More Green, Better Funding? Exploring the Dynamics between Corporate Bank Loans and Trade Credit

Abstract

:1. Introduction

2. Literature Review and Hypothesis Development

3. Data and Methodology

3.1. Sample and Data

3.2. Measures

3.2.1. Dependent Variable: Corporate Bank Loans

3.2.2. Independent Variable: Trade Credit

3.2.3. Control Variables

3.3. Model Specification

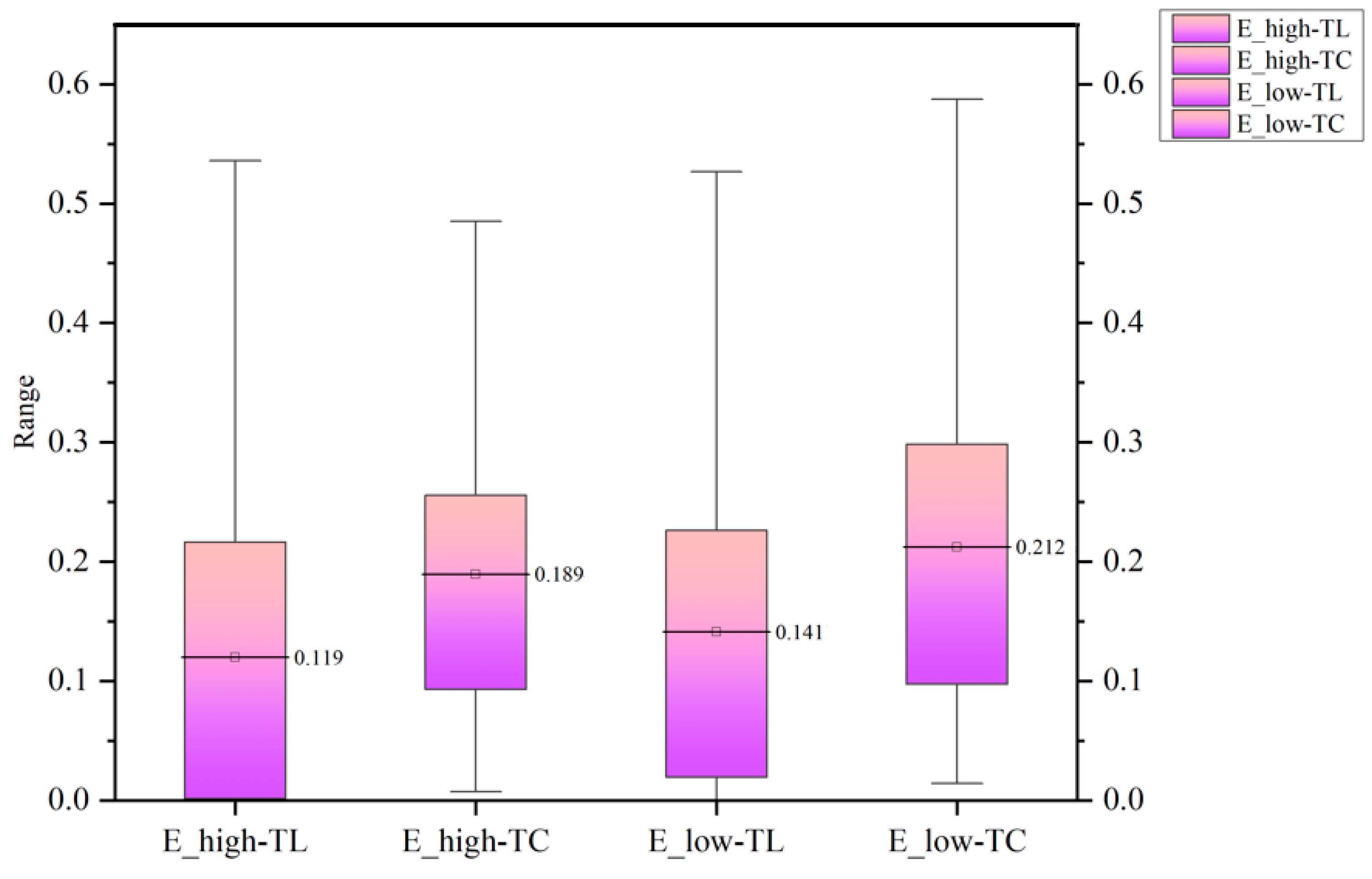

3.4. Descriptive Statistics

4. Empirical Results and Analysis

4.1. Baseline Regression Results

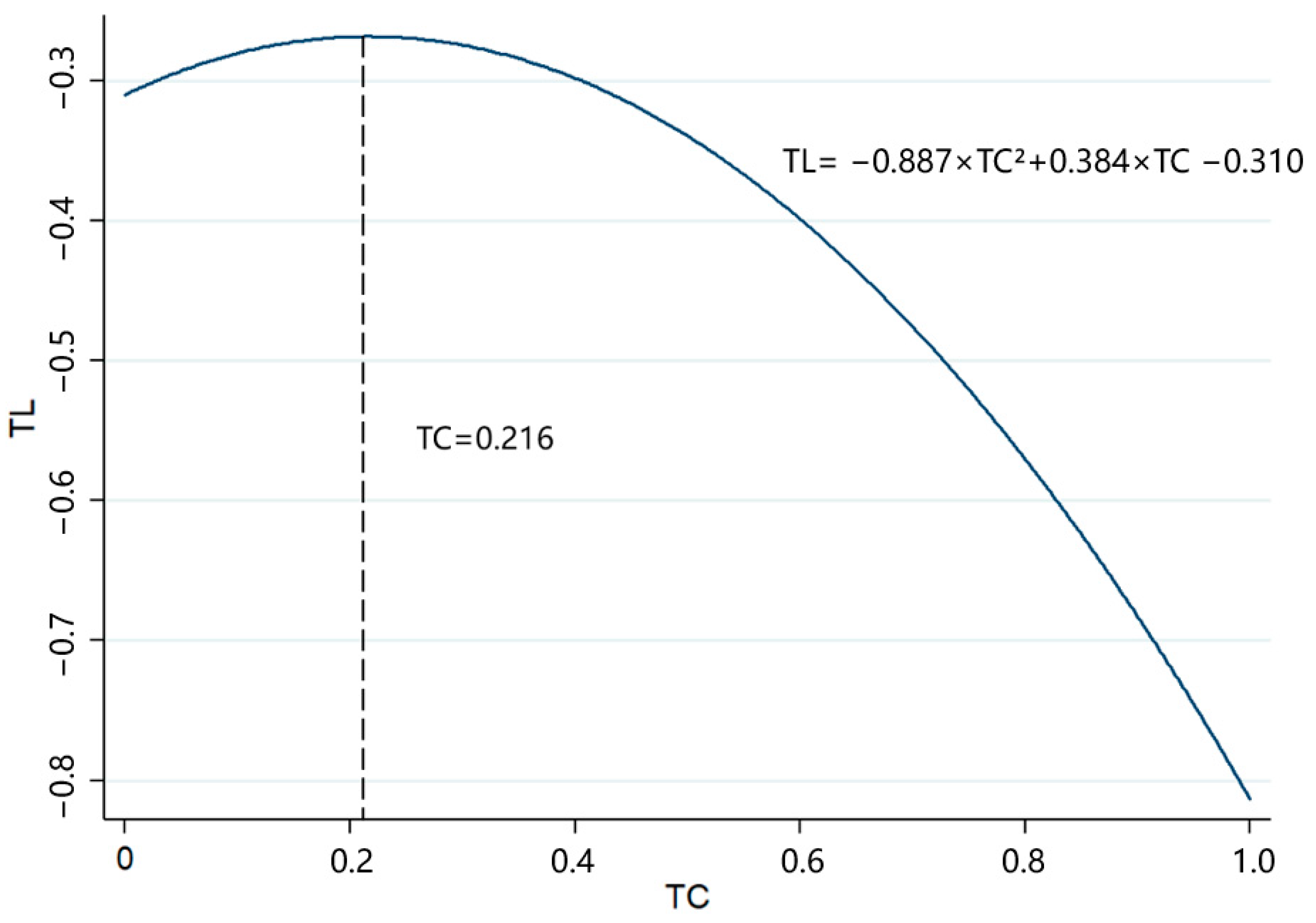

4.2. Extended Analysis—Nonlinear Effects of TC

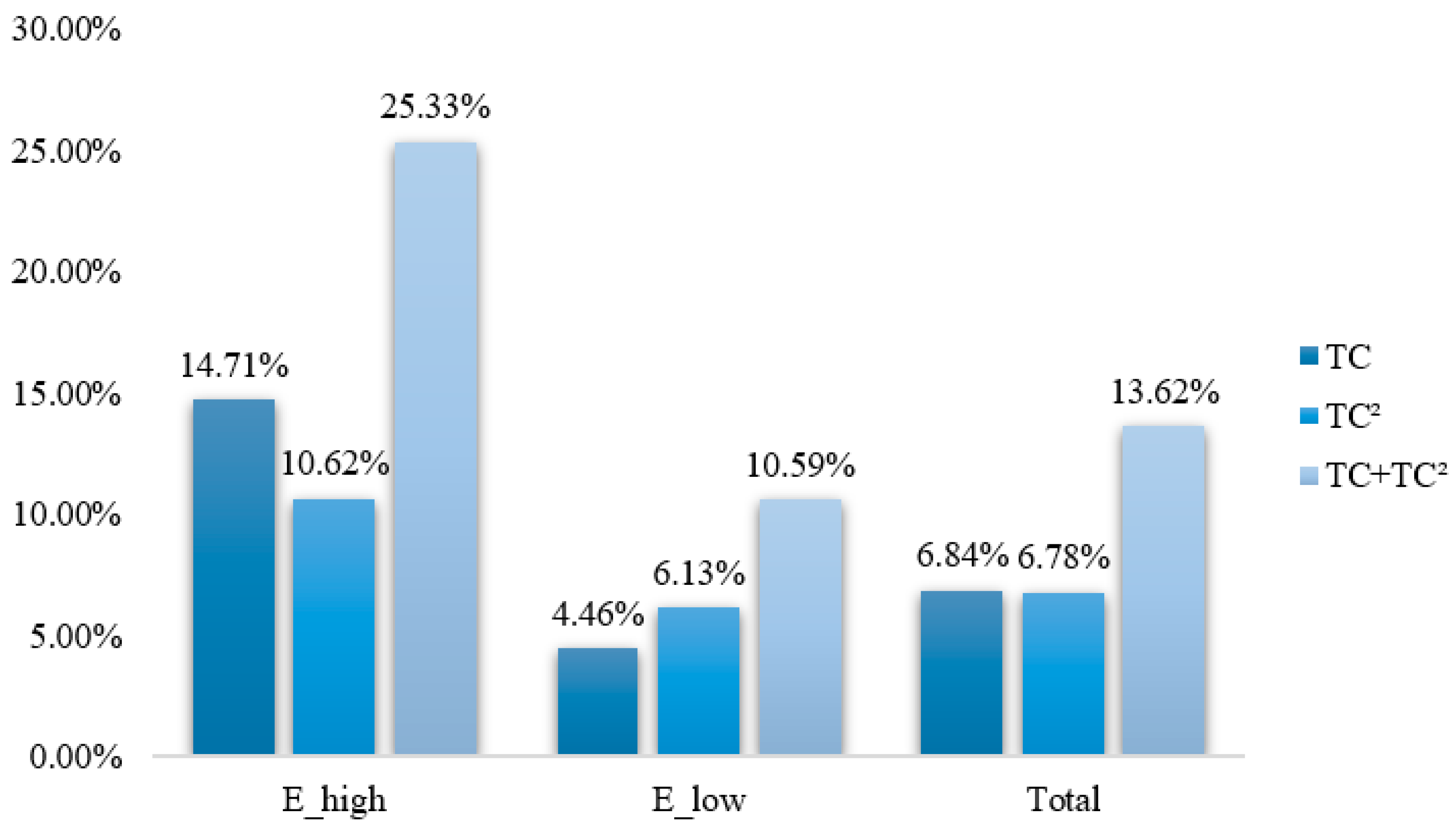

4.3. Decomposing the Explained Variation in TL

4.4. Endogeneity Test

4.5. Robustness Tests

4.5.1. Replacement of Dependent Variable

4.5.2. Replacement of Independent Variable

4.5.3. Increasing Control Variable

4.5.4. Grouped Regression

5. Discussions and Implications

6. Conclusions and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Schwerdtle, P.N.; Cavan, E.; Pilz, L.; Oggioni, S.D.; Crosta, A.; Kaleyeva, V.; Karim, P.H.; Szarvas, F.; Naryniecki, T. Interlinkages between Climate Change Impacts, Public Attitudes, and Climate Action—Exploring Trends before and after the Paris Agreement in the EU. Sustainability 2023, 15, 7542. [Google Scholar] [CrossRef]

- Bovera, F.; Lo Schiavo, L. From Energy Communities to Sector Coupling:A Taxonomy for Regulatory Experimentation in the Age of the European Green Deal. Energy Policy 2022, 171, 113299. [Google Scholar] [CrossRef]

- Perrin, J.A.; Bouisset, C. Emerging Local Public Action in Renewable Energy Production. Discussion of the Territorial Dimension of the Energy Transition Based on the Cases of Four Intermunicipal Cooperation Entities in France. Energy Policy 2022, 168, 113143. [Google Scholar] [CrossRef]

- Chi, Y.; Xu, S.; Yang, X.; Li, J.; Zhang, X.; Chen, Y. Research on Beijing Manufacturing Green-Oriented Transition Path under “Double Carbon” Goal-Based on the GML-SD Model. Sustainability 2023, 15, 7716. [Google Scholar] [CrossRef]

- Herrador, M.; de Jong, W.; Nasu, K.; Granrath, L. Circular Economy and Zero-Carbon Strategies between Japan and South Korea: A Comparative Study. Sci. Total Environ. 2022, 820, 153274. [Google Scholar] [CrossRef] [PubMed]

- Meng, L.; Yang, R.; Sun, M.; Zhang, L.; Li, X. Regional Sustainable Strategy Based on the Coordination of Ecological Security and Economic Development in Yunnan Province, China. Sustainability 2023, 15, 7540. [Google Scholar] [CrossRef]

- Liu, X.; Liu, Y.; Wang, B. Evaluating the Sustainability of Chinese Cities: Indicators Based on a New Data Envelopment Analysis Model. Ecol. Indic. 2022, 137, 108779. [Google Scholar] [CrossRef]

- Wang, C.; Wang, L. Green Credit and Industrial Green Total Factor Productivity: The Impact Mechanism and Threshold Effect Tests. J. Environ. Manag. 2023, 331, 117266. [Google Scholar] [CrossRef]

- Huang, S.; Huang, X. How Green Bankers Promote Behavioral Integration of Green Investment and Financing Teams—Evidence from Chinese Commercial Banks. Sustainability 2023, 15, 7350. [Google Scholar] [CrossRef]

- Lin, T.; Chou, J. Trade Credit and Bank Loan: Evidence from Chinese Firms. Int. Rev. Econ. Financ. 2015, 36, 17–29. [Google Scholar] [CrossRef]

- Zhou, Z.; Li, Z. Corporate Digital Transformation and Trade Credit Financing. J. Bus. Res. 2023, 160, 113793. [Google Scholar] [CrossRef]

- Yang, X. Trade Credit versus Bank Credit: Evidence from Corporate Inventory Financing. Q. Rev. Econ. Financ. 2011, 51, 419–434. [Google Scholar] [CrossRef]

- Lin, B.; Pan, T. Financing Decision of Heavy Pollution Enterprises under Green Credit Policy: Based on the Perspective of Signal Transmission and Supply Chain Transmission. J. Clean. Prod. 2023, 412, 147454. [Google Scholar] [CrossRef]

- Tsuruta, D. Bank Loan Availability and Trade Credit for Small Businesses during the Financial Crisis. Q. Rev. Econ. Financ. 2015, 55, 40–52. [Google Scholar] [CrossRef]

- Yu, B. Trade Credit Extension, Signaling Effect and Bank Loan An Empirical Analysis Based on Chinese Manufacturing Listed Companies. Secur. Mark. Her. 2017, 294, 34–42. [Google Scholar]

- Casey, E.; O’Toole, C.M. Bank Lending Constraints, Trade Credit and Alternative Financing during the Financial Crisis: Evidence from European SMEs. J. Corp. Financ. 2014, 27, 173–193. [Google Scholar] [CrossRef]

- Yang, X.; Wang, Y.; Hu, D.; Gao, Y. How Industry Peers Improve Your Sustainable Development? The Role of Listed Firms in Environmental Strategies. Bus. Strategy Environ. 2018, 27, 1313–1333. [Google Scholar] [CrossRef]

- Connelly, B.L.; Certo, S.T.; Ireland, R.D.; Reutzel, C.R. Signaling Theory: A Review and Assessment. J. Manag. 2011, 37, 39–67. [Google Scholar] [CrossRef]

- Winit, W.; Ekasingh, E.; Sampet, J. How Disclosure Types of Sustainability Performance Impact Consumers’ Relationship Quality and Firm Reputation. Sustainability 2023, 15, 803. [Google Scholar] [CrossRef]

- Carson, J.E.; Westerman, J.W. The Effectiveness of Organizational Sustainability Messaging to New Hires: An Exploratory Analysis of Signal Cost, Perceived Credibility, and Involvement Intention. Sustainability 2023, 15, 1167. [Google Scholar] [CrossRef]

- López-Concepción, A.; Gil-Lacruz, A.; Saz-Gil, I.; Bazán-Monasterio, V. Social Well-Being for a Sustainable Future: The Influence of Trust in Big Business and Banks on Perceptions of Technological Development from a Life Satisfaction Perspective in Latin America. Sustainability 2023, 15, 628. [Google Scholar] [CrossRef]

- Ren, M.; Ke, K.; Yu, X.; Zhao, J. Local Governments’ Economic Growth Target Pressure and Bank Loan Loss Provision: Evidence from China. Int. Rev. Econ. Financ. 2023, 87, 1–14. [Google Scholar] [CrossRef]

- Ho, K.; Wong, A. Effect of Climate-Related Risk on the Costs of Bank Loans: Evidence from Syndicated Loan Markets in Emerging Economies. Emerg. Mark. Rev. 2022, 55, 100977. [Google Scholar] [CrossRef]

- Vithessonthi, C. The Consequences of Bank Loan Growth: Evidence from Asia. Int. Rev. Econ. Financ. 2023, 83, 252–270. [Google Scholar] [CrossRef]

- Moraux, F.; Phan, D.A.; Vo, T.L.H. Collaborative Financing and Supply Chain Coordination for Corporate Social Responsibility. Econ. Model. 2023, 121, 106198. [Google Scholar] [CrossRef]

- Xing, C.; Zhang, Y.; Tripe, D. Green Credit Policy and Corporate Access to Bank Loans in China: The Role of Environmental Disclosure and Green Innovation. Int. Rev. Financ. Anal. 2021, 77, 101838. [Google Scholar] [CrossRef]

- Ding, X.; Ren, Y.; Tan, W.; Wu, H. Does Carbon Emission of Firms Matter for Bank Loans Decision? Evidence from China. Int. Rev. Financ. Anal. 2023, 86, 102556. [Google Scholar] [CrossRef]

- Love, I.; Zaidi, R. Trade Credit, Bank Credit and Financial Crisis. Int. Rev. Financ. 2010, 10, 125–147. [Google Scholar] [CrossRef]

- Du, J.; Lu, Y.; Tao, Z. Bank Loans vs. Trade Credit;Evidence from China. Econ. Transit. 2012, 20, 457–480. [Google Scholar] [CrossRef] [Green Version]

- Wang, G.; Du, Q.; Li, X.; Deng, X.; Niu, Y. From Ambiguity to Transparency: Influence of Environmental Information Disclosure on Financial Performance in the Context of Internationalization. Environ. Sci. Pollut. Res. 2023, 30, 10226–10244. [Google Scholar] [CrossRef]

- Wu, Z.; Ma, G. Incremental cost-benefit quantitative assessment of green building: A case study in China. Energy Build. 2022, 269, 112251. [Google Scholar] [CrossRef]

- Zhou, Y.; Evans, M.; Yu, S.; Sun, X.; Wang, J. Linkages between policy and business innovation in the development of China’s energy performance contracting market. Energy Policy 2020, 140, 111208. [Google Scholar] [CrossRef]

- Bai, K.; Ullah, F.; Arif, M.; Erfanian, S.; Urooge, S. Stakeholder-Centered Corporate Governance and Corporate Sustainable Development: Evidence from CSR Practices in the Top Companies by Market Capitalization at Shanghai Stock Exchange of China. Sustainability 2023, 15, 2990. [Google Scholar] [CrossRef]

- Wan, G.; Dawod, A.Y. ESG Rating and Northbound Capital Shareholding Preferences: Evidence from China. Sustainability 2022, 14, 9152. [Google Scholar] [CrossRef]

- Siegel, A.F.; Wagner, M.R. Chapter 12—Multiple Regression: Predicting One Variable From Several Others. In Practical Business Statistics, 8th ed.; Siegel, A.F., Wagner, M.R., Eds.; Academic Press: Cambridge, MA, USA, 2022; pp. 371–431. ISBN 978-0-12-820025-4. [Google Scholar]

- Tian, J.; Li, H.; You, P. Economic Policy Uncertainty, Bank Loan, and Corporate Innovation. Pac. Basin Financ. J. 2022, 76, 101873. [Google Scholar] [CrossRef]

- Atanassov, J. Arm’s Length Financing and Innovation: Evidence from Publicly Traded Firms. Manag. Sci. 2016, 62, 128–155. [Google Scholar] [CrossRef]

- Luo, C.; Wei, D.; He, F. Corporate ESG Performance and Trade Credit Financing—Evidence from China. Int. Rev. Econ. Financ. 2023, 85, 337–351. [Google Scholar] [CrossRef]

- Kong, D.; Pan, Y.; Tian, G.G.; Zhang, P. CEOs’ Hometown Connections and Access to Trade Credit: Evidence from China. J. Corp. Financ. 2020, 62, 101574. [Google Scholar] [CrossRef]

- Luthfiyanti, N.K.; Dahlia, L. The Effect of Enterprise Risk Management on Financial Distress. J. Account. Audit. Bus. 2020, 3, 30. [Google Scholar] [CrossRef]

- Callaway, B.; Karami, S. Treatment Effects in Interactive Fixed Effects Models with a Small Number of Time Periods. J. Econom. 2023, 233, 184–208. [Google Scholar] [CrossRef]

- Akinwande, M.O.; Dikko, H.G.; Samson, A. Variance Inflation Factor: As a Condition for the Inclusion of Suppressor Variable(s) in Regression Analysis. Open J. Stat. 2015, 05, 754–767. [Google Scholar] [CrossRef] [Green Version]

- Liu, X.; Anbumozhi, V. Determinant Factors of Corporate Environmental Information Disclosure: An Empirical Study of Chinese Listed Companies. J. Clean. Prod. 2009, 17, 593–600. [Google Scholar] [CrossRef]

- Xie, X.; Shi, X.; Gu, J.; Xu, X. Examining the Contagion Effect of Credit Risk in a Supply Chain under Trade Credit and Bank Loan Offering. Omega 2023, 115, 102751. [Google Scholar] [CrossRef]

- Lu, X.; Wu, Z. How Taxes Impact Bank and Trade Financing for Multinational Firms. Eur. J. Oper. Res. 2020, 286, 218–232. [Google Scholar] [CrossRef]

- Sun, H.; Wang, G.; Bai, J.; Shen, J.; Zheng, X.; Dan, E.; Chen, F.; Zhang, L. Corporate Sustainable Development, Corporate Environmental Performance and Cost of Debt. Sustainability 2023, 15, 228. [Google Scholar] [CrossRef]

- Yao, X.; Ma, S.; Bai, Y.; Jia, N. When Are New Energy Vehicle Incentives Effective? Empirical Evidence from 88 Pilot Cities in China. Transp. Res. Part A Policy Pract. 2022, 165, 207–224. [Google Scholar] [CrossRef]

- Markovich, K.A.; Alekseevna, E.A.; Alekseevna, C.D. Ecological, Social and Governance Impact on the Company’s Performance: Information Technology Sector Insight. Procedia Comput. Sci. 2022, 214, 1065–1072. [Google Scholar] [CrossRef]

- Carbó-Valverde, S.; Rodríguez-Fernández, F.; Udell, G.F. Trade Credit, the Financial Crisis, and SME Access to Finance. J. Money Credit Bank. 2016, 48, 113–143. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Meaning | Calculation Method |

|---|---|---|

| SIZE | Firm size | The natural logarithm of the total assets at the end of the year |

| LEV | Asset-liability ratio | Total liabilities/total assets |

| ROE | Return on equity | Net profit/capital of shareholders’equit |

| INT | Interest coverage multiple | Earnings Before Interest and Tax/Finance costs |

| GROWTH | The growth rate of total assets | (Total assets at the end of the period − Total assets initial value of the period)/(Total assets at the end of the period) |

| CASH | Financing demand | When the sum of net cash flow from operating activities and investing activities for the period is less than or equal to 0, the value is 1, otherwise, it is 0 |

| AM | Asset maturity | Net fixed assets/total assets |

| BETA | Degree of total leverage | Change in net profit/Change in revenue from the main business |

| Variable | Obs | Mean | Std. Dev | Min | Max | VIF |

|---|---|---|---|---|---|---|

| TL | 1020 | 0.130 | 0.162 | −0.418 | 1.841 | - |

| TC | 1020 | 0.201 | 0.135 | 0.007 | 0.737 | 1.58 |

| SIZE | 1020 | 23.087 | 1.499 | 18.385 | 28.480 | 1.25 |

| LEV | 1020 | 0.531 | 0.202 | 0.030 | 1.262 | 1.66 |

| GROWTH | 1020 | 0.247 | 1.483 | −3.005 | 33.370 | 1.01 |

| INT | 1020 | 2.353 | 136.683 | −18.278 | 27.701 | 1.00 |

| CASH | 1020 | 0.520 | 0.500 | 0 | 1 | 1.01 |

| AM | 1020 | 0.254 | 0.185 | 0.000 | 0.846 | 1.28 |

| BETA | 1020 | 2.802 | 5.725 | 0 | 123.395 | 1.03 |

| ROE | 1020 | 0.062 | 0.247 | −1.731 | 5.301 | 1.09 |

| TL | TC | SIZE | LEV | GROWTH | INT | CASH | AM | BETA | ROE | |

|---|---|---|---|---|---|---|---|---|---|---|

| TL | 1.000 | |||||||||

| TC | −0.137 *** | 1.000 | ||||||||

| SIZE | 0.093 *** | 0.072 ** | 1.000 | |||||||

| LEV | 0.315 *** | 0.432 *** | 0.407 *** | 1.000 | ||||||

| GROWTH | 0.047 | −0.001 | 0.010 | 0.016 | 1.000 | |||||

| INT | 0.005 | 0.031 | −0.001 | 0.038 | −0.005 | 1.000 | ||||

| CASH | −0.024 | 0.028 | −0.056 * | −0.029 | −0.012 | 0.034 | 1.000 | |||

| AM | 0.153 *** | −0.428 *** | 0.015 | −0.060 * | 0.062 ** | 0.006 | −0.088 *** | 1.000 | ||

| BETA | 0.121 *** | −0.068 ** | −0.003 | 0.066 ** | −0.026 | 0.006 | −0.040 | 0.142 *** | 1.000 | |

| ROE | 0.199 *** | −0.009 | 0.032 | −0.222 *** | 0.036 | 0.005 | 0.046 | −0.056 * | −0.021 | 1.000 |

| E_High | E_Low | Total | ||||

|---|---|---|---|---|---|---|

| Model 1a | Model 1b | Model 2a | Model 2b | Model 3a | Model 3b | |

| TC | - | −0.583 *** (0.061) | - | −0.481 *** (0.057) | - | −0.498 *** (0.043) |

| SIZE | −0.016 *** (0.005) | −0.029 *** (0.005) | 0.001 (0.006) | −0.009 * (0.006) | −0.006 (0.004) | −0.015 *** (0.004) |

| LEV | 0.338 *** (0.049) | 0.614 *** (0.053) | 0.362 *** (0.040) | 0.583 *** (0.046) | 0.268 *** (0.031) | 0.486 *** (0.035) |

| GROWTH | 0.003 (0.003) | 0.002 (0.003) | 0.004 (0.006) | 0.005 (0.006) | 0.003 (0.003) | 0.003 (0.003) |

| INT | −0.000 (0.000) | −0.000 (0.000) | −0.000 (0.000) | −0.000 (0.000) | −0.000 (0.000) | 0.000 (0.000) |

| CASH | −0.007 (0.012) | −0.007 (0.011) | 0.005 (0.014) | 0.008 (0.013) | 0.008 (0.009) | 0.011 (0.009) |

| AM | 0.180 *** (0.035) | 0.009 (0.037) | 0.063 * (0.038) | −0.060 (0.038) | 0.122 *** (0.026) | −0.015 (0.028) |

| BETA | 0.003 (0.168) | 0.002 (0.002) | 0.003 *** (0.001) | 0.002 ** (0.001) | 0.003 *** (0.001) | 0.003 *** (0.001) |

| ROE | 0.181 *** (0.062) | 0.272 *** (0.057) | 0.216 *** (0.021) | 0.233 *** (0.020) | 0.000 *** (0.000) | 0.000 *** (0.000) |

| _cons | 0.236 ** (0.102) | 0.551 *** (0.099) | −0.107 (0.129) | 0.138 (0.123) | 0.042 (0.079) | 0.280 *** (0.077) |

| Time effect | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 510 | 510 | 510 | 510 | 1020 | 1020 |

| Adj-R2 | 0.684 | 0.618 | 0.279 | 0.373 | 0.144 | 0.246 |

| Model 4a | Model 4b | Model 4c | |

|---|---|---|---|

| TC | −0.541 *** (0.138) | 0.384 * (0.197) | −0.394 *** (0.113) |

| TC2 | −0.074 (0.222) | −0.887 *** (0.340) | −0.178 (0.188) |

| SIZE | −0.029 *** (0.005) | 0.018 *** (0.006) | −0.015 *** (0.003) |

| LEV | 0.619 *** (0.053) | −0.006 (0.005) | 0.480 *** (0.034) |

| GROWTH | 0.002 (0.003) | 0.006 (0.007) | 0.003 (0.003) |

| INT | −0.000 (0.000) | 0.000 (0.000) | −0.000 (0.000) |

| CASH | −0.008 (0.011) | −0.002 (0.014) | 0.010 (0.009) |

| AM | 0.012 (0.037) | 0.014 (0.043) | −0.008 (0.028) |

| BETA | 0.002 (0.002) | 0.003 *** (0.001) | 0.003 *** (0.001) |

| ROE | 0.274 *** (0.057) | 0.188 *** (0.026) | 0.000 *** (0.000) |

| _cons | 0.557 *** (0.096) | −0.310 ** (0.149) | 0.272 *** (0.076) |

| Time effect | Yes | Yes | Yes |

| Observations | 510 | 510 | 1020 |

| Adj-R2 | 0.278 | 0.156 | 0.237 |

| Model 5a | Model 5b | Model 5c | |

|---|---|---|---|

| TC t−1 | −0.528 *** (0.060) | −0.389 *** (0.058) | −0.353 *** (0.039) |

| SIZE | −0.027 *** (0.005) | −0.008 (0.006) | −0.013 *** (0.003) |

| LEV | 0.594 *** (0.054) | 0.542 *** (0.047) | 0.452 *** (0.028) |

| GROWTH | 0.003 (0.003) | −0.000 (0.006) | 0.001 (0.003) |

| INT | 0.000 (0.000) | 0.000 (0.000) | 0.000 (0.000) |

| CASH | −0.012 (0.011) | 0.007 (0.013) | −0.006 (0.009) |

| AM | 0.014 (0.038) | −0.024 (0.038) | 0.063 ** (0.026) |

| BETA | 0.002 (0.002) | 0.002 ** (0.001) | 0.002 ** (0.001) |

| ROE | 0.272 *** (0.058) | 0.242 *** (0.020) | 0.228 *** (0.019) |

| _cons | 0.502 *** (0.100) | 0.099 (0.127) | 0.232 *** (0.073) |

| Time effect | Yes | Yes | Yes |

| Observations | 510 | 510 | 1020 |

| Adj-R2 | 0.580 | 0.361 | 0.283 |

| E_High | E_Low | Total | ||||

|---|---|---|---|---|---|---|

| Model 1a | Model 1b | Model 2a | Model 2b | Model 3a | Model 3b | |

| TC | - | −0.093 * (0.219) | - | −0.438 *** (0.044) | - | −0.317 *** (0.029) |

| SIZE | −0.002 (0.017) | −0.000 (0.017) | 0.001 (0.005) | −0.008 * (0.004) | −0.002 (0.003) | −0.006 ** (0.002) |

| LEV | −0.424 ** (0.162) | −0.468 ** (0.193) | 0.211 *** (0.032) | 0.411 *** (0.036) | 0.176 *** (0.019) | 0.277 *** (0.020) |

| GROWTH | 0.001 (0.011) | 0.001 (0.011) | 0.001 (0.005) | 0.002 (0.005) | −0.001 (0.002) | −0.000 (0.002) |

| INT | 0.001 ** (0.000) | 0.001 ** (0.000) | −0.000 (0.000) | −0.000 (0.000) | −0.000 (0.000) | −0.000 (0.000) |

| CASH | −0.101 ** (0.041) | −0.101 ** (0.041) | 0.004 (0.010) | 0.007 (0.010) | 0.005 (0.007) | 0.004 (0.006) |

| AM | −0.013 (0.117) | 0.014 (0.134) | 0.071 ** (0.030) | −0.041 (0.030) | 0.105 *** (0.019) | 0.015 (0.019) |

| BETA | 0.001 (0.006) | 0.002 (0.006) | 0.002 ** (0.001) | 0.001 (0.001) | 0.001 ** (0.001) | 0.001 * (0.001) |

| ROE | 0.143 (0.204) | 0.129 (0.207) | 0.233 *** (0.017) | 0.249 *** (0.015) | 0.209 *** (0.014) | 0.222 *** (0.013) |

| _cons | 0.424 (0.338) | 0.374 (0.358) | −0.111 (0.103) | 0.112 (0.096) | −0.028 (0.056) | 0.083 (0.054) |

| Time effect | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 510 | 510 | 510 | 510 | 1020 | 1020 |

| Adj-R2 | 0.061 | 0.061 | 0.326 | 0.440 | 0.228 | 0.308 |

| E_High | E_Low | Total | ||||

|---|---|---|---|---|---|---|

| Model 1a | Model 1b | Model 2a | Model 2b | Model 3a | Model 3b | |

| TC | - | −0.266 *** (0.043) | - | −0.061 * (0.057) | - | −0.127 *** (0.027) |

| SIZE | −0.013 *** (0.003) | −0.020 *** (0.003) | −0.001 (0.004) | −0.003 * (0.004) | −0.009 *** (0.002) | −0.010 *** (0.002) |

| LEV | 0.202 *** (0.033) | 0.328 *** (0.037) | 0.161 *** (0.025) | 0.189 *** (0.030) | 0.173 *** (0.017) | 0.214 *** (0.019) |

| GROWTH | 0.002 (0.002) | 0.002 (0.002) | 0.003 (0.004) | 0.003 (0.004) | 0.002 (0.002) | 0.002 (0.002) |

| INT | −0.000 (0.000) | −0.000 (0.000) | −0.000 (0.000) | −0.000 (0.000) | −0.000 (0.000) | −0.000 (0.000) |

| CASH | −0.015 * (0.008) | −0.015 * (0.008) | 0.004 (0.009) | 0.004 (0.009) | −0.007 (0.006) | −0.007 (0.006) |

| AM | 0.116 *** (0.024) | 0.038 (0.026) | −0.008 (0.024) | −0.024 (0.026) | 0.057 *** (0.016) | 0.021 (0.018) |

| BETA | 0.002 * (0.001) | 0.002 * (0.001) | 0.001 (0.001) | 0.001 (0.001) | 0.001 (0.001) | 0.001 (0.001) |

| ROE | 0.110 ** (0.041) | 0.152 *** (0.040) | 0.004 (0.013) | 0.007 (0.013) | 0.013 (0.000) | 0.018 (0.012) |

| _cons | 0.236 *** (0.068) | 0.379 *** (0.070) | 0.018 (0.081) | 0.050 (0.084) | 0.163 *** (0.048) | 0.207 *** (0.049) |

| Time effect | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 510 | 510 | 510 | 510 | 1020 | 1020 |

| Adj-R2 | 0.147 | 0.687 | 0.216 | 0.185 | 0.123 | 0.141 |

| Model 6a | Model 6b | Model 6c | |

|---|---|---|---|

| TTC | −0.548 *** (0.077) | −0.394 *** (0.057) | −0.400 *** (0.047) |

| SIZE | −0.021 *** (0.005) | −0.009 (0.006) | −0.012 *** (0.004) |

| LEV | 0.495 *** (0.052) | 0.507 *** (0.044) | 0.402 *** (0.034) |

| GROWTH | 0.003 (0.003) | 0.003 (0.006) | 0.002 (0.003) |

| INT | −0.000 (0.000) | −0.000 (0.000) | 0.000 (0.000) |

| CASH | −0.006 (0.012) | 0.007 (0.013) | 0.010 (0.009) |

| AM | 0.079 ** (0.037) | 0.012 (0.037) | 0.056 ** (0.027) |

| BETA | 0.003 * (0.002) | 0.002 ** (0.001) | 0.003 *** (0.001) |

| ROE | 0.216 *** (0.059) | 0.226 *** (0.001) | 0.000 *** (0.000) |

| _cons | 0.393 *** (0.100) | 0.107 (0.126) | 0.203 ** (0.079) |

| Time effect | Yes | Yes | Yes |

| Observations | 510 | 510 | 1020 |

| Adj-R2 | 0.537 | 0.345 | 0.204 |

| Model 7a | Model 7b | Model 7c | |

|---|---|---|---|

| TC | −0.587 *** (0.061) | −0.486 *** (0.057) | −0.432 *** (0.040) |

| SIZE | −0.029 *** (0.005) | −0.008 (0.006) | −0.015 *** (0.003) |

| LEV | 0.618 *** (0.054) | 0.591 *** (0.046) | 0.478 *** (0.028) |

| GROWTH | 0.002 (0.003) | 0.005 (0.006) | 0.002 (0.003) |

| INT | −0.000 (0.000) | 0.000 (0.000) | −0.000 (0.000) |

| CASH | −0.007 (0.011) | 0.007 (0.013) | −0.004 (0.009) |

| AM | 0.011 (0.037) | −0.062 (0.038) | 0.037 (0.026) |

| BETA | 0.002 (0.002) | 0.002 ** (0.001) | 0.002 ** (0.001) |

| ROE | 0.269 *** (0.058) | 0.235 *** (0.020) | 0.221 *** (0.018) |

| AGE | −0.010 (0.019) | −0.031 (0.031) | 0.013 (0.016) |

| _cons | 0.588 *** (0.120) | 0.207 (0.141) | 0.235 *** (0.088) |

| Time effect | Yes | Yes | Yes |

| Observations | 510 | 510 | 1020 |

| Adj-R2 | 0.572 | 0.375 | 0.308 |

| Model 8a | Model 8b | Model 8c | |

|---|---|---|---|

| TC | −0.583 *** (0.061) | −0.492 *** (0.057) | −0.518 *** (0.041) |

| SIZE | −0.029 *** (0.005) | −0.011* (0.006) | −0.023 *** (0.003) |

| LEV | 0.614 *** (0.053) | 0.589 *** (0.046) | 0.590 *** (0.034) |

| GROWTH | 0.002 (0.003) | 0.005 (0.006) | 0.003 (0.003) |

| INT | −0.000 (0.000) | -0.000 (0.000) | −0.000 (0.000) |

| CASH | −0.007 (0.011) | 0.009 (0.013) | −0.000 (0.008) |

| AM | 0.008 (0.037) | −0.062 (0.038) | -0.016 (0.026) |

| BETA | 0.002 (0.002) | 0.002 ** (0.001) | 0.002 ** (0.001) |

| ROE | 0.271 *** (0.058) | 0.233 *** (0.020) | 0.238 *** (0.018) |

| ND/EBITDA | 0.000 (0.000) | 0.000 (0.000) | 0.000 (0.000) |

| _cons | 0.553 *** (0.100) | 0.167 (0.124) | 0.434 *** (0.074) |

| Time effect | Yes | Yes | Yes |

| Observations | 510 | 510 | 1020 |

| Adj-R2 | 0.292 | 0.377 | 0.323 |

| Model 9a | Model 9b | Model 9c | Model 9d | |

|---|---|---|---|---|

| TC | −0.477 *** (0.051) | −0.625 *** (0.050) | −0.324 *** (0.084) | −0.242 *** (0.075) |

| SIZE | −0.014 *** (0.004) | −0.003 (0.006) | −0.039 *** (0.008) | −0.004 (0.006) |

| LEV | 0.603 *** (0.041) | 0.733 *** (0.049) | 0.372 *** (0.063) | 0.261 *** (0.059) |

| GROWTH | −0.007 (0.008) | 0.001 (0.004) | 0.008 *** (0.003) | 0.001 (0.021) |

| INT | 0.000 (0.000) | 0.000 (0.000) | 0.000 (0.000) | 0.000 (0.000) |

| CASH | 0.043 *** (0.010) | 0.052 *** (0.013) | −0.039 *** (0.013) | −0.049 *** (0.017) |

| AM | 0.132 *** (0.033) | 0.168 *** (0.037) | −0.105 * (0.054) | −0.134 *** (0.045) |

| BETA | 0.001 (0.002) | 0.001 (0.001) | 0.000 (0.001) | 0.002 * (0.001) |

| ROE | 0.000 * (0.000) | −0.000 (0.000) | 0.000 * (0.000) | 0.317 *** (0.021) |

| _cons | 0.200 ** (0.080) | −0.072 (0.122) | 0.849 *** (0.175) | 0.089 (0.122) |

| Time effect | Yes | Yes | Yes | Yes |

| Observations | 250 | 250 | 260 | 260 |

| Adj-R2 | 0.595 | 0.699 | 0.335 | 0.534 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Du, Q.; Li, H.; Fu, Y.; Fu, X.; Wang, R.; Jia, T. More Green, Better Funding? Exploring the Dynamics between Corporate Bank Loans and Trade Credit. Sustainability 2023, 15, 10050. https://doi.org/10.3390/su151310050

Du Q, Li H, Fu Y, Fu X, Wang R, Jia T. More Green, Better Funding? Exploring the Dynamics between Corporate Bank Loans and Trade Credit. Sustainability. 2023; 15(13):10050. https://doi.org/10.3390/su151310050

Chicago/Turabian StyleDu, Qi’ang, Hongbo Li, Yanyan Fu, Xintian Fu, Rui Wang, and Tingting Jia. 2023. "More Green, Better Funding? Exploring the Dynamics between Corporate Bank Loans and Trade Credit" Sustainability 15, no. 13: 10050. https://doi.org/10.3390/su151310050