Environmental Information Disclosure and Corporate Green Innovation: The Moderating Effect of Formal and Informal Institutions

Abstract

:1. Introduction

2. Literature Review and Research Hypothesis

2.1. Literature Review

2.1.1. Green Innovation

2.1.2. Environmental Information Disclosure

2.1.3. Theoretical Basis

2.1.4. Research Gap

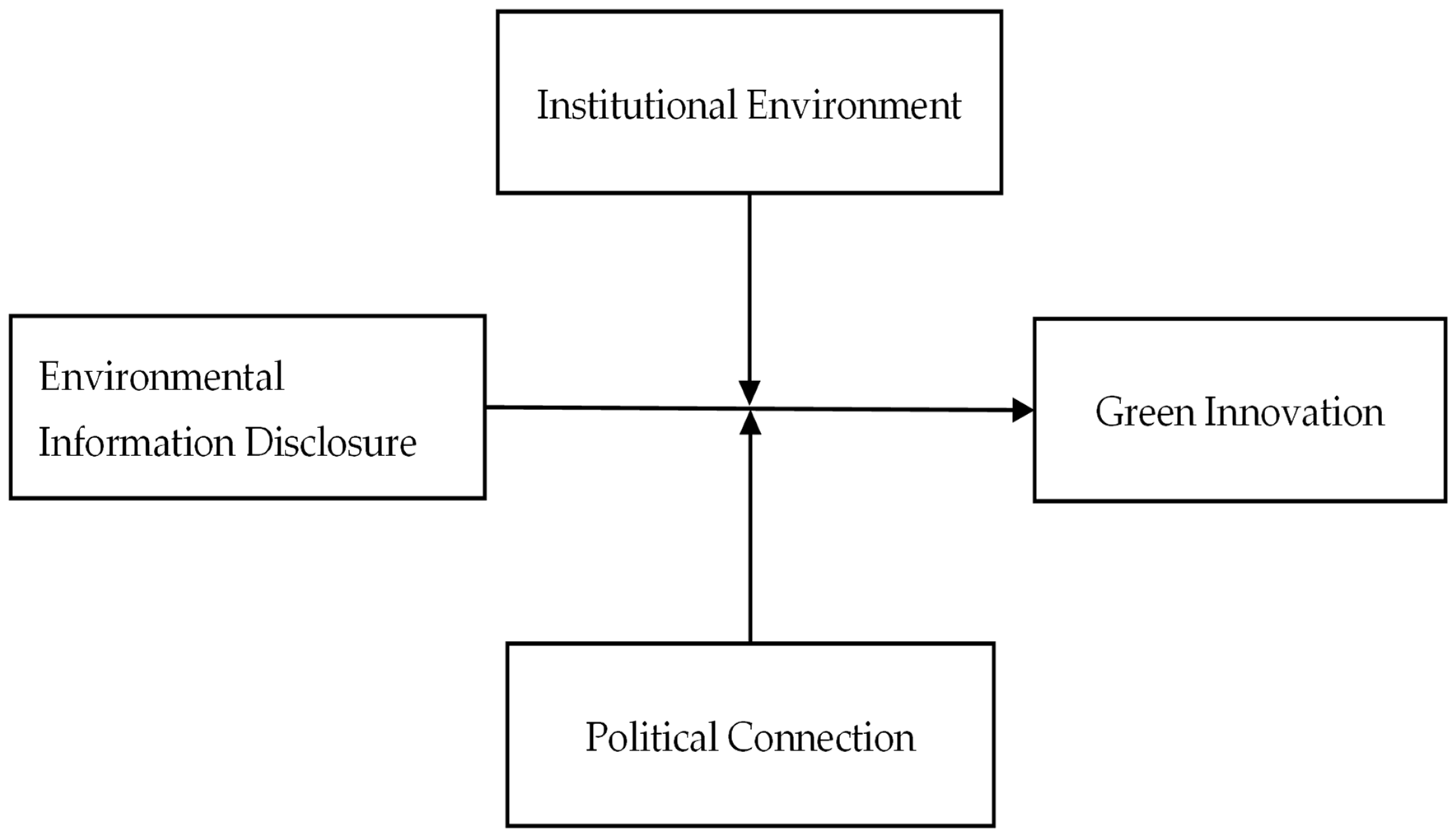

2.2. Research Hypothesis

2.2.1. Environmental Information Disclosure and Green Innovation

2.2.2. Moderation Effect of Institutional Environment

2.2.3. Moderation Effect of Political Connections

3. Data and Methodology

3.1. Data and Samples

3.2. Variables Definition

3.2.1. Dependent Variable

3.2.2. Independent Variable

3.2.3. Moderation Variables

3.2.4. Control Variables

3.3. Models

4. Empirical Findings

4.1. Descriptive Statistics and Correlation Analysis

4.2. Multiple Regression Analysis

4.2.1. The Effect of Environmental Information Disclosure on Green Innovation

4.2.2. Moderation Effect Test

4.2.3. Endogeneity Test

4.2.4. Robustness Test

5. Conclusions and Discussion

6. Theoretical Contribution

7. Practical Recommendation

8. Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Liu, S.; Xu, R.; Chen, X. Does green credit affect the green innovation performance of high-polluting and energy-intensive enterprises? Evidence from a quasi-natural experiment. Environ. Sci. Pollut. Res. 2021, 28, 65265–65277. [Google Scholar] [CrossRef] [PubMed]

- Zhang, S.; Zhang, M.; Qiao, Y.; Li, X.; Li, S. Does improvement of environmental information transparency boost firms’ green innovation? Evidence from the air quality monitoring and disclosure program in China. J. Clean. Prod. 2022, 357, 131921. [Google Scholar] [CrossRef]

- Takalo, S.K.; Tooranloo, H.S. Green innovation: A systematic literature review. J. Clean. Prod. 2021, 279, 122474. [Google Scholar] [CrossRef]

- Roh, T.; Lee, K.; Yang, J.Y. How do intellectual property rights and government support drive a firm’s green innovation? The mediating role of open innovation. J. Clean. Prod. 2021, 317, 1–13. [Google Scholar] [CrossRef]

- Li, G.; Xue, Q.; Qin, J. Environmental information disclosure and green technology innovation: Empirical evidence from China. Technol. Forecast. Soc. Chang. 2022, 176, 121453. [Google Scholar] [CrossRef]

- North, D.C. Institutions, Institutional Change and Economic Performance; Cambridge University Press: Cambridge, UK, 1990; pp. 1–159. [Google Scholar]

- Ghulam, Y. Institutions and firms’ technological changes and productivity growth. Technol. Forecast. Soc. Chang. 2021, 171, 120993. [Google Scholar] [CrossRef]

- Khanna, T.; Palepu, K. Why focused strategies. Harv. Bus. Rev. 1997, 75, 41–51. [Google Scholar]

- Fuentelsaz, L.; González, C.; Maicas, J.P. Formal institutions and opportunity entrepreneurship. The contingent role of informal institutions. BRQ Bus. Res. Q. 2019, 22, 5–24. [Google Scholar] [CrossRef]

- Choi, S.-J.; Liu, H.; Yin, J.; Qi, Y.; Lee, J.Y. The effect of political turnover on firms’ strategic change in the emerging economies: The moderating role of political connections and financial resources. J. Bus. Res. 2021, 137, 255–266. [Google Scholar] [CrossRef]

- You, D.; Zhang, Y.; Yuan, B. Environmental regulation and firm eco-innovation: Evidence of moderating effects of fiscal decentralization and political competition from listed Chinese industrial companies. J. Clean. Prod. 2019, 207, 1072–1083. [Google Scholar] [CrossRef]

- De Miranda Ribeiro, F.; Kruglianskas, I. Principles of environmental regulatory quality: A synthesis from literature review. J. Clean. Prod. 2015, 96, 58–76. [Google Scholar] [CrossRef]

- Hao, J.; He, F. Corporate social responsibility (CSR) performance and green innovation: Evidence from China. Financ. Res. Lett. 2022, 48, 102889. [Google Scholar] [CrossRef]

- Huang, Z.; Liao, G.; Li, Z. Loaning scale and government subsidy for promoting green innovation. Technol. Forecast. Soc. Chang. 2019, 144, 148–156. [Google Scholar] [CrossRef]

- Song, M.; Wang, S.; Zhang, H. Could environmental regulation and R&D tax incentives affect green product innovation? J. Clean. Prod. 2020, 258, 120849. [Google Scholar]

- Yi, Y.; Wei, Z.; Fu, C. An optimal combination of emissions tax and green innovation subsidies for polluting oligopolies. J. Clean. Prod. 2021, 284, 124693. [Google Scholar] [CrossRef]

- Liao, Y.C.; Tsai, K.H. Innovation intensity, creativity enhancement, and eco-innovation strategy: T he roles of customer demand and environmental regulation. Bus. Strategy Environ. 2019, 28, 316–326. [Google Scholar] [CrossRef]

- Gürlek, M.; Tuna, M. Reinforcing competitive advantage through green organizational culture and green innovation. Serv. Ind. J. 2018, 38, 467–491. [Google Scholar] [CrossRef]

- Awan, U.; Sroufe, R.; Kraslawski, A. Creativity enables sustainable development: Supplier engagement as a boundary condition for the positive effect on green innovation. J. Clean. Prod. 2019, 226, 172–185. [Google Scholar] [CrossRef]

- Galbreath, J. Drivers of green innovations: The impact of export intensity, women leaders, and absorptive capacity. J. Bus. Ethics 2019, 158, 47–61. [Google Scholar] [CrossRef]

- Yahya, S.; Jamil, S.; Farooq, M. The impact of green organizational and human resource factors on developing countries’ small business firms tendency toward green innovation: A natural resource-based view approach. Creat. Innov. Manag. 2021, 30, 726–741. [Google Scholar] [CrossRef]

- Yousaf, Z. Go for green: Green innovation through green dynamic capabilities: Accessing the mediating role of green practices and green value co-creation. Environ. Sci. Pollut. Res. 2021, 28, 54863–54875. [Google Scholar] [CrossRef] [PubMed]

- Cui, R.; Wang, J.; Xue, Y.; Liang, H. Interorganizational learning, green knowledge integration capability and green innovation. Eur. J. Innov. Manag. 2020, 24, 1–23. [Google Scholar] [CrossRef]

- Wang, C.; Weng, Y.; Wang, L. Effect of air quality on corporate environmental disclosure: The moderating role of institutional investors. Borsa Istanb. Rev. 2021, 21 (Suppl. 1), S1–S12. [Google Scholar] [CrossRef]

- Fan, L.; Yang, K.; Liu, L. New media environment, environmental information disclosure and firm valuation: Evidence from high-polluting enterprises in China. J. Clean. Prod. 2020, 277, 123253. [Google Scholar] [CrossRef]

- Wei, Y.; He, W. Can anti-corruption improve the quality of environmental information disclosure? Environ. Sci. Pollut. Res. 2022, 29, 5345–5359. [Google Scholar] [CrossRef]

- Gerged, A.M. Factors affecting corporate environmental disclosure in emerging markets: The role of corporate governance structures. Bus. Strategy Environ. 2021, 30, 609–629. [Google Scholar] [CrossRef]

- Berrone, P.; Fosfuri, A.; Gelabert, L.; Gomez-Mejia, L.R. Necessity as the mother of ‘green’ inventions: Institutional pressures and environmental innovations. Strateg. Manag. J. 2013, 34, 891–909. [Google Scholar] [CrossRef]

- Li, Y.; Zhang, X.; Yao, T.; Sake, A.; Liu, X.; Peng, N. The developing trends and driving factors of environmental information disclosure in China. J. Environ. Manag. 2021, 288, 1–11. [Google Scholar] [CrossRef]

- Freeman, R.E.; Phillips, R.; Sisodia, R. Tensions in stakeholder theory. Bus. Soc. 2020, 59, 213–231. [Google Scholar] [CrossRef]

- Stocker, F.; De Arruda, M.P.; Mascena, K.; Boaventura, J. Stakeholder engagement in sustainability reporting: A classification model. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 2071–2080. [Google Scholar] [CrossRef] [Green Version]

- Buallay, A. Sustainability reporting and firm’s performance: Comparative study between manufacturing and banking sectors. Int. J. Product. Perform. Manag. 2019, 69, 431–445. [Google Scholar] [CrossRef]

- Sun, D.; Zeng, S.; Chen, H.; Meng, X.; Jin, Z. Monitoring effect of transparency: How does government environmental disclosure facilitate corporate environmentalism? Bus. Strategy Environ. 2019, 28, 1594–1607. [Google Scholar] [CrossRef]

- Singh, S.K.; Del Giudice, M.; Chierici, R.; Graziano, D. Green innovation and environmental performance: The role of green transformational leadership and green human resource management. Technol. Forecast. Soc. Change 2020, 150, 119762. [Google Scholar] [CrossRef]

- Feng, Y.; He, F. The effect of environmental information disclosure on environmental quality: Evidence from Chinese cities. J. Clean. Prod. 2020, 276, 124027. [Google Scholar] [CrossRef]

- Lu, J.; Li, B.; Li, H.; Zhang, Y. Sustainability of enterprise export expansion from the perspective of environmental information disclosure. J. Clean. Prod. 2020, 252, 119839. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvar, F.P. Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Account. Organ. Soc. 2008, 33, 303–327. [Google Scholar] [CrossRef]

- Derakhshan, R.; Turner, R.; Mancini, M. Project governance and stakeholders: A literature review. Int. J. Proj. Manag. 2019, 37, 98–116. [Google Scholar] [CrossRef]

- Goss, A.; Roberts, G.S. The impact of corporate social responsibility on the cost of bank loans. J. Bank. Financ. 2011, 35, 1794–1810. [Google Scholar] [CrossRef]

- Luo, W.; Guo, X.; Zhong, S.; Wang, J. Environmental information disclosure quality, media attention and debt financing costs: Evidence from Chinese heavy polluting listed companies. J. Clean. Prod. 2019, 231, 268–277. [Google Scholar] [CrossRef]

- Aracil, E. Corporate social responsibility of Islamic and conventional banks: The influence of institutions in emerging countries. Int. J. Emerg. Mark. 2019, 14, 1–19. [Google Scholar] [CrossRef]

- Williamson, O.E. The New Institutional Economics: Taking Stock, Looking Ahead. Glob. Jurist 2000, 38, 595–613. [Google Scholar] [CrossRef] [Green Version]

- Mcmillan, J.; Woodruff, C. The Central Role of Entrepreneurs in Transition Economies. J. Econ. Perspect. 2002, 16, 153–170. [Google Scholar] [CrossRef]

- Joseph, J.; Gaba, V. Organizational structure, information processing, and decision-making: A retrospective and road map for research. Acad. Manag. Ann. 2020, 14, 267–302. [Google Scholar] [CrossRef]

- Huang, J.; Li, Y. Green innovation and performance: The view of organizational capability and social reciprocity. J. Bus. Ethics 2017, 145, 309–324. [Google Scholar] [CrossRef]

- Qi, G.; Jia, Y.; Zou, H. Is institutional pressure the mother of green innovation? Examining the moderating effect of absorptive capacity. J. Clean. Prod. 2021, 278, 123957. [Google Scholar] [CrossRef]

- Yang, J.; Basile, K. Communicating corporate social responsibility: External stakeholder involvement, productivity and firm performance. J. Bus. Ethics 2022, 178, 501–517. [Google Scholar] [CrossRef]

- Ivanovna, A.M. Formation of the institutional environment is the key factor for the innovative development of the country. Eur. Sci. Rev. 2018, 1, 271–273. [Google Scholar]

- Baalouch, F.; Ayadi, S.D.; Hussainey, K. A study of the determinants of environmental disclosure quality: Evidence from French listed companies. J. Manag. Gov. 2019, 23, 939–971. [Google Scholar] [CrossRef] [Green Version]

- Cheng, Z.; Wang, F.; Keung, C.; Bai, Y. Will corporate political connection influence the environmental information disclosure level? Based on the panel data of A-shares from listed companies in shanghai stock market. J. Bus. Ethics 2017, 143, 209–221. [Google Scholar] [CrossRef]

- Schoenherr, D. Political connections and allocative distortions. J. Financ. 2019, 74, 543–586. [Google Scholar] [CrossRef]

- Pan, X.; Tian, G.G. Political connections and corporate investments: Evidence from the recent anti-corruption campaign in China. J. Bank. Financ. 2020, 119, 105108. [Google Scholar] [CrossRef] [Green Version]

- Yan, J.Z.; Chang, S.J. The contingent effects of political strategies on firm performance: A political network perspective. Strateg. Manag. J. 2018, 39, 2152–2177. [Google Scholar] [CrossRef]

- Wang, F.; Xu, L.; Zhang, J.; Shu, W. Political connections, internal control and firm value: Evidence from China’s anti-corruption campaign. J. Bus. Res. 2018, 86, 53–67. [Google Scholar] [CrossRef]

- Gargiulo, M.; Benassi, M. Trapped in your own net? Network cohesion, structural holes, and the adaptation of social capital. Organ. Sci. 2000, 11, 183–196. [Google Scholar] [CrossRef]

- He, Y.; Xu, L.; Mciver, R.P. How does political connection affect firm financial distress and resolution in China? Appl. Econ. 2019, 51, 2770–2792. [Google Scholar] [CrossRef]

- Li, S.; Lu, J. A Dual-Agency Model of Firm CSR in Response to Institutional Pressure: Evidence from Chinese Publicly Listed Firms. Acad. Manag. J. 2020, 63, 2004–2032. [Google Scholar] [CrossRef]

- Wang, L.; Zeng, T.; Li, C. Behavior decision of top management team and enterprise green technology innovation. J. Clean. Prod. 2022, 367, 133120. [Google Scholar] [CrossRef]

- Meng, X.H.; Zeng, S.X.; Tam, C.M.; Xu, X.D. Whether top executives’ turnover influences environmental responsibility: From the perspective of environmental information disclosure. J. Bus. Ethics 2013, 114, 341–353. [Google Scholar] [CrossRef]

- Du, X.; Weng, J.; Zeng, Q.; Chang, Y.; Pei, H. Do lenders applaud corporate environmental performance? Evidence from Chinese private-owned firms. J. Bus. Ethics 2017, 143, 179–207. [Google Scholar] [CrossRef]

- Li, R.; Ramanathan, R. Can environmental investments benefit environmental performance? The moderating roles of institutional environment and foreign direct investment. Bus. Strategy Environ. 2020, 29, 3385–3398. [Google Scholar] [CrossRef]

- Wang, X.; Fan, G.; Yu, J. Marketization Index of China’s Provinces: NERI Report 2018 (in Chinese); Social Sciences Academic Press: Beijing, China, 2019. [Google Scholar]

- Song, M.; Ai, H.; Li, X. Political connections, financing constraints, and the optimization of innovation efficiency among China’s private enterprises. Technol. Forecast. Soc. Change 2015, 92, 290–299. [Google Scholar] [CrossRef]

- McCaffrey, D.F.; Lockwood, J.R.; Mihaly, K.; Sass, T.R. A review of Stata commands for fixed-effects estimation in normal linear models. Stata J. 2012, 12, 406–432. [Google Scholar] [CrossRef] [Green Version]

- Goldsmith-Pinkham, P.; Sorkin, I.; Swift, H. Bartik instruments: What, when, why, and how. Am. Econ. Rev. 2020, 110, 2586–2624. [Google Scholar] [CrossRef]

- Driscoll, J.C.; Kraay, A.C. Consistent Covariance Matrix Estimation with Spatially Dependent Panel Data. Rev. Econ. Stat. 1998, 80, 549–560. [Google Scholar] [CrossRef]

- Chen, X.; Yi, N.; Zhang, L.; Li, D. Does institutional pressure foster corporate green innovation? Evidence from China’s top 100 companies. J. Clean. Prod. 2018, 188, 304–311. [Google Scholar] [CrossRef]

- Kiefer, C.P.; Del Rio Gonzalez, P.; Carrillo Hermosilla, J. Drivers and barriers of eco-innovation types for sustainable transitions: A quantitative perspective. Bus. Strategy Environ. 2019, 28, 155–172. [Google Scholar] [CrossRef] [Green Version]

- Kim, I.; Pantzalis, C.; Zhang, Z. Multinationality and the value of green innovation. J. Corp. Financ. 2021, 69, 101996. [Google Scholar] [CrossRef]

- Xie, J.; Nozawa, W.; Yagi, M.; Fujii, H.; Managi, S. Do environmental, social, and governance activities improve corporate financial performance? Bus. Strategy Environ. 2019, 28, 286–300. [Google Scholar] [CrossRef] [Green Version]

- Hemingway, C.A.; Maclagan, P.W. Managers’ personal values as drivers of corporate social responsibility. J. Bus. Ethics 2004, 50, 33–44. [Google Scholar] [CrossRef]

- Feng, Y.; Wang, X.; Liang, Z. How does environmental information disclosure affect economic development and haze pollution in Chinese cities? The mediating role of green technology innovation. Sci. Total Environ. 2021, 775, 145811. [Google Scholar] [CrossRef]

- Jones, T.M.; Wicks, A.C.; Freeman, R.E. Stakeholder Theory: The State of the Art; The Blackwell guide to business ethics; Cambridge University Press: Cambridge, UK, 2017; pp. 17–37. [Google Scholar]

- Martin, H.D. Demystifying the link between institutional theory and stakeholder theory in sustainability reporting. Econ. Manag. Sustain. 2018, 3, 6–19. [Google Scholar]

- Freeman, R.E.; Dmytriyev, S.D.; Phillips, R.A. Stakeholder theory and the resource-based view of the firm. J. Manag. 2021, 47, 1757–1770. [Google Scholar] [CrossRef]

- Kentikelenis, A.E.; Babb, S. The making of neoliberal globalization: Norm substitution and the politics of clandestine institutional change. Am. J. Sociol. 2019, 124, 1720–1762. [Google Scholar] [CrossRef]

- Liu, G.; Xin, G.; Li, J. Making political connections work better: Information asymmetry and the development of private firms in China. Corp. Gov. Int. Rev. 2021, 29, 593–611. [Google Scholar] [CrossRef]

- Adhikari, A.; Derashid, C.; Zhang, H. Public policy, political connections, and effective tax rates: Longitudinal evidence from Malaysia. J. Account. Public Policy 2006, 25, 574–595. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Variables | Description | |

|---|---|---|

| Dependent Variable | GRInno | The indicators of the number of green patent applications include the total number of green patents. |

| Independent Variable | EID | This study summarizes the annual scores of the sum of each firm’s seven components, constructs a raw index of environmental information disclosure quality, and further standardizes the basic index by dividing the raw index by the maximum possible score to obtain a measure of environmental information disclosure quality. |

| Moderation Variables | MI | This study uses the score of the marketization index, especially in the Chinese research setting. The marketization index can assess the institutional environment of each province in mainland China systematically. |

| PC | This study uses an enterprise’s actual controller or chairman (i.e., a present or former government official, an NPC member, or a CPPCC member). When this condition exists, an enterprise can be defined as “politically connected”. | |

| Control Variables | Size | The natural logarithm of total assets |

| Age | The number of years that the firm has been established | |

| Board | The number of the corporate board of directors for the year | |

| Duality | If the chairman and the CEO are same people, the value is 1, and the opposite is 0 | |

| Inde | The number of independent directors/total number of board members | |

| Holder1 | Percentage of shares held by the largest shareholder | |

| Lev | The total liabilities of the enterprise are compared with the total assets | |

| ROA | Net profit divided by average total assets | |

| Tangibility | The total fixed assets of the enterprise are compared with the total assets | |

| Growth | The ratio of the difference between the current period’s operating income minus the previous period’s operating income divided by the prior period’s operating income | |

| Soe | The value is taken as 1 when the enterprise is a state-owned enterprise, and as 0 otherwise | |

| Variables | Mean | SD | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. GRInno | 0.383 | 0.778 | 1 | ||||||||||||||

| 2. EID | 0.078 | 0.162 | 0.102 c | 1 | |||||||||||||

| 3. MI | 9.244 | 3.253 | 0.078 c | −0.049 c | 1 | ||||||||||||

| 4. PC | 0.234 | 0.423 | 0.010 | 0.000 | −0.026 c | 1 | |||||||||||

| 5. Size | 22.022 | 1.267 | 0.243 c | 0.247 c | 0.047 c | −0.003 | 1 | ||||||||||

| 6. age | 2.863 | 0.340 | −0.043 c | 0.080 c | 0.234 c | −0.078 c | 0.166 c | 1 | |||||||||

| 7. Board | 2.258 | 0.175 | 0.063 c | 0.108 c | −0.135 c | −0.008 | 0.283 c | −0.002 | 1 | ||||||||

| 8. Dualiy | 0.259 | 0.438 | −0.007 | −0.065 c | 0.121 c | 0.000 | −0.208 c | −0.074 c | −0.185 c | 1 | |||||||

| 9. Inde | 0.372 | 0.053 | 0.026 c | −0.029 c | 0.037 c | 0.017 b | 0.014 b | −0.0110 | −0.504 c | 0.094 c | 1 | ||||||

| 10. Holder1 | 0.376 | 0.150 | 0.043 c | 0.043 c | 0.022 c | 0.003 | 0.147 c | −0.176 c | −0.00700 | −0.01 | 0.055 c | 1 | |||||

| 11. Lev | 0.416 | 0.208 | 0.101 c | 0.091 c | −0.110 c | −0.073 c | 0.487 c | 0.154 c | 0.177 c | −0.171 c | −0.018 b | −0.055 c | 1 | ||||

| 12. Roa | 0.040 | 0.060 | 0.022 c | −0.011 | 0.047 c | 0.049 c | −0.016 b | −0.090 c | −0.00400 | 0.062 c | −0.013 a | 0.174 c | −0.382 c | 1 | |||

| 13. Tangibility | 0.248 | 0.164 | −0.032 c | 0.268 c | −0.140 c | −0.019 c | 0.193 c | 0.044 c | 0.153 c | −0.113 c | −0.038 c | 0.028 c | 0.177 c | −0.135 c | 1 | ||

| 14. Growth | 0.206 | 0.399 | 0.008 | −0.092 c | −0.025 c | 0.039 c | −0.102 c | −0.238 c | −0.050 c | 0.134 c | 0.006 | 0.059 c | −0.176 c | 0.237 c | −0.243 c | 1 | |

| 15. Soe | 0.404 | 0.491 | 0.032 c | 0.118 c | −0.181 c | −0.090 c | 0.398 c | 0.150 c | 0.295 c | −0.316 c | −0.062 c | 0.099 c | 0.336 c | −0.126 c | 0.235 c | −0.192 c | 1 |

| Variables | (1) | (2) |

|---|---|---|

| GRInno | GRInno | |

| EID | 0.287 *** | 0.138 *** |

| (7.648) | (3.473) | |

| Size | 0.046 *** | 0.044 *** |

| (4.296) | (3.922) | |

| Age | 0.228 *** | 0.060 |

| (7.226) | (0.771) | |

| Board | 0.084 * | 0.089 * |

| (1.717) | (1.821) | |

| Dualiy | −0.019 | −0.024 * |

| (−1.381) | (−1.762) | |

| Inde | 0.232 * | 0.218 * |

| (1.774) | (1.674) | |

| Holder1 | −0.118 * | −0.149 ** |

| (−1.941) | (−2.416) | |

| Lev | 0.009 | 0.029 |

| (0.217) | (0.684) | |

| Roa | 0.081 | 0.107 |

| (0.948) | (1.247) | |

| Tangiblity | −0.034 | −0.036 |

| (−0.682) | (−0.725) | |

| Growth | −0.034 *** | −0.028 ** |

| (−3.059) | (−2.502) | |

| SOE | −0.043 | −0.023 |

| (−1.399) | (−0.741) | |

| Consatnt | −1.515 *** | −0.983 *** |

| (−6.551) | (−2.862) | |

| Firm FE | Yes | Yes |

| Industry FE | No | Yes |

| Year FE | No | Yes |

| N | 18,394 | 18,394 |

| Adj.R2 | 0.6491 | 0.6524 |

| Variables | (1) | (2) | (3) |

|---|---|---|---|

| GRInno | GRInno | GRInno | |

| EID | 0.146 *** | 0.168 *** | 0.177 *** |

| (3.670) | (3.938) | (4.130) | |

| MI | 0.018 | 0.019 | |

| (1.496) | (1.500) | ||

| EID × MI | 0.126 ** | 0.127 ** | |

| (2.262) | (2.271) | ||

| PC | −0.006 | −0.006 | |

| (−0.437) | (−0.399) | ||

| EID × PC | −0.134 ** | −0.136 ** | |

| (−1.961) | (−1.987) | ||

| Size | 0.045 *** | 0.045 *** | 0.045 *** |

| (3.973) | (3.980) | (4.029) | |

| Age | 0.059 | 0.061 | 0.061 |

| (0.765) | (0.796) | (0.791) | |

| Board | 0.088 * | 0.089 * | 0.088 * |

| (1.807) | (1.819) | (1.805) | |

| Dualiy | −0.025 * | −0.024 * | −0.025 * |

| (−1.797) | (−1.793) | (−1.826) | |

| Inde | 0.219 * | 0.220 * | 0.221 * |

| (1.682) | (1.683) | (1.691) | |

| Holder1 | −0.149 ** | −0.150 ** | −0.150 ** |

| (−2.418) | (−2.430) | (−2.433) | |

| Lev | 0.030 | 0.029 | 0.030 |

| (0.709) | (0.676) | (0.704) | |

| Roa | 0.101 | 0.107 | 0.101 |

| (1.173) | (1.247) | (1.173) | |

| Tangiblity | −0.037 | −0.038 | −0.038 |

| (−0.726) | (−0.760) | (−0.763) | |

| Growth | −0.028 ** | −0.029 ** | −0.029 ** |

| (−2.517) | (−2.546) | (−2.563) | |

| SOE | −0.023 | −0.023 | −0.023 |

| (−0.740) | (−0.744) | (−0.743) | |

| Consatnt | −0.982 *** | −0.994 *** | −1.002 *** |

| (−2.862) | (−2.893) | (−2.918) | |

| Firm FE | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes |

| N | 18,394 | 18,394 | 18,394 |

| Adj.R2 | 0.6523 | 0.6522 | 0.6523 |

| Variables | First Stage | Second Stage | |

|---|---|---|---|

| (1) | (2) | (3) | |

| EID | GRInno | GRInno | |

| EID | 0.580 *** | 0.529 ** | |

| (2.612) | (2.252) | ||

| IV_Bartik | 7.653 *** | ||

| (24.581) | |||

| Size | −0.084 *** | 0.031 ** | 0.032 ** |

| (−4.331) | (2.236) | (2.129) | |

| Age | 0.227 *** | 0.234 *** | 0.107 |

| (3.807) | (5.525) | (1.066) | |

| Board | −0.078 | 0.077 | 0.086 |

| (−0.617) | (1.273) | (1.418) | |

| Duality | −0.014 | −0.024 | −0.028 * |

| (−0.390) | (−1.400) | (−1.646) | |

| Inde | −0.237 | 0.088 | 0.090 |

| (−0.664) | (0.551) | (0.565) | |

| Holder1 | −0.232 * | −0.111 | −0.133 * |

| (−1.931) | (−1.493) | (−1.749) | |

| Lev | 0.321 *** | −0.029 | −0.005 |

| (3.010) | (−0.538) | (−0.088) | |

| Roa | 0.560 * | 0.080 | 0.103 |

| (1.807) | (0.748) | (0.950) | |

| Tangibility | 1.185 *** | −0.091 | −0.092 |

| (9.636) | (−1.446) | (−1.443) | |

| Growth | −0.043 | −0.025 | −0.019 |

| (−0.662) | (−1.254) | (−0.957) | |

| SOE | −0.043 | −0.069 * | −0.057 |

| (−1.060) | (−1.821) | (−1.480) | |

| Firm FE | Yes | Yes | Yes |

| Industry FE | Yes | No | Yes |

| Year FE | Yes | No | Yes |

| N | 13,291 | 13,291 | 13,291 |

| Adj.R2 | 0.4610 | 0.0162 | 0.0186 |

| Kleibergen–Paap rk LM statistic | 131.388 *** | ||

| Cragg–Donald Wald F statistic | 463.259 [16.38] | ||

| Variables | (1) | (2) | (3) |

|---|---|---|---|

| Authorized GRInno | Authorized GRInno | Authorized GRInno | |

| EID | 0.075 ** | 0.090 *** | 0.097 *** |

| (2.327) | (2.599) | (2.785) | |

| MI | 0.011 | 0.011 | |

| (1.111) | (1.115) | ||

| EID × MI | 0.101 ** | 0.101 ** | |

| (2.220) | (2.224) | ||

| PC | −0.008 | −0.008 | |

| (−0.693) | (−0.657) | ||

| EID × PC | −0.095 * | −0.096 * | |

| (−1.714) | (−1.738) | ||

| Size | 0.031 *** | 0.031*** | 0.032 *** |

| (3.427) | (3.442) | (3.493) | |

| Age | 0.108 * | 0.110 * | 0.109 * |

| (1.725) | (1.756) | (1.746) | |

| Board | 0.052 | 0.053 | 0.052 |

| (1.322) | (1.332) | (1.322) | |

| Duality | −0.018 | −0.018 | −0.018 * |

| (−1.606) | (−1.614) | (−1.647) | |

| Inde | 0.126 | 0.127 | 0.127 |

| (1.195) | (1.199) | (1.205) | |

| Holder1 | −0.035 | −0.035 | −0.035 |

| (−0.701) | (−0.701) | (−0.707) | |

| Lev | 0.033 | 0.032 | 0.033 |

| (0.958) | (0.911) | (0.941) | |

| Roa | 0.119 * | 0.124 * | 0.119 * |

| (1.705) | (1.774) | (1.706) | |

| Tangibility | −0.046 | −0.046 | −0.047 |

| (−1.116) | (−1.136) | (−1.143) | |

| Growth | −0.024 *** | −0.024 *** | −0.025 *** |

| (−2.680) | (−2.696) | (−2.717) | |

| SOE | −0.003 | −0.003 | −0.003 |

| (−0.123) | (−0.134) | (−0.130) | |

| Constant | −0.895 *** | −0.906 *** | −0.913 *** |

| (−3.217) | (−3.252) | (−3.277) | |

| Firm FE | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes |

| N | 18,394 | 18,394 | 18,394 |

| Adj.R2 | 0.6214 | 0.6213 | 0.6214 |

| Variables | (1) | (2) | (3) |

|---|---|---|---|

| GRInno | GRInno | GRInno | |

| EID | 0.146 *** | 0.168 *** | 0.177 *** |

| (3.436) | (3.368) | (3.343) | |

| MI | 0.018 ** | 0.019 ** | |

| (2.308) | (2.288) | ||

| EID × MI | 0.126 * | 0.127 ** | |

| (2.200) | (2.237) | ||

| PC | −0.006 | −0.006 | |

| (−0.424) | (−0.385) | ||

| EID × PC | −0.134 * | −0.136 * | |

| (−2.138) | (−2.115) | ||

| Size | 0.045 *** | 0.045 *** | 0.045 *** |

| (7.495) | (7.265) | (7.389) | |

| Age | 0.059 | 0.061 | 0.061 |

| (1.425) | (1.419) | (1.458) | |

| Board | 0.088 * | 0.089 * | 0.088 * |

| (1.825) | (1.852) | (1.818) | |

| Duality | −0.025 * | −0.024 * | −0.025 * |

| (−2.129) | (−2.134) | (−2.155) | |

| Inde | 0.219 | 0.220 | 0.221 |

| (1.262) | (1.267) | (1.260) | |

| Holder1 | −0.149 * | −0.150 * | −0.150 * |

| (−1.934) | (−1.931) | (−1.914) | |

| Lev | 0.030 | 0.029 | 0.030 |

| (0.600) | (0.556) | (0.590) | |

| Roa | 0.101 | 0.107 | 0.101 |

| (1.219) | (1.338) | (1.214) | |

| Tangibility | −0.037 | −0.038 | −0.038 |

| (−0.898) | (−0.957) | (−0.968) | |

| Growth | −0.028 *** | −0.029 *** | −0.029 *** |

| (−4.149) | (−4.065) | (−4.153) | |

| SOE | −0.023 | −0.023 | −0.023 |

| (−0.446) | (−0.441) | (−0.447) | |

| Constant | −0.922 ** | −0.939 ** | −0.937 ** |

| (−2.982) | (−2.944) | (−2.943) | |

| Firm FE | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes |

| N | 18,394 | 18,394 | 18,394 |

| Adj.R2 | 0.0390 | 0.0388 | 0.0393 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bai, X.; Lyu, C. Environmental Information Disclosure and Corporate Green Innovation: The Moderating Effect of Formal and Informal Institutions. Sustainability 2023, 15, 6169. https://doi.org/10.3390/su15076169

Bai X, Lyu C. Environmental Information Disclosure and Corporate Green Innovation: The Moderating Effect of Formal and Informal Institutions. Sustainability. 2023; 15(7):6169. https://doi.org/10.3390/su15076169

Chicago/Turabian StyleBai, Xiyan, and Chan Lyu. 2023. "Environmental Information Disclosure and Corporate Green Innovation: The Moderating Effect of Formal and Informal Institutions" Sustainability 15, no. 7: 6169. https://doi.org/10.3390/su15076169