Digital Finance Promotes Corporate ESG Performance: Evidence from China

Abstract

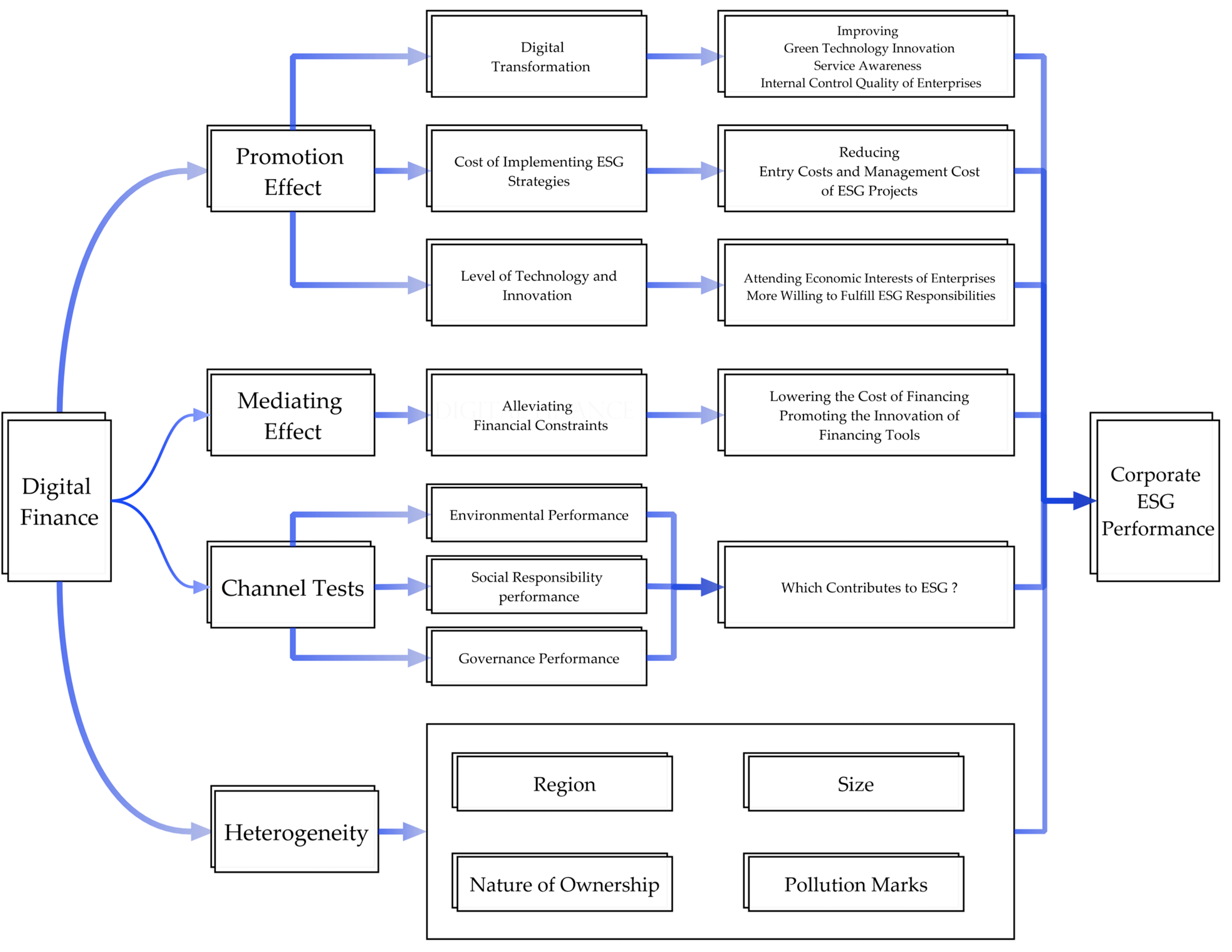

:1. Introduction

2. Research Hypotheses

2.1. Digital Finance Promotes Corporate ESG Performance

2.2. Digital Finance Promotes Corporate ESG Performance by Alleviating Its Financial Constraints

2.3. Channel Tests: Through Which Part of ESG Does Digital Finance Primarily Improve Corporate ESG Performance?

3. Methodology and Data

3.1. Data and Samples

3.2. Variables

3.2.1. Dependent Variable: Corporate ESG Performance (ESG_Index)

3.2.2. Independent Variable: DFI

3.2.3. Intermediary Variables: Financing Constraints

- WW index (WW): The financial constraint index constructed by Whited and Wu was used to measure the degree of financing distress faced by enterprises [53]. The larger the WW index, the greater the financing distress faced by enterprises.

- The ratio of annual interest expense to total debt (dfc): To verify that the results of this paper have not been affected by the selection of the financing constraint index, this paper referred to the research of Yu et al. [54]. The ratio of annual interest expense to total debt (dfc) was calculated as another proxy variable for corporate financing constraints.

3.2.4. Control Variables

- Referring to previous literature and our own investigation, we used the following control variables in our models:

- Firm year (Age): This paper uses the sample year minus the year the firm went public.

- Firm size (Size): This paper uses the natural logarithm of the firm’s total assets.

- Growth (Growth): This paper uses the growth rate of the firm’s operating revenue in the corresponding year.

- Profitability (LnEBIT): This paper uses the natural logarithm of the firm’s year-end Earnings Before Interest and Tax (EBIT).

- Board size (Board): This paper uses the logarithm of the number of board members.

- Percentage of independent directors (Indr): This paper uses the ratio of the number of independent directors to the total number of directors.

- Capital intensity (Capital): This paper uses the ratio of total assets to annual revenue.

- Corporate leverage ratio (Lev): This paper uses the ratio of total liabilities to total assets at the end of the period.

- Financial expense ratio (Fin): This paper uses the ratio of the enterprise’s current financial expense to operating revenue.

- Administrative expense ratio (mf): This paper uses the ratio of the enterprise’s current administrative expense to operating revenue.

3.3. Model

4. Results and Discussions

4.1. Descriptive Analysis

4.2. Empirical Results: Digital Finance Enhances Corporate ESG Performance

4.3. Empirical Results: Digital Finance Enhances Corporate ESG Performance by Alleviating Its Financial Constraints

4.4. Channel Tests

4.5. Robustness Tests

4.5.1. Replacing the Dependent Variable

4.5.2. Replacement of Independent Variable

4.5.3. Exclusion of Partial Data

4.5.4. Endogeneity Analysis

5. Further Research: Heterogeneity Analysis

5.1. Analysis of Regional Heterogeneity

5.2. Analysis of Property Rights

5.3. Analysis of Enterprise Size

5.4. Analysis of Polluting and Nonpolluting Enterprises

6. Research Conclusions and Policy Recommendations

7. Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Mohr, W.K.; Mahon, M.M. Dirty hands: The underside of marketplace health care. ANS 1996, 19, 28–37. [Google Scholar] [CrossRef] [PubMed]

- Evans-Reeves, K.; Lauber, K.; Hiscock, R. The ‘filter fraud’ persists: The tobacco industry is still using filters to suggest lower health risks while destroying the environment. Tob. Control 2022, 31, e80–e82. [Google Scholar] [CrossRef]

- Shun, T. The principle of profit maximization and consistent economic development—An economic paradox. Economist 2008, 3, 37–42. (In Chinese) [Google Scholar]

- Li, J.; Yang, Z.; Chen, J.; Cui, W. Study on the mechanism of ESG promoting corporate performance: Based on the perspective of corporate innovation ESG. Sci. Sci. Manag. ST 2021, 42, 71–89. Available online: http://www.ssstm.org/CN/Y2021/V42/I09/71 (accessed on 23 August 2022).

- Wu, S.; Li, X.; Du, X.; Li, Z. The impact of ESG performance on firm value: The moderating role of ownership structure. Sustainability 2022, 14, 14507. [Google Scholar] [CrossRef]

- Dexu, H.; Wenlong, M. Financial exclusion, financial inclusion and inclusive financial institution in China. Fin. Trade Econ. 2015, 3, 5–16. [Google Scholar] [CrossRef]

- Guo, F.; Wang, J.; Wang, F.; Kong, T.; Zhang, X.; Cheng, Z. Measuring China’s digital financial inclusion: Index compilation and spatial characteristics. China Econ. Q. 2020, 19, 1401–1418. [Google Scholar]

- Gomber, P.; Koch, J.A.; Siering, M. Digital Finance and FinTech: Current research and future research directions. J. Bus. Econ. 2017, 87, 537–580. [Google Scholar] [CrossRef]

- Cortina Lorente, J.; Schmukler, S.L. The fintech revolution: A threat to global banking? World Bank Res. Policy Briefs 2018, 14, 125038. [Google Scholar]

- Wang, Z. Digital finance, financing constraint and enterprise financial risk. J. Math. 2022, 2022, 2882113. [Google Scholar] [CrossRef]

- Li, J.; Wei, R.; Guo, Y. How can the financing constraints of SMEs be eased in China? -Effect analysis, heterogeneity test and mechanism identification based on digital inclusive finance. Front. Environ. Sci. 2022, 10, 949164. [Google Scholar] [CrossRef]

- Demertzis, M.; Merler, S.; Wolff, G.B. Capital markets union and the fintech opportunity. J. Finan. Regul. 2018, 4, 157–165. [Google Scholar] [CrossRef] [Green Version]

- Yu, L.; Zhao, D.; Xue, Z.; Gao, Y. Research on the use of digital finance and the adoption of green control techniques by family farms in China. Technol. Soc. 2020, 62, 101323. [Google Scholar] [CrossRef]

- Tang, D.; Chen, W.; Zhang, Q.; Zhang, J. Impact of digital finance on green technology innovation: The mediating effect of financial constraints. Sustainability 2023, 15, 3393. [Google Scholar] [CrossRef]

- Xue, Q.; Feng, S.; Chen, K.; Li, M. Impact of digital finance on regional carbon emissions: An empirical study of sustainable development in China. Sustainability 2022, 14, 8340. [Google Scholar] [CrossRef]

- Razzaq, A.; Yang, X. Digital finance and green growth in China: Appraising inclusive digital finance using web crawler technology and big data. Technol. Forecast. Soc. Chang. 2023, 188, 122262. [Google Scholar] [CrossRef]

- Lyu, Y.; Gu, B.; Zhang, J. Does digital finance enhance industrial green total factor productivity? Theoretical mechanism and empirical test. Environ. Sci. Pollut. Res. 2023; in press. [Google Scholar] [CrossRef]

- Muhammad, s.; Pan, Y.; Magazzino, C.; Luo, Y.; Waqas, M. The fourth industrial revolution and environmental efficiency: The role of fintech industry. J. Clean. Prod. 2022, 381, 135196. [Google Scholar] [CrossRef]

- Croutzet, A.; Dabbous, A. Do FinTech trigger renewable energy use? Evidence from OECD countries. Renew. Energy 2021, 179, 1608–1617. [Google Scholar] [CrossRef]

- Elheddad, M.; Benjasak, C.; Deljavan, R.; Alharthi, M.; Almabrok, J.M. The effect of the Fourth Industrial Revolution on the environment: The relationship between electronic finance and pollution in OECD countries. Technol. Forecast. Soc. Chang. 2021, 163, 120485. [Google Scholar] [CrossRef]

- Wen, B.; Cheng, P.; Liu, Y. The impact of digital financial development on commercial banks’ social responsibility—Based on the dual perspective of market environment and public concern. Study Pract. 2022, 8, 23–32. (In Chinese) [Google Scholar] [CrossRef]

- Alkhazaleh, A.M.K.; Haddad, H. How does the Fintech services delivery affect customer satisfaction: A scenario of Jordanian banking sector. Strateg. Chang. 2021, 30, 405–413. [Google Scholar] [CrossRef]

- Ayse, D.; Vanesa, P.; Yener, A.; Victor, M. Fintech, financial inclusion and income inequality: A quantile regression approach. Eur. J. Finan. 2022, 28, 86–107. [Google Scholar] [CrossRef]

- Henri, A.O.; Genevieve Lareine, A.B.; Kunz Modeste, M.B. Mobile money, family assistance and welfare in Cameroon. Telecommun. Policy 2023, 47, 102457. [Google Scholar] [CrossRef]

- Zhang, P.; Wang, Y.; Wang, R.; Wang, T. Digital finance and corporate innovation: Evidence from China. Appl. Econ. 2023, 1–24. [Google Scholar] [CrossRef]

- Huang, Z.; Tao, Y.; Luo, X.; Ye, Y.; Lei, T. Regional digital finance and corporate investment efficiency in China. Appl. Econ. 2022, 55, 5115–5134. [Google Scholar] [CrossRef]

- Chen, L. Digital inclusive finance, corporate governance and corporate M&A. Friends Account. 2022, 16, 91–98. (In Chinese) [Google Scholar]

- Al-Matari, E.M.; Mgammal, M.H.; Alosaimi, M.H.; Alruwaili, T.F.; Al-Bogami, S. Fintech, Board of Directors and Corporate Performance in Saudi Arabia Financial Sector: Empirical Study. Sustainability 2022, 14, 10750. [Google Scholar] [CrossRef]

- Arena, C.; Catuogno, S.; Naciti, V. Governing FinTech for performance: The monitoring role of female independent directors. Eur. J. Innovat. Manag. 2023. ahead-of-print. [Google Scholar] [CrossRef]

- Akhtar, Q.; Nosheen, S. The impact of fintech and banks M&A on Acquirer’s performance: A strategic win or loss? Borsa Istanbul Rev. 2022, 22, 1195–1208. [Google Scholar] [CrossRef]

- Abbasi, K.; Alam, A.; Du, M.; Huynh, T.L. FinTech, SME efficiency and national culture: Evidence from OECD countries. Technol. Forecast. Soc. Chang. 2021, 163, 120454. [Google Scholar] [CrossRef]

- Chen, M.; Luo, S. Digital finance development and the digital transformation of enterprises: Based on the perspective of financing constraint and innovation drive. J. Math. 2022, 1607020. [Google Scholar] [CrossRef]

- Thanh, T.T.; Ha, L.T.; Dung, H.P.; Huong, T.T.L. Impacts of digitalization on energy security: Evidence from European countries. Environ. Dev. Sustain. 2022, 1–46. [Google Scholar] [CrossRef] [PubMed]

- Xue, L.; Zhang, Q.; Zhang, X.; Li, C. Can digital transformation promote green technology innovation? Sustainability 2022, 14, 7497. [Google Scholar] [CrossRef]

- Meng, S.; Su, H.; Yu, J. Digital transformation and corporate social performance: How do board independence and institutional ownership matter? Front. Psychol. 2022, 13, 915583. [Google Scholar] [CrossRef] [PubMed]

- Cheng, L.; Hu, X. Enterprise digital development driven study on the quality improvement effect of internal control. Mod. Manag. Sci. 2022, 6, 111–119. (In Chinese) [Google Scholar]

- Xiao, H.; Shang, H. Digital corporate social responsibility: Current situation, problems and countermeasures. Rev. Ind. Econ. 2022, 6, 133–152. (In Chinese) [Google Scholar] [CrossRef]

- Wan, J.; Zhou, Q.; Xiao, Y. Digital finance, financial constraint and enterprise innovation. Econ. Rev. 2020, 1, 71–83. (In Chinese) [Google Scholar] [CrossRef]

- Claessens, S.; Tzioumis, K. Measuring Firms Access to Finance. World Bank 2006, 1–25. [Google Scholar]

- Deng, K.B.; Zeng, H.J. Financing constraints of Chinese firms: Characteristics, phenomena and causes. J. Econ. Res. 2014, 49, 47–60. [Google Scholar]

- Xie, X.; Shen, Y.; Zhang, H.; Guo, F. Can digital finance promote entrepreneurship? Evidence from China. China Econ. Q. 2018, 17, 1557–1580. [Google Scholar] [CrossRef]

- Ruan, J.; Shen, M.; Fan, Z. How can corporate debt financing costs be driven down? Utility identification, heterogeneity characteristics, and mechanism inspection in digital finance. Fin. Econ. Res. 2020, 35, 32–44. (In Chinese) [Google Scholar]

- Hao, Y. Corporate value creation and reinvention under ESG concept. Fin. Account. Monthly 2023, 44c, 20–25. (In Chinese) [Google Scholar] [CrossRef]

- Luo, X.; Du, S. Exploring the relationship between corporate social responsibility and firm innovation. Market. Lett. 2014, 26, 703–714. [Google Scholar] [CrossRef]

- Park, J.; Lee, H.; Kim, C. Corporate social responsibilities, consumer trust and corporate reputation: South Korean consumers’ perspectives. J. Bus. Res. 2014, 67, 295–302. [Google Scholar] [CrossRef]

- Barnett, M.L.; Salomon, R.M. Beyond dichotomy: The curvilinear relationship between social responsibility and financial performance. Strateg. Manag. J. 2006, 27, 1101–1122. [Google Scholar] [CrossRef]

- Turban, D.B.; Greening, D.W. Corporate social performance and organizational attractiveness to prospective employees. Acad. Manag. J. 1997, 40, 658–672. Available online: https://www.jstor.org/stable/257057 (accessed on 25 July 2022). [CrossRef]

- Chen, X.; Ma, L. Study on the relationship among the level of corporate governance, enterprise growth and enterprise value: The perspective of internal control. Forecasting 2015, 34, 28–32, 50. (In Chinese) [Google Scholar]

- Garcia, A.S.; Renato, J.O. Testing the institutional difference hypothesis: A study about environmental, social, governance, and financial performance. Bus. Strat. Environ. 2020, 29, 3261–3272. [Google Scholar] [CrossRef]

- Friedman, M. The social responsibility of business is to increase its profits. Corp. Ethics and Corp. Gov. 2007, 2007, 173–178. [Google Scholar] [CrossRef]

- Russo, M.V.; Fouts, P.A. A resource-based perspective on corporate environmental performance and profitability. Acad. Manag. J. 1997, 40, 534–559. [Google Scholar] [CrossRef]

- Kim, S.; Terlaak, A.; Potoski, M. Corporate sustainability and financial performance: Collective reputation as moderator of the relationship between environ-mental performance and firm market value. Bus. Strat. Environ. 2020, 30, 1689–1701. [Google Scholar] [CrossRef]

- Whited, T.M.; Wu, G. Financial constraints risk. Rev. Fin. Stud. 2006, 19, 531–559. [Google Scholar] [CrossRef]

- Yu, M.; Zhong, H.; Fan, R. Privatization, Privatization, financial constraints, and corporate innovation: Evidence from China’s industrial enterprises. J. Fin. Res. 2019, 4, 75–91. [Google Scholar]

- Wen, Z.; Ye, B. Analysis of mediating effects: Methodology and model development. Adv. Psychol. Sci. 2014, 22, 731–745. [Google Scholar] [CrossRef]

- Fuente, G.; Ortiz, M.; Velasco, P. The value of a firm’s engagement in ESG practices: Are we looking at the right side? Long Range Plann. 2022, 55, 102143. [Google Scholar] [CrossRef]

- Lin, M.; Xiao, Y. Digital finance, technological innovation and regional economic growth. J. Lanzhou Univ. 2022, 50, 47–59. (In Chinese) [Google Scholar] [CrossRef]

- Lv, L. Rethinking on deepening of state-owned enterprises reform. China Ind. Econ. 2002, 10, 5–11. (In Chinese) [Google Scholar] [CrossRef]

- Su, L. Trends in the responsibility of state-owned enterprises and new directions of corporate governance under ESG objectives. Communicat. Finan. Account. 2022, 18, 133–136, 147. (In Chinese) [Google Scholar] [CrossRef]

- Zhang, L.; Zhao, H. Does corporate environmental, social and corporate governance (ESG) performance affect corporate value?—An empirical study based on A-share listed companies. Wuhan Finan. Monthly 2019, 10, 36–43. (In Chinese) [Google Scholar]

- Zhang, X.; Hu, J. Does green credit policy inhibit investment in heavy polluters? Shandong Soc. Sci. 2022, 8, 138–146. (In Chinese) [Google Scholar] [CrossRef]

{kind=link}

| Variable | Variable Definitions | Symbols | Source |

|---|---|---|---|

| Dependent Variable | Corporate ESG performance | ESG_index | Hexun’s Social Responsibility Report for Listed Companies |

| ESG | ESG ratings published by Huazheng | ||

| Environmental performance | E_index | Secondary Index of Hexun’s Social Responsibility Report for Listed Companies | |

| Social performance | S_index | Secondary Index of Hexun’s Social Responsibility Report for Listed Companies | |

| Governance performance | G_index | Secondary Index of Hexun’s Social Responsibility Report for Listed Companies | |

| Independent Variable | Digital Finance Aggregate Index | DFI | Peking University DFI |

| Intermediary Variables | Financing Constraints | WW | WW Index |

| dfc | Interest Expense/Total Liabilities | ||

| Control variables | Firm Year | Age | Year of Sample–Year of Listing |

| Firm Size | Size | Ln (Enterprise’s Total Assets) | |

| Growth | Growth | The Growth Rate of the Enterprise’s Annual Operating Income | |

| Profitability | LnEBIT | Ln (EBIT) | |

| Board Size | Board | Ln (Number of Board Directors) | |

| Percentage of Independent Directors | Indr | Number of Independent Directors/ Number of Board Directors | |

| Capital Intensity | Capital | Total Assets/Annual Revenue | |

| Leverage | Lev | Total Liabilities/Total Assets | |

| Financial Expense Ratio | Fin | Financial Expenses/Revenue | |

| Administrative Expense Ratio | mf | Administrative Expenses/Operating Revenue |

| Variable | N | Mean | p50 | Sd | Min | Max |

|---|---|---|---|---|---|---|

| ESG_index | 9730 | 26.630 | 21.340 | 19.610 | −3.140 | 76.970 |

| ESG | 9730 | 3.995 | 4.000 | 1.047 | 1.000 | 6.000 |

| DFI | 9730 | 1.850 | 2.015 | 0.772 | 0.249 | 3.299 |

| WW | 9730 | −1.021 | −1.021 | 0.075 | −1.239 | −0.849 |

| dfc | 9730 | 0.024 | 0.023 | 0.015 | 0.000 | 0.067 |

| Age | 9730 | 11.960 | 12.000 | 6.075 | 1.000 | 24.000 |

| Size | 9730 | 22.380 | 22.220 | 1.277 | 19.850 | 26.180 |

| Growth | 9730 | 17.330 | 9.339 | 46.490 | −50.190 | 319.600 |

| LnEBIT | 9730 | 12.740 | 18.790 | 14.200 | −20.810 | 23.270 |

| Board | 9730 | 2.175 | 2.197 | 0.198 | 1.609 | 2.708 |

| Indr | 9730 | 37.160 | 33.330 | 5.325 | 33.330 | 57.140 |

| Capital | 9730 | 2.312 | 1.771 | 1.880 | 0.363 | 11.980 |

| Lev | 9730 | 0.487 | 0.487 | 0.200 | 0.083 | 0.959 |

| Fin | 9730 | 2.528 | 1.490 | 4.084 | −3.946 | 24.780 |

| mf | 9730 | 9.187 | 7.655 | 7.045 | 0.820 | 42.900 |

| ESG_Index | DFI | Age | Size | Growth | LnEBIT | Board | Indr | Capital | Lev | Fin | mf | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ESG_index | 1 | |||||||||||

| DFI | −0.122 *** | 1 | ||||||||||

| Age | −0.013 | 0.269 *** | 1 | |||||||||

| Size | 0.319 *** | 0.228 *** | 0.218 *** | 1 | ||||||||

| Growth | 0.036 *** | −0.0120 | −0.033 *** | 0.043 *** | 1 | |||||||

| LnEBIT | 0.328 *** | 0.0150 | −0.110 *** | 0.238 *** | 0.183 *** | 1 | ||||||

| Board | 0.122 *** | −0.074 *** | 0.049 *** | 0.245 *** | −0.021 ** | 0.048 *** | 1 | |||||

| Indr | 0.00800 | 0.035 *** | −0.00700 | 0.045 *** | −0.019 * | −0.023 ** | −0.440 *** | 1 | ||||

| Capital | −0.070 *** | 0.077 *** | 0.067 *** | 0.0120 | −0.061 *** | −0.156 *** | −0.0120 | 0.026 *** | 1 | |||

| Lev | −0.076 *** | −0.036 *** | 0.272 *** | 0.369 *** | 0.00200 | −0.120 *** | 0.105 *** | 0.0160 | −0.078 *** | 1 | ||

| Fin | −0.115 *** | −0.0100 | 0.160 *** | 0.112 *** | −0.074 *** | −0.167 *** | 0.066 *** | 0.00100 | 0.571 *** | 0.401 *** | 1 | |

| mf | −0.150 *** | 0.065 *** | −0.0160 | −0.348 *** | −0.104 *** | −0.310 *** | −0.104 *** | 0.047 *** | 0.495 *** | −0.216 *** | 0.173 *** | 1 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Variable | ESG_Index | ESG_Index | WW | ESG_Index | dfc | ESG_Index |

| DFI | 8.816 *** | 3.465 *** | −0.008 *** | 2.631 ** | −0.002 * | 3.309 *** |

| (1.466) | (1.260) | (0.002) | (1.238) | (0.001) | (1.256) | |

| WW | −99.719 *** | |||||

| (7.319) | ||||||

| dfc | −95.128 *** | |||||

| (22.089) | ||||||

| Age | 0.219 *** | 0.000 *** | 0.250 *** | 0.000 | 0.221 *** | |

| (0.055) | (0.000) | (0.054) | (0.000) | (0.055) | ||

| Size | 6.198 *** | −0.050 *** | 1.215 *** | −0.001 *** | 6.123 *** | |

| (0.274) | (0.000) | (0.449) | (0.000) | (0.271) | ||

| Growth | −0.006 * | −0.000 *** | −0.048 *** | −0.000 *** | −0.007 ** | |

| (0.003) | (0.000) | (0.005) | (0.000) | (0.003) | ||

| LnEBIT | 0.307 *** | −0.001 *** | 0.230 *** | −0.000 *** | 0.301 *** | |

| (0.018) | (0.000) | (0.018) | (0.000) | (0.018) | ||

| Board | 2.280 | −0.000 | 2.246 | −0.002 * | 2.086 | |

| (1.749) | (0.002) | (1.710) | (0.001) | (1.748) | ||

| Indr | 0.071 | 0.000 | 0.078 | 0.000 | 0.073 | |

| (0.060) | (0.000) | (0.058) | (0.000) | (0.060) | ||

| Capital | −0.612 *** | 0.001 ** | −0.536 *** | −0.002 *** | −0.843 *** | |

| (0.197) | (0.000) | (0.192) | (0.000) | (0.200) | ||

| Lev | −19.205 *** | 0.040 *** | −15.241 *** | −0.007 *** | −19.843 *** | |

| (1.813) | (0.003) | (1.783) | (0.002) | (1.807) | ||

| Fin | −0.118 | 0.000 ** | −0.085 | 0.003 *** | 0.156 | |

| (0.095) | (0.000) | (0.091) | (0.000) | (0.111) | ||

| mf | 0.187 *** | −0.000 | 0.176 *** | −0.000 *** | 0.161 *** | |

| (0.048) | (0.000) | (0.047) | (0.000) | (0.048) | ||

| Cons | 10.316 *** | −123.157 *** | 0.103 *** | −112.881 *** | 0.053 *** | −118.104 *** |

| (2.729) | (6.936) | (0.011) | (6.810) | (0.005) | (6.984) | |

| Time effect | YES | YES | YES | YES | YES | YES |

| Industry effect | YES | YES | YES | YES | YES | YES |

| N | 9730 | 9730 | 9730 | 9730 | 9730 | 9730 |

| Adj. | 0.095 | 0.305 | 0.863 | 0.324 | 0.434 | 0.308 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Variable | E_Index | E_Index | S_Index | S_Index | G_Index | G_Index |

| DFI | 0.060 | 0.024 | 1.901 *** | 1.715 ** | 1.463 *** | 0.850 *** |

| (0.437) | (0.438) | (0.737) | (0.738) | (0.350) | (0.292) | |

| WW | −4.334 * | −22.227 *** | −73.195 *** | |||

| (2.356) | (4.265) | (2.510) | ||||

| Age | 0.040 ** | 0.041 ** | 0.182 *** | 0.189 *** | −0.005 | 0.018 |

| (0.019) | (0.019) | (0.032) | (0.032) | (0.016) | (0.013) | |

| Size | 1.769 *** | 1.552 *** | 2.894 *** | 1.783 *** | 1.537 *** | −2.121 *** |

| (0.100) | (0.154) | (0.158) | (0.261) | (0.087) | (0.148) | |

| Growth | −0.004 *** | −0.006 *** | −0.006 *** | −0.016 *** | 0.005 *** | −0.026 *** |

| (0.001) | (0.002) | (0.002) | (0.003) | (0.001) | (0.001) | |

| LnEBIT | 0.007 | 0.004 | 0.090 *** | 0.073 *** | 0.208 *** | 0.151 *** |

| (0.006) | (0.006) | (0.011) | (0.011) | (0.006) | (0.005) | |

| Board | 0.639 | 0.637 | 1.203 | 1.196 | 0.358 | 0.333 |

| (0.621) | (0.621) | (1.022) | (1.017) | (0.449) | (0.378) | |

| Indr | 0.026 | 0.026 | 0.067 * | 0.068 ** | −0.024 | −0.018 |

| (0.021) | (0.021) | (0.035) | (0.035) | (0.016) | (0.013) | |

| Capital | −0.189 *** | −0.186 *** | −0.376 *** | −0.359 *** | −0.049 | 0.007 |

| (0.067) | (0.067) | (0.118) | (0.118) | (0.066) | (0.056) | |

| Lev | −2.505 *** | −2.333 *** | −5.082 *** | −4.198 *** | −11.547 *** | −8.637 *** |

| (0.607) | (0.613) | (1.051) | (1.058) | (0.563) | (0.480) | |

| Fin | 0.027 | 0.029 | −0.056 | −0.049 | −0.092 *** | −0.068 *** |

| (0.033) | (0.032) | (0.054) | (0.053) | (0.031) | (0.025) | |

| mf | 0.045 *** | 0.045 *** | 0.116 *** | 0.114 *** | 0.026 | 0.018 |

| (0.016) | (0.016) | (0.030) | (0.030) | (0.016) | (0.013) | |

| Cons | −38.319 *** | −37.872 *** | −63.496 *** | −61.205 *** | −21.024 *** | −13.481 *** |

| (2.486) | (2.499) | (3.917) | (3.922) | (2.191) | (1.879) | |

| Time effect | YES | YES | YES | YES | YES | YES |

| Industry effect | YES | YES | YES | YES | YES | YES |

| N | 9730 | 9730 | 9730 | 9730 | 9730 | 9730 |

| Adj. | 0.180 | 0.180 | 0.217 | 0.221 | 0.518 | 0.619 |

| (1) | (2) | |

|---|---|---|

| Variable | TobinQ | TobinQ |

| ESG_index | 0.007 *** | |

| (0.001) | ||

| E_index | 0.002 | |

| (0.004) | ||

| S_index | 0.006 ** | |

| (0.003) | ||

| G_index | 0.025 *** | |

| (0.004) | ||

| Age | 0.017 *** | 0.018 *** |

| (0.004) | (0.004) | |

| Size | −0.461 *** | −0.476 *** |

| (0.024) | (0.025) | |

| Growth | 0.001 *** | 0.001 ** |

| (0.000) | (0.000) | |

| LnEBIT | −0.002 | −0.005 *** |

| (0.001) | (0.001) | |

| Board | 0.109 | 0.111 |

| (0.093) | (0.094) | |

| Indr | 0.011 *** | 0.012 *** |

| (0.003) | (0.003) | |

| Capital | −0.070 *** | −0.070 *** |

| (0.015) | (0.015) | |

| Lev | 0.041 | 0.234 |

| (0.152) | (0.156) | |

| Fin | −0.004 | −0.002 |

| (0.006) | (0.006) | |

| mf | 0.042 *** | 0.042 *** |

| (0.005) | (0.005) | |

| Cons | 11.033 *** | 11.095 *** |

| (0.491) | (0.494) | |

| Time effect | YES | YES |

| Industry effect | YES | YES |

| N | 9379 | 9379 |

| Adj. | 0.403 | 0.407 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variable | ESG | ESG_Index | ESG_Index | ESG_Index |

| DFI | 0.148 * | 4.512 *** | 4.259 ** | |

| (0.076) | (1.563) | (1.681) | ||

| DFI_city | 1.252 * | |||

| (0.730) | ||||

| Age | −0.013 *** | 0.198 *** | 0.220 *** | 0.198 *** |

| (0.003) | (0.055) | (0.068) | (0.065) | |

| Size | 0.323 *** | 6.320 *** | 7.562 *** | 6.794 *** |

| (0.017) | (0.267) | (0.327) | (0.340) | |

| Growth | −0.002*** | −0.007 ** | 0.000 | −0.005 |

| (0.000) | (0.003) | (0.005) | (0.004) | |

| LnEBIT | 0.006 *** | 0.307 *** | 0.300 *** | 0.297 *** |

| (0.001) | (0.018) | (0.024) | (0.020) | |

| Board | 0.074 | 1.452 | 3.455 | 2.886 |

| (0.094) | (1.758) | (2.162) | (2.009) | |

| Indr | 0.016 *** | 0.043 | 0.125 | 0.065 |

| (0.003) | (0.061) | (0.076) | (0.067) | |

| Captial | −0.026 ** | −0.700 *** | −0.592 ** | −0.720 *** |

| (0.013) | (0.197) | (0.269) | (0.214) | |

| Lev | −1.126 *** | −20.082 *** | −21.277 *** | −19.816 *** |

| (0.108) | (1.837) | (2.342) | (1.999) | |

| Fin | −0.007 | −0.092 | −0.067 | −0.188 * |

| (0.005) | (0.096) | (0.123) | (0.102) | |

| mf | 0.001 | 0.193 *** | 0.195 *** | 0.250 *** |

| (0.003) | (0.049) | (0.061) | (0.057) | |

| Cons | −3.528 *** | −118.040 *** | −153.249 *** | −138.428 *** |

| (0.424) | (6.834) | (7.996) | (9.040) | |

| Time effect | YES | YES | YES | YES |

| Industry effect | YES | YES | YES | YES |

| N | 9730 | 9442 | 5687 | 7950 |

| Adj.R2 | 0.203 | 0.306 | 0.329 | 0.302 |

| IV-2sls (DFI_before1) | IV-2sls (Tele) | |||

|---|---|---|---|---|

| Stage 1 | Stage 2 | Stage 1 | Stage 2 | |

| Variable | DFI | ESG_Index | DFI | ESG_Index |

| DFI_before1 | 1.014 *** | |||

| (0.001) | ||||

| tele | 0.007 *** | |||

| (0.000) | ||||

| DFI | 3.089 ** | 4.847 *** | ||

| (1.215) | (1.543) | |||

| Kleibergen-Paap rk LM statistic P-val | 0 | 0 | ||

| Kleibergen-Paap rk Wald F statistic | 935.003 | 5618.510 | ||

| Hansen J statistic | 0 | 0 | ||

| Control variables | YES | YES | YES | YES |

| Time effect | YES | YES | YES | YES |

| Industry effect | YES | YES | YES | YES |

| N | 8256 | 9730 | ||

| 0.230 | 0.242 | |||

| ESG_Index | ESG_Index | |||

| Panel A | (1) | (2) | (3) | (4) |

| East | West | State-Owned | Non-State-Owned | |

| DFI | 3.396 ** | −7.548 | 4.738 *** | 2.493 |

| (1.360) | (8.908) | (1.725) | (1.793) | |

| Cons | −124.381 *** | −100.810 *** | −107.495 *** | −131.307 *** |

| (7.390) | (26.279) | (9.164) | (12.721) | |

| Control variables | YES | YES | YES | YES |

| Time effect | YES | YES | YES | YES |

| Industry effect | YES | YES | YES | YES |

| N | 8778 | 952 | 5184 | 4546 |

| 0.302 | 0.332 | 0.333 | 0.267 | |

| ESG_Index | ESG_Index | |||

| Panel B | (1) | (2) | (3) | (4) |

| Large-Scale | Small-Scale | Polluting | Nonpolluting | |

| DFI | 3.303 * | 3.636 ** | 3.615 * | 2.941 * |

| (1.742) | (1.617) | (2.159) | (1.580) | |

| Cons | −105.858 *** | −108.132 *** | −114.746 *** | −129.474 *** |

| (11.076) | (14.734) | (12.111) | (8.498) | |

| Control variables | YES | YES | YES | YES |

| Time effect | YES | YES | YES | YES |

| Industry effect | YES | YES | YES | YES |

| N | 4842 | 4888 | 3568 | 6162 |

| 0.315 | 0.224 | 0.307 | 0.308 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mo, Y.; Che, Y.; Ning, W. Digital Finance Promotes Corporate ESG Performance: Evidence from China. Sustainability 2023, 15, 11323. https://doi.org/10.3390/su151411323

Mo Y, Che Y, Ning W. Digital Finance Promotes Corporate ESG Performance: Evidence from China. Sustainability. 2023; 15(14):11323. https://doi.org/10.3390/su151411323

Chicago/Turabian StyleMo, Yalin, Yuchen Che, and Wenqiao Ning. 2023. "Digital Finance Promotes Corporate ESG Performance: Evidence from China" Sustainability 15, no. 14: 11323. https://doi.org/10.3390/su151411323