1. Introduction

With the proposal of a community with a shared future for humanity, countries worldwide are paying increasing attention to constructing an ecological civilization. The formulation and improvement of environmental protection policies and regulations have been of concern to experts and scholars from various countries. The signing of the Paris Agreement puts forward higher requirements for Chinese environmental governance. In order to build a green ecological society, the Chinese government has made environmental protection a basic national policy. For decades, under the economic model of the government-led and vigorously developing heavy industry, Chinese firms have achieved rapid development. However, they have simultaneously brought about severe ecological and environmental problems [

1]. Given this, China carried out the emission fee system in 1979, curbing the willful environmental violations of firms’ pollutant emissions [

2], which has made contributions to energy conservation and emission reduction. However, due to the lack of mandatory and supervisory power, the pollution levy system presents several problems, such as low executive power and nonstandard market supervision. To complete the economic assessment indicators, some local governments often co-operate with firms, interfere with the collection of environmental fees, and reduce the environmental supervision of high-polluting firms, resulting in the phenomenon of “treating while polluting” and the poor pollution reduction effect of the pollution levy system [

3]. In the new era, the Chinese government has put forward higher requirements for the green environmental protection behavior of firms and continuously improves relevant laws and regulations on environmental protection. Therefore, exploring whether macroeconomic environmental policies can effectively promote the improvement of corporate environmental behavior has theoretical and practical significance.

Environmental performance, as the ultimate standard for evaluating environmental policies, is also an important means of evaluating corporate environmental behavior. Its measurement not only includes financial indicators (such as the payment of environmental taxes, green innovation investment in environmental management, and government subsidies for environmental management) but also non-financial performance indicators (such as the development of environmental protection concepts, green culture, and environment-related policies). In the environmental governance system, the state regulates the environmental behavior of firms via environmental policies and relevant laws, and local governments urge enterprises to pay attention to environmental issues via environmental supervision and other means. However, as an “economic person”, a corporation will consider its economic interests from a cost–benefit perspective. It will avoid environmental responsibilities, resulting in the poor implementation of environmental policies. In addition, there is a U-shaped relationship between the environmental investment of firms and environmental regulation. Firms are willing to bear a lower penalty with weak environmental regulation and will not consider a higher environmental investment. In contrast, when environmental regulations are stricter, firms will increase investment in environmental protection, thus improving their environmental performance [

4]. Existing literature generally uses evaluation standards issued by relevant departments or pollution emission standards of companies as environmental performance evaluation indicators, such as using sulfur dioxide emission intensity to characterize environmental performance levels [

5,

6,

7,

8]. However, an increasing number of scholars are combining theories such as the Balanced Scorecard and EVA to construct a comprehensive environmental evaluation system based on information such as annual reports, social responsibility reports, and environmental reports of listed companies [

9,

10,

11,

12,

13]. This paper quantitatively evaluates the environmental protection strategy, environmental management, and environmental impact of enterprises based on the evaluation criteria constructed by existing literature, which can more comprehensively reflect the environmental performance of firms.

In order to optimize corporate environmental behavior, governments around the world have actively formulated environmental policies, and many scholars have evaluated the effectiveness of environmental policy implementation. According to the experimental results of the effects of environmental protection tax policies in developed countries, gradually increasing the tax can achieve a win–win situation for economic and environmental interests [

14]. Environmental tax policies in European countries can affect clean enterprise investment and financing activities [

15]. Based on years of implementation of environmental taxes abroad and extensive research by scholars, to solve the drawbacks of the pollution levy system and reduce the pollutant emissions of firms, the Standing Committee of the Twelfth National People’s Congress of China promulgated the Environmental Protection Tax Law of the People’s Republic of China (hereafter referred to as the Environmental Protection Tax) on 25 December 2016, which was officially implemented on 1 January 2018. In the academic community’s research on the policy effectiveness of stricter environmental regulations—Environmental Protection Tax—some scholars analyze the ecological footprint level of provinces from a macro level [

16], but more research mainly focuses on the impact of this policy on environmental protection investment, green innovation, and corporate performance at the micro-enterprise level. The research on the impact of environmental regulation on environmental protection investment has yet to reach an agreement [

17]. Without external intervention, most firms will not be willing to carry out green technology innovation actively. With government regulation, firms will greatly increase their investment in environmental protection and green technology innovation [

18,

19].

According to the innovation compensation theory, the strict Environmental Protection Tax will increase the environmental costs of firms in the short term. The firms can obtain green technology innovation by increasing their research and development expenditure, promoting a green transformation. In the long term, it can effectively reduce pollution emissions to offset the increased costs, enhance market competitiveness, and ultimately improve corporate performance, such as operating profit [

20,

21]. However, some scholars have proposed that the Environmental Protection Tax will increase firms’ green investment, crowding out other resources and reducing corporate performance [

22,

23]. The effect of the policy implementation on the performance improvement of firms is not evident in the short term. While strengthening the implementation of the policy, it is necessary to restrain the collusion of local governments and local firms in the emission of pollutants to promote and encourage firms to improve the ecological environment [

24].

In today’s world, where environmental accounting is increasingly valued, research on corporate environmental performance and the effectiveness of environmental policies is also increasing and becoming more detailed. However, most existing literature studies the macro impact of the Environmental Protection Tax, the impact of environmental taxes on firms (such as corporate environmental investment, green innovation investment, and green total factor productivity), and the impact of other environmental regulatory policies on corporate environmental performance. Can implementing the Environmental Protection Tax, which is still in its infancy, improve corporate environmental performance? Can local governments encourage firms to improve their environmental management level and play an essential role in enhancing corporate environmental performance in strengthening the environmental supervision of firms? The questions above have become vital issues that presently need to be discussed. However, there is currently limited research on the relationship between the Environmental Protection Tax, local regulation, and corporate environmental performance. Based on this, this paper links the three together and explores the impact of the Environmental Protection Tax on corporate environmental performance in heavily polluting industries. The intensity of local environmental regulation is used as an intermediary variable to further study its mediating role.

This paper compiles the relevant data of listed firms in the Chinese A-share heavy-pollution industries from 2016 to 2020 under the background of the environmental tax reform by using the differences-in-differences (DID) method to test the impact of the environmental tax reform on the corporate environmental performance and combines the environmental supervision intensity of local governments to analyze its internal mechanism and the heterogeneity of the impact. It is determined that the environmental tax reform will promote improving corporate environmental performance via local supervision. This policy has a more prominent effect on improving environmental performance in non-state-owned enterprises and western firms.

Compared with the existing literature, the contributions of this paper are as follows: Firstly, it enriches the research on the corporate environmental behavior of the environmental tax reform from the perspective of corporate environmental performance. Most of the available literature primarily focuses on the impact of pollutant emissions, environmental protection investment, green innovation capability, corporate financial performance, or other aspects. This paper, instead, focuses on the effect of the environmental tax reform on corporate environmental behavior to confirm the environmental governance effect of the policy on firms. The evaluation is more comprehensive and is a supplement to the existing literature research perspective.

Secondly, it effectively identifies the specific path of the effect of the environmental tax reform from the central government to firms, supplementing the perspective of institutional theory. This paper put central–local– firms within the same analytical framework, combining the principal–agent theory with institutional theory to analyze the role path of central policies. It is found that the environmental supervision intensity of the local government can increase the environmental governance pressure of firms, drive the green transformation and upgrading of firms, and effectively improve environmental performance.

Thirdly, it clarifies the effective boundary of the environmental tax reform to improve corporate environmental performance, providing policy recommendations for the subsequent reform of the environmental protection tax. The environmental tax reform has a more significant effect on improving corporate environmental performance with different property attributes and geographical locations. It provides a new concept for promoting the Environmental Protection Tax, giving full play to local governments’ regulatory role and improving environmental governance. It has significant practical significance for the central government in formulating laws, local governments in implementing supervision, and enterprises in improving environmental performance levels.

The remainder of this paper is organized as follows:

Section 2 provides the institutional background and research hypothesis,

Section 3 encompasses the research design,

Section 4 provides the empirical results and mechanism test,

Section 5 provides further analysis, and

Section 6 is the conclusion.

6. Discussion and Conclusions

6.1. Discussion

As a major reform of the Chinese environmental tax system, the environmental tax reform has promoted improving corporate environmental performance. Based on data from Chinese-listed heavy-pollution firms from 2016 to 2020, this paper evaluates the environmental management behavior of firms and the governance effectiveness of the environmental tax reform via the differences-in-differences (DID) method. It is found that implementing the environmental tax reform will promote the improvement of corporate environmental performance, which can be achieved via the environmental supervision of local governments. Among non-state enterprises and firms in the western region, the environmental tax reform has a more significant effect on improving corporate environmental performance.

Through the main effect test, the implementation of the Environmental Protection Tax will increase the environmental performance score of firms by 0.58. Our study shows that the implementation of the Environmental Protection Tax will improve firm environmental performance, and H1 is accepted. Although some scholars currently believe that the promotion effect is not significant [

23], more scholars believe that this policy is effective from the perspective of emission levels [

33]. The reason for the differences may lie in the inclusion of different measurement standards in the construction of environmental performance evaluation systems. This paper constructs an evaluation index system for the environmental protection strategy, environmental management, and environmental impact based on the annual report, social responsibility report, and environmental report of listed companies, selecting multiple indicators such as environmental pollution control, environmental pollution consumption, and environmental resource recovery, with wider coverage.

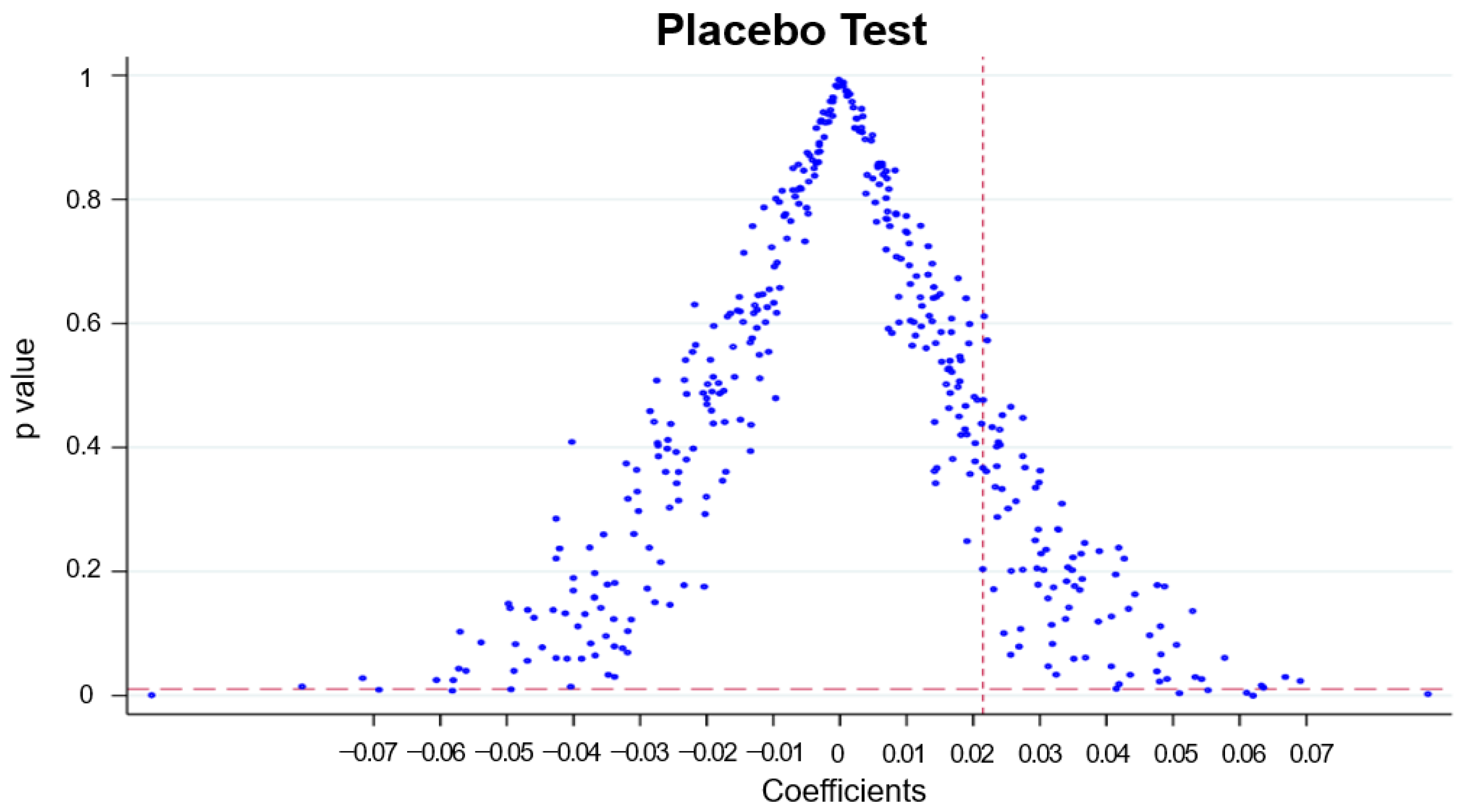

In the parallel trend test, we found that the interaction coefficient of the year after policy implementation has improved. Although the confidence interval at the 5% level is not significantly different from zero, it can be significantly different from zero with 90% confidence. In the year after implementation, the confidence interval can be significantly different from zero at the 5% confidence level. This can indicate that the implementation of policies has an impact on corporate environmental performance, but there is a certain lag in policies, which is basically consistent with the conclusions of existing literature [

24].

After adding the mechanism variable LER, the impact of the Environmental Protection Tax on corporate environmental performance is still significantly positive, indicating that the mediating effect of local environmental regulation is the result of partial mediation. After the implementation of the Environmental Protection Tax, all environmental taxes will belong to the local government, and the central government will supervise and assess the governance achievements of the local government. Starting from the principal–agent theory, the Environmental Protection Tax enhances the autonomy and governance enthusiasm of local governments. Therefore, local government regulation plays a positive role in promoting the growth of corporate environmental performance, and H2 is accepted.

In the heterogeneity test, the Environmental Protection Tax has a more significant effect on improving the environmental performance of non-state-owned and western-region enterprises. The positive impact of the Environmental Protection Tax on corporate environmental performance is not significant among state-owned enterprises, possibly due to the fact that state-owned enterprises already had better environmental performance before the policy implementation compared to non-state-owned enterprises. The overall environmental performance and local regulatory intensity of enterprises in the eastern region are higher, possibly because the environmental performance level of enterprises in the eastern region was already at a good level before the implementation of policies, and the impact of environmental tax policies on environmental performance is not significant. At the same time, it may be because the local governments in the central region did not have a significant difference in setting environmental protection tax collection standards compared to the previous pollution discharge fees, so the average interaction term of enterprises with the Environmental Protection Tax in the central region is significantly lower than in other regions.

6.2. Theoretical and Practical Contributions

This paper enriches the institutional theoretical framework by combining the principal–agent theory. The existing literature on the effectiveness of environmental systems is limited to the impact of policies on industries or firms, and lacks the observation of policy implementation paths. This paper considers the transmission mechanism of central policies, optimizes the agency relationship between the central government and local governments through environmental tax reform, and expands the application scenarios of institutional theory in environmental protection.

In response to the above discussions and conclusions, this paper proposes the following policy implications, which have practical guiding significance for the central government, local governments, and firms:

(1) The central government should adequately implement the rights and responsibilities of environmental governance to the local government, and the local government should strengthen the supervision of the environmental pollution emissions of local firms. The central government considers environmental protection an essential part of the national development strategy. Through implementing taxation and management power at all levels, the initiative of local governments in environmental protection can be enhanced. At the same time, the central government can reduce the possibility of local governments ignoring environmental performance and co-operating with high-polluting corporations to achieve economic performance indicators by building a comprehensive evaluation system and supervising local governments through a multi-dimensional environmental performance assessment of local governments.

(2) Local governments need to strengthen the environmental supervision of local firms further to achieve the long-term co-ordinated development of the regional economy and environmental protection. By improving the tax mechanism, enhancing tax collection management, and adequately raising the tax collection standards, the local government forces firms to reduce pollution, prevents firms from paying pollution discharge to pollute, and promotes the green transformation and modernization of firms.

(3) Firms with heavy pollution should optimize their internal environmental management and reduce their environmental risks according to the continuous changes in environmental policies. When there are major changes in the external environment (such as implementing stricter Environmental Protection Tax policies), non-state-owned enterprises with less supervision and firms with heavy pollution in the western region will be more affected. Firms should strengthen their management, enhance their green innovation capacity, actively disclose environmental protection policies and green performance, conduct production activities with higher standards, reduce the risks brought by changes in environmental policies to corporations, and take appropriate preventive measures.

6.3. Limitations and Further Study

The main limitations of this study are as follows: (1) The time window for studying the Environmental Protection Tax is relatively short. The policy was implemented in 2018, so this paper selects 2016–2020 as the research window period. However, the effects of macroeconomic environmental regulation policies often have hysteresis, making it difficult to see changes at the micro level in the short term of one or two years. (2) The research object is currently concentrated on listed companies of heavily polluting firms, and there are more heavily polluting small- and medium-sized firms that have not been considered. For these small- and medium-sized unlisted firms, government regulation will be more difficult and will have a partial impact on the results.

The following improvements can be made in future research: (1) Expand the sample object data, expand the policy research time to five years before and after, and use empirical verification to verify the conclusions again. (2) If the government puts forward more requirements for the disclosure of the environmental performance of various enterprises, we can include more non-listed companies in the future.

{kind=link}