Unveiling the Direct Effects of Family Firm Heterogeneity on Environmental Performance

Abstract

:1. Introduction

2. Conceptual Framework

3. Hypotheses

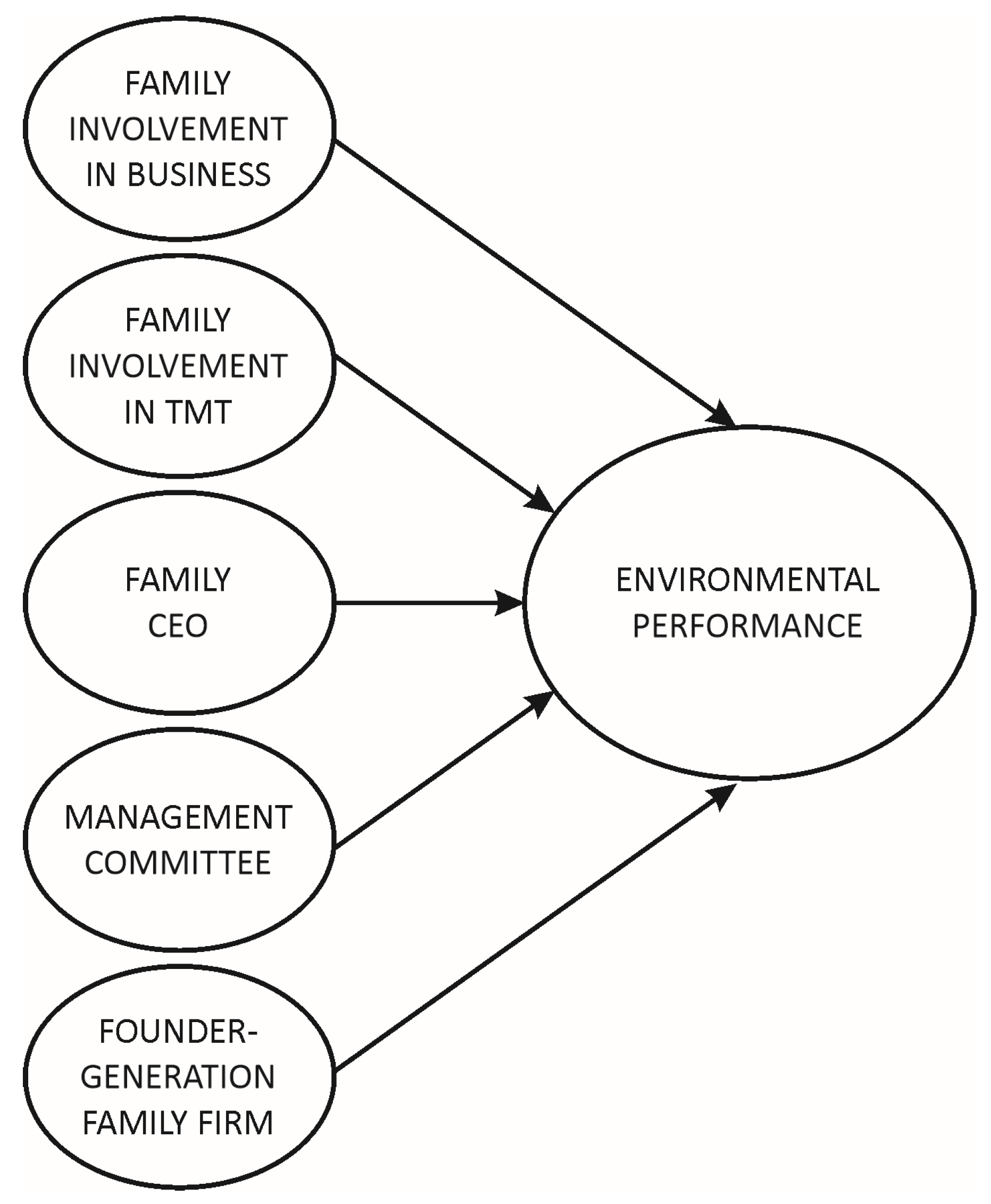

3.1. Family Involvement in the Business and in the Top Management Team (TMT), and Environmental Performance

3.2. Family Generation and Environmental Performance

3.3. Management Committee and Environmental Performance

4. Methodology

Sample and Data Collection

5. Variables

5.1. Dependent Variable: Environmental Performance

5.2. Independent Variables

5.3. Control Variables

6. Method of Analysis and Validity Tests

7. Results

8. Discussion

9. Conclusions, Limitations and Directions for Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Almgren, R.; Hjelm, O. Implementation of General Sustainability Objectives as Tools to Improve the Environmental Performance of Industry. Sustainability 2021, 13, 8144. [Google Scholar] [CrossRef]

- Fores, B. Beyond gathering the ‘low-hanging fruit’ of green technology for improved environmental performance: An empirical examination of the moderating effects of proactive environmental management and business strategies. Sustainability 2019, 11, 6299. [Google Scholar] [CrossRef] [Green Version]

- Aragón-Correa, J.A.; Sharma, S. A contingent resource-based view of proactive corporate environmental strategy. Acad. Manag. Rev. 2003, 28, 71–88. [Google Scholar] [CrossRef]

- Camisón-Zornoza, C. Effects of coercive regulation versus voluntary and cooperative auto-regulation on environmental adaptation and performance: Empirical evidence in Spain. Eur. Manag. J. 2010, 28, 346–361. [Google Scholar] [CrossRef]

- Hart, S.L. A natural-resource-based view of the firm. Acad. Manag. Rev. 1995, 20, 986–1014. [Google Scholar] [CrossRef] [Green Version]

- Barney, J. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Dierickx, I.; Cool, K. Asset stock accumulation and sustainability of competitive advantage. Manag. Sci. 1989, 35, 1504–1511. [Google Scholar] [CrossRef] [Green Version]

- Rumelt, R.P. Towards a strategic theory of the firm. In Competitive Strategic Management; Lamb, B., Ed.; Prentice Hall: Englewood Cliffs, NJ, USA, 1984; pp. 556–570. [Google Scholar]

- Weimann, V.; Gerken, M.; Hülsbeck, M. Business model innovation in family firms: Dynamic capabilities and the moderating role of socioemotional wealth. J. Bus. Econ. 2020, 90, 369–399. [Google Scholar] [CrossRef]

- Memili, E.; Dibrell, C. (Eds.) The Palgrave Handbook of Heterogeneity among Family Firms; Palgrave Macmillan: Cham, Switzerland, 2019. [Google Scholar]

- Gómez-Mejía, L.R.; Haynes, K.T.; Núñez-Nickel, M.; Jacobson, K.J.; Moyano-Fuentes, J. Socioemotional wealth and business risks in family-controlled firms: Evidence from Spanish olive oil mills. Adm. Sci. Q. 2007, 52, 106–137. [Google Scholar] [CrossRef] [Green Version]

- Brunninge, O.; Nordqvist, M. Ownership structure, board composition and entrepreneurship: Evidence from family firms and venture-capital-backed firms. Int. J. Entrep. Behav. Res. 2004, 10, 85–105. [Google Scholar] [CrossRef] [Green Version]

- Basco, R. Epilogue: The multiple embeddedness of family firms in the Arab world. In Family Businesses in the Arab World; Springer: Cham, Switzerland, 2017; pp. 247–256. [Google Scholar]

- Berrone, P.; Cruz, C.; Gomez-Mejia, L.R. Socioemotional wealth in family firms: Theoretical dimensions, assessment approaches, and agenda for future research. Fam. Bus. Rev. 2012, 25, 258–279. [Google Scholar] [CrossRef]

- Delmas, M.A.; Gergaud, O. Sustainable certification for future generations: The case of family business. Fam. Bus. Rev. 2014, 27, 228–243. [Google Scholar] [CrossRef] [Green Version]

- Le Breton-Miller, I.; Miller, D. Family firms and practices of sustainability: A contingency view. J. Fam. Bus. Strategy 2016, 7, 26–33. [Google Scholar] [CrossRef]

- Sharma, P.; Sharma, S. Drivers of proactive environmental strategy in family firms. Bus. Ethics Q. 2011, 21, 309–334. [Google Scholar] [CrossRef] [Green Version]

- Gomez-Mejia, L.R.; Lannelongue, G.; Muñoz-Bullón, F.; Requejo, I.; Sanchez-Bueno, M.J. Family firms’ concern for the environment: Does it pay off to pollute less? In Academy of Management Proceedings; Academy of Management: Boston, MA, USA, 2019. [Google Scholar]

- Kim, J.; Fairclough, S.; Dibrell, C. Attention, action, and greenwash in family-influenced firms? Evidence from polluting industries. Organ. Environ. 2017, 30, 304–323. [Google Scholar] [CrossRef]

- Berrone, P.; Cruz, C.; Gomez-Mejia, L.R.; Larraza-Kintana, M. Socioemotional wealth and corporate responses to institutional pressures: Do family-controlled firms pollute less? Adm. Sci. Q. 2010, 55, 82–113. [Google Scholar] [CrossRef]

- Barbaritano, M.; Savelli, E. Design and sustainability for innovation in family firms. A case study from the Italian furniture sector. Piccola Impresa/Small Bus. 2020, 1, 20–43. [Google Scholar]

- Abeysekera, A.P.; Fernando, C.S. Corporate social responsibility versus corporate shareholder responsibility: A family firm perspective. J. Corp. Finance 2020, 61, 101370. [Google Scholar] [CrossRef]

- Dal Maso, L.; Basco, R.; Bassetti, T.; Lattanzi, N. Family ownership and environmental performance: The mediation effect of human resource practices. Bus. Strategy Environ. 2020, 29, 1548–1562. [Google Scholar] [CrossRef]

- El Ghoul, S.; Guedhami, O.; Wang, H.; Kwok, C.C. Family control and corporate social responsibility. J. Bank. Financ. 2016, 73, 131–146. [Google Scholar] [CrossRef]

- Rees, W.; Rodionova, T. The influence of family ownership on corporate social responsibility: An international analysis of publicly listed companies. Corp. Gov. Int. Rev. 2015, 23, 184–202. [Google Scholar] [CrossRef]

- Villalonga, B.; Amit, R. How do family ownership, control and management affect firm value? J. Financ. Econ. 2006, 80, 385–417. [Google Scholar] [CrossRef] [Green Version]

- Kellermanns, F.W.; Eddleston, K.A.; Sarathy, R.; Murphy, F. Innovativeness in family firms: A family influence perspective. Small Bus. Econ. 2012, 38, 85–101. [Google Scholar] [CrossRef]

- Miroshnychenko, I.; De Massis, A.; Barontini, R.; Testa, F. Family firms and environmental performance: A meta-analytic review. Fam. Bus. Rev. 2022, 35, 68–90. [Google Scholar] [CrossRef]

- Heider, A.; Hülsbeck, M.; von Schlenk-Barnsdorf, L. The role of family firm specific resources in innovation: An integrative literature review and framework. Manag. Rev. Q. 2022, 72, 483–530. [Google Scholar] [CrossRef]

- Broccardo, L.; Truant, E.; Zicari, A. Internal corporate sustainability drivers: What evidence from family firms? A literature review and research agenda. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 1–18. [Google Scholar] [CrossRef] [Green Version]

- Kammerlander, N.; Ganter, M. An attention-based view of family firm adaptation to discontinuous technological change: Exploring the role of family CEOs’ noneconomic goals. J. Prod. Innov. Manag. 2015, 32, 361–383. [Google Scholar] [CrossRef]

- Sciascia, S.; Mazzola, P.; Kellermanns, F.W. Family management and profitability in private family-owned firms: Introducing generational stage and the socioemotional wealth perspective. J. Fam. Bus. Strategy 2014, 5, 131–137. [Google Scholar] [CrossRef]

- Forés, B.; Lara-Ortiz, M.L.; Ferreres, J.B.; Fernández-Yáñez, J.M. Los Objetivos de Desarrollo Sostenible en la Evolución del Turismo; Tirant Lo Blanch: Valencia, Spain, 2022. [Google Scholar]

- Niewiadomski, P. COVID-19: From temporary de-globalisation to a re-discovery of tourism? Tour. Geogr. 2020, 22, 651–656. [Google Scholar] [CrossRef]

- Lenzen, M.; Sun, Y.Y.; Faturay, F.; Ting, Y.P.; Geschke, A.; Malik, A. The carbon footprint of global tourism. Nat. Clim. Chang. 2018, 8, 522–528. [Google Scholar] [CrossRef]

- Arcese, G.; Valeri, M.; Poponi, S.; Elmo, G.C. Innovative drivers for family business models in tourism. J. Fam. Bus. Manag. 2020, 11, 402–422. [Google Scholar] [CrossRef]

- Memili, E.; Patel, P.C.; Koç, B.; Yazıcıoğlu, İ. The interplay between socioemotional wealth and family firm psychological capital in influencing firm performance in hospitality and tourism. Tour. Manag. Perspect. 2020, 34, 100651. [Google Scholar] [CrossRef]

- IEF, Instituto de Empresa Familiar (Spanish Family Firm Institute). 2022. Available online: https://www.iefamiliar.com/ (accessed on 15 March 2022).

- Fuetsch, E.; Suess-Reyes, J. Research on innovation in family businesses: Are we building an ivory tower? J. Fam. Bus. Manag. 2017, 7, 44–92. [Google Scholar] [CrossRef]

- Demil, B.; Lecocq, X. Business model evolution: In search of dynamic consistency. Long Range Plan. 2010, 43, 227–246. [Google Scholar] [CrossRef]

- Barney, J.B. Resource-based theories of competitive advantage: A ten-year retrospective on the resource-based view. J. Manag. 2001, 27, 643–650. [Google Scholar] [CrossRef]

- Peteraf, M.A. The cornerstones of competitive advantage: A resource-based view. Strateg. Manag. J. 1993, 14, 179–191. [Google Scholar] [CrossRef]

- Hart, S.L.; Dowell, G. Invited editorial: A natural-resource-based view of the firm: Fifteen years after. J. Manag. 2011, 37, 1464–1479. [Google Scholar] [CrossRef]

- Fama, E.F.; Jensen, M.C. Separation of ownership and control. J. Law Econ. 1983, 26, 301–325. [Google Scholar] [CrossRef]

- Jensen, M.C.; Meckling, W.H. Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Le Breton-Miller, I.; Miller, D. Why do some family businesses out–compete? Governance, long–term orientations, and sustainable capability. Entrep. Theory Pract. 2006, 30, 731–746. [Google Scholar] [CrossRef]

- Molly, V.; Laveren, E.; Deloof, M. Family business succession and its impact on financial structure and performance. Fam. Bus. Rev. 2010, 23, 131–147. [Google Scholar] [CrossRef]

- Han, J.; Lee, J.; Kim, S.J. How Does Family Involvement Affect Environmental Innovation? A Socioemotional Wealth Perspective. Sustainability 2021, 13, 13114. [Google Scholar] [CrossRef]

- Craig, J.; Dibrell, C. The natural environment, innovation, and firm performance: A comparative study. Fam. Bus. Rev. 2006, 19, 275–288. [Google Scholar] [CrossRef]

- Aiello, F.; Cardamone, P.; Mannarino, L.; Pupo, V. Green patenting and corporate social responsibility: Does family involvement in business matter? Corp. Soc. Responsib. Environ. Manag. 2021, 28, 1386–1396. [Google Scholar] [CrossRef]

- Ernst, R.A.; Gerken, M.; Hack, A.; Hülsbeck, M. Family firms as agents of sustainable development: A normative perspective. Technol. Forecast. Soc. Chang. 2022, 174, 121135. [Google Scholar] [CrossRef]

- Gersick, K.E.; Davis, J.A.; Hampton, M.M.; Lansberg, I. Generation to Generation, Life Cycles of the Family Business; Harvard Business School Press: Boston, MA, USA, 1997. [Google Scholar]

- Uhlaner, L.M.; Kellermanns, F.W.; Eddleston, K.A.; Hoy, F. The entrepreneuring family: A new paradigm for family business research. Small Bus. Econ. 2012, 38, 1–11. [Google Scholar] [CrossRef] [Green Version]

- Dekker, J.; Hasso, T. Environmental performance focus in private family firms: The role of social embeddedness. J. Bus. Ethics 2016, 136, 293–309. [Google Scholar] [CrossRef]

- Ward, J. Perpetuating the Family Business: 50 Lessons Learned from Long Lasting, Successful Families in Business; Springer: New York, NY, USA, 2016. [Google Scholar]

- Miller, D.; Le Breton-Miller, I. Managing for the Long Run: Lessons in Competitive Advantage from Great Family Businesses; Harvard Business Press: Boston, MA, USA, 2005. [Google Scholar]

- Le Breton-Miller, I.; Miller, D.; Lester, R.H. Stewardship or agency? A social embeddedness reconciliation of conduct and performance in public family businesses. Organ. Sci. 2011, 22, 704–721. [Google Scholar] [CrossRef]

- Villalonga, B.; Amit, R. How are US family firms controlled? Rev. Financ. Stud. 2009, 22, 3047–3091. [Google Scholar] [CrossRef] [Green Version]

- Lubatkin, M.H.; Durand, R.; Ling, Y. The missing lens in family firm governance theory: A self-other typology of parental altruism. J. Bus. Res. 2007, 60, 1022–1029. [Google Scholar] [CrossRef]

- Gomez-Mejia, L.R.; Makri, M.; Kintana, M.L. Diversification decisions in family-controlled firms. J. Manag. Stud. 2010, 47, 223–252. [Google Scholar] [CrossRef]

- Kellermanns, F.W.; Eddleston, K. Corporate venturing in family firms: Does the family matter? Entrep. Theory Pract. 2006, 30, 809–830. [Google Scholar] [CrossRef]

- Graafland, J. Family business ownership and cleaner production: Moderation by company size and family management. J. Clean. Prod. 2020, 255, 120120. [Google Scholar] [CrossRef]

- Campopiano, G.; De Massis, A.; Chirico, F. Firm philanthropy in small-and medium-sized family firms: The effects of family involvement in ownership and management. Fam. Bus. Rev. 2014, 27, 244–258. [Google Scholar] [CrossRef] [Green Version]

- Clark, R.; Reed, J.; Sunderland, T. Bridging funding gaps for climate and sustainable development: Pitfalls, progress and potential of private finance. Land Use Policy 2018, 71, 335–346. [Google Scholar] [CrossRef]

- Miller, D.; Le Breton-Miller, I. Deconstructing socioemotional wealth. Entrep. Theory Pract. 2014, 38, 713–720. [Google Scholar] [CrossRef] [Green Version]

- Mehrotra, V.; Morck, R.; Shim, J.; Wiwattanakantang, Y. Adoptive expectations: Rising sons in Japanese family firms. J. Financ. Econ. 2013, 108, 840–854. [Google Scholar] [CrossRef]

- Bertrand, M.; Schoar, A. The role of family in family firms. J. Econ. Perspect. 2006, 20, 73–96. [Google Scholar] [CrossRef] [Green Version]

- Bellow, A. In Praise of Nepotism: A Natural History; Doubleday: New York, NY, USA, 2003. [Google Scholar]

- Prendergast, C.; Topel, R.H. Favoritism in organizations. J. Political Econ. 1996, 104, 958–978. [Google Scholar] [CrossRef]

- Schulze, W.S.; Lubatkin, M.H.; Dino, R.N.; Buchholtz, A.K. Agency relationships in family firms: Theory and evidence. Organ. Sci. 2001, 12, 99–116. [Google Scholar] [CrossRef]

- Lubatkin, M.H.; Schulze, W.S.; Ling, Y.; Dino, R.N. The effects of parental altruism on the governance of family-managed firms. J. Organ. Behav. 2005, 26, 313–330. [Google Scholar] [CrossRef]

- Rondi, E.; De Massis, A.; Kraus, S. Servitization through open service innovation in family firms: Exploring the ability-willingness paradox. J. Bus. Res. 2021, 135, 436–444. [Google Scholar] [CrossRef]

- Pérez-González, F. Inherited control and firm performance. Am. Econ. Rev. 2006, 96, 1559–1588. [Google Scholar] [CrossRef] [Green Version]

- Basco, R.; Calabrò, A. Whom do I want to be the next CEO? Desirable successor attributes in family firms. J. Bus. Econ. 2017, 87, 487–509. [Google Scholar] [CrossRef]

- Scott-Young, C.M. Innovation in sustainable business practices: Greening the family firm. In Sustainable Business; Edward Elgar Publishing: Cheltenham, UK, 2013. [Google Scholar]

- Block, J.H.; Wagner, M. The effect of family ownership on different dimensions of corporate social responsibility: Evidence from large US firms. Bus. Strategy Environ. 2014, 23, 475–492. [Google Scholar] [CrossRef]

- Laguir, I.; Laguir, L.; Elbaz, J. Are family small-and medium-sized enterprises more socially responsible than nonfamily small-and medium-sized enterprises? Corp. Soc. Responsib. Environ. Manag. 2016, 23, 386–398. [Google Scholar] [CrossRef]

- Ioannou, I.; Serafeim, G. Corporate Sustainability: A Strategy? Harvard Business School Accounting & Management Unit Working Paper, 19-065; Harvard Business School Press: Boston, MA, USA, 2019. [Google Scholar]

- Tobak, J.; Nábrádi, A. The TONA model: A New methodology for assessing the development and maturity life cycles of family-owned enterprises. J. Innov. Knowl. 2020, 5, 236–243. [Google Scholar] [CrossRef]

- Arteaga, R.; Escribá-Esteve, A. Heterogeneity in family firms: Contextualising the adoption of family governance mechanisms. J. Fam. Bus. Manag. 2020, 11, 200–222. [Google Scholar] [CrossRef]

- Duran, P.; Kammerlander, N.; Van Essen, M.; Zellweger, T. Doing more with less: Innovation input and output in family firms. Acad. Manag. J. 2016, 59, 1224–1264. [Google Scholar] [CrossRef] [Green Version]

- Clauß, T.; Kraus, S.; Jones, P. Sustainability in family business: Mechanisms, technologies and business models for achieving economic prosperity, environmental quality and social equity. Technol. Forecast. Soc. Change 2022, 176, 121450. [Google Scholar] [CrossRef]

- Dick, M.; Wagner, E.; Pernsteiner, H. Founder-controlled family firms, overconfidence, and corporate social responsibility engagement: Evidence from survey data. Fam. Bus. Rev. 2021, 34, 71–92. [Google Scholar] [CrossRef]

- Marques, P.; Presas, P.; Simon, A. The heterogeneity of family firms in CSR engagement: The role of values. Fam. Bus. Rev. 2014, 27, 206–227. [Google Scholar] [CrossRef] [Green Version]

- Yang, B.; Nahm, A.; Song, Z. Succession, political resources, and innovation investments of family businesses: Evidence from China. Manag. Decis. Econ. 2022, 43, 321–338. [Google Scholar] [CrossRef]

- Camisón-Zornoza, C.; Forés, B.; Puig-Denia, A.; Camisón-Haba, S. Effects of ownership structure and corporate and family governance on dynamic capabilities in family firms. Int. Entrep. Manag. J. 2020, 16, 1393–1426. [Google Scholar] [CrossRef]

- Songini, L. The professionalization of family firms: Theory and practice. In Handbook of Research on Family Business; Edward Elgar: Cheltenham, UK, 2006; pp. 269–297. [Google Scholar]

- Pérez Rodríguez, M.J.; Basco, R.; García-Tenorio Ronda, J.; Giménez Sánchez, J.; Sánchez Quirós, I. Fundamentos en la Dirección de la Empresa Familiar: Emprendedor, Empresa y Familia; Editorial Paraninfo: Madrid, Spain, 2007. [Google Scholar]

- Gallo, M.A. Empresa Familiar: Textos y Casos; Praxis: Madrid, Spain, 1995. [Google Scholar]

- Sarkis, J.; Cordeiro, J.J. An empirical evaluation of environmental efficiencies and firm performance: Pollution prevention versus end-of-pipe practice. Eur. J. Oper. Res. 2001, 135, 102–113. [Google Scholar] [CrossRef]

- Hart, S.L.; Ahuja, G. Does it pay to be green? An empirical examination of the relationship between emission reduction and firm performance. Bus. Strategy Environ. 1996, 5, 30–37. [Google Scholar] [CrossRef]

- Van Essen, M.; Carney, M.; Gedajlovic, E.R.; Heugens, P.P. How does family control influence firm strategy and performance? A meta-analysis of US publicly listed firms. Corp. Gov. Int. Rev. 2015, 23, 3–24. [Google Scholar] [CrossRef]

- Anderson, R.C.; Reeb, D.M. Founding-family ownership, corporate diversification, and firm leverage. J. Law Econ. 2003, 46, 653–684. [Google Scholar] [CrossRef]

- Shanker, M.C.; Astrachan, J.H. Myths and realities: Family businesses’ contribution to the US economy—A framework for assessing family business statistics. Fam. Bus. Rev. 1996, 9, 107–123. [Google Scholar] [CrossRef]

- Handler, W.C. Methodological issues and considerations in studying family businesses. Fam. Bus. Rev. 1989, 2, 257–276. [Google Scholar] [CrossRef]

- Dillman, D.A. Mail and Telephone Surveys: The Total Design Method; John Wiley & Sons: New York, NY, USA, 1978. [Google Scholar]

- Zhu, Q.; Sarkis, J. The moderating effects of institutional pressures on emergent green supply chain practices and performance. Int. J. Prod. Res. 2007, 45, 4333–4355. [Google Scholar] [CrossRef]

- Lee, D. Implementation of collaborative activities for sustainable supply chain innovation: An analysis of the firm size effect. Sustainability 2019, 11, 3026. [Google Scholar] [CrossRef] [Green Version]

- Ong, T.S.; Lee, A.S.; Teh, B.H.; Magsi, H.B. Environmental innovation, environmental performance and financial performance: Evidence from Malaysian environmental proactive firms. Sustainability 2019, 11, 3494. [Google Scholar] [CrossRef] [Green Version]

- Singjai, K.; Winata, L.; Kummer, T.F. Green initiatives and their competitive advantage for the hotel industry in developing countries. Int. J. Hosp. Manag. 2018, 75, 131–143. [Google Scholar] [CrossRef]

- Hair, J.; Andreson, R.; Tatham, R.; Black, W. Multivariate Data Analysis, 5th ed.; Pearson Prentice-Hall: Hoboken, NJ, USA, 1998. [Google Scholar]

- Brown, T. Confirmatory Factor Analysis for Applied Research; The Guilford Press: New York, NY, USA, 2006. [Google Scholar]

- Chan, E.S.; Hawkins, R. Application of EMSs in a hotel context: A case study. Int. J. Hosp. Manag. 2012, 31, 405–418. [Google Scholar] [CrossRef]

- King, A.; Lenox, M. Exploring the locus of profitable pollution reduction. Manag. Sci. 2002, 48, 289–299. [Google Scholar] [CrossRef] [Green Version]

- Miles, R.E.; Snow, C.C.; Meyer, A.D.; Coleman, H.J., Jr. Organizational strategy, structure, and process. Acad. Manag. Rev. 1978, 3, 546–562. [Google Scholar] [CrossRef]

- Chan, E.S.; Okumus, F.; Chan, W. Barriers to environmental technology adoption in hotels. J. Hosp. Tour. Res. 2018, 42, 829–852. [Google Scholar] [CrossRef]

- Crosby, P.B. Quality Is Free. The Art of Making Quality Certain; McGraw-Hill: New York, NY, USA, 1979. [Google Scholar]

- Broekaert, W.; Andries, P.; Debackere, K. Innovation processes in family firms: The relevance of organizational flexibility. Small Bus. Econ. 2016, 47, 771–785. [Google Scholar] [CrossRef]

- Zahra, S.A.; Hayton, J.C.; Neubaum, D.O.; Dibrell, C.; Craig, J. Culture of family commitment and strategic flexibility: The moderating effect of stewardship. Entrep. Theory Pract. 2008, 32, 1035–1054. [Google Scholar] [CrossRef]

- Podsakoff, P.M.; MacKenzie, S.B.; Lee, J.Y.; Podsakoff, N.P. Common method biases in behavioral research: A critical review of the literature and recommended remedies. J. Appl. Psychol. 2003, 88, 879. [Google Scholar] [CrossRef]

- Cohen, P.; Cohen, J.; West, S.G.; Aiken, L.S. Applied Multiple Regression/Correlation Analysis for the Behavioral Sciences, 3rd ed.; Lawrence Erlbaum Mahwah: Mahwah, NJ, USA, 2003. [Google Scholar]

- Aiken, L.S.; West, S.G.; Reno, R.R. Multiple Regression: Testing and Interpreting Interactions; Sage: New York, NY, USA, 1991. [Google Scholar]

- Siemsen, E.; Roth, A.; Oliveira, P. Common method bias in regression models with linear, quadratic, and interaction effects. Organ. Res. Methods 2010, 13, 456–476. [Google Scholar] [CrossRef]

- Memili, E.; Fang, H.C.; Koc, B.; Yildirim-Öktem, Ö.; Sonmez, S. Sustainability practices of family firms: The interplay between family ownership and long-term orientation. J. Sustain. Tour. 2017, 26, 9–28. [Google Scholar] [CrossRef] [Green Version]

- Samara, G.; Jamali, D.; Sierra, V.; Parada, M.J. Who are the best performers? The environmental social performance of family firms. J. Fam. Bus. Strategy 2018, 9, 33–43. [Google Scholar] [CrossRef]

- Rondi, E.; De Massis, A.; Kotlar, J. Unlocking innovation potential: A typology of family business innovation postures and the critical role of the family system. J. Fam. Bus. Strategy 2019, 10, 100236. [Google Scholar] [CrossRef]

- Lumpkin, G.T.; Dess, G.G. Clarifying the entrepreneurial orientation construct and linking it to performance. Acad. Manag. Rev. 1996, 21, 135–172. [Google Scholar] [CrossRef]

- Becerra, M.; Cruz, C.; Graves, C. Innovation in family firms: The relative effects of wealth concentration versus family-centered goals. Fam. Bus. Rev. 2020, 33, 372–392. [Google Scholar] [CrossRef]

- Hang, M.; Geyer-Klingeberg, J.; Rathgeber, A.W. It is merely a matter of time: A meta-analysis of the causality between environmental performance and financial performance. Bus. Strategy Environ. 2018, 28, 257–273. [Google Scholar] [CrossRef]

- Aguilera, R.V.; Aragón-Correa, J.A.; Marano, V.; Tashman, P.A. The corporate governance of environmental sustainability: A review and proposal for more integrated research. J. Manag. 2021, 47, 1468–1497. [Google Scholar]

- Tabor, W.; Chrisman, J.J.; Madison, K.; Vardaman, J.M. Nonfamily members in family firms: A review and future research agenda. Fam. Bus. Rev. 2018, 31, 54–79. [Google Scholar] [CrossRef] [Green Version]

- Campopiano, G.; De Massis, A. Corporate social responsibility reporting: A content analysis in family and non-family firms. J. Bus. Ethics 2015, 129, 511–534. [Google Scholar] [CrossRef]

- Gjergji, R.; Vena, L.; Sciascia, S.; Cortesi, A. The effects of environmental, social and governance disclosure on the cost of capital in small and medium enterprises: The role of family business status. Bus. Strategy Environ. 2021, 30, 683–693. [Google Scholar] [CrossRef]

- Neubaum, D.O.; Dibrell, C.; Craig, J.B. Balancing natural environmental concerns of internal and external stakeholders in family and non-family businesses. J. Fam. Bus. Strategy 2012, 3, 28–37. [Google Scholar] [CrossRef]

{kind=link}

| PCA | CFA | |||||

|---|---|---|---|---|---|---|

| Item | Factor Loading | Eigen Value | Percentage of Variance Explained | Robust Standardized Loading | z | p > |z| |

| EP1 | 0.838 | 3.542 | 70.836 | 0.819 | 31.97 | 0.000 |

| EP2 | 0.879 | 0.870 | 46.93 | 0.000 | ||

| EP3 | 0.829 | 0.756 | 31.85 | 0.000 | ||

| EP4 | 0.823 | 0.750 | 27.59 | 0.000 | ||

| EP5 | 0.837 | 0.758 | 26.40 | 0.000 | ||

| VARIABLES | μ | σ² | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 | 19 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. ENVPERF | 3.678 | 1.366 | 1 | ||||||||||||||||||

| 2. HOTEL | 0.306 | 0.461 | 0.125 *** | 1 | |||||||||||||||||

| 3. RESTA | 0.406 | 0.491 | −0.138 *** | −0.550 *** | 1 | ||||||||||||||||

| 4. TOUR | 0.097 | 0.296 | 0.096 *** | −0.218 *** | −0.272 *** | 1 | |||||||||||||||

| 5. TRANSP | 0.044 | 0.205 | 0.089 *** | −0.143 *** | −0.178 *** | −0.071 ** | 1 | ||||||||||||||

| 6. SIZE | 28.567 | 127.824 | 0.091 *** | 0.090 *** | −0.051 * | −0.020 | −0.008 | 1 | |||||||||||||

| 7. GROUP | 0.204 | 0.402 | 0.018 | 0.036 | −0.108 *** | 0.124 *** | 0.069 ** | 0.042 | 1 | ||||||||||||

| 8. HIERARCHY | 1.816 | 0.914 | 0.001 | 0.171 *** | −0.074 ** | −0.034 | −0.027 | 0.207 *** | 0.145 *** | 1 | |||||||||||

| 9. AGE | 19,618 | 20.616 | 0.086 *** | 0.142 *** | −0.040 | −0.079 ** | 0.007 | 0.003 | 0.010 | 0.049 * | 1 | ||||||||||

| 10. ROS | 3.877 | 0.970 | 0.132 *** | 0.099 *** | −0.098 *** | 0.048 * | 0.018 | 0.073 ** | 0.083 ** | 0.070 ** | 0.054 * | 1 | |||||||||

| 11. NQUACOST | 3.820 | 7.090 | −0.019 | 0.032 | −0.049 * | 0.095 *** | 0.046 | 0.005 | 0.075 ** | 0.073 ** | −0.006 | 0.015 | 1 | ||||||||

| 12. DEF | 0.342 | 0.474 | −0.092 *** | −0.057 * | 0.097 *** | −0.009 | −0.004 | 0.021 | 0.020 | −0.023 | 0.023 | −0.044 | 0.091 *** | 1 | |||||||

| 13. PROS | 0.068 | 0.252 | 0.084 ** | 0.131 *** | −0.094 *** | 0.018 | −0.058 * | −0.013 | 0.073 ** | 0.049 * | −0.015 | 0.079 ** | 0.079 ** | −0.195 *** | 1 | ||||||

| 14. ANAL | 0.346 | 0.476 | 0.156 *** | 0.053 * | 0.016 | −0.012 | 0.049 * | 0.012 | 0.064 ** | 0.100 *** | −0.066 ** | 0.079 ** | −0.044 | −0.525 *** | −0.197 *** | 1 | |||||

| 15. INVOLTMT | 0.913 | 0.246 | −0.128 *** | −0.201 *** | 0.117 *** | 0.109 *** | −0.041 | −0.014 | −0.036 | −0.117 *** | 0.150 *** | −0.019 | −0.138 *** | −0.024 | −0.006 | −0.068 ** | 1 | ||||

| 16. INVOLB | 0.430 | 0.297 | −0.170 *** | −0.214 *** | 0.165 *** | −0.020 | −0.038 | −0.017 | −0.167 *** | −0.215 *** | 0.199 *** | −0.142 *** | −0.039 | 0.077 ** | −0.124 *** | −0.094 *** | 0.260 *** | 1 | |||

| 17. FCEO | 0.936 | 0.242 | −0.104 *** | −0.213 *** | 0.137 *** | 0.030 | 0.003 | −0.002 | −0.183 *** | −0.077 ** | 0.044 | −0.045 | −0.012 | 0.036 | −0.017 | −0.055 * | 0.087 *** | 0.127 *** | 1 | ||

| 18. MANCOMM | 0.236 | 0.319 | 0.173 *** | 0.170 *** | −0.131 *** | 0.046 | 0.050 * | 0.140 *** | 0.189 *** | 0.211 *** | −0.049 * | 0.091 *** | 0.087 *** | 0.017 | 0.056 * | 0.070 ** | −0.100 *** | −0.213 *** | −0.154 *** | 1 | |

| 19. FOUNGEN | 0.768 | 0.42194 | −0.202 *** | −0.207 *** | 0.157 *** | 0.031 | 0.010 | −0.040 | −0.085 ** | −0.091 *** | 0.322 *** | −0.057 * | 0.051 * | 0.055 * | −0.015 | −0.067 ** | 0.147 *** | 0.170 *** | 0.119 *** | −0.231 *** | 1 |

| Model I | Model II | Collinearity | |||||

|---|---|---|---|---|---|---|---|

| (1) | (2) | (1) | (2) | Tolerance | VIF | ||

| Constant | 12.418 ***(3) | 2.644 | 5.156(3) | 1.065 | |||

| Control Variables | |||||||

| 1 | HOTEL | 0.148 *** | 2.782 | 0.089 * | 1.681 | 0.416 | 2.405 |

| 2 | RESTA | 0.017 | 0.321 | 0.033 | 0.632 | 0.425 | 2.352 |

| 3 | TOUR | 0.151 *** | 3.466 | 0.150 *** | 3.498 | 0.630 | 1.586 |

| 4 | TRANSP | 0.124 *** | 3.128 | 0.112 *** | 2.901 | 0.776 | 1.289 |

| 5 | SIZE | 0.087 ** | 2.432 | 0.084 ** | 2.388 | 0.936 | 1.068 |

| 6 | GROUP | −0.035 | −0.959 | −0.074 ** | −2.036 | 0.883 | 1.132 |

| 7 | HIERARCHY | −0.057 | −1.554 | −0.093 ** | −2.540 | 0.865 | 1.157 |

| 8 | AGE | −0.073 ** | 2.039 | −0.007 | 0.189 | 0.849 | 1.178 |

| 9 | ROS | 0.093 *** | 2.616 | 0.075 ** | 2.137 | 0.944 | 1.059 |

| 10 | NQUACOST | −0.043 | −1.210 | −0.048 | −1.364 | 0.933 | 1.072 |

| 11 | DEF | 0.041 | 0.909 | 0.034 | 0.767 | 0.594 | 1.684 |

| 12 | PROS | 0.116 *** | 2.941 | 0.108 *** | 2.811 | 0.783 | 1.277 |

| 13 | ANAL | 0.181 *** | 3.964 | 0.160 *** | 3.578 | 0.581 | 1.720 |

| Explanatory Variables | |||||||

| 1 | INVOLTMT | −0.076 ** | −2.076 | 0.863 | 1.159 | ||

| 2 | INVOLB | −0.076 ** | −1.985 | 0.799 | 1.252 | ||

| 3 | FCEO | −0.057 | −1.581 | 0.909 | 1.100 | ||

| 4 | FOUNGEN | −0.136 *** | −3.588 | 0.812 | 1.231 | ||

| 5 | MANCOMM | 0.087 ** | 2.334 | 0.835 | 1.198 | ||

| F | 6.450 *** | 7.192 *** | |||||

| R2 | 0.103 | 0.151 | |||||

| Adjusted R2 | 0.087 | 0.130 | |||||

| Changes in R2 | - | 0.048 | |||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Forés, B.; Fernández-Yáñez, J.M.; Puig-Denia, A.; Boronat-Navarro, M. Unveiling the Direct Effects of Family Firm Heterogeneity on Environmental Performance. Sustainability 2022, 14, 10442. https://doi.org/10.3390/su141610442

Forés B, Fernández-Yáñez JM, Puig-Denia A, Boronat-Navarro M. Unveiling the Direct Effects of Family Firm Heterogeneity on Environmental Performance. Sustainability. 2022; 14(16):10442. https://doi.org/10.3390/su141610442

Chicago/Turabian StyleForés, Beatriz, José María Fernández-Yáñez, Alba Puig-Denia, and Montserrat Boronat-Navarro. 2022. "Unveiling the Direct Effects of Family Firm Heterogeneity on Environmental Performance" Sustainability 14, no. 16: 10442. https://doi.org/10.3390/su141610442