Social Responsibility: Opportunities for Integral Assessment and Analysis of Connections with Business Innovation

Abstract

:1. Introduction

2. Literature Review

3. Materials and Methods

- (1)

- Calculation of a comprehensive indicator of country-level social responsibility;

- (2)

- Assessment of the links between the country-level social responsibility and indicators characterizing business innovation.

- -

- The indicator is normalised and varies between 0 and 1, which makes it easy to interpret its value (values close to 1 correspond to a high level of development; values close to 0 correspond to a low level of development);

- -

- The indicator is focused on the study of objects or processes characterised by a large number of heterogeneous parameters;

- -

- The indicator is a synthetic value that considers the influence of the values of all individual indicators;

- -

- The indicator allows organising multidimensional objects or processes with respect to a given normative reference vector.

- (1)

- Standardisation of initial data for their reduction into a single scale of measurement, which is carried out according to the formulawhere is a standardised value of the i-th indicator for the j-th EU country ( = ; = ); is an arithmetic mean value of the i-th indicator for the j-th EU country; is a root mean square deviation of the i-th indicator;

- (2)

- Formation of a reference point (, ,…). Since the proposed indicators are stimulators, i.e., they exert a direct positive influence on the development of social responsibility in EU countries, the maximum values of the indicator are chosen for themwhere I is a set of indicators–stimulators.

- (3)

- Construction of the Euclidean distance, which characterises the distance of the value of each indicator to the reference pointwhere is the Euclidean distance of the indicator value to the reference point;

- (4)

- Calculation of a taxonomic indicator reflecting a comprehensive assessment of the level of social responsibility development in EU countries ()where is a comprehensive assessment of the level of social responsibility development in a separate EU country; is the arithmetic mean value of the corresponding Euclidean distance; is the root mean square deviation of the corresponding Euclidean distance.

4. Results

5. Discussion and Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Sendlhofer, T. Decoupling from moral responsibility for CSR: Employees’ visionary procrastination at a SME. J. Bus. Ethics 2020, 167, 361–378. [Google Scholar] [CrossRef] [Green Version]

- Vuong, Q.H.; La, V.P.; Nguyen, H.K.T.; Ho, M.T.; Vuong, T.T.; Ho, M.T. Identifying the moral–practical gaps in corporate social responsibility missions of Vietnamese firms: An event-based analysis of sustainability feasibility. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 30–41. [Google Scholar] [CrossRef]

- Jastrzębska, E.; Legutko-Kobus, P. Implementation of Sustainable Development by Cities and Businesses in Poland. Evolution of the Approach. Stud. Ecol. Bioethicae 2022, 1, 53–66. [Google Scholar] [CrossRef]

- Patuelli, A.; Carungu, J.o.; Lattanzi, N. Drivers and nuances of sustainable development goals: Transcending corporate social responsibility in family firms. J. Clean. Prod. 2022, 373, 133723. [Google Scholar] [CrossRef]

- Tarí, J.J.; Pereira-Moliner, J.; Molina-Azorín, J.F.; López-Gamero, M.D. A Taxonomy of Quality Standard Adoption: Its Relationship with Quality Management and Performance in Tourism Organizations In Spain. J. Tour. Serv. 2020, 21, 22–37. [Google Scholar] [CrossRef]

- Chen, C.C.; Khan, A.; Hongsuchon, T.; Ruangkanjanases, A.; Chen, Y.T.; Sivarak, O.; Chen, S.C. The role of corporate social responsibility and corporate image in times of crisis: The mediating role of customer trust. Int. J. Environ. Res. Public Health 2021, 18, 8275. [Google Scholar] [CrossRef]

- Stawicka, E. Sustainable Development in the Digital Age of Entrepreneurship. Sustainability 2021, 13, 4429. [Google Scholar] [CrossRef]

- Streimikiene, D.; Ahmed, R.R. The integration of corporate social responsibility and marketing concepts as a business strategy: Evidence from SEM-based multivariate and Toda-Yamamoto causality models. Oeconomia Copernic. 2021, 12, 125–157. [Google Scholar] [CrossRef]

- Vo, D.H.; Van, L.-T.H.; Dinh, L.-T.H.; Ho, C.M. Financial inclusion, corporate social responsibility and customer loyalty in the banking sector in Vietnam. J. Int. Stud. 2020, 13, 9–23. [Google Scholar] [CrossRef]

- Ye, H.; Kueh, T.-B.; Hou, L.; Liu, Y.; Yu, H. A bibliometric analysis of corporate social responsibility in sustainable development. J. Clean. Prod. 2020, 272, 122679. [Google Scholar] [CrossRef]

- OESD. Business Innovation Statistics and Indicators. 2021. Available online: https://www.oecd.org/innovation/inno/inno-stats.htm (accessed on 14 January 2023).

- Çera, G.; Belas, J.; Marousek, J.; Çera, E. Do size and age of small and medium-sized enterprises matter in corporate social responsibility? Econ. Sociol. 2020, 13, 86–99. [Google Scholar] [CrossRef]

- Myšková, R.; Hájek, P. Relationship between corporate social responsibility in corporate annual reports and financial performance of the US companies. J. Int. Stud. 2019, 12, 269–282. [Google Scholar] [CrossRef] [Green Version]

- Jurkowska-Gomułka, A.; Kurczewska, K.; Bilan, Y. Corporate social responsibility in public administration. Case of Polish central administrative institutions. Adm. Manag. Public 2021, 36, 116–133. [Google Scholar] [CrossRef]

- Metzker, Z.; Streimikis, J. CSR activities in the Czech SME segment. Int. J. Entrep. Knowl. 2020, 8, 49–64. [Google Scholar] [CrossRef]

- Oliinyk, O. Social responsibility assessment in the field of employment (case study of manufacturing). Nauk. Visnyk Natsionalnoho Hirnychoho Universytetu 2020, 3, 131–136. [Google Scholar] [CrossRef]

- Hrybinenko, O.; Bulatova, O.; Zakharova, O. Evaluation of demographic component of countries’ economic security. Bus. Manag. Econ. Eng. 2020, 18, 307–330. [Google Scholar] [CrossRef]

- Makarenko, I.; Plastun, A.; Kozmenko, S.; Kozmenko, O.; Rudychenko, A. Corporate Transparency, Sustainable Development and SDG 2 and 12 in Agriculture: The Case of Ukraine. AGRIS-Line Pap. Econ. Inform. 2022, 14, 57–70. [Google Scholar] [CrossRef]

- Fallah Shayan, N.; Mohabbati-Kalejahi, N.; Alavi, S.; Zahed, M.A. Sustainable Development Goals (SDGs) as a Framework for Corporate Social Responsibility (CSR). Sustainability 2022, 14, 1222. [Google Scholar] [CrossRef]

- Kulkarni, V.; Aggarwal, A. A Theoretical Review of whether Corporate Social Responsibility (CSR) Complement Sustainable Development Goals (SDGs) Needs. Theor. Econ. Lett. 2022, 12, 575–600. [Google Scholar] [CrossRef]

- Liczmańska-Kopcewicz, K.; Mizera, K.; Pypłacz, P. Corporate social responsibility and sustainable development for creating value for FMCG sector enterprises. Sustainability 2019, 11, 5808. [Google Scholar] [CrossRef] [Green Version]

- Gond, J.; Augustine, G.; Shin, H.; Tirapani, A.; Mosonyi, S. How Corporate Social Responsibility and Sustainable Development Functions Impact the Workplace: A Review of the Literature, ILO Working Paper 71 (Geneva, ILO). 2022. Available online: https://www.ilo.org/wcmsp5/groups/public/---dgreports/---inst/documents/publication/wcms_850856.pdf (accessed on 15 January 2023).

- Aluchna, M.; Roszkowska-Menkes, M. Integrating Corporate Social Responsibility and Corporate Governance at the Company Level. Towards a Conceptual Model. Inz. Ekon.-Eng. Econ. 2019, 30, 349–361. [Google Scholar] [CrossRef] [Green Version]

- Mukhuty, S.; Upadhyay, A.; Rothwell, H. Strategic sustainable development of Industry 4.0 through the lens of social responsibility: The role of human resource practices. Bus. Strategy Environ. 2022, 31, 2068–2081. [Google Scholar] [CrossRef]

- Skerhakova, V.; Kobra, P.; Harnicarova, M.; Ali Taha, V. Talent Retention: Analysis of the Antecedents of Talented Employees’ Intention to Stay in the Organizations. Eur. J. Interdiscip. Stud. 2022, 14, 56–67. [Google Scholar] [CrossRef]

- Iershova, N.Y.; Portna, O.V.; Uhrimova, I.V.; Chaika, T.Y. The Impact of Employee Attitudes on the Effectiveness of Corporate Governance and Social External Effects: Business Analytics Platform. Montenegrin J. Econ. 2022, 18, 73–84. [Google Scholar] [CrossRef]

- Murillo-Avalos, C.L.; Cubilla-Montilla, M.; Celestino Sánchez, M.Á.; Vicente-Galindo, P. What environmental social responsibility practices do large companies manage for sustainable development? Corp. Soc. Responsib. Environ. Manag. 2021, 28, 153–168. [Google Scholar] [CrossRef]

- Gaur, A.; Vazquez-Brust, D.A. Sustainable Development Goals: Corporate Social Responsibility? A Critical Analysis of Interactions in the Construction Industry Supply Chains Using Externalities Theory. Sustainable Development Goals and Sustainable Supply Chains in the Post-global Economy. Green. Ind. Netw. Stud. 2019, 7, 133–157. [Google Scholar] [CrossRef]

- Safonchyk, O.; Vitman, K. Prospects of corporate social responsibility development in the EU in sustainable development. Balt. J. Econ. Stud. 2019, 5, 212–220. [Google Scholar] [CrossRef]

- Mishchuk, H.; Štofková, J.; Krol, V.; Joshi, O.; Vasa, L. Social Capital Factors Fostering the Sustainable Competitiveness of Enterprises. Sustainability 2022, 14, 11905. [Google Scholar] [CrossRef]

- Oliinyk, O.O. Corporate social responsibility in the field of occupational safety and health. In Naukovyi Visnyk Natsionalnoho Hirnychoho Universytetu; State Higher Educational Institution National Mining University Ukraine: Dnipro, Ukraine, 2017; pp. 128–133. [Google Scholar]

- Samoliuk, N.; Bilan, Y.; Mishchuk, H.; Mishchuk, V. Employer brand: Key values influencing the intention to join a company. Management & Marketing. Chall. Knowl. Soc. 2022, 17, 61–72. [Google Scholar] [CrossRef]

- Almashhadani, M. Internal Control Mechanisms, CSR, and Profitability: A. Int. J. Bus. Manag. Invent. 2021, 10, 38–43. [Google Scholar]

- Devie, D.; Liman, L.P.; Tarigan, J.; Jie, F. Corporate social responsibility, financial performance and risk in Indonesian natural resources industry. Soc. Responsib. J. 2020, 16, 73–90. [Google Scholar] [CrossRef]

- Mishchuk, H.; Samoliuk, N.; Yurchyk, H. Decent Work: Evaluation and Ensuring in Human Capital Management: Monograph: Szczecin: Centre of Sociological Research. 2021. 140p. Available online: https://csr-pub.eu/?49,en_decent-work-evaluation-and-ensuring-in-human-capital-management (accessed on 14 January 2023).

- Maldonado-Erazo, C.P.; Álvarez-García, J.; del Río-Rama MD, L.C.; Correa-Quezada, R. Corporate social responsibility and performance in SMEs: Scientific coverage. Sustainability 2020, 12, 2332. [Google Scholar] [CrossRef] [Green Version]

- Li, W.; Bhutto, M.Y.; Waris, I.; Hu, T. The Nexus between Environmental Corporate Social Responsibility, Green Intellectual Capital and Green Innovation towards Business Sustainability: An Empirical Analysis of Chinese Automobile Manufacturing Firms. Int. J. Environ. Res. Public Health 2023, 20, 1851. [Google Scholar] [CrossRef]

- Brammer, S.J.; Pavelin, S. Corporate Reputation and Social Performance: The Importance of Fit. J. Manag. Stud. 2006, 43, 435–455. [Google Scholar] [CrossRef]

- Calabrese, A.; Costa, R.; Gastaldi, M.; Ghiron, N.L.; Montalvan RA, V. Implications for Sustainable Development Goals: A framework to assess company disclosure in sustainability reporting. J. Clean. Prod. 2021, 319, 128624. [Google Scholar] [CrossRef]

- SOLABILITY. The Global Sustainable Competitiveness Index 2021. 2021. Available online: https://solability.com/the-global-sustainable-competitiveness-index/the-index (accessed on 13 January 2023).

- Lafortune, G.; Cortés Puch, M.; Mosnier, A.; Fuller, G.; Diaz, M.; Riccaboni, A.; Kloke-Lesch, A.; Zachariadis, T.; Carli, E.; Oger, A. Europe Sustainable Development Report 2021: Transforming the European Union to Achieve the Sustainable Development Goals. SDSN 2021, SDSN Europe and IEEP. Available online: https://s3.amazonaws.com/sustainabledevelopment.report/2021/Europe+Sustainable+Development+Report+2021.pdf (accessed on 12 January 2023).

- Social Progress Imperative. Social Progress Index 2021. Executive Summary. 2021. Available online: https://www.socialprogress.org/static/9e62d6c031f30344f34683259839760d/2021%20Social%20Progress%20Index%20Executive%20Summary-compressed_0.pdf (accessed on 14 January 2023).

- Pluta, W. Wielowymiarowa Analiza Porównawcza w Badaniach Ekonomicznych: Metody Taksonomiczne i Analizy Czynnikowej; Państwowe Wydawnictwo Ekonomiczne: Warszawa, Poland, 1977; 150p. [Google Scholar]

- Oliinyk, O.; Mishchuk, H.; Bilan, Y.; Skare, M. Integrated assessment of the attractiveness of the EU for intellectual immigrants: A taxonomy-based approach. Technol. Forecast. Soc. Change 2022, 182, 121805. [Google Scholar] [CrossRef]

- Sroczyńska, K.; Chainho, P.; Vieira, S.; Adão, H. What makes a better indicator? Taxonomic vs functional response of nematodes to estuarine gradient. Ecol. Indic. 2021, 121, 107113. [Google Scholar] [CrossRef]

- WIPO. Global Innovation Index 2021. Tracking Innovation through the COVID-19 Crisis. 2021. Available online: https://www.wipo.int/edocs/pubdocs/en/wipo_pub_gii_2021.pdf (accessed on 14 January 2023).

- WIPO. The Global Innovation Index (GII) Conceptual Framework. 2017. Available online: https://www.wipo.int/edocs/pubdocs/en/wipo_pub_gii_2017-annex1.pdf (accessed on 15 January 2023).

- SOLABILITY. The Global Sustainable Competitiveness Index 2020. 2020. Available online: https://solability.com/sustainability-publications/the-global-sustainable-competitiveness-index-2 (accessed on 16 January 2023).

- SDSN & IEEP. The 2020 Europe Sustainable Development Report: Meeting the Sustainable Development Goals in the Face of the COVID-19 Pandemic; Sustainable Development Solutions Network: Paris, France; Institute for European Environmental Policy: Brussels, Belgium, 2020; Available online: https://www.sdgindex.org/reports/europe-sustainable-development-report-2020/ (accessed on 14 January 2023).

- SDSN & IEEP. The 2019 Europe Sustainable Development Report; Sustainable Development Solutions Network: Paris, France; Institute for European Environmental Policy: Brussels, Belgium, 2019; Available online: https://s3.amazonaws.com/sustainabledevelopment.report/2019/2019_europe_sustainable_development_report.pdf (accessed on 14 January 2023).

- Green, M.; Harmacek, J.; Htitich, M.; Krylova, P.; Social Progress Index 2020. Executive Summary. 2020. Available online: https://www.socialprogress.org/static/37348b3ecb088518a945fa4c83d9b9f4/2020-social-progress-index-executive-summary.pdf (accessed on 15 January 2023).

- Social Progress Imperative. Social Progress Index 2019. 2019. Available online: https://www2.deloitte.com/content/dam/Deloitte/at/Documents/presse/at-social-progress-index-2019-global.pdf (accessed on 15 January 2023).

- Salas-Velasco, M. Production efficiency measurement and its determinants across OECD countries: The role of business sophistication and innovation. Econ. Anal. Policy 2018, 57, 60–73. [Google Scholar] [CrossRef]

- Zhou, H.; Wang, Q.; Zhao, X. Corporate social responsibility and innovation: A comparative study. Ind. Manag. Data Syst. 2020, 120, 863–882. [Google Scholar] [CrossRef]

- Bocquet, R.; Le Bas, C.; Mothe, C.; Poussingc, N. Strategic CSR for innovation in SMEs: Does diversity matter? Long Range Plan. 2019, 52, 101913. [Google Scholar] [CrossRef]

- Rozsa, Z.; Tupa, M.; Belas, J., Jr.; Metzker, Z.; Suler, P. CSR conception and its prospective implementation in the SMEs business of Visegrad countries. Transform. Bus. Econ. 2022, 21, 274–289. [Google Scholar]

- Ulewicz, R.; Blaskova, M. Sustainable development and knowledge management from the stakeholders’ point of view. Pol. J. Manag. Stud. 2018, 18, 363–374. [Google Scholar] [CrossRef]

{kind=link}

| Name | Publisher | Coverage of Countries | Components |

|---|---|---|---|

| The Global Sustainable Competitiveness Index | SolAbility | 180 | Natural capital (the given natural environment and climate, minus human-induced degradation and pollution), social capital, intellectual capital (the ability to compete in a globalised market through sustained innovation), resource management (the ability to extract the highest possible value from existing resources (natural, human and financial)), governance (the framework given, normally by government policies and investments in which a national economy operates) |

| The Sustainable Development Goals Index | Cambridge | 163 | SDG1—no poverty; SDG2—zero hunger; SDG3—good health and well-being; SDG4—quality education; SDG5—gender equality; SDG6—clean water and sanitation; SDG7—affordable and clean energy; SDG8—decent work and economic growth; SDG9—industry, innovation and infrastructure; SDG10—reduced inequalities; SDG11—sustainable cities and communities; SDG12—responsible consumption and production; SDG13—climate action; SDG14—life below water; SDG15—life on land; SDG16—peace, justice and strong institutions; SDG17—partnerships for the goals |

| The Social Progress Index | The Social Progress Imperative | 168 | Basic human needs (nutrition and basic medical care, water and sanitation, shelter and personal safety); foundations of well-being (access to basic knowledge, access to information and communications, health and wellness and environmental quality); opportunity (personal rights, personal freedom and choice, inclusiveness and access to advanced education) |

| Country | The Global Sustainable Competitiveness Index, Score | The SDG Index, Score | The Social Progress Index, Score | ||||||

|---|---|---|---|---|---|---|---|---|---|

| 2019 | 2020 | 2021 | 2019 | 2020 | 2021 | 2019 | 2020 | 2021 | |

| Belgium | 51.30 | 52.10 | 53.00 | 70.30 | 71.70 | 72.50 | 86.77 | 89.46 | 88.68 |

| Bulgaria | 49.20 | 51.60 | 49.60 | 57.10 | 55.80 | 57.60 | 76.17 | 79.86 | 78.81 |

| Czech Republic | 53.10 | 55.20 | 52.90 | 71.80 | 72.70 | 72.60 | 84.36 | 86.69 | 86.60 |

| Denmark | 57.00 | 61.00 | 60.20 | 79.80 | 80.10 | 79.30 | 90.09 | 92.11 | 92.15 |

| Germany | 53.50 | 54.60 | 56.60 | 75.30 | 74.60 | 75.30 | 88.84 | 90.56 | 90.32 |

| Estonia | 54.90 | 59.40 | 56.1 | 70.40 | 71.80 | 73.70 | 83.98 | 87.26 | 87.38 |

| Ireland | 53.60 | 56.80 | 57.6 | 68.20 | 68.70 | 70.60 | 87.97 | 90.35 | 89.47 |

| Greece | 47.40 | 50.00 | 49.60 | 58.90 | 62.00 | 64.80 | 82.48 | 85.78 | 84.37 |

| Spain | 48.50 | 51.80 | 52.70 | 66.80 | 67.80 | 68.50 | 87.47 | 88.71 | 87.53 |

| France | 52.00 | 55.50 | 56.80 | 74.70 | 73.00 | 72.70 | 87.79 | 88.78 | 88.23 |

| Croatia | 54.20 | 57.20 | 55.10 | 63.20 | 66.40 | 68.00 | 79.21 | 81.92 | 82.82 |

| Italy | 49.90 | 51.60 | 51.70 | 65.30 | 67.10 | 68.50 | 85.69 | 87.36 | 86.56 |

| Cyprus | 45.80 | 47.60 | 47.50 | 55.00 | 60.30 | 58.60 | 83.14 | 86.64 | 85.03 |

| Latvia | 54.40 | 58.20 | 53.50 | 65.20 | 68.30 | 69.30 | 80.42 | 83.19 | 83.43 |

| Lithuania | 50.60 | 55.90 | 53.00 | 62.60 | 64.40 | 66.10 | 81.30 | 83.97 | 85.58 |

| Luxembourg | 54.50 | 58.00 | 53.90 | 66.00 | 64.20 | 65.80 | 87.66 | 89.56 | 88.75 |

| Hungary | 49.20 | 52.90 | 50.80 | 65.10 | 68.70 | 68.50 | 78.77 | 81.02 | 80.15 |

| Malta | 46.60 | 50.90 | 51.70 | 62.30 | 62.40 | 63.60 | 82.63 | 84.89 | 85.24 |

| The Netherlands | 50.50 | 52.90 | 53.90 | 71.80 | 71.70 | 72.10 | 88.31 | 91.06 | 90.57 |

| Austria | 54.20 | 56.70 | 56.60 | 76.70 | 77.40 | 78.00 | 86.40 | 89.50 | 89.44 |

| Poland | 51.90 | 52.80 | 51.20 | 66.10 | 69.60 | 71.00 | 81.25 | 84.32 | 83.08 |

| Portugal | 51.10 | 55.00 | 54.80 | 66.20 | 67.50 | 69.10 | 87.12 | 87.79 | 85.97 |

| Romania | 50.80 | 54.50 | 52.30 | 55.90 | 58.30 | 61.60 | 74.81 | 78.35 | 78.41 |

| Slovenia | 53.80 | 55.90 | 54.30 | 71.70 | 74.00 | 73.50 | 85.80 | 87.71 | 85.83 |

| Slovakia | 51.60 | 54.90 | 53.10 | 65.20 | 68.80 | 70.00 | 80.43 | 83.15 | 83.69 |

| Finland | 59.50 | 60.40 | 60.70 | 79.10 | 81.10 | 80.80 | 89.56 | 91.89 | 92.26 |

| Sweden | 60.60 | 62.10 | 61.20 | 79.40 | 81.00 | 80.60 | 89.45 | 91.62 | 91.20 |

| Country | The Global Sustainable Competitiveness Index | The SDG Index | The Social Progress Index | ||||||

|---|---|---|---|---|---|---|---|---|---|

| 2019 | 2020 | 2021 | 2019 | 2020 | 2021 | 2019 | 2020 | 2021 | |

| Belgium | −0.25907 | 0.361203 | 0.57012 | −0.83261 | 0.377384 | −0.19084 | −0.32374 | 0.020421 | 0.618998 |

| Bulgaria | −0.85618 | −1.53193 | −1.94326 | −0.97525 | −2.05887 | −0.1966 | −1.33462 | −1.72761 | −2.00728 |

| Czech Republic | 0.252746 | 0.576331 | −0.00132 | 0.051774 | 0.530608 | −0.1925 | −0.35348 | 0.269764 | 0.065536 |

| Denmark | 1.361672 | 1.723682 | 1.357329 | 1.706423 | 1.664464 | −0.18924 | 1.816936 | 1.939992 | 1.542321 |

| Germany | 0.366482 | 1.078297 | 1.06094 | −0.1194 | 0.821733 | −0.19018 | 0.746596 | 0.823492 | 1.055381 |

| Estonia | 0.764558 | 0.375545 | −0.09142 | 1.249968 | 0.392707 | −0.19216 | 0.597937 | 0.318396 | 0.273084 |

| Ireland | 0.394916 | 0.060023 | 0.854653 | 0.508229 | −0.08229 | −0.1903 | 1.043912 | 0.333606 | 0.829207 |

| Greece | −1.36799 | −1.27377 | −0.44709 | −1.4317 | −1.10889 | −0.19305 | −1.33462 | −0.91306 | −0.52784 |

| Spain | −1.05522 | −0.14076 | 0.736098 | −0.91819 | −0.22019 | −0.19129 | −0.41294 | 0.086168 | 0.312998 |

| France | −0.06003 | 0.992246 | 0.811973 | 0.137359 | 0.576575 | −0.19124 | 0.806059 | 0.519903 | 0.499259 |

| Croatia | 0.56552 | −0.65707 | −1.22244 | 0.622342 | −0.4347 | −0.19537 | 0.30062 | −0.27012 | −0.94027 |

| Italy | −0.65714 | −0.35589 | 0.31404 | −0.97525 | −0.32744 | 5.003689 | −0.71026 | −0.41801 | 0.054893 |

| Cyprus | −1.82293 | −1.8331 | −0.29059 | −2.11639 | −1.36937 | −0.19253 | −1.95899 | −1.74474 | −0.35222 |

| Latvia | 0.622388 | −0.37023 | −0.93553 | 0.907627 | −0.14358 | −0.1946 | −0.17509 | 0.209511 | −0.77796 |

| Lithuania | −0.4581 | −0.74312 | −0.72688 | 0.251473 | −0.74115 | −0.19413 | −0.32374 | −1.35945 | −0.20587 |

| Luxembourg | 0.650822 | −0.2555 | 0.781149 | 0.85057 | −0.77179 | −0.19078 | −0.05616 | −1.25612 | 0.637624 |

| Hungary | −0.85618 | −0.38457 | −1.32677 | −0.60438 | −0.08229 | −0.19591 | −0.97784 | −0.2012 | −1.65073 |

| Malta | −1.59546 | −0.78615 | −0.41152 | −1.17495 | −1.0476 | −0.19358 | −0.71026 | −0.92475 | −0.29634 |

| The Netherlands | −0.48654 | 0.576331 | 0.935271 | −0.60438 | 0.377384 | −0.18988 | −0.05616 | 0.071758 | 1.121903 |

| Austria | 0.56552 | 1.279083 | 0.482389 | 0.4797 | 1.25076 | −0.19081 | 0.746596 | 0.867597 | 0.821224 |

| Poland | −0.08846 | −0.24116 | −0.73873 | −0.63291 | 0.055615 | −0.19392 | −0.85892 | 0.292805 | −0.87109 |

| Portugal | −0.31593 | −0.22681 | 0.653109 | −0.00528 | −0.26616 | −0.19184 | 0.211425 | −0.13068 | −0.1021 |

| Romania | −0.40124 | −1.70403 | −2.26573 | −0.14793 | −1.67581 | −0.19751 | −0.53187 | −0.61718 | −2.11372 |

| Slovenia | 0.451784 | 0.561989 | 0.340123 | 0.251473 | 0.729799 | −0.19189 | 0.062767 | 0.103269 | −0.13935 |

| Slovakia | −0.17376 | −0.37023 | −0.93316 | −0.03381 | −0.06696 | −0.19463 | −0.29401 | −0.31318 | −0.70878 |

| Finland | 2.072521 | 1.623289 | 1.23166 | 1.535252 | 1.817687 | −0.18938 | 1.965595 | 2.22293 | 1.571591 |

| Sweden | 2.385295 | 1.666314 | 1.205578 | 2.020236 | 1.802365 | −0.18954 | 2.114253 | 1.796486 | 1.289538 |

| Etalon | 2.385295 | 1.723682 | 1.357329 | 2.020236 | 1.817687 | 5.003689 | 2.114253 | 2.22293 | 1.571591 |

| 2019 | 2020 | 2021 | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Euclidean Distance | Ki | Euclidean Distance | Ki | Euclidean Distance | Ki | |||||||||||||

| Belgium | −2.6444 | −1.3625 | −0.7872 | 9.4687 | 3.0771 | 0.9072 | −2.8528 | −1.4403 | −5.1945 | 37.1963 | 6.0989 | 0.8882 | −2.4380 | −2.2025 | −0.9526 | 11.7023 | 3.4209 | 0.9017 |

| Bulgaria | −3.2415 | −3.2556 | −3.3006 | 32.0000 | 5.6569 | 0.8294 | −2.9955 | −3.8766 | −5.2003 | 51.0437 | 7.1445 | 0.8690 | −3.4489 | −3.9505 | −3.5789 | 40.3099 | 6.3490 | 0.8176 |

| Czech Republic | −2.1325 | −1.1474 | −1.3586 | 7.7101 | 2.7767 | 0.9163 | −1.9685 | −1.2871 | −5.1962 | 32.5318 | 5.7037 | 0.8954 | −2.4677 | −1.9532 | −1.5061 | 12.1727 | 3.4889 | 0.8997 |

| Denmark | −1.0236 | 0.0000 | 0.0000 | 1.0478 | 1.0236 | 0.9691 | −0.3138 | −0.1532 | −5.1929 | 27.0885 | 5.2047 | 0.9046 | −0.2973 | −0.2829 | −0.0293 | 0.1693 | 0.4115 | 0.9882 |

| Germany | −2.0188 | −0.6454 | −0.2964 | 4.5800 | 2.1401 | 0.9355 | −2.1396 | −0.9960 | −5.1939 | 32.5462 | 5.7049 | 0.8954 | −1.3677 | −1.3994 | −0.5162 | 4.0954 | 2.0237 | 0.9418 |

| Estonia | −1.6207 | −1.3481 | −1.4487 | 6.5431 | 2.5580 | 0.9229 | −0.7703 | −1.4250 | −5.1958 | 29.6207 | 5.4425 | 0.9002 | −1.5163 | −1.9045 | −1.2985 | 7.6126 | 2.7591 | 0.9207 |

| Ireland | −1.9904 | −1.6637 | −0.5027 | 6.9820 | 2.6424 | 0.9203 | −1.5120 | −1.9000 | −5.1940 | 32.8736 | 5.7336 | 0.8949 | −1.0703 | −1.8893 | −0.7424 | 5.2663 | 2.2948 | 0.9341 |

| Greece | −3.7533 | −2.9975 | −1.8044 | 26.3278 | 5.1311 | 0.8453 | −3.4519 | −2.9266 | −5.1967 | 47.4868 | 6.8911 | 0.8736 | −3.4489 | −3.1360 | −2.0994 | 26.1368 | 5.1124 | 0.8531 |

| Spain | −3.4405 | −1.8644 | −0.6212 | 15.6992 | 3.9622 | 0.8805 | −2.9384 | −2.0379 | −5.1950 | 39.7751 | 6.3067 | 0.8844 | −2.5272 | −2.1368 | −1.2586 | 12.5365 | 3.5407 | 0.8983 |

| France | −2.4453 | −0.7314 | −0.5454 | 6.8120 | 2.6100 | 0.9213 | −1.8829 | −1.2411 | −5.1949 | 32.0729 | 5.6633 | 0.8962 | −1.3082 | −1.7030 | −1.0723 | 5.7616 | 2.4003 | 0.9310 |

| Croatia | −1.8198 | −2.3808 | −2.5798 | 15.6348 | 3.9541 | 0.8808 | −1.3979 | −2.2524 | −5.1991 | 34.0575 | 5.8359 | 0.8930 | −1.8136 | −2.4930 | −2.5119 | 15.8140 | 3.9767 | 0.8857 |

| Italy | −3.0424 | −2.0796 | −1.0433 | 14.6695 | 3.8301 | 0.8845 | −2.9955 | −2.1451 | 0.0000 | 13.5745 | 3.6844 | 0.9324 | −2.8245 | −2.6409 | −1.5167 | 17.2528 | 4.1536 | 0.8806 |

| Cyprus | −4.2082 | −3.5568 | −1.6479 | 33.0756 | 5.7511 | 0.8266 | −4.1366 | −3.1871 | −5.1962 | 54.2697 | 7.3668 | 0.8649 | −4.0732 | −3.9677 | −1.9238 | 36.0347 | 6.0029 | 0.8275 |

| Latvia | −1.7629 | −2.0939 | −2.2929 | 12.7495 | 3.5707 | 0.8923 | −1.1126 | −1.9613 | −5.1983 | 32.1067 | 5.6663 | 0.8961 | −2.2893 | −2.0134 | −2.3496 | 14.8153 | 3.8491 | 0.8894 |

| Lithuania | −2.8434 | −2.4668 | −2.0842 | 18.5139 | 4.3028 | 0.8703 | −1.7688 | −2.5588 | −5.1978 | 36.6935 | 6.0575 | 0.8889 | −2.4380 | −3.5824 | −1.7775 | 21.9366 | 4.6837 | 0.8654 |

| Luxembourg | −1.7345 | −1.9792 | −0.5762 | 7.2575 | 2.6940 | 0.9188 | −1.1697 | −2.5895 | −5.1945 | 35.0560 | 5.9208 | 0.8914 | −2.1704 | −3.4790 | −0.9340 | 17.6867 | 4.2056 | 0.8792 |

| Hungary | −3.2415 | −2.1083 | −2.6841 | 22.1563 | 4.7070 | 0.8581 | −2.6246 | −1.9000 | −5.1996 | 37.5343 | 6.1265 | 0.8877 | −3.0921 | −2.4241 | −3.2223 | 25.8208 | 5.0814 | 0.8540 |

| Malta | −3.9808 | −2.5098 | −1.7688 | 25.2745 | 5.0274 | 0.8484 | −3.1952 | −2.8653 | −5.1973 | 45.4307 | 6.7402 | 0.8764 | −2.8245 | −3.1477 | −1.8679 | 21.3749 | 4.6233 | 0.8671 |

| The Netherlands | −2.8718 | −1.1474 | −0.4221 | 9.7420 | 3.1212 | 0.9059 | −2.6246 | −1.4403 | −5.1936 | 35.9362 | 5.9947 | 0.8901 | −2.1704 | −2.1512 | −0.4497 | 9.5404 | 3.0888 | 0.9112 |

| Austria | −1.8198 | −0.4446 | −0.8749 | 4.2748 | 2.0676 | 0.9377 | −1.5405 | −0.5669 | −5.1945 | 29.6775 | 5.4477 | 0.9001 | −1.3677 | −1.3553 | −0.7504 | 4.2705 | 2.0665 | 0.9406 |

| Poland | −2.4738 | −1.9648 | −2.0961 | 14.3735 | 3.7912 | 0.8857 | −2.6531 | −1.7621 | −5.1976 | 37.1593 | 6.0958 | 0.8882 | −2.9732 | −1.9301 | −2.4427 | 18.5318 | 4.3049 | 0.8763 |

| Portugal | −2.7012 | −1.9505 | −0.7042 | 11.5970 | 3.4054 | 0.8973 | −2.0255 | −2.0838 | −5.1955 | 35.4386 | 5.9530 | 0.8908 | −1.9028 | −2.3536 | −1.6737 | 11.9615 | 3.4585 | 0.9006 |

| Romania | −2.7865 | −3.4277 | −3.6231 | 32.6405 | 5.7132 | 0.8277 | −2.1682 | −3.4935 | −5.2012 | 43.9580 | 6.6301 | 0.8784 | −2.6461 | −2.8401 | −3.6853 | 28.6497 | 5.3525 | 0.8462 |

| Slovenia | −1.9335 | −1.1617 | −1.0172 | 6.1227 | 2.4744 | 0.9254 | −1.7688 | −1.0879 | −5.1956 | 31.3060 | 5.5952 | 0.8974 | −2.0515 | −2.1197 | −1.7109 | 11.6289 | 3.4101 | 0.9020 |

| Slovakia | −2.5591 | −2.0939 | −2.2905 | 16.1796 | 4.0224 | 0.8787 | −2.0540 | −1.8847 | −5.1983 | 34.7935 | 5.8986 | 0.8918 | −2.4083 | −2.5361 | −2.2804 | 17.4317 | 4.1751 | 0.8800 |

| Finland | −0.3128 | −0.1004 | −0.1257 | 0.1237 | 0.3517 | 0.9894 | −0.4850 | 0.0000 | −5.1931 | 27.2031 | 5.2157 | 0.9044 | −0.1487 | 0.0000 | 0.0000 | 0.0221 | 0.1487 | 0.9957 |

| Sweden | 0.0000 | −0.0574 | −0.1518 | 0.0263 | 0.1622 | 0.9951 | 0.0000 | −0.0153 | −5.1932 | 26.9699 | 5.1933 | 0.9048 | 0.0000 | −0.4264 | −0.2821 | 0.2614 | 0.5113 | 0.9853 |

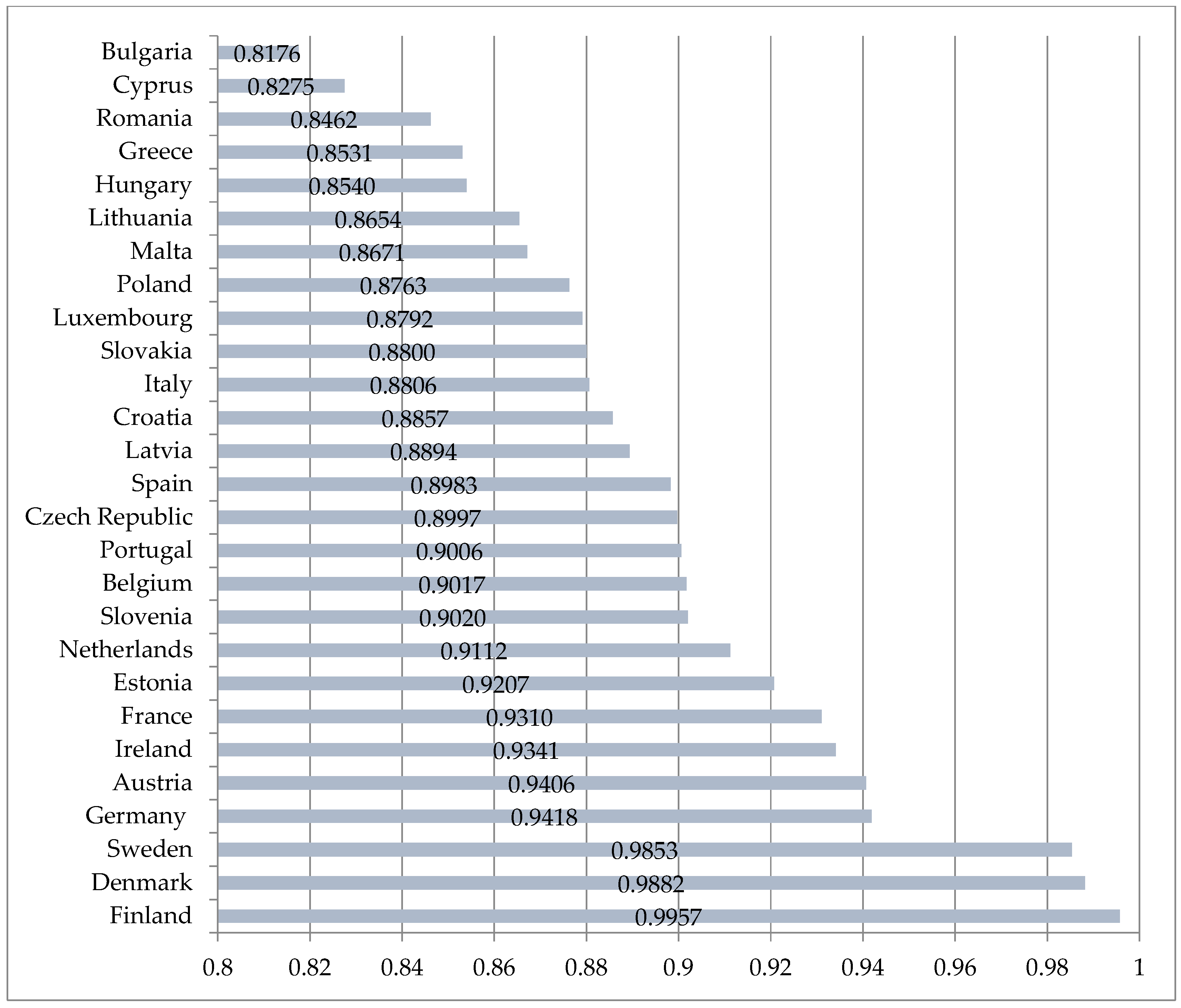

| Country | Ki | Business Sophistication | Innovative Firms (Product/Process), as a Percentage of Total SMEs |

|---|---|---|---|

| Belgium | 0.9017 | 51.7 | 60.88 |

| Bulgaria | 0.8176 | 32.6 | * |

| Czech Republic | 0.8997 | 43.5 | * |

| Denmark | 0.9882 | 55.2 | 56.50 |

| Germany | 0.9418 | 54.5 | 62.63 |

| Estonia | 0.9207 | 39.9 | 65.59 |

| Ireland | 0.9341 | 51.5 | * |

| Greece | 0.8531 | 25.9 | * |

| Spain | 0.8983 | 35.5 | 26.46 |

| France | 0.9310 | 50.4 | 45.73 |

| Croatia | 0.8857 | 27.7 | * |

| Italy | 0.8806 | 36.7 | 56.16 |

| Cyprus | 0.8275 | 42.6 | * |

| Latvia | 0.8894 | 34.1 | 29.39 |

| Lithuania | 0.8654 | 31.5 | 46.96 |

| Luxembourg | 0.8792 | 57.8 | * |

| Hungary | 0.8540 | 37.5 | 24.60 |

| Malta | 0.8671 | 53.7 | * |

| The Netherlands | 0.9112 | 61 | * |

| Austria | 0.9406 | 52.3 | 57.30 |

| Poland | 0.8763 | 34.2 | 20.34 |

| Portugal | 0.9006 | 33.6 | 35.34 |

| Romania | 0.8462 | 28 | * |

| Slovenia | 0.9020 | 42.8 | * |

| Slovakia | 0.8800 | 32.5 | 25.05 |

| Finland | 0.9957 | 61 | 54.41 |

| Sweden | 0.9853 | 68.1 | 60.25 |

| Correlation coefficient | 0.7002 | 0.6217 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Oliinyk, O.; Mishchuk, H.; Vasa, L.; Kozma, K. Social Responsibility: Opportunities for Integral Assessment and Analysis of Connections with Business Innovation. Sustainability 2023, 15, 5608. https://doi.org/10.3390/su15065608

Oliinyk O, Mishchuk H, Vasa L, Kozma K. Social Responsibility: Opportunities for Integral Assessment and Analysis of Connections with Business Innovation. Sustainability. 2023; 15(6):5608. https://doi.org/10.3390/su15065608

Chicago/Turabian StyleOliinyk, Olena, Halyna Mishchuk, Laszlo Vasa, and Katalin Kozma. 2023. "Social Responsibility: Opportunities for Integral Assessment and Analysis of Connections with Business Innovation" Sustainability 15, no. 6: 5608. https://doi.org/10.3390/su15065608