Gender Inclusiveness and Female Representation on the Board of Directors of the Benefit Company Model: Evidence from Italy

Abstract

:1. Introduction

2. The Italian Benefit Company

- (a)

- “shared benefit”: referring to the achievement, jointly, of the BC’s economic activities, of one or more positive effects, or of the reduction in negative effects;

- (b)

- “other stakeholders”: the entities or clusters of entities directly or indirectly involved in, or affected by the actions of the BC, such as employees, customers, providers, financiers, creditors, public administration, and community;

- (c)

- “third-party standard”: procedures and measures needed to evaluate the impact produced by the BC concerning the shared benefit;

- (d)

- “evaluation areas”: areas to be integrated in the evaluation of the actions of shared benefit.

3. Theoretical Background and Hypothesis Development

4. Materials and Methods

4.1. Sample

- Only companies established before 2009 were selected in order to identify those companies that transformed their model from a non-BC model to a BC model. Therefore, companies that were originally established as BCs were excluded;

- The companies for which financial information was not available for a maximum of three years in the time interval (2009–2018) analysed were eliminated.

- -

- In the Aida BvD database, a search was carried out of Italian companies that were active and established until 2009;

- -

- From this dataset of active Italian companies, with the exclusion of the already selected BCs, a dataset of companies was randomly sampled;

- -

- The companies for which financial information was not available for a maximum of three years in the time interval considered were eliminated.

4.2. Variables

4.2.1. Dependent Variable

4.2.2. Independent Variable

4.2.3. Control Variables

4.3. Analytical Approach and Strategy

5. Results

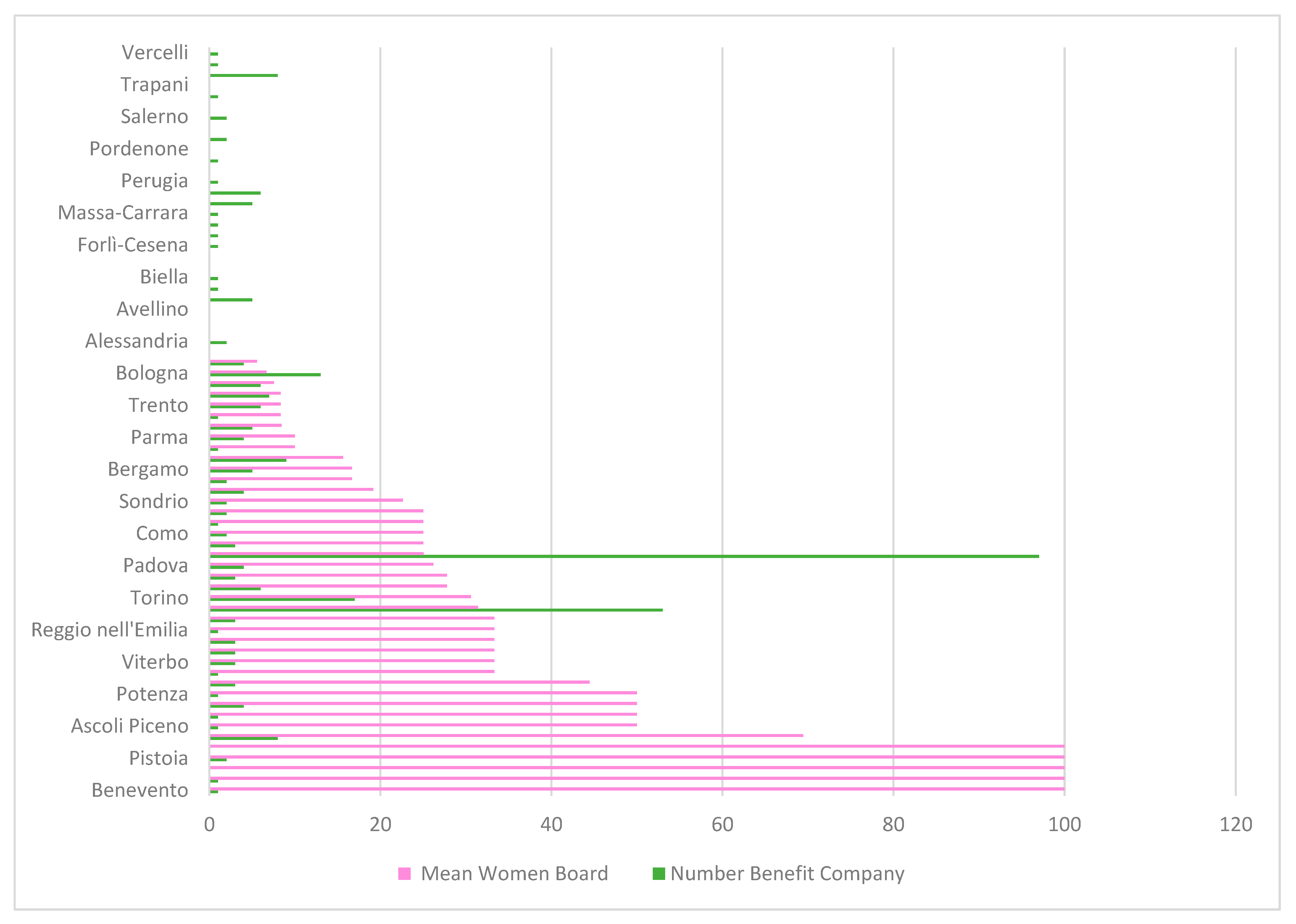

5.1. Descriptive Statistics

5.2. Estimation of the Fractional Regression Probit Model

5.3. Robustness Test: Endogeneity Problem

6. Discussion

6.1. Theoretical Implications

6.2. Practical and Social Implications

6.3. Limitation and Future Direction of Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Gazzola, P.; Amelio, S.; Papagiannis, F.; Michaelides, Z. Sustainability reporting practices and their social impact to NGO funding in Italy. Crit. Perspect. Account. 2021, 79, 102085. [Google Scholar] [CrossRef]

- Malesios, C.; De, D.; Moursellas, A.; Dey, P.K.; Evangelinos, K. Sustainability performance analysis of small and medium sized enterprises: Criteria, methods and framework. Socio-Econ. Plan. Sci. 2021, 75, 100993. [Google Scholar] [CrossRef]

- Kucharska, W.; Kowalczyk, R. How to achieve sustainability?—Employee’s point of view on company’s culture and CSR practice. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 453–467. [Google Scholar] [CrossRef]

- Roloff, J. Benefit Corporation und Social Entrepreneurship. In Handbuch Wirtschaftsethik; JB Metzler: Stuttgart, Germany, 2022; pp. 665–667. [Google Scholar]

- Baudot, L.; Dillard, J.; Pencle, N. The emergence of benefit corporations: A cautionary tale. Crit. Perspect. Account. 2020, 67, 102073. [Google Scholar] [CrossRef]

- Cooper, L.A.; Weber, J. Does Benefit Corporation status matter to investors? An exploratory study of investor perceptions and decisions. Bus. Soc. 2021, 60, 979–1008. [Google Scholar] [CrossRef]

- Lingenfelter, G.; Cohen, R. To B or not to B: Etsy’s decision whether to re-incorporate as a public benefit corporation and maintain its B Lab certification. CASE J. 2019, 15, 510–527. [Google Scholar] [CrossRef]

- Fisch, J.E.; Solomon, S.D. The Value of a Public Benefit Corporation. In Research Handbook on Corporate Purpose and Personhood; Edward Elgar Publishing: Cheltenham, UK, 2021; Available online: https://scholarship.law.upenn.edu/faculty_scholarship/2225 (accessed on 16 November 2022).

- Hussain, N.; Rigoni, U.; Cavezzali, E. Does it pay to be sustainable? Looking inside the black box of the relationship between sustainability performance and financial performance. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 1198–1211. [Google Scholar] [CrossRef] [Green Version]

- Corsi, C.; Prencipe, A.; Boffa, D. Corporate governance and the choice to take on the hybrid organizational model of the benefit company: Evidence from Italy. J. Model. Manag. 2020, 16, 904–921. [Google Scholar] [CrossRef]

- Omarova, S.T. The franchise view of the corporation: Purpose, personality, public policy. In Research Handbook on Corporate Purpose and Personhood; Edward Elgar Publishing: Cheltenham, UK, 2021. [Google Scholar]

- Czinkota, M.; Kaufmann, H.R.; Basile, G.; Ferri, M.A. For-Benefit company (fBComp): An innovative social-business model. The Italian case. J. Bus. Res. 2020, 119, 377–387. [Google Scholar] [CrossRef]

- Fallah Shayan, N.; Mohabbati-Kalejahi, N.; Alavi, S.; Zahed, M.A. Sustainable development goals (SDGs) as a framework for corporate social responsibility (CSR). Sustainability 2022, 14, 1222. [Google Scholar] [CrossRef]

- Lanza, G.G. Nuove sinergie tra territori e imprese: Le benefit corporation come possibili attori di sviluppo sostenibile. Doc. Geogr. 2017, 1, 37–61. [Google Scholar] [CrossRef]

- Hiller, J.S. The benefit corporation and corporate social responsibility. J. Bus. Ethics 2013, 118, 287–301. [Google Scholar] [CrossRef]

- Palazzi, F.; Sentuti, A.; Sgrò, F. Gender Differences in the Personal Values of For-Benefit Entrepreneurs. An Investigation of Italian Benefit Corporations. In Organizational Resilience and Female Entrepreneurship During Crises; Springer: Cham, Switzerland, 2022; pp. 31–45. [Google Scholar]

- Esposito, R.T. The Social Enterprise Revolution in Corporate Law: A Primer on Emerging Corporate Entities in Europe and the United States and the Case for the Benefit Corporation. Wm. Mary Bus. L. Rev. 2012, 4, 639. Available online: https://scholarship.law.wm.edu/wmblr/vol4/iss2/7 (accessed on 9 December 2022).

- Battaglia, M.; Gragnani, P.; Annesi, N. Moving Businesses toward Sustainable Development Goals (SDGs): Evidence from an Italian “Benefit-For-Nature”Corporation”. Entrep. Res. J. 2020, 10, 1–36. [Google Scholar] [CrossRef]

- Lafuente, A.; Viñuales, V.; Pueyo, R.; Llaría, J. Responsabilidad Social Corporativas y Politicas Publicas; Fundacion Alternativas: Madrid, Spain, 2003. [Google Scholar]

- Galli, D.; Torelli, R.; Tibiletti, V. Signaling the Adoption of the Benefit Corporation Model: A Step towards Transparency. Sustainability 2021, 13, 6967. [Google Scholar] [CrossRef]

- Marchini, P.L.; Tibiletti, V.; Fellegara, A.M.; Mazza, T. Pursuing a strategy of ‘common benefit’in business: The adoption of the benefit corporation model in Italy. Bus. Strategy Environ. 2022, 1–23. [Google Scholar] [CrossRef]

- Wang, Y.; Ma, J.; Wang, T. Do all female directors have the same impact on corporate social responsibility? The role of their political connection. Asia Pac. J. Manag. 2021, 1–28. [Google Scholar] [CrossRef]

- Hartmann, C.C.; Carmenate, J. Does board diversity influence firms’ corporate social responsibility reputation? Soc. Responsib. J. 2020, 17, 1299–1319. [Google Scholar] [CrossRef]

- Setó-Pamies, D. The relationship between women directors and corporate social responsibility. Corp. Soc. Responsib. Environ. Manag. 2015, 22, 334–345. [Google Scholar] [CrossRef]

- Amorelli, M.F.; García-Sánchez, I.M. Trends in the dynamic evolution of board gender diversity and corporate social responsibility. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 537–554. [Google Scholar] [CrossRef]

- Boukattaya, S.; Omri, A. Impact of board gender diversity on corporate social responsibility and irresponsibility: Empirical evidence from France. Sustainability 2021, 13, 4712. [Google Scholar] [CrossRef]

- Liao, L.; Luo, L.; Tang, Q. Gender diversity, board independence, environmental committee and greenhouse gas disclosure. Br. Account. Rev. 2015, 47, 409–424. [Google Scholar] [CrossRef]

- Buertey, S. Board gender diversity and corporate social responsibility assurance: The moderating effect of ownership concentration. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 1579–1590. [Google Scholar] [CrossRef]

- Orazalin, N.; Baydauletov, M. Corporate social responsibility strategy and corporate environmental and social performance: The moderating role of board gender diversity. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 1664–1676. [Google Scholar] [CrossRef]

- Saggese, S.; Sarto, F. Women on Board and Disclosure Quality: An Empirical Research. In Organizational Resilience and Female Entrepreneurship during Crises; Springer: Cham, Switzerland, 2022; pp. 47–56. [Google Scholar]

- Klettner, A.; Clarke, T.; Boersma, M. Strategic and regulatory approaches to increasing women in leadership: Multilevel targets and mandatory quotas as levers for cultural change. J. Bus. Ethics 2016, 133, 395–419. [Google Scholar] [CrossRef]

- Leszczyńska, M. Mandatory quotas for women on boards of directors in the European Union: Harmful to or good for company performance? Eur. Bus. Organ. Law Rev. 2018, 19, 35–61. [Google Scholar] [CrossRef] [Green Version]

- Post, C.; Byron, K. Women on boards and firm financial performance: A meta-analysis. Acad. Manag. J. 2015, 58, 1546–1571. [Google Scholar] [CrossRef]

- Cabeza-García, L.; Fernández-Gago, R.; Nieto, M. Do board gender diversity and director typology impact CSR reporting? Eur. Manag. Rev. 2018, 15, 559–575. [Google Scholar] [CrossRef]

- Konadu, R. Gender diversity impact on corporate social responsibility (CSR) and greenhouse gas emissions in the UK. Econ. Bus. Rev. 2017, 3, 127–148. [Google Scholar] [CrossRef]

- Garriga, E.; Melé, D. Corporate social responsibility theories: Mapping the territory. J. Bus. Ethics 2004, 53, 51–71. [Google Scholar] [CrossRef]

- Sánchez, P.E.; Benito-Hernández, S. CSR policies: Effects on labour productivity in Spanish micro and small manufacturing companies. J. Bus. Ethics 2015, 128, 705–724. [Google Scholar] [CrossRef] [Green Version]

- Tang, Z.; Hull, C.E.; Rothenberg, S. How corporate social responsibility engagement strategy moderates the CSR–financial performance relationship. J. Manag. Stud. 2012, 49, 1274–1303. [Google Scholar] [CrossRef]

- Hao, J.; He, F. Corporate social responsibility (CSR) performance and green innovation: Evidence from China. Financ. Res. Lett. 2022, 48, 102889. [Google Scholar] [CrossRef]

- Zaman, R.; Jain, T.; Samara, G.; Jamali, D. Corporate governance meets corporate social responsibility: Mapping the interface. Bus. Soc. 2022, 61, 690–752. [Google Scholar] [CrossRef]

- Popescu, C.R.G. Corporate social responsibility, corporate governance and business performance: Limits and challenges imposed by the implementation of directive 2013/34/EU in Romania. Sustainability 2019, 11, 5146. [Google Scholar]

- Grosser, K.; Moon, J. Gender mainstreaming and corporate social responsibility: Reporting workplace issues. J. Bus. Ethics 2005, 62, 327–340. [Google Scholar] [CrossRef]

- Schultz, I. Case Study on Gender Equality in CSR in the Banking Sector; Working Paper of the RARE Project; Institute for Social-Ecological Research (ISOE): Frankfurt, Germany, 2007. [Google Scholar]

- Stropnik, N. Flexible working and genderequality: The case of Slovenia. Exchange of good practices on gender and equality. In New Forms of Work; European Commision: Den Haag, The Netherlands, 2010. [Google Scholar]

- Godfrey, C.; Hoepner, A.G.; Lin, M.T.; Poon, S.H. Women on boards and corporate social irresponsibility: Evidence from a Granger style reverse causality minimisation procedure. Eur. J. Financ. 2020, 1–27. [Google Scholar] [CrossRef]

- Zyglidopoulos, S.C. The issue life-cycle: Implications for reputation for social performance and organizational legitimacy. Corp. Reput. Rev. 2003, 6, 70–81. [Google Scholar] [CrossRef]

- Pollach, I. Strategic corporate social responsibility: The struggle for legitimacy and reputation. Int. J. Bus. Gov. Ethics 2015, 10, 57–75. [Google Scholar] [CrossRef]

- Rao, K.; Tilt, C. Board composition and corporate social responsibility: The role of diversity, gender, strategy and decision making. J. Bus. Ethics 2016, 138, 327–347. [Google Scholar] [CrossRef]

- Gomez-Trujillo, A.M.; Velez-Ocampo, J.; Gonzalez-Perez, M.A. A literature review on the causality between sustainability and corporate reputation: What goes first? Manag. Environ. Qual. Int. J. 2020, 31, 406–430. [Google Scholar] [CrossRef]

- Larkin, M.B.; Bernardi, R.A.; Bosco, S.M. Board gender diversity, corporate reputation and market performance. Int. J. Bank. Financ. 2012, 9, 1–26. [Google Scholar]

- Bernardi, R.A.; Bosco, S.M.; Columb, V.L. Does female representation on boards of directors associate with the ‘most ethical companies’ list? Corp. Reput. Rev. 2009, 12, 270–280. [Google Scholar] [CrossRef]

- Terjesen, S.; Sealy, R.; Singh, V. Women directors on corporate boards: A review and research agenda. Corp. Gov. Int. Rev. 2009, 17, 320–337. [Google Scholar] [CrossRef] [Green Version]

- Hillman, A.J.; Dalziel, T. Boards of directors and firm performance: Integrating agency and resource dependence perspectives. Acad. Manag. Rev. 2003, 28, 383–396. [Google Scholar] [CrossRef]

- Reddy, S.; Jadhav, A.M. Gender diversity in boardrooms—A literature review. Cogent Econ. Financ. 2019, 7, 1644703. [Google Scholar] [CrossRef]

- Zinko, R.; Ferris, G.R.; Blass, F.R.; Dana Laird, M. Toward a theory of reputation in organizations. In Research in Personnel and Human Resources Management; Martocchio, J.J., Ed.; Emerald Group Publishing Limited: Bingley, UK, 2007; Volume 26, pp. 163–204. [Google Scholar] [CrossRef]

- Aksak, E.O.; Ferguson, M.A.; Duman, S.A. Corporate social responsibility and CSR fit as predictors of corporate reputation: A global perspective. Public Relat. Rev. 2016, 42, 79–81. [Google Scholar]

- Davis, G.F.; Cobb, J. Resource Dependence Theory: Past and future. Res. Sociol. Organ. 2010, 28, 21–42. [Google Scholar] [CrossRef] [Green Version]

- Frynas, J.G.; Yamahaki, C. Corporate social responsibility: Review and roadmap of theoretical perspectives. Bus. Ethics Eur. Rev. 2016, 25, 258–285. [Google Scholar] [CrossRef]

- Gazzola, P.; Grechi, D.; Ossola, P.; Pavione, E. Certified Benefit Corporations as a new way to make sustainable business: The Italian example. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 1435–1445. [Google Scholar] [CrossRef]

- Palladino, R.; Sasso, P.; Profita, S.; Carusone, R.; Fiano, F.; Giudice, M.D. Assessing the Italian benefit corporation disclosure: A content analysis. Int. J. Manag. Financ. Account. 2022, 14, 217–235. [Google Scholar] [CrossRef]

- Nicholas, A.J.; Sacco, S. People, Planet, Profit: Benefit and B Certified Corporations—Comprehension and Outlook of Business Students; Salve Regina University: Newport, RI, USA, 2017. [Google Scholar]

- Castellini, M.; Marzano, M.; Riso, V. Are B corporations’a model of disclosure of intellectual capital? An analysis by ecosystem. Soft Regulating Integrated Reporting for SMEs: The Case of Italy. In Proceedings of the 13th Interdisciplinary Workshop on Intangibles and Intellectual Capital, EURAM Conference, Ancona, Italy, 21–22 September 2017. [Google Scholar]

- Di Cesare, P.; Ezechieli, E. Le benefit corporation e l’evoluzione del Capitalismo. In L’azienda Sostenibile: Trend Strumenti e Case Study; Edizioni Ca’ Foscari: Venice, Italy, 2017; pp. 55–78. [Google Scholar] [CrossRef]

- Agafonow, A.; Donaldson, C. The economic rationale behind the social business model: A research agenda. Soc. Bus. 2015, 5, 5–16. [Google Scholar] [CrossRef]

- Hussain, N.; Rigoni, U.; Orij, R.P. Corporate governance and sustainability performance: Analysis of triple bottom line performance. J. Bus. Ethics 2018, 149, 411–432. [Google Scholar] [CrossRef]

- Michelon, G.; Parbonetti, A. The effect of corporate governance on sustainability disclosure. J. Manag. Gov. 2012, 16, 477–509. [Google Scholar] [CrossRef]

- Shin, S.; Lee, J.; Bansal, P. From a shareholder to stakeholder orientation: Evidence from the analyses of CEO dismissal in large US firms. Strateg. Manag. J. 2022, 43, 1233–1257. [Google Scholar] [CrossRef]

- Bouslah, K.; Hmaittane, A.; Kryzanowski, L.; M’Zali, B. CSR Structures: Evidence, Drivers, and Firm Value Implications. J. Bus. Ethics 2022, 1–31. [Google Scholar] [CrossRef]

- Bondy, K.; Moon, J.; Matten, D. An institution of corporate social responsibility (CSR) in multi-national corporations (MNCs): Form and implications. J. Bus. Ethics 2012, 111, 281–299. [Google Scholar] [CrossRef] [Green Version]

- Metcalf, L.; Benn, S. The corporation is ailing social technology: Creating a ‘fit for purpose’design for sustainability. J. Bus. Ethics 2012, 111, 195–210. [Google Scholar] [CrossRef]

- Bashir, M. Corporate social responsibility and financial performance—The role of corporate reputation, advertising and competition. PSU Res. Rev. 2022. ahead-of-print. [CrossRef]

- Bitektine, A. Toward a theory of social judgments of organizations: The case of legitimacy, reputation, and status. Acad. Manag. Rev. 2011, 36, 151–179. [Google Scholar] [CrossRef]

- De Quevedo-Puente, E.; De La Fuente-Sabaté, J.M.; Delgado-García, J.B. Corporate social performance and corporate reputation: Two interwoven perspectives. Corp. Reput. Rev. 2007, 10, 60–72. [Google Scholar] [CrossRef] [Green Version]

- Atif, M.; Liu, B.; Nadarajah, S. The effect of corporate environmental, social and governance disclosure on cash holdings: Life-cycle perspective. Bus. Strategy Environ. 2022, 31, 2193–2212. [Google Scholar] [CrossRef]

- Rawhouser, H.; Cummings, M.E.; Marcus, A. Sustainability standards and stakeholder engagement: Lessons from carbon markets. Organ. Environ. 2018, 31, 263–282. [Google Scholar] [CrossRef]

- Bernardi, R.A.; Bosco, S.M.; Vassill, K.M. Does female representation on boards of directors associate with Fortune’s “100 best companies to work for” list? Bus. Soc. 2006, 45, 235–248. [Google Scholar] [CrossRef]

- Bear, S.; Rahman, N.; Post, C. The impact of board diversity and gender composition on corporate social responsibility and firm reputation. J. Bus. Ethics 2010, 97, 207–221. [Google Scholar] [CrossRef]

- Greening, D.W.; Turban, D.B. Corporate social performance as a competitive advantage in attracting a quality workforce. Bus. Soc. 2000, 39, 254–280. [Google Scholar] [CrossRef]

- Bernardi, R.A.; Bean, D.F.; Weippert, K.M. Signaling gender diversity through annual report pictures: A research note on image management. Account. Audit. Account. J. 2002, 15, 609–616. [Google Scholar] [CrossRef]

- Li, Y.; de Villiers, C.; Li, L.Z.; Li, L. The moderating effect of board gender diversity on the relation between corporate social responsibility and firm value. J. Manag. Control 2022, 33, 109–143. [Google Scholar]

- Eisenhardt, K.M. Agency theory: An assessment and review. Acad. Manag. Rev. 1989, 14, 57–74. [Google Scholar] [CrossRef] [Green Version]

- Noreen, E. The economics of ethics: A new perspective on agency theory. Account. Organ. Soc. 1988, 13, 359–369. [Google Scholar] [CrossRef]

- Hillman, A.J.; Cannella, A.A., Jr.; Harris, I.C. Women and racial minorities in the boardroom: How do directors differ? J. Manag. 2022, 28, 747–763. [Google Scholar] [CrossRef]

- Dezsö, C.L.; Ross, D.G. Does female representation in top management improve firm performance? A panel data investigation. Strateg. Manag. J. 2012, 33, 1072–1089. [Google Scholar] [CrossRef] [Green Version]

- Bernardi, R.A.; Threadgill, V.H. Women directors and corporate social responsibility. EJBO Electron. J. Bus. Ethics Organ. Stud. 2011, 15, 15–21. [Google Scholar]

- Harjoto, M.; Laksmana, I.; Lee, R. Board diversity and corporate social responsibility. J. Bus. Ethics 2015, 132, 641–660. [Google Scholar] [CrossRef]

- Carpenter, M.A.; Westphal, J.D. The strategic context of external network ties: Examining the impact of director appointments on board involvement in strategic decision making. Acad. Manag. J. 2001, 44, 639–660. [Google Scholar] [CrossRef] [Green Version]

- Yoon, N. Understanding theoretical orientation and consequences of board interlock: Integration and future directions. Nonprofit Manag. Leadersh. 2021, 31, 717–736. [Google Scholar] [CrossRef]

- Connelly, B.L.; Certo, S.T.; Ireland, R.D.; Reutzel, C.R. Signaling theory: A review and assessment. J. Manag. 2011, 37, 39–67. [Google Scholar] [CrossRef]

- Karasek, R., III; Bryant, P. Signaling theory: Past, present, and future. Acad. Strateg. Manag. J. 2012, 11, 91. [Google Scholar]

- Navarro-García, J.C.; Ramón-Llorens, M.C.; García-Meca, E. Female directors and corporate reputation. BRQ Bus. Res. Q. 2020, 25, 352–365. [Google Scholar] [CrossRef]

- Brammer, S.; Millington, A.; Pavelin, S. Corporate reputation and women on the board. Br. J. Manag. 2009, 20, 17–29. [Google Scholar] [CrossRef]

- Chen, S.; Ni, X.; Tong, J.Y. Gender diversity in the boardroom and risk management: A case of R&D investment. J. Bus. Ethics 2016, 136, 599–621. [Google Scholar] [CrossRef]

- Allison, P.D. Discrete-time methods for the analysis of event histories. Soc. Methodol. 1982, 13, 61–98. [Google Scholar] [CrossRef]

- De Cabo, R.M.; Gimeno, R.; Escot, L. Disentangling discrimination on Spanish boards of directors. Corp. Gov. Int. Rev. 2011, 19, 77–95. [Google Scholar] [CrossRef] [Green Version]

- Solakoglu, M.N.; Demir, N. The role of firm characteristics on the relationship between gender diversity and firm performance. Manag. Decis. 2016, 54, 1407–1419. [Google Scholar] [CrossRef]

- Weber, A.; Zulehner, C. Female hires and the success of start-up firms. Am. Econ. Rev. 2010, 100, 358–361. [Google Scholar] [CrossRef] [Green Version]

- Baron, J.N.; Hannan, M.T.; Hsu, G.; Koçak, Ö. In the company of women: Gender inequality and the logic of bureaucracy in start-up firms. Work Occup. 2007, 34, 35–66. [Google Scholar] [CrossRef]

- Laužikas, M.; Tindale, H.; Bilota, A.; Bielousovaitė, D. Contributions of sustainable start-up ecosystem to dynamics of start-up companies: The case of Lithuania. Entrep. Sustain. Issues 2015, 3, 8–24. [Google Scholar] [CrossRef]

- Honeyman, R.; Jana, T. The B Corp Handbook: How You Can Use Business as a Force for Good; Berrett-Koehler Publishers: Oakland, CA, USA, 2019. [Google Scholar]

- Nahavandi, A.; Malekzadeh, A.R. Leader style in strategy and organizational performance: An integrative framework. J. Manag. Stud. 1993, 30, 405–425. [Google Scholar] [CrossRef]

- Li, H.; Chen, P. Board gender diversity and firm performance: The moderating role of firm size. Bus. Ethics Eur. Rev. 2018, 27, 294–308. [Google Scholar] [CrossRef]

- Xie, Q. CEO tenure and ownership mode choice of Chinese firms: The moderating roles of managerial discretion. Int. Bus. Rev. 2014, 23, 910–919. [Google Scholar] [CrossRef]

- Kılıç, M.; Kuzey, C. The effect of board gender diversity on firm performance: Evidence from Turkey. Gend. Manag. Int. J. 2016, 31, 434–455. [Google Scholar] [CrossRef]

- Isidro, H.; Sobral, M. The effects of women on corporate boards on firm value, financial performance, and ethical and social compliance. J. Bus. Ethics 2015, 132, 1–19. [Google Scholar] [CrossRef]

- Đặng, R.; Houanti, L.H.; Reddy, K.; Simioni, M. Does board gender diversity influence firm profitability? A control function approach. Econ. Model. 2020, 90, 168–181. [Google Scholar] [CrossRef]

- Martinez-Jimenez, R.; Hernández-Ortiz, M.J.; Fernández, A.I.C. Gender diversity influence on board effectiveness and business performance. Corp. Gov. Int. J. Bus. Soc. 2020, 20, 307–323. [Google Scholar] [CrossRef]

- Joecks, J.; Pull, K.; Vetter, K. Gender diversity in the boardroom and firm performance: What exactly constitutes a “critical mass”? J. Bus. Ethics 2013, 118, 61–72. [Google Scholar] [CrossRef]

- Turban, S.; Wu, D.; Zhang, L. When gender diversity makes firms more productive. Harv. Bus. Rev. 2019, 11, 17. [Google Scholar]

- Şener, İ.; Karaye, A.B. Board composition and gender diversity: Comparison of Turkish and Nigerian listed companies. Procedia-Soc. Behav. Sci. 2014, 150, 1002–1011. [Google Scholar] [CrossRef] [Green Version]

- Pucheta-Martínez, M.C.; Bel-Oms, I. The board of directors and dividend policy: The effect of gender diversity. Ind. Corp. Change 2016, 25, 523–547. [Google Scholar] [CrossRef]

- Baixauli-Soler, J.S.; Lucas-Perez, M.E.; Martin-Ugedo, J.F.; Minguez-Vera, A.; Sanchez-Marin, G. Executive directors’ compensation and monitoring: The influence of gender diversity on Spanish boards. J. Bus. Econ. Manag. 2016, 17, 1133–1154. [Google Scholar] [CrossRef] [Green Version]

- Jizi, M.I.; Nehme, R. Board gender diversity and firms’ equity risk. Equal. Divers. Incl. Int. J. 2017, 36, 590–606. [Google Scholar] [CrossRef]

- Marinova, J.; Plantenga, J.; Remery, C. Gender diversity and firm performance: Evidence from Dutch and Danish boardrooms. Int. J. Hum. Resour. Manag. 2016, 27, 1777–1790. [Google Scholar] [CrossRef]

- Papke, L.E.; Wooldridge, J.M. Econometric methods for fractional response variables with an application to 401 (k) plan participation rates. J. Appl. Econom. 1996, 11, 619–632. [Google Scholar] [CrossRef]

- Hardin, J.W.; Hilbe, J.M. Generalized Estimating Equations; Chapman and Hall/CRC: Boca Raton, FL, USA, 2002. [Google Scholar]

- Stillman, S. Review of generalized estimating equations by Hardin and Hilbe. Stata J. 2003, 3, 208–210. [Google Scholar]

- Wagner, J. Unobserved firm heterogeneity and the size-exports nexus: Evidence from German panel data. Rev. World Econ. 2003, 139, 161–172. [Google Scholar] [CrossRef] [Green Version]

- Papke, L.E.; Wooldridge, J.M. Panel data methods for fractional response variables with an application to test pass rates. J. Econom. 2008, 145, 121–133. [Google Scholar] [CrossRef]

- Bates, M.; Wooldridge, J.; Papke, L. Nonlinear Correlated Random Effects Models with Endogeneity and Unbalanced Panels; Working Papers 202214; University of California at Riverside: Riverside, CA, USA, 2022. [Google Scholar]

- Ramalho, E.A.; Ramalho, J.J.; Murteira, J.M. Alternative estimating and testing empirical strategies for fractional regression models. J. Econ. Surv. 2011, 25, 19–68. [Google Scholar] [CrossRef]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis, 7th ed.; Prentice-Hall, Inc.: Upper Saddle River, NJ, USA, 2010. [Google Scholar] [CrossRef]

- Larcker, D.F.; Rusticus, T.O. On the use of instrumental variables in accounting research. J. Account. Econ. 2010, 49, 186–205. [Google Scholar] [CrossRef]

- Roodman, D. How to do xtabond2: An introduction to difference and system GMM in Stata. Stata J. 2009, 9, 86–136. [Google Scholar] [CrossRef]

- Wintoki, M.B.; Linck, J.S.; Netter, J.M. Endogeneity and the dynamics of internal corporate governance. J. Financ. Econ. 2012, 105, 581–606. [Google Scholar] [CrossRef]

- Finkelstein, S.; Mooney, A.C. Not the usual suspects: How to use board process to make boards better. Acad. Manag. Perspect. 2003, 17, 101–113. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

| Variable | N. of Obs. | Mean | S.D. | Min. | Max. |

|---|---|---|---|---|---|

| Women board | 2700 | 0.2105 | 0.3261 | 0.0000 | 1.0000 |

| Benefit company | 9540 | 0.3711 | 0.4831 | 0.0000 | 1.0000 |

| Firm age | 9540 | 12.4120 | 12.0173 | 0.0000 | 1.0000 |

| ROS | 3893 | 3.6613 | 10.8309 | −50.0000 | 29.9900 |

| Firm size | 4601 | 13.3316 | 1.9539 | 6.8416 | 21.3821 |

| Independent directors | 9540 | 0.3438 | 1.1444 | 0.0000 | 14.0000 |

| Directors age | 7780 | 53.19152 | 12.8576 | 21.0000 | 98.0000 |

| Board size | 9540 | 0.6572 | 1.4220 | 0.0000 | 14.0000 |

| Variables | Women Board = 0 | Women Board > 0 | ||||

|---|---|---|---|---|---|---|

| N. of Obs. | Mean | S.D. | N. of Obs. | Mean | S.D. | |

| Benefit company | 1670 | 0.3054 | 0.4607 | 7870 | 0.3850 | 0.4866 |

| Firm age | 1670 | 16.0539 | 14.7218 | 7870 | 11.6391 | 11.2108 |

| ROS | 951 | 3.7106 | 9.7379 | 2942 | 3.6453 | 11.1629 |

| Firm size | 1085 | 14.1496 | 2.0744 | 3516 | 13.0791 | 1.8436 |

| Independent directors | 1670 | 0.7545 | 1.2551 | 7870 | 0.2567 | 1.1000 |

| Directors Age | 1660 | 56.0060 | 12.7571 | 6120 | 52.4281 | 12.7793 |

| Board size | 1670 | 1.6587 | 1.2228 | 7870 | 0.4447 | 1.3697 |

| Variables | Firm—Years without Women on BoD (Obs = 8510) | Firm—Years with at Least One Woman on BoD (Obs = 1030) | t-Test |

|---|---|---|---|

| Benefit company | 0.3149 | 0.8350 | −34.6144 *** |

| Firm age | 12.5065 | 11.6311 | 2.2085 ** |

| ROS | 3.8557 | 2.0536 | 3.2245 ** |

| Firm size | 13.2973 | 13.0791 | −3.3671 *** |

| Independent directors | 0.1481 | 1.9612 | −55.1496 *** |

| Directors age | 53.0667 | 54.0097 | −2.1931 ** |

| Board size | 0.3255 | 3.3981 | −88.2825 *** |

| Variables | Non-Benefit Companies | Benefit Companies | t-Test |

|---|---|---|---|

| Women board | 0.1278 | 0.2908 | −13.4020 *** |

| Firm age | 16.0550 | 6.2373 | 41.9524 *** |

| ROS | 3.8725 | 2.7761 | 2.4927 ** |

| Firm size | 13.3933 | 13.1120 | 4.0471 *** |

| Independent directors | 0.0900 | 0.7740 | −29.4565 *** |

| Directors age | 55.0654 | 50.2697 | 16.3235 *** |

| Board size | 0.2217 | 1.3955 | −42.4703 *** |

| Variable | VIF | 1/VIF |

|---|---|---|

| Independent directors | 3.8900 | 0.2569 |

| Board size | 3.8100 | 0.2624 |

| Firm size | 1.1400 | 0.8801 |

| Firm age | 1.1300 | 0.8878 |

| Directors age | 1.1000 | 0.9108 |

| ROS | 1.0100 | 0.9919 |

| MEAN VIF | 2.0100 |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | ||

|---|---|---|---|---|---|---|---|---|---|

| 1 | Women board | 1.0000 | |||||||

| 2 | Benefit company | 0.2498 * | 1.0000 | ||||||

| 3 | Firm age | −0.0723 * | −0.3947 * | 1.0000 | |||||

| 4 | ROS | −0.0632 * | −0.0399 * | 0.0144 | 1.0000 | ||||

| 5 | Firm size | −0.1819 * | −0.0596 * | 0.5059 * | 0.0353 * | 1.0000 | |||

| 6 | Independent directors | 0.0861 * | 0.2888 * | 0.0183 | −0.0614 * | 0.2038 * | 1.0000 | ||

| 7 | Directors age | −0.0948 * | −0.1820 * | 0.3431 * | −0.0302 | 0.2798 * | 0.1021 * | 1.0000 | |

| 8 | Board size | 0.1444 * | 0.3988 * | −0.0124 | −0.0598 * | 0.1941 * | 0.8345 * | 0.0724 * | 1.0000 |

| (i) | (ii) | |

|---|---|---|

| Benefit company | 0.9065 *** (0.1027) | |

| Control variables | ||

| Firm age | 0.0095 ** (0.0028) | 0.0107 *** (0.0028) |

| ROS | −0.0040 (0.0030) | −0.0044 (0.0030) |

| Firm size | −0.1602 *** (0.0210) | −0.1529 *** (0.0210) |

| Independent directors | −0.0170 (0.0277) | 0.0896 ** (0.0303) |

| Directors age | −0.0078 ** (0.0028) | −0.0062 ** (0.0029) |

| Board size | 0.1475 *** (0.0283) | −0.1377 ** (0.0406) |

| Years | ||

| 2010 | −0.0095 (0.1756) | 0.0084 (0.1764) |

| 2011 | 0.0298 (0.1720) | 0.0401 (0.1731) |

| 2012 | −0.0193 (0.1721) | −0.012 (0.1730) |

| 2013 | −0.0108 (0.1698) | −0.0069 (0.1711) |

| 2014 | 0.0157 (0.1675) | 0.0217 (0.1691) |

| 2015 | −0.0372 (0.1661) | −0.0388 (0.1684) |

| 2016 | −0.0315 (0.1616) | −0.0282 (0.1638) |

| 2017 | 0.0035 (0.1594) | −0.0148 (0.1623) |

| 2018 | −0.0351 (0.1566) | −0.0624 (0.1588) |

| N. of obs. | 1361 | 1361 |

| Wald chi2 | 129.1500 *** | 180.6300 *** |

| Pseudo R2 | 0.0585 | 0.0858 |

| Log pseudolikelihood | −615.6870 | −597.8401 |

| (i) | |

|---|---|

| Benefit company | 0.8462 *** (0.1872) |

| Control variables | |

| Firm age | 0.0026 ** (0.0008) |

| ROS | −0.0020 ** (0.0010) |

| Firm size | −0.0349 *** (0.0058) |

| Independent directors | 0.0880 *** (0.0230) |

| Directors age | 0.0002 (0.0009) |

| Board size | −0.2247 *** (0.0593) |

| Years | |

| 2010 | - |

| 2011 | 0.0094 (0.0476) |

| 2012 | −0.0061 (0.0459) |

| 2013 | −0.0058 (0.0447) |

| 2014 | 0.0106 (0.0450) |

| 2015 | −0.0110 (0.0448) |

| 2016 | −0.0126 (0.0435) |

| 2017 | 0.0033 (0.0444) |

| 2018 | −0.0232 (0.0439) |

| N. of obs. | 1163 |

| F | 9.0500 *** |

| Centred R2 | −0.0586 |

| Uncentred R2 | 0.1940 |

| Root MSE | 0.3394 |

| Hansen J statistic (chi-square, p-value) | 1.2610 (0.5324) |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Boffa, D.; Prencipe, A.; D’Amico, L.; Corsi, C. Gender Inclusiveness and Female Representation on the Board of Directors of the Benefit Company Model: Evidence from Italy. Sustainability 2023, 15, 5852. https://doi.org/10.3390/su15075852

Boffa D, Prencipe A, D’Amico L, Corsi C. Gender Inclusiveness and Female Representation on the Board of Directors of the Benefit Company Model: Evidence from Italy. Sustainability. 2023; 15(7):5852. https://doi.org/10.3390/su15075852

Chicago/Turabian StyleBoffa, Danilo, Antonio Prencipe, Luciano D’Amico, and Christian Corsi. 2023. "Gender Inclusiveness and Female Representation on the Board of Directors of the Benefit Company Model: Evidence from Italy" Sustainability 15, no. 7: 5852. https://doi.org/10.3390/su15075852