Does ESG Impact Firms’ Sustainability Performance? The Mediating Effect of Innovation Performance

,

,

Abstract

:1. Introduction

- RQ 1: How does ESG performance influence the sustainability performance of the Bangladeshi manufacturing industry?

- RQ 2: How does innovation mediate the relationship between ESG initiatives and sustainability performance in the Bangladeshi manufacturing industry?

2. Literature Review and Hypothesis Development

2.1. Theoretical Background

2.2. Sustainability Performance

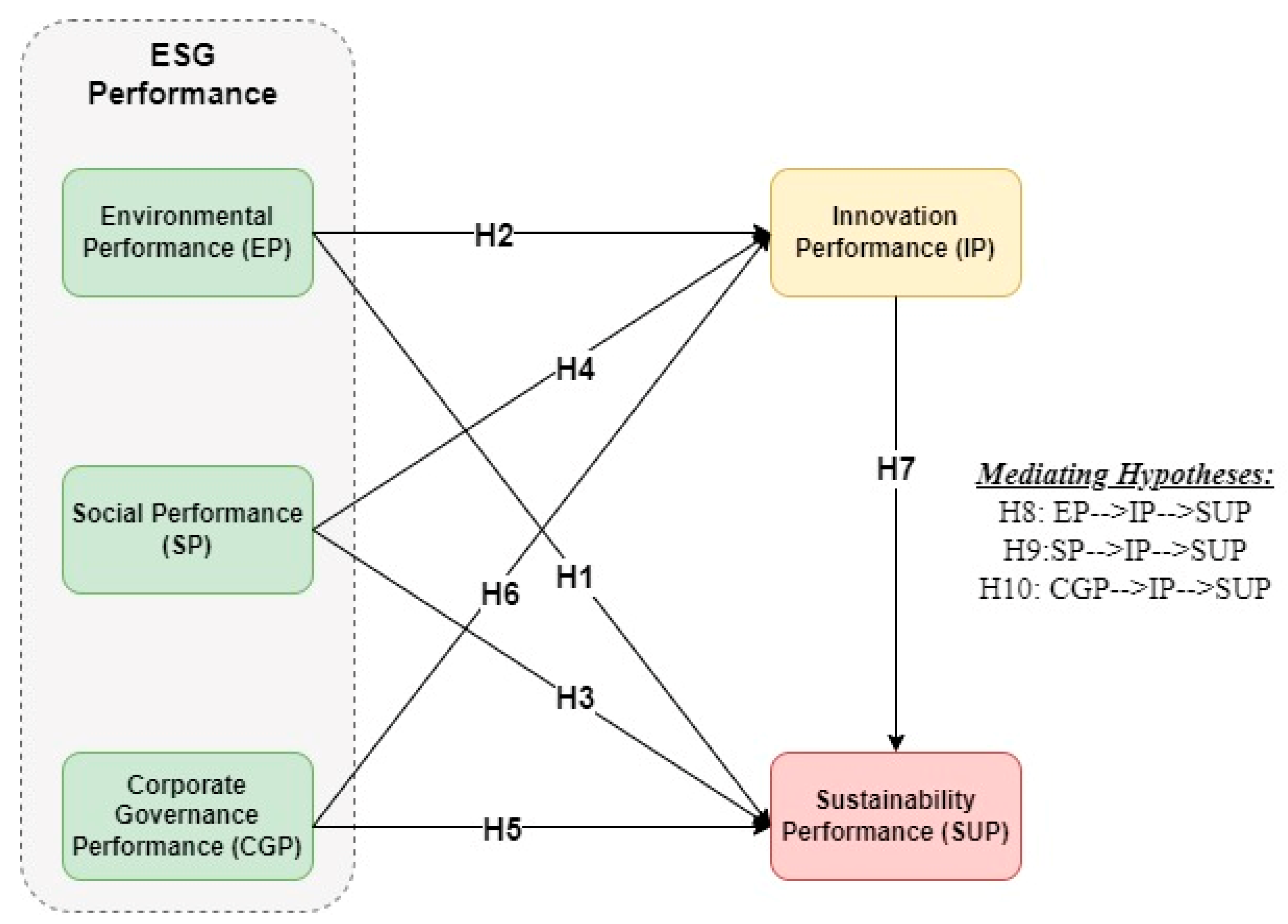

2.3. Hypothesis Development

2.3.1. Environmental Performance, Innovation Performance and Sustainability Performance

2.3.2. Social Performance, Innovation Performance and Sustainability Performance

2.3.3. Corporate Governance Performance, Innovation Performance and Sustainability Performance

2.3.4. Innovation Performance and Sustainability Performance

2.3.5. The Mediating Role of Innovation on the Relationship between ESG and Sustainability Performance

3. Materials and Methods

3.1. Sample and Data Collection Procedure

3.2. Measurement Instrument

3.3. Variables Description

3.4. Data Analysis Tools

4. Results

4.1. Descriptive Statistics

4.2. Reflective Measurement Model

4.3. Model Fit Statistics

4.4. SEM Hypotheses Testing

5. Discussion and Conclusions

6. Theoretical and Practical Implications of the Study

7. Limitations and Directions for Future Studies

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Item Code | Descriptions | Sources |

|---|---|---|

| Environmental Performance (ENP) | ||

| ENP1 | Reduction of air emissions. | [110] |

| ENP2 | Minimization of effluent/solid waste. | |

| ENP3 | Less consumption of hazardous/harmful/toxic materials. | |

| ENP4 | Reduced the frequency of environmental accidents. | |

| Social Performance (SOP) | ||

| SOP5 | Training and development of employee | [17] |

| SOP6 | Promotion of employee occupational health and safety | |

| SOP7 | Employee job security and satisfaction | |

| SOP8 | Commitment to community and society satisfaction | |

| SOP9 | Supplier commitment and initiative | |

| Corporate governance performance (CGP) | ||

| CGP10 | Compliance with the set standards | [39] |

| CGP11 | Improvement of environmental compliance | |

| CGP12 | Improved the set of rules and regulations | |

| CGP13 | Enhancement of risk control mechanism | |

| CGP14 | Promotion of transparency and accountability | |

| Innovation performance (INP) | ||

| INP15 | Improvement of the level of customer satisfaction with product design and development. | [76] |

| INP16 | Development of products that are easy to recycle, reuse and decompose. | |

| INP17 | Improved continual introduction of new product ideas into the production process. | |

| INP18 | Improved market success of new products being tested. | |

| Sustainability performance (SUP) | ||

| SUP19 | Reduction of the rate of energy consumption and enhancement of economic development | [42,43] |

| SUP20 | Strengthening of the capacity for innovation in green technology and enhancement of competitiveness in the global arena | |

| SUP21 | Promotion of sustainable development and preservation of the environment for future generations | |

| SUP22 | Promotion of best practices and public awareness of the sustainability performance. | |

References

- Chin, T.A.; Tat, H.H.; Sulaiman, Z. Green Supply Chain Management, Environmental Collaboration and Sustainability Performance. Procedia CIRP 2015, 26, 695–699. [Google Scholar] [CrossRef] [Green Version]

- Acciaro, M.; Vanelslander, T.; Sys, C.; Ferrari, C.; Roumboutsos, A.; Giuliano, G.; Lee Lam, J.S.; Kapros, S. Environmental sustainability in seaports: A framework for successful innovation. Marit. Policy Manag. 2014, 41, 480–500. [Google Scholar] [CrossRef]

- Iqbal, Q.; Ahmad, N.H.; Halim, H.A. Insights on entrepreneurial bricolage and frugal innovation for sustainable performance. Bus. Strat. Dev. 2021, 4, 237–245. [Google Scholar] [CrossRef]

- Niroumand, M.; Shahin, A.; Naghsh, A.; Peikari, H.R. Frugal innovation enablers: A comprehensive framework. Int. J. Innov. Sci. 2020, 12, 1–20. [Google Scholar] [CrossRef]

- Iqbal, Q.; Ahmad, N.H.; Ahmad, B. Enhancing sustainable performance through job characteristics via workplace spirituality: A study on SMEs. J. Sci. Technol. Policy Manag. 2021, 12, 463–490. [Google Scholar] [CrossRef]

- Holden, E.; Linnerud, K.; Banister, D. The Imperatives of Sustainable Development: Needs, Justice, Limits; Routledge: Oxford, UK, 2017. [Google Scholar]

- Xu, J.; Liu, F.; Shang, Y. R&D investment, ESG performance and green innovation performance: Evidence from China. Kybernetes 2020, 50, 737–756. [Google Scholar] [CrossRef]

- Li, T.-T.; Wang, K.; Sueyoshi, T.; Wang, D.D. ESG: Research Progress and Future Prospects. Sustainability 2021, 13, 11663. [Google Scholar] [CrossRef]

- Broadstock, D.C.; Chan, K.; Cheng, L.T.; Wang, X. The role of ESG performance during times of financial crisis: Evidence from COVID-19 in China. Financ. Res. Lett. 2021, 38, 101716. [Google Scholar] [CrossRef]

- Alsayegh, M.F.; Rahman, R.A.; Homayoun, S. Corporate Economic, Environmental, and Social Sustainability Performance Transformation through ESG Disclosure. Sustainability 2020, 12, 3910. [Google Scholar] [CrossRef]

- Hussain, N.; Rigoni, U.; Orij, R. Corporate Governance and Sustainability Performance: Analysis of Triple Bottom Line Performance. J. Bus. Ethic 2018, 149, 411–432. [Google Scholar] [CrossRef]

- Maali, K.; Rakia, R.; Khaireddine, M. How corporate social responsibility mediates the relationship between corporate governance and sustainability performance in UK: A multiple mediator analysis. Soc. Bus. Rev. 2021, 16, 201–217. [Google Scholar] [CrossRef]

- Yang, Q.; Du, Q.; Razzaq, A.; Shang, Y. How volatility in green financing, clean energy, and green economic practices derive sustainable performance through ESG indicators? A sectoral study of G7 countries. Resour. Policy 2022, 75, 102526. [Google Scholar] [CrossRef]

- Ye, C.; Song, X.; Liang, Y. Corporate sustainability performance, stock returns, and ESG indicators: Fresh insights from EU member states. Environ. Sci. Pollut. Res. 2022, 29, 87680–87691. [Google Scholar] [CrossRef] [PubMed]

- Yoon, B.; Lee, J.H.; Byun, R. Does ESG Performance Enhance Firm Value? Evidence from Korea. Sustainability 2018, 10, 3635. [Google Scholar] [CrossRef] [Green Version]

- Rajesh, R. Exploring the sustainability performances of firms using environmental, social, and governance scores. J. Clean. Prod. 2020, 247, 119600. [Google Scholar] [CrossRef]

- Sultana, S.; Zulkifli, N.; Zainal, D. Environmental, Social and Governance (ESG) and Investment Decision in Bangladesh. Sustainability 2018, 10, 1831. [Google Scholar] [CrossRef] [Green Version]

- Zheng, G.-W.; Siddik, A.B.; Masukujjaman, M.; Fatema, N. Factors Affecting the Sustainability Performance of Financial Institutions in Bangladesh: The Role of Green Finance. Sustainability 2021, 13, 10165. [Google Scholar] [CrossRef]

- Tribune, D. Is Bangladesh’s Manufacturing Sector Fit to Compete? 2022. Available online: https://www.dhakatribune.com/business/2022/10/11/is-bangladeshs-manufacturing-sector-fit-to-compete (accessed on 12 October 2022).

- Zaid, A.A.; Jaaron, A.A.M.; Bon, A.T. The impact of green human resource management and green supply chain management practices on sustainable performance: An empirical study. J. Clean. Prod. 2018, 204, 965–979. [Google Scholar] [CrossRef]

- Hossan, C.G.; Sarker, M.A.R.; Afroze, R. Recent unrest in the RMG sector of Bangladesh: Is this an outcome of poor labour practices? Int. J. Bus. Manag. 2012, 7, 206. [Google Scholar] [CrossRef] [Green Version]

- Ansary, M.A.; Barua, U. Workplace safety compliance of RMG industry in Bangladesh: Structural assessment of RMG factory buildings. Int. J. Disaster Risk Reduct. 2015, 14, 424–437. [Google Scholar] [CrossRef]

- Rashid, M.H.U.; Zobair, S.A.M.; Shadek, M.J.; Hoque, M.A.; Ahmad, A. Factors Influencing Green Performance in Manufacturing Industries. Int. J. Financ. Res. 2019, 10, 159–173. [Google Scholar] [CrossRef]

- Tariq, A.; Badir, Y.; Chonglerttham, S. Green innovation and performance: Moderation analyses from Thailand. Eur. J. Innov. Manag. 2019, 22, 446–467. [Google Scholar] [CrossRef]

- Jahid, M.A.; Rashid, M.H.U.; Hossain, S.Z.; Haryono, S.; Jatmiko, B. Impact of Corporate Governance Mechanisms on Corporate Social Responsibility Disclosure of Publicly-Listed Banks in Bangladesh. J. Asian Financ. Econ. Bus. 2020, 7, 61–71. [Google Scholar] [CrossRef]

- Flammer, C.; Kacperczyk, A. Corporate social responsibility as a defense against knowledge spillovers: Evidence from the inevitable disclosure doctrine. Strat. Manag. J. 2019, 40, 1243–1267. [Google Scholar] [CrossRef]

- Atan, R.; Alam, M.M.; Said, J.; Zamri, M. The impacts of environmental, social, and governance factors on firm performance: Panel study of Malaysian companies. Manag. Environ. Qual. Int. J. 2018, 29, 182–194. [Google Scholar] [CrossRef]

- Jahid, A.; Rashid, M.H.U.; Masud, A.K.; Yaya, R. A longitudinal study of corporate social responsibility expenditure and ownership structure of financial firms. Banks Bank Syst. 2022, 17, 24. [Google Scholar] [CrossRef]

- Masud, M.A.K.; Rahman, M.; Rashid, M.H.U. Anti-Corruption Disclosure, Corporate Social Expenditure and Political Corporate Social Responsibility: Empirical Evidence from Bangladesh. Sustainability 2022, 14, 6140. [Google Scholar] [CrossRef]

- Rashid, M.H.U.; Khanam, R.; Ullah, M.H. Corporate governance and IFSB standard-4: Evidence from Islamic banks in Bangladesh. Int. J. Islam. Middle East. Financ. Manag. 2022, 15, 1–17. [Google Scholar] [CrossRef]

- Freeman, R.E.; Dmytriyev, S. Corporate Social Responsibility and Stakeholder Theory: Learning From Each Other. Symph. Emerg. Issues Manag. 2017, 1, 7–15. [Google Scholar] [CrossRef] [Green Version]

- Zheng, Y.; Rashid, M.H.U.; Siddik, A.B.; Wei, W.; Hossain, S.Z. Corporate Social Responsibility Disclosure and Firm’s Productivity: Evidence from the Banking Industry in Bangladesh. Sustainability 2022, 14, 6237. [Google Scholar] [CrossRef]

- Rashid, M.H.U.; Hossain, S.Z. Does board independence moderate the effect of politician directors on CSR disclosure? Evidence from the publicly listed banks in Bangladesh. Soc. Responsib. J. 2022, 18, 935–950. [Google Scholar] [CrossRef]

- Rashid, M.H.U.; Zobair, S.A.M.; Chowdhury, M.A.I.; Islam, A. Corporate governance and banks’ productivity: Evidence from the banking industry in Bangladesh. Bus. Res. 2020, 13, 615–637. [Google Scholar] [CrossRef] [Green Version]

- Rezaee, Z. Business sustainability research: A theoretical and integrated perspective. J. Account. Lit. 2016, 36, 48–64. [Google Scholar] [CrossRef]

- Kramer, M.R.; Porter, M. Creating Shared Value; FSG: Boston, MA, USA, 2011; Volume 17. [Google Scholar]

- Uddin, M.N.; Rashid, M.H.U.; Rahman, M.T. Profitability, marketability, and CSR disclosure efficiency of the banking industry in Bangladesh. Heliyon 2022, 8, e11904. [Google Scholar] [CrossRef] [PubMed]

- Guthrie, J.; Parker, L.D. Corporate Social Reporting: A Rebuttal of Legitimacy Theory. Account. Bus. Res. 1989, 19, 343–352. [Google Scholar] [CrossRef]

- Masud, M.A.K.; Rashid, M.H.U.; Khan, T.; Bae, S.M.; Kim, J.D. Organizational strategy and corporate social responsibility: The mediating effect of triple bottom line. Int. J. Environ. Res. Public Health 2019, 16, 4559. [Google Scholar] [CrossRef] [Green Version]

- Michelon, G.; Pilonato, S.; Ricceri, F. CSR reporting practices and the quality of disclosure: An empirical analysis. Crit. Perspect. Account. 2015, 33, 59–78. [Google Scholar] [CrossRef] [Green Version]

- Elkington, J. Partnerships from cannibals with forks: The triple bottom line of 21st-century business. Environ. Qual. Manag. 1998, 8, 37–51. [Google Scholar] [CrossRef]

- Kamble, S.S.; Gunasekaran, A.; Gawankar, S.A. Achieving sustainable performance in a data-driven agriculture supply chain: A review for research and applications. Int. J. Prod. Econ. 2020, 219, 179–194. [Google Scholar] [CrossRef]

- Helleno, A.L.; de Moraes, A.J.I.; Simon, A.T. Integrating sustainability indicators and Lean Manufacturing to assess manufacturing processes: Application case studies in Brazilian industry. J. Clean. Prod. 2017, 153, 405–416. [Google Scholar] [CrossRef]

- Moktadir, M.A.; Rahman, T.; Rahman, M.H.; Ali, S.M.; Paul, S.K. Drivers to sustainable manufacturing practices and circular economy: A perspective of leather industries in Bangladesh. J. Clean. Prod. 2018, 174, 1366–1380. [Google Scholar] [CrossRef]

- Rashid, M.H.U.; Uddin, M.M. Green financing for sustainability: Analysing the trends with challenges and prospects in the context of Bangladesh. Int. J. Green Econ. 2018, 12, 192–208. [Google Scholar] [CrossRef]

- Bae, S.M.; Masud, A.K.; Rashid, M.H.U.; Kim, J.D. Determinants of climate financing and the moderating effect of politics: Evidence from Bangladesh. Sustain. Account. Manag. Policy J. 2022, 13, 247–272. [Google Scholar] [CrossRef]

- Firoj, M.; Sultana, N.; Khanom, S.; Rashid, M.H.U.; Sultana, A. Pollution haven hypothesis and the environmental Kuznets curve of Bangladesh: An empirical investigation. Asia-Pac. J. Reg. Sci. 2022, 7, 197–227. [Google Scholar] [CrossRef]

- Mustafa, S.; Zhang, W.; Sohail, M.T.; Rana, S.; Long, Y. A moderated mediation model to predict the adoption intention of renewable wind energy in developing countries. PLoS ONE 2023, 18, e0281963. [Google Scholar] [CrossRef]

- Zhu, D. Research from global Sustainable Development Goals (SDGs) to sustainability science based on the object-subject-process framework. Chin. J. Popul. Resour. Environ. 2017, 15, 8–20. [Google Scholar] [CrossRef]

- Mousa, S.K.; Othman, M. The impact of green human resource management practices on sustainable performance in healthcare organisations: A conceptual framework. J. Clean. Prod. 2020, 243, 118595. [Google Scholar] [CrossRef]

- Abdul-Rashid, S.H.; Sakundarini, N.; Ghazilla, R.A.R.; Thurasamy, R. The impact of sustainable manufacturing practices on sustainability performance: Empirical evidence from Malaysia. Int. J. Oper. Prod. Manag. 2017, 37, 182–204. [Google Scholar] [CrossRef]

- Ali, M.H.; Zailani, S.; Iranmanesh, M.; Foroughi, B. Impacts of Environmental Factors on Waste, Energy, and Resource Management and Sustainable Performance. Sustainability 2019, 11, 2443. [Google Scholar] [CrossRef] [Green Version]

- Ahmad, A.; Khan, M.A.; Abdullah, A.A.M.; Rashid, M.H.U. Environmental disclosures: A study on some selected pharmaceutical and chemical companies in Bangladesh. IIUC Bus. Rev. 2017, 6, 9–24. [Google Scholar]

- Ong, T.S.; Lee, A.S.; Teh, B.H.; Magsi, H.B. Environmental Innovation, Environmental Performance and Financial Performance: Evidence from Malaysian Environmental Proactive Firms. Sustainability 2019, 11, 3494. [Google Scholar] [CrossRef] [Green Version]

- Crossan, M.M.; Apaydin, M. A Multi-Dimensional Framework of Organizational Innovation: A Systematic Review of the Literature. J. Manag. Stud. 2010, 47, 1154–1191. [Google Scholar] [CrossRef]

- Cohen, W.M.; Levinthal, D.A. Absorptive capacity: A new perspective on learning and innovation. Adm. Sci. Q. 1990, 35, 128–152. [Google Scholar] [CrossRef]

- Delmas, M.A.; Burbano, V.C. The drivers of greenwashing. Calif. Manag. Rev. 2011, 54, 64–87. [Google Scholar] [CrossRef] [Green Version]

- Wagner, M. Innovation and competitive advantages from the integration of strategic aspects with social and environmental management in European firms. Bus. Strat. Environ. 2009, 18, 291–306. [Google Scholar] [CrossRef]

- Chiou, T.-Y.; Chan, H.K.; Lettice, F.; Chung, S.H. The influence of greening the suppliers and green innovation on environmental performance and competitive advantage in Taiwan. Transp. Res. Part E Logist. Transp. Rev. 2011, 47, 822–836. [Google Scholar] [CrossRef]

- Sezen, B.; Çankaya, S.Y. Effects of Green Manufacturing and Eco-innovation on Sustainability Performance. Procedia Soc. Behav. Sci. 2013, 99, 154–163. [Google Scholar] [CrossRef] [Green Version]

- Taddese, G.; Durieux, S.; Duc, E. Sustainability performance indicators for additive manufacturing: A literature review based on product life cycle studies. Int. J. Adv. Manuf. Technol. 2020, 107, 3109–3134. [Google Scholar] [CrossRef]

- Chaim, O.; Muschard, B.; Cazarini, E.; Rozenfeld, H. Insertion of sustainability performance indicators in an industry 4.0 virtual learning environment. Procedia Manuf. 2018, 21, 446–453. [Google Scholar] [CrossRef]

- Avery, G. Leadership for Sustainable Futures: Achieving Success in a Competitive World; Edward Elgar Publishing: Cheltenham, UK, 2005. [Google Scholar]

- Ketprapakorn, N.; Kantabutra, S. Sustainable Social Enterprise Model: Relationships and Consequences. Sustainability 2019, 11, 3772. [Google Scholar] [CrossRef] [Green Version]

- Chams, N.; García-Blandón, J. On the importance of sustainable human resource management for the adoption of sustainable development goals. Resour. Conserv. Recycl. 2019, 141, 109–122. [Google Scholar] [CrossRef]

- Kim, J. Social dimension of sustainability: From community to social capital. J. Glob. Sch. Mark. Sci. 2018, 28, 175–181. [Google Scholar] [CrossRef]

- Duque-Grisales, E.; Aguilera-Caracuel, J. Environmental, Social and Governance (ESG) Scores and Financial Performance of Multilatinas: Moderating Effects of Geographic International Diversification and Financial Slack. J. Bus. Ethic 2021, 168, 315–334. [Google Scholar] [CrossRef]

- Choi, J.; Wang, H. Stakeholder relations and the persistence of corporate financial performance. Strat. Manag. J. 2009, 30, 895–907. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D. Corporate social responsibility and financial performance: Correlation or misspecification? Strateg. Manag. J. 2000, 21, 603–609. [Google Scholar] [CrossRef]

- Mahlouji, H.; Anaraki, N.K. Corporate social responsibility towards social responsible innovation: A dynamic capability approach. Int. Rev. Bus. Res. Pap. 2009, 5, 185–194. [Google Scholar]

- Broadstock, D.C.; Matousek, R.; Meyer, M.; Tzeremes, N.G. Does corporate social responsibility impact firms’ innovation capacity? The indirect link between environmental & social governance implementation and innovation performance. J. Bus. Res. 2020, 119, 99–110. [Google Scholar] [CrossRef]

- Zhang, Q.; Loh, L.; Wu, W. How do environmental, social and governance initiatives affect innovative performance for corporate sustainability? Sustainability 2020, 12, 3380. [Google Scholar] [CrossRef] [Green Version]

- Rodrigue, M.; Magnan, M.; Cho, C.H. Is Environmental Governance Substantive or Symbolic? An Empirical Investigation. J. Bus. Ethic 2013, 114, 107–129. [Google Scholar] [CrossRef]

- Ricart, J.E.; Rodríguez, M.Á.; Sanchez, P. Sustainability in the boardroom: An empirical examination of Dow Jones Sustainability World Index leaders. Corp. Gov. Int. J. Bus. Soc. 2005, 5, 24–41. [Google Scholar] [CrossRef] [Green Version]

- Liao, L.; Luo, L.; Tang, Q. Gender diversity, board independence, environmental committee and greenhouse gas disclosure. Br. Account. Rev. 2015, 47, 409–424. [Google Scholar] [CrossRef]

- Rashid, M.H.U.; Hamid, M.A. Measurement of CSR Performance in Manufacturing Industries: A SEM Approach. Int. J. Soc. Ecol. Sustain. Dev. 2022, 13, 1–18. [Google Scholar] [CrossRef]

- Arora, P.; Dharwadkar, R. Corporate Governance and Corporate Social Responsibility (CSR): The Moderating Roles of Attainment Discrepancy and Organization Slack. Corp. Gov. Int. Rev. 2011, 19, 136–152. [Google Scholar] [CrossRef]

- Bravo, F.; Reguera-Alvarado, N. Sustainable development disclosure: Environmental, social, and governance reporting and gender diversity in the audit committee. Bus. Strat. Environ. 2019, 28, 418–429. [Google Scholar] [CrossRef]

- Rao, K.; Tilt, C. Board Composition and Corporate Social Responsibility: The Role of Diversity, Gender, Strategy and Decision Making. J. Bus. Ethic 2016, 138, 327–347. [Google Scholar] [CrossRef]

- Martín, C.J.G.; Herrero, B. Do board characteristics affect environmental performance? A study of EU firms. Corp. Soc. Responsib. Environ. Manag. 2019, 27, 74–94. [Google Scholar] [CrossRef]

- E-Vahdati, S.; Zulkifli, N.; Zakaria, Z. Corporate governance integration with sustainability: A systematic literature review. Corp. Gov. Int. J. Bus. Soc. 2018, 19, 255–269. [Google Scholar] [CrossRef]

- Gutiérrez-Martínez, I.; Duhamel, F. Translating sustainability into competitive advantage: The case of Mexico’s hospitality industry. Corp. Gov. Int. J. Bus. Soc. 2019, 19, 1324–1343. [Google Scholar] [CrossRef]

- Wang, Y.; Abbasi, K.; Babajide, B.; Yekini, K.C. Corporate governance mechanisms and firm performance: Evidence from the emerging market following the revised CG code. Corp. Gov. Int. J. Bus. Soc. 2019, 20, 158–174. [Google Scholar] [CrossRef]

- AlHares, A. Corporate governance mechanisms and R&D intensity in OECD courtiers. Corp. Gov. Int. J. Bus. Soc. 2020, 20, 863–885. [Google Scholar]

- Lu, J.; Wang, W. Managerial conservatism, board independence and corporate innovation. J. Corp. Financ. 2018, 48, 1–16. [Google Scholar] [CrossRef]

- Omri, W.; Becuwe, A.; Mathe, J.C. Ownership structure and innovative behavior: Testing the mediatory role of board composition. J. Account. Emerg. Econ. 2014, 4, 220–239. [Google Scholar] [CrossRef]

- Nidumolu, R.; Prahalad, C.K.; Rangaswami, M.R. Why sustainability is now the key driver of innovation. Harv. Bus. Rev. 2009, 87, 56–64. [Google Scholar]

- Knowles, C.D. Measuring Innovativeness in the North American Softwood Sawmilling Industry; Oregon State University: Corvallis, OR, USA, 2007. [Google Scholar]

- Varis, M.; Littunen, H. Types of innovation, sources of information and performance in entrepreneurial SMEs. Eur. J. Innov. Manag. 2010, 13, 128–154. [Google Scholar] [CrossRef] [Green Version]

- Chen, J.; Liu, Z.-C.; Wu, N.-Q. Relationships between organizational learning, innovation and performance: An empirical examination. In Proceedings of the 2009 International Conference on Information Management, Innovation Management and Industrial Engineering, Xi’an, China, 26–27 December 2009; IEEE: Piscataway, NJ, USA, 2009. [Google Scholar]

- Bakhtina, V.A. Innovation and its potential in the context of the ecological component of sustainable development. Sustain. Account. Manag. Policy J. 2011, 2, 248–262. [Google Scholar] [CrossRef]

- Mustafa, S.; Hao, T.; Qiao, Y.; Shah, S.K.; Sun, R. How a Successful Implementation and Sustainable Growth of e-Commerce can be Achieved in Developing Countries: A Pathway Towards Green Economy. Front. Environ. Sci. 2022, 10, 1–17. [Google Scholar] [CrossRef]

- Ivanaj, S.; Ivanaj, V.; McIntyre, J.; Da Costa, N.G.; Lozano, R. Multinational Enterprises’ strategic dynamics and climate change: Drivers, barriers and impacts of necessary organisational change. J. Clean. Prod. 2015, 30, 1e4. [Google Scholar] [CrossRef]

- Faulkner, W.; Badurdeen, F. Sustainable Value Stream Mapping (Sus-VSM): Methodology to visualize and assess manufacturing sustainability performance. J. Clean. Prod. 2014, 85, 8–18. [Google Scholar] [CrossRef]

- Commerce, T. The US Department of The International Trade Administration and the US Department of Commerce’s definition for Sustainable Manufacturing; The US Department of Commerce: Washington, DC, USA, 2010.

- Mustafa, S.; Hao, T.; Jamil, K.; Qiao, Y.; Nawaz, M. Role of Eco-Friendly Products in the Revival of Developing Countries’ Economies and Achieving a Sustainable Green Economy. Front. Environ. Sci. 2022, 10, 1082. [Google Scholar] [CrossRef]

- Kanashiro, P.; Rivera, J. Do Chief Sustainability Officers Make Companies Greener? The Moderating Role of Regulatory Pressures. J. Bus. Ethic 2019, 155, 687–701. [Google Scholar] [CrossRef]

- Wong, W.P.; Tseng, M.-L.; Tan, K.H. A business process management capabilities perspective on organisation performance. Total Qual. Manag. Bus. Excel. 2014, 25, 602–617. [Google Scholar] [CrossRef]

- Huang, X.-X.; Hu, Z.-P.; Liu, C.-S.; Yu, D.-J.; Yu, L.-F. The relationships between regulatory and customer pressure, green organizational responses, and green innovation performance. J. Clean. Prod. 2016, 112, 3423–3433. [Google Scholar] [CrossRef]

- Dicuonzo, G.; Donofrio, F.; Ranaldo, S.; Dell’Atti, V. The effect of innovation on environmental, social and governance (ESG) practices. Meditari Account. Res. 2022, 30, 1191–1209. [Google Scholar] [CrossRef]

- Carayannis, E.G.; Sindakis, S.; Walter, C. Business Model Innovation as Lever of Organizational Sustainability. J. Technol. Transf. 2015, 40, 85–104. [Google Scholar] [CrossRef]

- Ahmad, M.; Wu, Y. Combined role of green productivity growth, economic globalization, and eco-innovation in achieving ecological sustainability for OECD economies. J. Environ. Manag. 2022, 302, 113980. [Google Scholar] [CrossRef] [PubMed]

- Du, K.; Li, J. Towards a green world: How do green technology innovations affect total-factor carbon productivity. Energy Policy 2019, 131, 240–250. [Google Scholar] [CrossRef]

- Xu, X.; Imran, M.; Ayaz, M.; Lohana, S. The Mediating Role of Green Technology Innovation with Corporate Social Responsibility, Firm Financial, and Environmental Performance: The Case of Chinese Manufacturing Industries. Sustainability 2022, 14, 16951. [Google Scholar] [CrossRef]

- Ge, G.; Xiao, X.; Li, Z.; Dai, Q. Does ESG Performance Promote High-Quality Development of Enterprises in China? The Mediating Role of Innovation Input. Sustainability 2022, 14, 3843. [Google Scholar] [CrossRef]

- Yoo, C.; Yeon, J.; Lee, S. Beyond “good company”: The mediating role of innovation in the corporate social responsibility and corporate firm performance relationship. Int. J. Contemp. Hosp. Manag. 2022, 34, 3677–3696. [Google Scholar] [CrossRef]

- Shih, T.-Y. Exploring the Effects of Prospective Corporate Social Responsibility on Firm Performance: The Mediating Role of Innovation. In Technology Analysis & Strategic Management; Taylor & Francis: Abingdon, UK, 2022; pp. 1–13. [Google Scholar]

- Javed, M.; Ali, H.Y.; Asrar-ul-Haq, M.; Ali, M.; Kirmani, S.A.A. Responsible leadership and triple-bottom-line performance—Do corporate reputation and innovation mediate this relationship? Leadersh. Organ. Dev. J. 2020, 41, 501–517. [Google Scholar]

- Anderson, J.C.; Gerbing, D.W. The effect of sampling error on convergence, improper solutions, and goodness-of-fit indices for maximum likelihood confirmatory factor analysis. Psychometrika 1984, 49, 155–173. [Google Scholar] [CrossRef]

- Tan, K.; Siddik, A.B.; Sobhani, F.A.; Hamayun, M.; Masukujjaman, M. Do Environmental Strategy and Awareness Improve Firms’ Environmental and Financial Performance? The Role of Competitive Advantage. Sustainability 2022, 14, 10600. [Google Scholar] [CrossRef]

- Van Riel, A.C.; Henseler, J.; Kemény, I.; Sasovova, Z. Estimating hierarchical constructs using consistent partial least squares: The case of second-order composites of common factors. Ind. Manag. Data Syst. 2017, 117, 459–477. [Google Scholar] [CrossRef] [Green Version]

- Hair, J.F., Jr.; Sarstedt, M.; Ringle, C.M.; Gudergan, S.P. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM); Sage Publications: New York, NY, USA, 2021. [Google Scholar]

- Ringle, C.M.; Wende, S.; Becker, J.-M. SmartPLS 3; SmartPLS GmbH: Boenningstedt, Germany, 2015. [Google Scholar]

- Hair, J.F.; Anderson, R.E.; Tatham, R.L.; Black, W.C. Multivariate Data Analysis with Readings, 1995; Petroleum Publishing: Tulsa, OK, USA, 1984. [Google Scholar]

- Hair, J.; Hollingsworth, C.L.; Randolph, A.B.; Chong, A.Y.L. An updated and expanded assessment of PLS-SEM in information systems research. Ind. Manag. Data Syst. 2017, 117, 442–458. [Google Scholar] [CrossRef]

- Hair, J.F., Jr.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis: A Global Perspective, 7th ed.; Pearson Education: Upper Saddle River, NJ, USA, 2010. [Google Scholar]

- Cohen, J. Statistical Power Analysis for the Behavioural Sciences; Baskı: Hillsdale, NJ, USA, 1988. [Google Scholar]

- Steiger, J.H. Understanding the limitations of global fit assessment in structural equation modeling. Pers. Individ. Differ. 2007, 42, 893–898. [Google Scholar] [CrossRef]

- Julienti, L.; Bakar, A.; Ahmad, H. Assessing the relationship between firm resources and product innovation performance: A resource-based view. Bus. Process Manag. J. 2010, 16, 420–435. [Google Scholar] [CrossRef]

- Aslam, S.; Ahmad, M.; Amin, S.; Usman, M.; Arif, S. The impact of corporate governance and intellectual capital on firm’s performance and corporate social responsibility disclosure. Pak. J. Commer. Soc. Sci. 2018, 12, 283–308. [Google Scholar]

| Items | Categories | Frequency | Percent |

|---|---|---|---|

| Types of companies | Steel | 65 | 26.0 |

| Cement | 64 | 25.6 | |

| Glass | 70 | 28.0 | |

| Textile | 51 | 20.4 | |

| Number of employees | Below 100 | 57 | 22.8 |

| More than 100 | 189 | 77.2 | |

| Employee position | Top level | 81 | 32.4 |

| Middle and lower level | 193 | 67.6 | |

| Firm age | Less than 20 years | 115 | 54.0 |

| More than 20 years | 135 | 46.0 | |

| Total | 250 | 100 |

| Variables | Description |

|---|---|

| Sustainability Performance | The concept of “Triple Bottom Line” focuses on the alignment of social and environmental goals with economic growth to meet the present needs of society and corporations without comprising future needs [39,41,42,43]. |

| Innovation Performance | Innovation performance could be described as the employment of green technologies in developing business processes and products to facilitate environmental protection and get a sustainable competitive edge [23,54,60]. |

| Environmental Performance | Environmental performance could be referred to as the consideration of environmental protection strategies, mission and structures in business practices and decision-making processes [17,55]. |

| Societal Performance | Social performance can be defined as the impacts of discretionary business activities of a corporation to meet the demand and expectations of society and external stakeholders beyond the interest of shareholders and the firm [61,66,67]. |

| Corporate Governance Performance | Corporate governance performances include the use of risk control tools, enhancing transparency and accountability, improvement rules and regulations, presence of a diversified board, compliance with social and environmental standards and use of a sustainability committee [74,78,81]. |

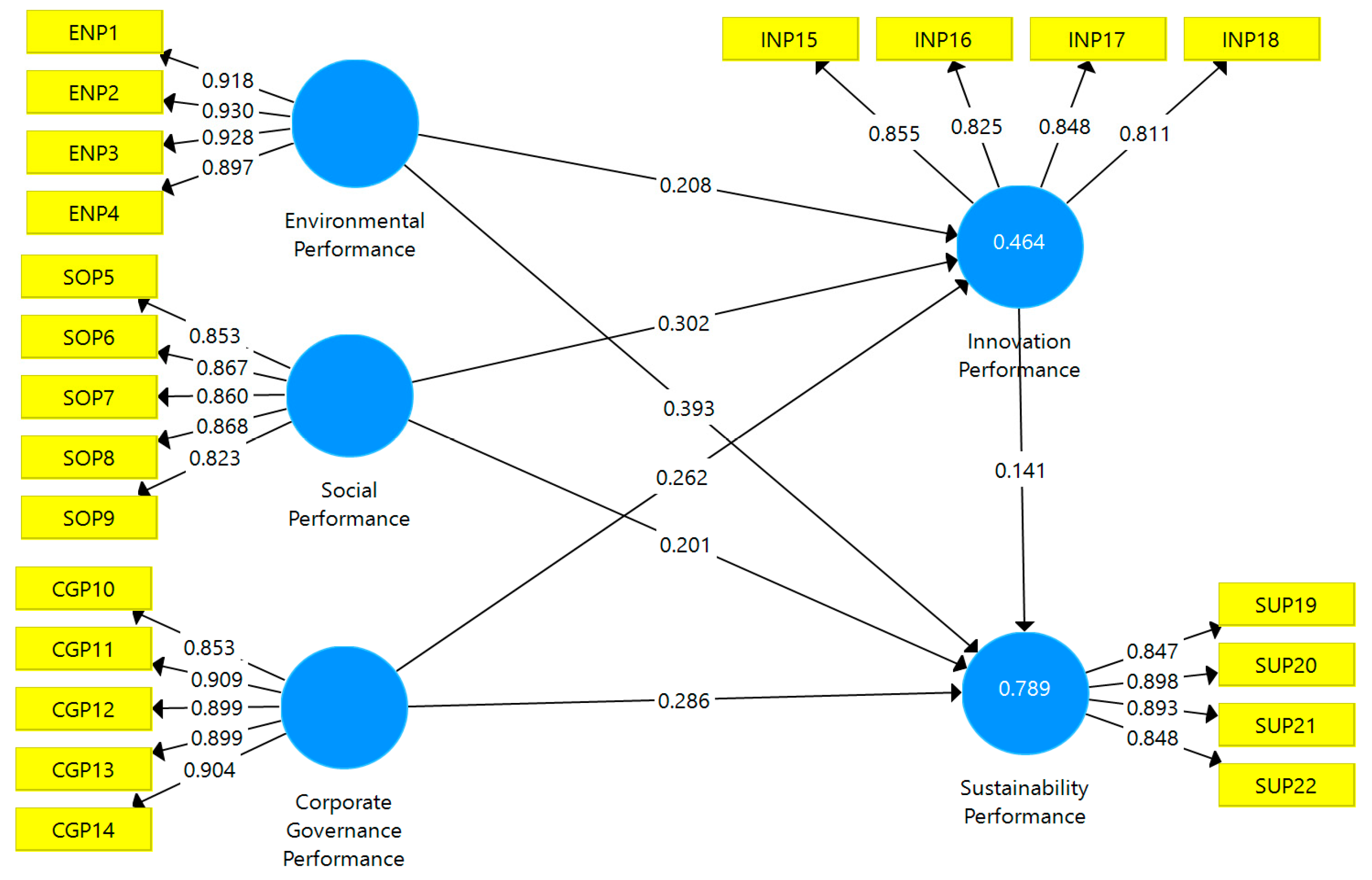

| Variables | Items | Mean | Standard Deviation | Kurtosis | Skewness | Factor Loadings | VIF |

|---|---|---|---|---|---|---|---|

| Corporate Governance Performance (CGP) | CGP10 | 5.812 | 0.67 | −0.799 | 0.24 | 0.853 | 2.784 |

| CGP11 | 5.836 | 0.646 | −0.656 | 0.17 | 0.909 | 3.761 | |

| CGP12 | 5.836 | 0.627 | −0.541 | 0.138 | 0.899 | 3.581 | |

| CGP13 | 5.84 | 0.637 | −0.603 | 0.152 | 0.899 | 3.825 | |

| CGP14 | 5.828 | 0.631 | −0.575 | 0.155 | 0.904 | 4.128 | |

| Environmental Performance (EP) | ENP1 | 5.88 | 0.64 | −0.367 | 0.02 | 0.918 | 3.696 |

| ENP2 | 5.852 | 0.656 | −0.334 | −0.006 | 0.93 | 4.233 | |

| ENP3 | 5.876 | 0.617 | −0.174 | −0.019 | 0.928 | 4.109 | |

| ENP4 | 5.852 | 0.656 | −0.521 | 0.079 | 0.897 | 3.067 | |

| Innovation Performance (IP) | INP15 | 5.924 | 0.592 | −0.166 | 0.021 | 0.855 | 2.087 |

| INP16 | 5.88 | 0.595 | −0.249 | 0.043 | 0.825 | 1.931 | |

| INP17 | 5.876 | 0.636 | −0.565 | 0.111 | 0.848 | 2.156 | |

| INP18 | 5.916 | 0.584 | −0.102 | 0.013 | 0.811 | 1.87 | |

| Social Performance (SP) | SOP5 | 5.908 | 0.61 | −0.337 | 0.05 | 0.853 | 2.306 |

| SOP6 | 5.916 | 0.604 | −0.283 | 0.039 | 0.867 | 2.658 | |

| SOP7 | 5.928 | 0.609 | −0.314 | 0.038 | 0.86 | 2.664 | |

| SOP8 | 5.896 | 0.637 | −0.554 | 0.092 | 0.868 | 2.761 | |

| SOP9 | 5.912 | 0.633 | −0.516 | 0.073 | 0.823 | 2.161 | |

| Sustainability Performance (SUP) | SUP19 | 5.9 | 0.64 | −0.579 | 0.092 | 0.847 | 2.159 |

| SUP20 | 5.864 | 0.649 | −0.66 | 0.141 | 0.898 | 2.95 | |

| SUP21 | 5.9 | 0.647 | −0.623 | 0.098 | 0.893 | 2.781 | |

| SUP22 | 5.892 | 0.645 | −0.618 | 0.105 | 0.848 | 2.302 |

| Variables | Cronbach’s Alpha | rho_A | Composite Reliability | AVE | R2 |

|---|---|---|---|---|---|

| Corporate Governance Performance | 0.937 | 0.937 | 0.952 | 0.798 | - |

| Environmental Performance | 0.938 | 0.938 | 0.956 | 0.843 | - |

| Innovation Performance | 0.855 | 0.86 | 0.902 | 0.697 | 0.789 |

| Social Performance | 0.907 | 0.91 | 0.931 | 0.73 | - |

| Sustainability Performance | 0.895 | 0.896 | 0.927 | 0.76 | 0.464 |

| Fornell–Larcker Approach | |||||

| Variables | CGP | EP | IP | SOP | SUP |

| Corporate Governance Performance | 0.893 | ||||

| Environmental Performance | 0.769 | 0.918 | |||

| Innovation Performance | 0.616 | 0.592 | 0.835 | ||

| Social Performance | 0.642 | 0.606 | 0.596 | 0.854 | |

| Sustainability Performance | 0.804 | 0.819 | 0.67 | 0.707 | 0.872 |

| HTMT Approach | |||||

| Corporate Governance Performance | |||||

| Environmental Performance | 0.82 | ||||

| Innovation Performance | 0.684 | 0.658 | |||

| Social Performance | 0.691 | 0.654 | 0.672 | ||

| Sustainability Performance | 0.877 | 0.893 | 0.762 | 0.779 | |

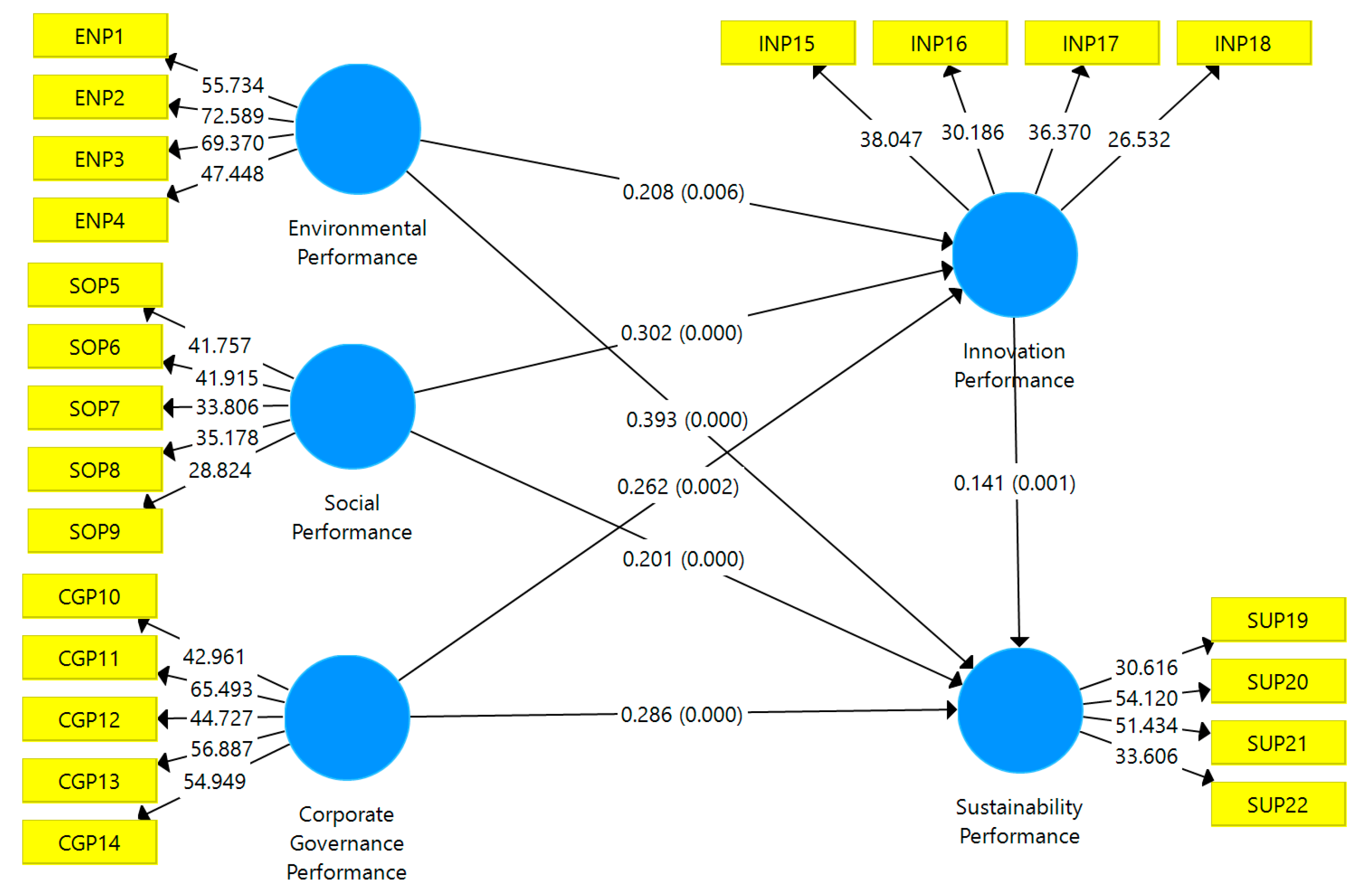

| Hypothesis | Paths | Beta Value | T Statistics | p Values | Remarks |

|---|---|---|---|---|---|

| H1 | EP −> SUP | 0.393 | 6.097 | 0.000 *** | Supported |

| H2 | EP −> IP | 0.208 | 2.704 | 0.007 *** | Supported |

| H3 | SOP −> SUP | 0.201 | 4.228 | 0.000 *** | Supported |

| H4 | SOP −> IP | 0.302 | 4.265 | 0.000 *** | Supported |

| H5 | CGP −> SUP | 0.286 | 4.966 | 0.000 *** | Supported |

| H6 | CGP −> IP | 0.262 | 3.169 | 0.002 *** | Supported |

| H7 | IP −> SUP | 0.141 | 3.157 | 0.002 *** | Supported |

| Mediation analysis | |||||

| H8 | EP −> IP −> SUP | 0.029 | 2.053 | 0.040 ** | Full mediation |

| H9 | SOP −> IP −> SUP | 0.043 | 2.537 | 0.011 ** | Full mediation |

| H10 | CGP −> IP −> SUP | 0.037 | 2.236 | 0.025 ** | Full mediation |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhou, S.; Rashid, M.H.U.; Mohd. Zobair, S.A.; Sobhani, F.A.; Siddik, A.B. Does ESG Impact Firms’ Sustainability Performance? The Mediating Effect of Innovation Performance. Sustainability 2023, 15, 5586. https://doi.org/10.3390/su15065586

Zhou S, Rashid MHU, Mohd. Zobair SA, Sobhani FA, Siddik AB. Does ESG Impact Firms’ Sustainability Performance? The Mediating Effect of Innovation Performance. Sustainability. 2023; 15(6):5586. https://doi.org/10.3390/su15065586

Chicago/Turabian StyleZhou, Shukang, Md. Harun Ur Rashid, Shah Asadullah Mohd. Zobair, Farid Ahammad Sobhani, and Abu Bakkar Siddik. 2023. "Does ESG Impact Firms’ Sustainability Performance? The Mediating Effect of Innovation Performance" Sustainability 15, no. 6: 5586. https://doi.org/10.3390/su15065586