinus | EN | 1.1 | 42,854 | 49,594 | 20,272 | 22,013 |

| 52 | Macrothele calpeiana | VU | 2.6 | 220 | 589 | 1418 | 3693 |

| 53 | Micropyropsis tuberosa | EN | 17.1 | 2301 | 39,473 | 2967 | 50,681 |

| 54 | Milvus migrans | NT | 0.5 | 4486 | 2607 | 6120 | 3120 |

| 55 | Milvus milvus | CR | 2.5 | 334 | 871 | 0 | 0 |

| 56 | Miniopterus schreibersii | VU | 0.4 | 1090 | 500 | 2035 | 787 |

| 57 | Mustela putorius | NT | 0.1 | 52,966 | 11,560 | 34,187 | 5021 |

| 58 | Myotis blythii | VU | 0.5 | 1029 | 602 | 2321 | 1193 |

| 59 | Myotis emarginata | VU | 1.6 | 679 | 1,1278 | 68 | 108 |

| 60 | Myotis escalerai | VU | 2.4 | 3713 | 9280 | 6449 | 15,657 |

| 61 | Myotis myotis | VU | 0.3 | 1881 | 829 | 1610 | 594 |

| 62 | Narcissus fernandesii | VU | 0.7 | 1253 | 1006 | 0 | 0 |

| 63 | Narcissus humilis | LC | 0.8 | 1481 | 1336 | 7501 | 6230 |

| 64 | Narcissus triandrus | LC | 0.2 | 27,291 | 8196 | 3286 | 752 |

| 65 | Narcissus viridiflorus | VU | 16.2 | 115 | 1871 | 1225 | 19,884 |

| 66 | Neophron percnopterus | CR | 0.3 | 10,315 | 3892 | 2235 | 684 |

| 67 | Nyctalus lasiopterus | VU | 9.3 | 7849 | 73,867 | 2623 | 24,498 |

| 68 | Nyctalus leisleri | VU | 5.1 | 10,486 | 54,442 | 5315 | 27,214 |

| 69 | Nyctalus noctula | EW | 28.3 | 5638 | 159,838 | 2623 | 74,173 |

| 70 | Orobanche densiflora | LC | 0.3 | 8666 | 3187 | 9014 | 2671 |

| 71 | Otis tarda | CR | 0.3 | 755 | 293 | 1207 | 383 |

| 72 | Pandion haliaetus | VU | 11.2 | 413 | 4680 | 0 | 0 |

| 73 | Pelobates cultripes | NT | 0.5 | 3031 | 1676 | 6034 | 2906 |

| 74 | Pica pica | LC | 0.1 | 6598 | 1011 | 8545 | 699 |

| 75 | Picris willkommi. | VU | 38.9 | 0 | 0 | 214 | 8335 |

| 76 | Pipistrellus kuhlii | NT | 8.9 | 1880 | 16,812 | 1281 | 11,368 |

| 77 | Pipistrellus pygmaeus | DD | 2.2 | 14,943 | 33,801 | 10,293 | 22,547 |

| 78 | Plantago algarbiensis | NT | 80.5 | 1872 | 150,803 | 2488 | 200,290 |

| 79 | Plecotus austriacus | NT | 2.5 | 431 | 1126 | 3424 | 8694 |

| 80 | Quercus alpestris | EN | 0.6 | 1080 | 770 | 1759 | 1129 |

| 81 | Rhinolophus euryale | VU | 0.3 | 1881 | 822 | 10,010 | 369 |

| 82 | Rhinolophus ferrumequinum | VU | 0.2 | 4391 | 1110 | 5214 | 946 |

| 83 | Rhinolophus hipposideros | VU | 1.1 | 0 | 0 | 724 | 799 |

| 84 | Rhinolophus mehelyi | EN | 0.6 | 1161 | 835 | 1759 | 1139 |

| 85 | Salix salviifolia | NT | 3.0 | 1623 | 4963 | 1798 | 5369 |

| 86 | Scilla odorata | NT | 7.4 | 0 | 0 | 1760 | 13,106 |

| 87 | Scolopax rusticola | LC | 1.1 | 2116 | 2453 | 1798 | 1955 |

| 88 | Silene mariana | VU | 3.5 | 2623 | 9397 | 440 | 1545 |

| 89 | Silene stockeni. | EN | 4.2 | 0 | 0 | 623 | 2641 |

| 90 | Spiranthes aestivalis | NT | 1.3 | 949 | 1278 | 31 | 39 |

| 91 | Streptopelia turtur | VU | 0.4 | 6179 | 2969 | 7105 | 2907 |

| 92 | Sturnus vulgaris | LC | 0.1 | 6611 | 1024 | 8550 | 714 |

| 93 | Sylvia atricapilla | NT | 0.1 | 139,596 | 24,804 | 103,673 | 11,020 |

| 94 | Sylvia cantillans | LC | 0.2 | 339 | 112 | 264 | 68 |

| 95 | Sylvia communis | NT | 0.7 | 393 | 327 | 520 | 396 |

| 96 | Sylvia hortensis | DD | 1.5 | 57 | 92 | 86 | 132 |

| 97 | Sylvia melanocephala | LC | 0.1 | 139,596 | 19,920 | 103,673 | 7393 |

| 98 | Testudo graeca | EN | 0.7 | 24,263 | 20,337 | 2618 | 2005 |

| 99 | Thymus carnosus | VU | 36 | 302 | 10,880 | 813 | 29,268 |

| 100 | Turdus iliacus | LC | 0.1 | 6566 | 1029 | 8539 | 729 |

| 101 | Turdus philomelos | LC | 0.1 | 6611 | 1033 | 8550 | 725 |

| 102 | Turdus torquatus | LC | 0.3 | 17,213 | 7577 | 12,981 | 4788 |

| 103 | Turdus viscivorus | LC | 0.1 | 139,121 | 32,887 | 101,481 | 16,745 |

| 104 | Turnix sylvatica | CR | 1.6 | 4963 | 8597 | 7534 | 12,512 |

| Total | 8.1 | 139,836 | 1,225,964 | 103,723 | 841,172 | ||

References

- European Commission; International Monetary Fund; Organization for Economic Co-operation and Development; United Nations; World Bank. System of National Accounts 2008 (SNA 2008); United Nations: New York, NY, USA, 2009; 722p, Available online: http://unstats.un.org/unsd/nationalaccount/docs/SNA2008.pdf (accessed on 27 September 2017).

- European Commission. COM (2020) 380 Final: EU Strategy on Biodiversity between Now and 2030 Reintegrate Nature into Our Lives; European Commission: Brussels, Belgium, 2020; 25p, Available online: https://ec.europa.eu/info/sites/default/files/communication-annex-eu-biodiversity-strategy-2030_en.pdf (accessed on 28 April 2022).

- Ivanić, K.-Z.; Stolton, S.; Figueroa Arango, C.; Dudley, N. Protected Areas Benefits Assessment Tool + (PA-BAT+): A Tool to Assess Local Stakeholder Perceptions of the Flow of Benefits from Protected Areas; IUCN: Gland, Switzerland, 2020; xii + 84p. [Google Scholar] [CrossRef]

- The Economics of Ecosystems and Biodiversity (TEEB). Mainstreaming the Economics of Nature: A Synthesis of the Approach, Conclusions and Recommendations of TEEB; The Economics of Ecosystems and Biodiversity: Valletta, Malta, 2010; 39p, Available online: http://www.teebweb.org/wp-content/uploads/Study%20and%20Reports/Reports/Synthesis%20report/TEEB%20Synthesis%20Report%202010.pdf (accessed on 6 June 2022).

- United Nations; et al. System of Environmental-Economic Accounting—Ecosystem Accounting (SEEA EA). White Cover Publication, Pre-Edited Text Subject to Official Editing; United Nations: New York, NY, USA, 2021; 371p, Available online: https://seea.un.org/sites/seea.un.org/files/documents/EA/seea_ea_white_cover_final.pdf (accessed on 6 June 2022).

- Protected Planet Report. Tracking Progress towards Global Targets for Protected and Conserved Areas; UNEP-WCMC: Cambridge, UK; IUCN: Gland, Switzerland, 2020; Available online: https://livereport.protectedplanet.net/ (accessed on 6 June 2022).

- Brundtland, G.H. Editorial: The Scientific Underpinning of Policy. Science 1997, 277, 457. [Google Scholar] [CrossRef]

- Montes, C.; Lomas, P. La Evaluación de los Ecosistemas del Milenio en España. Ciencia y política para el beneficio de la sociedad y la naturaleza. Ambienta 2010, 91, 56–75. [Google Scholar]

- CBD. Protected Areas in Today’s World: Their Values and Benefits for the Welfare of the Planet; Technical Series no. 36; Secretariat of the Convention on Biological Diversity: Montreal, QC, Canada, 2008; vii + 96p, Available online: https://www.cbd.int/doc/publications/cbd-ts-36-en.pdf (accessed on 28 April 2022).

- Fundación Biodiversidad. Evaluación de los Ecosistemas del Milenio en España. Ecosistemas y Biodiversidad de España para el Bienestar Humano. Valoración Económica de los Servicios de los Ecosistemas Suministrados por los Ecosistemas de España. Informe Técnico Final EMEC; Ministerio de Agricultura, Alimentación y Medio Ambiente: Madrid, Spain, 2014; 168p. Available online: http://www.ecomilenio.es/wp-content/uploads/2009/04/Informe-EMEC-def_web.pdf (accessed on 28 April 2022).

- García, S. Beneficios Económicos de la Red Natura 2000 en España; Ministerio para la Transición Ecológica: Madrid, Spain, 2019; 364p. Available online: https://www.miteco.gob.es/es/biodiversidad/temas/espacios-protegidos/beneficios_economicos_n2000_web_2019_tcm30-498070.pdf (accessed on 28 April 2022).

- Campos, P.; Caparrós, A.; Oviedo, J.L.; Ovando, P.; Álvarez-Farizo, B.; Díaz-Balteiro, L.; Carranza, J.; Beguería, S.; Díaz, M.; Herruzo, A.C.; et al. Bridging the gap between national and ecosystem accounting application in Andalusian forests, Spain. Ecol. Econ. 2019, 157, 218–236. [Google Scholar] [CrossRef]

- Campos, P.; Álvarez, A.; Oviedo, J.L.; Ovando, P.; Mesa, B.; Caparrós, A. Environmental incomes: Refined standard and extended accounts applied to cork oak open woodlands in Andalusia, Spain. Ecol. Indic. 2020, 117, 106551. [Google Scholar] [CrossRef]

- Campos, P.; Álvarez, A.; Oviedo, J.L.; Ovando, P.; Mesa, B.; Caparrós, A. Income and Ecosystem Service Comparisons of Refined National and Agroforestry Accounting Frameworks: Application to Holm Oak Open Woodlands in Andalusia, Spain. Forests 2020, 11, 185. [Google Scholar] [CrossRef] [Green Version]

- Campos, P.; Álvarez, A.; Mesa, B.; Oviedo, J.L.; Caparrós, A. Linking standard Economic Account for Forestry and ecosystem accounting: Total forest incomes and environmental assets in publicly-owned conifer farms in Andalusia-Spain. For. Policy Econ. 2021, 128, 102482. [Google Scholar] [CrossRef]

- Campos, P. Cuentas convencionales y agroforestales comparadas del bosque: Aplicación en la finca pública de pino piñonero Mazagón en el espacio natural protegido de Doñana, Moguer-Huelva. In INIAV: Livro Homenagem Inocêncio Seita Coelho; Instituto Nacional de Investigação Agrária e Veterinária: Oeiras, Portugal, in revision.

- United Nations. Monetary Valuation of Ecosystem Services and Ecosystem Assets for Ecosystem Accounting: Interim Version; United Nations Department of Economic and Social Affairs, Statistics Division: New York, NY, USA, 2022. [Google Scholar]

- MFE. Mapa Forestal de España, Escala 1:1.000.000 (MFE1000); Ministerio de Medio Ambiente: Madrid, Spain, 2003. Available online: https://www.miteco.gob.es/es/biodiversidad/servicios/banco (accessed on 28 April 2022).

- Norton, B.G. Why Preserve Natural Variety? Princeton University Press: Princeton, NJ, USA, 1987; 281p. [Google Scholar]

- Campos, P.; Oviedo, J.L.; Álvarez, A.; Ovando, P.; Mesa, B.; Caparrós, A. Measuring environmental incomes beyond standard national and ecosystem accounting frameworks: Testing and comparing the agroforestry Accounting System in a holm oak dehesa case study in Andalusia-Spain. Land Use Policy 2020, 99, 104984. [Google Scholar] [CrossRef]

- Pearce, D. Do we really care about Biodiversity? Environ. Resour. Econ. 2007, 37, 313–333. [Google Scholar] [CrossRef]

- European Commission. Flash Eurobarometer 491. A Long Term Vision for EU Rural Areas. Summary; European Commission: Brussels, Belgium, 2021; 10p, Available online: https://webgate.ec.europa.eu/ebsm/api/public/deliverable/download?doc=true&deliverableId=75807 (accessed on 28 April 2022).

- IESA-CSIC. Ecobarómetro de Andalucía 2018; Consejería de Agricultura, Ganadería, Pesca y Desarrollo Sostenible; Instituto de Estudios Sociales de Andalucía: Seville, Spain, 2018; 131p. Available online: https://www.juntadeandalucia.es/medioambiente/portal/documents/20151/405696/EBA2018_informe_completo.pdf/6e3b9950-c818-40f6-f404-6ff1b7f3b683?t=1572896267000 (accessed on 6 June 2022).

- Díaz, M.; Concepción, E.D.; Oviedo, J.L.; Caparrós, A.; Farizo, B.A.; Campos, P. A comprehensive index for threatened biodiversity valuation. Ecol. Ind. 2020, 108, 105696. [Google Scholar] [CrossRef]

- Ojeda, J.F.; Díaz, F. El Condado Litoral onubense: A la búsqueda de un modelo de desarrollo interno. Rev. De Estud. Andal. 1987, 8, 165–183. [Google Scholar]

- Junta de Andalucía. Plan Estratégico del Sector de la Piña en Andalucía; Junta de Andalucía: Seville, Spain, 2013; 141p. Available online: http://www.juntadeandalucia.es/medioambiente/portal_web/web/temas_ambientales/montes/usos_y_aprov/jornada_pina/Plan%20estrategico/plan_estrategico_borrador.pdf (accessed on 6 June 2022).

- Montero, G.; Martínez, F.; Alía, R.; Candela, J.A.; Ruíz-Peinado, R.; Cañellas, I.; Mutke, S.; Calama, R.; Gutiérrez, M.; Pavón, J.; et al. El Pino Piñonero (Pinus Pinea L.) en Andalucía: Ecología, Distribución y Selvicultura; Dirección General de Medio Ambiente; Consejería de Medio Ambiente and Junta de Andalucía: Seville, Spain, 2004; 260p.

- Council of Europe. European Landscape Convention; European Treaty Series no. 176; Council of Europe: Florence, Italy, 2000; Available online: http://www.convenzioneeuropeapaesaggio.beniculturali.it/uploads/Council%20of%20Europe%20-%20European%20Landscape%20Convention.pdf (accessed on 28 April 2022).

- Ovando, P.; Campos, P. Renta y capital del gasto público en los sistemas forestales de Andalucía. In Valoración de los Servicios Públicos y la Renta Total Social de los Sistemas Forestales de Andalucía; Memorias Científicas de RECAMAN, Campos, P., Caparrós, A., Eds.; Memorias Científicas de RECAMAN; Editorial CSIC: Madrid, Spain, 2016; Volume 5, memoria 5.3; pp. 283–425. Available online: http://libros.csic.es/product_info.php?products_id=1013 (accessed on 27 April 2018).

- BOE. Directiva 92/43/CEE del Consejo, de 21 de Mayo de 1992, Relativa a la Conservación de los Hábitats Naturales y de la Fauna y Flora Silvestres (DO 1992, L 206, p. 7), en su Versión Modificada por la Directiva 2013/17/UE del Consejo, de 13 de Mayo de 2013 (DO 2013, L 158, p. 193); Boletín Oficial del Estado: Madrid, Spain, 1992; 44p, Available online: https://www.boe.es/doue/1992/206/L00007-00050.pdf (accessed on 28 April 2022).

- Berrens, R. The safe minimum standard of conservation and endangered species: A review. Environ. Conserv. 2001, 28, 104–116. [Google Scholar] [CrossRef]

- Campos, P.; Caparrós, A.; Oviedo, J.L.; Almazán, E.; Ovando, P.; Álvarez, A.; Mesa, B. RECAMAN Project Georeferenced Economic Accounts for Andalusian Forest Systems; Consejería de Agricultura, Pesca y Desarrollo Sostenible de la Junta de Andalucía, Ed.; CSIC: Seville, Spain, 2015. Available online: https://recaman.agenciamedioambienteyagua.es/VICAF/visor.html (accessed on 5 July 2022).

| Class | Acronym | This Paper’s rSEEA | United Nations SEEA [5] | Accounting Identity |

|---|---|---|---|---|

| Output | O | Service of preserving wild species threatened with risk of extinction. It is valued by summing additional consumer tax (ACT) and total cost (TC). ACT is measured by a choice experiment survey to Andalusian households. TC is measured by biodiversity production function accruing from Andalusian government unpublished sources. | Service of preserving wild species threatened with risk of extinction is hidden in the government general production account of the System of National Accounts (SNAs). It is valued at total cost (TC). | OrSEEA = ACT + TC OrSEEA = ACT + OSEEA OSEEA = TC |

| Intermediate consumption | IC | Purchases of raw materials (RM) and services (SS) used as inputs in the generation of the output (O) in the accounting period. | Purchases of raw materials (RM) and services (SS) used as inputs in the generation of the output (O) in the accounting period. | IC = RM + SS |

| Gross valued added | GVA | Value of the biodiversity output (O) less intermediate consumption (IC). | Value of the biodiversity total cost (TC) less intermediate consumption (IC). | GVArSEEA = OrSEEA − IC GVASEEA = TC − IC |

| Depreciation | D | Consumption due to the use and obsolescence of produced durable goods used in the generation of output in the accounting period. Depreciation is valued at its replacement price. The components of durable goods are buildings (BD) and equipment (ED). | It coincides with rSEEA. | D = BD + ED |

| Net value added | NVA | Remuneration of the production factors of labour cost (LC) and benefits (B) at social price. | Omits the benefits (B). | NVArSEEA = GVA − D NVArSEEA = LC + B NVASEEA = LC |

| Labour cost | LC | Employee compensation. | Employee compensation. | |

| Benefit | B | Simulated benefit is valued at additional consumer tax (ACT) transaction price for Stone pine forests (SP) which the adult population of Andalusia would be willing to pay via an annual payment to avoid a one-species variation in the number of threatened species at the close of the period compared with the number at the opening of the period. Benefit is divided into imputed competitive produced capital benefit (PB) and residual environmental benefit of durable ecosystem asset (EB). | Rejects the existence of simulated benefit at transaction price for the existence value of threatened biodiversity [5] (para. 6.72, p. 137). | BrSEEA = PB + EB BrSEEA = OrSEEA − TC |

| Total cost | TC | Produced production factors of intermediate consumption (IC), labour cost (LC) and depreciation of durable capital (D) of ordinary produced fixed capital (D) used up in the accounting period by the government (ecosystem trustee) in the provision of the output (O) of threatened biodiversity. | It coincides with rSEEA. | TC = IC + LC + D |

| Class | Protected Areas (SPPAs) | Non-Protected Areas (SPNPAs) | Ratio | ||

|---|---|---|---|---|---|

| (ha) | (%) | (ha) | (%) | SPPAs/SPNPAs | |

| Pinus pinea without secondary species | 41,616 | 29.8 | 49,343 | 47.6 | 0.8 |

| Pinus pinea without tertiary species | 55,558 | 39.7 | 32,224 | 31.1 | 1.7 |

| Pinus pinea with tertiary species | 35,294 | 25.2 | 15,498 | 14.9 | 2.3 |

| Others | 7367 | 5.3 | 6657 | 6.4 | 1.1 |

| Total | 139,836 | 100.0 | 103,723 | 100.0 | 1.3 |

| Class | Publicly Owned (SPPAs) | Privately Owned (SPNPAs) | Stone Pine Forests (SPs) |

|---|---|---|---|

| Non-protected areas | 72,985 | 30,738 | 103,723 |

| Protected areas | 97,850 | 41,986 | 139,836 |

| Sites of Community Importance (SCI) | 43,261 | 24,565 | 67,827 |

| Protected landscape | 396 | 321 | 716 |

| Natural Site | 2408 | 685 | 3092 |

| National Park | 7185 | 1537 | 8722 |

| Natural Park | 42,178 | 14,828 | 57,006 |

| Concerted Natural Reserve | 115 | 0 | 115 |

| Protected zone | 1360 | 13 | 1373 |

| Buffer protected area of National Parks | 946 | 37 | 983 |

| Total | 170,835 | 72,724 | 243,559 |

| Class | Protected Areas | Non-Protected Areas | Ratio |

|---|---|---|---|

| SPPas (€/ha) | SPNPAs (€/ha) | SPPAs/SPNPAs | |

| 1. Output at social prices (O*) | 21.0 | 14.0 | 1.5 |

| 1.1 Additional consumer tax (ACT) | 8.8 | 8.1 | 1.1 |

| 1.2 Total cost (TC) | 12.2 | 5.9 | 2.1 |

| 2. Intermediate consumption (IC) | 3.4 | 1.8 | 1.9 |

| 2.1 Raw material (RM) | 0.1 | 0.0 | 4.0 |

| 2.2 Services (SS) | 3.3 | 1.8 | 1.8 |

| 3. Gross valued added (GVA) | 17.6 | 12.2 | 1.4 |

| 4. Depreciation of produced durable capital (D) | 1.5 | 0.6 | 2.6 |

| 5. Net valued added at social prices (NVA) | 16.1 | 11.6 | 1.4 |

| 5.1 Labour cost (LC) | 7.4 | 3.5 | 2.1 |

| 5.2 Benefit (B) | 8.8 | 8.1 | 1.1 |

| 5.2.1 Produced benefit of durable capital (PB) | 0.7 | 0.1 | 5.6 |

| 5.2.2 Environmental benefit of durable ecosystem asset (EB) | 8.0 | 8.0 | 1.0 |

| 6. Total cost (TC) | 12.2 | 5.9 | 2.1 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Campos, P.; Oviedo, J.L.; Álvarez, A.; Mesa, B. Measurement of the Threatened Biodiversity Existence Value Output: Application of the Refined System of Environmental-Economic Accounting in the Pinus pinea Forests of Andalusia, Spain. Land 2022, 11, 1119. https://doi.org/10.3390/land11071119

Campos P, Oviedo JL, Álvarez A, Mesa B. Measurement of the Threatened Biodiversity Existence Value Output: Application of the Refined System of Environmental-Economic Accounting in the Pinus pinea Forests of Andalusia, Spain. Land. 2022; 11(7):1119. https://doi.org/10.3390/land11071119

Chicago/Turabian StyleCampos, Pablo, José L. Oviedo, Alejandro Álvarez, and Bruno Mesa. 2022. "Measurement of the Threatened Biodiversity Existence Value Output: Application of the Refined System of Environmental-Economic Accounting in the Pinus pinea Forests of Andalusia, Spain" Land 11, no. 7: 1119. https://doi.org/10.3390/land11071119