The Impact of Officials’ Off-Office Accountability Audit of Natural Resource Assets on Firms’ Green Innovation Strategies: A Quasi-Natural Experiment in China

Abstract

:1. Introduction

2. Institutional Background and Literature Review

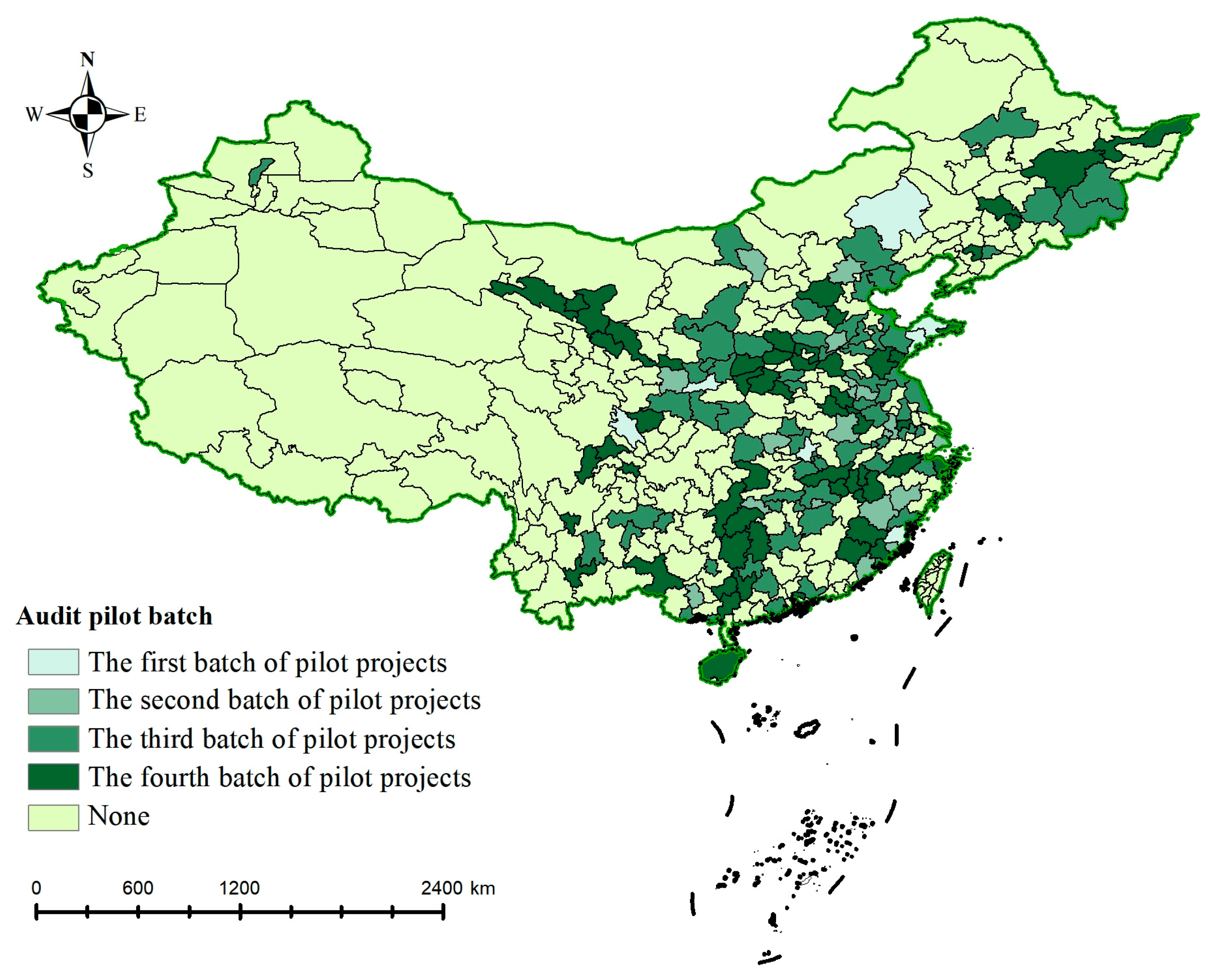

2.1. Institutional Background

2.2. Literature Review

2.2.1. Economic Consequences of Government Audits

2.2.2. The Debate on Green Innovation

3. Hypothesis Development

4. Research Design

4.1. Data and Sample Selection

4.2. Dependent Variables

4.3. Baseline Regression Model

5. Empirical Results and Analysis

5.1. Descriptive Statistics

5.2. Baseline Regression Results

5.3. Robustness Tests

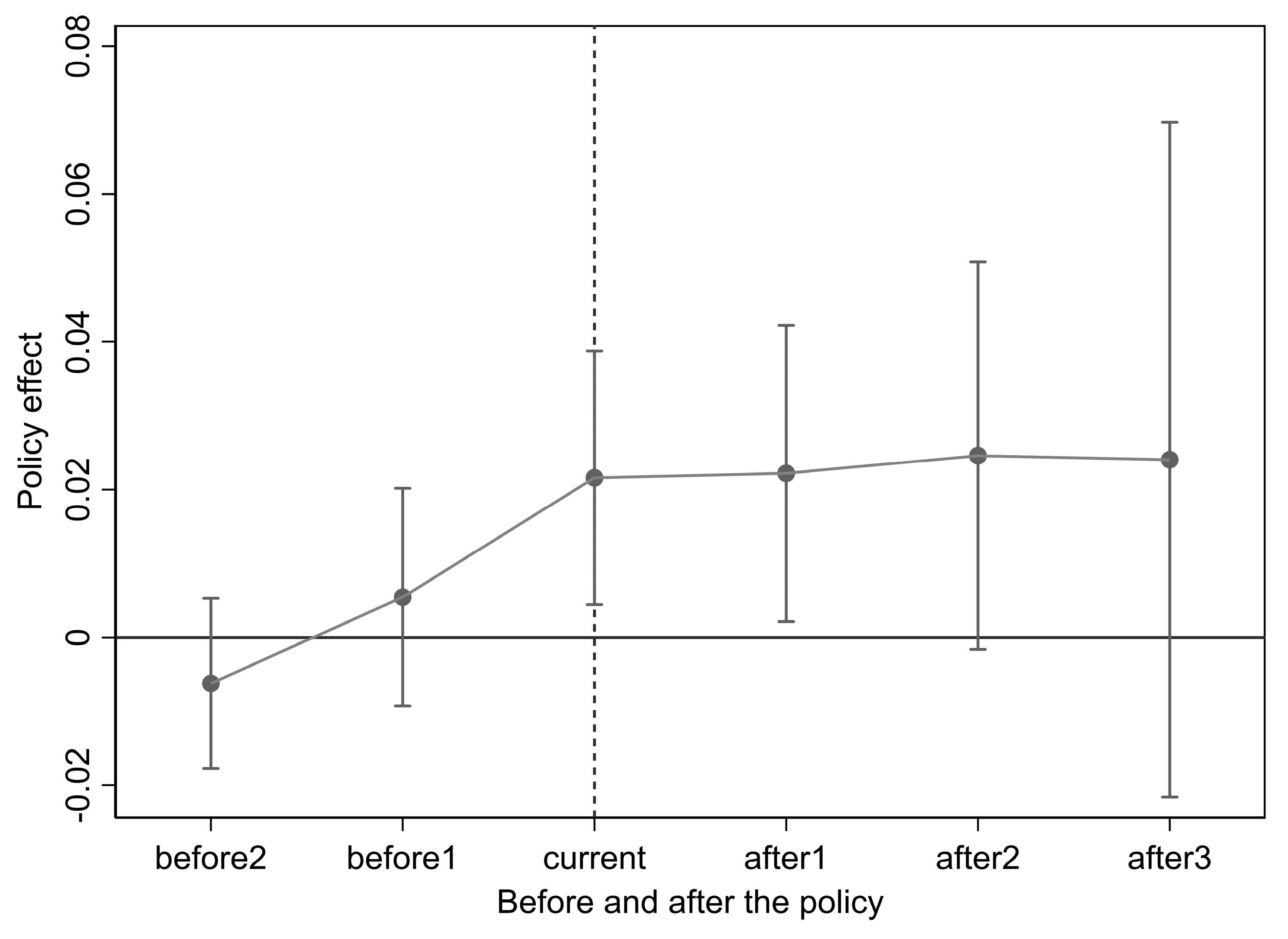

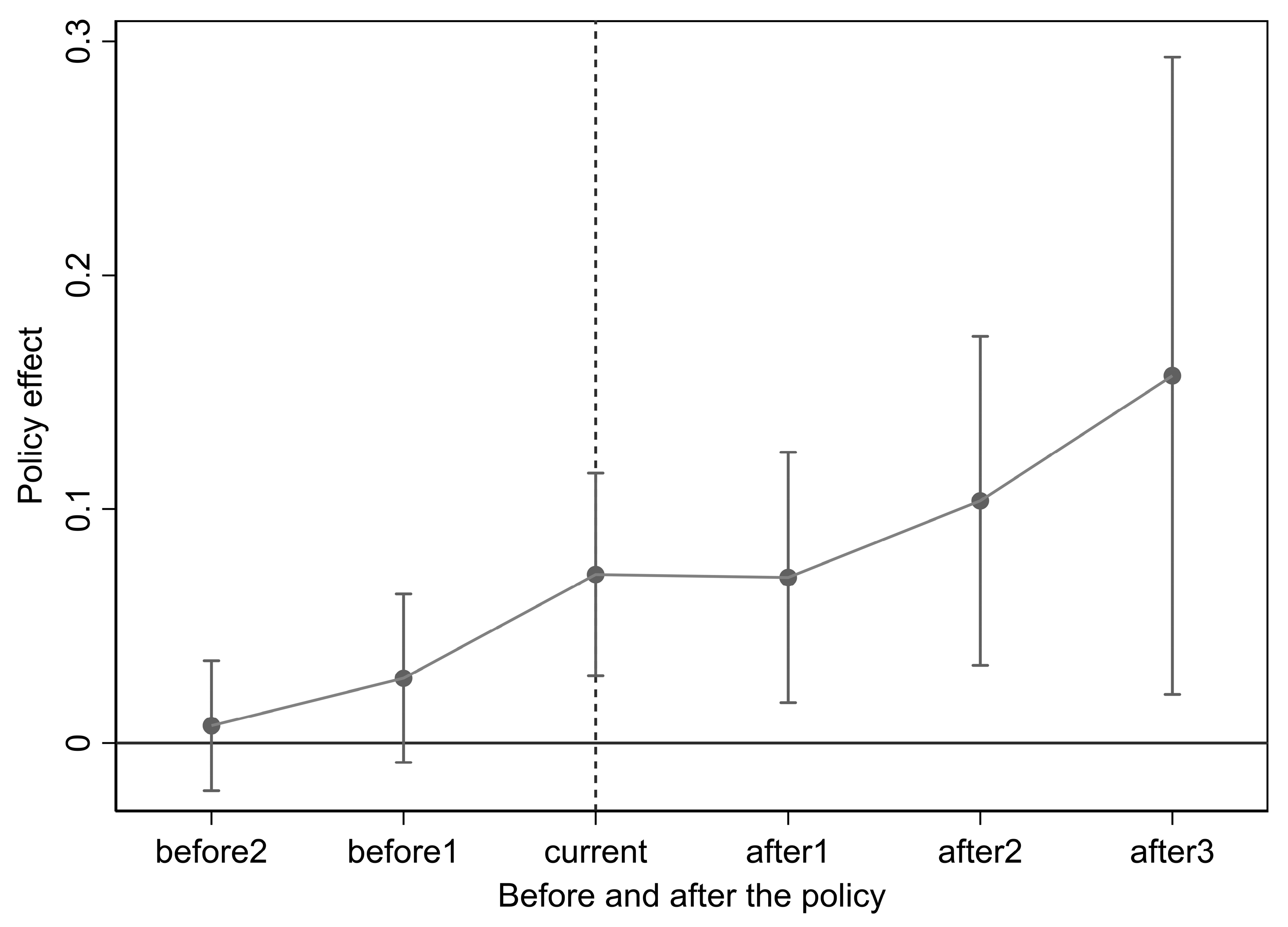

5.3.1. Parallel Trend Test

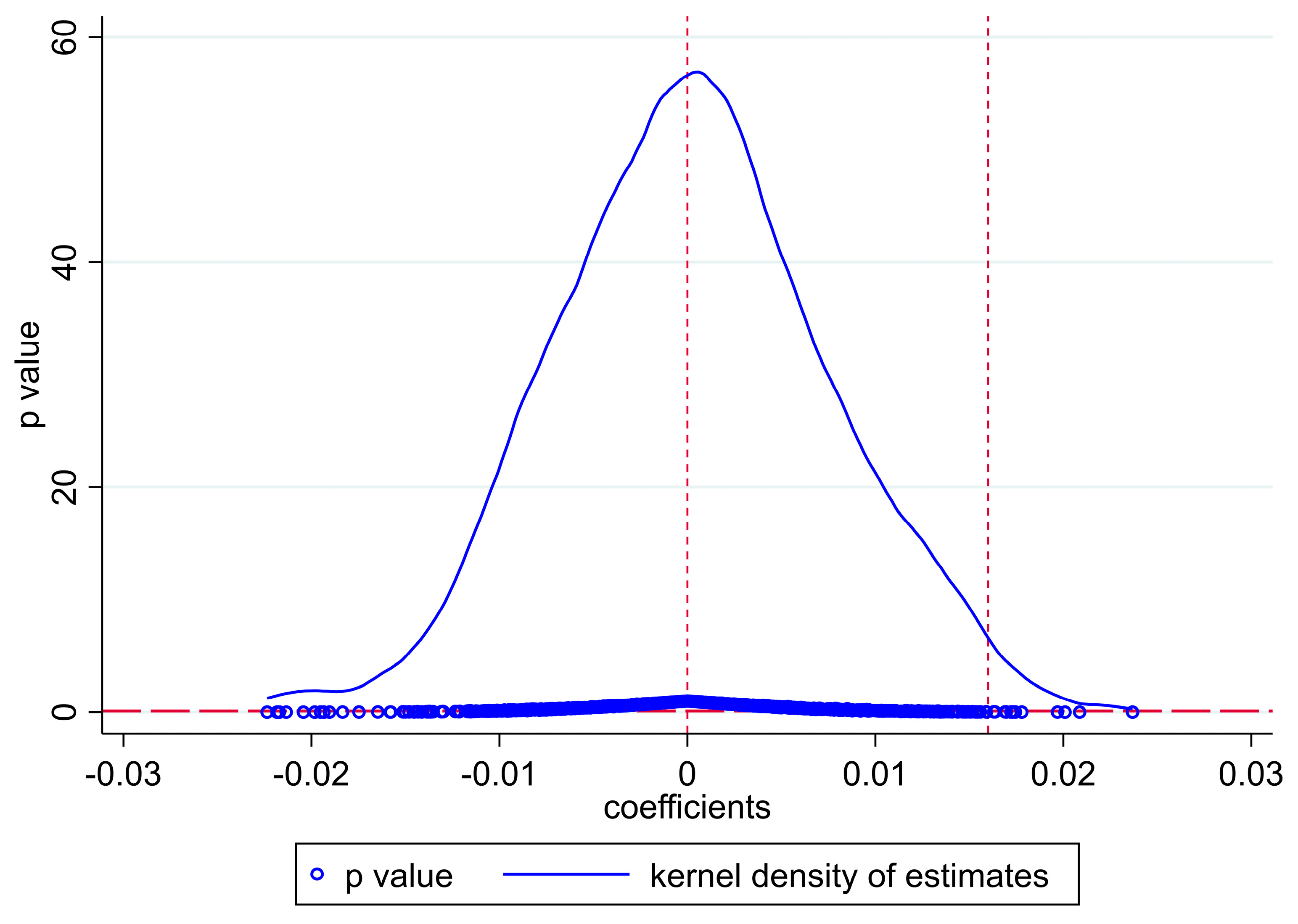

5.3.2. Placebo Test

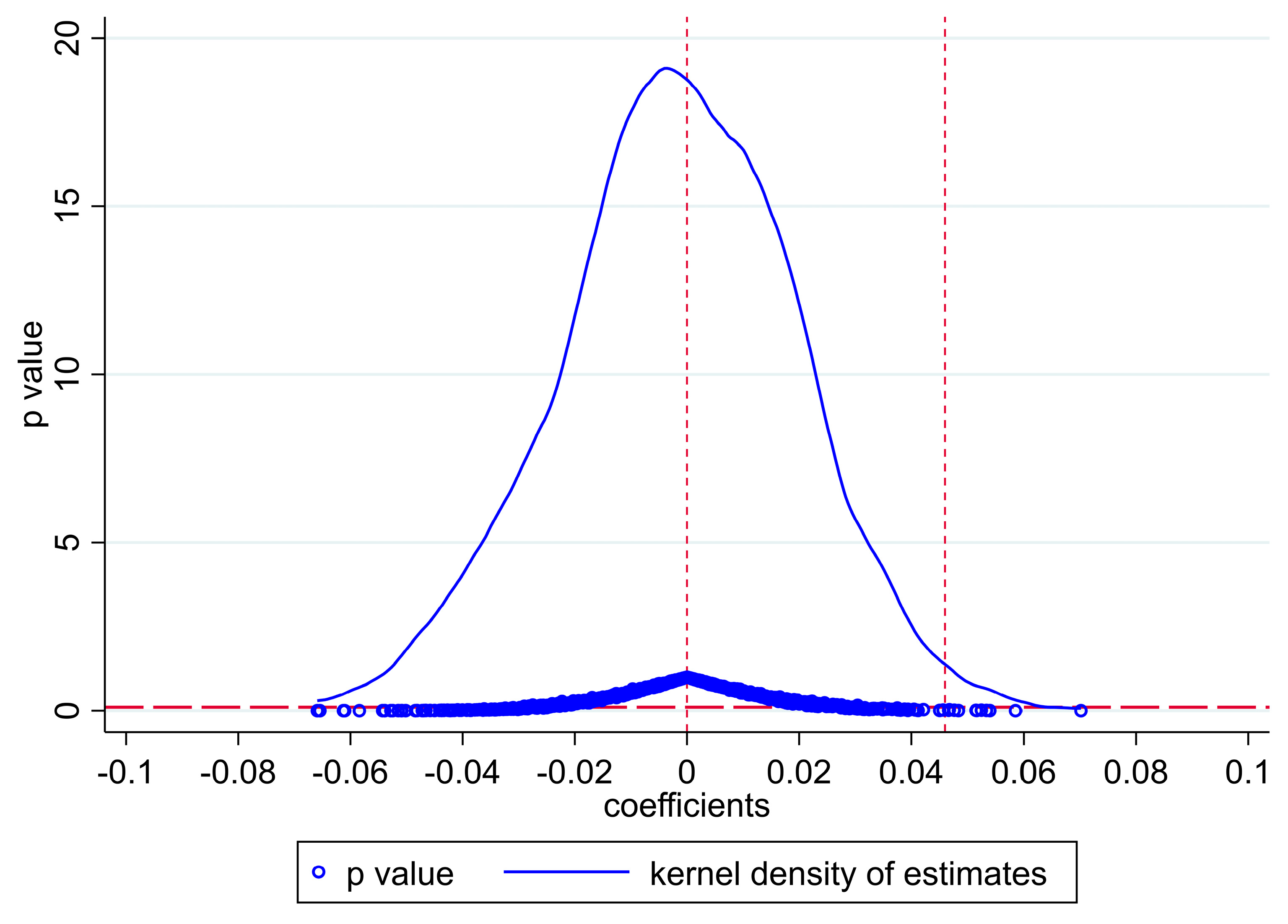

5.3.3. PSM Test

5.3.4. Entropy Balancing Test

5.3.5. Balanced Panel Regression Test

5.3.6. Excluding Special Cities

5.3.7. Additional Controls

5.3.8. Excluding Other Concurrent Policies

5.4. Further Analyses

5.4.1. Cross-Sectional Tests

- Local environmental protection pressure

- b.

- Government control over firms

- c.

- Capital market performance pressure

5.4.2. The Impact of the Accountability Audit Pilot on the Allocation of Environmental Protection Investment

5.4.3. Economic Consequences

6. Conclusions and Policy Implications

6.1. Conclusions

6.2. Policy Implications

6.3. Research Limitations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Definition |

|---|---|

| TECH_PROXIMITY | Green innovation technology proximity, calculated by formula (1), indicates the extent to which firms’ green innovations are similar or close to existing green innovations |

| KNOWN | Incremental green innovation, calculated as the natural logarithm of incremental green innovation |

| UNKNOWN | Radical green innovation, calculated as the natural logarithm of radical green innovation |

| SIZE | Firm size, calculated as the natural logarithm of total assets |

| EMENUM | Firm size, calculated as the natural logarithm of the number of employees |

| LEV | Leverage ratio, defined as the book value of debt to the book value of total assets |

| ROA | Return on assets, defined as net profit to net assets at the end of the period |

| BM | Book-to-market ratio, defined as the book value of equity to the market value of equity |

| GROWTH | Growth rate of total operating revenue, defined as the increase in gross operating income to gross operating income in the previous year |

| TANG | Proportion of fixed assets, defined as fixed assets to total assets |

| INTANG | Proportion of intangible assets, defined as intangible assets to total assets |

| FGNSALE | Proportion of overseas business income, measured as firms’ export ratio over sales in each year |

| AGE | Firm age, calculated as the natural logarithm of firm age |

| TOP | Shares held by the largest shareholder, measured as the number of shares held by the largest shareholder to the total number of shares |

| INDB | Proportion of independent directors, calculated as the number of independent directors to the total number of directors |

| SEG | Number of subsidiaries, calculated as the natural logarithm of the number of subsidiaries |

| LNGDP_PC | GDP per capita, calculated as the natural logarithm of the GDP per capita of the city in which the firm is located |

| LNPOPULATION | Population size, calculated as the natural logarithm of the population size of the city in which the firm is located |

| DEFICIT | Fiscal deficit, measured by the ratio of fiscal income to fiscal expenses of the city in which the firm is located |

| MKT | Market development, using the Marketization Index of the province in which the firm is located |

| LNCO2 | City CO2 emissions, calculated as the natural logarithm of the number of CO2 emissions of the city in which the firm is located |

| LNIWW | Industrial wastewater discharges, calculated as the natural logarithm of the amount of industrial wastewater of the city in which the firm is located |

| LNSO2 | Industrial SO2 emissions, calculated as the natural logarithm of the amount of industrial SO2 emissions of the city in which the firm is located |

| LNISD | Industrial smoke and dust emissions, calculated as the natural logarithm of the amount of industrial smoke and dust emissions of the city in which the firm is located |

| AIR | Regional air pollution, an indicator variable that equals 1 if the average annual concentration of PM2.5 is above the median and 0 otherwise |

| GPA | Green production attention, an indicator variable that equals 1 if the frequency of green production-related words divided by total word frequency is above the median and 0 otherwise |

| SOEP | State shareholding ratio, an indicator variable that equals 1 if firm i’s proportion of state-owned shares is above the median and 0 otherwise |

| TF | Tax preferences, an indicator variable that equals 1 if the tax refund received by firm i is above the median and 0 otherwise |

| AC | Analyst coverage, an indicator variable that equals 1 if firm i has high analyst coverage (above the median) and 0 otherwise |

| ISR | Institutional shareholding ratio, an indicator variable that equals 1 if the fund’s shareholding ratio is above the median and 0 otherwise |

| EPI | Environmental protection investment, calculated as total environmental protection investment to total assets |

| EVA | Enterprise economic performance, measured as EVA to operating income |

| CSRID | CSR disclosure, defined as 1 if firm i discloses its social responsibility report in year t and 0 otherwise |

References

- Hao, Y.; Deng, Y.X.; Lu, Z.N.; Chen, H. Is environmental regulation effective in China? Evidence from city-level panel data. J. Clean. Prod. 2018, 188, 966–976. [Google Scholar] [CrossRef]

- Wang, C.; Wu, J.; Zhang, B. Environmental regulation, emissions, and productivity: Evidence from Chinese COD–emitting manufacturers. J. Environ. Econ. Manag. 2018, 92, 54–73. [Google Scholar] [CrossRef]

- Li, H.; Zhou, L. Political turnover, and economic performance: The incentive role of personnel control in China. J. Public. Econ. 2005, 89, 1743–1762. [Google Scholar] [CrossRef]

- Guo, R.; Lv, S.; Liao, T.; Xi, F.; Zhang, J.; Zuo, X.; Cao, X.; Feng, Z.; Zhang, Y. Classifying green technologies for sustainable innovation and investment. Resour. Conserv. Recycl. 2020, 153, 104580. [Google Scholar] [CrossRef]

- Chen, Y.; Ma, Y. Does green investment improve energy firm performance? Energy Pol. 2021, 153, 112252. [Google Scholar] [CrossRef]

- Lin, B.; Ma, R. Green technology innovations, urban innovation environment, and CO2 emission reduction in China: Fresh evidence from a partially linear functional-coefficient panel model. Technol. Forecast. Soc. 2022, 176, 121434. [Google Scholar] [CrossRef]

- Long, X.; Chen, Y.; Du, J.; Oh, K.; Han, I. Environmental innovation and its impact on economic and environmental performance: Evidence from Korean–owned firms in China. Energy Pol. 2017, 107, 131–137. [Google Scholar] [CrossRef]

- Wang, M.; Li, Y.; Li, J.; Wang, Z. Green process innovation, green product innovation, and its economic performance improvement paths: A survey and structural model. J. Environ. Manag. 2021, 297, 113282. [Google Scholar] [CrossRef]

- Yang, X.; He, L.; Xia, Y.; Chen, Y. Effect of government subsidies on renewable energy investments: The threshold effect. Energy Pol. 2019, 132, 156–166. [Google Scholar] [CrossRef]

- Seroka-Stolka, O.; Fijorek, K. Enhancing corporate sustainable development: Proactive environmental strategy, stakeholder pressure, and the moderating effect of firm size. Bus. Strat. Env. 2020, 29, 2338–2354. [Google Scholar] [CrossRef]

- Sharma, S.; Prakash, G.; Kumar, A.; Mussada, E.K.; Antony, J.; Luthra, S. Analyzing the relationship of adaption of green culture, innovation, green performance for achieving sustainability: Mediating role of employee commitment. J. Clean. Prod. 2021, 303, 127039. [Google Scholar] [CrossRef]

- March, J. Exploration and exploitation in organizational learning. Organ. Sci. 1991, 2, 71–87. [Google Scholar] [CrossRef]

- Ma, X.; Shahbaz, M.; Song, M. Off–office audit of natural resource assets and water pollution: A quasi–natural experiment in China. J. Enterp. Inf. Manag. 2022. ahead-of-print. [Google Scholar] [CrossRef]

- Xu, J.; Hong, J.; Zhou, Z. Local attention to environment and green innovation: Evidence from listed manufacturing companies in 120 cities in China. Emerg. Mark. Financ. Trade. 2022. ahead-of-print. [Google Scholar] [CrossRef]

- Cao, H.; Zhang, L.; Yu, Q.; Yang, Z.; Li, X. Government auditing and environmental governance: Evidence from China’s auditing system reform. Environ. Impact Assess. Rev. 2022, 93, 106705. [Google Scholar] [CrossRef]

- Feng, Y.; Wang, X.; Liang, Z. How does environmental information disclosure affect economic development and haze pollution in Chinese cities? The mediating role of green technology innovation. Sci. Total Environ. 2021, 775, 145811. [Google Scholar] [CrossRef]

- Liu, Y.; She, Y.; Liu, S.; Tang, H. Can the leading officials’ accountability audit of natural resources policy stimulate Chinese heavy-polluting enterprises’ green behavior? Environ. Sci. Pollut. Control Ser. 2022, 29, 47772–47799. [Google Scholar] [CrossRef] [PubMed]

- Zeng, H.; Li, X.; Zhou, Q.; Wang, L. Local government environmental regulatory pressures and corporate environmental strategies: Evidence from natural resource accountability audits in China. Bus. Strat. Env. 2022. ahead-of-print. [Google Scholar] [CrossRef]

- Huang, J.; Li, Y. Green innovation and performance: The view of organizational capability and social reciprocity. J. Bus. Ethics. 2017, 145, 309–324. [Google Scholar] [CrossRef]

- Zhang, S.; Yu, Y.; Zhu, Q.; Qiu, C.; Tian, A. Green innovation mode under carbon tax and innovation subsidy: An evolutionary game analysis for portfolio policies. Sustainability 2020, 12, 1385. [Google Scholar] [CrossRef] [Green Version]

- Wang, D.; Zhang, Z.; Shi, R. Fiscal decentralization, green technology innovation, and regional air pollution in China: An investigation from the perspective of intergovernmental competition. Int. J. Environ. Res. Public Health 2022, 19, 8456. [Google Scholar] [CrossRef] [PubMed]

- Beerepoot, M.; Beerepoot, N. Government regulation as an impetus for innovation: Evidence from energy performance regulation in the Dutch residential building sector. Energy Pol. 2007, 35, 4812–4825. [Google Scholar] [CrossRef]

- Beck, M.; Lopes-Bento, C.; Schenker-Wicki, A. Radical or incremental: Where does R&D policy hit? Res. Policy 2016, 45, 869–883. [Google Scholar] [CrossRef]

- Forés, B.; Camisón, C. Does incremental and radical innovation performance depend on different types of knowledge accumulation capabilities and organizational size? J. Bus. Res. 2016, 69, 831–848. [Google Scholar] [CrossRef]

- Foucart, R.; Li, Q. The role of technology standards in product innovation: Theory and evidence from UK manufacturing firms. Res. Policy 2021, 50, 104157. [Google Scholar] [CrossRef]

- Freixanet, J.; Rialp, J. Disentangling the relationship between internationalization, incremental and radical innovation, and firm performance. Glob. Strateg. J. 2021, 12, 57–81. [Google Scholar] [CrossRef]

- Ismail, M.; Bello-Pintado, A.; Garcia-Marco, T. How many to be different? The role of number and the partner type on innovation performance. Innov-Organ. Manag. 2022. ahead-of-print. [Google Scholar] [CrossRef]

- Shu, C.; Zhou, K.; Xiao, Y. How green management influences product innovation in China: The role of institutional benefits. J. Bus. Ethics. 2016, 133, 471–485. [Google Scholar] [CrossRef]

- Byun, S.K.; Oh, J.M.; Xia, H. Incremental vs. breakthrough innovation: The role of technology spillovers. Manag. Sci. 2021, 67, 1779–1802. [Google Scholar] [CrossRef]

- Feng, Y.; Wang, X.; Du, W.; Wu, H.; Wang, J. Effects of environmental regulation and FDI on urban innovation in China: A spatial Durbin econometric analysis. J. Clean. Prod. 2019, 235, 210–224. [Google Scholar] [CrossRef]

- Wang, C.; Qi, T.; Lin, S. A Summary of the research on natural resource assets departure audit on leading cadres. IOP Conf. Ser. Earth Environ. Sci. 2020, 555, 012096. [Google Scholar] [CrossRef]

- Yan, B.; Wu, L.; Wang, X.; Wu, J. How can environmental intervention work during rapid urbanization? Examining the moderating effect of environmental performance–based accountability in China. Environ. Impact Assess. Rev. 2021, 86, 106476. [Google Scholar] [CrossRef]

- Xie, R.; Yuan, Y.; Huang, J. Different types of environmental regulations and heterogeneous influence on “green” productivity: Evidence from China. Ecol. Econ. 2017, 132, 104–112. [Google Scholar] [CrossRef]

- Patriarca, R.; Di Gravio, G.; Costantino, F.; Tronci, M. The functional resonance analysis method for a systemic risk based environmental auditing in a sinter plant: A semi-quantitative approach. Ecol. Econ. 2017, 63, 72–86. [Google Scholar] [CrossRef]

- Xiong, H.; Li, Y.; He, J. Construction and Application of the Evaluation System of Natural Resources Asset Accountability Audit of Officials: A Case Study of Jiangxi, China. Sustainability 2022, 14, 528. [Google Scholar] [CrossRef]

- Liao, X.; Shi, X. Public appeal, environmental regulation, and green investment: Evidence from China. Energy Pol. 2018, 119, 554–562. [Google Scholar] [CrossRef]

- Yang, L.; Qin, H.; Gan, Q.; Su, J. Internal control quality, enterprise environmental protection investment, and finance performance: An empirical study of China’s A-share heavy pollution industry. Int. J. Environ. Res. Public Health 2020, 17, 6082. [Google Scholar] [CrossRef]

- Palmer, K.; Oates, W.E.; Portney, P.R. Tightening environmental standards: The benefit–cost or the no–cost paradigm? J. Econ. Perspect. 1995, 9, 119–132. [Google Scholar] [CrossRef]

- Porter, M.E.; van der Linde, C. Toward a new conception of the environment competitiveness relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef]

- Jaffe, A.B.; Palmer, K. Environmental regulation and innovation: A panel data study. Rev. Econ. Stat. 1997, 79, 610–619. [Google Scholar] [CrossRef]

- Du, L.; Lin, W.; Du, J.; Jin, M.; Fan, M. Can vertical environmental regulation induce enterprise green innovation? A new perspective from automatic air quality monitoring station in China. J. Environ. Manag. 2022, 317, 115349. [Google Scholar] [CrossRef] [PubMed]

- Du, K.; Cheng, Y.; Yao, X. Environmental regulation, green technology innovation, and industrial structure upgrading: The road to the green transformation of Chinese cities. Energy Econ. 2021, 98, 105247. [Google Scholar] [CrossRef]

- Huang, C.; Wang, Q.; Wang, S.; Ren, M.; Ma, R.; He, Y. Air pollution Prevention and control policy in China. Adv. Exp. Med. Biol. 2017, 1017, 243–261. [Google Scholar] [CrossRef] [PubMed]

- Li, D.; Zheng, M.; Cao, C.; Chen, X.; Ren, S.; Huang, M. The impact of legitimacy pressure and corporate profitability on green innovation: Evidence from China top 100. J. Clean. Prod. 2017, 141, 41–49. [Google Scholar] [CrossRef]

- Xie, X.; Huo, J.; Zou, H. Green process innovation, green product innovation, and corporate financial performance: A content analysis method. J. Bus. Res. 2019, 101, 697–706. [Google Scholar] [CrossRef]

- Balsmeier, B.; Fleming, L.; Manso, G. Independent boards and innovation. J. Financ. Econ. 2017, 123, 536–557. [Google Scholar] [CrossRef]

- Gao, H.; Hsu, P.H.; Li, K. Innovation strategy of private firms. J. Financ. Quant. Anal. 2018, 53, 1–32. [Google Scholar] [CrossRef]

- Chen, X.; Zhang, J.; Zeng, H. Is corporate environmental responsibility synergistic with governmental environmental responsibility? Evidence from China. Bus. Strat. Env. 2020, 29, 3669–3686. [Google Scholar] [CrossRef]

- Zhang, Y.; Wang, J.; Xue, Y.; Yang, J. Impact of environmental regulations on green technological innovative behavior: An empirical study in China. J. Clean. Prod. 2018, 188, 763–773. [Google Scholar] [CrossRef]

- Zhang, Y.; Peng, Y.; Ma, C.; Shen, B. Can environmental innovation facilitate carbon emissions reduction? Evidence from China. Energy Pol. 2017, 100, 18–28. [Google Scholar] [CrossRef]

- Xu, H.; Qiu, L.; Liu, B.; Liu, B.; Wang, H.; Lin, W. Does regional planning policy of Yangtze River Delta improve green technology innovation? Evidence from a quasi–natural experiment in China. Environ. Sci. Pollut. Control Ser. 2021, 28, 62321–62337. [Google Scholar] [CrossRef] [PubMed]

- González-Benito, J.; González-Benito, Ó. A study of determinant factors of stakeholder environmental pressure perceived by industrial companies. Bus. Strat. Env. 2010, 19, 164–181. [Google Scholar] [CrossRef]

- Hart, S.L. A Natural-Resource-Based View of the Firm. Acad. Manag. Rev. 1995, 20, 986–1014. [Google Scholar] [CrossRef]

- Du, X.; Chang, Y.; Zeng, Q.; Du, Y.; Pei, H. Corporate environmental responsibility (CER) weakness, media coverage, and corporate philanthropy: Evidence from China. Asia. Pac. J. Manag. 2016, 33, 551–581. [Google Scholar] [CrossRef]

- Issa, J.S.; Abbaszadeh, M.R.; Salehi, M. The Impact of Islamic Banking Corporate Governance on Green Banking. Adm. Sci. 2022, 12, 190. [Google Scholar] [CrossRef]

- Lee, J.W.; Kim, Y.M.; Kim, Y.E. Antecedents of adopting corporate environmental responsibility and green practices. J. Bus. Ethics. 2018, 148, 397–409. [Google Scholar] [CrossRef]

- Zhao, X.; Yin, H.; Zhao, Y. Impact of environmental regulations on the efficiency and CO2 emissions of power plants in China. Appl. Energy 2015, 149, 238–247. [Google Scholar] [CrossRef]

- Kang, Y.; He, X. Institutional forces and environmental management strategy: Moderating effects of environmental orientation and innovation capability. Manag. Organ. Rev. 2018, 14, 577–605. [Google Scholar] [CrossRef]

- Testa, F.; Iraldo, F.; Frey, M. The effect of environmental regulation on firms’ competitive performance: The case of the building and construction sector in some EU regions. J. Environ. Manag. 2011, 92, 2136–2144. [Google Scholar] [CrossRef]

- Sun, H.; Edziah, B.K.; Sun, C.; Kporsu, A.K. Institutional quality, green innovation, and energy efficiency. Energy Pol. 2019, 135, 111002. [Google Scholar] [CrossRef]

- Howell, S.T. Financing innovation: Evidence from R&D grants. Am. Econ. Rev. 2017, 107, 1136–1164. [Google Scholar] [CrossRef]

- Li, X.; Shao, X.; Chang, T.; Albu, L.L. Does digital finance promote the green innovation of China’s listed companies? Energy Econ. 2022, 114, 106254. [Google Scholar] [CrossRef]

- Wang, F.; Feng, L.; Wang, L. Environmental regulation, tenure length of officials, and green innovation of enterprises. Int. J. Environ. Res. Public Health 2020, 17, 2284. [Google Scholar] [CrossRef] [PubMed]

- Hart, S.L.; Ahuja, G. Does it pay to be green? An empirical examination of the relationship between emission reduction and firm performance. Bus. Strat. Environ. 1996, 5, 30–37. [Google Scholar] [CrossRef]

- Zhang, S.; Zhang, M.A.; Qiao, Y.; Li, X.; Li, S. Does improvement of environmental information transparency boost firms’ green innovation? Evidence from the air quality monitoring and disclosure program in China. J. Clean. Prod. 2022, 357, 131921. [Google Scholar] [CrossRef]

- Dai, J.; Cui, J.; Zhao, X. Does environmental regulation induce green innovation? Evidence from Chinese listed firms. Acad. Manag. Ann. 2020, 1, 12378. [Google Scholar] [CrossRef]

- Qi, G.; Jia, Y.; Zou, H. Is institutional pressure the mother of green innovation? Examining the moderating effect of absorptive capacity. J. Clean. Prod. 2021, 278, 123957. [Google Scholar] [CrossRef]

- Bendig, D.; Kleine-Stegemann, L.; Schulz, C.; Eckardt, D. The effect of green startup investments on incumbents’ green innovation output. J. Clean. Prod. 2022, 376, 134316. [Google Scholar] [CrossRef]

- Chen, Y.; Yao, Z.; Zhong, K. Do environmental regulations of carbon emissions and air pollution foster green technology innovation: Evidence from China’s prefecture-level cities. J. Clean. Prod. 2022, 350, 131537. [Google Scholar] [CrossRef]

- Cheng, C.; Li, S.; Liu, S.; Zhang, S. Origin matters: The institution imprint effect and green innovation in family businesses. Financ. Res. Lett. 2022, 50, 103324. [Google Scholar] [CrossRef]

- Sun, Y.; Razzaq, A.; Sun, H.; Irfan, M. The asymmetric influence of renewable energy and green innovation on carbon neutrality in China: Analysis from nonlinear ARDL model. Renew. Energy 2022, 193, 334–343. [Google Scholar] [CrossRef]

- Belderbos, R.; Faems, D.; Leten, B.; Looy, B.V. Technological activities and their impact on the financial performance of the firm: Exploitation and exploration within and between firms. J. Prod. Innovat. Manag. 2010, 27, 869–882. [Google Scholar] [CrossRef]

- Wagner, M. On the relationship between environmental management, environmental innovation and patenting: Evidence from German manufacturing firms. Res. Policy 2007, 36, 1587–1602. [Google Scholar] [CrossRef]

- Chen, L.; Liu, S.; Liu, X.; Wang, J. The carbon emissions trading scheme and corporate environmental investments: A Quasinatural experiment from China. Emerg. Mark. Financ. Trade 2022, 58, 2670–2681. [Google Scholar] [CrossRef]

- Santoro, G.; Bresciani, S.; Papa, A. Collaborative modes with cultural and creative industries and innovation performance: The moderating role of heterogeneous sources of knowledge and absorptive capacity. Technova 2020, 92, 102040. [Google Scholar] [CrossRef]

- Huang, L.; Wang, C.; Chin, T.; Huang, J.; Cheng, X. Technological knowledge coupling and green innovation in manufacturing firms: Moderating roles of mimetic pressure and environmental identity. Int. J. Prod. Econ. 2022, 248, 108482. [Google Scholar] [CrossRef]

- Frondel, M.; Horbach, J.; Rennings, K. End–of–pipe or cleaner production? An empirical comparison of environmental innovation decisions across OECD countries. Bus. Strat. Environ. 2007, 16, 571–584. [Google Scholar] [CrossRef]

- Kock, C.J.; Santalo, J.; Diestre, L. Corporate governance and the environment: What type of governance creates greener companies? J. Manag. Stud. 2012, 49, 492–514. [Google Scholar] [CrossRef]

- Wolf, J. The relationship between sustainable supply chain management, stakeholder pressure, and corporate sustainability performance. J. Bus. Ethics 2014, 119, 317–328. [Google Scholar] [CrossRef]

- Li, Z.; Si, X.; Zhang, W.; Feng, Z.; Li, T.; Guo, Y. Official tenure and governance effectiveness of China’s basic pension insurance system: An inverted U–shaped curve. Front. Public Health 2022, 10, 975459. [Google Scholar] [CrossRef]

- Deng, Z.; Hofman, P.S.; Newman, A. Ownership concentration and product innovation in Chinese private SMEs. Asia Pac. J. Manag. 2013, 30, 717–734. [Google Scholar] [CrossRef]

- De Marchi, V.; Cainelli, G.; Grandinetti, R. Multinational subsidiaries and green innovation. Int. Bus. Rev. 2022, 31, 102027. [Google Scholar] [CrossRef]

- He, F.; Yan, Y.; Hao, J.; Wu, J.G. Retail investor attention and corporate green innovation: Evidence from China. Energy Econ. 2022, 115, 106308. [Google Scholar] [CrossRef]

- Usman, M.; Javed, M.; Yin, J. Board internationalization and green innovation. Econ. Lett. 2020, 197, 109625. [Google Scholar] [CrossRef] [PubMed]

- Shipman, J.E.; Swanquist, Q.T.; Whited, R.L. Propensity score matching in accounting research. Account. Rev. 2017, 92, 213–244. [Google Scholar] [CrossRef]

- Atanasov, V.; Black, B. The trouble with instruments: The need for pretreatment balance in shock–based instrumental Variables designs. Manag. Sci. 2021, 67, 1270–1302. [Google Scholar] [CrossRef]

- Hong, Q.; Cui, L.; Hong, P. The impact of carbon emissions trading on energy efficiency: Evidence from quasi–experiment in China’s carbon emissions trading pilot. Energy Econ. 2022, 110, 106025. [Google Scholar] [CrossRef]

- Rosenbaum, P.R.; Rubin, D.B. The central role of the propensity score in observational studies for causal effects. Biometrika 1983, 70, 41–55. [Google Scholar] [CrossRef]

- Hainmueller, J. Entropy balancing for causal effects: A multivariate reweighting method to produce balanced samples in observational studies. Polit. Anal. 2012, 20, 25–46. [Google Scholar] [CrossRef]

- McMullin, J.; Schonberger, B. When good balance goes bad: A discussion of common pitfalls when using entropy balancing. J. Financ. Rep. 2022, 7, 167–196. [Google Scholar] [CrossRef]

- Zhu, Y.; Sun, Z.; Zhang, S.; Wang, X. Economic policy uncertainty, environmental regulation, and green innovation—An empirical study based on Chinese high-tech enterprises. Int. J. Environ. Res. Public Health 2021, 18, 9503. [Google Scholar] [CrossRef] [PubMed]

- Xia, L.; Gao, S.; Wei, J.; Ding, Q. Government subsidy and corporate green innovation—Does board governance play a role? Energy Pol. 2022, 161, 112720. [Google Scholar] [CrossRef]

- Fang, Z.; Kong, X.; Sensoy, A.; Cui, X.; Cheng, F. Government’s awareness of environmental protection and corporate green innovation: A natural experiment from the new environmental protection law in China. Econ. Anal. Policy 2021, 70, 294–312. [Google Scholar] [CrossRef]

- Chen, F.; Wang, M.; Pu, Z. The impact of technological innovation on air pollution: Firm–level evidence from China. Technol. Forecast. Soc. 2022, 177, 121521. [Google Scholar] [CrossRef]

- Wu, H.; Li, Y.; Hao, Y.; Ren, S.; Zhang, P. Environmental decentralization, local government competition, and regional green development: Evidence from China. Sci. Total Environ. 2020, 708, 135085. [Google Scholar] [CrossRef] [PubMed]

- Chen, Z.; Kahn, M.E.; Liu, Y.; Wang, Z. The consequences of spatially differentiated water pollution regulation in China. J. Environ. Econ. Manag. 2018, 88, 468–485. [Google Scholar] [CrossRef]

- Wu, H.; Guo, H.; Zhang, B.; Bu, M. Westward movement of new polluting firms in China: Pollution reduction mandates and location choice. J. Comp. Econ. 2017, 45, 119–138. [Google Scholar] [CrossRef]

- Kao, W.C. Innovation quality of firms with the research and development tax credit. Rev. Quant. Financ. ACC 2018, 51, 43–78. [Google Scholar] [CrossRef]

- Liu, M.; Li, Y. Environmental regulation and green innovation: Evidence from China’s carbon emissions trading policy. Financ. Res. Lett. 2022, 48, 103051. [Google Scholar] [CrossRef]

- Hu, J.; Pan, X.; Huang, Q. Quantity or quality? The impacts of environmental regulation on firms’ innovation—Quasi–natural experiment based on China’s carbon emissions trading pilot. Technol. Forecast. Soc. 2020, 158, 120122. [Google Scholar] [CrossRef]

- Guceri, I. Will the real R&D employees please stand up? Effects of tax breaks on firm–level outcomes. Int. Tax. Public Financ. 2018, 25, 1–63. [Google Scholar] [CrossRef]

- Guo, Y.; Xia, X.; Zhang, S.; Zhang, D. Environmental regulation, government R&D funding, and green technology innovation: Evidence from China provincial data. Sustainability 2018, 10, 940. [Google Scholar] [CrossRef]

- Huang, Z. Whether tax preference promotes innovation in enterprises? Mod. Econ. 2019, 10, 371. [Google Scholar] [CrossRef]

- He, J.; Tian, X. Do Short Sellers Exacerbate or Mitigate Managerial Myopia? Evidence from Patenting Activities; University of Georgia work: Athens, GA, USA, 2016. [Google Scholar] [CrossRef]

- He, J.J.; Tian, X. The dark side of analyst coverage: The case of innovation. J. Financ. Econ. 2013, 109, 856–878. [Google Scholar] [CrossRef]

- Guo, B.; Pérez-Castrillo, D.; Toldrà-Simats, A. Firms’ innovation strategy under the shadow of analyst coverage. J. Financ. Econ. 2019, 131, 456–483. [Google Scholar] [CrossRef]

- Li, D.; Shen, W. Can corporate digitalization promote green innovation? The moderating roles of internal control and institutional ownership. Sustainability 2021, 13, 13983. [Google Scholar] [CrossRef]

- Belev, B. Institutional investors in Bulgarian corporate governance reform: Obstacles or facilitators? J. World. Bus. 2003, 38, 361–374. [Google Scholar] [CrossRef]

- Romer, P.M. Endogenous technological change. J. Polit. Econ. 1990, 98, S71–S102. [Google Scholar] [CrossRef]

- Romer, P.M. Increasing returns and long-run growth. J. Polit. Econ. 1986, 94, 1002–1037. [Google Scholar] [CrossRef] [Green Version]

- Kim, T.H.; Kim, B. Firm’s environmental expenditure, R&D intensity, and profitability. Sustainability 2018, 10, 2071. [Google Scholar] [CrossRef]

- Triguero, Á.; Cuerva, M.C.; Álvarez-Aledo, C. Environmental innovation and employment: Drivers and synergies. Sustainability 2017, 9, 2057. [Google Scholar] [CrossRef]

- Ramanathan, R.; He, Q.; Black, A.; Ghobadian, A.; Gallear, D. Environmental regulations, innovation and firm performance: A revisit of the Porter hypothesis. J. Clean. Prod. 2017, 155, 79–92. [Google Scholar] [CrossRef]

- Ramanathan, R.; Ramanathan, U.; Bentley, Y. The debate on flexibility of environmental regulations, innovation capabilities, and financial performance—A novel use of DEA. Omega 2018, 75, 131–138. [Google Scholar] [CrossRef]

- Filbeck, G.; Gorman, R.F. The relationship between the environmental and financial performance of public utilities. Environ. Resour. Econ. 2004, 29, 137–157. [Google Scholar] [CrossRef]

- Sun, W.; Zhao, C.; Wang, Y.; Cho, C.H. Corporate social responsibility disclosure and catering to investor sentiment in China. Manag. Decis. 2018, 56, 1917–1935. [Google Scholar] [CrossRef]

- Ali, W.; Wilson, J.; Husnain, M. Determinants/motivations of corporate social responsibility disclosure in developing economies: A survey of the extant literature. Sustainability 2022, 14, 3474. [Google Scholar] [CrossRef]

- Garde Sánchez, R.; Rodríguez Bolívar, M.P.; López Hernández, A.M. Corporate and managerial characteristics as drivers of social responsibility disclosure by state–owned enterprises. Rev. Manag. Sci. 2017, 11, 633–659. [Google Scholar] [CrossRef]

- Hussainey, K.; Achek, I. The effect of national culture on the association between profitability and corporate social and environmental disclosure: A meta–analysis. Meditari. Account. Res. 2015, 23, 296–321. [Google Scholar] [CrossRef] [Green Version]

| Initial Sample of A-Share Listed Firms, 2010–2017 | 21,366 | |

|---|---|---|

| Observations from ST/PT firms | (985) | |

| Observations from financial and insurance firms | (389) | |

| Observations from cross-listed firms | (1166) | |

| Observations with missing data for the control variables in the main test | (2037) | |

| Final sample | 16,789 |

| Variable | Sample Size | Mean | Standard Deviation | Minimum Value | 25th | Maximum Value | 75th | Max |

|---|---|---|---|---|---|---|---|---|

| TECH_ PROXIMITY | 16,789 | 0.068 | 0.231 | 0.000 | 0.000 | 0.000 | 0.000 | 1.040 |

| KNOWN | 16,789 | 0.215 | 0.648 | 0.000 | 0.000 | 0.000 | 0.000 | 3.296 |

| UNKNOWN | 16,789 | 0.156 | 0.455 | 0.000 | 0.000 | 0.000 | 0.000 | 2.197 |

| SIZE | 16,789 | 22.008 | 1.166 | 19.722 | 21.157 | 21.877 | 22.717 | 25.401 |

| LEV | 16,789 | 0.572 | 0.212 | 0.103 | 0.408 | 0.580 | 0.745 | 0.952 |

| ROA | 16,789 | 0.039 | 0.050 | −0.155 | 0.014 | 0.036 | 0.065 | 0.187 |

| BM | 16,789 | 0.574 | 0.233 | 0.110 | 0.393 | 0.571 | 0.753 | 1.061 |

| GROWTH | 16,789 | 0.212 | 0.476 | −0.542 | −0.009 | 0.126 | 0.302 | 3.133 |

| TANG | 16,789 | 0.220 | 0.164 | 0.002 | 0.093 | 0.186 | 0.314 | 0.709 |

| INTANG | 16,789 | 0.046 | 0.049 | 0.000 | 0.016 | 0.034 | 0.058 | 0.304 |

| EMENUM | 16,789 | 7.570 | 1.213 | 4.290 | 6.778 | 7.541 | 8.368 | 10.636 |

| AGE | 16,789 | 2.773 | 0.349 | 1.609 | 2.565 | 2.833 | 2.996 | 3.401 |

| FGNSALE | 16,789 | 0.120 | 0.202 | 0.000 | 0.000 | 0.009 | 0.157 | 0.875 |

| TOP | 16,789 | 0.350 | 0.151 | 0.088 | 0.231 | 0.330 | 0.452 | 0.750 |

| INDB | 16,789 | 0.373 | 0.053 | 0.333 | 0.333 | 0.333 | 0.429 | 0.571 |

| SEG | 16,789 | 0.021 | 0.012 | 0.000 | 0.016 | 0.023 | 0.029 | 0.048 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Variable | TECH_PROXIMITY | KNOWN | UNKNOWN |

| POST | 0.016 *** | 0.046 *** | −0.006 |

| (2.59) | (2.95) | (−0.46) | |

| SIZE | 0.019 *** | 0.070 *** | 0.051 *** |

| (2.76) | (3.69) | (3.23) | |

| LEV | −0.025 | −0.070 | 0.005 |

| (−1.32) | (−1.44) | (0.12) | |

| ROA | 0.020 | −0.028 | 0.164 |

| (0.44) | (−0.25) | (1.48) | |

| BM | 0.018 | 0.021 | 0.007 |

| (1.11) | (0.53) | (0.18) | |

| GROWTH | −0.009 *** | −0.032 *** | −0.016 ** |

| (−3.17) | (−4.47) | (−2.26) | |

| TANG | 0.005 | 0.100 | 0.011 |

| (0.23) | (1.59) | (0.20) | |

| INTANG | 0.060 | 0.153 | −0.254 * |

| (0.84) | (0.93) | (−1.70) | |

| EMENUM | 0.007 | 0.017 | 0.011 |

| (1.60) | (1.55) | (1.25) | |

| AGE | 0.025 | 0.156 | −0.009 |

| (0.62) | (1.37) | (−0.11) | |

| FGNSALE | 0.024 | 0.037 | −0.095 * |

| (1.06) | (0.67) | (−1.95) | |

| TOP | −0.009 | −0.136 | −0.039 |

| (−0.28) | (−1.55) | (−0.56) | |

| INDB | 0.047 | 0.022 | 0.087 |

| (0.86) | (0.16) | (0.73) | |

| SEG | 0.019 | −0.163 | −1.106 * |

| (0.07) | (−0.22) | (−1.80) | |

| Constant | −0.502 *** | −1.857 *** | −1.006 *** |

| (−2.94) | (−4.03) | (−2.66) | |

| FirmFE | Yes | Yes | Yes |

| InduFE | Yes | Yes | Yes |

| YearFE | Yes | Yes | Yes |

| CityFE | Yes | Yes | Yes |

| N | 16,789 | 16,789 | 16,789 |

| Adj. R2 | 0.478 | 0.596 | 0.137 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Variable | TECH_PROXIMITY | KNOWN | UNKNOWN |

| BEFORE2 | −0.006 | 0.010 | −0.004 |

| (−0.98) | (0.74) | (−0.30) | |

| BEFORE1 | 0.005 | 0.029 | 0.002 |

| (0.71) | (1.60) | (0.11) | |

| CURRENT | 0.021 ** | 0.074 *** | −0.005 |

| (2.44) | (3.33) | (−0.24) | |

| AFTER1 | 0.021 ** | 0.071 *** | −0.010 |

| (2.03) | (2.60) | (−0.45) | |

| AFTER2 | 0.022 | 0.098 *** | 0.032 |

| (1.61) | (2.74) | (1.00) | |

| AFTER3 | 0.022 | 0.154 ** | −0.007 |

| (0.95) | (2.24) | (−0.14) | |

| SIZE | 0.019 *** | 0.069 *** | 0.050 *** |

| (2.74) | (3.63) | (3.20) | |

| LEV | −0.025 | −0.071 | 0.005 |

| (−1.32) | (−1.47) | (0.13) | |

| ROA | 0.020 | −0.024 | 0.165 |

| (0.45) | (−0.22) | (1.49) | |

| BM | 0.018 | 0.022 | 0.006 |

| (1.09) | (0.53) | (0.16) | |

| GROWTH | −0.009 *** | −0.031 *** | −0.015 ** |

| (−3.16) | (−4.39) | (−2.15) | |

| TANG | 0.006 | 0.103 | 0.012 |

| (0.25) | (1.64) | (0.21) | |

| INTANG | 0.058 | 0.152 | −0.258 * |

| (0.81) | (0.92) | (−1.74) | |

| EMENUM | 0.007 | 0.017 | 0.011 |

| (1.59) | (1.53) | (1.24) | |

| AGE | 0.028 | 0.170 | −0.007 |

| (0.67) | (1.49) | (−0.08) | |

| FGNSALE | 0.023 | 0.034 | −0.096 * |

| (1.03) | (0.61) | (−1.95) | |

| TOP | −0.009 | −0.134 | −0.040 |

| (−0.26) | (−1.53) | (−0.56) | |

| INDB | 0.049 | 0.029 | 0.087 |

| (0.90) | (0.21) | (0.74) | |

| SEG | 0.018 | −0.149 | −1.092 * |

| (0.07) | (−0.20) | (−1.77) | |

| Constant | −0.509 *** | −1.890 *** | −1.001 *** |

| (−2.97) | (−4.09) | (−2.65) | |

| FirmFE | Yes | Yes | Yes |

| InduFE | Yes | Yes | Yes |

| YearFE | Yes | Yes | Yes |

| CityFE | Yes | Yes | Yes |

| N | 16,789 | 16,789 | 16,789 |

| Adj. R2 | 0.478 | 0.596 | 0.137 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Variable | TECH_PROXIMITY | KNOWN | UNKNOWN |

| POST | 0.016 *** | 0.047 *** | −0.006 |

| (2.59) | (2.99) | (−0.46) | |

| SIZE | 0.020 *** | 0.071 *** | 0.051 *** |

| (2.77) | (3.71) | (3.23) | |

| LEV | −0.025 | −0.069 | 0.005 |

| (−1.31) | (−1.41) | (0.13) | |

| ROA | 0.020 | −0.032 | 0.165 |

| (0.44) | (−0.29) | (1.49) | |

| BM | 0.018 | 0.020 | 0.007 |

| (1.12) | (0.49) | (0.19) | |

| GROWTH | −0.009 *** | −0.032 *** | −0.016 ** |

| (−3.19) | (−4.48) | (−2.27) | |

| TANG | 0.005 | 0.100 | 0.011 |

| (0.23) | (1.58) | (0.20) | |

| INTANG | 0.060 | 0.153 | −0.254 * |

| (0.84) | (0.93) | (−1.70) | |

| EMENUM | 0.007 | 0.017 | 0.012 |

| (1.58) | (1.54) | (1.25) | |

| AGE | 0.025 | 0.155 | −0.011 |

| (0.60) | (1.36) | (−0.12) | |

| FGNSALE | 0.024 | 0.037 | −0.095 * |

| (1.06) | (0.68) | (−1.95) | |

| TOP | −0.009 | −0.131 | −0.041 |

| (−0.28) | (−1.49) | (−0.58) | |

| INDB | 0.046 | 0.019 | 0.087 |

| (0.85) | (0.14) | (0.73) | |

| SEG | 0.021 | −0.152 | −1.105 * |

| (0.08) | (−0.21) | (−1.79) | |

| Constant | −0.503 *** | −1.867 *** | −1.004 *** |

| (−2.94) | (−4.05) | (−2.65) | |

| FirmFE | Yes | Yes | Yes |

| InduFE | Yes | Yes | Yes |

| YearFE | Yes | Yes | Yes |

| CityFE | Yes | Yes | Yes |

| N | 16,779 | 16,779 | 16,779 |

| Adj. R2 | 0.478 | 0.596 | 0.137 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Variable | TECH_PROXIMITY | KNOWN | UNKNOWN |

| POST | 0.020 *** | 0.059 *** | −0.003 |

| (2.99) | (3.23) | (−0.19) | |

| SIZE | 0.028 *** | 0.086 *** | 0.043 ** |

| (3.37) | (3.87) | (2.25) | |

| LEV | −0.045 ** | −0.097 * | −0.016 |

| (−2.29) | (−1.88) | (−0.31) | |

| ROA | 0.019 | 0.053 | 0.066 |

| (0.37) | (0.42) | (0.42) | |

| BM | 0.023 | 0.040 | 0.002 |

| (1.18) | (0.83) | (0.04) | |

| GROWTH | −0.012 *** | −0.035 *** | −0.012 |

| (−4.04) | (−4.03) | (−1.36) | |

| TANG | 0.035 | 0.142 * | 0.004 |

| (1.21) | (1.88) | (0.06) | |

| INTANG | 0.114 | 0.246 | −0.336 ** |

| (1.19) | (1.11) | (−1.97) | |

| EMENUM | 0.003 | 0.011 | 0.023 * |

| (0.47) | (0.88) | (1.80) | |

| AGE | 0.014 | 0.153 | −0.077 |

| (0.37) | (1.30) | (−0.68) | |

| FGNSALE | 0.028 | 0.059 | −0.071 |

| (1.14) | (0.93) | (−1.15) | |

| TOP | −0.014 | −0.174 * | −0.067 |

| (−0.43) | (−1.66) | (−0.72) | |

| INDB | 0.017 | −0.110 | 0.163 |

| (0.30) | (−0.80) | (1.08) | |

| SEG | −0.369 | −0.974 | −1.748 ** |

| (−1.11) | (−1.02) | (−2.00) | |

| Constant | −0.602 *** | −2.087 *** | −0.722 |

| (−3.14) | (−4.20) | (−1.44) | |

| FirmFE | Yes | Yes | Yes |

| InduFE | Yes | Yes | Yes |

| YearFE | Yes | Yes | Yes |

| CityFE | Yes | Yes | Yes |

| N | 16,789 | 16,789 | 16,789 |

| Adj. R2 | 0.492 | 0.608 | 0.143 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Variable | TECH_PROXIMITY | KNOWN | UNKNOWN |

| POST | 0.022 ** | 0.046 ** | 0.005 |

| (2.40) | (2.00) | (0.24) | |

| SIZE | 0.021 * | 0.101 *** | 0.072 *** |

| (1.68) | (2.99) | (2.81) | |

| LEV | −0.006 | 0.050 | −0.002 |

| (−0.16) | (0.56) | (−0.02) | |

| ROA | −0.011 | −0.234 | 0.313 * |

| (−0.15) | (−1.17) | (1.84) | |

| BM | 0.041 | 0.036 | −0.031 |

| (1.61) | (0.55) | (−0.53) | |

| GROWTH | −0.010 ** | −0.029 ** | −0.017 * |

| (−1.98) | (−2.25) | (−1.69) | |

| TANG | 0.029 | 0.128 | 0.056 |

| (0.72) | (1.16) | (0.63) | |

| INTANG | 0.116 | 0.289 | −0.131 |

| (0.98) | (1.02) | (−0.60) | |

| EMENUM | 0.017 ** | 0.035 * | 0.015 |

| (2.16) | (1.84) | (1.12) | |

| AGE | 0.012 | 0.054 | −0.124 |

| (0.19) | (0.33) | (−0.99) | |

| FGNSALE | 0.011 | 0.031 | −0.166 * |

| (0.27) | (0.32) | (−1.89) | |

| TOP | −0.109 * | −0.399 ** | −0.243 ** |

| (−1.86) | (−2.43) | (−1.97) | |

| INDB | 0.043 | −0.031 | 0.278 |

| (0.49) | (−0.15) | (1.54) | |

| SEG | −0.071 | −0.611 | −1.693 * |

| (−0.18) | (−0.56) | (−1.92) | |

| Constant | −0.568 * | −2.337 *** | −1.166 * |

| (−1.94) | (−2.82) | (−1.87) | |

| FirmFE | Yes | Yes | Yes |

| InduFE | Yes | Yes | Yes |

| YearFE | Yes | Yes | Yes |

| CityFE | Yes | Yes | Yes |

| N | 7824 | 7824 | 7824 |

| Adj. R2 | 0.487 | 0.632 | 0.134 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Variable | TECH_PROXIMITY | KNOWN | UNKNOWN |

| POST | 0.027 *** | 0.071 *** | −0.009 |

| (3.59) | (3.67) | (−0.51) | |

| SIZE | 0.023 *** | 0.074 *** | 0.058 *** |

| (2.65) | (3.31) | (3.11) | |

| LEV | −0.024 | −0.053 | 0.022 |

| (−1.09) | (−0.96) | (0.47) | |

| ROA | 0.024 | −0.044 | 0.219 * |

| (0.46) | (−0.35) | (1.81) | |

| BM | 0.021 | 0.038 | −0.001 |

| (1.15) | (0.83) | (−0.02) | |

| GROWTH | −0.012 *** | −0.040 *** | −0.017 ** |

| (−3.37) | (−4.81) | (−2.08) | |

| TANG | 0.001 | 0.069 | 0.010 |

| (0.04) | (0.97) | (0.16) | |

| INTANG | 0.097 | 0.250 | −0.420 ** |

| (1.07) | (1.25) | (−2.36) | |

| EMENUM | 0.011 * | 0.036 ** | 0.018 |

| (1.87) | (2.49) | (1.54) | |

| AGE | −0.000 | 0.054 | −0.041 |

| (−0.00) | (0.44) | (−0.45) | |

| FGNSALE | 0.041 | 0.076 | −0.057 |

| (1.46) | (1.18) | (−1.02) | |

| TOP | −0.005 | −0.159 | −0.051 |

| (−0.13) | (−1.61) | (−0.65) | |

| INDB | 0.078 | 0.053 | 0.237 * |

| (1.25) | (0.36) | (1.78) | |

| SEG | −0.028 | −0.425 | −1.916 *** |

| (−0.09) | (−0.51) | (−2.72) | |

| Constant | −0.552 *** | −1.815 *** | −1.174 *** |

| (−2.77) | (−3.46) | (−2.67) | |

| FirmFE | Yes | Yes | Yes |

| InduFE | Yes | Yes | Yes |

| YearFE | Yes | Yes | Yes |

| CityFE | Yes | Yes | Yes |

| N | 13,396 | 13,396 | 13,396 |

| Adj. R2 | 0.464 | 0.581 | 0.108 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Variable | TECH_PROXIMITY | KNOWN | UNKNOWN |

| POST | 0.027 *** | 0.068 *** | −0.016 |

| (3.39) | (3.32) | (−0.88) | |

| LNGDP_PC | −0.007 | 0.018 | −0.028 |

| (−0.57) | (0.64) | (−1.01) | |

| LNPOPULATION | 0.066 | 0.208 | −0.092 |

| (1.10) | (1.19) | (−0.67) | |

| DEFICIT | 0.005 | 0.020 | 0.032 |

| (0.11) | (0.17) | (0.29) | |

| MKT | −0.014 * | −0.025 | 0.006 |

| (−1.74) | (−1.39) | (0.38) | |

| LNCO2 | −0.016 | −0.001 | −0.008 |

| (−1.05) | (−0.03) | (−0.24) | |

| LNIWW | 0.011 | 0.047 * | 0.019 |

| (0.99) | (1.80) | (0.87) | |

| LNSO2 | −0.006 | −0.019 | −0.003 |

| (−0.79) | (−1.09) | (−0.17) | |

| LNISD | −0.007 | −0.023 * | 0.007 |

| (−1.24) | (−1.83) | (0.58) | |

| Constant | −0.577 | −2.980 ** | −0.941 |

| (−1.31) | (−2.53) | (−0.83) | |

| Controls | Yes | Yes | Yes |

| FirmFE | Yes | Yes | Yes |

| InduFE | Yes | Yes | Yes |

| YearFE | Yes | Yes | Yes |

| CityFE | Yes | Yes | Yes |

| N | 11,228 | 11,228 | 11,228 |

| Adj. R2 | 0.476 | 0.596 | 0.110 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Variable | TECH_PROXIMITY | KNOWN | UNKNOWN |

| POST | 0.015 ** | 0.044 *** | −0.006 |

| (2.46) | (2.86) | (−0.41) | |

| POST2*INDU | −0.012 | −0.039 * | 0.019 |

| (−1.51) | (−1.90) | (1.08) | |

| POST3 | −0.003 | −0.003 | −0.000 |

| (−0.36) | (−0.11) | (−0.02) | |

| SIZE | 0.019 *** | 0.068 *** | 0.052 *** |

| (2.67) | (3.57) | (3.31) | |

| LEV | −0.024 | −0.068 | 0.004 |

| (−1.29) | (−1.40) | (0.09) | |

| ROA | 0.024 | −0.014 | 0.157 |

| (0.55) | (−0.12) | (1.41) | |

| BM | 0.020 | 0.027 | 0.004 |

| (1.21) | (0.68) | (0.10) | |

| GROWTH | −0.009 *** | −0.032 *** | −0.016 ** |

| (−3.17) | (−4.47) | (−2.26) | |

| TANG | 0.007 | 0.106 * | 0.008 |

| (0.31) | (1.69) | (0.14) | |

| INTANG | 0.060 | 0.153 | −0.254 * |

| (0.84) | (0.93) | (−1.70) | |

| EMENUM | 0.007 | 0.017 | 0.012 |

| (1.55) | (1.49) | (1.30) | |

| AGE | 0.025 | 0.155 | −0.009 |

| (0.62) | (1.37) | (−0.10) | |

| FGNSALE | 0.023 | 0.035 | −0.094 * |

| (1.03) | (0.64) | (−1.93) | |

| TOP | −0.009 | −0.136 | −0.039 |

| (−0.29) | (−1.55) | (−0.56) | |

| INDB | 0.047 | 0.024 | 0.086 |

| (0.87) | (0.18) | (0.72) | |

| SEG | 0.028 | −0.141 | −1.116 * |

| (0.10) | (−0.19) | (−1.81) | |

| Constant | −0.485 *** | −1.803 *** | −1.033 *** |

| (−2.85) | (−3.91) | (−2.74) | |

| FirmFE | Yes | Yes | Yes |

| InduFE | Yes | Yes | Yes |

| YearFE | Yes | Yes | Yes |

| CityFE | Yes | Yes | Yes |

| N | 16,789 | 16,789 | 16,789 |

| Adj. R2 | 0.478 | 0.596 | 0.137 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Variable | TECH_ PROXIMITY | KNOWN | UNKNOWN | TECH_ PROXIMITY | KNOWN | UNKNOWN |

| Regional Air Pollution (PM2.5) | Environmental Concerns | |||||

| POST | 0.003 | 0.009 | 0.038 | 0.006 | 0.018 | 0.001 |

| (0.24) | (0.32) | (1.12) | (0.79) | (0.97) | (0.07) | |

| POST*AIR | 0.031 * | 0.102 ** | −0.061 | |||

| (1.81) | (2.56) | (−1.53) | ||||

| AIR | 0.003 | 0.009 | 0.038 | |||

| (0.24) | (0.32) | (1.12) | ||||

| POST*EC | 0.022 ** | 0.055 ** | −0.015 | |||

| (2.46) | (2.46) | (−0.72) | ||||

| EC | −0.001 | −0.006 | 0.011 | |||

| (−0.36) | (−0.66) | (1.15) | ||||

| SIZE | 0.012 | 0.063 *** | 0.070 *** | 0.020 *** | 0.074 *** | 0.053 *** |

| (1.25) | (2.58) | (3.16) | (2.82) | (3.83) | (3.28) | |

| LEV | −0.030 | −0.044 | 0.046 | −0.025 | −0.065 | 0.014 |

| (−1.28) | (−0.72) | (0.90) | (−1.26) | (−1.27) | (0.31) | |

| ROA | 0.054 | 0.061 | 0.241 * | 0.012 | −0.066 | 0.142 |

| (0.99) | (0.48) | (1.81) | (0.26) | (−0.57) | (1.25) | |

| BM | 0.036 * | 0.055 | −0.022 | 0.009 | −0.002 | −0.000 |

| (1.82) | (1.16) | (−0.47) | (0.55) | (−0.05) | (−0.01) | |

| GROWTH | −0.009 ** | −0.033 *** | −0.017 ** | −0.009 *** | −0.032 *** | −0.016 ** |

| (−2.33) | (−3.66) | (−2.05) | (−3.11) | (−4.39) | (−2.26) | |

| TANG | 0.008 | 0.095 | −0.040 | −0.002 | 0.088 | −0.003 |

| (0.29) | (1.37) | (−0.62) | (−0.07) | (1.33) | (−0.05) | |

| INTANG | 0.123 | 0.369 * | −0.471 ** | 0.054 | 0.165 | −0.201 |

| (1.17) | (1.76) | (−2.28) | (0.75) | (0.99) | (−1.30) | |

| EMENUM | 0.016 *** | 0.039 *** | 0.009 | 0.008 * | 0.018 | 0.010 |

| (2.78) | (2.78) | (0.67) | (1.67) | (1.60) | (1.05) | |

| AGE | −0.012 | 0.051 | −0.075 | 0.025 | 0.157 | 0.002 |

| (−0.25) | (0.39) | (−0.76) | (0.61) | (1.34) | (0.02) | |

| FGNSALE | 0.021 | −0.003 | −0.021 | 0.020 | 0.017 | −0.093 * |

| (0.69) | (−0.04) | (−0.33) | (0.89) | (0.32) | (−1.85) | |

| TOP | 0.008 | −0.099 | −0.053 | −0.010 | −0.141 | −0.040 |

| (0.19) | (−1.02) | (−0.58) | (−0.30) | (−1.57) | (−0.55) | |

| INDB | 0.063 | −0.069 | 0.390 *** | 0.055 | 0.059 | 0.105 |

| (0.95) | (−0.47) | (2.71) | (0.97) | (0.43) | (0.85) | |

| SEG | 0.239 | −0.381 | −2.250 *** | 0.036 | −0.142 | −1.274 ** |

| (0.74) | (−0.48) | (−2.89) | (0.13) | (−0.19) | (−2.03) | |

| Constant | −0.334 | −1.589 *** | −1.305 *** | −0.518 *** | −1.945 *** | −1.073 *** |

| (−1.54) | (−2.84) | (−2.62) | (−2.96) | (−4.14) | (−2.77) | |

| FirmFE | Yes | Yes | Yes | Yes | Yes | Yes |

| InduFE | Yes | Yes | Yes | Yes | Yes | Yes |

| YearFE | Yes | Yes | Yes | Yes | Yes | Yes |

| CityFE | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 11,227 | 11,227 | 11,227 | 16,218 | 16,218 | 16,218 |

| Adj. R2 | 0.467 | 0.583 | 0.099 | 0.480 | 0.597 | 0.140 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Variable | TECH_ PROXIMITY | KNOWN | UNKNOWN | TECH_ PROXIMITY | KNOWN | UNKNOWN |

| State shareholding ratio | Tax preferences | |||||

| POST | 0.012 * | 0.031 ** | −0.012 | 0.003 | −0.007 | −0.012 |

| (1.86) | (1.98) | (−0.84) | (0.36) | (−0.39) | (−0.72) | |

| POST*SOEP | 0.032 ** | 0.118 *** | 0.046 | |||

| (1.96) | (2.73) | (1.31) | ||||

| SOEP | −0.010 | −0.026 | 0.003 | |||

| (−1.47) | (−1.47) | (0.18) | ||||

| POST*TF | 0.025 ** | 0.102 *** | 0.010 | |||

| (2.56) | (4.13) | (0.45) | ||||

| TF | −0.004 | −0.013 | 0.009 | |||

| (−0.77) | (−0.97) | (0.64) | ||||

| SIZE | 0.020 *** | 0.070 *** | 0.049 *** | 0.020 *** | 0.071 *** | 0.050 *** |

| (2.78) | (3.65) | (3.13) | (2.79) | (3.71) | (3.18) | |

| LEV | −0.025 | −0.076 | −0.003 | −0.024 | −0.067 | 0.006 |

| (−1.31) | (−1.57) | (−0.06) | (−1.28) | (−1.38) | (0.14) | |

| ROA | 0.020 | −0.028 | 0.165 | 0.016 | −0.041 | 0.164 |

| (0.44) | (−0.25) | (1.49) | (0.37) | (−0.36) | (1.48) | |

| BM | 0.018 | 0.019 | 0.003 | 0.017 | 0.017 | 0.006 |

| (1.10) | (0.47) | (0.09) | (1.05) | (0.42) | (0.16) | |

| GROWTH | −0.009 *** | −0.032 *** | −0.016 ** | −0.009 *** | −0.031 *** | −0.015 ** |

| (−3.10) | (−4.41) | (−2.28) | (−3.09) | (−4.33) | (−2.22) | |

| TANG | 0.003 | 0.092 | 0.008 | 0.005 | 0.098 | 0.011 |

| (0.13) | (1.46) | (0.15) | (0.20) | (1.55) | (0.19) | |

| INTANG | 0.060 | 0.152 | −0.258 * | 0.058 | 0.146 | −0.255 * |

| (0.85) | (0.92) | (−1.73) | (0.82) | (0.89) | (−1.71) | |

| EMENUM | 0.007 | 0.016 | 0.011 | 0.007 | 0.016 | 0.011 |

| (1.53) | (1.45) | (1.20) | (1.55) | (1.46) | (1.20) | |

| AGE | 0.028 | 0.165 | −0.005 | 0.025 | 0.154 | −0.010 |

| (0.68) | (1.45) | (−0.06) | (0.61) | (1.35) | (−0.11) | |

| FGNSALE | 0.024 | 0.038 | −0.094 * | 0.024 | 0.039 | −0.098 ** |

| (1.07) | (0.70) | (−1.92) | (1.09) | (0.71) | (−2.00) | |

| TOP | −0.011 | −0.139 | −0.038 | −0.008 | −0.128 | −0.037 |

| (−0.33) | (−1.59) | (−0.54) | (−0.23) | (−1.47) | (−0.53) | |

| INDB | 0.047 | 0.027 | 0.092 | 0.043 | 0.008 | 0.087 |

| (0.87) | (0.21) | (0.78) | (0.79) | (0.06) | (0.73) | |

| SEG | 0.025 | −0.148 | −1.107 * | 0.016 | −0.181 | −1.121 * |

| (0.09) | (−0.20) | (−1.80) | (0.06) | (−0.25) | (−1.82) | |

| Constant | −0.508 *** | −1.853 *** | −0.977 ** | −0.500 *** | −1.844 *** | −0.989 *** |

| (−2.97) | (−4.00) | (−2.57) | (−2.94) | (−4.01) | (−2.61) | |

| FirmFE | Yes | Yes | Yes | Yes | Yes | Yes |

| InduFE | Yes | Yes | Yes | Yes | Yes | Yes |

| YearFE | Yes | Yes | Yes | Yes | Yes | Yes |

| CityFE | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 16,789 | 16,789 | 16,789 | 16,789 | 16,789 | 16,789 |

| Adj. R2 | 0.479 | 0.597 | 0.137 | 0.479 | 0.597 | 0.137 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Variable | TECH_ PROXIMITY | KNOWN | UNKNOWN | TECH_ PROXIMITY | KNOWN | UNKNOWN |

| Analyst coverage | Institutional shareholding ratio | |||||

| POST | −0.003 | −0.016 | −0.019 | −0.002 | 0.002 | −0.023 |

| (−0.44) | (−0.93) | (−1.20) | (−0.25) | (0.12) | (−1.34) | |

| POST*AC | 0.036 *** | 0.122 *** | 0.025 | |||

| (3.75) | (4.84) | (1.15) | ||||

| AC | −0.013 *** | −0.036 *** | −0.012 | |||

| (−2.74) | (−3.11) | (−1.04) | ||||

| POST*ISR | 0.031 *** | 0.079 *** | 0.030 | |||

| (3.34) | (3.30) | (1.41) | ||||

| ISR | −0.008 ** | −0.037 *** | −0.020 ** | |||

| (−1.98) | (−3.53) | (−2.00) | ||||

| SIZE | 0.019 *** | 0.067 *** | 0.051 *** | 0.019 *** | 0.072 *** | 0.053 *** |

| (2.62) | (3.46) | (3.18) | (2.67) | (3.77) | (3.34) | |

| LEV | −0.025 | −0.071 | 0.006 | −0.025 | −0.069 | 0.006 |

| (−1.31) | (−1.45) | (0.14) | (−1.34) | (−1.42) | (0.15) | |

| ROA | 0.029 | −0.004 | 0.175 | 0.021 | −0.018 | 0.171 |

| (0.66) | (−0.03) | (1.57) | (0.47) | (−0.16) | (1.53) | |

| BM | 0.015 | 0.012 | 0.003 | 0.014 | −0.002 | −0.007 |

| (0.88) | (0.29) | (0.07) | (0.82) | (−0.06) | (−0.18) | |

| GROWTH | −0.008 *** | −0.030 *** | −0.015 ** | −0.009 *** | −0.030 *** | −0.015 ** |

| (−2.94) | (−4.16) | (−2.18) | (−2.96) | (−4.21) | (−2.12) | |

| TANG | 0.000 | 0.085 | 0.007 | 0.004 | 0.094 | 0.008 |

| (0.02) | (1.35) | (0.13) | (0.17) | (1.49) | (0.14) | |

| INTANG | 0.056 | 0.141 | −0.257 * | 0.059 | 0.154 | −0.252 * |

| (0.78) | (0.85) | (−1.73) | (0.83) | (0.94) | (−1.70) | |

| EMENUM | 0.007 | 0.016 | 0.011 | 0.007 | 0.016 | 0.011 |

| (1.49) | (1.41) | (1.21) | (1.50) | (1.45) | (1.20) | |

| AGE | 0.015 | 0.122 | −0.017 | 0.022 | 0.144 | −0.015 |

| (0.36) | (1.08) | (−0.20) | (0.54) | (1.27) | (−0.17) | |

| FGNSALE | 0.023 | 0.036 | −0.096 * | 0.023 | 0.036 | −0.096 * |

| (1.04) | (0.65) | (−1.95) | (1.04) | (0.65) | (−1.96) | |

| TOP | −0.007 | −0.129 | −0.037 | −0.007 | −0.137 | −0.042 |

| (−0.21) | (−1.48) | (−0.53) | (−0.23) | (−1.56) | (−0.59) | |

| INDB | 0.047 | 0.023 | 0.087 | 0.046 | 0.022 | 0.088 |

| (0.86) | (0.17) | (0.74) | (0.84) | (0.17) | (0.74) | |

| SEG | 0.022 | −0.152 | −1.104 * | 0.038 | −0.127 | −1.096 * |

| (0.08) | (−0.21) | (−1.79) | (0.14) | (−0.17) | (−1.78) | |

| Constant | −0.448 *** | −1.652 *** | −0.983 ** | −0.471 *** | −1.833 *** | −1.017 *** |

| (−2.59) | (−3.56) | (−2.55) | (−2.78) | (−4.01) | (−2.67) | |

| FirmFE | Yes | Yes | Yes | Yes | Yes | Yes |

| InduFE | Yes | Yes | Yes | Yes | Yes | Yes |

| YearFE | Yes | Yes | Yes | Yes | Yes | Yes |

| CityFE | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 16,789 | 16,789 | 16,789 | 16,789 | 16,789 | 16,789 |

| Adj. R2 | 0.479 | 0.597 | 0.137 | 0.479 | 0.597 | 0.137 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variable | KNOWN | UNKNOWN | KNOWN | UNKNOWN |

| EPI | 0.784 ** | −0.388 | 0.431 | −0.107 |

| (2.12) | (−1.35) | (1.24) | (−0.35) | |

| POST*EPI | 2.022 * | −1.660 *** | ||

| (1.81) | (−2.65) | |||

| POST | 0.039 ** | −0.001 | ||

| (2.49) | (−0.04) | |||

| SIZE | 0.068 *** | 0.052 *** | 0.069 *** | 0.051 *** |

| (3.61) | (3.28) | (3.66) | (3.26) | |

| LEV | −0.069 | 0.004 | −0.069 | 0.005 |

| (−1.41) | (0.09) | (−1.41) | (0.12) | |

| ROA | −0.025 | 0.165 | −0.033 | 0.167 |

| (−0.22) | (1.48) | (−0.29) | (1.51) | |

| BM | 0.025 | 0.006 | 0.022 | 0.006 |

| (0.62) | (0.15) | (0.55) | (0.17) | |

| GROWTH | −0.032 *** | −0.016 ** | −0.032 *** | −0.015 ** |

| (−4.40) | (−2.28) | (−4.48) | (−2.22) | |

| TANG | 0.098 | 0.012 | 0.096 | 0.015 |

| (1.56) | (0.20) | (1.51) | (0.26) | |

| INTANG | 0.162 | −0.259 * | 0.159 | −0.256 * |

| (0.99) | (−1.74) | (0.97) | (−1.72) | |

| EMENUM | 0.019 * | 0.011 | 0.018* | 0.011 |

| (1.70) | (1.21) | (1.65) | (1.19) | |

| AGE | 0.154 | −0.010 | 0.157 | −0.009 |

| (1.35) | (−0.12) | (1.38) | (−0.10) | |

| FGNSALE | 0.042 | −0.096 ** | 0.038 | −0.096 ** |

| (0.76) | (−1.96) | (0.69) | (−1.97) | |

| TOP | −0.130 | −0.041 | −0.125 | −0.047 |

| (−1.49) | (−0.58) | (−1.43) | (−0.67) | |

| INDB | 0.018 | 0.087 | 0.025 | 0.085 |

| (0.13) | (0.74) | (0.19) | (0.72) | |

| SEG | −0.209 | −1.094 * | −0.211 | −1.072 * |

| (−0.28) | (−1.78) | (−0.29) | (−1.74) | |

| Constant | −1.823 *** | −1.014 *** | −1.853 *** | −1.007 *** |

| (−3.96) | (−2.68) | (−4.03) | (−2.67) | |

| FirmFE | Yes | Yes | Yes | Yes |

| InduFE | Yes | Yes | Yes | Yes |

| YearFE | Yes | Yes | Yes | Yes |

| CityFE | Yes | Yes | Yes | Yes |

| N | 16,789 | 16,789 | 16,789 | 16,789 |

| Adj. R2 | 0.596 | 0.137 | 0.597 | 0.137 |

| (1) | (2) | |

|---|---|---|

| EVA | CSRID | |

| POST | 0.046 * | 0.019 *** |

| (1.70) | (2.68) | |

| SIZE | 0.082 * | 0.074 *** |

| (1.65) | (6.87) | |

| LEV | 0.252 *** | 0.116 *** |

| (3.79) | (4.58) | |

| BM | −0.145 *** | −0.023 |

| (−3.03) | (−1.09) | |

| GROWTH | 0.113 *** | −0.021 *** |

| (4.11) | (−5.18) | |

| TANG | −0.075 | 0.014 |

| (−1.04) | (0.45) | |

| INTANG | −0.250 | −0.163 |

| (−1.22) | (−1.44) | |

| EMENUM | 0.041 ** | 0.013 * |

| (2.42) | (1.92) | |

| AGE | −0.245 | −0.010 |

| (−0.88) | (−0.19) | |

| FGNSALE | −0.059 | −0.031 |

| (−1.37) | (−1.20) | |

| TOP | 0.525 | −0.011 |

| (0.99) | (−0.23) | |

| INDB | 0.104 | 0.011 |

| (0.39) | (0.17) | |

| SEG | 1.497 | −0.734 ** |

| (1.40) | (−2.01) | |

| Constant | −1.787 ** | −1.489 *** |

| (−2.33) | (−5.49) | |

| FirmFE | Yes | Yes |

| InduFE | Yes | Yes |

| YearFE | Yes | Yes |

| CityFE | Yes | Yes |

| N | 16,789 | 16,789 |

| Adj. R2 | 0.071 | 0.804 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, X.; Ou, J.; Tang, X.; Yang, Q. The Impact of Officials’ Off-Office Accountability Audit of Natural Resource Assets on Firms’ Green Innovation Strategies: A Quasi-Natural Experiment in China. Sustainability 2023, 15, 2640. https://doi.org/10.3390/su15032640

Chen X, Ou J, Tang X, Yang Q. The Impact of Officials’ Off-Office Accountability Audit of Natural Resource Assets on Firms’ Green Innovation Strategies: A Quasi-Natural Experiment in China. Sustainability. 2023; 15(3):2640. https://doi.org/10.3390/su15032640

Chicago/Turabian StyleChen, Xihui, Juan Ou, Xuemei Tang, and Qinghe Yang. 2023. "The Impact of Officials’ Off-Office Accountability Audit of Natural Resource Assets on Firms’ Green Innovation Strategies: A Quasi-Natural Experiment in China" Sustainability 15, no. 3: 2640. https://doi.org/10.3390/su15032640