1. Motivation and Context for Increased Organizational Sustainability

To ‘go green’ and protect the natural environment has become popular among companies. Many seek to reduce their negative impacts on the natural environment [

1], offer sustainable products and services [

2], and issue sustainability reports that document the environmental impacts of their corporate actions [

3].

The reasons for such actions are diverse. Some companies see it as their obligation and a moral responsibility [

2]. Some are taking this change in societal priorities as a chance to further develop their business models [

4], adjust their companies’ strategic orientations [

5], or increase their operational and organizational efficiencies [

2].

Similarly, the means of achieving sustainability are also numerous. In the current ‘era of digital transformation’, an ever-growing number of companies realize that they need to become both more digitalized and more sustainable [

6], and they see the adoption of information technologies (IT) and information systems (IS) as a potential way to achieve digitally enabled sustainability [

7]. This realization has consequently led to a similarly increasing demand for technologies and solutions that bridge both needs [

8].

The associated technologies are often referred to as Green IT, which describe the usage and management of IT during their lifecycles, as well as Green IS, which coins governance practices, internal processes and operations that connect a company to its external market [

9]. These IT resources and IS capabilities [

10] not only offer utilitarian benefits [

11], but also a sustainability-based competitive advantage [

5]. They improve a company’s environmental sustainability “by informing stakeholders of the need to make changes to business as usual, by motivating them to take actions to achieve environmental objectives, and by assessing the impact of such actions on economic and environmental performance” ([

12], p. 12).

Although technological and sustainability benefits such as these seem promising, and various companies have developed successful pro-environmental strategies and actions [

13], “sustainability has failed to become a game-changing, mainstream business practice” ([

2], p. 941). Many companies only slowly or reluctantly adopt sustainability practices, and they seem to only act as the pressures from governments [

14], societal interest groups [

15], and ethically aware consumers [

16] continue to grow. For instance, accusations have been aimed at Unilever, Shell, and Nike that they only “use sustainability to build either brand image or act as an insulator in brand risk management” ([

2], p. 938). In the case of Shell—which is a leading global oil and gas company—the Dutch district court in The Hague saw it as imminent that Shell would breach its obligation to reduce its carbon dioxide emissions and ordered it to lower them by 45% by 2030 compared with their 2019 levels [

5]. Other companies have been directly confronted with greenwashing accusations, such as BP another oil and gas company, which frequently highlights “the company’s investments in renewable energy without mentioning their major efforts in petroleum exploration” ([

17], p. 4).

Academic insights into the genuine relevance of sustainability to companies and the reasons that they might avoid real sustainability changes are rare. Some researchers address this topic as a side note, such as Zimmermann [

18], who documented that—because companies are driven by multiple motives—they integrate corporate sustainability practices into their core business practices differently (e.g., from strict to non-existent). In other studies on energy- and material-saving technologies, researchers have found comparable results. They have found that manufacturing companies only rarely adopt these technologies [

19], and that, at the overarching country level, there are substantial differences in the statuses and further development of different countries around the globe [

20].

In addition, there is only limited research on why Green IT and Green IS are still not being widely diffused and implemented [

11]. There are some practitioner insights (e.g., [

21]) that view misaligned incentives, competing priorities, and a lack of expertise as the core issues of proper institutional Green IT usage. However, current academic research seems primarily focused on general aspects of Green IT/IS [

22], such as the understanding of Green IT and Green IS (e.g., [

9,

23]), or their roles in different areas or literature (e.g., [

24,

25]). Specific insights into the innovative process of their systematic adoption and the factors that affect it are few [

11]. Schmermbeck [

26], for instance, proposed a framework that captures the reasons, processes, and potential benefits of sustainable technology and Green IT/IS adoption. Although the author generated novel insights into a variety of environmental, societal, organizational, and individual factors, they remained conceptual.

Studies that present an overview of multiple companies from different countries and their sustainability initiatives—which might allow for a more detailed evaluation—are even more scarce. That of Alsdorf et al. [

27] is one of the few. These authors undertook a multi-national study assessing 1535 companies and found that—although more than 70% regarded sustainability as relevant—only about 24% also defined their performance indicators to measure and steer their strategic sustainability goals. This substantial discrepancy raises questions about the sincerity of the respective sustainability strategies being followed, and the reasons why so many companies are not adopting tangible means of sustainability.

We thus sought to provide a better understanding of the factors that negatively influence or prevent companies from meaningful pro-environmental engagement and/or hinder them from adopting and using sustainability-engaging technologies, such as Green IT/IS. We specifically asked:

RQ: Which aspects negatively influence a company’s sustainability engagement and its subsequent adoption and usage of sustainability technologies, such as Green IT and Green IS?

We consequently aim to enrich and deepen the understanding of this area, as well as provide rich descriptions of the background and context of why companies (not) adopt sustainability and sustainable technologies, such as Green IT/IS. We focus on (top) managerial perceptions, as their leadership is the key to leading and coordinating sustainability efforts [

28].

The current paper is a continuation of previous work that provides empirical insights into the corporate adoption and relevance of Green IT/IS in Germany, Austria, and Switzerland [

27], but also into the conceptual foundations, such as the process of Green IT/IS adoption, and the influential factors inside and outside of an organization [

26].

Because there was limited previous research to build our work on, we chose an exploratory approach because it allowed us to add the intended context data [

29]. As a starting point, we used qualitative data from an ongoing study on the adoption and usage of Green IT/IS. We extracted insights from the 21 interviews that we conducted, and we summarized them into specific statements that describe the constraints on: (i) the determinants of sustainable technology adoption; (ii) the determinants of sustainability as a societal phenomenon; (iii) more specific details on the adoption and usage of Green IT/IS. We used these statements as a basis for a follow-up round of interviews with four representatives of two companies from the initial study.

The results from this follow-up interview study seem beneficial for both research and practice. They provide details on why sustainability, as well as sustainable technologies, needs to be treated, evaluated, and managed differently than traditional innovations (e.g., [

26]). Furthermore, they also underline that corporate sustainability efforts indeed face certain hindrances, such as prejudices or hidden assumptions, that can be addressed, for instance, by extending and transparently addressing the evaluation criteria of impending traditional and sustainable innovations.

The remainder of the paper is structured as follows: In

Section 2, we provide a brief overview of the central concepts and terms of this research, and how we understand the organizational adoption process.

Section 3 contains detailed descriptions of the research design, with a focus on the collected data that serve as the core of this work, and on the recent interview study, including the data analysis. We also describe how we addressed the credibility, transferability, dependability, and confirmability quality criteria of the qualitative research [

30].

Section 4,

Section 5 and

Section 6 contain the results of the initial and current studies, followed by a brief discussion of each. We thematically sorted the sections according to general sustainability (

Section 4), sustainable technology adoption (

Section 5), and Green IT/IS adoption and usage (

Section 6). In

Section 7, we draw conclusions and state the limitations of the studies, as well as the potential for further research.

3. Research Design and Process

In this section, we elaborate on our research process. Although the published research is still dominated by research methods that can be regarded as quantitative [

55], we chose a qualitative approach. Our aim is not to gain insights into the influence of specific factors and the relationship [

56] between them or predict outcomes [

57], but to enrich and deepen the understanding [

58]. We seek to better understand a complex phenomenon [

55], and to provide rich descriptions of the background and context of why companies do or do (not) adopt sustainable practices and sustainable technologies, such as Green IT/IS.

To structure this elaboration, as well as the overall process, we used the four-step outline of Mayring [

29]: (i) planning the research; (ii) conducting the interviews; (iii) preparing the analysis; (iv) conducting the analysis. Researchers also frequently use this generally accepted approach for qualitative data generation and analysis to, for instance, investigate the contextual factors of organizational structures and organizational effectiveness [

59], evaluate the dimensions of digital transformation success [

60], or develop new constructs for technology acceptance and adoption [

61].

However, we should not mistake this for a standardized process that is to be strictly followed. Rather, it is a guideline that may be adjusted to specific research goals, materials, and insights [

29].

3.1. Planning and Aligning the Research

This research project is the continuation of a larger and still-ongoing research endeavor on corporate sustainability technology and Green IT/IS adoption at our research institute. Through this endeavor, which sets the overall theme, we seek to provide insights into (i) adoption intentions, (ii) the contextual factors of sustainable technology and Green IT/IS adoption, and (iii) the measurement of the adoption and usage of these technologies. Previous work has been both conceptual and empirical. The conceptual work has provided insights into (i) the nature of Green IT and Green IS as resources and capabilities that organizations use to generate a lasting competitive advantage [

10], (ii) the overall Green IT/IS adoption process and its ties to factors that are both internal and external to an organization [

26], and (iii) quick wins, with which companies can achieve long-lasting sustainability improvements as a first step towards increased corporate sustainability [

47]. On the empirical side, we build on works that (i) underline the benefits of sustainable innovations and Green IT/IS in organizations which have already been using these resources and capabilities for a considerable timespan [

46], and (ii) underline the relevance of sustainability and the associated technologies across Austrian, German, and Swiss companies [

27].

We also build on three currently unpublished studies (referred to as

initial studies), which we explicitly report on in

Section 3.5. In Study I, we focused on the reasons for corporate Green IT/IS adoption and the measurement of the specific benefits of these technologies. In Study II, we focused on the acquisition and development of Green IT and Green IS capabilities. In Study III, we focused on the influence of the internal and external factors that influence a company’s Green IT/IS adoption and usage.

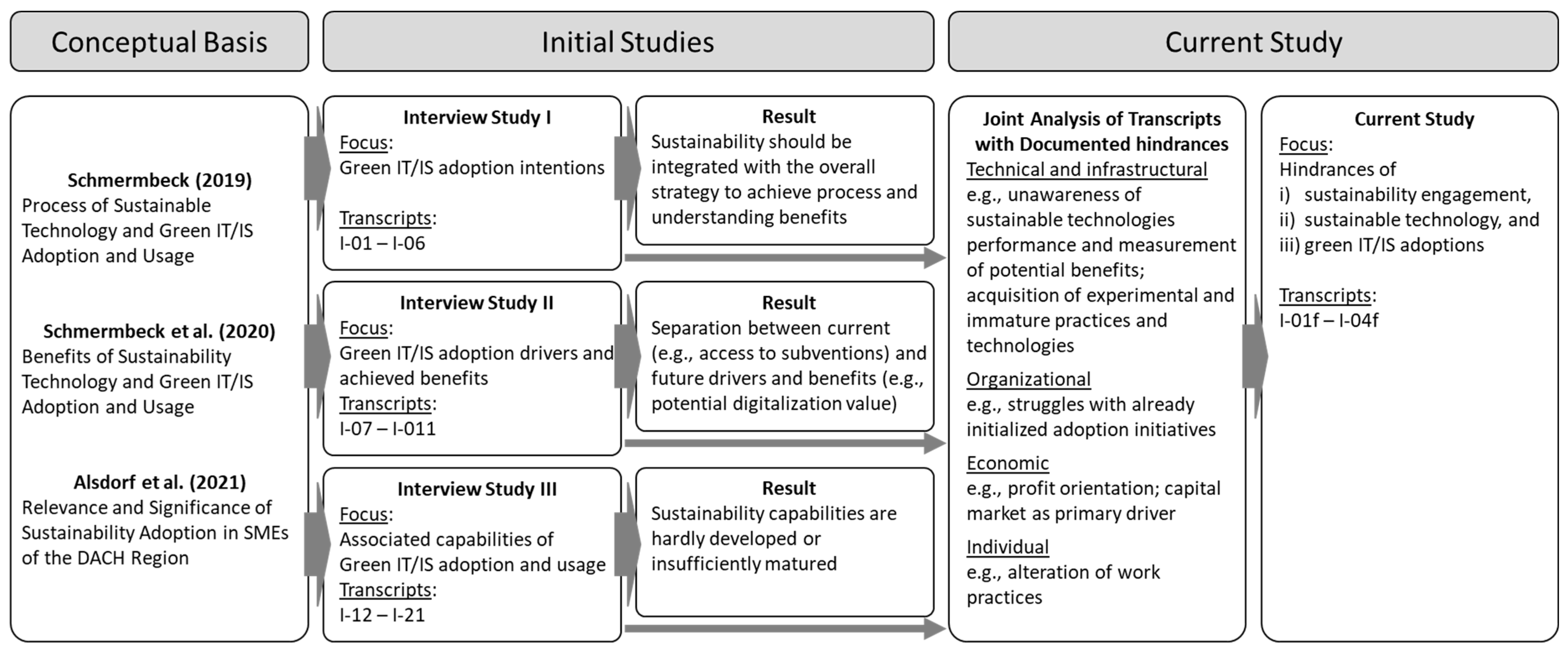

With their ties to the overall research endeavor, all the studies share the same conceptual and empirical bases, which was also synchronized between the individual data collections, and which allowed them to be interlinked, compared, and jointly worked up. We present an overview of the overall research process with the conceptual basis, results of the initial studies, and take aways from the current study in

Figure 1.

3.2. Selection of Expert Interviews

The initial studies, as well as this one, are of a qualitative nature and relied on expert interviews. We chose experts (i.e., corporate decisionmakers whose work concerns strategic or tactical work on sustainability or Green IT/IS matters) due to their core role in leading and coordinating corporate sustainability efforts [

28]. The active participants were specifically educated in the areas of interest (i.e., strategic decision making; IT/IS planning and operations; an understanding of Green IT/IS) [

62], and they offered us “privileged access to information and knowledge on the subject” ([

63], p. 7) and rich insights into the promises of and hindrances to sustainability management [

5].

We used semi-structured interviews as the research instrument, the prime benefit of which is that we can address the key dimensions of interest in a structured manner while also maintaining an open conversation with the interviewee [

63]. The method not only allowed us access to personal insights, views, and feelings, but it also allowed us to dig deeper into matters that we did not anticipate during the design of the study and the creation of the interview guide.

3.3. Performing Initial Studies

In the three initial studies, we focused on German companies, and we specifically investigated those with business models that either heavily relied on IT/IS usage (e.g., software developers, IT infrastructure providers), were linked to IT/IS (e.g., IT service providers, IT strategy consultancies), or were highly dependent on IT/IS usage (e.g., energy providers, industrial manufacturing). We acquired the companies and their representatives in diverse ways. We chose some through their publicly accessible sustainability listings and websites (e.g., Blauer Engel, Deutscher Nachhaltigkeitskodex), while we chose other representatives because they were personally known to the researchers, or because they had already taken part in one of the previous studies (i.e., [

27,

46]).

We initially contacted all the potential interviewees via email with an invitation to participate in a qualitative interview study. This email contained a brief description of the overall endeavor (see

Section 3.1), a more detailed description of the respective study, and a link to a bookable calendar so that the interviewees could easily schedule the dates of their interviews. After they booked their timeslots, we sent them confirmatory emails.

We conducted the interviews via phone or video conferencing tool. We had conducted 21 interviews as of September 2019: 6 for Study I (I-01–I-06), 5 for the initial Study II (I-07–I-11), and 10 for Study III (I-12–I-21). Overall, 2 interviewees came from a company with 50 employees or less, 7 interviewees came from a company with up to 250 employees, 5 came from a company with from 251 to 10,000 employees, and 9 came from a company with more than 10,000 employees. Regarding the industry, 4 interviewees came from a financial services company or energy provider, 3 were from industrial manufacturing or software development, and 2 were from consultancies (see

Table 1). We transcribed the conducted interviews of the initial study and sent them to the interviewees with a request for approval.

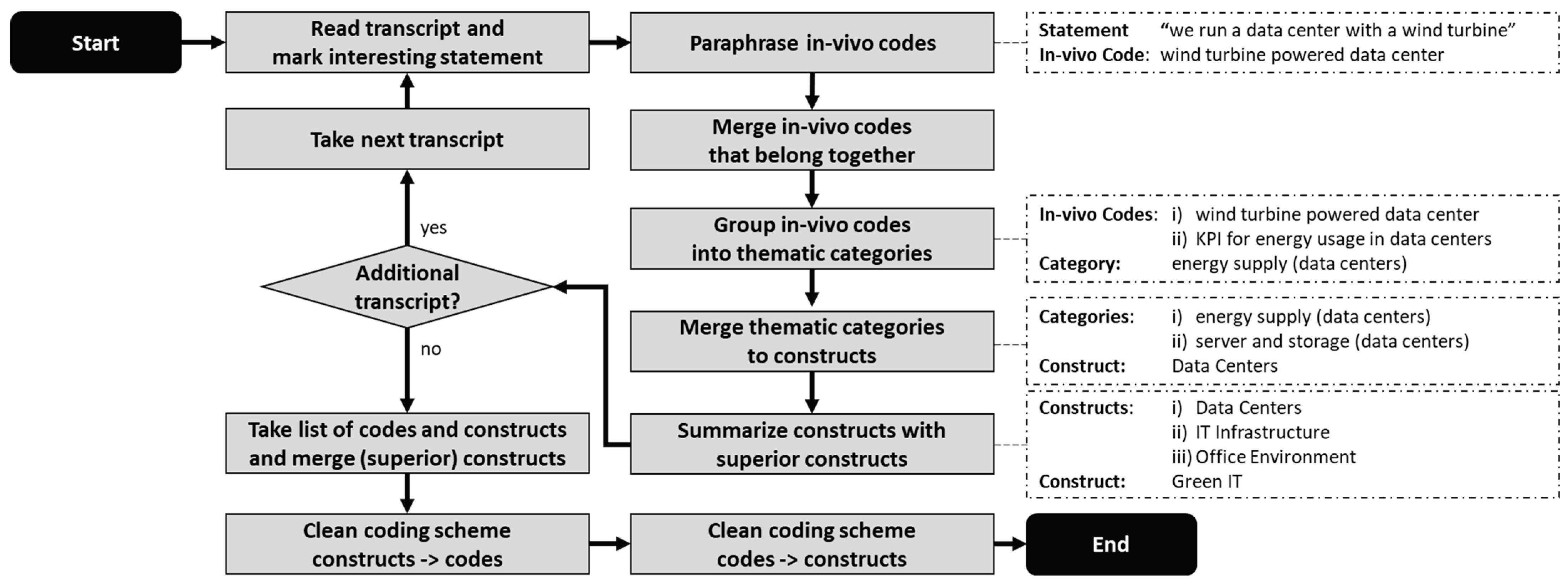

3.4. Data Analysis of Initial Study Data

The transcripts of the initial studies formed the unit of analysis of our research, and we analyzed them using MAXQDA 22. We first followed an open coding approach and marked all passages that provided any insight into: (i) the context of organizational sustainability intentions and actions; (ii) sustainability technology adoption and usage; (iii) hindrances to sustainability or sustainable technology adoption and usage.

We performed the coding in the following way:

We read the transcript and marked the interesting statements or passages. We then paraphrased these with in vivo codes (as the transcripts were in German, and the language of the overall research project is English, we formulated all the in vivo codes and the following further categorizations in English);

We summarized all the in vivo codes that belonged together in one category. For instance, we merged the marked text passages “we run a data center with a wind turbine” (I-08; p. 2) and “I would definitely put our project, with the wind turbine, at the front” (I-08; p. 11) under the in vivo code “wind turbine powered data center”;

We thematically grouped all the summarized codes. For instance, we thematically grouped “wind turbine powered data center” (I-14), “KPI for energy usage in data centers” (I-14), and “measurement of power usage efficiency in data center”’ (I-21) under “energy supply (data centers)”;

We merged constructs that fit together into one thematic construct. Certain code constructs and families had already been outlined and defined before the analysis (deductive category development [

29]), such as the previously addressed code family for the definition of the ‘Green IT’ concept [

9].

Other code constructs were the result of the data analysis (inductive category development) [

64]. For instance, we categorized the following statement under the code family “Not realized Green IT means”: “If we were to sell the [IT equipment] to our employees, we would still have [...] the problem that we are asked when something does not work and to get around this, we said no.” (I-17; l. 68–71);

If needed, we summarized the thematic constructs by an additional superior construct. For instance, we summarized the constructs ‘Data Center’, ‘General IT Management’, and ‘Office Environment’, for instance were summarized by the superior (first order) construct of ‘IT Operations’. We summarized inferior constructs as second-order constructs, and we summarized superior constructs as first-order constructs;

(a) If there was a further transcript, then we began the process again from Step 1. However, we did not separately group the additional merged in vivo codes, but integrated them into the already existing thematic categories (Step 3);

(b) If there was no further transcript, then we took the list of codes and constructs and assessed whether the present merged constructs could be further worked up and summarized by a code family;

The cleaning consisted of two rounds. We first started from top to bottom (from constructs to in vivo codes) to ensure that all the code families and constructs were on the same level of abstraction. The second round was from bottom to top to ensure that all the codes of the respective constructs were thematically fitting.

We visualized the overall analysis process and present it in

Figure 2. An overview of the logic of the marked passages, in vivo codes, code constructs and code families is presented in

Figure 3.

3.5. Description of Key Findings of Initial Studies

3.5.1. Findings and Implications of Study I

In the initial study, we focused on large companies in Germany. We investigated the specific corporate adoption intentions and preadoption drivers [

26] that initialize the adoption process itself. We conducted six interviews in two companies (I-01–I-06). We selected them based on the leading positions that they took in in their respective markets, and thus also on their potential to be relatively important influencing and guiding forces on markets, competitors, and the value chain. The generated insights shared certain similarities. For instance, both companies viewed sustainability as something that needs to be fully integrated into the other strategic goals, rather than as a separate entity. Moreover, both also valued IT and IS as enablers of the goals of simplifying and rationalizing the processes and deepening the understanding of them. Furthermore, both organizations seemed to see the immense potential in incorporating sustainable IT/IS innovations into a broad range of their products and processes, and to, for instance, further improve their carbon tracking. Despite this, I-01 mentioned that only a few of these alterations are actually put into practice and that more action could be taken. I-01, similar to I-02 and I-04, attributed this to a lack of commitment from the top management, and to the fact that, —as an

economic hindrance—organizations such as theirs are driven by investors, the capital market, and customers.

3.5.2. Findings and Implications of Study II

In the second study, we focused on SMEs in Germany. Although individually they are not as powerful as the large players on the market, taken together they have a nonnegligible influence on national and international markets and the economy. In the European Union, SMEs account for approximately 99.8% of all active companies [

65], and for 53% of the European gross domestic product [

66]. They also have substantially higher innovation speeds than large companies [

67]. Both reasons could be important factors for increasing the overall corporate sustainability of markets.

In the study, we asked the following: What are the reasons that SMEs adopt Green IT/IS? How do they measure the specific benefits of the technologies used? The first question is primarily relevant to this study because it is also specifically focused on the preadoption phase [

26]. To answer this question, we interviewed five representatives of five SMEs (I-7–I-11). The representatives had taken part in a previous study (i.e., [

27]) and were willing to be contacted again.

During the analysis of the data, we documented several adoption drivers, which we split into two categories: (i) current and (ii) future Green IT/IS adoption drivers. Because we conducted the study in June 2021, the COVID-19 pandemic was one of the most frequently named current societal drivers, as it primarily drove the acceptance and adoption of video conferencing and remote working technologies and regulations. We also documented several drivers at the organizational (e.g., access to external funding or subventions, the promise of increased power efficiency) and individual (e.g., increased environmental awareness) levels. For the future drivers, the study documented that the companies expected that the ways of virtual and remote working that were initialized by the COVID-19 pandemic would continue to grow and become more established in the future, thus leading to the adoption of more (Green) IT/IS that, on the one hand, will drive the company’ digital transformation and, on the other hand, reduce its environmental footprint. They further expected that the organizational, societal, and individual drivers would continue to interact and further drive them towards Green IT/IS adoption. For instance, I-09 expected that the changes that the automobile industry is currently facing—with altered consumer demands and increased governmental and environmental pressures—might eventually also affect the IT/IS industry, with similar mandatory changes. He expected that it would soon be mandatory that data centers be connected to district heating, or that their waste heat be used for heating the office buildings that they are installed in.

We also documented several hurdles to Green IT/IS adoption noted by the interviewees that are also key to this work. The interviewees noted that

technical or infrastructural hindrances or difficulties were especially problematic for the adoption of Green IT/IS. For instance, I-07 stated that they had no way of installing the measurement instruments to evaluate whether the IT/IS equipment needed improvement, or of knowing whether the potentially installed IT/IS would (environmentally) be beneficial. I-09 stated an analogous situation. He explained that with high technological risk often comes an

economic hindrance. If his company, for instance, wanted to switch its data center from a conventional air-cooling system to a substantially more efficient water-cooling system, then it would have to switch to a partially experimental technology, which, in itself, would also pose a substantial financial risk, as the company and its employees have no experience setting up, operating, or maintaining the novel technology. I-08 also mentioned certain

individual-level hindrances [

46], such as that certain employees need substantial convincing to use or adopt new technologies, or that working practices and the concern of companies for the natural environment are not as highly valued—or at least not as attractive—as established individuals working habits.

3.5.3. Findings and Implications of Study III

In the third study, we focused on the managerial aspects that accompany Green IT/IS adoption. We focused on the associated and needed capabilities of (a) the strategic planning and alignment of Green IT/IS objectives; (b) active process management (e.g., of technology lifecycle management, or enhancing business processes with IT/S); (c) establishing and adopting a sustainability-fostering culture and language; (d) compelling governance structures with relevant corporate policy processes to establish regulatory compliance [

10]. We specifically asked how these capabilities can be gained and managed, and we thus focused on the aspects of the adoption and postadoption phases [

26]. To answer this question, we conducted ten interviews across ten organizations (I-12–I-21). The results were rather unexpected, as it turned out that most of the companies did not have developed capabilities, nor did they seem to be actively developing them.

Hence, we asked the interviewees for the reasons that their companies were being prevented from adopting Green IT/IS and the associated capabilities. I-13 and I-16 stated that the reason was the lack of knowledge regarding its benefits. Some interviewees mentioned that—as a technological hindrance—they were not only unaware as to how the technology performed compared with the current technology (I-13–l. 321–323), but they were also unaware of certain aspects of the performance of the current technology (I-16–l. 244–254). For instance, they were aware that their data centers consumed energy, but they were unaware as to how much of it specifically accounted for running the hardware, cooling it, lighting the facilities, etc. For others, such as I-14, Green IT/IS simply had no management priority. I-14 saw no benefit to engaging a Green IT/IS adoption endeavor because the current digitalization initiatives were already a struggle. I-15 guessed that this strategic neglect was rooted in a fundamental issue that is primarily observable in the IT/IS industry: “Companies in the IT industry lay little value on green. There is a very high emphasis on selling and if possible, to throw away and buy new” (l. 125–127).

3.6. Creation of Semistructured Interview Guide

We based the semi-structured interview guide used in this study on the extracted findings from the 21 interviews that we initially conducted. We structured it into four thematically interconnected topic blocks: (I) interviewee background; (II) general sustainability; (III) adoption and usage of sustainable technologies; (IV) adoption and usage of Green IT/IS. While Block I only contained questions, we split Blocks II–IV into two parts. The first part consisted of questions that aimed to provide context on the interviewees’ views, standpoints, and experiences. In the second part, which was the focus of our attention, we confronted the interviewees with specific statements that we derived from the analysis of the initial interviews.

Taking the analyzed data from Studies I–III (see

Section 3.5), we evaluated them for the context factors of sustainable technology and Green IT/IS adoption and usage. To shed light on the research goal of providing a better understanding of the factors that negatively influence or prevent companies from meaningful pro-environmental engagement, we primarily focused on the risks, challenges, or otherwise negatively or critically perceived aspects of (i) sustainability in general (Block II); (ii) sustainable technologies and innovations (Block III); and (iii) Green IT/IS (Block IV). We not only synthesized specific ideas and arguments that, in our view, mirrored the crucial aspects in the respective categories, but we also decided to formulate statements out of these insights (in the following claims) that interviewees might consider potentially provocative or at least exaggerated, while not missing the content specificity. We did this with the clear intention of appealing to the interviewees’ emotions, to encourage them to speak more freely and answer more honestly, and to thereby create more interesting and meaningful insights into the contextual factors of sustainability and Green IT/IS adoption and usage, and also potentially into the rather delicate matter of why a company, or its decisionmakers, might decide against a specifically sustainable course of action.

Blocks II–IV comprised two organizational blocks: A welcome block and farewell block. In the former, we welcomed the interviewees, and we presented the researcher and study aim. We also informed them that we wanted to record them, and we read them a statement about the purpose and ethical standards of the study (e.g., voluntary participation, confidentiality, anonymity). After the participants agreed, we began the recording.

After the fourth block of questions and obtaining the respective statements, we asked the interviewees whether they had additional comments or concluding remarks to the interview. After this, we stopped the recording, thanked the interviewees for their participation, and outlined the further proceedings (i.e., transcription of data, data analysis, workup). We present an excerpt of the interview guide in

Table 2.

3.7. Planning and Performing the Study

We selected the energy and industrial manufacturing companies for further analysis for two reasons: (1) focusing on these industries had the benefit that similarly large companies could be selected of which the interviewees would have similar or at least comparable views on sustainability and sustainable technology usage; (2) the focus on two large companies and their representatives also made it possible to interview decisionmakers that had similar positions and obligations. All of them were also part of their corporate sustainability strategy teams, and they thus had the required experience with the companies’ sustainability plans, as well as with their internal and external influences. We contacted all six interviewees. Only four interviewees were willing to participate in the follow-up study (I-01f–I-04f).

After conducting the interviews, we transcribed them, sent them to the interviewees for their approval, and formed the unit of analysis for the investigation of the constraints. We analyzed the transcripts for their direct and indirect statements and responses to the statements, and we worked up the analysis.

3.8. Transferability as Core Quality Criterion

As with any other study, the initial and follow-up studies also faced the challenge of adhering to certain quality criteria. The usual quality criteria for research used to establish generalizability are reliability and internal and external validity [

64]. As qualitative research results cannot be and are not intended to be generalizable, but rather transferable to other contexts, we undertook our decisions as to our courses of action (as described in this section) with the intention of ensuring credibility, transferability, dependability, and confirmability [

30].

To ensure credibility, we aimed to interview persons with long-term engagement within our areas of interest, and we assessed and ensured that they were from the top or a higher level of management, and that their responsibilities included general strategic management, corporate sustainability management, or IT/IS management. We also briefed them about the intentions of the studies, and we asked them to provide honest, spontaneous, and truthful answers.

To address the transferability criterion, we provided a detailed description of our study, its context, and the results. We also ensured, in every interview of the initial and the follow-up studies, that the understanding of the core terminology between the researcher and interviewee was synchronized. The term ‘sustainability’ and the concepts of Green IT and Green IS especially needed clarification, as they were core to the data collection but are also often ambiguously understood (as previously outlined).

We achieved the high dependability by purposefully sampling the companies and adhering to the ethical standards of data generation (i.e., the confidentiality of the interviewees and their companies), as well as through a thorough analysis of the data and detailed descriptions of them. To achieve confirmability, we thoroughly transcribed the interview recordings, and we asked the interviewees to assess and approve the transcripts. We also separated the descriptions and the discussion of the findings of the initial and follow-up studies (see

Section 4).

4. Constraints on Sustainability and Sustainable Technologies

In the following sections, we present the statements on the constraints on sustainability and sustainable technologies that we derived from the initial studies, which represent the context factors and reasons that companies do not adopt sustainability (

Section 4) and sustainable technologies (

Section 5), such as Green IT/IS (

Section 6). We present them first, followed by a summary of the comments, thoughts, and insights into the statements from the follow-up study, as well as a brief discussion.

4.1. Sustainability Is Considered Unattractive and Not Innovative

When adopting a technology, companies frequently only look at the financials and neglect other categories. Regarding the purchasing department, one interviewee (I-12) personally felt that “sustainability plays a rather subordinate role” (l. 44–46). Another was glad that he had the freedom to “decide some things against our purchasing department, which tends to only look at the money.” (I-15; l. 86–87). Consequently, although sustainability seems to be of great interest to companies [

46], they often seem opposed to sustainable innovations, and sometimes not just because of reasons directly linked to a technology, but because of external factors, such as political and social factors, or internal factors, such as the value system or personal attitude of the adopting entity, which play important roles [

68].

Using a digital or mobile device for more than two years seems to have become a sign of being old fashioned or not innovative. For instance, one interviewee stated that, especially for digital devices, “one always seems old school, or […] are perceived as un-innovative when you use something for a long time” (I-01; l. 316–317). This individual adoption phenomenon also translates to organizational adoption practices and standards. Of course, it is individual managers and decisionmakers that set the standards for how long a technology is used within a company, as well as which technology is purchased and adopted in the first place. One interviewee reported this link between corporate and private decisions, describing a situation in which a company replaced the corporate car fleet of internal-combustion-engine cars with electric cars, as “the private [behavior] has […] also had an impact on the professional [behavior]” (I-07; l. 82–83).

We translated these observations (see

Table 3) into a statement, with which we confronted the interviewees in the follow-up study: “

Sustainability is not sexy”. We felt that this not only captured and reflected the (still) predominant societal sentiment, but also captured the reason why (i) sustainable products and services are still niche products on the mainstream markets; (ii) companies do not substantially alter their internal processes towards increased sustainability.

As expected, we received mixed comments on and responses to this statement (see

Table 4). Of the four interviewees, two agreed and two disagreed with it. The two interviewees who agreed argued that the unattractiveness of sustainable technologies was a social issue. One said, “Innovations that are sustainable are usually also not so terribly in demand, because for most users an innovation means nice, sexy and more comfortable” (I-02f; l. 159–160). He seems to directly take up our previous argumentation that only novel (digital) products are seen as innovative and are thus valued and purchased.

A second interviewee commented that “sustainability, in the general perception, is still too much associated with restrictions, renunciations and higher costs. […] That is why it is not attractive per se” (I-04f; l. 149–151), thereby presenting an argument that seems to support the reason that customers only seem to value new products. He also presented a reason why sustainability may always be seen as a burden: “It is not sexy because sustainability does not just exist, but sustainability exists because there are certain problems and challenges in this world” (I-04f; l. 165). As an illustrative example, he states that the hunger in the world is not nice, but addressing it is a serious goal, and that addressing sustainability issues is not sexy but quite dramatic (I-04f; l. 159–165).

The two other interviewees had different perspectives on this. One argued that the attractiveness of sustainability may be a generational question, and that the Fridays for Future movement nicely illustrates this. In his view, the younger generations are substantially different than previous generations: “in personal consumption and in terms of which employer I choose and in which area I would like to work. Sustainability is a key offer, both to customers and to employees, who also demand it. In that respect […] [s]ustainability is super sexy” (I-01f; l. 135–138). The second interviewee supported this claim, arguing that “sustainability is very sexy, as it fulfills a purpose, and it gives people and employees the opportunity to actually see the positive outcome of what they are doing” (I-03f; l. 191–193).

In our view, the arguments both—for and against the sexiness and attractiveness of sustainability to individuals and organizations—seem legitimate. Nevertheless, we also recognize the opportunity for companies to redefine the perception of sustainability to make it sexy, offer products to clients that are revolutionary and sustainable, and redefine and open new markets, thereby standing up against unsustainable forms of consumerism. A general market in which this transition is already visible is the food market. Alternative diets, such as vegetarianism and veganism, have become, and are still becoming, more and more popular. Some established meat production companies have recognized this trend. For instance, Rügenwalder Mühle recognized this and took the opportunity to alter and extend their business model, and it is now one of the most popular brands for meat replacement products on the growing market [

69,

70].

When thinking about sustainable IT/IS products, only a few companies come to mind that have successfully established sustainability-based businesses and products aside from the mainstream. One company is Fairphone B.V., which developed and produced a smartphone (the Fairphone) that is produced and marketed as sustainably as possible while maintaining its competitiveness on the regular market. By defining innovation as something beyond the functional improvements to a device, which also happens at a company level (i.e., business values, business processes, etc.) [

71], they set a clear example that sustainable IT/IS products do not need to be ‘lesser of a product’ or unsexy.

Researchers have proposed many views on how companies adopt and diffuse innovations (e.g., [

26,

45]) to establish a competitive advantage [

4]. Especially when discussing innovations in light of their potential to add to a companies’ sustainability, one core question is whether sustainable innovations—or those that are labeled and described as such—need to be regarded as a separate form, or whether they are merely regular innovations with alternate quality criteria.

Sustainable innovations—similar to any other impending innovation—require an initial cost–benefit analysis [

8]. However, it seems as though sustainable innovations are often not welcomed or are even opposed based on contextual reasons, such as infrastructural, political, or social factors [

68]. Hence, it seems beneficial to shed further light on this supposed difference and the potential reasons for non-adoption.

4.2. Sustainable Innovations Are Regarded as Inferior Investments

In the initial studies, we did not directly ask the interviewees whether they noticed a specific differentiation between regular and sustainable innovations, but they made various statements to this effect (see

Table 3). For instance, one interviewee stated, “at the end of the day, you still have to turn the coin left and right, and of course that’s always an investment that’s being made, and that’s currently more important than this sustainability idea” (I-07; l. 529–531). His view underlines the traditional view that prioritizes financials first and sustainability and ecology second [

72]. Another interviewee partially opposed this view by stating that “there are always […] two views, one is more the financial and management view, the other is more the area of sustainability. […] [and] it is simply crucial that it is possible to marry both worlds” (I-15; l. 36–38). Another interviewee also stated that, especially for sustainability innovations, “this understanding [of the investment logic of sustainability], […] must first be developed” (I-09; l. 311–312).

We were intrigued by the insight that, under certain circumstances, sustainable technologies might need to be evaluated differently than traditional technologies, and that they thus also do not need to adhere to the traditional investment logic. We consequentially wanted to find out whether there was a differentiation between the two technology and innovation forms (traditional and sustainable), and whether this also affected the investment logic. Thus, we first asked the follow-up interviewees whether they noticed a difference between regular and sustainable technologies, and we confronted them with the proposition: “Sustainable innovations are only investments that must pay off in the long term”.

We were surprised that—contrary to the initial interviewees—all the follow-up interviewees were of the view that there is no difference between sustainable and regular innovations, and consequently, that there is no difference between sustainable and regular investments (see

Table 4). Regarding the difference between sustainable and regular innovations, one interviewee stated, “One could […] define that a sustainable product would be CO2 neutral, or CO

2 positive. Also, on the other ecological components like the supply chain and the resource consumption. But because I will never completely reduce this consumption to zero […] there is then somewhere an arbitrary limit to what is sustainable and what is not” (I-01f; l.95–99). For him, a sustainable innovation would only be achieved as such if it made the company more sustainable compared with its as-is state (I-01f; l. 110–112). He also complements this argument by stating that discussions on the ecological aspects of sustainable innovations are hard to separate from the economic and social aspects of the proposed innovation: “Sustainability means making something financially and environmentally sustainable, and not at the expense of the next generation” (I-01f; l. 282–283), and “of course, a product or project must also be financially sound, otherwise it is not sustainable. That is exactly the definition. But then again, that does not mean that you should do it at the expense of ecology, in no way” (I-01f; l. 286–290).

Consequentially, our interviewees all agreed that there is no difference in the investment logic between sustainable innovations and the investments in them. However, there might be “idealists who see it differently and who might say: ‘I’ll put my solar panels on the roof and pay 10% more for electricity […]’. There are those, too”, according to I-02f (l. 450–452). However, in the end, I-04f concludes that “we are not a world of do-gooders. Money makes the world go round, and especially from the perspective of a DAX company; I have to say: We are investor-driven” (I-04f; l. 429–430).

Although this seems to be a non-negligible downside to investments in sustainable technologies, the interviewees also stated that “a sustainable product means, that I can make money from this very idea of ecology” (I-01f; l. 286–290), and that “in the long term—investing in a sustainable technology is cheaper than not investing and having to finance the environmental impact […] and the climate crisis. Thus, accordingly, [a sustainable innovation] is a good investment” (I-03f; l. 354–357). Consequently, we propose that, compared with a traditional investment, a sustainable investment is nowadays likely to be evaluated as inferior. When sustainability criteria (i.e., ecological and social criteria) are added to the investment proposal, thus creating a more holistic view on technologies [

26], this shift might likely change the balance of the investment decision, which would thus render the traditional product inferior.

5. Constraints on Sustainable Technology Adoption

5.1. Becoming Sustainable Requires Precise Measurements in Dimensions That Are Hard and Costly to Realize

As almost any business decision seems to be made based on numbers (e.g., investment cost, return-on-investment, amortization duration), it seems that sustainability and sustainability initiatives should also be precisely planned, measured, and controlled. The most fitting statement from the initial round of interviews in support of this argument was “If you want to be climate neutral or optimize in this direction, you then first have to open your wallet to realize measuring points in order to have meaningful figures to optimize towards. Otherwise, everything is just a rough estimate, and the measures may not be efficient at all” (I-09; l. 217–220). Other interviewees also agreed with this view: “Of course we want to reduce our CO2 footprint. Absolutely clear. But the exciting challenge is, first of all, to determine the status [of our footprint]. Where is it actually? How do you measure it? […] We are currently devoting a lot of energy to setting up sustainability reporting and making things measurable” (I-07; l. 153–156).

While others generally agreed with this, they also stated that purposefully operationalizing sustainability measurements was challenging for them: “It would be nice if we could control that a little bit more, also maybe make it [sustainability] more measurable” (I-08; l. 451–452). Another interviewee supported this argument by stating that sustainability was less an issue of realizing measurements and more one of investing in the right measurements: “If someone says to you, I can’t measure this at all, then he has invested in the wrong place or not in the right place. […] we […] have such measurement possibilities, because only if you have real numbers […] you can also go and say, now we go into optimization” (I-09; l. 183–187).

We thus wanted to find out more and to see whether the first steps towards greater sustainability are to primarily establish precise measurements or invest in tangible sustainability means (we present an overview of all the relevant statements in

Table 5). We thus confronted the follow-up interviewees with a proposition that we took almost verbatim from Interviewee I-09: “

If you want to be climate neutral, you first must open your wallet to realize measurement points in order to have meaningful data to optimize towards. Otherwise, everything is just kind of a rough estimate, and the measures may not be efficient at all”.

Two of the four interviewees agreed with this statement (see

Table 6). For instance, I-01 stated that, especially for him as a strategist, “measurability is always very important” (I-01f; l. 272). I-02 compared this issue to building a house, which requires an architect who ensures that all the measures fit together (I-02f; l. 493).

I-04 fully disagreed with the proposition. He stated, “The challenges are clear. […] We know that energy is an issue. We know that resource consumption is an issue. We know that recycling is an issue. We know that emissions are an issue. In this respect, it’s not really about knowing exactly where I have to compensate or reduce something and how much […] It’s just a matter of questioning all processes and structures and […] I don’t always have to be able to quantify that exactly” (I-04f; l. 448–454). I-03 agreed, stating that “both are needed. Quasi activities in direct implementation, in order to implement the first step with really realized measures in order to achieve the […] mindset shift” (I-03f; l. 376–379). He argued that after initializing the original change, measurement points need to be established to ensure transparent and quantifiable sustainability measures.

In our view, whether companies choose to precisely control the sustainability benefits of sustainable innovations depends on the companies’ overall sustainability maturity. If they are about to implement initial changes, then it might be beneficial for them to start with general and easy-to-implement means. Otherwise, the drive for sustainability will be blocked and hindered by bureaucratic and mathematical processes. Interviewee I-04f indicated exactly this by stating “Everyone knows that you should drive less and fly less. I can calculate for a long time how much I drive or fly per year. But it would be much cooler if I simply started taking the train tomorrow.” (I-04f; l. 465–467.) If a company is more mature, and if it has adopted a certain drive for change and sustainability, then it is certainly beneficial and logical to assess the current measures, not just to show that they are truly beneficial, but to also document and plan the areas for which the company has further room for sustainability improvement.

5.2. Adopting Highly Visible Sustainability Measures Often Only Has a Small Impact on Sustainability

During the first round of interviews, we asked the interviewees about the sustainability or Green IT/IS measures that their companies had already adopted and put into action. The most frequently mentioned initiative was the replacement of many or some of the company internal-combustion-engine car fleets with hybrid and/or fully electric cars (e.g., I-07; I-08; I-10; I-16). Others mentioned that they had started to produce their own energy by using solar panels on company buildings (e.g., I-10), had started to better separate their waste (e.g., I-17), or had installed water dispensers and were using glass bottles (e.g., I-08). Regarding Green IT/IS measures, many seemed to have already adopted some green IT quick wins [

47], such as reductions in the use of printers or multifunctional devices, or the implementation of restrictive printing policies (e.g., I-08, I-12, I-14, I-16; I-18).

While all of these measures have some benefit to the overall sustainability of companies, it nevertheless seems as though these low-hanging fruits were the first and sometimes the only initiatives mentioned, and that some companies stopped after taking the first steps towards real sustainability improvement. Only a few of the interviewees mentioned that they had or were undertaking measures with greater sustainability impact. For instance, as a software developer, I-07 develops the company software and its respective architecture as leanly as possible so that it runs faster and consumes fewer resources (RAM, storage), and thus less energy. I-15 also stated that completely redesigning the company data centers increased the power-usage efficiencies (from ca.1.5 to ca. 1.34) and significantly reduced the energy consumption by approximately 30–40%, which also reduced the respective CO

2 emissions by 60%. We present an overview of the relevant statements in

Table 5.

We wanted to dig deeper and understand how the sustainability experts of the follow-up study viewed this. We did not want to explicitly use the term ‘greenwashing’, as we felt that this would have shifted the discussion in a rather negative direction, and that it might also have put the interviewees in a rather defensive position. We thus avoided the term. Instead, we proposed the statement “Many of the highly visible sustainability measures have very little real impact on sustainability”, and we asked the follow-up-study participants to comment on it.

Although unexpected, Interviewee I-01f opined on the greenwashing topic: “Yes, it’s this classic greenwashing accusation […]. When a company is committed to sustainability, it is natural to start with the low hanging fruit. And these are oftentimes very effective.” However, his view differed from the other three follow-up interviewees, who agreed with our proposition. I-04f was critical: “Yes, I fully agree with that. My perception is that sustainability is very much associated with, let’s say, a fleet of electric vehicles. Or with, I don’t know, planting trees, creating flower meadows somewhere, or putting up insect hotels. That’s all very nice. But that’s not where the real issues are” (l. 477–486).

Interviewees I-02f and I-03f were not so sure whether the proposition was true for all cases. For instance, I-03f added that it might be the case for many initiatives, as it is “a question of external representation. In the media, the typical topic is planting trees. This is always taken with pleasure, although the effect appears only after 10-15 years and probably exists in many places also first no effect at all” (l. 363–365). I-02f, although agreeing that, in many cases, the sustainability effects are only rather marginal, urged being more cautious about it and individually evaluating the initiatives and outcomes (l. 483–486).

One potential explanation as to why companies do not do as much as they could or would rather not invest in measures that are not connected to their core businesses may be that there is no real incentive for them to become more ecologically sustainable. Oftentimes, their customers and clients do not request further sustainability, and governmental initiatives and regulations seem to be lacking, or they are at least not as effective as they could be.

Energy might be a good example of this. All businesses depend on it, but the incentives for companies to save energy and become more energy efficient are only small. Although increasing numbers of CO

2 pricing measures are being enforced [

14], which also subsequently affect energy prices in the long run, energy, and especially for companies, is still too cheap. For instance, one interviewee stated, “saving 10 percent electricity in the data center, that’s good for the environment, but it doesn’t mean that we cheer for that. Ultimately, electricity is too cheap for that. […] if you have industrial tariffs, the savings effects do not pay off quite as quickly as they do for private consumers” (I-16; l. 142).

6. Constraints on Green IT/IS Adoption and Usage

6.1. Many Green IT/IS Initiatives Only Focus on End-of-the-Pipe Measures

Our next observation takes Constraint 5.2 into account and addresses whether the adoption of Green IT/IS is merely the treatment of a symptom or is sought to initiate real sustainability change.

In the initial studies, we asked the interviewees about their current Green IT/IS means, and we categorized their responses into the Green IT and Green IS dimensions [

9]. We documented 212 Green IT (IT sourcing: 85; IT operations: 82; IT disposal: 45) and 76 Green IS (IT governance: 18; IT organization: 47; IT external market: 11) codes. According to this analysis, companies seem to focus more on Green IT and hardware management measures than Green IS. Although we do not claim completeness or generalizability, this finding is supported by other research, such as that of Alsdorf et al. [

27], who came to similar conclusions. When taking a closer look, we also found that many interviewees named multiple initiatives that were categorized into one of the Green IT/IS dimensions. For instance, I-02 mentioned six measures in the Green IT disposal dimension, which we further divided into two subdimensions: (i) reusing and refurbishing (i.e., giving IT hardware to employees; donating it to social projects; selling it on the market; returning it to the producer); (ii) recycling (i.e., shredding hard drives and selling them as scrap metal; disposing of parts).

Other frequently named means were making changes to the data center, printer, or office energy management by, for instance, outsourcing their data centers (3), optimizing their cooling by placing them in the northernmost departments of the companies (3), or centralizing or rearranging the structure of the data center itself (3). For reducing printer usage, many companies had already adopted initiatives of going paperless (9), reducing printers (3), and digitizing processes to reduce the necessity of printing (3). We analyzed and eliminated several nominations for each of the Green IT/IS dimensions, and we realized that most companies undertook measures that fall under the sourcing (10), operation (13), and disposal (10) categories. While six companies named means that fall under the external market dimension, only three also undertook IT governance, and only two undertook organization means.

The interviewees more frequently named hardware-related means than capability-related means (see

Table 7 and

Table 8), but only a few Green IT/IS initiatives were focused on reducing and minimizing their environmental impacts without making grand alterations (e.g., to the overall corporate or production processes or structures) (see

Table 9). We thus were keen to gain further insight into this potential adoption hindrance, and we proposed the following: “

Current Green IT/IS measures in companies focus too much on end-of-the-pipe measures—i.e.,

measures that seek to reduce the environmental impact of the IT/IS used by means of downstream measures and do not change the product or the production process itself”.

All four follow-up-study interviewees agreed with the statement, and some also regarding their companies (see

Table 10): “That’s how I would see it at [COMPANY], yes. Well, the dialog with the employees, the view on the supply chain is not so much in focus when it comes to sustainability” (I-01f; l. 349–350). However, some saw this focus on end-of-the-pipe means as less critical than others. For instance, Interviewee I-03f stated, “That is indeed the case, from my point of view. Simply because it provides the entry point [for more sustainability means]” (l. 434–437). Others, such as I-04f, viewed this as more critical: “Yes, I would agree with that. Especially since the responsibility of a company usually stops where something leaves the company” (l. 565–569). He agreed that some partners are certified to recycle or reuse hardware in a sustainable manner, but he generally criticized the lack of end-to-end responsibility: “The question of avoidance, and question of procurement, and question of construction, actually starting from scratch and thinking purely technically, I don’t see that at all” (I-04f; l. 570–575). I-03f also observed an extended focus on cleaning-up measures as the most critical. In his view, companies have wasted too much time, and now “we don’t have the time to focus on end-of-the-pipe anymore, but we really need to get to the core of the whole thing” (l. 435–437).

Consequently, it seems as though not that many Green IT innovations had been adopted, but that there was a rather strong focus on them, and that only a few Green IS initiatives had been initialized and adopted. Thus, as in the digitalization context, sustainability matters, but companies seem to focus on conservative renovation. They seek to reengineer and replace one technology with another, without reimagining their companies and processes, or making more fundamental changes and addressing structural issues [

73]. For the initial adoption of sustainable technologies and Green IT/IS, this seems fine, and some changes, such as altering processes to fully digital processes, may be an ideal starting point for companies (as indicated by I-03f). However, many companies seem to stop after this initial change and, consequently, they not only miss the opportunity to become more innovative, but also more sustainable.

6.2. The Use of Green IT/IS Is Feared for Adverse or Rebound Effects

The last boundary condition for the adoption and usage that we noticed was that some interviewees mentioned that the usage of IT and IS might (sustainability wise) lead to contrary effects. The primary issue here seems to be that users often do not see the negative impacts of their digital technology usage, and that the more profound impacts are hard to measure (see Constraint 5.1). For instance, as a software developer, I-07 sought to not only use leaner coding principles, but to also ensure that the dimension of the application sufficiently covered the client’s needs, but could be seamlessly scaled if needed (I-07; l. 519–522). However, the clients seem mostly unaware that developing software in this way also benefits them by ensuring that the software not only consumes fewer hardware resources, but that it also saves money as a consequence (e.g., quicker runtimes mean less energy consumed). He stated, “this danger of rebound effects, that the more you transform digitally, for example, [the more you] accordingly must also control the energy consumption, this is, at the moment, still a side note” (I-07; l. 238–240).

Moreover, some of the sustainability managers, such as I-20, feared that using Green IT/IS might not be as revolutionarily efficient as was hoped. He compared Green IT/IS with the invention of the steam engine, for which “on had high hopes of high efficiency effects, but in the end only had an extreme acceleration, and also more consumption of energy, and more consumption of resource consumption that one originally not have had” (l. 185–187). He also feared similar effects from other digital technologies that he was not overly familiar with, such as Blockchain.

Another side effect of digital products and services is that they require the work of fewer people. Some interviewees referred to this, and one specifically described a discussion that he had with a client about a production machine in development. He stated that “the factor that he [i.e., the client] needs less personnel with this new machine, was enormously important for him. It thus was of course also a key performance indicator how much less personnel is needed compared to before” (I-11; l. 193–197). He also speculated that one reason for the fear of rebound effects may be that “the digitalization measures in a company are considered completely independently with sustainability measures” (l. 516–517), and that “the digital technologies that are used [in a company] only make sense or can only be designed in a resilient and sustainable manner if they have also been developed in a sustainable manner” (l. 174–176).

We took this mix of speculations and insights (presented in

Table 10), and we formulated the following statement: “

The usage of Green IT/IS carries a high risk of rebound effects—i.e.,

the risk that an increased use of Green IT/IS will lead to ecologically opposite (negative) effects”. In terms of this proposition, the follow-up interviewees had mixed verdicts.

On the one hand, Interviewees I-01f and I-03f presented reasons why the risk of sustainability rebound effects might not be unjustified. Referring to the risk caused by inadequate or non-existent planning, Interviewee I-03f (l. 442–447) stated, “The more digitalization, the more energy consumption, the less attention I pay and the less thought I put into it, the more the danger that it will actually go into overdrive and then the rebound will set in”. Interviewee I-01f only partially recognized the sustainability rebound risk, and primarily for IT: “In the case of IT, one could only think, that the threshold for personal usage drops. People would say, ‘Okay, the iPhone is green, so I can buy one every 2 years instead of every 5 years.” (l. 361–363). However, he was rather on the contrary side, stating, “I don’t think that’s how users think. I think the user only has his mind only on the IT and the idea of sustainability is not yet rooted enough for it to have an influence” (I-01f; l. 361–365). Interviewee 04 argued the same, adding that “you can’t suddenly buy unlimited amounts of something that is somehow more sustainable. So no, I would say it’s just a matter of replacement [i.e., a product] in existing structures. And then things will continue exactly as before.” On the company side, Interviewee 03 argued that Green IS “are more on the architectural level: How can I shift my computing processes, make them more efficient, so that they consume less power? And I think that’s in the backend. That has little impact on the user in the end. Ideally, there is no green rebound effect” (I-01f; l. 355–360).

Overall, we conclude that our interviewees did not see the risk of the sustainability rebound effects of Green IT/IS usage. They argue that consumers will only replace a nonsustainable product with a more sustainable one, while in corporations, Green IT/IS adoption and usage will be aligned and integrated with other sustainability and innovation initiatives to address this risk.

7. Conclusions

The research on the corporate adoption of sustainability and the associated sustainable technologies, such as Green IT/IS, is constantly growing [

9,

22]. However, there is a lack of studies that improve our understanding of the drivers and hindrances of meaningful corporate sustainability interventions, as well as their associated risks and challenges. According to some practitioners’ insights (e.g., [

21]), misaligned incentives, competing priorities, and a lack of expertise are the core issues of proper institutional Green IT usage.

We addressed this shortcoming by investigating the factors that negatively influence or prevent companies from meaningful pro-environmental engagement and/or hinder them from adopting and using sustainability-engaging technologies, such as Green IT/IS. As this study is part of an ongoing research project (see

Section 3.1), we took already-published work as the conceptual basis and used the insights of 21 interviews from three interconnected yet unpublished studies as our initial basis (see

Section 3.5). We identified the boundary conditions of sustainability and sustainability technology adoption, and we worked them up into six statements. Then, we took these constraints and discussed them with four interviewees of the initial studies. We now elaborate on the generated insights, which are valuable for research and practice.

For the

first constraint (

Section 4.1), we found that sustainability and sustainable products—due to their nature of addressing global, societal, and environmental issues—are (currently) not regarded as attractive for mainstream adoption. One interviewee stated, “[Sustainability] tends to be associated with constraints or with self-constraint” (I-01f; l. 142–144). However, we, as well as the interviewees, also see that societies seem to be in a permanent state of flux. Younger generations may be seen as “sustainability natives” (I-06; l. 245–246) that demand sustainability and sustainable products (I-01f), and sustainability and sustainable innovations may thus continuously lose their stigma.

Some of the interviewees also recognized that, sooner or later, “non-sustainable management will eventually take its toll on the company” (I-07; l. 169–170), perhaps because governments continue to pass increasingly strict environmental regulations, or because their competitors have outperformed them so that they are forced to drastically react, if not go out of business. Hence, companies should test and experiment with these technologies not only to establish quick wins [

47,

74], but also to prepare themselves, analyze their motivation for sustainability, and derive the consequential means and goals [

2].

Research could guide and document these processes, and it could also shed further light on the seeming unattractiveness of sustainability and sustainable technologies. It might be promising to evaluate different consumer groups and their perceptions, as well as the usage of (non-)mainstream sustainable products and services. For IT products, the Fairphone [

71], for instance, could be one example that could be further investigated and that might also serve as an example of positioning a sustainable product on a mainstream market, and as a competing product in a corporate setting.

In terms of the

second constraint (

Section 4.2), regarding whether there is a difference between ‘traditional’ and ‘sustainable innovations’, and their consequential investment logics, we found it difficult to specify or pinpoint a specific differentiation, at least in terms of terminology. Sustainable technologies, while performing at least slightly worse than traditional technologies in the established categories (i.e., technological compatibility, financial upfront investments), arguably seem to have certain non-negligible benefits (i.e., for the companies’ sustainable competitive advantages and environmental footprints). Our interviewees acknowledged this fact, and they stated that many of the decisionmakers did not seem to understand the investment logic (I-09; l. 311–312), and that sustainable innovations will likely make up the initial disadvantage (I-01f; 282–287). Thus, sustainable innovations seem to share certain similarities with disruptive technologies [

75], which should be further investigated in future research.

As the specific contribution of an investment is traditionally associated with the financial benefits for a company, we investigated whether the sustainability benefits need to be similarly controlled (the

third constraint of

Section 5.1). We found that the precise measurement of sustainable benefits was generally beneficial and necessary. However, for initial sustainability initiatives, our interviewees widely agreed that the areas of engagement are rather clear, and that it is a matter of initializing the change rather than specifically measuring and quantifying it. Thus, it would be fruitful to further investigate quick wins [

47], and to specify if and how they, as well as their successive means and initiatives, can be initiated. As it seems illogical to initialize change without specifying any controlling instrument, it might also be beneficial to conceptualize and suggest easily quantifiable indicators so that decisionmakers not only see the impacts of their decisions, but also understand the effects that their corporate actions have on the planet’s biosphere.

We investigated how our interviewees assessed the impact of highly visible corporate sustainability efforts and their sustainability benefits (the

fourth constraint of

Section 5.2). In their view, many of these actions undoubtedly have a positive impact on corporate sustainability. However, they make the criticism that many companies do not seem to address the aspects that companies need to make a real contribution to sustainability. A frequently referred to example was the corporate planning of trees, which undeniably has a positive effect on the planet’s biosphere but takes many years to manifest. To further address this issue, we suggest cataloguing frequently used corporate sustainability actions and investigating their effectiveness (i.e., in the respective amount of reduced or compensated CO

2), as well as the time taken to reach their highest or fullest effectiveness. This suggestion harkens back to the quick-win call (see above), and we propose combining both efforts.

Many Green IT/IS initiatives seem to only focus on end-of-the-pipe measures (the

fifth constraint of

Section 6.1), which is a claim that is supported by the observation that the companies adopted substantially more (hardware-related) Green IT means than (process-related) Green IS initiatives (see

Table 8 and

Table 9). While this seems to be a viable option for initial sustainability adoption, it runs the risk that companies will miss the chance to initialize real sustainability changes. By focusing only on hardware-related issues, decisionmakers might conclude that sustainability is nothing more than an alternative investment decision. However, by following this assumption, companies overlook initializing real change, which requires redesigning corporate processes and altering the governance and culture [

10]. Further research should take up this insight and specifically investigate cases in which companies have started to develop Green IS and sustainability capabilities. These insights promise to be fruitful for other companies that first need to initialize sustainability changes, or for those whose sustainability changes are not as effective as hoped.

Finally, we also assessed whether the adoption and usage of Green IT/IS has a high risk of rebound or ecologically adverse effects (the

sixth constraint of

Section 6.2). This was only partially supported by our interviewees, and their reasoning primarily lies in the fact that sustainable IT/IS seems to only be adopted to directly replace another IT/IS. This insight needs to be regarded in the context of the fifth constraint, as it also seems to indicate that companies refrain from initializing real sustainability changes and often “only cure a symptom”. This underlines that more substantial research is needed not only into why this is, but also into the nature of Green IT/IS, so that corporate decisionmakers understand them better to select the most promising means and initiatives for their companies that can then be integrated into the organization’s future architecture.

7.1. Limitations

One limitation that should be addressed in further studies is that, in the follow-up study, we interviewed only four interviewees from two large German companies. This is a substantial limitation, as it only reflects the drivers and hindrances from the perspective of companies that, although equipped with substantial financial power, are primarily driven by shareholder and legislator interests. It would be beneficial to reflect upon and deepen our insights into SMEs. For this, we suggest focusing on Austrian, German, and Swiss companies to close the circle with the initial studies [

27].

7.2. Further Research

In terms of the specific further research outlined before (see

Section 7), we also feel that it is necessary to further investigate the general topics of the corporate adoption processes of sustainable innovations and Green IT/IS [

26]. In our study, we underlined that large companies, especially, seem to be primarily influenced by only societal (i.e., regulatory and financial drivers) and organizational (i.e., internal financial drivers) drivers. It would be interesting to see whether these drivers can be directly translated to other corporations, such as SMEs. Some of our interviewees doubted this and suspected that family-owned or cooperative companies, especially, were more likely to put emphasis on the social and ecological factors of the TBL [

32]: “I think that an owner-managed company is definitely more willing to anchor such cultural values within the corporate culture […] than a stock corporation.” (I-02f; l.427–428).

Furthermore, it would be interesting to investigate Green IT/IS adoption in a long-term case, or even in an action research setting [

76]. Selecting a company and accompanying it through the entire adoption process would offer rich insights into the proceedings, and well as into the challenges and how they can be overcome.

7.3. Theoretical and Practical Contributions

Our study is beneficial for both researchers and practitioners. From a theoretical perspective, we underline that sustainable innovations have certain crucial differences from traditional non-sustainable innovations. With an (potential) initial worse performance in the traditional financial dimensions, we underline that sustainable innovations share certain similarities with disruptive innovations [

75]. This insight also indicates that we need to regard the adoption process of sustainable innovations from a holistic perspective [

26].