2. Literature Review

A study by Ivanov and Faulkner (2020) [

1] has shown that ownership of real estate is slowly shifting to large firms that own it for the purpose of sublease. Their study disproves the previously held view that companies prefer to lease real estate over owning it, and their research focused primarily on S&P 500 companies. Furthermore, investing in real estate has been discussed by Lekander (2015) [

2], who stated that real estate investing is influenced by local factors, rather than global ones.

Kliber and Rutkowska-Ziarko (2021) [

3] focused on the investment of companies and institutions in real estate in the form of apartments and its impact on the value of society. Therefore, during the COVID-19 pandemic, there was a favorable risk–return tradeoff, especially in terms of investment in housing.

Ding (2009) [

4] also discussed the promotion of real estate investing at an international conference in 2009, presenting the relationship between the promotion of real estate and the real needs of real estate.

Ling et al. (2021) [

5] dealt with the return on equity in real estate investment trusts (REITs) and private commercial real estate (CRE), concluding that real estate return shows some lag in converting corporate capital market assets into stock prices. The profitability of commercial real estate has been further addressed by Plazi et al. (2010) [

6], who assumed only low volatility between the price of estate and the rental amount.

Niskanen and Falkenbach (2012) [

7] studied the differences between (REOCS) and (REITS) in terms of liquidity. Their results showed that (REITS) shows higher liquidity than (REOCS), and thus represents a more preferable investment instrument. Jian and Bo (2011) [

8] concluded that real estate investment is particularly suitable for hedging against inflation.

Income from real estate is represented both by the collection of rents and the increase in the price of the real estate on the market. The following chapter focuses on rents.

Deng (2018) [

9] investigated the risk of investing in real estate at an empirical level by using a model example of US companies to determine how real estate investments negatively affect a company's long-term investment. However, when measuring risk, it is essential to identify the risks so that it is clear how much risk the real estate investment in question poses to the company. The article thus provides a new picture of the perceived risk of investing in corporate decision-making. In his article, van der Spek (2017) [

10] focused on whether real estate is perceived as debt or fixed income by examining debt risks with real estate investments using a model example. His research has shown that real estate is primarily debt-free and is therefore perceived as long-term income. This fact should be reflected in the valuation of the property. Ambrose, Fuerst, Mansley, and Wang (2019) [

11] researched the amount of economies of scale in real estate companies in Europe. Through regression of the data, they examined the effects on the size of expenditures, capital costs, revenues, and profitability. The result of their research was the finding that strong European real estate companies generate higher revenues per unit size of the company. The net operating income to return is higher, while administrative costs decrease depending on the size of the company.

Vrbka et al. (2019) [

12] mentioned in their publication based on a specific example that a methodology that can determine the amount of rent, including its verification. Their methodology depends on the market value of the property and its expected yield. Rental housing and yield is also a subject of research of Martin et al. (2018) [

13]. In the Chinese real estate market, the trend of rapidly rising real estate prices is an unstable element in connection with the smooth and sustainable macroeconomic development. In their contribution presented at an international conference in 2008, Sun, Tao, and Yang (2008) [

14] analyzed the specifics of real estate that are conflicting in the market in relation to supply and demand. The results of their analysis then identified empirical factors that affect housing prices.

DiBartolomeo et al. (2021) [

15] have examined the liquidity of real estate investment trusts (REITs) and their measurement of returns in liquidity shocks, which are very broad and related to their sensitivity. They have certain rules for dividend and cash payout, and this should make them beneficial to investors. REITs, unlike real estate companies, exhibit broad liquidity shocks with negative sensitivity. Hence, when the overall market liquidity declines, the price of REITs rises relative to the broader stock market. It can thus be concluded that the risk of broad liquidity is lower when a company adapts and converts to a REIT than when it still operates as a non-REIT. Agrawal (2017) [

16] deals with a similar topic, although from a different perspective, instead focusing on the global real estate market and its dynamics. The author´s conclusion, which is supported by studies by other academic experts from around the world, is that it is necessary to know and understand the processes related to the real estate market, which are very complex but also important, as they are the basis of these markets. They emerged in the US, Asia, and Europe, and their development has been very rapid in terms of the structure of real estate markets in the past few years and REITs are a clear example of this. A study by Lee, Lee, and Chiang (2008) [

17] examined the relationship of REIT and private real estate. Their research has shown the existence of a close relationship between these factors since 1993. In their publication, Kroencke, Schindler, and Steininger (2018) [

18] shows the results of their research of the types of risks and rates of return on real estate investments. Their research was conducted on a model in the US and the findings of these real estate returns are applicable to a wide range of users ranging from academics to authorities. Leng, Wang, and Xu (2008) [

19] (REIT) examined the Chinese market in domestic policy and law. They also stated that real estate investment trusts (REITs) are a positive source for financing real estate on the capital market. In their publication, Abdulai et al. (2016) [

20] presented the view that the relationship is between real estate development and economic development and its boom in specific countries. Furthermore, a very specific topic in their book is the conjuncture of real estate financing and investment. The paper by Jarošová, Čermáková, Kadeřábková and Procházka (2016) [

21] examined institutional factors influencing the labor market. In locations with a higher unemployment rate, there is a higher share of owner-occupied housing, because, in such a case, there is a rigidity of labor migration. In their study, Jarošová and Kadeřábková (2019) [

22] examined the level and development of inflation affecting the labor market in various parts of the Czech Republic. Furthermore, real and nominal unit labor costs were selected, while the development of these costs was then assessed in various regions of the Czech Republic, together with the extent of their inflation potential. Moreover, the limits for the negative impact of wages on prices and possible further predictions of the national economy were identified.

Mauck and Price (2017) [

23] examined differences in foreign real estate investment and related them to the domestic market. The basic factor is a different registered office of the company and the location of the real estate in which the investment is made. The research provided the results regarding the likelihood of acquiring a smaller stake in larger assets. In general, a smaller share of investments is made in industrial, retail, office, and warehouse real estate. Peng (2020) [

24] analysed real estate returns between individual US cities and identified the local influence on real estate returns. Similarly, real estate returns (yield) are also observed by An (2016) [

25], who based his research on the data obtained between 2001 and 2010, and found significant regional differences in property yields. Bokhari (2012) [

26] proposed a two-stage model for monitoring real estate returns, which unfortunately failed to catch on in practice. Another view of real estate investments was provided by Chinloy, Hardin, and WU (2017) [

27], who described the process of real estate investing in terms of a closing auction. Real estate purchased at auction is traded at a discount, therefore prices are lower than the selling prices, and price differences are logical and intuitive. The article by Kaderabkova et al. (2017) [

28] examined the dependence of real estate prices on time spent commuting to work. The authors found that every minute of commuting time closer to the city center corresponds to the additional cost of CZK 43,391 for an average-sized apartment in Prague.

Hayunga and Pace (2010) [

29] addressed the risk-return tradeoff in relation to the location of a commercial real estate.

The relationship between the service life of buildings and the investor's costs during the life cycle of buildings is addressed by Heralová (2017) [

30]. The costs of property maintenance are further discussed by Macek (2010) [

31]. His publication can serve as a methodology for building own by owners/investors to predict future maintenance costs. The projection of life-cycle maintenance costs has also been addressed by Karásek (2018) [

32].

A property can be valued using various valuation methods. Vrbka et al. (2020) [

33] focused on the synthesis of valuation methods that determine the total amount of investment.

3. Materials and Methods

The outputs used in this article are based on data provided by EVAL software. EVAL software is a tool developed by one of the authors of this article. SW EVAL is used only by authors; the license and all rights of SW EVAL is a personal property owned by one of authors. In this case SW EVAL is not used by other authors/studies. This software is able to analyze, collect, and evaluate real estate advertising from main real estate servers in the Czech Republic (e.g.,

www.sreality.cz;

www.reality.idnes.cz;

https://stredo.ceskereality.cz/ (accessed on 6 September 2021)). In the database of this software, about 750 thousand new records are registered every six months. The database contains data on the sale and rental of apartments. These are offer prices from real estate offers; actual negotiated prices may vary slightly.

This article uses basic statistical methods, such as regression analysis, which was used to identify the relationships between the unit selling price, the unit rental price, and other technical and socioeconomic factors concerning the real estate market. This article used the data for the period of January 2018–June 2021.

This article examined the following socioeconomic and technical parameters:

Dependence between the selling price of an apartment per m2 and the average annual rental yield.

Dependence between the average annual rental yield and the average number of months needed to pay for the apartment.

Dependence between the average annual rental yield and the number of ads on sale of apartments per 1000 inhabitants.

Dependence between the average annual rental yield and the number of ads on rental of apartments per 1000 inhabitants.

Dependence between the average annual rental yield and the number of ads on new apartments per 1000 inhabitants.

Dependence between the average annual rental yield and the share of persons facing distraint.

Dependence between the unit selling price of an apartment per m2 and the unit price of an apartment for rent per month.

The calculation is based on data from 76 districts in the Czech Republic. The EVAL software provided data for all municipalities of the Czech Republic. The data were further aggregated into relevant districts of the Czech Republic. A total of 880,675 records related to sale of apartments and a total of 701,465 records related to rental of apartments were included in the calculation. The calculation also works with data from the Czech Statistical Office [

34] and the web Mapa exekucí (Map of distraints) [

35].

It has been found that the relation between market price of a real estate (sales, rental) and technical and socioeconomic factors may be expressed by means of linear regression or possibly logarithmic regression. Linear regression represents a straight line approximation of given values using the method of least squares. Such a line is expressed by the following equation:

where the optimal values are found for coefficients

b1 and

b2.

Logarithmic regression is a specific case of linear regression where the data set is prolonged by logarithmic function:

4. Results

This chapter presents graphs and tables of the dependence between the basic economic parameters on the real estate market (price per m2—sale/lease) and selected technical and socioeconomic parameters.

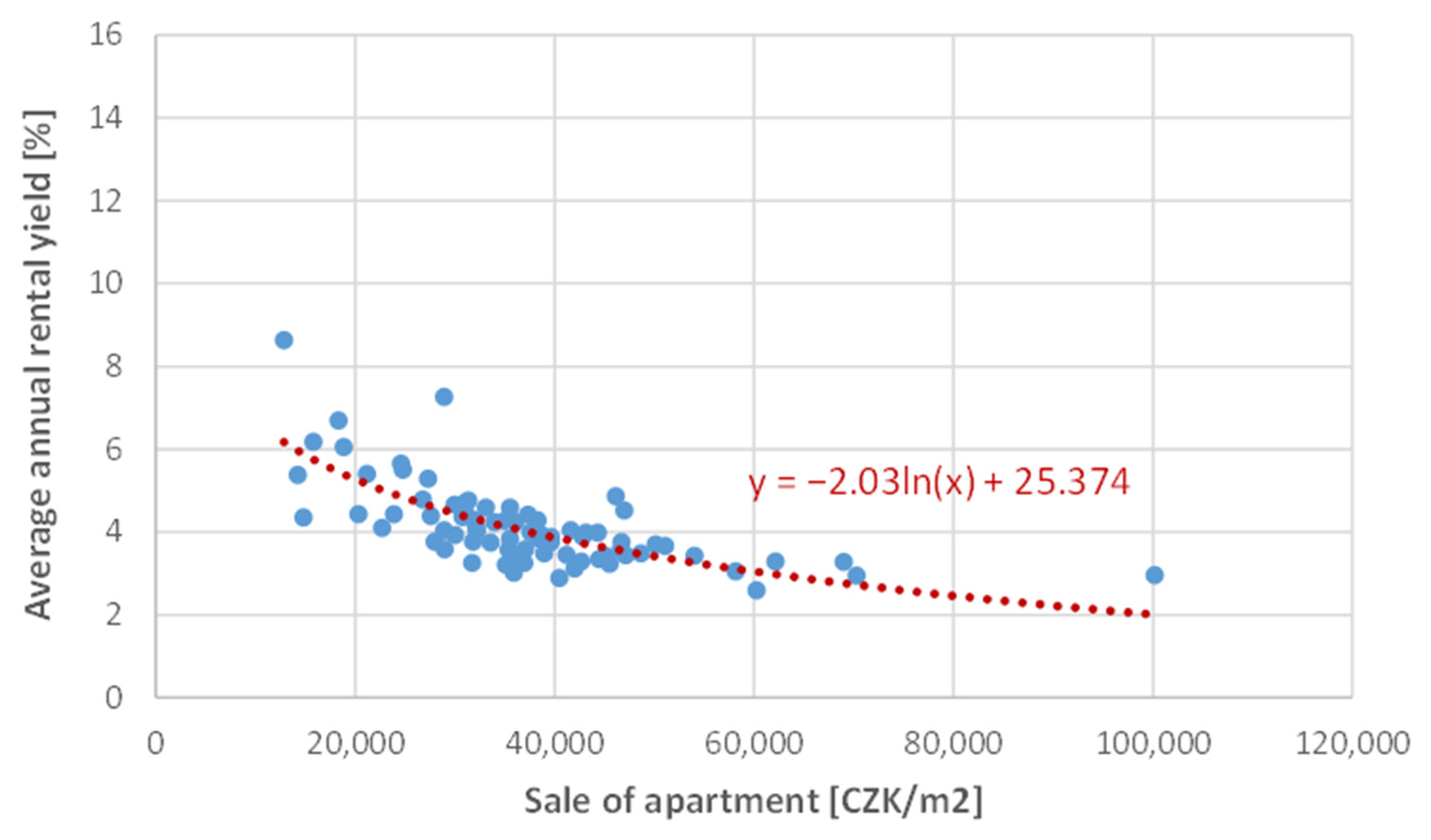

Figure 1 shows the relationship between the sale price per 1 m

2 of an average-sized apartment in the Czech Republic (floor area is 50 m

2) and the average net achievable rentability for the investor. The calculation includes the costs associated with the ownership and maintenance of real estate, property taxes, income taxes, property insurance, maintenance and renovation costs, risk reserve, and a percentage taking into account the potential loss of income if the tenant left the apartment or the tenant stopped paying rent for any reason. Note on conversion rate: 1 EUR = 25.38 CZK.

It follows from

Figure 1 that the higher the price of an apartment per m

2, the lower the average annual return on investment. Conversely, cheap real estate means higher returns for the investor. This fact is caused by several factors. On the one hand, the average level of rent shows a smaller degree of deviation across regions in the Czech Republic than real estate sales prices. Locations where real estate is offered for sale at very high prices do not offer an adequate amount of achievable rent. Locations where real estate is sold at a significantly lower price than the average price in the Czech Republic usually have social and economic problems in society at the same time. In these locations, the state makes up the income of low-earning and poor tenants from the state budget. This fact causes a certain ambiguity in the prices for sale and rental of apartments. Another fact is that investing in socially excluded locations represents a greater risk for investors, which results in higher returns. Such risks can be seen in the risk of lease failure—the inability to rent a property for a longer time because of low demand. Another risk is the maintenance of the property, since, in socially excluded locations, there is a higher probability of improper treatment of the property by the tenant. The investor is thus forced to have higher maintenance reserve.

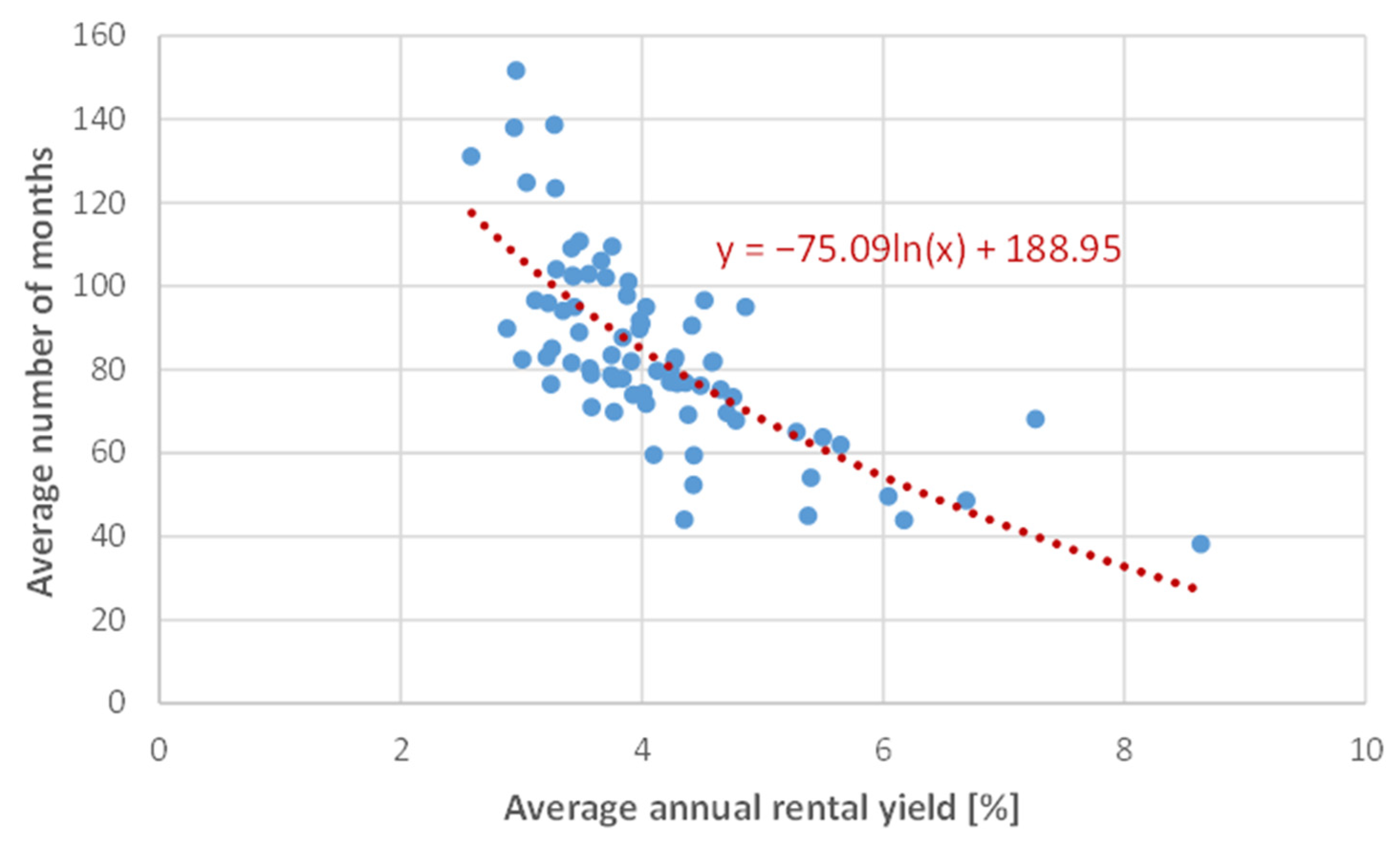

Figure 2 shows the relationship between the average number of months it takes an investor to pay the purchase price of an apartment from an average salary and an achievable average annual return on investment. It turns out that the lower the percentage of profitability, the more months the investor needs to repay the investment. The calculation considers the acquisition of an apartment with a floor area of 50 m

2. The average gross monthly salary in a given region is considered. It is assumed that the investor spends the entire salary to repay the investment. The calculation takes into account standard maintenance and renovation of the apartment and other common risks associated with holding the investment. The result in

Figure 2 is given, among other things, by the fact that an expensive real estate achieves a lower return on investment (see also

Figure 1).

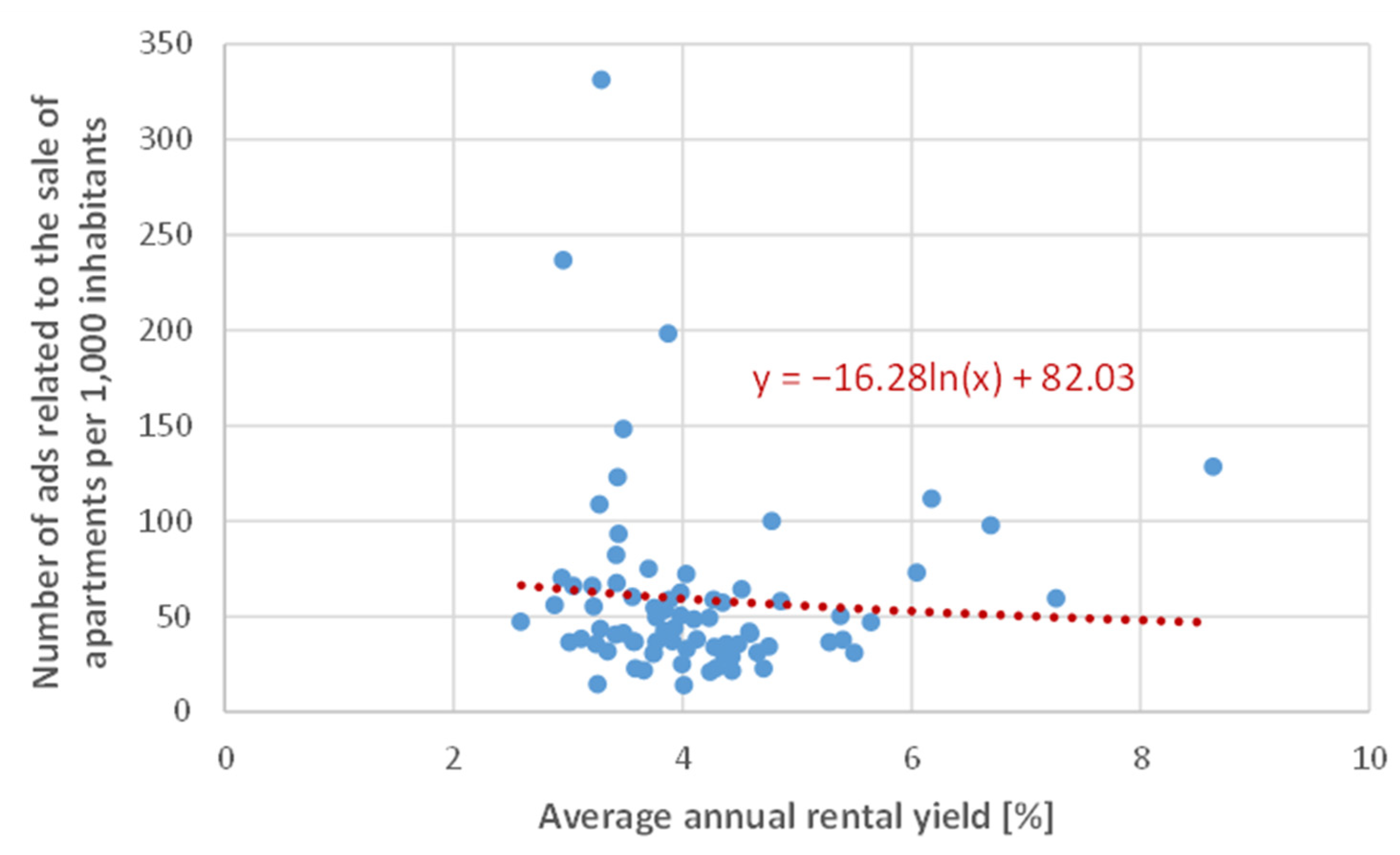

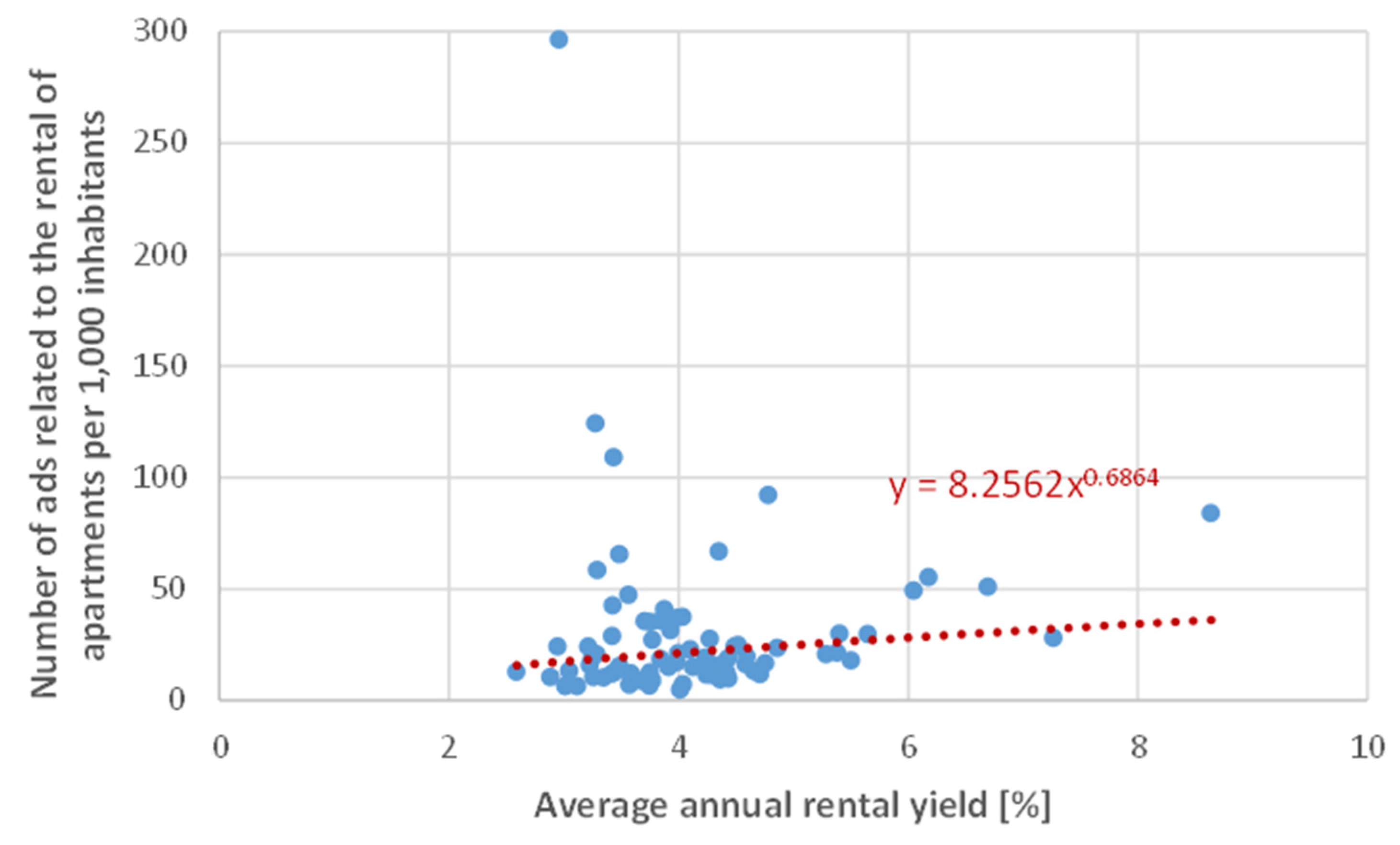

Figure 3 and

Figure 4 show the dependence between the number of advertisements concerning the sale or rental of apartments per 1000 inhabitants (for 3 years) and the achievable annual return on investment. In both cases, the degree of correlation appears to be low. This is due to the fact that the activities of investors and real estate companies are mainly concentrated in large regional cities in the Czech Republic. Foreign investors are interested in investing in the real estate market in the Czech Republic almost exclusively in the Prague or Brno region. Investment activities in the real estate market in other cities in the Czech Republic and in the countryside are mainly carried out only by domestic investors. Another factor is that, in the Czech Republic, there are also large cities and regions that have a disturbed socioeconomic environment and demographic structure. It is thus difficult to make an objective comparison between regions where standard economic links are established and regions with a disrupted economic and demographic structure.

The average number of advertisements per 1000 inhabitants (for 3 years, real estate market turnover) is based on the value of 59.33 in the case of the sale of apartments and 30.54 in the case of rental. More detailed data is shown in

Table 1. Based on the obtained data, it can be stated that the majority of real estate and investment activities in the Czech Republic take place in the Prague and Brno regions. In other regions of the Czech Republic, real estate activities are at a significantly lower level. It was also found that the larger the city, the greater the number of rental apartments offered in real estate advertising is when calculated per 1000 inhabitants.

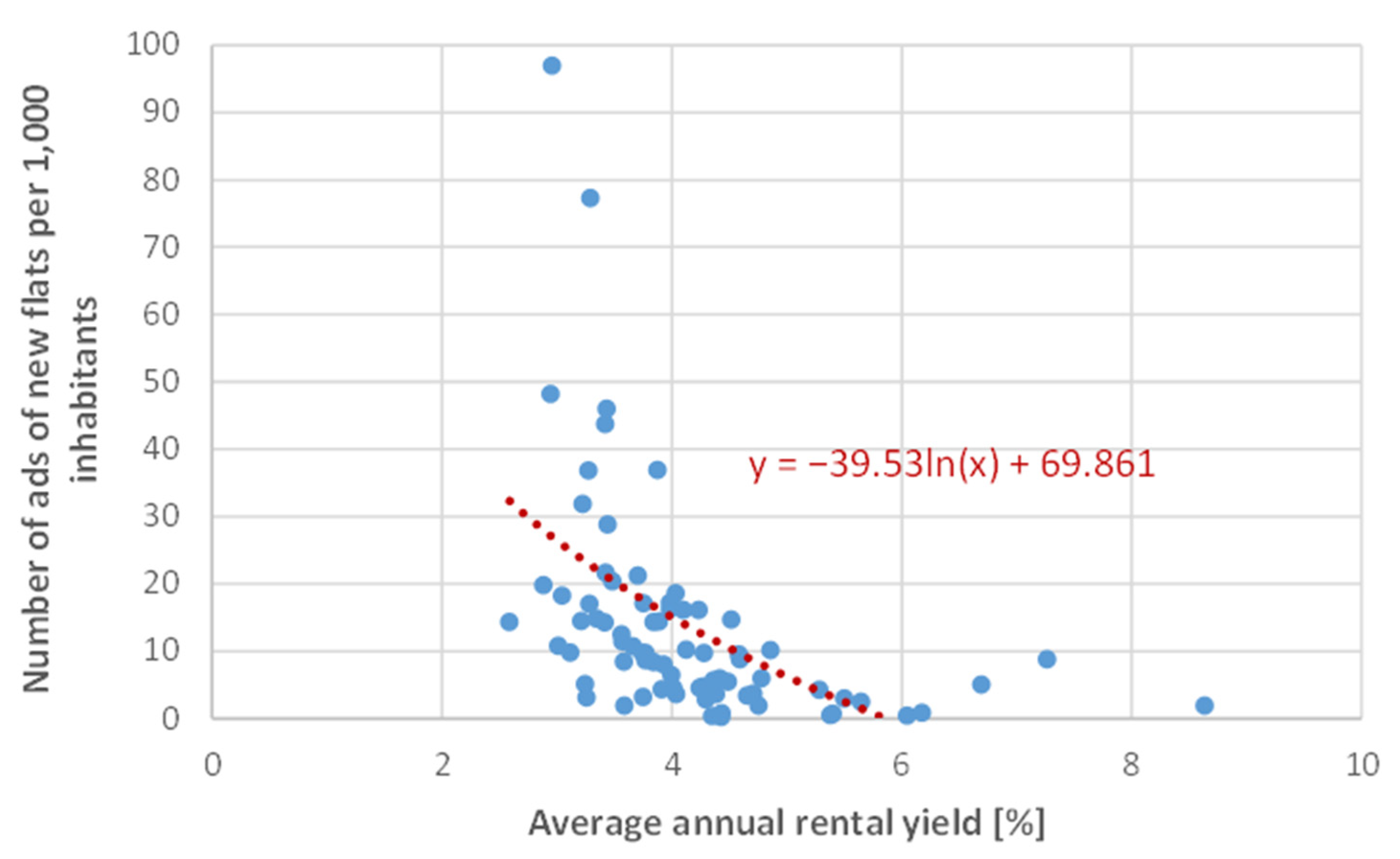

Figure 5 examines the relationship between the number of advertisements on the sale of a new apartment per 1000 inhabitants in a given region (for 3 years) and the average annual return on investment. It turns out that, the more new apartments that are built in a given region when calculated per 1000 inhabitants, the lower the achievable annual return on investment. This is due to the comparison of supply and demand for new housing in the region. In the event that developers and investors find that there is a big difference between supply and demand in a region, they initiate new housing construction as a response. Gradually, supply and demand balance out in this region, which also reduces the return on investment. In the construction industry, however, there are long time cycles from the design of a project plan to the finished building, therefore it takes longer to balance out the demand and supply. In addition, the building permit process in the Czech Republic takes an above-average length of time compared to other developed countries in the world.

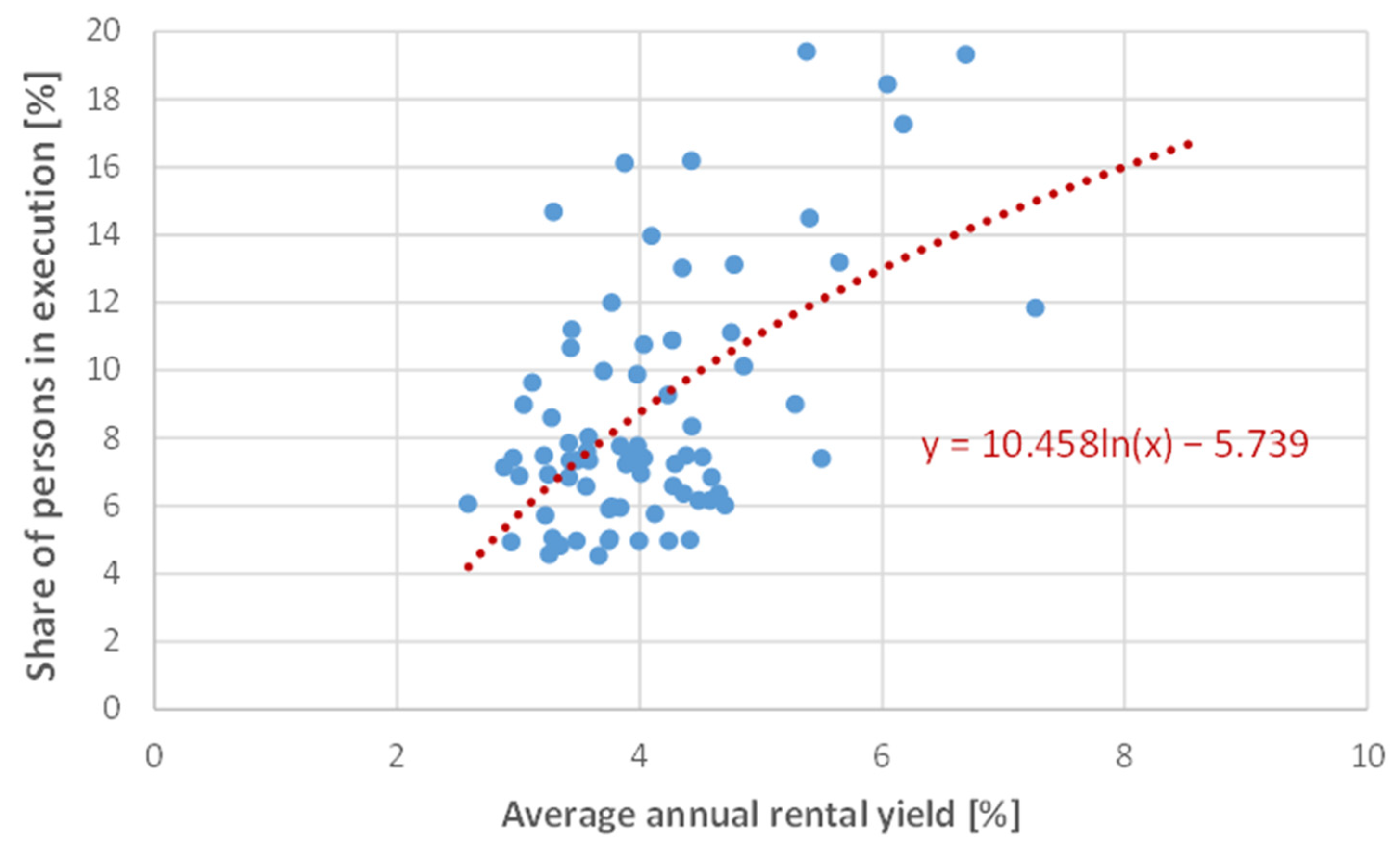

Unfortunately, in the Czech Republic, there are regions with serious socioeconomic problems and a complicated demographic structure. These are regions with a high unemployment rate, an outdated industrial structure (such as coal mining, coal power plants, etc.,) and many able-bodied young people most often leave these regions for large regional cities (especially Prague). These regions are also characterized by a significant above-average number of persons facing distraint.

Figure 6 shows the relationship between the number of persons facing distraint in a given region and the achievable return on investment. It turns out that, the larger the number of persons facing distraint, the higher the return on investment. This is caused by several factors. On the one hand, the state provides the income support to households affected in this way, and these persons thus have the financial means to pay the rent. Investors in structurally disadvantaged regions may demand a higher rent from tenants than would otherwise be the case, as there is a greater risk associated with renting an apartment. Such a risk arises from the ability of tenants to meet their obligations in the long run. Another risk is related to the possible bankruptcy of a tenant, where the rent due becomes very difficult to collect.

Many people in such regions are not able to buy their own apartment, therefore the only option for them is to rent one. This increases the demand for rental housing and thus the return on investment. On the other hand, the selling price of real estate in such regions is relatively low.

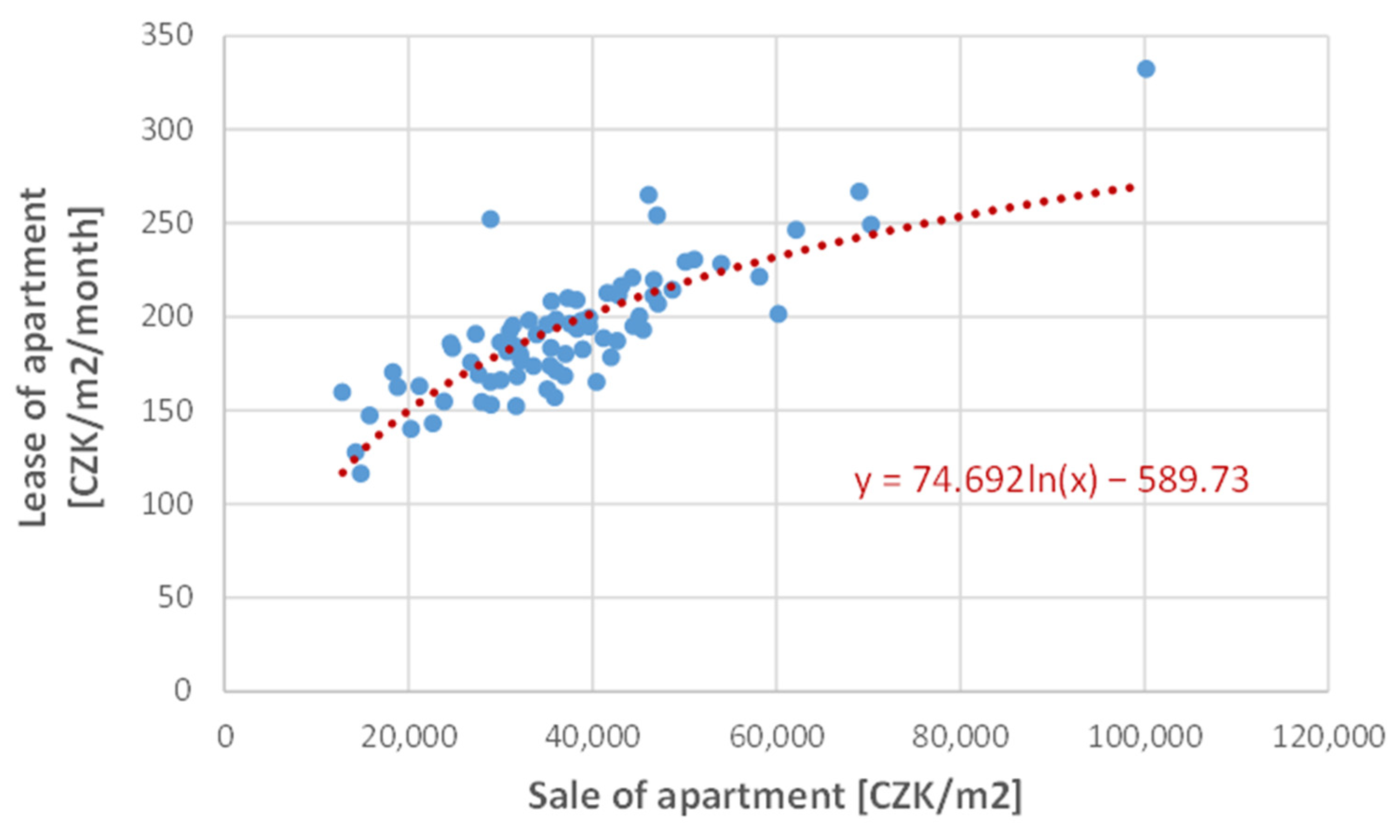

Figure 7 shows the dependence between the sale price and rental price of an apartment. It turns out that there is a high degree of correlation between the sale and rental price. The higher the sale price of the apartment, the higher the possibility of renting the apartment at a higher price. More expensive apartments are usually situated in a better location, for example in the centers of large cities, where there are more opportunities for work and social life. More expensive apartments also offer a higher standard of living and non-conflict neighbors. It is a non-linear dependence that decreases as the selling price increases, which may be due to the relationship with the monthly income of the customer. Note on conversion rate: 1 EUR = 25.38 CZK.

5. Conclusions

It has been found that, on the real estate market, there are many correlations between the market price of the apartment and other technical and socioeconomic factors.

Table 2 shows the calculated correlation coefficients for the examined technical and socioeconomic factors. For the dependencies shown in

Figure 3 and

Figure 4, the correlation coefficients are close to zero.

Based on the research conducted, it can be concluded that there is a relatively strong dependence between the parameters under review. From an investor’s point of view, it is advisable to monitor the selected parameters to maximize the benefit of real estate investing. This article also shows that properties which are located in regions with more people that are facing distrain bring higher yield. Thus, due to the general risk–return relationship, it can be concluded that investors in excluded locations perceive a higher risk and demand and a higher return for taking it. In general, these are regions with higher unemployment and thus a higher turnover of apartment users and higher vacancy rates.

The strongest correlation was found between rent and the total sale price of the property. However, this is not a linear dependence but rather a gradually decreasing dependence, i.e., the amount of the rent decreases with increasing sales price. This decline thus confirms the general distribution of the purchasing power of the population when higher rents can be afforded by a more limited group of the population, which is in lower demand for such properties, and investors are forced to demand lower rents.

Further research could focus on other macroeconomic parameters to develop a model for forecasting.

The result shows that, rental yield in the Czech Republic is ca. 4%. This result can be compared internationally, e.g., with property yields. Rental yields in major German cities are 3.5–3.7%, while in Spain, it is 4%, and ca. 7% in Romania, which means the Czech market is the most similar to the Spanish market, and investors feel a similar risk for their investments. despite of different currency in Czech rep. and in Spain, the risk for investors covered by market yield is nearly the same.

The main recommendation of the article is that investors looking for investments with a significant rate of return on profitability (yield) will prefer to invest in excluded localities where there is a higher proportion of citizens in personal bankruptcy and foreclosure.

In further research, we want to focus on examining the dependencies of some technical-economic and macroeconomic parameters: the dependence of the offer price of an apartment on the distance from the center of the capital, the influence a balcony may have on the price of the apartment, and the dependence between the offering price of the apartment and the floor on which the apartment is situated.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}