1. Introduction

Since the rapid development of industrialization, socio-economic growth has long been accompanied by large emissions of various carbon compounds, gradually causing climate concerns of the greenhouse effect worldwide. According to the statistics published by the UN’s Intergovernmental Panel on Climate Change (IPCC), during the 2010 to 2019 period, average annual global greenhouse gas emissions were at the highest level in human history, with a total emission of around 59 billion tons in 2019 [

1]. While the average annual growth rate of the emission amount has declined from 2.1% in the 2000s to 1.3% in the 2010s, it is still essential for governments to work closely and take measures to mitigate the negative impacts of greenhouse gases [

1]. Among the identified greenhouse gases, carbon dioxide is by all means the most widespread and the most influential [

2], making governments and international organizations put more efforts in creating available carbon-reducing technologies, as well as regulatory policies. For instance, starting from 2005, the European Union launched its Emissions Trading Scheme (EU-ETS) to use market mechanisms in chasing the EU’s carbon-reducing targets. For now, the EU-ETS has become the world largest carbon emission trading market, providing practical guidance for countries using similar market-incentive methods for carbon emission regulations. Moreover, the United Nations Climate Change Conference in Glasgow (COP26) has made progress on setting rules for building the global carbon trading market, making the effectiveness of the carbon trading mechanism in helping achieve the carbon-reducing goal a highly discussed topic, in both the academic and practical areas.

Following the practical experience of EU-ETS, the Chinese government began to prepare the Chinese carbon emission trading pilot in 2011, and successively launched its pilot trading system from 2013 in eight provinces or cities. This includes Beijing, Shanghai, Shenzhen, Guangdong and Tianjin in 2013, Hubei and Chongqing in 2014, and finally Fujian in 2016 [

3]. After the several-year pilot operating and the nationwide system designing in 2021, the national carbon emission trading market was officially launched in cooperation with China’s “carbon peaking” and “carbon neutrality” targets set in 2020. In fact, to the best of our knowledge, the carbon emission trading system is currently the only market-incentive carbon-reducing practice in China, and thus attracts academic discussions on its practical effectiveness. Specifically, from the micro perspective at the firm level, existing literature generally concludes that Chinese companies under such market-incentive regulation will significantly reduce their carbon emissions [

4,

5], promote their own green innovation activities [

6,

7], and experience increased corporate total productivities in the long term [

8,

9]. On the other hand, from the macro perspective at the regional level, studies present mixed results by stating that the leakage effect of carbon emitting and the spillover effect of carbon reducing may simultaneously exist after the implementation of the Chinese carbon emission trading pilot [

10,

11]. With the fact that one public policy can have positive or negative impacts on certain entities and that a favorable outcome to one social entity might be unfavorable to another, examining policy impacts from different perspectives brings insights on comprehensively understating how a certain policy affects socio-economic development. While commonly using Chinese A-share listed companies as the research sample, current studies seem to leave how the capital market evaluates the influence of the Chinese pilot on corporate environmental performance an undiscussed topic. Such issue remains vital both because environment protection is a crucial factor of socio-economic sustainable development and because evaluations from capital market participants generally determines the survival of the listed companies, especially in the current period, under China’s carbon peaking and carbon neutrality goals, as well as under the comprehensive reform of the registration-based IPO system in the Chinese capital market. By focusing on the connection between a market-incentive environmental regulation and market-ranked corporate environmental performance, we provide additional evidence in this article to extend the current research scope in the empirical field of environmental accounting.

Using archival data of the Chinese A-share listed companies from 2011 to 2019, we empirically examine whether and how the Chinese carbon emission trading pilot affects corporate environmental performance, ranked by a professional market rating agency, the Bloomberg database. The major findings demonstrate that the market-ranked environmental performance of the companies that are selected in the pilot experience significant improvements after the pilot implementation, suggesting that such environmental regulation enhances corporate sustainable investment values in the capital market. Second, compared with the hypothesized increasing green investment channel, the lowering production level channel is statistically salient in explaining how the Chinese listed companies improve their environmental performance during the pilot period, revealing the listed companies’ preferences of short-term carbon-reducing behaviors rather than the long-term sustainable methods. Finally, moderating effect analyses further prove the synergistic effects of corporate environmental pressure and internal control quality. That is, the positive capital market value-adding effect of the pilot can be strengthened in companies that are under greater pressures of the external environmental law enforcement or that operate with better internal control systems.

This study contributes to the current literature in the following aspects. First, when discussing the effectiveness of the Chinese carbon emission trading pilot on micro socio-economic areas, previous studies mainly focus on how the Chinese listed companies react to such environmental regulation [

7,

12], while often ignoring evaluations from professional capital market participants, such as indexing or rating agencies. Given the fact that market institutions are essential information intermediaries among various stakeholders in the capital market, the way in which they assess corporate environmental performance before and after the pilot implementation reflects the views of capital market investors, and thus contains direct market-incentive information, which potentially redirect market fund flows. From the perspective of capital market investors, we supplement the current studies regarding whether and how the capital market participants respond to the new environmental regulation implementations, and thus provide additional empirical evidence for deeply and comprehensively understanding the socio-economic impacts of a market-incentive environmental regulation in the Chinese emerging market. Second, concerning the existing debate about how the listed companies trade off among multiple methods in dealing with carbon emission quota limitations under the pilot [

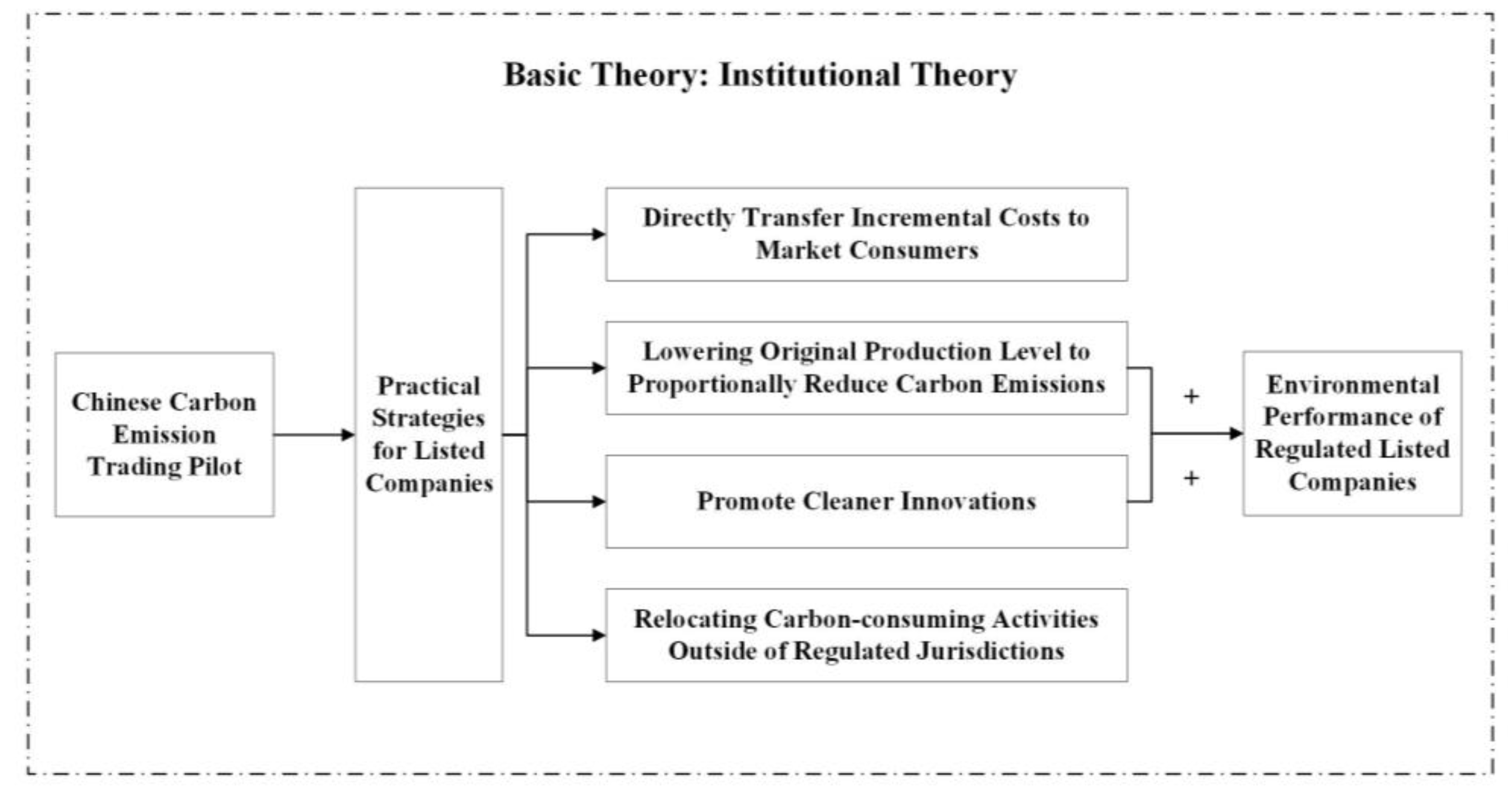

13,

14,

15], we present new evidence to support the view that companies will generally lower their production levels in response to emission quota limitations, which then helps them achieve better environmental performance, while making few environment protection investments under the pilot regulation. Our findings thus shed light on internal connections between the implementation of the Carbon emission trading pilot and the promotion of the Chinese listed companies’ market-ranked environmental performance. Third, by examining the moderating effects of corporate environmental pressures and internal control quality, this study provides additional evidence on regulatory synergies brought by both the external law enforcement and corporate internal governance, emphasizing the necessity for developing systemic environmental regulatory mechanisms among policy makers, law enforcers, and corporate governors.

The remaining parts of this article are:

Section 2, which provides the literature review and hypothesis development; our research design is introduced in

Section 3;

Section 4 shows the empirical results, including baseline regression, robustness tests, influential mechanism analysis, and moderating effect analysis; the main findings are then further discussed in

Section 5; and

Section 6 concludes the whole article.

5. Discussion

We present empirical evidence on whether and how the Chinese carbon emission trading pilot affects the listed companies’ market-ranked environmental performance, and thus extend related research scope from the capital market evaluation perspective. Still, similar with exiting literature, e.g., [

4,

5,

6,

7,

8,

9], the ultimate goal of this study is to examine whether and how the carbon emission trading pilot causes influences on regulated companies within the Chinese capital market. Overall, we present additional favorable results on China’s first market-incentive carbon-reducing regulatory practices, stating that compared with the companies not required to participate in the pilot, regulated companies will lower their production level and therefore achieve higher environmental performance ranked by the rating institution in the capital market. For the companies not regulated by the pilot, their environmental performance shows no significant changes during our research period, as shown in

Figure 2. However, our main results do not deny the identified carbon leakage effect [

10], in that the regulated listed companies may not choose another listed company for potential carbon emission transferring, even though the company has not been regulated by the pilot. Instead, potential carbon emission outsourcing activities may be empirically found between the regulated companies and their affiliated enterprises, of which the data are not observable at the current stage.

One limitation of this article exists in exploring how capital market institutions actually use and evaluate corporate environmental performance data in their rating system. Although ordinary rating considerations and rating results are commonly available to the public, researchers would shed more light on the original processes of turning environmental regulatory policies to incremental value-adding information in the capital market if they were accessible to the actual rating practices in capital market institutions. We thus hope that further studies will provide complements to this limitation in the topic, by implementing field or case studies.

Besides proving the validity of our research topic, the regression results also suggest some potential directions for future research. For example, the regression coefficient of the variable CCET in Panel A of

Table 8 remains significant when examining the lowering production channel, implying that there may be other influential mechanisms that can explain the connection between the carbon emission trading pilot and the Chinese listed companies’ environmental performance. Alongside that, from the mediating effect analyses, it is worth noticing that when dealing with environmental regulations, the Chinese listed companies generally tend to be short-sighted in choosing not to invest in green innovation activities, but to simply lower their production levels instead. We speculate that such an unsustainable situation might be influenced by some immature rules in the carbon emission trading pilot, and we thus suggest for further studies to keep up with this potential direction in finding internal reasons and improvement measures. Moreover, future research may focus on potential connections between other institutional changes and companies’ environmental-related behaviors, or consider comparing carbon-emission-reducing practices among various capital markets as a feasible starting point.

6. Conclusions

Using data of the Chinese A-share listed companies from 2011 to 2019, we empirically examine the potential connections between the Chinese carbon emission trading pilot and companies’ environmental performance. The main results reveal that companies will improve their environmental performance after they are selected to participate in the pilot. Several robustness tests are also implemented to prove the validity of our conclusions. Second, influential mechanism analyses illustrate that the lowering production channel plays an essential role in explaining our identified connections, while the explanatory power of the increasing green investment channel is not salient. Third, the results of the moderating effect tests indicate that, along with the development of the carbon emission trading market, regulators can also put efforts on strengthening environmental regulation enforcement and improving corporate internal governance to maximize favorable impacts of environmentally friendly policies.

Based on the main findings in this study, the implications for future environmental regulatory practices may include improving the listed companies’ environmental performance in the long-term, more environmental regulations either encouraging or requiring companies’ environmental protection activities that can be carefully designed and implemented in the future, as such market- or administrative-incentive regulations are likely to cause significant influences on the listed companies’ operating decisions. Second, it is noticeable that under environmental regulation that may bring an additional economic burden, the listed companies generally promote their environmental performance at the cost of directly lowering the production levels, instead of making long-term green investments. This phenomenon should be further improved by regulatory adjustments such as providing subsidies for companies to equip greener facilities and setting a transitional period for companies to better prepare for stricter environmental regulations, since sustainable development requires finding a balance point between companies’ economic benefit chasing and environmental protection activities. Third, ensuring environmental law enforcement and making companies build a better internal governance system are also essential for well-designed environmental policy to play a strengthened role. Thus, regulators in both legal institutions and the capital market are advised to further provide high-quality supportive mechanisms in promoting the effectiveness of well-designed environmental policies.

{kind=link}

{kind=link}