1. Introduction

Intensification of smallholder agricultural production is generally considered a key strategy for supporting their competitive position in agri-food systems [

1]. Changes in cropping patterns, improvements of land use practices and investments in yield-enhancing inputs can provide positive returns to smallholders and, by resulting in large volumes, can improve their bargaining power vis-à-vis midstream actors, such as rural traders and processors. Large volumes allow farmers to spread-out the costs of accessing alternative markets and thus increases their outside options in bargaining with buyers. This is, however, not a zero sum game but may, in fact, lead to scale-economies and quality improvements that further reduce transaction costs and increase the value added potential for midstream actors too [

2]. Therefore, smallholder intensification in primary production can be supported by value added upgrading in the mid-stream segment of value chains and these can thus become mutually reinforcing processes. Technology adoption in agriculture has, however, remained strikingly low in many sub-Sahara Africa countries and therefore production systems are rather stagnant [

3]. Even while agricultural production in Africa slightly increased over the past decades, such progress is mainly attributed to land area expansion and mobilization of agricultural labour force and far less to increased use of yield-enhancing technologies [

4].

Most explanations in the literature relate to supply-side constraints, such as inadequate access by farmers to finance and high-quality farm inputs [

5,

6,

7,

8,

9]. Far less attention is given to the role of mid-stream value chain actors. This group includes a wide array of rural collectors, traders, truck drivers, shipping agents, warehouses, moneylenders and banks, and standard control agents. These mid-stream agents interact with farmers through spot exchange [

10,

11] but also through contractual exchange systems where farmers receive input support (seeds, fertilizers, equipment) and engage in delivery arrangements against pre-arranged prices [

12].

High risks, uncertainties, and the inability to meet quality standards in primary production result in supply shortages for midstream agribusinesses involved in bulking, storage, processing and trade. Since consumer food demand continues to increase due to high growth in population and consumer income, the use of sustainable modern technologies for raising agricultural productivity become indispensable, also for these mid-stream actors.

Mid-stream agents can affect smallholder intensification through a number of channels [

13]. The first is by providing farmers access to (higher value) markets as higher productivity (in terms of higher yields or higher revenue per hectare) can result from incentives to invest related to quality standards set by mid-stream agents. Second, prices paid by the mid-stream segment impact agricultural productivity directly (in terms of revenue per hectare or per hour worked) and indirectly, by providing an incentive to adopt yield-enhancing technologies. As a second-order effect, enhanced farm revenue may, in turn, provide farmers with increased access to finance to make productivity-enhancing investments. A final channel is through institutional innovations within the value chain introduced by lead firms that can enhance farms’ access to productivity-enhancing technology.

The empirical literature studying this predominantly looks at the farm-level effects of participating in certain

types of value chains, such as value chains for urban supermarket chains [

14] and export agencies or value chains governed by contractual relationships [

15] and other forms of value chain governance [

16]. This literature uses farm-level micro-data to better understand the effect of the mid-stream and downstream parts of the value chain on farm-level income, productivity, and wellbeing.

Most pathways towards agricultural intensification focus on incentives for improving farmers’ access to knowledge and resources [

17] and look at the effectiveness of the delivery mechanisms towards smallholder farmers. A comprehensive overview of different types of incentives shows that risks and credit constraints mostly limit technology adoption in developing countries [

18]. Few studies have analysed incentives implemented through value chains integration and the role of inclusive value-chain development [

16,

19]. Linkages between producers and midstream actors are helpful to reduce risks and uncertainties regarding sales volume, quality and prices. Overcoming these constraints is increasingly important as a driver for adoption of improved production practices and technologies.

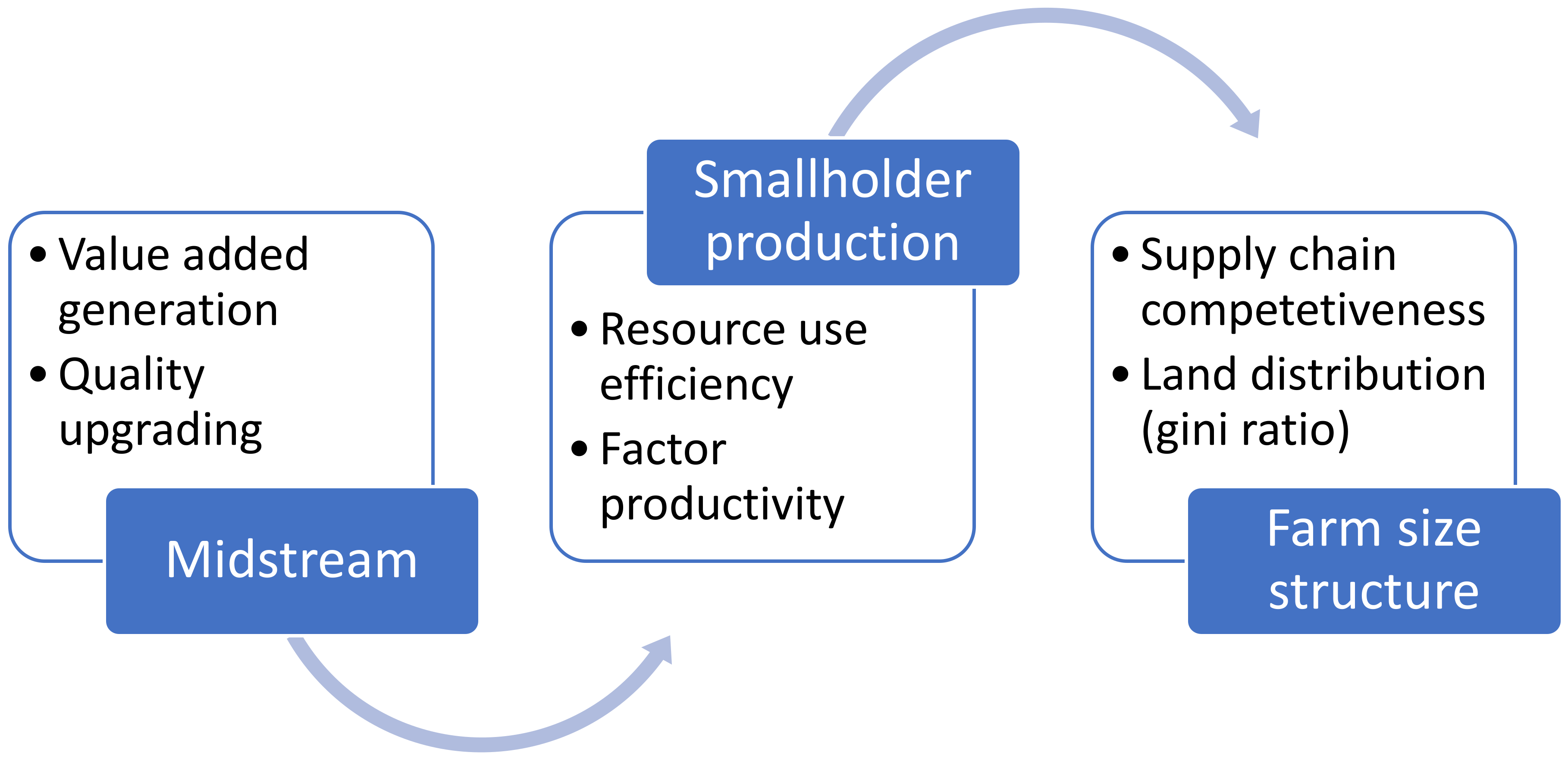

This article offers a new meso-level analytical framework for studying the linkages between the midstream value chain and the primary agri-food production sector. It draws on comparative data from six different agri-food value chains in sub-Saharan Africa (SSA) to study the structural relationship between smallholder farmers production and value addition in the midstream segment. The amount of value addition taking place in the midstream is an indication for its strength, either in terms of its ability to add value or the capacity to bargain for a larger surplus vis-à-vis farmers and retailers. The analysis relies on a detailed reconstruction of the cost and revenue structure along different stages of the value chain that is subsequently used to assess sector-wide effects on factor intensity and farm-size structure at primary production.

Our analysis aims to better understand the role and importance of midstream agents in the value added generation throughout the agricultural supply chain, its impact on smallholder’s resource use and investment decisions and the implications thereof for farm size competitiveness in the supply chain (see

Figure 1). We show how strength in the midstream trade and processing activities is closely related to farm-level changes in capital and labour use, and influences the farm size structure for commercially-oriented smallholder production.

The remainder of this article is structured as follows.

Section 2 outlines the analytical framework for assessing interactions between primary production and midstream value chain operations.

Section 3 presents the data and discusses the methods for comparative data analysis. In

Section 3 the empirical results are presented, followed in

Section 4 by a discussion on the policy implications and the prospects for further research on the role of production-midstream linkages for agricultural and rural development.

2. Materials and Methods

This study relies on empirical field data generated by the Value Chains Analysis for Development (VCA4D) project, funded by the European Union/DEVCO and executed through the Agrinatura network. It uses a data collection and analysis approach that carefully separates between value added generation in primary production and in midstream activities. Therefore, a functional analysis is made of the product flows and transformation processes throughout the value chain and of the actors involved in these activities. Hereafter, the economic performance of each of the actors involved in the value chain activities is reconstructed, using field survey data from a selected sample of each of the actors. In addition, social conditions and environmental effects (using a life cycle approach) are assessed with interviews and case studies. This paper relies only on the value added data from the economic analysis.

The purpose of VCA4D program is to provide evidence-based information for assessing inclusive and sustainable agricultural development strategies. The analysis is directed to policymakers and business stakeholders to support a constructive policy dialogue on the opportunities and constraints for value chain upgrading. Comparing different agricultural VCs is considered helpful to uncover major development pathways, and to identify at which stages of the value chain and for which actors opportunities for investment and technical support can generate tangible economic benefits, and how specific strategies can be designed to foster VC sustainability and inclusiveness.

2.1. Value Added Composition

The VCA4D program analyses agricultural value chains according to the sequence of production processes from the primary production to its end uses. It considers a sequence of different types of actors involved in the production and exchange of commodities orientated towards the final market. Major actors are input providers (for seed and fertilizers), farmers, traders and collectors, transporters, processors, wholesalers (including storage) and retailers. In addition, there are several public and private agencies involved to control on quality and safety standards, collecting taxes and to maintain lawful exchange relationships.

The VCA4D program uses a stylized methodological framework to assess the structure and performance of VCs from an economic, social and environmental perspective. This includes a functional analysis that identifies the different stakeholders involved in agricultural VC, followed by a technical diagnosis of the activities performed at different stages and an analysis of the underlying governance and power structures. Finally, the composition of the production value and the value added created at different stages of the VC is reconstructed to enable a further assessment of resource use intensity, labour productivity, capital intensity and profitability.

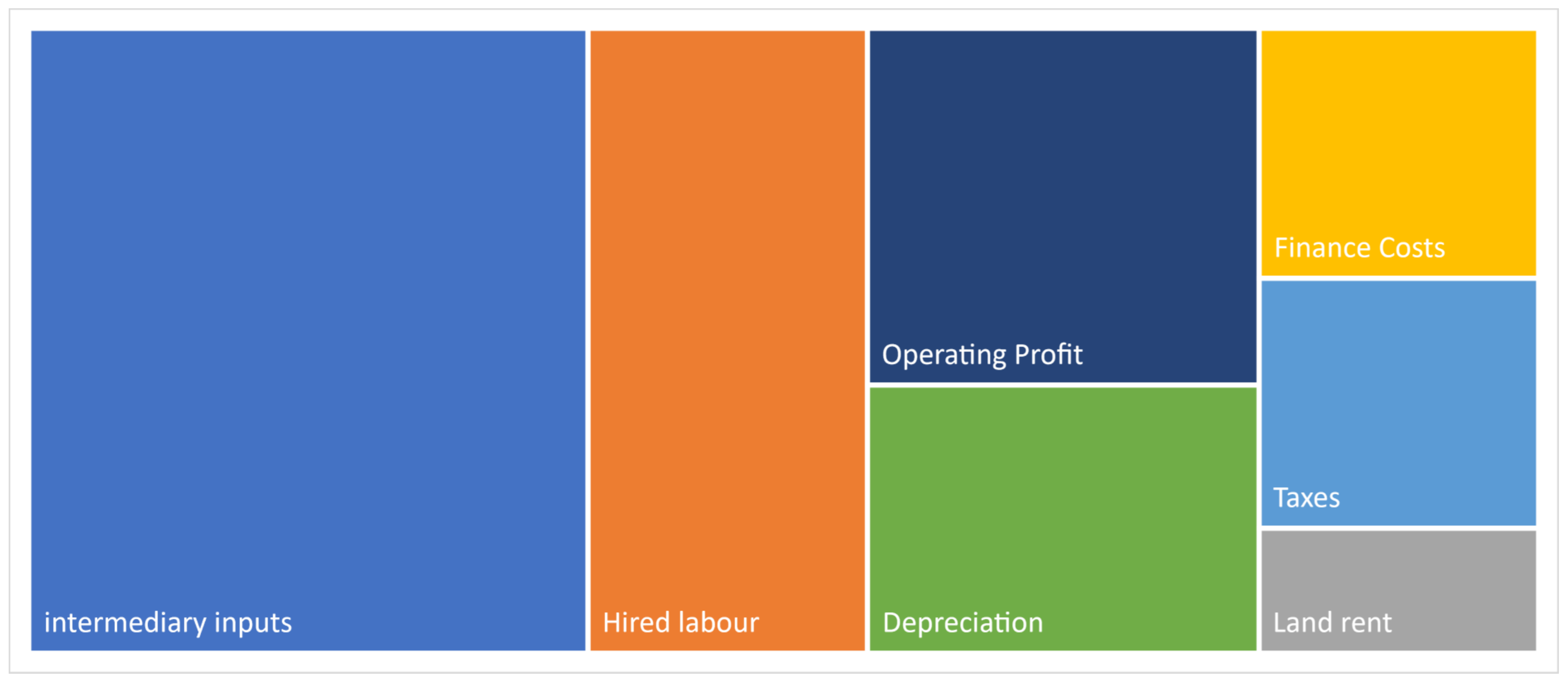

Figure 2 illustrates how the value that is realized in primary production and subsequently in midstream operations is decomposed into the costs of purchased intermediary inputs (such as seeds and fertilizers in agricultural production, and the raw materials purchased as inputs for the food industry) and a number of additional inputs, ranging from land (rent), labour (wages), finance (interest paid for credit), depreciation (degradation of the stock of capital resources) and taxes, subsidies and fees (paid to/by the government) to generate a gross market value. What remains after compensating for the costs of these inputs is an operating profit that compensates for the business initiative and covers the entrepreneurial risk.

The decomposition of the value added by stages of the value chain (between primary production and midstream activities) permits to identify the stage of development and the degree of vertical integration of agri-food production. Moreover, the shares of intermediary inputs, labour costs and capital depreciation compared to total value added offer insight into the relative factor intensity of production and midstream activities. Finally, the comparison between operational profit with total value added creation illustrates the profitability of activities.

The decomposition of the value added permits the calculation of several performance indicators. The proportional shares of value added creation and employment generation are divided between primary production and midstream activities. Capital intensity is defined as the ratio between depreciation costs and total value added, whereas input intensity is the ratio between intermediary inputs and total value added. Profitability refers to the operating profit as a share of value added. These intensity indicators are calculated separately for primary production and midstream activities. The Gini ratio of primary production reflects the cumulative proportion of the population of farmers against the cumulative proportion of the value added that they generate. It ranges between 0 in the case of perfect equality and 1 in the case of perfect inequality.

2.2. Value Chain Configurations

We selected from the VCA4D portfolio six studies that cover different categories of production systems and value chains, focussing on cases from the sub-Sahara region in order to control for major variation from contextual sources. This explorative analysis of primary production and midstream operations is useful for developing some hypothesis about the potential effects of value added distribution on the factor intensity of production systems and the composition of the firm structure. This enables a comparison of the importance of some ‘typical’ midstream value chain configurations for different categories of products (see

Table 1):

Commodities: cotton in Ethiopia [

20] and cocoa in Cameroon [

21]

Commercial crops: green beans in Kenya [

22] and sorghum in Ghana [

23]

Staple Foods: maize in Nigeria [

24] and groundnut in Ghana [

25]

Table 1.

Primary production and value chain characteristics.

Table 1.

Primary production and value chain characteristics.

| Commodity | Country | Farm Type | Production

Systems | Marketing

Systems | Labour Use |

|---|

| Cotton | Ethiopia | Small, medium and large farms | Rainfed/conventional | Cooperatives and Contracts | Family labour and temporary contract labour |

| Cocoa | Cameroon | Small-scale producers | Input intensive | Producers groups and regional confederations | Family labour |

| Green beans | Kenya | Small-scale (with self-help groups) | Greenhouse | Contract farming for exports | Family and hired labour (permanent) |

| Sorghum | Ghana | Small-scale commercial farmers | Semi-technified; input-credit by large aggregators | Customary deliveries to aggregators and processors | Family labour and seasonal hired labour |

| Maize | Nigeria | Commercial smallholders | External-input technology | Contracts with aggregators (regional sales to urban centres and for livestock feed) | Family labour complemented by wage labour |

| Groundnut | Ghana | Small-scale producers | Labour-intensive production | Input-output contracts | Family and hired labour (planting and harvesting) |

Table 1 provides an overview of the production conditions and the commercial regimes for each of these crop/market combinations. They show clear differences in farm organization (small-scale to family farmers) and production technologies (traditional to semi-technified) accompanied by a diversity in labour arrangements (family, hired, contract) and a large variation in market outlets (custom, contract, auction).

Classical commodities cotton and cocoa are produced by a large number smallholders in countries under fairly strict control by the government (Ethiopia) or by multinational firms (Cameroon). Commercial crops like green beans (Kenya) and sorghum (Ghana) are procured by processing firms and sold on global and local markets. Traditional staple foods such as maize (Nigeria) and groundnut (Ghana) involve many low-input smallholders that deliver to their produce to artisanal processors for local and regional sales.

2.3. Brief Characterization of Selected Value Chains

Cotton in Ethiopia: production is divided between 7000 traditional and 19,000 semi-modernized family farms, and a few very large commercial farms that use irrigation and modern inputs and control 2/3 of the land and value added. The traditional cotton sector generates 60,000 self-employed jobs, whereas in the modern sector 40,000 jobs are created. Local spinning and traditional weaving are gradually replaced by industrial ginneries and spinning mills, as well as several medium- and large size oil processing mills. The development of cotton is promoted by government to substitute imports and eventually to promote exports, but high production costs and low value chain efficiency remain important constraints.

Cocoa in Cameroon: mixed production structure dominated by 200,000 smallholders producing 70% of output that is sold at local spot-markets alongside 90,000 family farmers producing the remainder under contract conditions. Production involves some 100,000 seasonal workers. Aggregation is divided between 1500 local intermediaries and organized cooperatives that control 40% of production, of which 1/3 is certified. There are 3 local processing plants that buy 22% of production (processed into butter and paste) and 6 large multinationals that control major share of exports. Main profits are realized by export traders, while cocoa value chain also remains important for fiscal levies.

Green beans in Kenya: involves primary production by some 20,000 scattered smallholders delivering on spot markets and 32,000 mid-size family farmers delivering green beans on contract, alongside some 60 large farms that control 45% of market deliveries. This bimodal production structure is linked to a marketing structure where a few packhouses and canning factories control 90% of all processing and sales. Half of the production is exported as fresh or canned beans, whereas 40% is rejected and remains for domestic consumption and 10% is lost and used for animal feed and compost.

Sorghum in Ghana: some 175,000 low-input smallholders and 47,000 more technically advanced smallholders are responsible for 98% of all sorghum production. One-third of output is locally consumed and post-harvest losses are 12%. From the marketed surplus, 80% is used by local micro-brewers and 15% by industrial brewers. This smallholder-dominated production structure is linked to a rather decentralized midstream trader and processor organization with low entry costs and very lucrative margins.

Groundnut in Ghana: primary production is dominated by 375,000 family farmers that produce about 90% of output, complemented by some 28,500 small- and midsize producers that deliver the remainder under contracts with buyers. Market orientation is diversified, including informal and formal aggregators and a whole range of different processors (i.e., paste, flour, kulikuli, snacks). The groundnut value chain offers employment to some 440,000 self-employed and 350,000 wage workers, but wages are far below living income standards. Women play a key role in production, trade and processing. The informal value chain with a large number of SMEs accounts for 88% of all processing activities.

Maize in Nigeria: half of the maize is produced by more than 2.5 million local smallholders and the other half is divided between some 350,000 more commercially oriented small- and midsize farms and a few (very) large farms. Employment in maize sector is estimated at 23 million jobs (mainly self-employment), of which 10% in midstream activities. The maize market is divided between informal and formal segments: most smallholder maize is used for milling and consumed locally, whereas midsize and large farms supply maize to larger (peri-)urban markets in the South. Margins in production and processing are attractive, but trade margins are thin due to strong competition.

Table 2 presents an overview of the main characteristics of each of the value chains with respect to input intensity, market orientation, scale of operations and value chain organization.

There is considerable variation in the configuration of midstream sector structures. Production of commodities such as cotton (Ethiopia) and cocoa (Cameroon) is still fairly extensive and involves limited prospects for value added creation. Commercial crops oriented towards local processing for regional and export markets (green beans in Kenya; sorghum in Ghana) rely on more intensive technologies, mainly to safeguard quality and freshness. On the other hand, production and processing activities in food staples (maize in Nigeria, groundnut in Ghana) oriented towards local and national markets are usually characterized by low or mediocre resource-intensity. For almost all products, firms engaged in midstream value chains include both small-scale self-employment enterprises as well as more formal SMEs. These businesses mostly co-exist (mixed) or are mutually connected (differentiated), but in some countries, this is controlled by government regulation (Ethiopia) or contracts (Kenya; Cameroon).

2.4. Archetypes of Production—Market VC Linkages

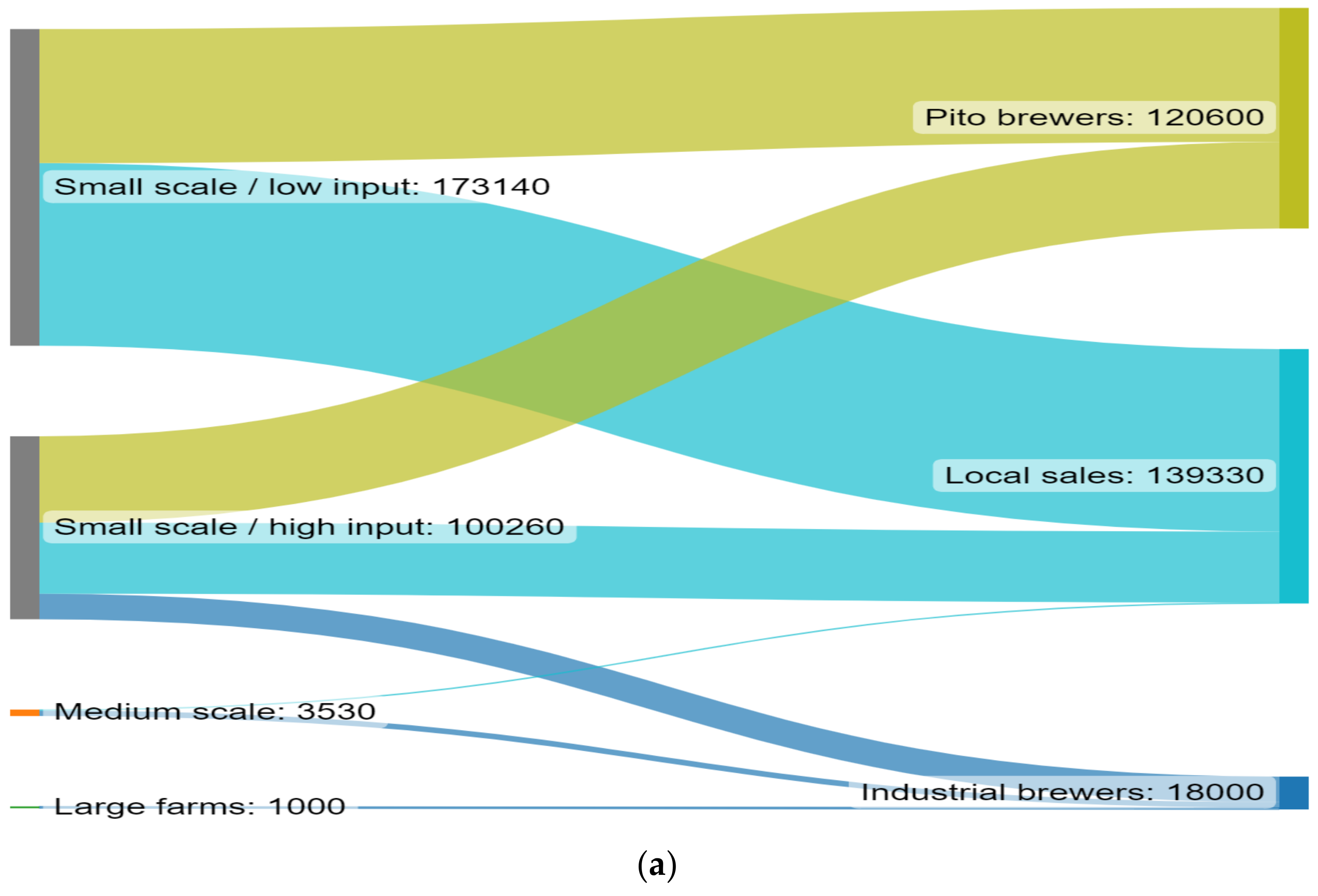

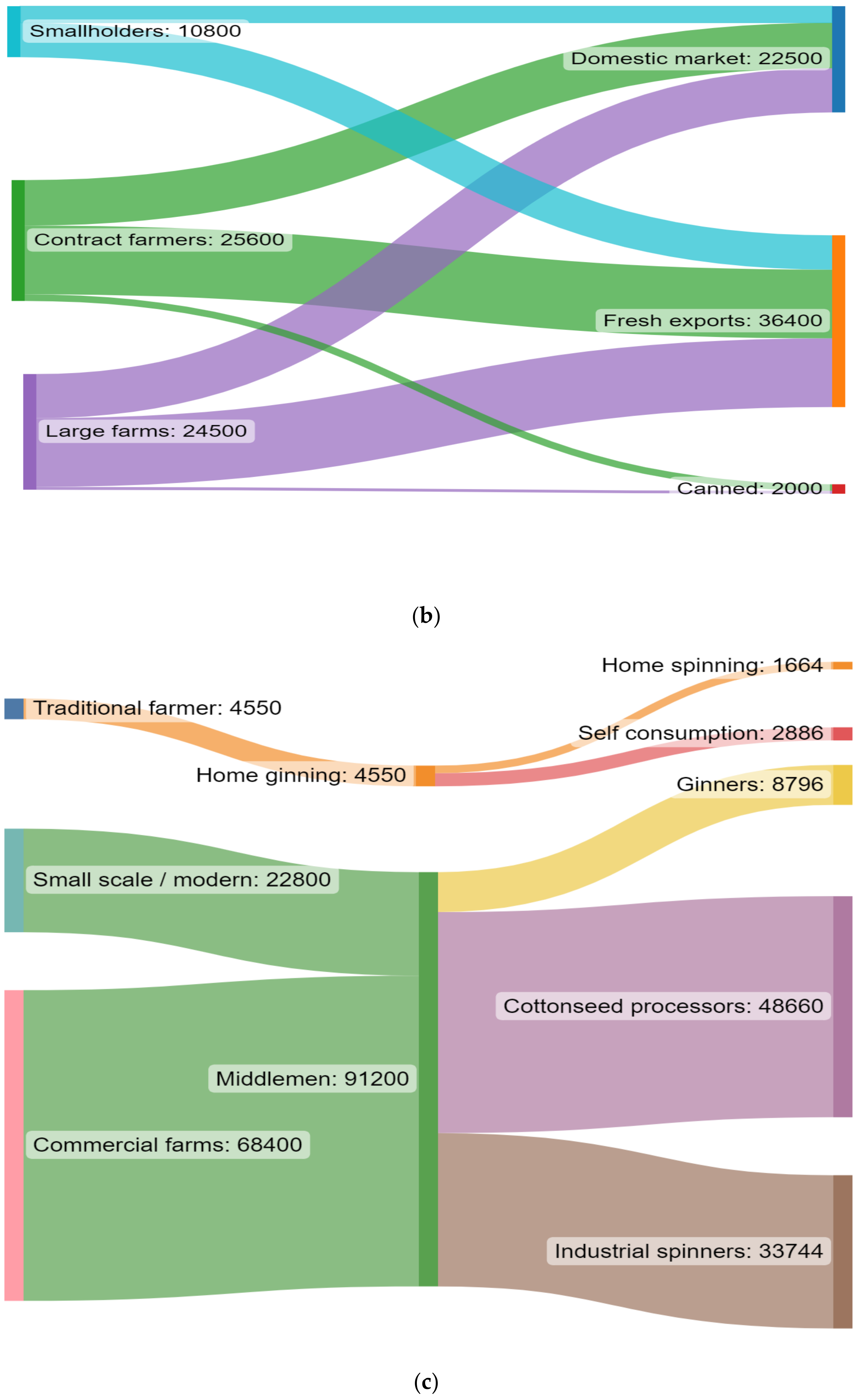

The commodity flows between primary producers and midstream agents can be illustrated with Sankey diagrams that show the origin and destination of products]. Three typical archetypes of VC can be distinguished (see

Figure 3a–c):

The sorghum value chain (Ghana) connects a large number of scattered smallholder producers with highly decentralized artisan pita brewers (processors) and local markets (direct sales to consumers). Average traded volumes are limited and competition is strong (due to low entry costs), leading to relatively small margins for traders. A small number of industrial brewers organize their sourcing from medium-scale and large farms, but also purchase from small-scale producers.

In the green beans value chain in Kenya, smallholders working with and without delivery contracts deliver products to a few packhouses and canning factories. Half of the production is exported as fresh or canned/frozen beans, whereas the other half is for domestic consumption, animal feed and compost. A few large farms control 45% of market supply and are mainly export-oriented (of fresh, canned and frozen beans), but their sub-standard products are sold locally.

The cotton sector in Ethiopia is dominated by a few large commercial farms that are linked through selected middlemen with a cluster of industrial spinners and cottonseed processors. Small traditional cotton farmers are linked only to local outlets. These two market segments coexist but hardly interact, mainly due to large differences in scale of operations, quality norms and investment requirement.

3. Results

In this section, we present an overview of the comparative performance of the six agri-food VCs and the implications of differences in midstream organization for primary production systems. First, we look at the structure of primary production and the smallholder contribution to the production value and the marketable surplus. Second, we assess the linkages between primary production and midstream VCs, especially looking at the importance for the creation of (wage) employment and the generation of value added. Third, we analyse the impact of midstream development (in terms of value added share) on the primary production structure and the implicit incentives for factor use intensification.

3.1. Structure of Primary Production

Smallholders play a dominant role in many agricultural production systems. They have a comparative advantage for more labour intensive crops [

26], because they can mobilize flexible amounts of (family) labour for seasonal operations (land preparation, harvesting). Medium-scale farms are becoming more important for input-intensive production systems with higher quality standards. Large scale farms appear when economies of scale and scope arise.

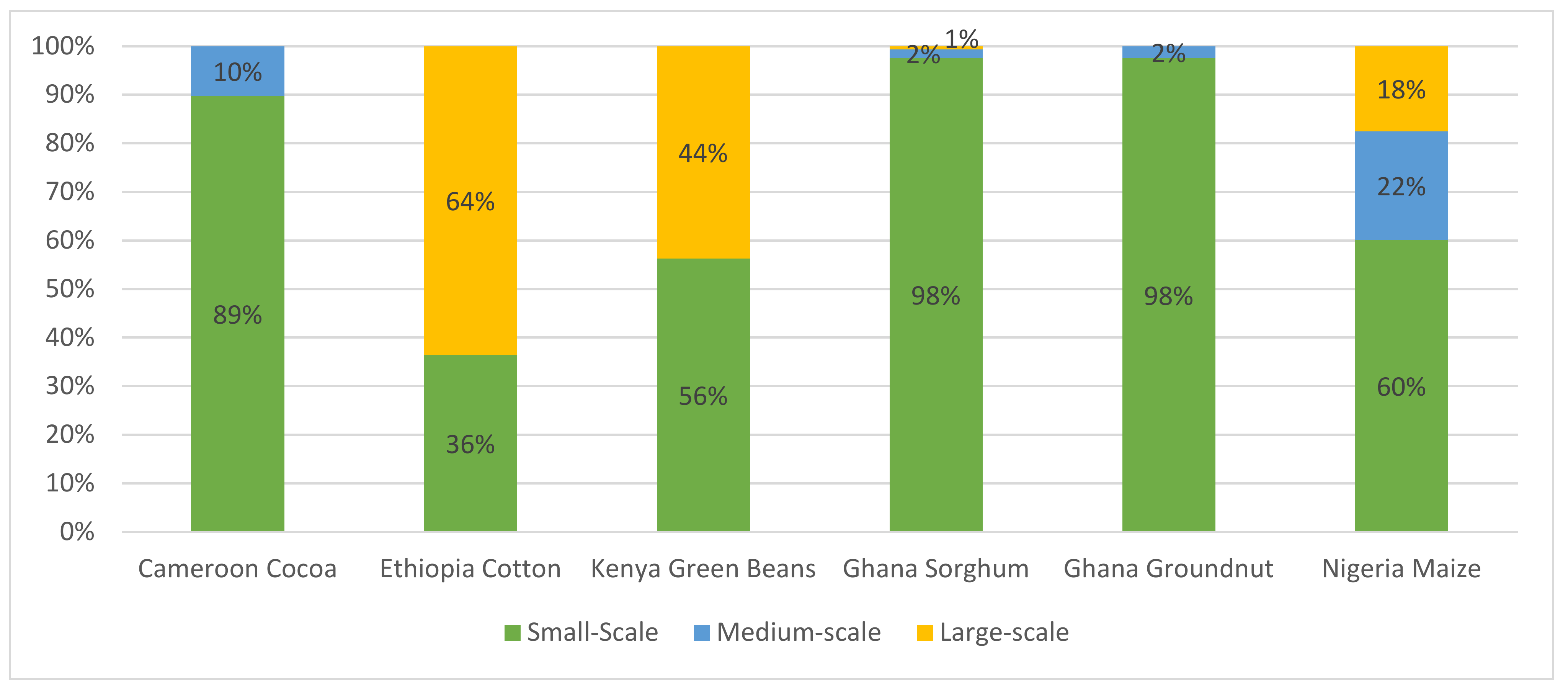

Figure 4 shows important differences in the farm size structure between the six value chains [

27]. We define small-scale as between 0 and 3 hectares, medium-scale as between 3 and 20 hectares, and large scale as above 20 hectares. However, within each size-category there is considerable variation in average farm size. The average “large-scale farm” in the cocoa sector of Cameroon has 25 hectares, for example, while the average “large-scale” farm in the cotton sector of Ethiopia has over 400 hectares. In countries like Ghana (sorghum and groundnut) and Cameroon (cocoa), smallholder farmers contribute 90% or more to the total value of production, whereas in Kenya (green beans) and in Ethiopia (cotton) large farmers are particularly important for the generation of marketable surplus. This confirms the trend that smallholders maintain a comparative advantage in staple production for local outlets linked to consumer markets (sorghum and groundnut in Ghana) or for direct processing (cocoa in Cameroon), whereas midsize and large firms become more important for food deliveries to urban conglomerates (maize in Nigeria), semi-industrial processors for national markets (cotton in Ethiopia) or export markets (green beans in Kenya).

The intensive linkages between producers and processors through procurement contracts (green beans in Kenya) or other delivery arrangements (cotton in Ethiopia) create space for larger companies that are better able to guarantee continuous deliveries and standard quality norms. For cocoa (Cameroon) deliveries of raw material is still mainly dominated by smallholders that rely on fairly traditional production systems. Their production is committed to traditional small-scale local processors through input delivery contracts (seedlings, fertilizers) and pre-finance arrangements.

These differences in the structure of primary production are reflected in the prices received by different farm sizes. Larger farms receive up to a 40% higher farm-gate price compared to medium size farms, and this rises to 75% higher prices compared to those paid to smallholder producers. This implies that differences in production size are translated into even higher discrepancies in value added distribution between small and large producers.

3.2. Importance of Midstream VC

Whereas primary agricultural production has been traditionally responsible for a major share of rural (self- and wage-)employment and value added, the importance of midstream enterprises is gradually increasing and some agri-food VCs are becoming more oriented towards employment creation and value added generation in downstream segments [

28]

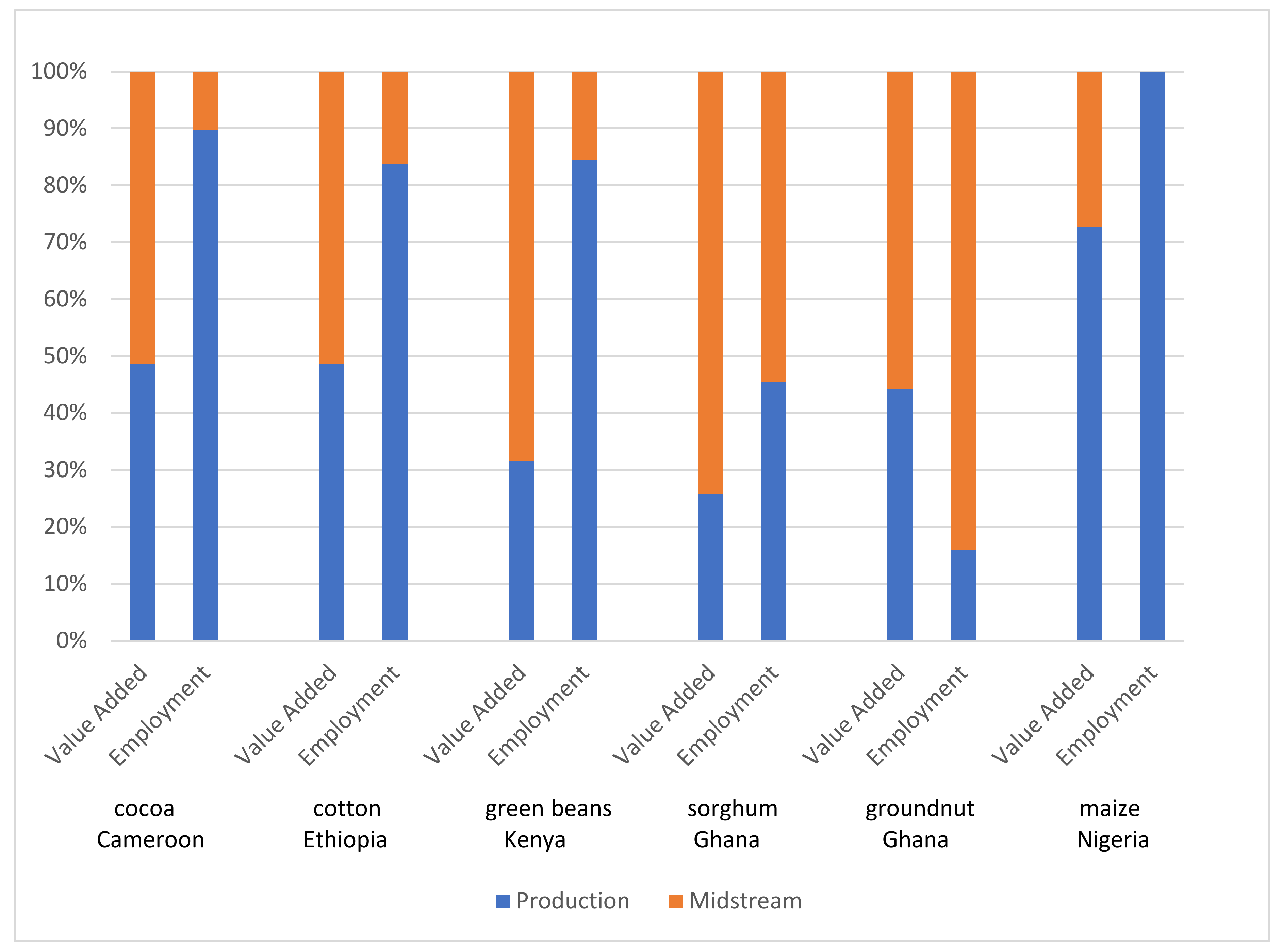

1. We present the value added and employment structure of the six VCs (

Figure 5) and distinguish three different structural patterns: (a) VCs where employment and value added are dominated by midstream agents (groundnut and sorghum in Ghana), (b) VCs where primary production still dominates employment and value added (maize in Nigeria, and—to a minor extent—cotton in Ethiopia) and (c) mixed or bi-modal VCs (green beans in Kenya, cocoa in Cameroon) where the midstream controls a major share of value added but primary producers still dominates employment generation.

Figure 3a–c show the structure of material commodity flows between primary producers and midstream agents illustrated with Sankey diagrams that characterize the origin and destination of products.

The importance of midstream activities is usually larger in value added creation than in employment generation, with the sole exception of groundnut (Ghana) that relies on very labour-intensive and informal local processing. Production systems with many smallholders (maize in Nigeria, cocoa in Cameroon and cotton in Ethiopia) keep a large share of employment in primary production. Rising opportunities for downstream value added creation (such as for sorghum in Ghana and green beans in Kenya) give room for a market-oriented transition in VCs where midstream value added shares rise faster than the midstream employment share. Sorghum and groundnut (both in Ghana) show an opposite pattern of midstream expansion, with a higher value added share in sorghum VCs compared to a higher employment share in groundnut VCs. This is mainly related to the larger local processing options in sorghum and the very extensive character of groundnut cultivation that leaves little room for employment creation.

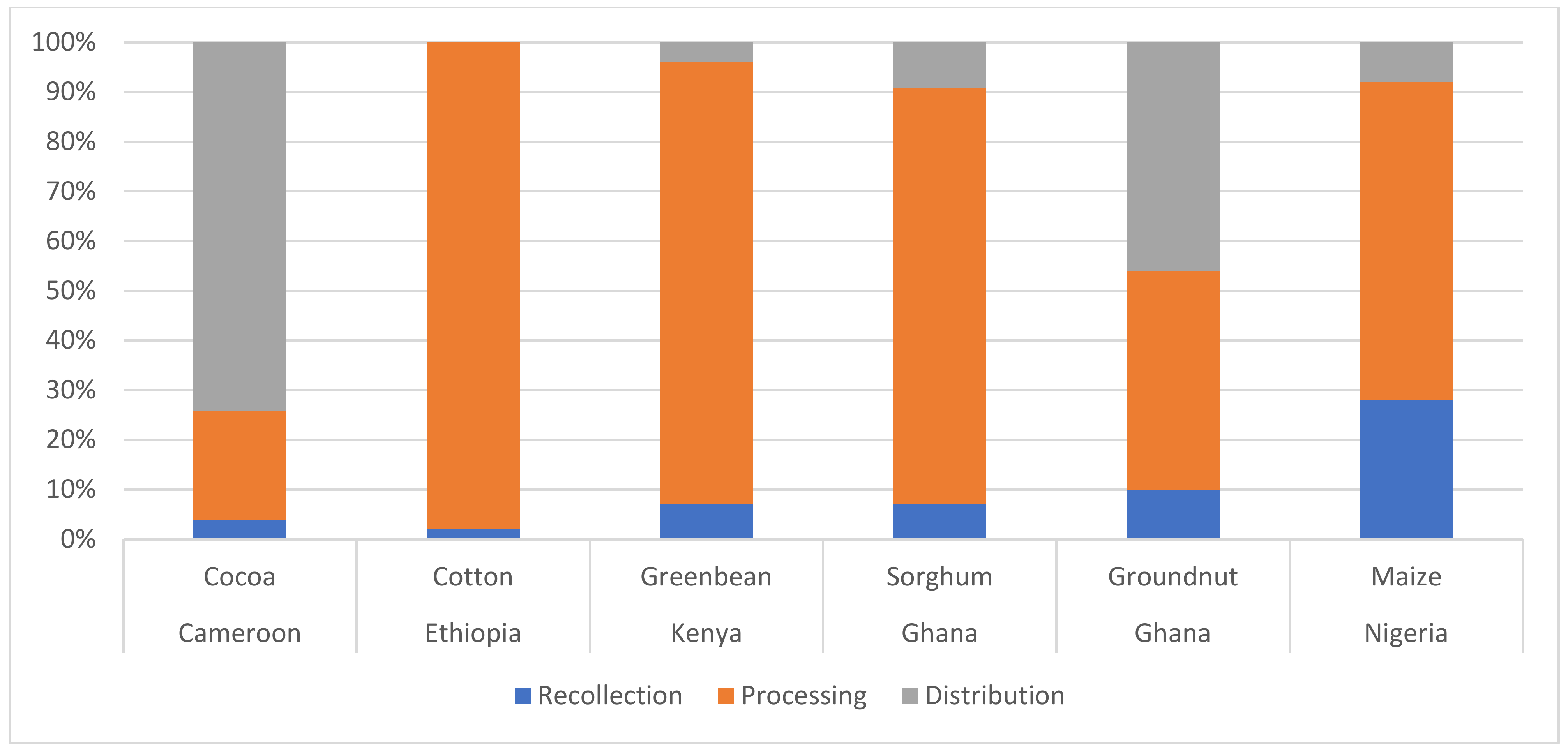

The structure of value added distribution within midstream operations is also quite different (see

Figure 6). In the food staple VCs (maize, groundnut and—to a minor extent—sorghum) the recollection of the produce at farm gate and its storage and transport to local markets still represents 15–30% of value added. There is a dominant role of processing activities in value added creation for VCs of cotton (Ethiopia), green beans (Kenya) and sorghum for beer brewing (Ghana). In groundnut and cocoa VCs, a relatively high share of value added share remains with wholesale traders and distribution agents that are responsible for linking local producers and processors to larger wholesale traders and exporters.

3.3. Relationships between the Midstream Value Chain and Smallholder Production Systems

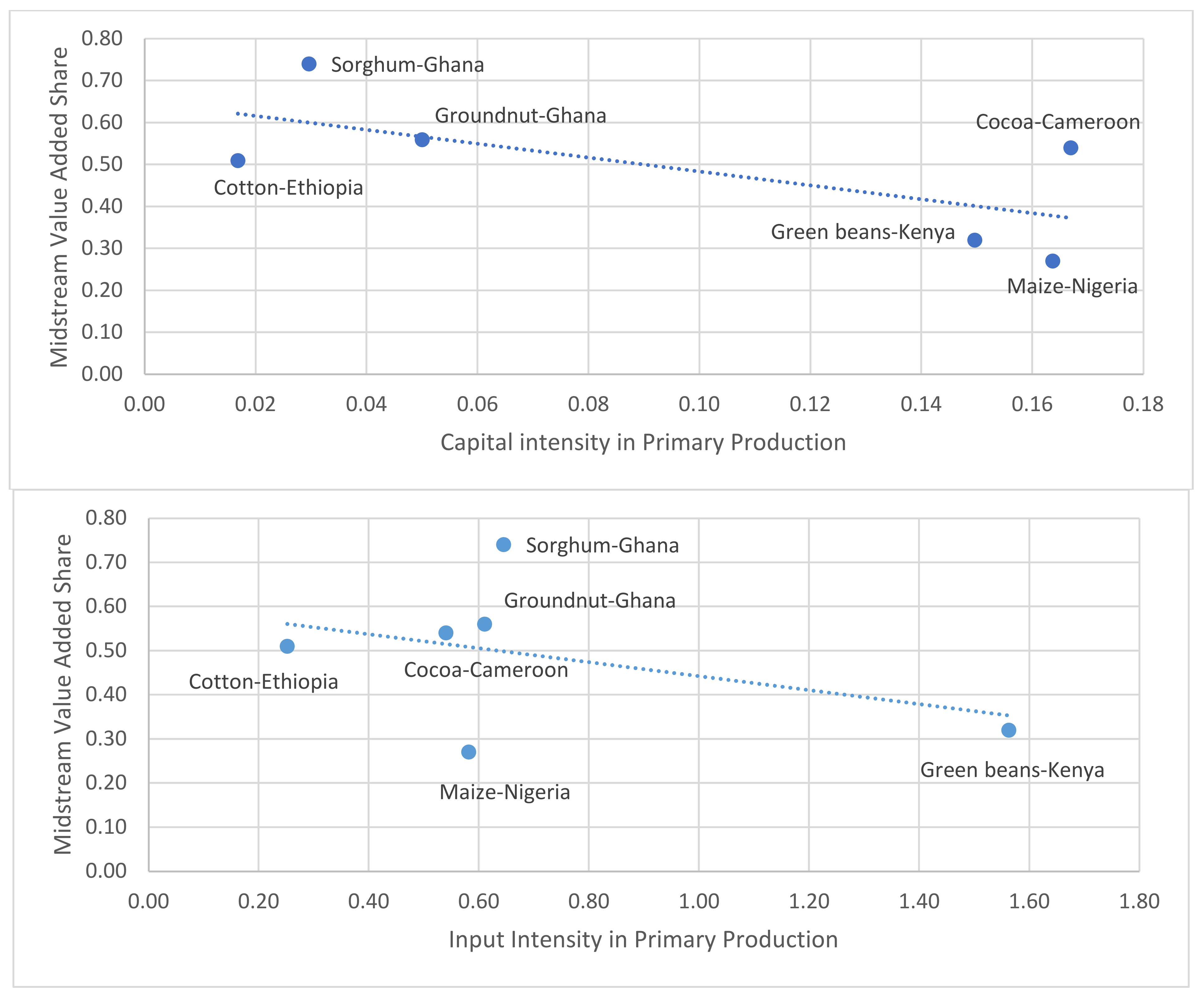

Growing importance of midstream agents in the generation of value added may create (dis)incentives for smallholder investments in production system intensification, as discussed in the introduction. Both input intensity (use of intermediate inputs) as well as capital intensity (depreciation of capital stocks) in primary production are negatively associated with the value added share captured by midstream agents and, thus, positively associated with the value added share captured by primary production (see

Figure 7). This is particularly the case for more intensive primary production systems of green beans (Kenya) and cocoa (Cameroon) that require large amounts of inputs and capital which translate into a lower value added share that can be realized in midstream operations. On the other hand, more extensive cropping systems in crops like sorghum and groundnut (Ghana) and cotton (Ethiopia) tend to lose a larger share of value added to competitive midstream agents.

This can also be explained by mechanisms that run in opposite direction but are, in fact, mutually reinforcing. Input and capital might increase production volumes and production quality. Higher quality in itself is a way to increase value addition, but higher volumes and higher quality can also increase the access to remunerative markets and improve the farm sector’s bargaining position, leading to a larger value added share vis-à-vis the midstream. The causal mechanism might also run in the opposite direction: a lower value-added share in the midstream sector might be an indication for weaker bargaining power and might provide an incentive for farmers to invest in production because they are able to retain a large portion of the surplus generated.

The interaction between factor intensity and value added distribution at different levels of the VC provides important opportunities for the design of appropriate strategies towards smallholder intensification. Constraints of input and capital intensity in primary production are easily translated into deficiencies in midstream VC competitiveness. Otherwise, investments in input use and capital at the level of primary production improve competitiveness with midstream operations and enable smallholder farmers to retain a larger share of value added.

Factor intensity not only depends on particular crop requirement, but is also related to the external production environment [

27]. Countries with a higher degree of urbanization (Ghana, Cameroon), with more infrastructure facilities (Ghana, Kenya) and a better business climate (Nigeria, Ethiopia) enable midstream agents to capture a large value added share.

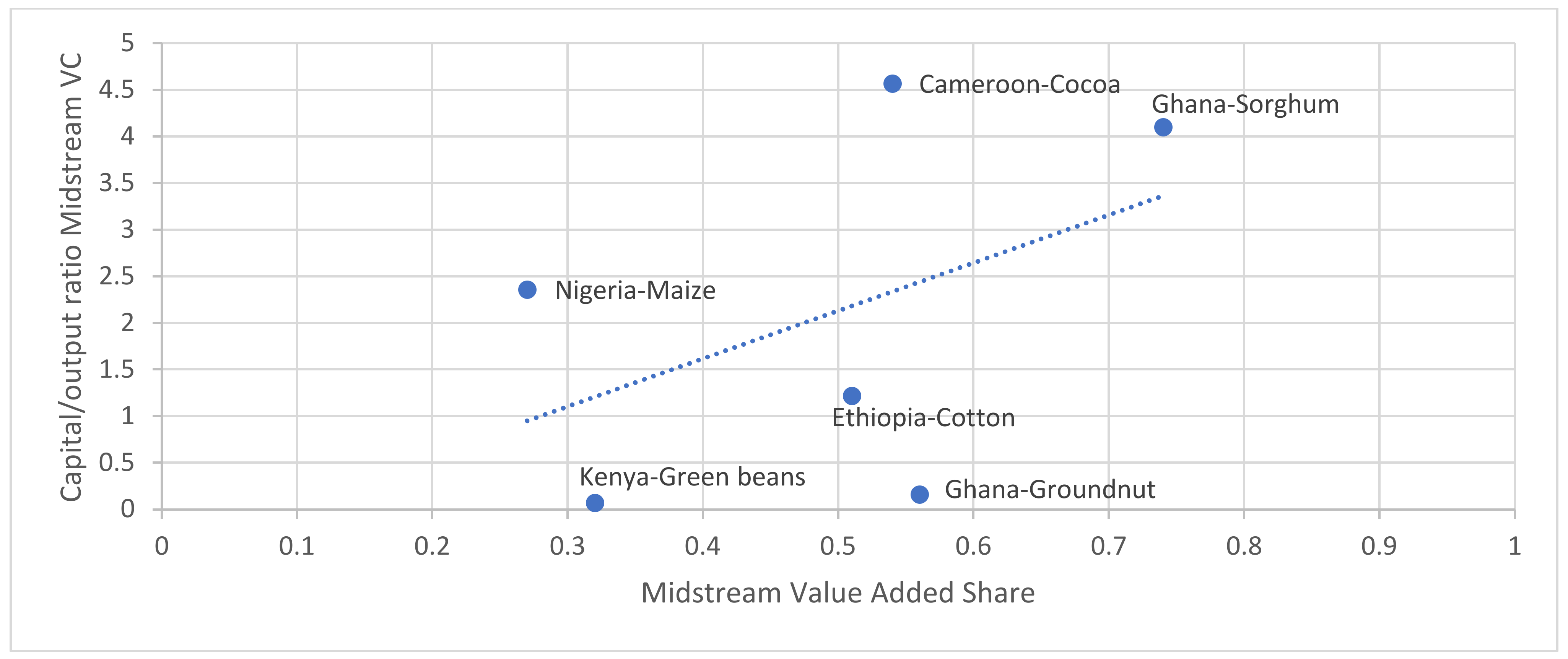

Additionally, value chains that require large investments of capital resources (compared to their output value) in midstream operations show to be able to capture a substantially larger midstream value-added shares (see

Figure 8) as a compensation for these efforts. Products that require more investments for direct local processing (cocoa in Cameroon and sorghum in Ghana) are able to realize a larger VA share in midstream activities, while commodities with simple processing requirements (green beans in Kenya) receive a lower VA share for midstream activities. This can, again, be explained by mechanisms that run in both causal directions and that are mutually reinforcing: (1) the application of capital has a positive effect on quality and volumes, leading to more bargaining power and a higher value-added share; and/or (2) a higher value added share is related to higher bargaining power, which provides an incentive for investing more capital.

In summary, we notice that smallholder producers involved in VCs with a high midstream value added share are less inclined to invest inputs and capital resources in the primary production stage. However, intensification of primary production may be considered as a relevant strategy to counteract the unrestricted value added capture by midstream agents.

3.4. Midstream Value Chains and Farm Size Structure

The relative importance of primary production by farmers and midstream activities undertaken by trading and processing firms is reflected in the value added shares realized in each of these VC stages. This also reflects the relative bargaining power of farm vs. firm operations that shape market exchange conditions. Smallholder farmers will be better able to engage in intensification of their production processes if they can reap the benefits of their investment. Otherwise, large VA shares for primary producers can be realized in markets where contractual delivery arrangements prevail (green beans in Kenya and cocoa in Cameroon). In both cases, market competition is based on quality compliance and therefore producers receive price incentives. Consequently, opportunities for maintaining smallholder farming systems are closely linked to the trade and investment opportunities provided by midstream stakeholders.

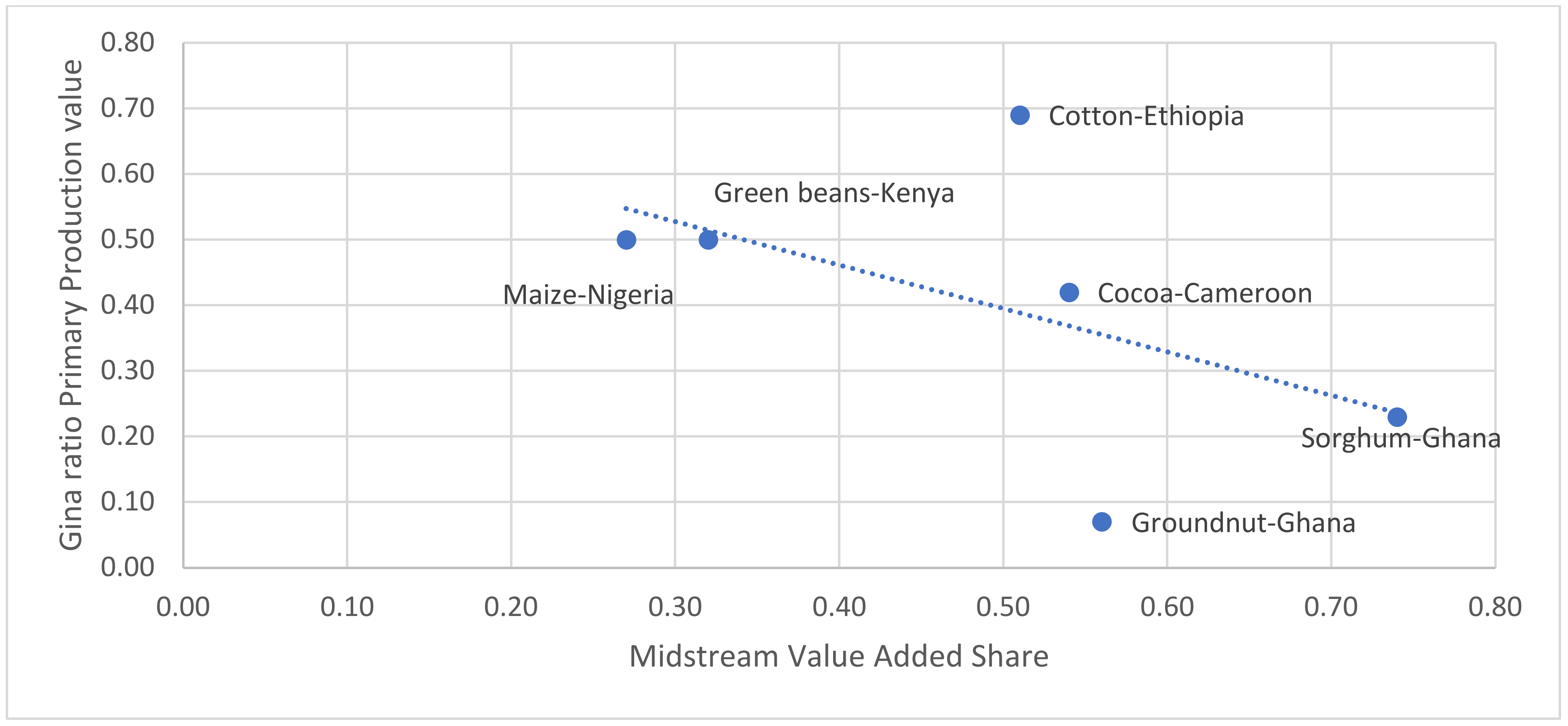

Figure 9 shows the relationship between the importance of midstream firms (expressed as the share of total value added) with the farm size structure (using the Gini ratio as indicator for relative inequality of the production value amongst farms) [

27]. A larger value added share generated outside primary production is associated with a more balanced farm size distribution (Gini < 0.3) and a growing space for family and midsize farms. This is likely to be based on more standardized primary production systems with easy entry that focus on high volume and rapid turnover in midstream operations. When the role of midstream agents in value added production becomes smaller, smallholder farming remains dominant but farm size inequality tends to become higher (Gini > 0.5). This may be due to higher quality requirements that ask for careful attention in primary production.

We can now look at the implications of the before-outlined differences in primary production systems and their linkages to midstream operations for the farm size structure. As expected, we find higher farm size inequality in more commercially oriented commodities with strong bimodal VCs, such as in Ethiopia (cotton) and Kenya (green beans). The high Gini ratio for maize in Nigeria is explained by the important segment of midsize and large farms that are responsible for supplying maize at scale for large (peri-)urban markets in other regions. On the other hand, food staple crops (sorghum and groundnut) in Ghana maintain a more balanced farm size distribution since their output is usually sold through a large number of midstream traders at nearby local or sub-regional markets. Cocoa production (Cameroon) is an intermediary case where post-harvest midstream operations are particularly important for guaranteeing quality through adequate drying, fermentation and packaging, but primary production remains largely dominated by smallholder farmers that are fairly well organized and maintain a rather strong bargaining position.

This general picture seems to indicate that development of input and output markets (that lead to increasing midstream value-added creation) could be a helpful strategy to support a more equitable farm size distribution (even while we have no proof of causality). Smallholder farms dominate the production and marketing of many staple food crops (maize, sorghum, groundnut) that are both used for local consumption and (peri-)urban processing. Larger farms dominate the production of highly commercial activities such as green beans (Kenya) and cotton (Ethiopia). Cocoa appears as a typical case of a smallholder-dominated crop with high commercialization rates where total value added is distributed equally between the production and the commercialization/processing stage.

This pattern roughly confirms earlier findings that midstream firms are critical for providing key services (i.e., input supply, technical assistance, service contracts, etc.) to smallholder producers [

29]. Consequently, efforts to develop midstream enterprise activities can be supportive for the viability of small-scale (commercially oriented) producers. Average farm sizes are indeed increasing in most middle-income countries and emerging economies, including several East and Southern African countries [

26]. More detailed country studies confirm that the share of land accounted for by marginal small-scale (0–2 hectares) holdings is generally declining in most sub-Saharan African countries, whereas medium-size farms (2–20 ha) are gradually becoming more important, both in terms of cultivated area and in terms of contribution to (commercial) crop production [

30]. The number of mid-size farms is growing rapidly and medium-scale farms will soon account for the majority of operated farmland and generate a growing share of the marketable food in many African countries.

4. Discussion and Conclusions

Recent developments in the organization and governance of agri-food value chains in sub-Saharan Africa show a remarkable dynamics in terms of labour allocation, investments, trade transactions and value added distribution. We used primary data from six typical agri-food chains to assess the implications of the growing importance of midstream operations for the competitive position of smallholder farmers, in order to better understand the opportunities and constraints for value chain-driven strategies towards agricultural intensification.

We therefore analysed the relationships between productions systems, value chain organization and farm size structure. This analysis is based on the idea that the structural farm-size composition is a reflection of the competitive relationships at land, labour, capital and commodity markets [

31]. Typical farm size structures emerge in response to opportunities for intensifying market linkages (efficiency and scale economies) and for upgrading factor productivity (through innovations that influence crop and technology choice and improve quality performance).

Smallholder farms play a critical role in the absorption of rural labour, but midsize farms are better able to respond to market challenges. Growing opportunities for mechanization and standardization may eventually lead to further farm concentration. Many smallholders only produce a small surplus and therefore the marketed volume is exceedingly concentrated among a small group of medium-size and large producers [

32]. This is a reason to question the exclusive commitment to smallholders and argue for a much more open-minded approach to midsize producers [

33].

The analysis in this article focuses on two research issues. First, we looked at the role of smallholder linkages with commercial midstream value chains actors and their implications for investments in improving farm-level efficiency and factor productivity. We find that midstream activities become increasingly important for value added generation, even while in smallholder-dominated VCs primary production keeps a major share of employment creation. Rising opportunities for downstream value added generation give room for a market-oriented transition in VCs where the midstream value added shares rises faster than the midstream employment share. VCs with larger opportunities for local processing and/or more extensive cultivation practices leaves more room for midstream employment creation.

The growth of midstream value added has profound effects on farm-level operations. Investments in better input use and capital at the level of primary production lead to improved competitiveness with midstream operations and enable smallholder farmers to retain a larger share of value added activity. Prospects for intensification in primary production increase when the value added share captured by midstream agents remains restricted. More intensive primary production systems that require larger amounts of inputs and capital realize a lower value added share in midstream operations, while more extensive cropping systems tend to transfer a larger share of total value added to competitive midstream agents.

Second, we assessed the importance of value added generation in midstream value chain segments for composition of the farm size structure in primary production. Contrary to our expectations, we find that a larger value added share generated in midstream operations is associated with a more balanced farm size distribution. This is mainly due to the growing importance of quality compliance operations in primary production. Smallholders meet prospects in VC integration that relies more on value added than just larger volumes. This implies that further deepening of trade, processing and wholesale/retail activities can be beneficial as well for primary producers. These backwards linkages are particularly important in VCs of food staples and—to a minor extent—in cocoa, where local recollection and direct processing are critical for maintaining quality and reliability.

The growing interactions between smallholder production and midstream operations have profound implications for the design of policies and programs aiming at VC intensification. Whereas most traditional rural development focus on ‘push’ incentives (training, credit, extension), it appears that smallholders’ decisions towards farming system intensification depend far more on the prospects for engaging in rewarding value-chain linkages and procurement contracts with midstream agents. These ‘pull’ incentives from VC partners are critical for reducing risks and transaction costs that are required to enhance the likelihood of investment decisions.

Further research on the linkages between midstream VC development and the competitiveness of smallholder producers should focus attention on the (technical) opportunities for improving the input efficiency of primary production systems and the (economic) strategies for enhancing the profitability of value chain operations. Therefore, due attention needs to be given to the possibilities for strengthening the potential for greater reliance on contractual arrangements strategies for reducing transaction costs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}