Pursuing the Sustainability of Real Estate Market: The Case of Chinese Land Resources Diversification

Abstract

:1. Introduction

2. Literature Review

2.1. Ripple Effects across Different Regions

2.2. Heterogeneity of Different Submarkets and Real Estate Portfolios

3. Portfolio Theory and Research Methodology

3.1. Ripple Effects across Different Regions

3.2. The Long-Run Equilibrium Model: Cointegration and the ECM

3.3. Toda-Yamamoto (TY) Causality Test: Individual Ripple Effects

4. Data Description

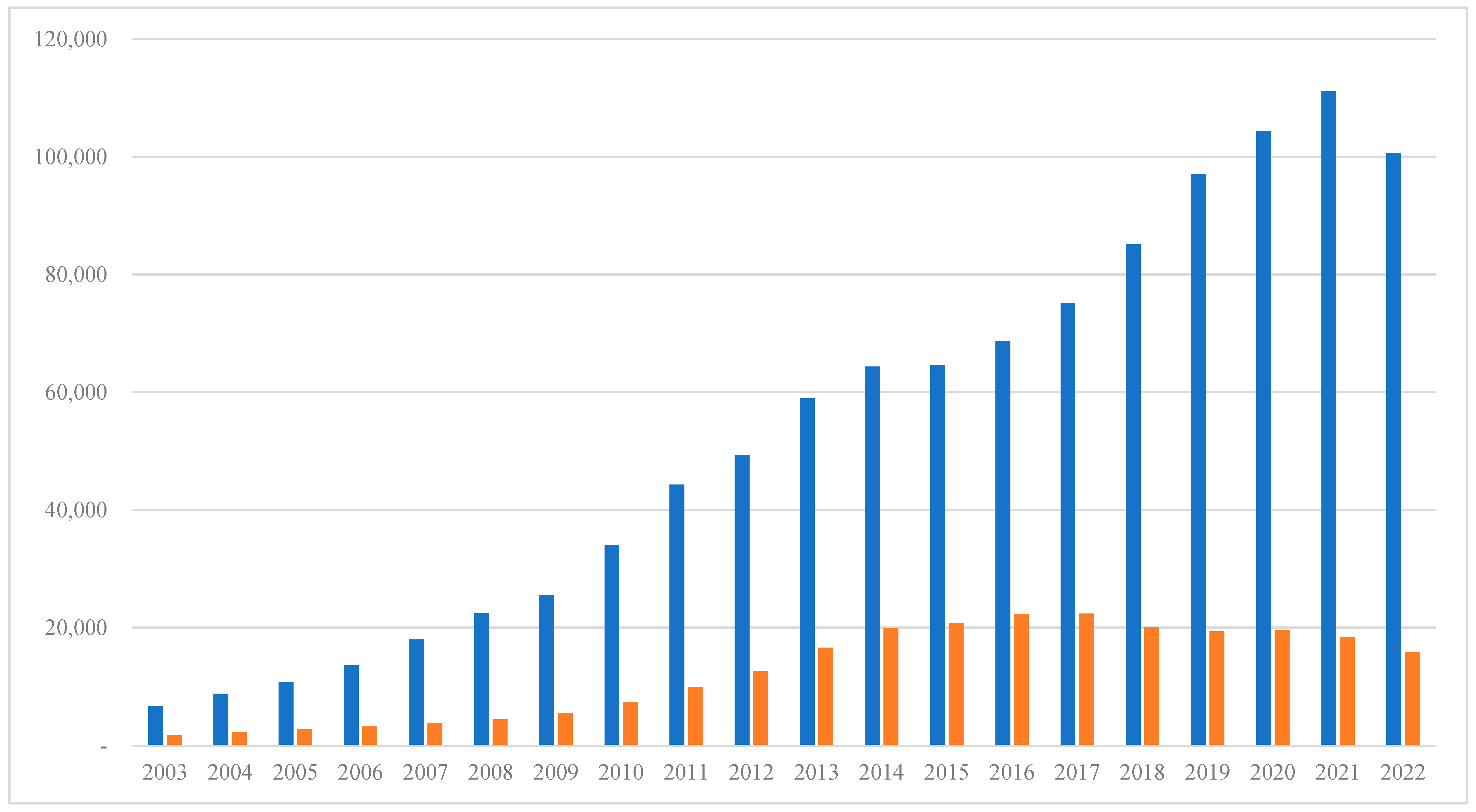

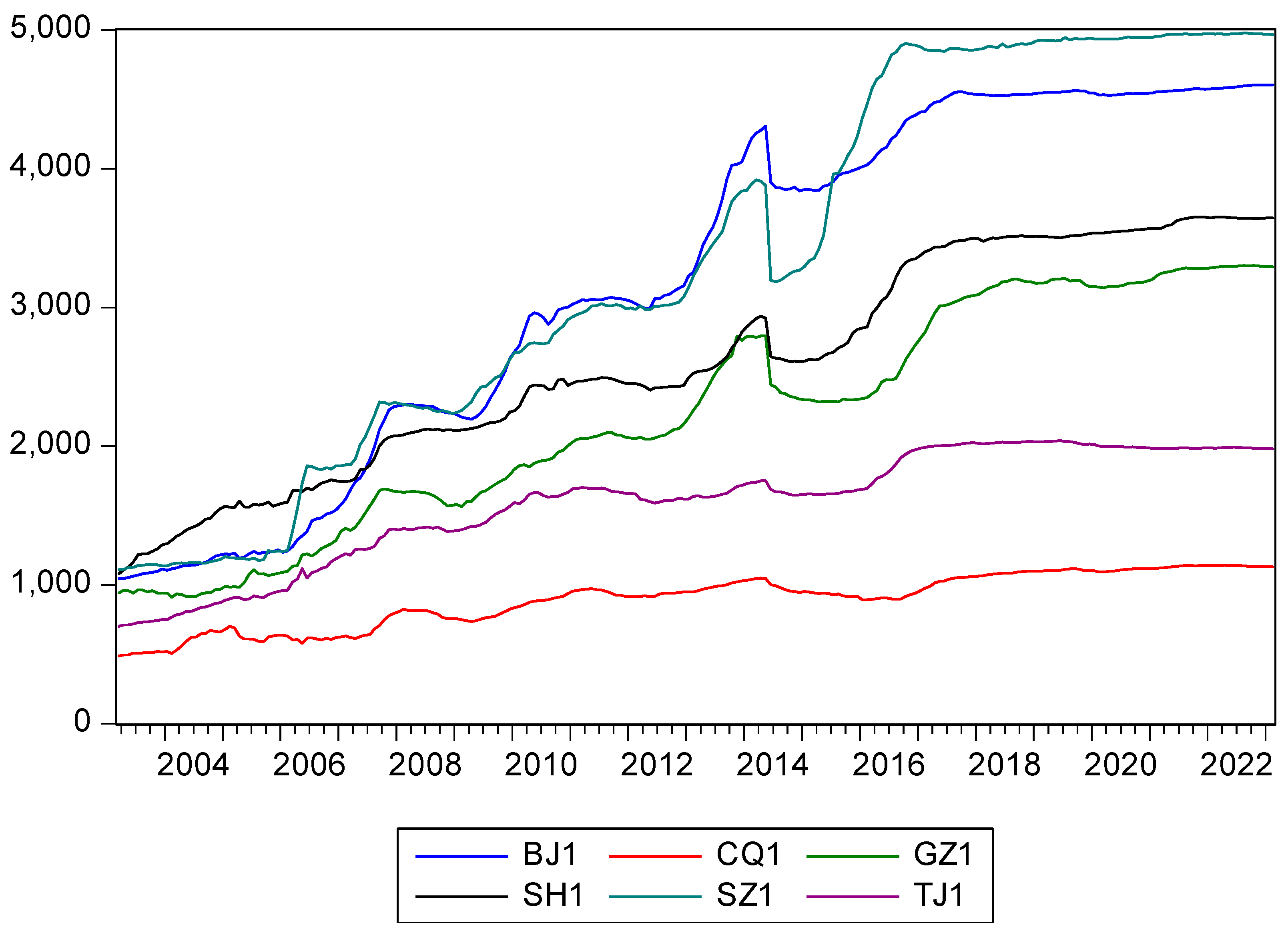

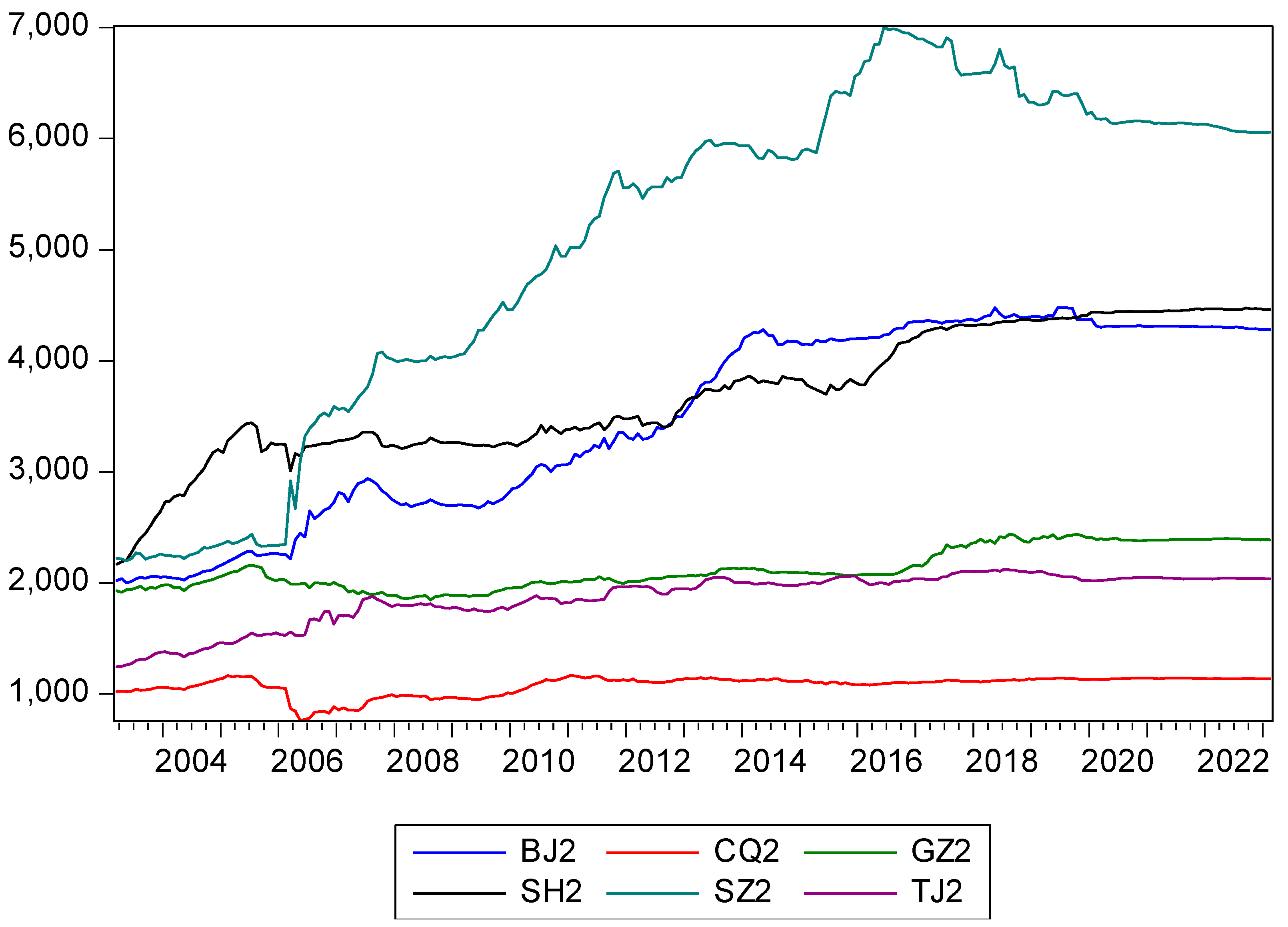

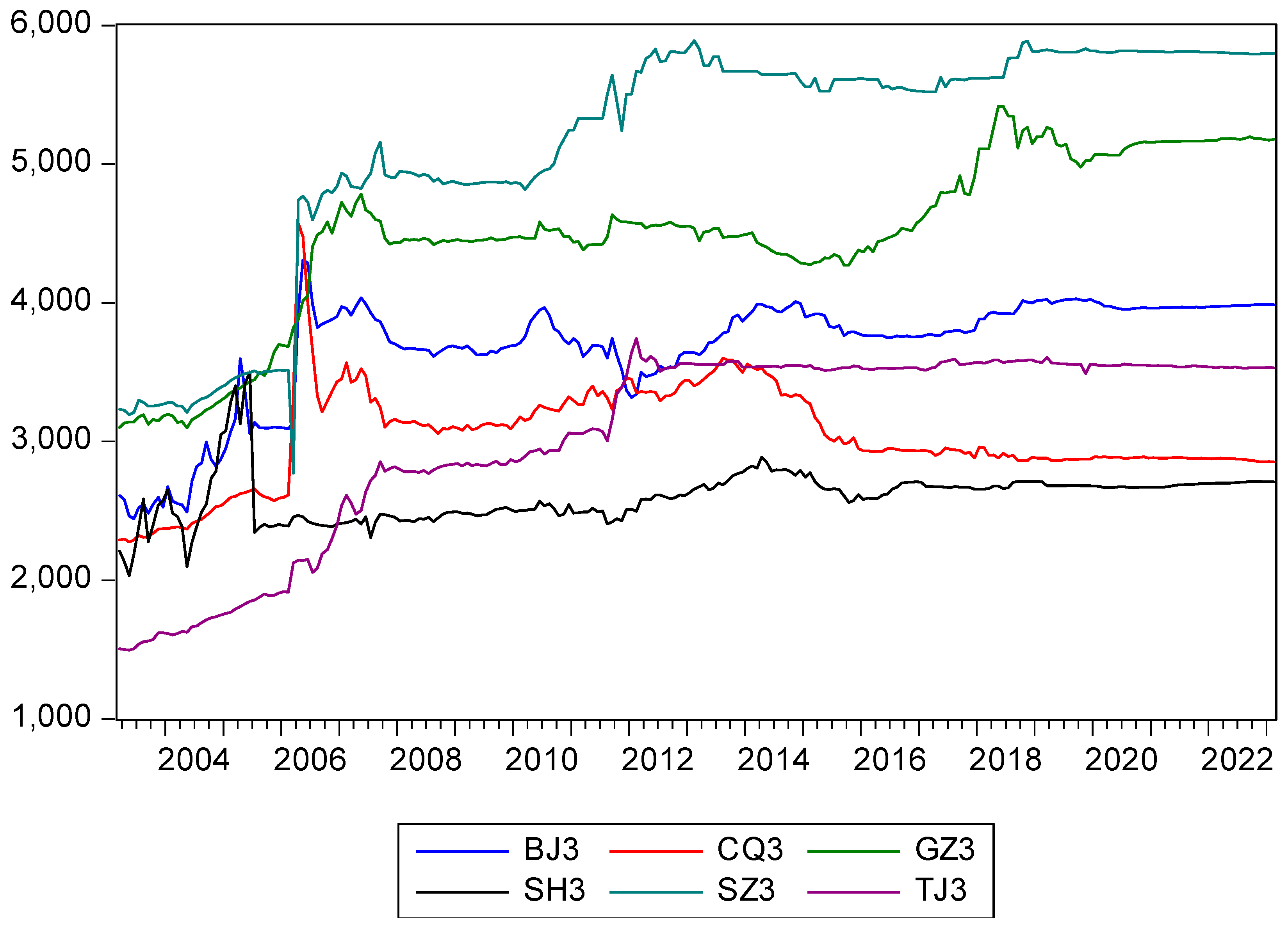

4.1. Real Estate Submarket Price Data for China’s Mega-Cities

4.2. Real Estate Development in the Six Mega-Cities

5. Estimation Results and Policy Considerations

5.1. Long-Run Equilibrium and the ECM: Evidence of Ripple Effects

5.2. Ripple Effects across the Six Cities in the Three Submarkets

5.3. Policy Implications

6. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Zhang, C.; An, G.; Yu, X. What drives China’s house prices: Marriage or money? China World Econ. 2012, 20, 19–36. [Google Scholar] [CrossRef]

- Yang, Z.; Chen, J. Housing Reform and the Housing Market in Urban China (Chapter 2) from Housing Affordability and Housing Policy in Urban China; Springer: Berlin, Germany, 2014. [Google Scholar]

- Hui, E.C.M.; Chan, K.K.K. Foreign direct investment in China’s real estate market. Habitat Int. 2014, 43, 231–239. [Google Scholar] [CrossRef]

- Chen, J.; Guo, F.; Wu, Y. One decade of urban housing reform in China: Urban housing price dynamics and the role of migration and urbanization, 1995–2005. Habitat Int. 2011, 35, 1–8. [Google Scholar] [CrossRef]

- Ofori, G.; Han, S. Testing hypotheses on construction and development using data on China’s provinces, 1990–2000. Habitat Int. 2003, 27, 37–62. [Google Scholar] [CrossRef]

- Chen, J.; Guo, F.; Zhu, A. The housing-led growth hypothesis revisited: Evidence from the Chinese provincial panel data. Urban Stud. 2011, 48, 2049–2067. [Google Scholar] [CrossRef]

- Kong, Y.; Glascock, J.L.; Lu-Andrews, R. An investigation into real estate investment and economic growth in China: A dynamic panel data approach. Sustainability 2016, 8, 66. [Google Scholar] [CrossRef] [Green Version]

- Wu, J.; Gyourko, J.; Deng, Y. Evaluating conditions in major Chinese housing markets. Reg. Sci. Urban Econ. 2012, 42, 531–543. [Google Scholar] [CrossRef] [Green Version]

- Glaeser, E.; Huang, W.; Ma, Y.; Shleifer, A. A real estate boom with Chinese characteristics. J. Econ. Perspect. 2017, 31, 93–116. [Google Scholar] [CrossRef] [Green Version]

- Weng, Y.; Gong, P. On price co-movement and volatility spillover effects in China’s housing markets. Int. J. Strateg. Prop. Manag. 2017, 21, 240–255. [Google Scholar] [CrossRef] [Green Version]

- Chen, C.; Chiang, S. Time-varying spillovers among first-tier housing markets in China. Urban Stud. 2020, 57, 844–864. [Google Scholar] [CrossRef]

- Tan, Z.; Tang, Q.; Meng, J. The effect of monetary policy on China’s housing prices before and after 2017: A dynamic analysis in DSGE model. Land Use Policy 2022, 113, 105927. [Google Scholar] [CrossRef]

- Zhang, C. Money, housing and inflation in China. J. Policy Model. 2013, 35, 75–87. [Google Scholar] [CrossRef]

- Chiang, S. Rising residential rents in Chinese mega cities: The role of monetary policy. Urban Stud. 2016, 53, 3493–3509. [Google Scholar] [CrossRef]

- Toda, H.Y.; Yamamoto, T. Statistical inference in vector autoregressions with possibly integrated processes. J. Econom. 1995, 66, 225–250. [Google Scholar] [CrossRef]

- Giussani, B.; Hadjimatheou, G. Modelling regional house prices in the UK. Pap. Reg. Sci. 1991, 70, 201–219. [Google Scholar] [CrossRef]

- MacDonald, R.; Taylor, M. Regional house prices in Britain: Long-run relationships and short-run dynamics. Scott. J. Political Econ. 1993, 40, 43–55. [Google Scholar] [CrossRef]

- Drake, L. Testing for convergence between UK regional house prices. Reg. Stud. 1995, 29, 357–366. [Google Scholar] [CrossRef]

- Alexander, C.; Barrow, M. Seasonality and cointegration of regional house prices in the UK. Urban Stud. 1994, 31, 1667–1689. [Google Scholar] [CrossRef]

- Holly, S.; Pesaran, H.; Yamagata, T. The spatial and temporal diffusion of house prices in the UK. J. Urban Econ. 2011, 69, 2–23. [Google Scholar] [CrossRef] [Green Version]

- Cascio, I.L. A wavelet analysis of the ripple effect in UK regional housing markets. Int. Rev. Econ. Financ. 2021, 76, 1093–1105. [Google Scholar] [CrossRef]

- Luo, Z.; Liu, C.; Picken, D. Housing price diffusion pattern of Australia’s state capital cities. Int. J. Strateg. Prop. Manag. 2007, 11, 227–242. [Google Scholar] [CrossRef] [Green Version]

- Liu, C.; Luo, Z.Q.; Ma, L.; Picken, D. Identifying house price diffusion patterns among Australian state capital cities. Int. J. Strateg. Prop. Manag. 2008, 12, 237–250. [Google Scholar] [CrossRef] [Green Version]

- Shi, S.; Young, M.; Hargreaves, B. The ripple effect of local house price movements in New Zealand. J. Prop. Res. 2009, 26, 1–24. [Google Scholar] [CrossRef]

- Hurn, S.; Shi, S.; Wang, B. Housing networks and driving forces. J. Bank. Financ. 2022, 134, 106318. [Google Scholar] [CrossRef]

- Lee, C.; Chien, M. Empirical modeling of regional house prices and the ripple effect. Urban Stud. 2011, 48, 2029–2047. [Google Scholar] [CrossRef]

- Chen, P.; Chien, M.; Lee, C. Dynamic modeling of regional house price diffusion in Taiwan. J. Hous. Econ. 2011, 20, 315–332. [Google Scholar] [CrossRef]

- Chien, M. Structural breaks and the convergence of regional house prices. J. Real Estate Financ. Econ. 2010, 40, 77–88. [Google Scholar] [CrossRef]

- Balcilar, M.; Beyene, A.; Gupta, R.; Seleteng, M. ‘Ripple’ effects in South African house prices. Urban Stud. 2013, 50, 876–894. [Google Scholar] [CrossRef] [Green Version]

- Gupta, R.; André, C.; Gil-Alana, L. Comovement in Euro area housing prices: A fractional cointegration approach. Urban Stud. 2014, 51, 3123–3143. [Google Scholar] [CrossRef] [Green Version]

- Helgers, R.; Buyst, E. Spatial and temporal diffusion of housing prices in the presence of a linguistic border: Evidence from Belgium. Spat. Econ. Anal. 2016, 11, 92–122. [Google Scholar] [CrossRef]

- Teye, A.L.; Ahelegbey, D.F. Detecting spatial and temporal house price diffusion in the Netherlands: A Bayesian network approach. Reg. Sci. Urban Econ. 2017, 65, 56–64. [Google Scholar] [CrossRef] [Green Version]

- Gupta, R.; Miller, S.S. “Ripple effects” and forecasting home prices in Los Angeles, Las Vegas and Phoenix. Ann. Reg. Sci. 2012, 48, 763–782. [Google Scholar] [CrossRef] [Green Version]

- Yunus, N.; Swanson, P.E. A closer look at the U.S. housing market: Modeling relationships among regions. Real Estate Econ. 2013, 41, 542–568. [Google Scholar] [CrossRef]

- Cohen, J.P.; Zabel, J. Local house price diffusion. Real Estate Econ. 2020, 48, 710–743. [Google Scholar] [CrossRef]

- Tsai, I. Features of the ripple effect in the US regional housing markets: A viewpoint of nonsynchronous trading. Int. J. Urban Sci. 2022, 26, 373–397. [Google Scholar] [CrossRef]

- Ranjbar, O.; Gholipour, H.F.; Saboori, B.; Chang, T. Tehran’s house price ripple effects in Iran: Application of bootstrap asymmetric panel Granger non-causality in the frequency domain. Hous. Stud. 2022, 37, 1566–1597. [Google Scholar] [CrossRef]

- Chiang, S. Housing markets in China and policy implications: Co-movement or ripple effect. China World Econ. 2014, 22, 103–120. [Google Scholar] [CrossRef]

- Lee, C.; Lee, C.; Chiang, S. Ripple effect and regional house prices dynamics in China. Int. J. Strateg. Prop. Manag. 2016, 20, 397–408. [Google Scholar] [CrossRef] [Green Version]

- Gong, Y.; Hu, J.; Boelhouwer, P.J. Spatial interrelations of Chinese housing markets: Spatial causality, convergence and diffusion. Reg. Sci. Urban Econ. 2016, 59, 103–117. [Google Scholar] [CrossRef]

- Zhang, F.; Morley, B. The convergence of regional house prices in China. Appl. Econ. Lett. 2014, 21, 205–208. [Google Scholar] [CrossRef] [Green Version]

- Mao, G. Do regional house prices converge or diverge in China? China Econ. J. 2016, 9, 154–166. [Google Scholar] [CrossRef]

- Chow, W.W.; Fung, M.K.; Cheng, A.C.S. Convergence and spillover of house prices in Chinese cities. Appl. Econ. 2016, 48, 4922–4941. [Google Scholar] [CrossRef]

- Xiao, Q. Equilibrating ripple effect, disturbing information cascade effect and regional disparity—A perspective from China’s tiered housing markets. Int. J. Financ. Econ. 2023, 28, 858–878. [Google Scholar] [CrossRef]

- Gyourko, J.; Linneman, P. Owner-occupied homes, income-producing properties and REITs as inflation hedges: Empirical findings. J. Real Estate Financ. Econ. 1988, 1, 347–372. [Google Scholar] [CrossRef]

- Wheaton, W.C. Real estate “Cycles”: Some fundamentals. Real Estate Econ. 1999, 27, 209–230. [Google Scholar] [CrossRef]

- Ghebreegziabiher, D.; Pels, E.; Rietveld, P. The impact of railway stations on residential and commercial property value: A meta-analysis. J. Real Estate Financ. Econ. 2007, 35, 161–180. [Google Scholar]

- Davis, M. The price and quantity of land by legal form of organization in the United States. Reg. Sci. Urban Econ. 2009, 39, 350–359. [Google Scholar] [CrossRef]

- Nichols, J.B.; Onliner, S.D.; Mulhall, M.R. Swings in commercial and residential land prices in the United States. J. Urban Econ. 2013, 73, 57–76. [Google Scholar] [CrossRef]

- Gyourko, J. Understanding commercial real estate: How different from housing is it? J. Portf. Manag. 2009, 35, 23–37. [Google Scholar] [CrossRef]

- Hui, E.C.M.; Zheng, X. Exploring the dynamic relationship between housing and retail property markets: An empirical study of Hong Kong. J. Prop. Res. 2012, 29, 85–102. [Google Scholar] [CrossRef]

- Chiang, S. Interaction among real estate properties in China using three submarket panels. Habitat Int. 2016, 53, 243–253. [Google Scholar] [CrossRef]

- Kishor, N.K. Comovements and spillovers in international commercial and residential real estate markets. J. Eur. Real Estate Res. 2022, 15, 311–331. [Google Scholar] [CrossRef]

- Ibbotson, R.G.; Fall, C.L. The United States market wealth portfolio. J. Portf. Manag. 1979, 6, 82–92. [Google Scholar] [CrossRef]

- Gyourko, J.; Nelling, E. Systematic risk and diversification in the equity REIT market. Real Estate Econ. 1996, 24, 493–515. [Google Scholar] [CrossRef]

- Capozza, D.R.; Seguin, P.J. Managerial style and firm value. Real Estate Econ. 1998, 26, 131–150. [Google Scholar] [CrossRef] [Green Version]

- Chen, J.; Peiser, R. The risk and return characteristics of REITs. Real Estate Financ. 1999, 16, 61–68. [Google Scholar]

- Brown, R.J.; Li, L.; Lusht, K. A note on intracity geographic diversification of real estate portfolios: Evidence from Hong Kong. J. Real Estate Portf. Manag. 2000, 6, 131–140. [Google Scholar] [CrossRef]

- Chan, S.; Erickson, J.; Wang, K. Real Estate Investment Trust: Structure, Performance and Investment Opportunities; Oxford University Press: Oxford, UK, 2003. [Google Scholar]

- Hartzell, D.; Heckman, J.; Miles, M. Diversification categories in investment real estate. Real Estate Econ. 1986, 14, 230–254. [Google Scholar] [CrossRef]

- Clayton, J.; MacKinnon, G. The time-varying nature of the link between REIT, real estate and financial asset returns. J. Real Estate Portf. Manag. 2001, 7, 43–54. [Google Scholar] [CrossRef]

- Heston, S.L.; Rouwenhorst, G.K. Does industrial structure explain the benefits of international diversification? J. Financ. Econ. 1994, 36, 3–27. [Google Scholar] [CrossRef]

- Van Dijk, R.; Keijzer, T. Region, sector and style selection in global equity markets. J. Asset Manag. 2004, 4, 293–307. [Google Scholar] [CrossRef]

- Hamelink, F.; Hoesli, M. What factors determine international real estate security returns? Real Estate Econ. 2004, 32, 437–462. [Google Scholar] [CrossRef] [Green Version]

- Gallo, J.G.; Zhang, Y. Global property market diversification. J. Real Estate Financ. Econ. 2010, 41, 458–485. [Google Scholar] [CrossRef]

- De Wit, I. International diversification strategies for direct real estate. J. Real Estate Financ. Econ. 2010, 41, 433–457. [Google Scholar] [CrossRef]

- Clapp, J.M.; Tirtiroglu, D. Positive feedback trading and diffusion of asset price changes: Evidence from housing transactions. J. Econ. Behav. Organ. 1994, 24, 337–355. [Google Scholar] [CrossRef]

- Clapp, J.M.; Dolde, W.; Tirtiroglu, D. Imperfect information and investor inferences from housing price dynamics. Real Estate Econ. 1995, 23, 239–269. [Google Scholar] [CrossRef]

- Dolde, W.; Tirtiroglu, D. Temporal and spatial information diffusion in real estate price changes and variances. Real Estate Econ. 1997, 25, 539–565. [Google Scholar] [CrossRef]

- Fernando, F.; Gyourko, J. Heterogeneity in neighborhood-level price growth in the United States, 1993–2009. Am. Econ. Rev. 2012, 102, 134–140. [Google Scholar]

- DeFusco, A.; Ding, W.; Ferreira, F.; Gyourko, J. The role of price spillovers in the American housing boom. J. Urban Econ. 2018, 108, 72–84. [Google Scholar] [CrossRef]

- Zhu, E.; Wu, J.; Liu, H.; Li, X. Within-city spatial distribution, heterogeneity and diffusion of house price: Evidence from a spatiotemporal index for Beijing. Real Estate Econ. 2022, 50, 621–655. [Google Scholar] [CrossRef]

- Hu, J.; Xiong, X.; Cai, Y.; Yuan, F. The ripple effect and spatiotemporal dynamics of intra-urban housing prices at the submarket level in Shaghai, China. Sustainability 2020, 12, 5073. [Google Scholar] [CrossRef]

- Grigoryeva, I.; Ley, D. The price ripple effect in the Vancouver housing market. Urban Geogr. 2019, 40, 1168–1190. [Google Scholar] [CrossRef]

- Bangura, M.; Lee, C.L. House price diffusion of housing submarkets in Greater Sydney. Hous. Stud. 2020, 35, 1110–1141. [Google Scholar] [CrossRef]

- Kim, L.; Seo, W. Micro-analysis of price spillover effect among regional housing submarkets in Korea: Evidence from the Seoul metropolitan area. Land 2021, 10, 879. [Google Scholar] [CrossRef]

- Ho, L.; Ma, Y.; Haurin, D.R. Domino effects within a housing market: The transmission of house price changes across quality tiers. J. Real Estate Financ. Econ. 2008, 37, 299–311. [Google Scholar] [CrossRef]

- Brzezicka, J.; Laszek, J.; Olszewski, K.; Waszczuk, J. Analysis of the filtering process and the ripple effect on the primary and secondary housing market in Warsaw, Poland. Land Use Policy 2019, 88, 204098. [Google Scholar] [CrossRef]

- Markowitz, H.M. Portfolio selection. J. Financ. 1952, 7, 77–91. [Google Scholar]

- Meen, G.P. Regional house prices and the ripple effect: A new interpretation. Hous. Stud. 1999, 33, 425–444. [Google Scholar] [CrossRef]

- Hui, E.C.M.; Yue, S. Housing price bubbles in Hong Kong, Beijing and Shanghai: A comparative study. J. Real Estate Financ. Econ. 2006, 33, 299–327. [Google Scholar] [CrossRef]

- Tsai, I.; Chiang, S. Exuberance and spillovers in housing markets: Evidence from first- and second-tier cities in China. Reg. Sci. Urban Econ. 2019, 77, 75–86. [Google Scholar] [CrossRef]

- Chiang, S.; Hui, E.C.M.; Chen, C. Asymmetric housing information diffusions in China: An investor perspective. Urban Stud. 2022, 59, 2036–2052. [Google Scholar] [CrossRef]

- Johansen, S. Likelihood-based Inference in Cointegrated Vector Autoregressive Models; Oxford University Press: Oxford, UK, 1995. [Google Scholar]

- MacKinnon, J.G.; Haug, A.A.; Michelis, L. Numerical distribution functions of likelihood ratio tests for cointegration. J. Appl. Econom. 1999, 14, 563–577. [Google Scholar] [CrossRef]

- Black, A.; Fraser, P.; Hoesli, M. House prices, fundamentals and bubbles. J. Bus. Financ. Account. 2006, 33, 1535–1555. [Google Scholar] [CrossRef]

- Phillips, P.C.B.; Shi, S.; Yu, J. Specification sensitivity in right-tailed unit root testing for explosive behaviour. Oxf. Bull. Econ. Stat. 2014, 76, 315–333. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Mean | 3202.787 | 894.6708 | 2219.500 | 2610.208 | 3321.000 | 1586.246 |

| Median | 3302.500 | 937.0000 | 2282.000 | 2533.500 | 3191.000 | 1657.000 |

| Maximum | 4606.000 | 1142.000 | 3303.000 | 3653.000 | 4978.000 | 2039.000 |

| Minimum | 1046.000 | 487.0000 | 911.0000 | 1080.000 | 1111.000 | 703.0000 |

| Std. Dev. | 1273.626 | 192.6036 | 801.4528 | 774.0704 | 1387.401 | 404.5648 |

| Mean | 3482.354 | 1077.275 | 2123.221 | 3693.671 | 5065.242 | 1865.2 |

| Median | 3649 | 1115 | 2074 | 3663 | 5814.5 | 1971 |

| Maximum | 4479 | 1165 | 2439 | 4474 | 7004 | 2122 |

| Minimum | 2000 | 761 | 1846 | 2167 | 2196 | 1245 |

| Std. dev. | 857.08 | 85.917 | 183.877 | 572.51 | 1521.7 | 230.297 |

| Mean | 3678.427 | 3035.433 | 4481.642 | 2601.735 | 5134.871 | 3049.521 |

| Median | 3786 | 2952 | 4496 | 2651.25 | 5553 | 3526 |

| Maximum | 4309 | 4572 | 5416 | 3501.5 | 5891 | 3743 |

| Minimum | 2442 | 2275 | 3099 | 2031.5 | 2771 | 1495 |

| Std. dev. | 403.346 | 351.472 | 593.003 | 184.192 | 845.373 | 680.339 |

| 2.577 | −2.642 * | −0.623 | |

| 2.023 | −2.229 | −2.399 | |

| 2.795 | −1.715 | −1.277 | |

| 4.046 | −3.661 *** | −2.767 | |

| 2.524 | −1.922 | −1.284 | |

| 2.995 | −3.994 *** | −1.873 | |

| 2.439 | −2.169 | −0.839 | |

| 0.252 | −2.200 | −2.719 | |

| 1.325 | −0.643 | −1.845 | |

| 3.796 | −4.619 *** | −5.066 *** | |

| 1.866 | −2.418 | −1.025 | |

| 2.529 | −3.688 *** | −2.497 | |

| 1.180 | −3.329 *** | −3.239 * | |

| 0.504 | −2.632 * | −2.547 | |

| 2.721 | −2.661 * | −1.869 | |

| 0.336 | −4.764 *** | −5.211 *** | |

| −1.593 | −2.420 | −1.945 | |

| 2.831 | −3.674 *** | −1.600 | |

| −4.334 *** | −6.094 *** | −8.712 *** | |

| −10.132 *** | −10.419 *** | −10.535 *** | |

| −6.975 *** | −7.655 *** | −11.570 *** | |

| −5.370 *** | −11.197 *** | −11.781 *** | |

| −8.808 *** | −9.307 *** | −9.437 *** | |

| −6.400 *** | −7.248 *** | −8.204 *** | |

| −5.549 *** | −6.150 *** | −6.501 *** | |

| −7.986 *** | −7.975 *** | −7.958 *** | |

| −8.572 *** | −8.689 *** | −8.680 *** | |

| −13.328 *** | −14.033 *** | −14.494 *** | |

| −5.557 *** | −5.930 *** | −6.367 *** | |

| −14.182 *** | −14.524 *** | −14.953 *** | |

| −11.541 *** | −11.617 *** | −11.723 *** | |

| −10.533 *** | −10.531 *** | −10.661 *** | |

| −4.959 *** | −5.176 *** | −14.083 *** | |

| −8.557 *** | −8.553 *** | −8.553 *** | |

| −11.748 *** | −14.893 *** | −15.024 *** | |

| −11.392 *** | −11.947 *** | −12.645 *** |

| BJ | CQ | GZ | SH | SZ | TJ | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Types | A | B | A | B | A | B | A | B | A | B | A | B |

| 2003 | 0.756 | 0.244 | 0.739 | 0.261 | 0.828 | 0.172 | 0.834 | 0.166 | 0.801 | 0.199 | 0.825 | 0.175 |

| 2004 | 0.733 | 0.267 | 0.747 | 0.253 | 0.793 | 0.207 | 0.847 | 0.153 | 0.757 | 0.243 | 0.799 | 0.201 |

| 2005 | 0.716 | 0.284 | 0.772 | 0.228 | 0.762 | 0.238 | 0.818 | 0.182 | 0.766 | 0.234 | 0.814 | 0.186 |

| 2006 | 0.661 | 0.339 | 0.821 | 0.179 | 0.738 | 0.262 | 0.749 | 0.251 | 0.768 | 0.232 | 0.84 | 0.16 |

| 2007 | 0.661 | 0.339 | 0.85 | 0.15 | 0.783 | 0.217 | 0.726 | 0.274 | 0.799 | 0.201 | 0.777 | 0.223 |

| 2008 | 0.696 | 0.304 | 0.87 | 0.13 | 0.79 | 0.21 | 0.702 | 0.298 | 0.801 | 0.199 | 0.806 | 0.194 |

| 2009 | 0.712 | 0.288 | 0.85 | 0.15 | 0.729 | 0.271 | 0.711 | 0.289 | 0.766 | 0.234 | 0.792 | 0.208 |

| 2010 | 0.717 | 0.283 | 0.868 | 0.132 | 0.678 | 0.322 | 0.724 | 0.276 | 0.758 | 0.242 | 0.734 | 0.266 |

| 2011 | 0.729 | 0.271 | 0.842 | 0.158 | 0.723 | 0.277 | 0.753 | 0.247 | 0.777 | 0.223 | 0.706 | 0.294 |

| 2012 | 0.711 | 0.289 | 0.807 | 0.193 | 0.702 | 0.298 | 0.723 | 0.277 | 0.802 | 0.198 | 0.778 | 0.222 |

| 2013 | 0.65 | 0.35 | 0.797 | 0.203 | 0.718 | 0.282 | 0.684 | 0.316 | 0.799 | 0.201 | 0.788 | 0.212 |

| 2014 | 0.628 | 0.372 | 0.775 | 0.225 | 0.658 | 0.342 | 0.635 | 0.365 | 0.767 | 0.233 | 0.767 | 0.233 |

| 2015 | 0.581 | 0.419 | 0.745 | 0.255 | 0.713 | 0.287 | 0.618 | 0.382 | 0.748 | 0.252 | 0.778 | 0.222 |

| 2016 | 0.619 | 0.381 | 0.727 | 0.273 | 0.701 | 0.299 | 0.618 | 0.382 | 0.652 | 0.348 | 0.809 | 0.191 |

| 2017 | 0.606 | 0.394 | 0.761 | 0.239 | 0.738 | 0.262 | 0.652 | 0.348 | 0.536 | 0.464 | 0.847 | 0.153 |

| 2018 | 0.708 | 0.292 | 0.818 | 0.182 | 0.757 | 0.243 | 0.659 | 0.341 | 0.583 | 0.417 | 0.901 | 0.099 |

| 2019 | 0.761 | 0.239 | 0.835 | 0.165 | 0.769 | 0.231 | 0.669 | 0.331 | 0.608 | 0.392 | 0.906 | 0.094 |

| 2020 | 0.808 | 0.192 | 0.856 | 0.144 | 0.771 | 0.229 | 0.635 | 0.365 | 0.634 | 0.366 | 0.902 | 0.098 |

| 2021 | 0.836 | 0.164 | 0.869 | 0.131 | 0.811 | 0.189 | 0.676 | 0.324 | 0.631 | 0.369 | 0.899 | 0.101 |

| r | Specification 1 | Specification 2 | Specification 3 |

|---|---|---|---|

| Residential form | |||

| 0 | 199.895 *** | 183.540 *** | 197.246 *** |

| 1 | 124.355 *** | 114.417 *** | 125.583 *** |

| 2 | 77.283 *** | 70.212 *** | 80.591 *** |

| 3 | 35.716 *** | 31.160 ** | 41.462 |

| Office form | |||

| 0 | 157.532 *** | 147.178 *** | 159.189 *** |

| 1 | 89.407 *** | 82.628 *** | 94.339 *** |

| 2 | 54.588 ** | 47.946 *** | 55.102 |

| 3 | 29.343 | 22.945 | 31.101 |

| Retail form | |||

| 0 | 153.456 *** | 140.669 *** | 170.321 *** |

| 1 | 98.705 *** | 91.718 *** | 118.180 *** |

| 2 | 63.140 *** | 57.226 *** | 74.410 *** |

| 3 | 34.337 * | 31.530 ** | 37.202 |

| Outcomes | BJ | CQ | GZ | SH | SZ | TJ | |

|---|---|---|---|---|---|---|---|

| Causes | |||||||

| BJ | 2.082 | 4.950 * | 5.479 * | 0.241 | 13.868 *** | ||

| CQ | 2.136 | 8.169 *** | 0.322 | 10.841 *** | 14.007 *** | ||

| GZ | 10.407 *** | 4.034 | 0.136 | 1.477 | 19.965 *** | ||

| SH | 7.429 ** | 1.729 | 1.225 | 0.673 | 5.898 *** | ||

| SZ | 2.118 * | 0.593 | 0.559 | 1.483 | 2.338 | ||

| TJ | 1.870 | 4.272 | 1.549 | 2.748 | 1.001 | ||

| Abbreviations | 1. GZ → BJ 2. SH → BJ | 4. BJ → GZ 5. CQ → GZ | 6. BJ → SH | 7. CQ → SZ | 8. BJ → TJ 9. CQ → TJ | ||

| 3. SZ → BJ | 10. GZ → TJ 11. SH → TJ | ||||||

| Conclusions | BJ GZ (1 and 4); BJ SH (2 and 6); SZ → BJ (3); CQ → GZ (5); CQ → SZ (7); BJ → TJ (8); CQ → TJ (9); GZ → TJ (10); SH → TJ (11) | ||||||

| Outcomes | BJ | CQ | GZ | SH | SZ | TJ | |

|---|---|---|---|---|---|---|---|

| Causes | |||||||

| BJ | 2.082 | 3.950 | 5.479 * | 0.241 | 40.48 *** | ||

| CQ | 2.136 | 8.169 *** | 0.322 | 10.84 *** | 14.001 *** | ||

| GZ | 10.407 *** | 4.034 | 0.131 | 1.447 | 19.965 *** | ||

| SH | 2.327 | 1.729 | 1.225 | 0.673 * | 5.898 ** | ||

| SZ | 2.118 | 0.593 | 0.559 | 1.483 | 2.338 | ||

| TJ | 1.870 | 4.270 | 1.549 | 2.748 | 1.001 | ||

| Abbreviations | 1. GZ → BJ | 2.CQ → GZ | 3. BJ → SH | 4. CQ → SZ 5. SH → SZ | 6. BJ → TJ 7. CQ → TJ 8. GZ → TJ 9. SH → TJ | ||

| Conclusions | All are uni-directional causalities | ||||||

| Outcomes | BJ | CQ | GZ | SH | SZ | TJ | |

|---|---|---|---|---|---|---|---|

| Causes | |||||||

| BJ | 0.283 | 2.716 | 1.137 | 7.471 ** | 0.835 | ||

| CQ | 4.367 | 5.942 * | 0.093 | 6.818 *** | 27.750 *** | ||

| GZ | 1.920 | 0.922 | 0.172 | 0.410 | 1.420 | ||

| SH | 2.970 | 0.081 | 4.412 | 3.921 | 0.006 | ||

| SZ | 38.792 *** | 1.102 | 0.512 | 13.819 *** | 15.775 *** | ||

| TJ | 1.012 | 10.770 *** | 0.276 | 2.566 | 1.138 | ||

| Abbreviations | 1. SZ → BJ | 2.TJ → CQ | 3. CQ → GZ | 4. SZ → SH | 5. BJ → SZ 6. CQ → SZ | 7. CQ → TJ 8. SZ → TJ | |

| Conclusions | BJ SZ (1 and 5); CQ TJ (2 and 7); CQ → GZ (3); SZ → SH (4); CQ → SZ (6); SZ → TJ (8) | ||||||

| Sources | Number of Causalities | Bi-Directional (Co-Movement) | Uni-Directional (Ripple Effects) | |

|---|---|---|---|---|

| Housing | BJ and CQ | 11 | 2 | 7 |

| Office | CQ | 9 | 0 | 9 |

| Retail | SZ and CQ | 8 | 2 | 4 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lee, C.-W.; Chiang, S.-H.; Wen, Z.-Q. Pursuing the Sustainability of Real Estate Market: The Case of Chinese Land Resources Diversification. Sustainability 2023, 15, 5850. https://doi.org/10.3390/su15075850

Lee C-W, Chiang S-H, Wen Z-Q. Pursuing the Sustainability of Real Estate Market: The Case of Chinese Land Resources Diversification. Sustainability. 2023; 15(7):5850. https://doi.org/10.3390/su15075850

Chicago/Turabian StyleLee, Cheng-Wen, Shu-Hen Chiang, and Zhong-Qin Wen. 2023. "Pursuing the Sustainability of Real Estate Market: The Case of Chinese Land Resources Diversification" Sustainability 15, no. 7: 5850. https://doi.org/10.3390/su15075850