The Impact of Green Innovation on Enterprise Performance: The Regulatory Role of Government Grants

Abstract

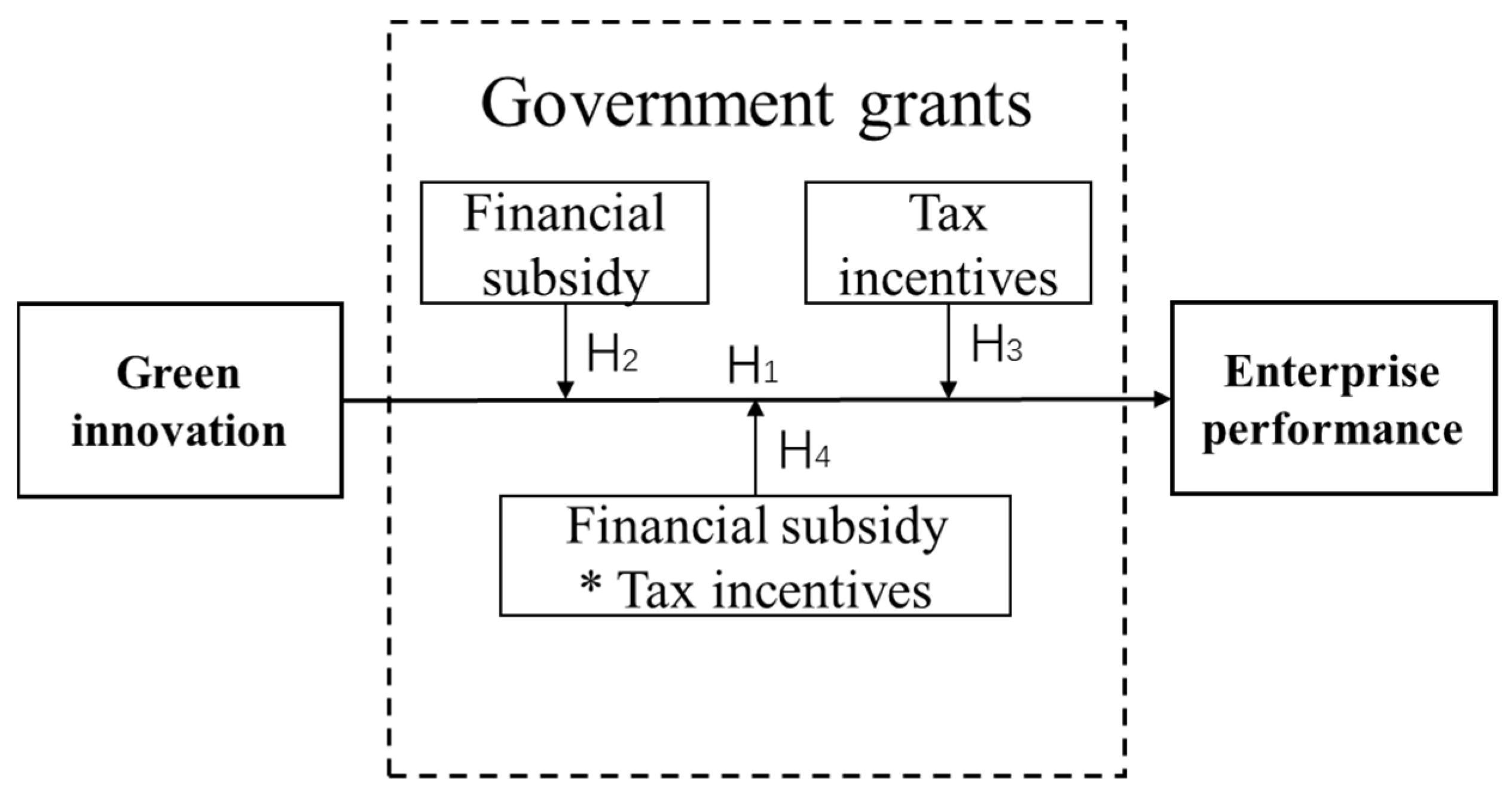

:1. Introduction

2. Theoretical Framework

2.1. Green Innovation and Enterprise Performance

2.2. The Regulatory Role of Government Grants

2.2.1. Regulatory Role of Fiscal Subsidies

2.2.2. Regulatory Role of Preferential Taxation

2.2.3. The Regulatory Effect of Fiscal Subsidies and Preferential Taxation When They Go Hand in Hand

3. Materials and Methods

3.1. Sample Selection and Data Sources

3.2. Variable Design

3.3. Modeling

4. Empirical Results and Analysis

4.1. Descriptive Statistics

4.2. Correlation Test

4.3. Regression Analysis

4.4. Robustness Test

4.4.1. Endogenous Test

4.4.2. Replacement Indicators

4.4.3. Model Replacement

4.5. Further Analysis

5. Conclusions and Policy Implications

5.1. Conclusions

5.2. Policy Implication

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Hao, X.; Chen, F.; Chen, Z. Does green innovation increase enterprise value? Bus. Strategy Environ. 2022, 31, 1232–1247. [Google Scholar] [CrossRef]

- Dai, D.; Xue, Y. The Impact of Green Innovation on a Firm’s Value from the Perspective of Enterprise Life Cycles. Sustainability 2022, 14, 1226. [Google Scholar] [CrossRef]

- Feng, Z.; Chen, W. Environmental regulation, green innovation, and industrial green development: An empirical analysis based on the Spatial Durbin model. Sustainability 2018, 10, 223. [Google Scholar] [CrossRef] [Green Version]

- Sun, Y.; Sun, H. Green innovation strategy and ambidextrous green innovation: The mediating effects of green supply chain integration. Sustainability 2021, 13, 4876. [Google Scholar] [CrossRef]

- Zhou, M.; Govindan, K.; Xie, X.; Yan, L. How to drive green innovation in China’s mining enterprises? Under the perspective of environmental legitimacy and green absorptive capacity. Resour. Policy 2021, 72, 102038. [Google Scholar] [CrossRef]

- Zhang, Y.; Xing, C.; Wang, Y. Does green innovation mitigate financing constraints? Evidence from China’s private enterprises. J. Clean. Prod. 2020, 264, 121698. [Google Scholar] [CrossRef]

- Song, M.; Chen, M.; Wang, S. Global supply chain integration, financing restrictions, and green innovation: Analysis based on 222,773 samples. Int. J. Logist. Manag. 2018, 29, 539–554. [Google Scholar] [CrossRef]

- Xiang, X.; Liu, C.; Yang, M. Who is financing corporate green innovation? Int. Rev. Econ. Financ. 2022, 78, 321–337. [Google Scholar] [CrossRef]

- Yu, C.-H.; Wu, X.; Zhang, D.; Chen, S.; Zhao, J. Demand for green finance: Resolving financing constraints on green innovation in China. Energy Policy 2021, 153, 112255. [Google Scholar] [CrossRef]

- Ma, W.; Zhang, R.; Chai, S. What drives green innovation? A game theoretic analysis of government subsidy and cooperatiRanran Zhanon contract. Sustainability 2019, 11, 5584. [Google Scholar] [CrossRef]

- Owen, R.; Brennan, G.; Lyon, F. Enabling investment for the transition to a low carbon economy: Government policy to finance early stage green innovation. Curr. Opin. Env. Sust. 2018, 31, 137–145. [Google Scholar] [CrossRef]

- Gohoungodji, P.; N’Dri, A.B.; Latulippe, J.-M.; Matos, A.L.B. What is stopping the automotive industry from going green? A systematic review of barriers to green innovation in the automotive industry. J. Clean. Prod. 2020, 277, 123524. [Google Scholar] [CrossRef]

- Soltmann, C.; Stucki, T.; Woerter, M. The impact of environmentally friendly innovations on value added. Environ. Resour. Econ. 2015, 62, 457–479. [Google Scholar] [CrossRef]

- Meckling, J.; Sterner, T.; Wagner, G. Policy sequencing toward decarbonization. Nat. Energy 2017, 2, 918–922. [Google Scholar] [CrossRef]

- Junaid, M.; Zhang, Q.; Syed, M.W. Effects of sustainable supply chain integration on green innovation and firm performance. Sustain. Prod. Consump. 2022, 30, 145–157. [Google Scholar] [CrossRef]

- Singh, M.K.; Kumar, P.; Agrawal, S. Analyzing the Green Manufacturing and Organizational Performance of the Indian SMEs. In Recent Trends in Industrial and Production Engineering; Springer: Singapore, 2022; pp. 47–56. [Google Scholar]

- Wong, C.Y.; Wong, C.W.; Boon-itt, S. Effects of green supply chain integration and green innovation on environmental and cost performance. Int. J. Prod. Res. 2020, 58, 4589–4609. [Google Scholar] [CrossRef]

- Sellitto, M.A.; Camfield, C.G.; Buzuku, S. Green innovation and competitive advantages in a furniture industrial cluster: A survey and structural model. Sustain. Prod. Consump. 2020, 23, 94–104. [Google Scholar] [CrossRef]

- Robinson, S.; Stubberud, H.A. Green innovation in Germany: A comparison by business size. J. Int. Bus. Res. 2013, 12, 47. [Google Scholar]

- Chang, C.-H. The influence of corporate environmental ethics on competitive advantage: The mediation role of green innovation. J. Bus. Ethics 2011, 10, 361–370. [Google Scholar] [CrossRef]

- Zhang, X.; Tang, Z. Construction of computer model for enterprise green innovation by PSO-BPNN algorithm and its impact on economic performance. PLoS ONE 2022, 17, e0262963. [Google Scholar] [CrossRef]

- Hao, J.; He, F. Corporate social responsibility (CSR) performance and green innovation: Evidence from China. Financ. Res. Lett. 2022, 48, 102889. [Google Scholar] [CrossRef]

- Kim, I.; Pantzalis, C.; Zhang, Z. Multinationality and the value of green innovation. J. Corp. Financ. 2021, 69, 101996. [Google Scholar] [CrossRef]

- Satta, G.; Spinelli, R.; Parola, F. Is tourism going green? A literature review on green innovation for sustainable tourism. Tour. Anal. 2019, 24, 265–280. [Google Scholar] [CrossRef]

- Li, Z.; Liao, G.; Wang, Z.; Huang, Z. Green loan and subsidy for promoting clean production innovation. J. Clean. Prod. 2018, 187, 421–431. [Google Scholar] [CrossRef]

- Chen, Y.-S. The driver of green innovation and green image–green core competence. J. Bus. Ethics 2008, 81, 531–543. [Google Scholar] [CrossRef]

- Kraus, S.; Rehman, S.U.; García, F.J.S. Corporate social responsibility and environmental performance: The mediating role of environmental strategy and green innovation. Technol. Forecast. Soc. 2020, 160, 120262. [Google Scholar] [CrossRef]

- Soewarno, N.; Tjahjadi, B.; Fithrianti, F. Green innovation strategy and green innovation: The roles of green organizational identity and environmental organizational legitimacy. Manag. Decis. 2019, 57, 3061–3078. [Google Scholar] [CrossRef]

- Chen, J.; Liu, L. Profiting from green innovation: The moderating effect of competitive strategy. Sustainability 2018, 11, 15. [Google Scholar] [CrossRef] [Green Version]

- Li, J.; Du, Y. Spatial effect of environmental regulation on green innovation efficiency: Evidence from prefectural-level cities in China. J. Clean. Prod. 2021, 286, 125032. [Google Scholar] [CrossRef]

- Arfi, W.B.; Hikkerova, L.; Sahut, J. External knowledge sources, green innovation and performance. Technol. Forecast. Soc. 2018, 129, 210–220. [Google Scholar] [CrossRef]

- Tariq, A.; Badir, Y.; Chonglerttham, S. Green innovation and performance: Moderation analyses from Thailand. Eur. J. Innov. Manag. 2019, 22, 446–467. [Google Scholar] [CrossRef]

- Hu, G.; Wang, X.; Wang, Y. Can the green credit policy stimulate green innovation in heavily polluting enterprises? Evidence from a quasi-natural experiment in China. Energy Econ. 2021, 98, 105134. [Google Scholar] [CrossRef]

- Zhang, Z.; Duan, H.; Shan, S.; Liu, Q.; Geng, W. The impact of green credit on the green innovation level of heavy-polluting enterprises—Evidence from China. Int. J. Environ. Res. Public Health 2022, 19, 650. [Google Scholar] [CrossRef]

- Peng, J.; Song, Y.; Tu, G.; Liu, Y. A study of the dual-target corporate environmental behavior (DTCEB) of heavily polluting enterprises under different environment regulations: Green innovation vs. pollutant emissions. J. Clean. Prod. 2021, 297, 126602. [Google Scholar] [CrossRef]

- Zhong, Z.; Peng, B. Can environmental regulation promote green innovation in heavily polluting enterprises? Empirical evidence from a quasi-natural experiment in China. Sustain. Prod. Consump. 2022, 30, 815–828. [Google Scholar] [CrossRef]

- Wang, H.; Qi, S.; Zhou, C.; Zhou, J.; Huang, X. Green credit policy, government behavior and green innovation quality of enterprises. J. Clean. Prod. 2022, 331, 129834. [Google Scholar] [CrossRef]

- Li, X.; Lai, X.; Zhang, F. Research on green innovation effect of industrial agglomeration from perspective of environmental regulation: Evidence in China. J. Clean. Prod. 2021, 288, 125583. [Google Scholar] [CrossRef]

- Fan, F.; Lian, H.; Liu, X.; Wang, X. Can environmental regulation promote urban green innovation Efficiency? An empirical study based on Chinese cities. J. Clean. Prod. 2021, 287, 125060. [Google Scholar] [CrossRef]

- Hsu, C.-C.; Quang-Thanh, N.; Chien, F.; Li, L.; Mohsin, M. Evaluating green innovation and performance of financial development: Mediating concerns of environmental regulation. Environ. Sci. Pollut. R. 2021, 28, 57386–57397. [Google Scholar] [CrossRef] [PubMed]

- Zhang, Q.; Ma, Y. The impact of environmental management on firm economic performance: The mediating effect of green innovation and the moderating effect of environmental leadership. J. Clean. Prod. 2021, 292, 126057. [Google Scholar] [CrossRef]

- Agustia, D.; Sawarjuwono, T.; Dianawati, W. The mediating effect of environmental management accounting on green innovation-Firm value relationship. Int. J. Energy Econ. Policy 2019, 9, 299–306. [Google Scholar]

- Qi, G.; Zeng, S.; Tam, C.; Yin, H.; Zou, H. Stakeholders’ influences on corporate green innovation strategy: A case study of manufacturing firms in China. Corp. Soc. Resp. Env. Ma. 2013, 20, 1–14. [Google Scholar]

- Roy, M.; Khastagir, D. Exploring role of green management in enhancing organizational efficiency in petro-chemical industry in India. J. Clean. Prod. 2016, 121, 109–115. [Google Scholar] [CrossRef]

- Wang, N.; Zhang, J.; Zhang, X.; Wang, W. How to Improve Green Innovation Performance: A Conditional Process Analysis. Sustainability 2022, 14, 2938. [Google Scholar] [CrossRef]

- Li, D.; Zheng, M.; Cao, C.; Chen, X.; Ren, S.; Huang, M. The impact of legitimacy pressure and corporate profitability on green innovation: Evidence from China top 100. J. Clean. Prod. 2017, 141, 41–49. [Google Scholar] [CrossRef] [Green Version]

- Singh, S.K.; Del Giudice, M.; Chierici, R.; Graziano, D. Green innovation and environmental performance: The role of green transformational leadership and green human resource management. Technol. Forecast. Soc. 2020, 150, 119762. [Google Scholar] [CrossRef]

- Gupta, H.; Barua, M.K. Supplier selection among SMEs on the basis of their green innovation ability using BWM and fuzzy TOPSIS. J. Clean. Prod. 2017, 152, 242–258. [Google Scholar] [CrossRef]

- Huang, J.-W.; Li, Y.-H. Green innovation and performance: The view of organizational capability and social reciprocity. J. Bus. Ethics 2017, 145, 309–324. [Google Scholar] [CrossRef]

- Fazal-e-Hasan, S.M.; Ahmadi, H.; Sekhon, H.; Mortimer, G.; Sadiq, M.; Kharouf, H.; Abid, M. The role of green innovation and hope in employee retention. Bus. Strategy Environ. 2022, 1–20. [Google Scholar] [CrossRef]

- Weng, H.-H.; Chen, J.-S.; Chen, P.-C. Effects of green innovation on environmental and corporate performance: A stakeholder perspective. Sustainability 2015, 7, 4997–5026. [Google Scholar] [CrossRef] [Green Version]

- Wu, G.-C. The influence of green supply chain integration and environmental uncertainty on green innovation in Taiwan’s IT industry. Supply. Chain. Manag. 2013, 18, 539–552. [Google Scholar] [CrossRef]

- Kong, T.; Sun, R.; Sun, G.; Song, Y. Effects of digital finance on green innovation considering information asymmetry: An empirical study based on Chinese listed firms. Emerg. Mark. Financ. Trade 2022, 1–13. [Google Scholar] [CrossRef]

- Li, D.; Huang, M.; Ren, S.; Chen, X.; Ning, L. Environmental legitimacy, green innovation, and corporate carbon disclosure: Evidence from CDP China 100. J. Bus. Ethics 2018, 150, 1089–1104. [Google Scholar] [CrossRef]

- Huang, Z.; Liao, G.; Li, Z. Loaning scale and government subsidy for promoting green innovation. Technol. Forecast. Soc. 2019, 144, 148–156. [Google Scholar] [CrossRef]

- Hu, D.; Qiu, L.; She, M.; Wang, Y. Sustaining the sustainable development: How do firms turn government green subsidies into financial performance through green innovation? Bus. Strategy Environ. 2021, 30, 2271–2292. [Google Scholar] [CrossRef]

- Yi, Y.; Wei, Z.; Fu, C. An optimal combination of emissions tax and green innovation subsidies for polluting oligopolies. J. Clean. Prod. 2021, 284, 124693. [Google Scholar] [CrossRef]

- Zhang, S.; Yu, Y.; Zhu, Q.; Qiu, C.M.; Tian, A. Green innovation mode under carbon tax and innovation subsidy: An evolutionary game analysis for portfolio policies. Sustainability 2020, 12, 1385. [Google Scholar] [CrossRef] [Green Version]

- Yang, W.; Ma, Q.; He, J.; Lu, S.; Chen, X. Can green innovation subsidies reduce the systemic risk of green innovative enterprises? A simulation study. Technol. Anal. Strategy 2021, 1–17. [Google Scholar] [CrossRef]

- Wang, Y.; Yu, L. Can the current environmental tax rate promote green technology innovation?-Evidence from China’s resource-based industries. J. Clean. Prod. 2021, 278, 123443. [Google Scholar] [CrossRef]

- Guo, Y.; Xia, X.; Zhang, S.; Zhang, D. Environmental regulation, government R&D funding and green technology innovation: Evidence from China provincial data. Sustainability 2018, 10, 940. [Google Scholar]

- Long, S.; Liao, Z. Are fiscal policy incentives effective in stimulating firms’ eco-product innovation? The moderating role of dynamic capabilities. Bus. Strategy Environ. 2021, 30, 3095–3104. [Google Scholar] [CrossRef]

- De Azevedo, R.L.; Bansi, A.C.; Alves, M.F.R.; Galina, S.V.R. Take your time: Examining when green innovation affects financial performance in multinationals. J. Clean. Prod. 2019, 233, 993–1003. [Google Scholar]

- Chouaibi, S.; Chouaibi, J.; Rossi, M. ESG and corporate financial performance: The mediating role of green innovation: UK common law versus Germany civil law. Euromed. J. Bus. 2021, 17, 46–71. [Google Scholar] [CrossRef]

- Amore, M.D.; Bennedsen, M. Corporate governance and green innovation. J. Environ. Econ. Manag. 2016, 75, 54–72. [Google Scholar] [CrossRef]

- Zhou, X.; Yu, Y.; Yang, F.; Shi, Q. Spatial-temporal heterogeneity of green innovation in China. J. Clean. Prod. 2021, 282, 124464. [Google Scholar] [CrossRef]

- Li, D.; Zhao, Y.; Zhang, L.; Chen, X.; Cao, C. Impact of quality management on green innovation. J. Clean. Prod. 2018, 170, 462–470. [Google Scholar] [CrossRef]

- Yaoteng, Z.; Xin, L. Research on green innovation countermeasures of supporting the circular economy to green finance under big data. J. Enterp. Inf. Manag. 2021, 35, 1305–1322. [Google Scholar] [CrossRef]

- Woo, C.; Chung, Y.; Chun, D.; Han, S.; Lee, D. Impact of green innovation on labor productivity and its determinants: An analysis of the Korean manufacturing industry. Bus. Strategy Environ. 2014, 23, 567–576. [Google Scholar] [CrossRef]

- Majeed, A.; Ye, C.; Chenyun, Y.; Wei, X. Roles of natural resources, globalization, and technological innovations in mitigation of environmental degradation in BRI economies. PLoS ONE 2022, 17, e0265755. [Google Scholar] [CrossRef]

- Ahmad, M.; Majeed, A.; Khan, M.A.; Sohaib, M.; Shehzad, K. Digital financial inclusion and economic growth: Provincial data analysis of China. China Econ. J. 2021, 14, 291–310. [Google Scholar] [CrossRef]

{kind=link}

| Variable Type | Variable Name | Symbol | Calculation |

|---|---|---|---|

| Explained variable | Business Performance | Tobin’s Q | Tobin’s Q = year-end market value/book value of the business (%) |

| Explanatory variables | Green innovation | Gpatents | Number of green patent applications |

| Moderator | Financial subsidy | Sub | Government subsidy with one lag period in the statement (Yuan) |

| Tax incentives | Taxp | Income Tax Rate minus Effective Tax Rate (%) | |

| control variable | Company years | Age | Year of measurement minus A year of establishment (Years) |

| Enterprise size | Size | Total assets log (Yuan) | |

| capital concentration | INVE | Net Fixed Assets/Total Assets (%) | |

| company growth | Growth | operating income growth rate | |

| financial leverage | LEV | EBIT/EBIT (%) | |

| Operational efficiency | CE | Operating cost/operating income (%) | |

| Operating cash flow | CF | Net cash flow from operating activities/total assets (%) | |

| years | Year | control year |

| Variables | Obs | Average | S.D. | Min | Max |

|---|---|---|---|---|---|

| Tobin’s | 4039 | 2.712 | 1.71 | 0.776 | 21.476 |

| Gpatents | 4039 | 1.166 | 6.423 | 0 | 206 |

| Sub | 4039 | 0.228 | 0.658 | 0 | 16.877 |

| Taxp | 4039 | 0.067 | 0.371 | 0 | 14.482 |

| Age | 4039 | 13.515 | 5.099 | 2 | 35 |

| Size | 4039 | 3.27 | 0.935 | 0.778 | 7.573 |

| INVE | 4039 | 0.061 | 0.051 | 0 | 0.391 |

| Growth | 4039 | 0.302 | 1.653 | −1.243 | 62.182 |

| LEV | 4039 | 1.916 | 37.85 | −8.998 | 2402.774 |

| CE | 4039 | 0.906 | 0.112 | 0.37 | 3.739 |

| CF | 4039 | 0.043 | 0.063 | −0.319 | 0.372 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) |

|---|---|---|---|---|---|---|---|---|---|---|---|

| (1) Tobin’Q | 1 | ||||||||||

| (2) Gpatents | −0.058 *** | 1 | |||||||||

| (3) Sub | −0.053 *** | 0.385 *** | 1 | ||||||||

| (4) Taxp | 0.009 | −0.002 | 0.002 | 1 | |||||||

| (5) Age | 0.028 * | 0.033 ** | 0.030 * | 0.014 | 1 | ||||||

| (6) Size | −0.287 *** | 0.241 *** | 0.427 *** | 0.001 | 0.146 *** | 1 | |||||

| (7) INVE | −0.037 ** | 0.027 * | −0.035 ** | −0.026 * | −0.176 *** | −0.083 *** | 1 | ||||

| (8) Growth | 0.031 * | 0.008 | 0.022 | 0.003 | 0.006 | 0.046 *** | −0.037 ** | 1 | |||

| (9) LEV | −0.016 | 0.019 | −0.004 | 0.002 | −0.02 | 0.016 | −0.018 | −0.001 | 1 | ||

| (10) CE | −0.253 *** | 0.051 *** | 0.042 *** | 0.106 *** | 0.084 *** | 0.073 *** | −0.116*** | −0.003 | 0.022 | 1 | |

| (11) CF | 0.186 *** | −0.013 | 0.02 | −0.015 | 0.064 *** | 0.015 | 0.070 *** | −0.034 ** | −0.027 * | −0.276 *** | 1 |

| Variables | Tobin’s Q | |||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| Gpatents | 0.0065 *** | 0.0457 * | 0.0464 *** | 0.0469 * |

| (2.71) | (1.89) | (2.76) | (1.94) | |

| Sub | −0.1604 *** | −0.1611 *** | ||

| (−2.97) | (−2.98) | |||

| Gpatents × Sub | 0.0040 * | 0.0040 * | ||

| (1.72) | (1.70) | |||

| Taxp | −0.0242 *** | −0.0243 *** | ||

| (−3.12) | (−3.10) | |||

| Gpatents × Taxp | 0.0247 ** | 0.0245 ** | ||

| (2.54) | (2.52) | |||

| Age | 0.0665 *** | 0.0692 *** | 0.0678 *** | 0.0705 *** |

| (4.41) | (4.58) | (4.46) | (4.63) | |

| Size | −0.8865 *** | −0.8651 *** | −0.8899 *** | −0.8684 *** |

| (−10.69) | (−10.47) | (−10.68) | (−10.46) | |

| INVE | 1.2157 * | 1.2475 * | 1.2153 * | 1.2468 * |

| (1.72) | (1.76) | (1.71) | (1.75) | |

| Growth | 0.0234 * | 0.0233 * | 0.0234 * | 0.0233 * |

| (1.82) | (1.82) | (1.82) | (1.82) | |

| LEV | −0.0007 *** | −0.0007 *** | −0.0007 *** | −0.0007 *** |

| (−12.82) | (−12.44) | (−14.07) | (−13.61) | |

| CE | −1.7958 *** | −1.7846 *** | −1.7973 *** | −1.7862 *** |

| (−3.78) | (−3.79) | (−3.77) | (−3.78) | |

| CF | 0.9978 ** | 0.9978 ** | 0.9794 ** | 0.9791 ** |

| (2.13) | (2.13) | (2.08) | (2.08) | |

| Year | Yes | Yes | Yes | Yes |

| Constant | 5.5053 *** | 5.3808 *** | 5.5080 *** | 5.3745 *** |

| (13.03) | (12.67) | (13.02) | (12.64) | |

| Obs | 4039 | 4039 | 4031 | 4031 |

| R-squared | 0.4256 | 0.4271 | 0.426 | 0.4275 |

| Variables | Tobin’s Q |

|---|---|

| (1) | |

| Gpatents | 0.0262 *** |

| (1.92) | |

| Age | 0.0582 |

| (3.10) | |

| Size | −0.8280 |

| (−10.45) | |

| INVE | 3.2582 |

| (1.56) | |

| Growth | 0.0134 *** |

| (6.23) | |

| Lev | −0.0007 |

| (−13.06) | |

| CE | −2.0206 |

| (−3.53) | |

| CF | 1.0822 |

| (2.49) | |

| N | 3046 |

| AR(1) | 0.000 |

| AR(2) | 0.835 |

| Hansen | 0.326 |

| Variables | Replace Explained Variable | Substitution of Explanatory and Moderator Variables | ||||||

|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (1) | (2) | (3) | (4) | |

| Input | 0.0076 * | |||||||

| (1.93) | ||||||||

| Gpatents | 0.2667 *** | 0.3083 * | 1.5301 *** | 0.3823 ** | −0.0208 | −0.0315 | −0.0290 | |

| (3.11) | (1.85) | (16.67) | (2.46) | (−1.12) | (−1.61) | (−1.43) | ||

| Sub | −0.5128 *** | −0.4595 *** | −0.0817 *** | −0.0772 *** | ||||

| (−4.85) | (−4.63) | (−4.39) | (−4.11) | |||||

| Gpatents × Sub | 0.6879 *** | 0.5810 *** | 0.0067 *** | 0.0044 ** | ||||

| (10.27) | (8.76) | (4.25) | (2.33) | |||||

| Taxp | −0.7120 *** | 3.3829 *** | −0.0157 | 0.0061 | ||||

| (−10.31) | (39.48) | (−0.70) | (0.33) | |||||

| Gpatents × Taxp | 0.0179 | 0.0451 *** | 0.0050 *** | 0.0027 * | ||||

| (1.46) | (4.28) | (4.22) | (1.73) | |||||

| Controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Year | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Constant | −0.1943 *** | −0.7573 *** | 0.2691 *** | 1.0897 *** | 4.8333 *** | 4.7555 *** | 4.7990 *** | 4.7590 *** |

| (−0.11) | (−0.13) | (0.05) | (0.20) | (14.11) | (13.76) | (13.94) | (13.76) | |

| Obs | 12,938 | 12,835 | 12,938 | 12,570 | 10,680 | 10,680 | 10,680 | 10,680 |

| R-squared | 0.227 | 0.250 | 0.196 | 0.293 | 0.385 | 0.386 | 0.385 | 0.386 |

| Variables | High-Tech Manufacturing | Traditional Manufacturing | ||||||

|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (1) | (2) | (3) | (4) | |

| Gpatents | 0.006 ** | 0.040 ** | 0.024 ** | 0.039 ** | 0.004 ** | −0.179 | −0.033 | −0.246 * |

| (1.45) | (2.11) | (1.42) | (2.12) | (1.16) | (−1.65) | (−1.21) | (−1.79) | |

| Sub | −0.050* | −0.051 * | 0.048 | 0.049 | ||||

| (−1.70) | (−1.70) | (0.80) | (0.82) | |||||

| Gpatents × Sub | 0.021 * | 0.022 * | 0.047 * | 0.071 * | ||||

| (1.63) | (1.68) | (1.95) | (1.92) | |||||

| Taxp | 0.061 ** | 0.063 ** | −0.095 * | −0.102 * | ||||

| (2.06) | (2.08) | (−1.74) | (−1.86) | |||||

| Gpatents × Taxp | 0.045 ** | 0.047 ** | 0.044** | −0.033 | ||||

| (2.29) | (2.33) | (2.33) | (−1.19) | |||||

| Controls | control | control | control | control | control | control | control | control |

| Year | control | control | control | control | control | control | control | control |

| Constant | 4.766 *** | 4.730 *** | 4.694 *** | 4.654 *** | 4.518 *** | 4.648 *** | 4.450 *** | 4.565 *** |

| (7.51) | (7.62) | (7.41) | (7.52) | (5.57) | (6.07) | (5.54) | (6.04) | |

| Obs | 2484 | 2484 | 2457 | 2457 | 1 555 | 1 555 | 1 574 | 1 574 |

| R-squared | 0.446 | 0.448 | 0.449 | 0.450 | 0.354 | 0.355 | 0.355 | 0.356 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liang, H.; Li, G.; Zhang, W.; Chen, Z. The Impact of Green Innovation on Enterprise Performance: The Regulatory Role of Government Grants. Sustainability 2022, 14, 13550. https://doi.org/10.3390/su142013550

Liang H, Li G, Zhang W, Chen Z. The Impact of Green Innovation on Enterprise Performance: The Regulatory Role of Government Grants. Sustainability. 2022; 14(20):13550. https://doi.org/10.3390/su142013550

Chicago/Turabian StyleLiang, Hanyuan, Guangliang Li, Weikun Zhang, and Zhe Chen. 2022. "The Impact of Green Innovation on Enterprise Performance: The Regulatory Role of Government Grants" Sustainability 14, no. 20: 13550. https://doi.org/10.3390/su142013550