2. Materials and Methods

2.1. Data Collection, Processing, and Limitations

Poland was selected for the study, utilising a purposive selection method. It is one of the largest countries in the European Union, with an excellent geographical location in Europe. There are many global logistics companies in this country. Logistics is also developing rapidly. Poland already fulfils vital functions in Central and Eastern Europe and could become Europe’s most important logistics hub in the future. The research period covered the years 2015–2021. The adoption of such a period is substantively justified. By 2019, changes in logistics activities resulting from the normal functioning of the economy can be observed. In 2020, there was an economic crisis caused by the COVID-19 pandemic. The European continent was quite severely affected by COVID-19. The last year in which complete research data were available was 2021. In addition, it was the second year of the COVID-19 pandemic.

The data used in the study come from several sources. Logistics activities in Poland are not studied comprehensively by one unit. The results are scattered over several research units. Data collection is limited by the lack of detailed and up-to-date information on comprehensive logistics activities. Data are often not aggregated at the country level but relate to individual areas of logistics activity, so there is a problem in performing this type of analysis. The following data sources were used:

Rankings of TSL companies are published annually by Dziennik Gazeta Prawna (Dziennik Gazeta Prawna is a nationwide legal and economic journal published by the Polish company Infor Biznes. It is published five times a week, from Monday to Friday. Every year in June, Gazeta publishes the TSL Companies Ranking. The ranking of TSL companies is prepared on the basis of an on-line survey. Substantive supervision is carried out by the student—Warsaw School of Economics. In 2022, the 27th ranking was already published.). The ranking annually takes into account approximately 70 largest logistics companies in Poland. Including a company in the ranking is to have revenue from the core TSL activity of at least PLN 2 million (approx. EUR 450 thousand). This revenue should represent at least 51% of the total revenue for the company;

Reports on the Polish warehouse market published annually by AXI IMMO Group (AXI IMMO Group is a leader among Polish consulting companies providing comprehensive services on the commercial real estate market. One of the areas of activity is the creation of reports and publications on the commercial real estate market, including warehouse market. Reports of this kind have been produced since 2011.);

Reports on the state of the postal market published annually by the Office of Electronic Communications;

Yearbooks entitled Transport-activity results (Transport-activity results is publication containing basic data on the results of the transport sector activity. The aim of this publication is to present the aspects (economic and infrastructural) that determine the development of the sector and its operational activity. Reports have been published since 2002.) published annually by Statistics Poland.

In addition to the presented sources of numerical data, other sources were used concerning the results of research already carried out and the regularities occurring in the industry. Literature in the form of books, articles in scientific and popular magazines, industry reports, and articles in portals dealing with logistics topics was used.

The study is the result of the author’s previous research on logistics. More recently, the authors’ field of interest has been the impact of COVID-19 on the situation in various sectors of the economy. The two areas are closely linked as, without efficient logistics, the economy could not function smoothly during the pandemic. All the authors are economists. Therefore, an aspect related to economics was raised. In addition, attention was drawn to the lack of up-to-date scientific studies on the relationship between the functioning of logistics in Poland and economic development.

2.2. Applied Methods

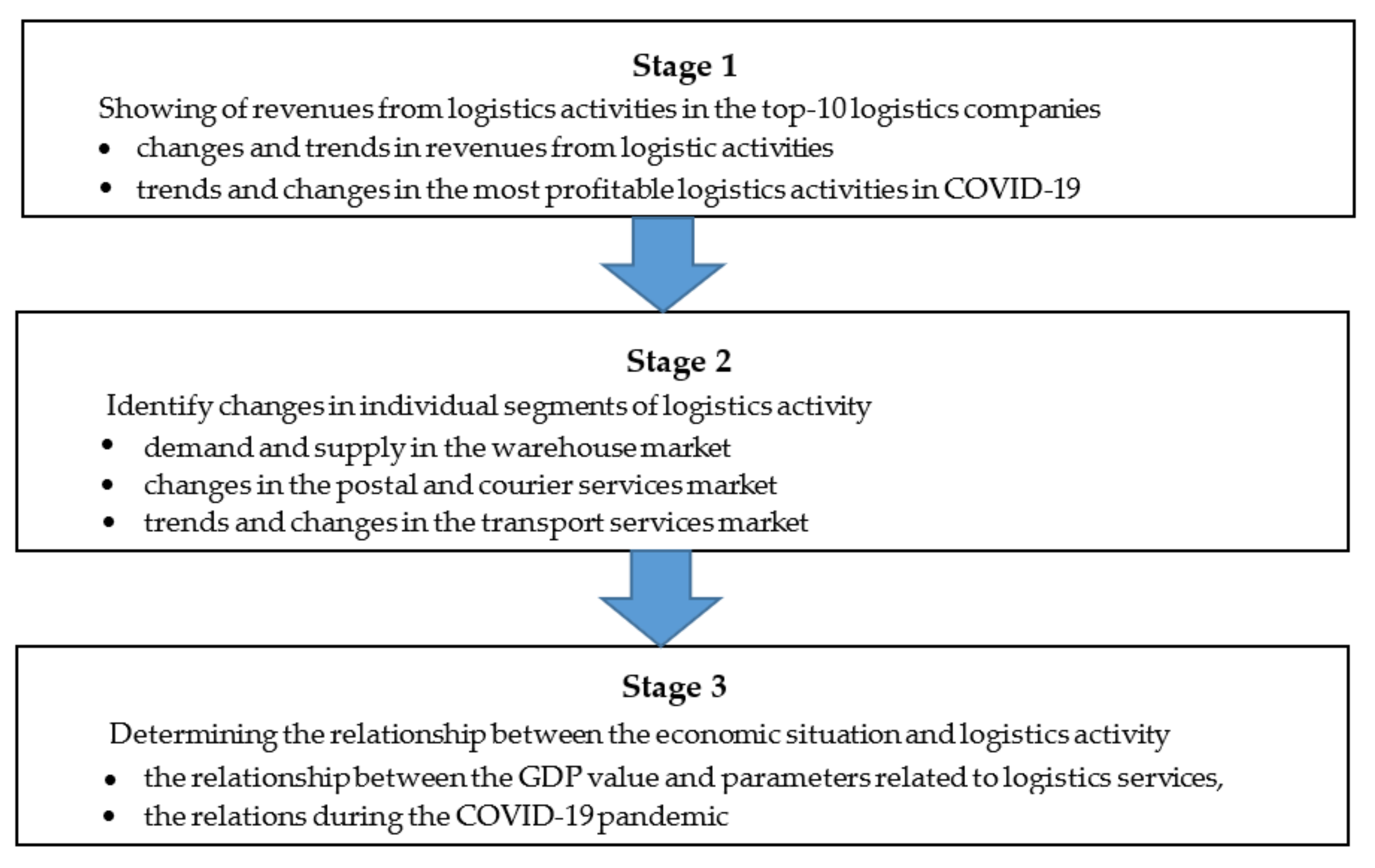

The research was divided into stages.

Figure 1 shows a diagram of the conducted research.

The first stage of the research presented the situation in Poland before and during the COVID-19 pandemic (2015–2021) in terms of the top logistics companies’ revenues. Such data made it possible to identify changes in logistics activities. These changes can happen because the top companies set the direction of change and provide a barometer of the situation in the industry. For this purpose, chained and fixed-base dynamic indicators were used. The coefficients of variation were used to show the variability in individual periods. The analyses presented were supplemented by listing the top 10 companies in revenue dynamics in the years in question. In this case, it was possible to identify changes based on the fastest-growing companies. This also made it possible to compare the situation and growth opportunities before COVID-19 and during the pandemic. In addition, it was determined which logistics business segments developed best in the different periods. This section aimed to show the directions of change and the actual leaders in the logistics business in Poland in the period before and during the pandemic.

The second step of the research presents the results for the individual segments of the logistics services market. In the first step, the situation in the warehouse space market was shown, which was the segment particularly affected by the pandemic; however, the effects were positive. The focus was on the basic parameters related to the market, such as demand and supply and the most important indicators. Changes were shown through chained and fixed-base dynamic indicators. As a result, the directions and strength of the analysed variables were obtained. Fixed-base dynamics indicators were calculated for the three periods 2015–2019, 2015–2020, and 2015–2021. This will allow the impact of COVID-19 on changes in the first and second years of the pandemic to be determined. In a second step, postal services were addressed. Among these, courier services and postal parcels are the most important. Calculations were made for the dynamics of individual value and quantity parameters. As before, two dynamics indicators were used to determine the strength and direction of change, particularly during the COVID-19 period. This section additionally presents the structure of the services and their change over the years. The section also identifies the changes that have taken place in the market. The key logistics area, transport, was addressed in a third step. Similarly, research was carried out into the changes in the value of revenue generated, the number of transport work carried out, and the number of freight and passengers transported. Identical to the previous logistics business segments, two types of dynamic indicators were calculated. The patterns occurring, the strength, and directions of change in transport activity were identified. This way, comparisons were made between periods before and during the pandemic.

In this paper, the chain simple dynamic indicators were used as follows [

37]:

where:

yt—level of the phenomenon in a certain period,

yt−1—level of the phenomenon during one period earlier.

The dynamics indices with a constant base were used for the research too. The constant-based dynamics index has the following formula [

37]:

where:

yn—the level of the phenomenon in a certain period,

y0—level of the phenomenon during the reference period.

The variation coefficient marked as

Cv eliminates the assessment unit from the standard deviation of a set of digits. It is done by obtaining the quotient of standard deviation divided by the arithmetic mean. Formally, for the sequence of N numbers, the variation coefficient is calculated as follows [

38]:

where:

S—standard deviation from the exemplar set of numbers,

M—arithmetic mean of the exemplar set of numbers.

The third stage of the research concerns the determination of the relationship between the value of GDP and changes in individual parameters concerning the logistics services market in general and its most important segments. The logistics parameters and indicators presented in the first and second stages of the research were used. A total of 28 parameters and indicators relating to logistics activities and their segments were used. For the economic situation, one parameter was used, i.e., GDP. Tests performed with other parameters concerning the economy (domestic demand, total consumption including households, value of exports and imports) gave similar results. Therefore, it was decided to present only the result for the value of GDP. The tests were performed for the three periods 2015–2019, 2015–2020, and 2015–2021. This will allow the impact of the pandemic on the results achieved to be determined. The logic for performing the tests for the different periods was the same as for the momentum indicators. The non-parametric test will make it possible to check the interdependencies that exist and answer the question: is logistics developing interdependently with the economy, or are there differences in this respect between segments of the logistics business? Of particular interest are the changes that have occurred due to the pandemic. With this study, it is possible to determine the importance of the parameters and the strength of their association with economic prosperity before and during the COVID-19 pandemic. In this project phase, a non-parametric test was applied to define the correlation between the variables. Kendall’s tau correlation coefficient was used. It is established on the difference between the probability that two variables fall in the same sequence (for the interpreted data) and the probability that these factors are different. This coefficient fluctuates in the range of values <−1, 1>. Value 1 means complete match, value 0 indicates no match of order, and value −1 indicates the complete opposite. The Kendall coefficient suggests not only the robustness but also the direction of the interdependence. It is a valuable tool for representing the similarity of the ordered data sets. The following formula can be used to calculate Kendall’s tau correlation coefficient [

39]:

where:

—concordance probability, i.e., the probability that random variables X and Y move in one direction (increase or decrease),

—the probability of nonconformity, i.e., the probability that the random variables X and Y move in the opposite direction.

The given formula evaluates Kendall’s tau based on a statistical sample. First, all possible pairs of the observed population are combined. Next, the pairs are split into three possible units:

P-compatible pairs, when the analysed factors within two observations fluctuate in the same trend, i.e., either in the first observation both are higher than in the second, or both are less significant,

Q-incompatible pairs, when the factors differ against each other in the opposite trend, i.e., one of them is more significant for this observation in the pair, while the other is smaller,

T-related pairs in the case of one of the variables having equal values in both observations.

The Kendall tau coefficient is then calculated from the following formula:

The pattern can be quantified as:

Descriptive, tabular, and graphic methods were also used to present some of the findings.

4. Discussion

The evaluation of logistics activities and changes in the COVID-19 result did not apply to all segments. There is a great deal of research on the transport segment. For example, Arellana et al. [

40] studied the seven most populated cities in Colombia, analysing the impact on three elements of the transport system: air transport, freight transport, and urban transport. In the first months of the pandemic, only freight transport increased, while passenger transport was reduced. The same results were obtained in our study. The same three transport systems were studied by Munawar et al. [

41], using Australia as an example. In the early stages of the pandemic, revenue declines were found in the transport industry’s air, public transport, and freight sectors. The first two systems involved passenger transport, and the last involved freight. In general, there is a great deal of research on the negative consequences of passenger transport, such as Li et al. [

42] on the situation of passenger air transport worldwide, which was closely related to the rate of disease increase. Similar results were obtained by Sun et al. [

43,

44] for the world as a whole and by Linka et al. [

45,

46] for European countries. Rahman and Thill [

47] confirmed the patterns occurring based on studies on 86 countries. A higher number of confirmed COVID-19 cases and deaths reduced human mobility. In our study, similar results were obtained for passenger transport. In addition, the first year of the pandemic was the most difficult, while adaptation measures were introduced in the second year, which allowed partial recovery of lost passenger transport. Łącka and Suproń [

48] examined the impact of the COVID-19 pandemic on the Polish road freight transport industry. They found that the imposition of the blockade on the European economy had a negative impact on the short-term activities of transport companies. On the other hand, the number of road kilometres travelled by the surveyed companies increased following the reduction of infections and the subsequent reduction of restrictions. This increase was higher than in the corresponding periods of previous years. In turn, Periokaitė and Dobrovolskienė [

49] found that in Lithuania, road transport companies experienced a decrease in profitability rates during the first wave of COVID-19. In our study, we obtained similar results. Freight transport was stagnant in the first year of the pandemic, which could be due to this short-lived decrease in the initial months of 2020. In the following months, there was an increase. As a result, there was a slight increase in 2020. A decline in revenue profitability was also found in road transport companies in the first year of the pandemic. In the following year, increases in transport work were already higher. Alaimo et al. [

50] and Chang and Meyerhoefer [

51] found that there was a change in shopping habits and preferences, which became a growth opportunity for transport companies due to the increased interest in the e-commerce industry. Our research also points to the strong growth of the e-commerce industry in Poland. The consequence of this is an increase in demand for warehouse space. Sansa [

52] and Ghazanfari [

53] pointed to the drop in fuel prices on global markets, which also supported road freight transport. Similar observations were confirmed by Osińska and Zalewski [

54] with regard to the Polish road freight market. Demand shocks caused by operating restrictions in other sectors, on the other hand, were a threat. On the other hand, Ivanov and Dolgui [

55] concluded that demand for certain products increased dramatically in a pandemic. Such regularities may be an explanation for our research results. We found that revenues were maintained during the first year of the pandemic in the road freight transport industry.

The growth of the e-commerce market has occurred in virtually all countries. There are many examples of studies on this market in Croatia [

56], Saudi Arabia [

57], Italy [

58], and Germany [

59]. Overall, it can be said that it was a global trend. In 2020, global e-commerce sales increased by 19% compared to a year earlier [

60]. Abdelrhim and Elsayed [

61] studied the impact of COVID-19 on global e-commerce companies, where the five largest e-commerce companies in the world were selected in terms of revenue and market value. They confirmed a large impact of the pandemic on their financial performance. However, everything depended on the severity of COVID-19, with online purchases also increasing during the increased incidence. Associated with the growth of e-commerce is an increase in demand for warehouse space. This area is very poorly covered in the literature. We found only a few articles, making our study all the more valuable. Kaur et al. [

62] point to the inadequate number of warehouses in India serving major cities and supplying food. The greater need is due to demand and supply shocks created by the pandemic. New warehouses needed to be built, the location of which would reduce transport costs. Information on the warehouse segment is presented in industry reports. In the USA, for example, retailers accelerated investment in warehouses to sell goods stored on their websites. Demand for warehouse space and logistics centres has increased tremendously, which has also influenced rental prices [

63]. Prologis, the global leader in logistics real estate, also points to the increased interest in renting warehouses. As a result of the pandemic, demand for warehouses and distribution centres has increased, as consumers’ shopping habits have changed and manufacturers and retailers are adapting to changing demands [

64]. Similar results were obtained in our study. A boom in warehouse space was observed in 2020, but demand was partially realised in 2021. Indeed, investments in warehouses take time.

Based on the Philippine market, Dones and Young [

65] found that the demand for courier services has increased significantly due to the threat of the COVID-19 pandemic. Demand is always followed by supply, which means that courier companies can fulfil the reported service needs. Courier services provide delivery of virtually any type of goods. Izzah [

66], in a Malaysian market study, found a significant relationship between courier companies and e-business companies. In addition, logistics companies have contributed to the emergence of new services developed specifically for critical situations such as COVID-19. The pandemic has also accelerated the trend towards widespread digitisation. On the other hand, the professionalisation of logistics customer service requires standardisation to ensure both the distinction of the company and the distinction of the services offered by the company [

67]. In turn, standardisation enables the digitisation and automation of processes [

68]. COVID-19 also contributed to an increase in customer needs and expectations in terms of ease of purchase and greater flexibility. New solutions allowed the selection of additional delivery features such as place, time, delivery date and payment method [

69]. Such solutions have led to the emergence of multiple sales channels. The pandemic accelerated this phenomenon [

70]. In our research, we obtained similar patterns in developing general courier services and logistics services. There is a worldwide shift away from traditional postal services. In Malaysia, for example, lower demand for letter mail and higher operating costs were indicated. For this reason, public operators are focusing on express and parcel posts. These areas are characterised by high competition but allow revenue growth [

71]. Similar results were obtained in our research for the Polish postal services market.

Logistics providers during the pandemic focused on five topics, i.e., creating revenue streams, increasing operational transport flexibility, forcing digitalisation and data management, optimising logistics infrastructure, and also optimising staff capacity. These topics could give logistics companies resilience during the COVID-19 crisis [

72]. Our research shows that the largest logistics companies in Poland paid attention to these elements. Such measures also contributed to revenue growth. Atayah et al. [

73] examined the financial performance of logistics companies in G20 countries during the first months of the pandemic. Financial performance in 14 countries was higher compared to other countries. In contrast, Germany, Korea, Russia, Mexico, Saudi Arabia, and the UK performed worse than in the pre-pandemic period. Nguyen [

74] examined the financial performance of 114 logistics forms listed on the Vietnamese stock exchange and compared the years 2019 and 2020. Financial performance did not improve and even worsened. Only a few logistics companies grew. Liu et al. [

75], using the Chinese market as an example, found that in the initial period, the pandemic caused many problems for logistics companies. The number of companies incurring losses increased. After the initial shock, logistics companies will develop rapidly under the influence of three driving forces, i.e., market, technology, and politics. The specifics of the Chinese market are different from those of the Polish market. In China, ports were periodically closed due to the pandemic, which entailed significant losses. Subsequently, solutions were developed that allowed the logistics industry to function and proliferate. In our research, virtually all companies increased revenues in the first year of the pandemic. In contrast, the second year of operation under COVID-19 conditions was a record year in revenue. Logistics companies learned their lessons and adapted their solutions to the situation. It can be said that the adaptation was swift and effective.

During the pandemic, digitalisation and sustainable solutions became a priority for logistics companies. Managing logistics operations for sustainability has become a major challenge [

76]. Dovbischuk [

77] found that a dynamic capacity for innovation reinforces dynamic adaptability in logistics companies. Logistics service providers have generally been successful in creating new services and responding to changing market conditions regarding logistics service quality and company performance. The ability to disseminate new knowledge, effectively train employees, develop cross-functional cooperation within the company, develop long-term inter-firm relationships with business partners, and learn from rivals are key. According to Dilyard et al. [

78], it is crucial to use digital technologies to make logistics operations more flexible and resilient to crises. This way of operating will also contribute to sustainability. Alesiuniene et al. [

79] point out additional advantages of digitalisation, such as reduced energy consumption and environmental impact. Lachvajderová [

80], on the other hand, points to the emergence during the pandemic of new standards for the sustainable operation of supply chains in order to minimise the negative environmental impact of their activities. Such benefits have also been confirmed in many other studies, such as de Andres Gonzalez et al. [

81], Pernestål et al. [

82] and Todorovic et al. [

83]. We obtained similar results in our research and literature review on logistics companies operating in Poland. Large logistics companies were efficiently implementing new IT tools and digitalisation. Such activities, on the one hand, were an opportunity to adapt to new market conditions and competition and, on the other hand, were perfectly in line with the strategy of sustainable business development. Work on the introduction of new, often innovative solutions was already underway. The pandemic, on the other hand, accelerated everything and, in a way, contributed to taking a few steps forward. The benefits of the transformation will accrue to logistics companies, consumers, and the environment as a result of better efficiency and less involvement and consumption of resources.

,

,

{kind=link}