Analyzing the Impact of Digital Inclusive Finance on Poverty Reduction: A Study Based on System GMM in China

Abstract

:1. Introduction

2. Literature Review

3. Methodology and Data

3.1. Methodology

3.2. Empirical Specification

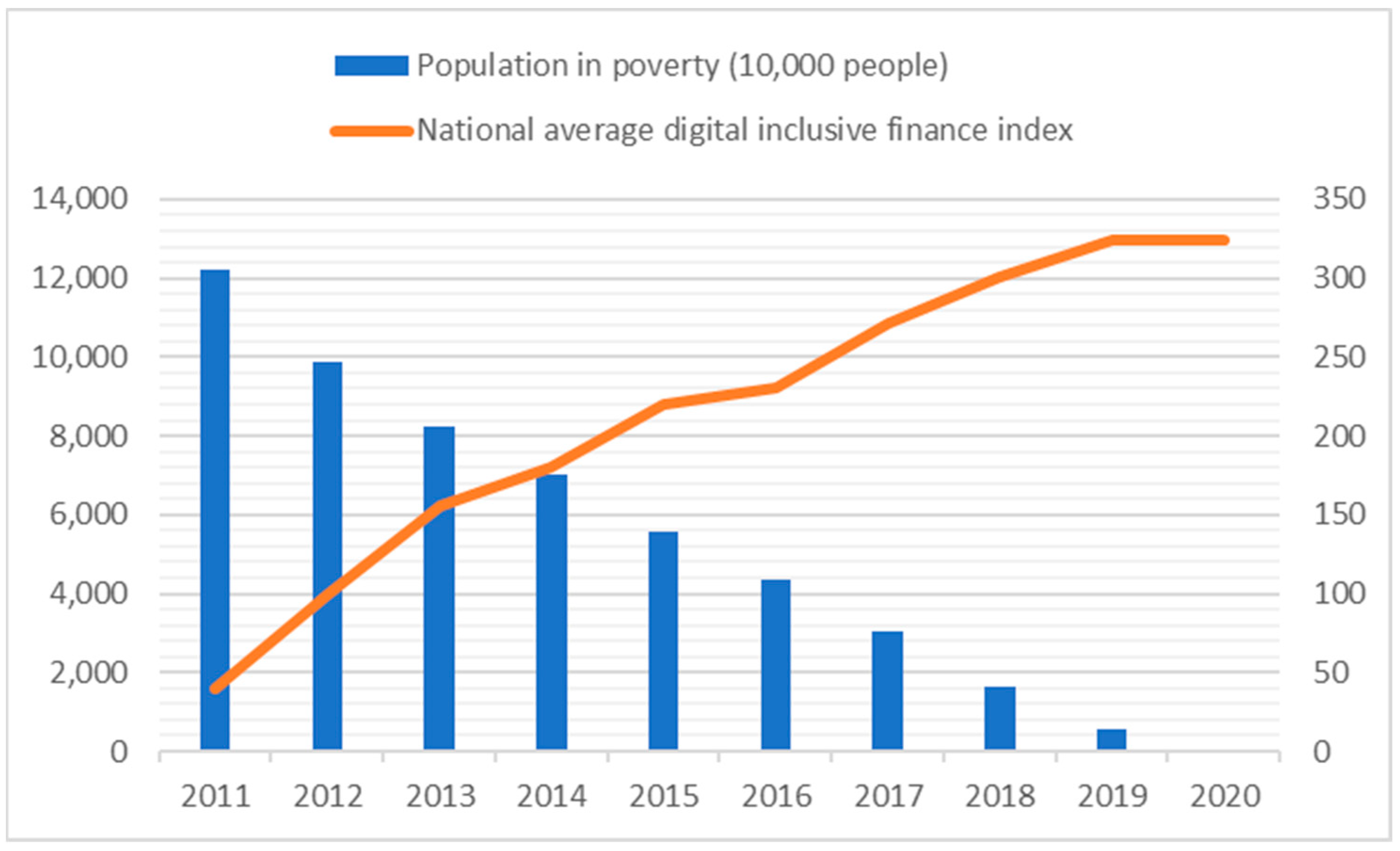

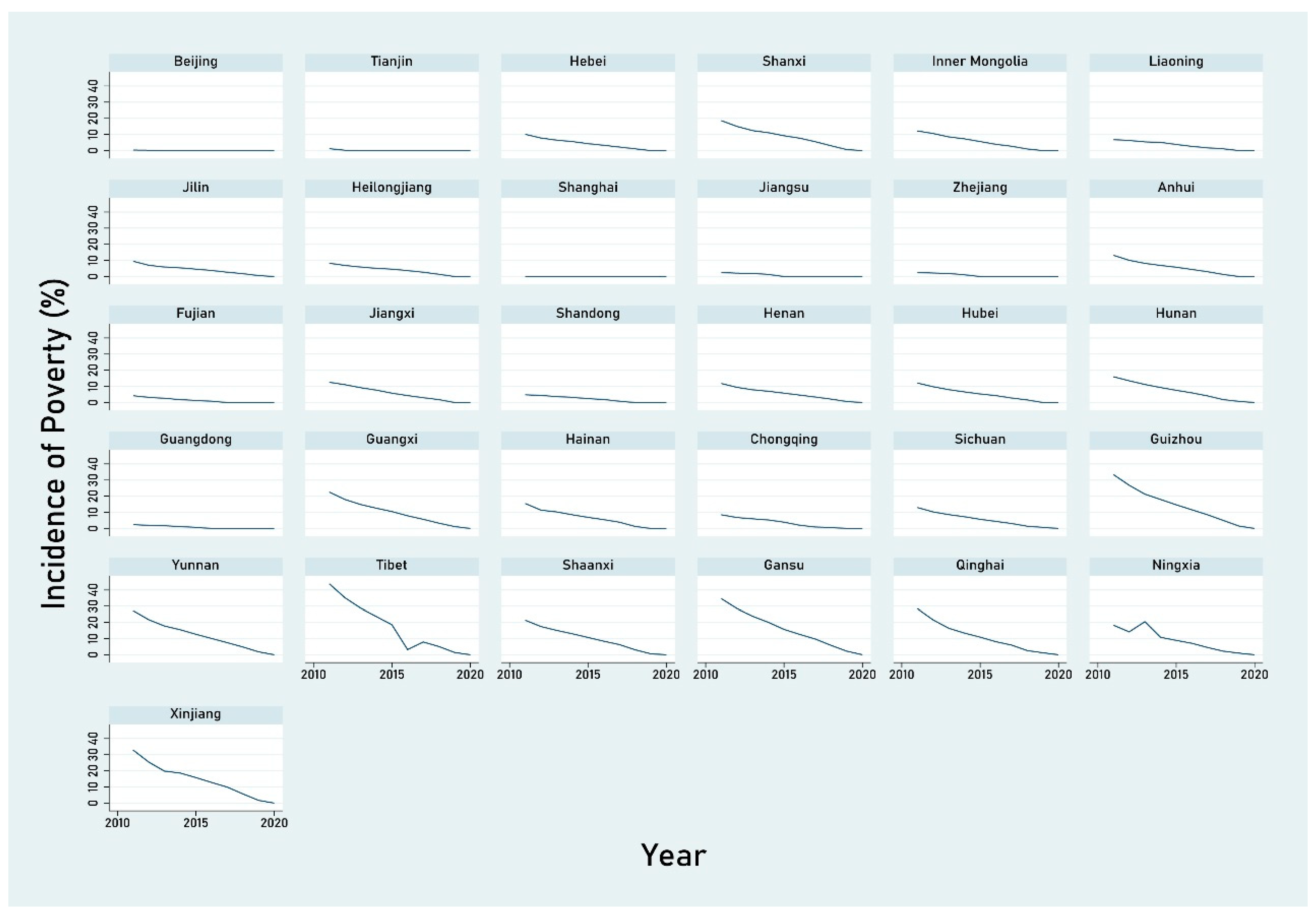

- Incidence of poverty (IP)This paper uses the incidence of poverty to measure the degree of poverty. The data on the incidence of poverty comes from the 2011–2020 China Rural Poverty Monitoring Report.

- Digital inclusive finance index (DIFI)There is a scarcity of scientific and authoritative index assessment systems as a result of the late introduction of DIF. The “Peking University digital inclusive finance index” was created by the Digital Finance Research Center at Peking University, based on massive data on digital inclusive finance provided by the Ant Group (The Ant Group is a leading global digital platform that enables consumers and businesses to connect and transact globally. Its goal is to promote digital upgrading of the service industry and bring about little changes in the world). The index calculates the digital inclusive finance index based on three dimensions: coverage; depth; and digitization of digital financial services and serves as a reference data source for relevant research in digital inclusive finance. When assessing the development level of DIF in China, this article uses province data from 2011 to 2020 to estimate the progress made.

- Regional GDP (RGDP)This paper picks the regional GDP growth rate as the indicator of a region’s economic development level. Regional GDP refers to the ultimate output of all permanent inhabitants of a region’s productive activities over a given time period. Economic growth may lead to the accumulation of wealth, the creation of new job possibilities, and an improvement in the welfare of disadvantaged populations. There is also a “trickle-down effect” in economic expansion, whereby the benefits produced by prosperity continue to permeate from developed regions to neighboring poor ones, so helping the poor. Theoretically, the larger the rate of economic growth, the better the effectiveness of poverty reduction in a region.

- Gini coefficient (GINI)Based on the Lorenz curve, the Gini index is an indication of the equality of income distribution. It is commonly utilized in economics studies. This paper employs the approach of Tian [44] for computing the Gini coefficient for 31 Chinese provinces, cities, and autonomous territories. The data comes from the China Statistics Yearbook and the statistical yearbooks of China’s various provinces.

- Other control variablesOther variables affecting poverty are selected as follows:Industrial structure (Is): The optimization of the industrial structure is conducive to the coordinated development of various industries, promotes high-quality economic growth, and drives more labor employment [45]. Moreover, the continuous optimization of the industrial structure can promote poor areas to achieve industrial poverty alleviation, reduce the vulnerability of single agricultural production, and improve the income security of poor groups [46]. This paper selects the ratio of the total output value of the secondary and tertiary industries to RGDP to measure the industrial structure.Urbanization level (Urban): The urbanization level can help rural communities receive their fair share of financial resources and reduce the rural surplus. However, it can also lead to excessive urbanization, which will affect rural economic development. Although urbanization can help improve the living conditions of rural communities, it can also lead to a rise in poverty. This paper aims to study the effects of urbanization on poverty using the proportion of urban residents in a region.Financial support for agriculture (Fs): Improvement in financial support for farming is beneficial for rural areas as it promotes the construction of rural infrastructure and local industrial development. This paper shows that the proportion of the total financial support for agriculture that is allocated for local finance is relative to the total financial expenditure.Education level (Edu): It is a factor that influences the accumulation of human capital. It can also help poor households improve their competitiveness and earn higher wages. This paper uses the mean years of schooling to measure the average level of education in different provinces.Economic Openness (Open): Economic openness can promote the development of regions with comparative advantage industries so as to reduce poverty in such regions. However, for some regions without comparative advantage industries and lack of relevant resource endowment, economic openness may have a negative impact. This paper uses the proportion of regional net exports of goods and services to RGDP to measure the level of economic openness, in which the regional net exports of goods and services are converted into RMB by the weighted average exchange rate of that year.

3.3. Data

4. Results

5. Discussion

6. Conclusions

- The development of finance must support the growth of actual industry and society. The goal of inclusive finance is to guarantee that every member of society has equal access to the benefits of financial services.

- For low-income and impoverished individuals, it is vital to increase education and training in financial-related information and to ensure that the link between risk and income is appropriately understood. Effectively enhancing the ability of the poor to confront risks through prudent use of financial instruments is possible, but the current level of financial literacy among the poor is insufficient for them to make reasonable decisions in a complicated market environment.

- It is vital to increase the administration and oversight of digital financial goods and services, particularly those that are inclusive and assist the agricultural sector. Owing to a lack of corresponding financial expertise, it is challenging for the poor to appropriately assess the risks associated with complicated financial instruments. Hence, financial items offered to the poor must be supervised and managed by the appropriate departments.

- Exploring Economic Development Growth Rates Across Different Regions:Economic development growth rates across various regions interact intricately with poverty reduction strategies. Understanding this interaction is pivotal as different regions might possess unique economic characteristics, and a uniform poverty reduction strategy might not yield the desired results everywhere;

- The Effect on Poverty Reduction: Understanding how growth rates affect poverty can help in tailoring specific economic policies. A region experiencing rapid growth might require different strategies than a stagnating area;

- The Role of Government and Policy: How local governments respond to different growth rates in terms of policy interventions can be a vital area of study. This can help in understanding whether local conditions are considered in policy formulation;

- Intersection with Digital Inclusion: Future research could also delve into how digital inclusion strategies fit into regions with different economic growth rates. This could lead to insights into what types of digital interventions are most effective in various economic contexts;

- 2.

- Examining Specific Digital Financial Inclusion Products:Digital financial inclusion products play a significant role in addressing regional poverty, and a deeper examination of specific products and their effectiveness is an exciting prospect;

- Effectiveness in Poverty Alleviation: Understanding which products have been most effective, why, and in what contexts could lead to more targeted interventions;

- Barriers and Opportunities: Identifying barriers to accessing these products and ways to overcome them can be vital for making digital financial inclusion a reality for all, especially in underprivileged areas;

- Innovation and Development: Research into developing new or improving existing products that are tailored to the needs of those in poverty could spark innovation in the field;

- 3.

- Comparing Different Digital Financial Inclusion Products:Beyond examining individual products, there is a wealth of knowledge to be gained from comparing different digital financial inclusion products;

- Understanding Diverse Impacts: Different products may have varying impacts on poverty alleviation. Comparative studies could lead to a more nuanced understanding of what works best, where, and why;

- Tailoring Products to Needs: A comparative study could also help in tailoring products to the specific needs of different populations or regions. This could help in creating more effective, targeted poverty reduction strategies;

- 4.

- Poverty as a Multifaceted Problem:This study also opens avenues for recognizing poverty not merely as an economic challenge but as a multifaceted problem that requires a comprehensive approach;

- Sociocultural Aspects: Understanding the cultural and social dynamics that contribute to poverty can lead to more humane and effective interventions;

- Environmental Factors: Researching how environmental factors intersect with poverty could open doors to sustainable development strategies;

- Education and Awareness: Delving into the role of education in both understanding financial products and lifting individuals out of poverty could be a crucial aspect of a more comprehensive approach.

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Singh, P.K.; Chudasama, H. Evaluating poverty alleviation strategies in a developing country. PLoS ONE 2020, 15, e0227176. [Google Scholar] [CrossRef]

- Zhou, L.; Wang, H. An Approach to Study the Poverty Reduction Effect of Digital Inclusive Finance from a Multidimensional Perspective Based on Clustering Algorithms. Sci. Program. 2021, 2021, 4645596. [Google Scholar] [CrossRef]

- Bhatia, S.; Singh, S. Empowering Women Through Financial Inclusion: A Study of Urban Slum. Vikalpa J. Decis. Makers 2019, 44, 182–197. [Google Scholar] [CrossRef]

- Lai, J.T.; Yan, I.K.; Yi, X.; Zhang, H. Digital financial inclusion and consumption smoothing in China. China World Econ. 2020, 28, 64–93. [Google Scholar]

- Sarma, M.; Pais, J. Financial Inclusion and Development. J. Int. Dev. 2011, 23, 613–628. [Google Scholar] [CrossRef]

- Hasan, M.; Yajuan, L.; Khan, S. Promoting China’s Inclusive Finance Through Digital Financial Services. Glob. Bus. Rev. 2022, 23, 984–1006. [Google Scholar] [CrossRef]

- Dai, D.; Fu, M.; Ye, L.; Shao, W. Can Digital Inclusive Finance Help Small- and Medium-Sized Enterprises Deleverage in China? Sustainability 2023, 15, 6625. [Google Scholar] [CrossRef]

- Li, J.; Wu, Y.; Xiao, J.J. The impact of digital finance on household consumption: Evidence from China. Econ. Model. 2020, 86, 317–326. [Google Scholar] [CrossRef]

- Liu, Y.; Luan, L.; Wu, W.; Zhang, Z.; Hsu, Y. Can digital financial inclusion promote China’s economic growth? Int. Rev. Financ. Anal. 2021, 78, 101889. [Google Scholar] [CrossRef]

- Wang, X.; He, G. Digital Financial Inclusion and Farmers’ Vulnerability to Poverty: Evidence from Rural China. Sustainability 2020, 12, 1668. [Google Scholar] [CrossRef]

- Liu, F.; Liu, M.; Guo, F. The Research on Relationship between Financial Development Scale, Efficiency and Counties Anti-poverty: An Analysis Based on SYS-GMM of 50 Poverty Counties in Shaanxi Province. Stat. Inf. Forum 2015, 30, 42–48. [Google Scholar]

- Law, S.H.; Tan, H.B.; Azman-Saini, W.N.W. Financial Development and Income Inequality at Different Levels of Institutional Quality. Emerg. Mark. Finance Trade 2014, 50, 21–33. [Google Scholar] [CrossRef]

- Cui, Y. Financial Development, Urbanization and Poverty Alleviation: Estimation with System GMM. Lanzhou Acad. J. 2014, 35, 152–158. Available online: https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFD2014&filename=LZXK201408025&uniplatform=NZKPT&v=5toiSIaLw_QPzL7ueUME1UrNkDcBSBWS-_1kCq6K8LcEcrFgk5RNUB0zgomi7Afx (accessed on 1 May 2022).

- Cui, Y.; Sun, G. Is Financial Development the Cause of Poverty Reduction?—Evidence from China. J. Financ. Res. 2012, 55, 116–127. Available online: https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFD2012&filename=JRYJ201211011&uniplatform=NZKPT&v=0v72DW%25mmd2BiZqiiyEfqH5wnW6VABAXb08dAbCjQlaHlSq63VUVWX2o%25mmd2FDpsAKuoKZ9Op (accessed on 1 May 2022).

- Ozturk, I.; Ullah, S. Does digital financial inclusion matter for economic growth and environmental sustainability in OBRI economies? An empirical analysis. Resour. Conserv. Recycl. 2022, 185, 106489. [Google Scholar] [CrossRef]

- Gruin, J.; Knaack, P. Not Just Another Shadow Bank: Chinese Authoritarian Capitalism and the ‘Developmental’ Promise of Digital Financial Innovation. New Politcal Econ. 2020, 25, 370–387. [Google Scholar] [CrossRef]

- Chen, S.; Zhang, H. Does digital finance promote manufacturing servitization: Micro evidence from China. Int. Rev. Econ. Finance 2021, 76, 856–869. [Google Scholar] [CrossRef]

- Lyons, A.C.; Kass-Hanna, J. Financial Inclusion, Financial Literacy and Economically Vulnerable Populations in the Middle East and North Africa. Emerg. Mark. Finance Trade 2021, 57, 2699–2738. [Google Scholar] [CrossRef]

- Bond, S.R.; Hoeffler, A.; Temple, J.R. GMM Estimation of Empirical Growth Models. 2001. Available online: https://ssrn.com/abstract=290522 (accessed on 1 May 2022).

- Dollar, D.; Kraay, A. Growth is Good for the Poor. J. Econ. Growth 2002, 7, 195–225. Available online: https://link.springer.com/content/pdf/10.1023/A:1020139631000.pdf (accessed on 1 May 2022). [CrossRef]

- Zhang, L.; Zhan, Y. The Analysis of Three Major Effects of Financial Development on the Urban-rural Income Gap. J. Quant. Tech. Econ. 2006, 23, 73–81. Available online: https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFD2006&filename=SLJY200612008&uniplatform=NZKPT&v=1g7mhVMAu%25mmd2FQ2XuLrJmbkTlP07Mhsvt6Zxi38GbaV7ZsUzBSrSNGaf1Vat6rlxPK4 (accessed on 1 May 2022).

- Beck, T.; Demirgüç-Kunt, A.; Levine, R. Finance, Inequality and the Poor. J. Econ. Growth 2007, 12, 27–49. Available online: https://link.springer.com/content/pdf/10.1007/s10887-007-9010-6.pdf (accessed on 1 May 2022). [CrossRef]

- Jeanneney, S.G.; Kpodar, K. Financial Development and Poverty Reduction: Can There be a Benefit Without a cost? J. Dev. Stud. 2011, 47, 143–163. Available online: https://www.tandfonline.com/doi/pdf/10.1080/00220388.2010.506918 (accessed on 1 May 2022). [CrossRef]

- Arestis, P.; Caner, A. Financial Liberalization and Poverty: Channels of Influence. Working Paper 2004. Available online: https://www.econstor.eu/bitstream/10419/31636/1/504003046.pdf (accessed on 1 May 2022).

- Wen, T.; Ran, G.; Xiong, D. China’s Financial Development and Rural Income Growth. Econ. Res. J. 2005, 9, 143. Available online: http://www.erj.cn/UploadFiles/%E4%B8%AD%E5%9B%BD%E9%87%91%E8%9E%8D%E5%8F%91%E5%B1%95%E4%B8%8E%E5%86%9C%E6%B0%91%E6%94%B6%E5%85%A5%E5%A2%9E%E9%95%BF.pdf (accessed on 1 May 2022).

- Kai, H.; Hamori, S. Globalization, financial depth and inequality in Sub-Saharan Africa. Econ. Bull. 2009, 29, 2025–2037. Available online: http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.568.1086&rep=rep1&type=pdf (accessed on 1 May 2022).

- Ang, J.B. Finance and Inequality: The Case of INDIA. South. Econ. J. 2010, 76, 738–761. Available online: https://www.jstor.org/stable/pdf/27751495.pdf (accessed on 1 May 2022). [CrossRef]

- Wang, L.; Zhu, X.; Wu, Q. The Predicament and Countermeasures of Rural Financial Poverty Alleviation—Taking Hubei Province as An Example. J. Chin. Acad. Gov. 2012, 14, 99–103. Available online: https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFD2012&filename=LJXZ201206017&uniplatform=NZKPT&v=mrwIoPfkcsZZrZFhhUdEVhdAvzgIN7TC41q3mZpZeyNO6%25mmd2BRQGuTmq%25mmd2FYoeQO5a8H0 (accessed on 1 May 2022).

- Deng, K. Evaluation of Financial Efficiency of Poverty Alleviation and Agricultural Benefit—A Case Study of Bazhong City in Qinba Mountain Area. Rural. Econ. 2015, 33, 86–91. Available online: https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFDLAST2015&filename=NCJJ201505017&uniplatform=NZKPT&v=38fn6VRuduFGPYe5LZQGGrwoaztzuanPeUBtiK5j3bX6k6TLNJQSUvojEzujx3Mj (accessed on 1 May 2022).

- Greenwood, J.; Jovanovic, B. Financial development, growth, and the distribution of income. J. Political Econ. 1990, 98, 1076–1107. Available online: https://www.nber.org/system/files/working_papers/w3189/w3189.pdf (accessed on 1 May 2022). [CrossRef]

- Barro, R.J. Inequality and Growth in a Panel of Countries. J. Econ. Growth 2000, 5, 5–32. Available online: https://link.springer.com/content/pdf/10.1023/A:1009850119329.pdf (accessed on 1 May 2022). [CrossRef]

- Chibba, M. Financial Inclusion, Poverty Reduction and the Millennium Development Goals. Eur. J. Dev. Res. 2009, 21, 213–230. Available online: https://link.springer.com/article/10.1057/ejdr.2008.17 (accessed on 1 May 2022). [CrossRef]

- Hannig, A.; Jansen, S. Financial Inclusion and Financial Stability: Current Policy Issues. 2010. Available online: https://www.econstor.eu/bitstream/10419/53699/1/654899762.pdf (accessed on 1 May 2022).

- Park, C.-Y.; Mercado, R. Financial Inclusion, Poverty, and Income Inequality in Developing Asia. Asian Development Bank Economics Working Paper Series. 2015. Available online: https://www.adb.org/sites/default/files/publication/153143/ewp-426.pdf (accessed on 1 May 2022).

- Jia, J.; Xiao, J. The Innovative Development of Rural Inclusive Financial System in the Context of Taking Targeted Measures for Poverty Alleviation. Theor. Investig. 2017, 34, 70–75. Available online: https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFDLAST2017&filename=LLTT201701012&uniplatform=NZKPT&v=Xb9Cy6XLwjvNr6S1Ba1gVzgvF4f2MrfsRCP0ts2pFK8IvrG73tq%25mmd2BRkbAyn8enoXU (accessed on 1 May 2022).

- Ten Departments Including the People’s Bank of China Issued The Guiding Opinions on Promoting The Healthy Development of Internet Finance. Available online: http://www.gov.cn/xinwen/2015-07/18/content_2899360.htm (accessed on 18 July 2015).

- Dong, Y.; Liu, T.; Lu, Z. The Realistic Demand, Dilemma and Suggestion of Rural Internet Finance. New Financ. 2016, 29, 32–36. Available online: https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFDLAST2016&filename=XJRO201611007&uniplatform=NZKPT&v=84a91jtWYGp%25mmd2Fplii7YQ%25mmd2BNS4RZ5Z8MGf6n8emc6PDTLYgXz5rhs8jSAUm4GNuvvhl (accessed on 1 May 2022).

- Yan, S.; Zhong, C. Feasibility Analysis and Path Discussion of Internet Finance Supporting Targeted Poverty Alleviation. Heilongjiang Financ. 2016, 37, 27–29. Available online: https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFDLAST2016&filename=HLJR201607017&uniplatform=NZKPT&v=IqzKi3zUj%25mmd2Faty%25mmd2BenwAY3andfI3fgxReqDxapkb%25mmd2FTPoTst%25mmd2B1cBBmjQ4VfwSGlWv9%25mmd2B (accessed on 1 May 2022).

- Li, Y.; Wang, C. Risk Identification, Future Value and Credit Capitalization: Research on the Theory and Policy of Poverty Alleviation by Internet Finance. China Financ. Econ. Rev. 2017, 5, 1. Available online: https://chinafinanceandeconomicreview.springeropen.com/articles/10.1186/s40589-017-0045-3 (accessed on 1 May 2022). [CrossRef]

- Arellano, M.; Bond, S. Some Tests of Specification for Panel Data: Monte Carlo Evidence and an Application to Employment Equations. Rev. Econ. Stud. 1991, 58, 277–297. [Google Scholar] [CrossRef]

- Blundell, R.; Bond, S. Initial Conditions and Moment Restrictions in Dynamic Panel Data Models. J. Econom. 1998, 87, 115–143. [Google Scholar] [CrossRef]

- Su, J.; Liao, J. Empirical Analysis of Financial Development, Income Distribution and Poverty: Based on Dynamic Panel Data. Financ. Econ. 2009, 36, 10–16. [Google Scholar]

- Liu, J.; Bi, Z. Inclusive Finance and Its Income Distribution Effect—Based on the Dual Perspective of Economic Growth and Poverty Alleviation. Res. Econ. Manag. 2019, 40, 37–46. [Google Scholar] [CrossRef]

- Tian, W. Calculation of Gini Coefficient in China and Analysis of Its Changing Trend. J. Humanit. 2012, 2, 56–61. [Google Scholar] [CrossRef]

- Alfani, G. Epidemics, inequality, and poverty in preindustrial and early industrial times. J. Econ. Lit. 2022, 60, 3–40. [Google Scholar] [CrossRef]

- Amar, S.; Pratama, I. Exploring the Link Between Income Inequality, Poverty Reduction and Economic Growth: An ASEAN Perspective. Int. J. Innov. Creat. Change 2020, 11, 24–41. [Google Scholar]

- Pesaran, M.H. Testing Weak Cross-Sectional Dependence in Large Panels. Econom. Rev. 2015, 34, 1089–1117. [Google Scholar] [CrossRef]

- Pesaran, M.H. A simple panel unit root test in the presence of cross—Section dependence. J. Appl. Econom. 2007, 22, 265–312. [Google Scholar] [CrossRef]

- Im, K.S.; Pesaran, M.H.; Shin, Y. Testing for unit roots in heterogeneous panels. J. Econom. 2003, 115, 53–74. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Reference | Research Method | Main Findings | Unique Aspects |

|---|---|---|---|

| [20] Dollar and Kraay (2002) | Theoretical Analysis | Financial development promotes poverty alleviation through economic growth (“trickle-down effect”) | Focus on indirect effect through economic growth |

| [21] Zhang and Zhan (2006) | Theoretical Analysis | Financial development alleviates urban–rural income disparity and poverty | Urban–rural disparity focus |

| [22] Beck et al. (2007) | Empirical Analysis | Financial development reduces the proportion of the population living on less than $1 per day. | Global perspective |

| [23] Jeanneney and Kpodar (2011) | Empirical Analysis (1966–2000) | Banking system’s role in poverty reduction through distributive effects | Focus on developing nations |

| [24] Arestis and Caner (2004) | Theoretical Analysis | Financial liberalization impedes poverty reduction, lowers income | Focus on unproductive sectors |

| [25] Wen et al. (2005) | Empirical Analysis (1952–2003), China | Financial development stifles farmer income growth, widens urban–rural income divide | Focus on China’s rural economics |

| [26] Kai and Hamori (2009) | Empirical Analysis (1980–2002), Sub-Saharan Africa | Globalization and financial deepening increase inequality | Focus on Sub-Saharan Africa |

| [27] Ang (2010) | Empirical Analysis, India | Financial progress reduces inequality, while liberalization increases it | Focus on India |

| [28] Wang et al. (2012) | Empirical Analysis, Hubei Province | Unclear effect on poverty alleviation by rural finance in Hubei Province | Focus on rural financial exclusion |

| [29] Deng (2015) | Panel Data Analysis (2011–2014), Sichuan Province | Agriculture-related loans do not improve farmers’ income | Focus on specific financial tool |

| [31] Barro (2000) | Theoretical Analysis | “U” shaped relationship between financial development and poverty alleviation in the USA | Introduces “U” shaped relationship |

| [14] Cui and Sun (2012) | Empirical Analysis | Financial development can reduce poverty after financial regulations | Focus on financial regulations |

| [12] Law et al. (2014) | Threshold Regression Approach | Threshold effect of institutional quality between financial development and income inequality | Introduces threshold effect |

| [32] Chibba (2009); [34] Park and Mercado (2015); [35] Jia and Xiao (2017) | Theoretical and Empirical Analysis | Financial inclusion and digital finance promote poverty alleviation and improve living conditions for the poor | Focus on digital finance and financial inclusion |

| [37] Dong et al. (2016); [38] Yan and Zhong (2016); [39] Li and Wang (2017); [10] Wang and He (2020) | Theoretical and Empirical Analysis | Internet finance and digital finance offer solutions for poverty alleviation and cater to middle and lower-income groups | Focus on Internet finance, digital technology |

| Variables | Symbols | Index Calculation |

|---|---|---|

| Incidence of poverty | IP | Number of poor people in the region/total population in the region |

| Digital Inclusive Finance | DIFI | Peking University Digital Inclusive Financial Index |

| Regional GDP | RGDP | Regional GDP |

| Gini coefficient | GINI | Gini coefficient |

| Industrial structure | IS | Total output value of secondary and tertiary industries/GDP |

| Urbanization level | URBAN | Regional urban population/total regional population |

| Financial support for agriculture | FS | Financial expenditure for agriculture/total financial expenditure |

| Education level | EDU | Mean years of schooling |

| Economic Openness | OPEN | Regional Net Exports of Goods and Services/RGDP |

| Year | IP | DIFI | RGDP | GINI | IS | URBAN | FS | EDU | OPEN |

|---|---|---|---|---|---|---|---|---|---|

| 2011 | 14.48 (11.40) | 40.00 (18.61) | 12.53 (1.99) | 43.58 (4.99) | 89.39 (5.29) | 52.20 (14.46) | 10.88 (2.88) | 8.85 (3.35) | −9.58 (15.24) |

| 2012 | 11.58 (9.08) | 99.68 (22.34) | 12.05 (3.11) | 43.79 (4.61) | 89.49 (5.20) | 53.35 (14.25) | 11.22 (2.81) | 8.94 (2.98) | −12.85 (18.30) |

| 2013 | 9.82 (7.59) | 155.35 (26.18) | 10.44 (3.44) | 43.26 (4.92) | 89.54 (5.14) | 54.65 (13.96) | 11.24 (2.69) | 9.05 (3.24) | −15.75 (21.66) |

| 2014 | 8.15 (6.29) | 179.75 (23.46) | 8.16 (2.71) | 42.63 (4.94) | 90.07 (4.98) | 55.91 (13.45) | 11.13 (2.82) | 9.04 (3.22) | −16.69 (24.42) |

| 2015 | 6.51 (5.20) | 220.01 (22.94) | 5.30 (3.53) | 42.20 (4.58) | 90.09 (5.06) | 57.40 (12.85) | 11.77 (3.10) | 9.08 (2.81) | −18.63 (28.75) |

| 2016 | 4.68 (3.79) | 230.41 (21.19) | 7.59 (6.36) | 43.21 (4.48) | 90.23 (5.09) | 58.89 (12.34) | 12.05 (3.58) | 9.09 (2.55) | −18.99 (28.41) |

| 2017 | 3.50 (3.01) | 271.98 (24.06) | 8.15 (5.48) | 41.97 (4.31) | 91.07 (4.93) | 60.27 (11.87) | 11.58 (3.33) | 9.21 (2.54) | −17.94 (30.28) |

| 2018 | 1.90 (1.80) | 300.21 (29.77) | 8.18 (2.87) | 42.43 (3.99) | 91.34 (4.76) | 61.48 (11.58) | 11.93 (3.77) | 10.06 (2.43) | −0.42 (9.22) |

| 2019 | 0.51 (0.67) | 323.73 (33.29) | 6.83 (12.29) | 42.45 (4.53) | 91.08 (5.13) | 62.62 (11.34) | 12.12 (4.22) | 10.05 (2.41) | −0.55 (9.71) |

| 2020 | 0 (0) | 341.22 (34.72) | 3.15 (2.79) | 43.32 (5.18) | 90.44 (5.43) | 63.73 (11.06) | 12.20 (4.19) | 10.70 (2.38) | −0.17 (9.71) |

| Variables | CD-Test | CADF | CIPS |

|---|---|---|---|

| DIFI | 68.05 *** | −2.585 *** | −1.334 |

| RGDP | 26.79 *** | −2.193 ** | −2.899 *** |

| GINI | −0.86 | −1.745 | −2.509 *** |

| IS | 31.91 *** | −1.699 | −1.748 |

| URBAN | 62.35 *** | −2.956 *** | −2.598 *** |

| FS | 3.37 *** | −1.464 | −1.722 |

| EDU | 27.76 *** | −1.877 | −2.071 * |

| OPEN | 23.36 *** | −2.024 * | −2.424 *** |

| Variables | (1) GMM | (2) GMM | (3) OLS |

|---|---|---|---|

| L. IP | 0.7774 *** (0.0041) | 0.8019 *** (0.0096) | 0.7961 *** (0.0185) |

| DIFI | −0.0056 *** (0.0004) | −0.0036 *** (0.0007) | −0.0043 *** (0.0013) |

| RGDP | −0.0161 *** (0.0029) | −0.0210 *** (0.0042) | −0.0208 (0.0131) |

| GINI | 0.0109 *** (0.0039) | 0.0125 (0.0157) | |

| IS | −0.0546 *** (0.0202) | −0.0249 (0.0208) | |

| URBAN | 0.0038 (0.0046) | 0.0077 (0.0118) | |

| FS | −0.1477 *** (0.0319) | −0.0938 *** (0.0358) | |

| EDU | −0.0245 ** (0.0022) | −0.0167 (0.0335) | |

| OPEN | −0.0050 *** (0.0011) | −0.0056 (0.0043) | |

| Constant | 1.3539 *** (0.1317) | 6.7396 ** (2.9067) | 2.7134 (2.4084) |

| AR(1) | 0.152 | 0.145 | |

| AR(2) | 0.284 | 0.299 | |

| Sargan P | 0.000 | 0.000 | |

| Hansen P | 1.000 | 1.000 | |

| R-squared | 0.9734 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Xie, X. Analyzing the Impact of Digital Inclusive Finance on Poverty Reduction: A Study Based on System GMM in China. Sustainability 2023, 15, 13331. https://doi.org/10.3390/su151813331

Xie X. Analyzing the Impact of Digital Inclusive Finance on Poverty Reduction: A Study Based on System GMM in China. Sustainability. 2023; 15(18):13331. https://doi.org/10.3390/su151813331

Chicago/Turabian StyleXie, Xiaowen. 2023. "Analyzing the Impact of Digital Inclusive Finance on Poverty Reduction: A Study Based on System GMM in China" Sustainability 15, no. 18: 13331. https://doi.org/10.3390/su151813331