Beer Industry in the Czech Republic: Reasons for Founding a Craft Brewery

Department of Landscape Management, Faculty of Agriculture, University of South Bohemia in České Budějovice, Na Zlaté stoce 3, 37005 České Budějovice, Czech Republic

Sustainability 2021, 13(17), 9680; https://doi.org/10.3390/su13179680

Submission received: 24 June 2021

/

Revised: 16 August 2021

/

Accepted: 21 August 2021

/

Published: 28 August 2021

(This article belongs to the Topic Toward the New Era of Sustainable Design, Manufacturing and Management)

Abstract

:The goal of this article is to evaluate the evolution of the brewing industry in the Czech Republic with an emphasis on the phenomenon of craft-brewery development. It deals with the influence of globalization on the structure of the Czech beer market and the rise of craft-breweries between 2000 and 2019. The main outputs come from research where a representative sample of 48 craft breweries was questioned from the Czech Republic. The result is the identification of the main factors influencing the increase of craft-breweries (legislation changes enabling entrepreneurship, increase of purchasing power of consumers, increase in demand for different beer styles, craft beers and specials, change of consumer behavior) but also the challenges that prevent their further expansion (lack of qualified brewers, complicated administration). The main motive for founding a craft brewery is an effort to improve beer culture in the Czech Republic and the ever-increasing demand for diversified beer (as opposed to the demand for the so-called euro-beers) and a good business opportunity stemming from this, which has been attracting more and more investors into this field.

1. Introduction

The brewing industry in Europe, as well as in the world, underwent significant changes recently. Until the end of the 19th century, most of the breweries were local and privately owned. National, let alone international brands, did not exist [1]. Until the second half of the 20th century, beer was mostly a local product. With the expansion of the biggest breweries into new regions and industrial consolidation, the brewing industry is becoming a global one after this period. On the one side, there is a process of gradual consolidation with numerous fusions and acquisitions of large commercial breweries and brewery groups, whose main goal is to achieve economies of scale. This process is reflected in the ever-increasing share of large brewery groups on the market. Other changes that took place in the last decades in Eastern Europe (mainly a wave of revolutions leading to democratic systems) led to the loosening of barriers to entry of specific beer markets by international companies and chains and to further gradual consolidation, which resulted in a lower number of active breweries around the world [2]. This trend had a significant influence on the brewing industry; in 1998 the market share of the four biggest beer producing companies made up 22%, however, in 2010 it was almost 50% of the global beer market [3,4]. Contemporary global beer production is under the control of a few large brewery groups: Anheuser–Busch InBev (AB InBev, Leuven, Belgium) including SAB Miller (London, Great Britain), Heineken (Amsterdam, The Netherlands) and Carlsberg (Copenhagen, Denmark), Asahi Group Holding (Japan). These companies make up approximately 41% of global beer production [5]. The beer prepared by these large companies is very homogeneous and it is exactly homogenization of beer that is one of the reasons for craft beer’s success [6].

On the other side, there is a pronounced trend of founding craft-breweries and craft breweries (as a reaction to the aforementioned) that focus on the production of craft beer. This trend began in the 1970s in the USA [7,8]. Western Europe joined this trend in the 1980s, while in Eastern Europe, including the Czech Republic, a significant increase of craft-breweries and craft breweries came after the year 2000. In recent decades there was a “craft beer revolution“ phenomenon, which was started by American beer enthusiasts and homebrewers in 1979 when they enforced a law that left the decision concerning home brewing to national jurisdiction [6]. Acitelli [7] says that “craft beer revolution” started in 1965 when Fritz Maytag purchased a 51% stake in the Anchor Steam Brewing Company from San Francisco. We can say that craft breweries and home brewers have been included in the brewing industry since the end of the twentieth century. Craft breweries and home brewers all share some characteristics, such as the use of traditional production methods, quality ingredients and the volume of their production that is set differently for every country. For craft-breweries in, for example, Slovakia and Poland, it is up to 200,000 hL/year, in the Czech Republic it is 10,000 hL/year and in the USA it is 23,848 hL year [8,9,10,11]. The term craft brewery is defined by production up to 9,539,200 hL per year in the USA [12]. In the Czech Republic, the terms craft brewery and micro brewery are not differentiated, it is always a brewery with production up to 10,000 hL/year in which the beer is brewed according to traditional recipes, unfiltered and unpasteurized [13]. For the purposes of this article, only the term craft brewery will be used from here on. The volume of home-brewing is limited to 2000 hL per year and household.

In 2015, there were more than 10,000 craft breweries in the world from which 86% were located in North America and Europe [13]. Craft beer became a key driving force in the development of new products in Western Europe whereas there has been a two-digit increase in the number of craft breweries since 2011. Large industrial breweries are now trying to react to the increase of the popularity of craft beer brewed in craft breweries by including special types of beer (trying to compete with craft beers with their taste and fullness) in their product portfolio. However, the consumers have not shown much interest in these special beers because they still consider them to be industrially produced. This is why some large breweries have started creating subsidiaries and are brewing beer under a different brand or include beers from friendly craft breweries in their portfolio [14,15,16].

Another change that affects the brewing industry is the relocation of beer consumption to regions outside of Europe [17]. The Czech Republic is still first in terms of worldwide beer consumption per inhabitant (144 L in 2019), however, the increase of overall beer consumption in the 21st century is caused by increased consumption in these regions outside of Europe. The consumption in traditional beer areas in Europe either stagnates or even decreases [16,17,18,19,20]. China has the largest beer consumption in the world as a country, where 489.9 million hectoliters are consumed every year, followed by the USA (241.7 million hectoliters), Brazil (131.5 million hectoliters), Russia (100.1 million hectoliters) and Germany (84.4 million hectoliters). The overall consumption in the countries of the EU was 359 million hectoliters in 2016, from which consumption in the Czech Republic made up 15.1 million hectoliters, which is 4% of the overall consumption in the EU [15]. As mentioned above, Czech Republic has the highest beer consumption per inhabitant in Europe (144 L followed by Germany (107 L), Austria (104 L), Poland (98 L), Lithuania (95 L) and Slovakia (73 L) [15]. Craft beer makes up 3%–5% of the overall beer consumption in Western Europe and the USA while in Eastern Europe it is just about 1% and in the Czech Republic it is estimated to be around 2.5% [21,22,23]. All of the above changes are leading to an increase in the number of craft breweries around the world. The topic of this article consists of what other reasons lead to their establishment in the Czech Republic and what are the obstacles to their further development from the perspective of the owners of the craft brewery.

2. Theoretical Background

History, development and current state of brewing in the Czech Republic.

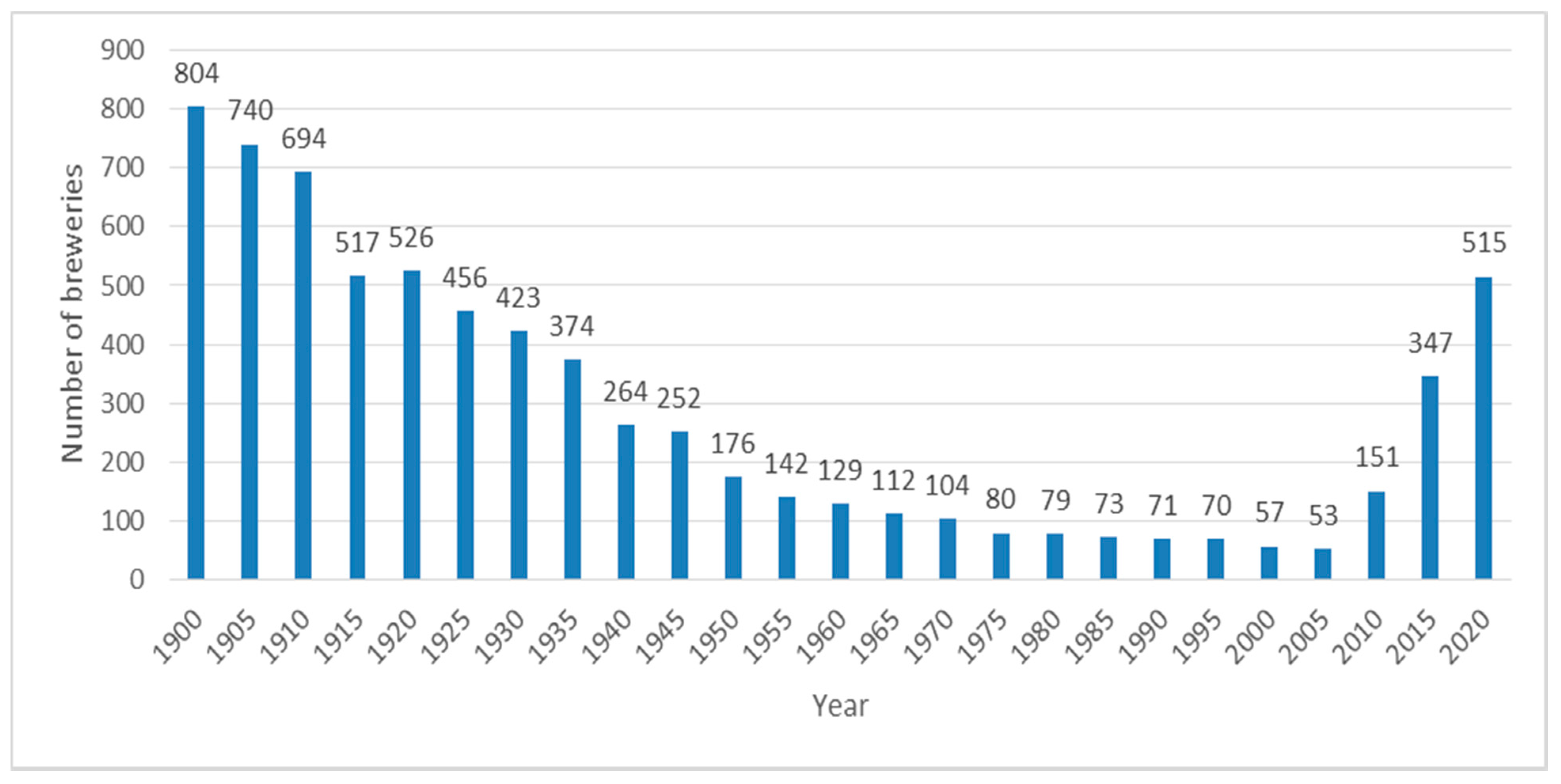

There were 804 breweries in the Czech Republic in 1900. During the first World War, the brewing industry was impacted very negatively. Breweries had a set ration of barley, which covered approximately one-quarter of what was needed. In 1916, processing barley and malt was completely banned. Brewery equipment from copper, brass and bronze was disassembled for war purposes. Production declined to a mere 14% of the pre-war level during the war. During this time, 122 breweries closed. This trend continued, and in 1918 there were 526 active breweries in Czechoslovakia. After 1918 there were no new breweries because of the difficulties in Czechoslovakia caused by the war, such as low standard of living, shortage of goods and loss of foreign markets and destruction of machinery [24]. The crisis in the brewing industry was also caused by the changes in beer production and increased beer prices. Production was concentrated in bigger production units since 1923, so this caused another decline in the number of active breweries—there were 456 in that year [24]. This trend further continued with the beginning and course of the second World War when there were 374 breweries in Czechoslovakia. In 1946, the Economic Group of Brewing and Malting Industry was created and later a National Company of Czechoslovakian Breweries was created, and breweries with a production volume of over 150,000 hectoliters were nationalized. The change of the ownership structure was the beginning of an orientation towards a planned economy with the consequence of (1948) the establishment of 22 national businesses, which associated 194 active breweries at that time. Central planners decided on the number of breweries and their production, as well as the amount of beer to import and export. During this time, there was almost no beer imported to Czechoslovakia. As for the type of beer, the only produced and consumed beer during this time was lager. Lagers produced during this period were, however, more differentiated by taste and quality than they are today [24].

The transition of Czechoslovakia from socialism and planned economy to democracy and market economy, which hit Eastern Europe, also had a significant impact on the beer market in the Czech Republic and in Slovakia (both countries became independent in 1992). Breweries were privatized and later taken over by international companies such as Heineken and SABMiller (they later joined with AB InBev, which sold their assets in the Czech Republic and the whole of Eastern Europe to the Japanese group Asahi), which dominates the Czech beer industry today [25].

Czech breweries were gradually increasing the effectiveness of the industry, mostly because of the influx of international know-how and technologies, improvement of vertical coordination in the supply chain and utilizing economies of scale [26]. Traditional local beer was replaced by homogenous beer produced by big companies. The technology of beer production was altered so that shorter production cycles could be achieved (processes of fermentation and aging were connected). This led to the standardization of quality, which on the one hand caused the elimination of lower quality beer, but on the other hand also lowered the differentiation of product.

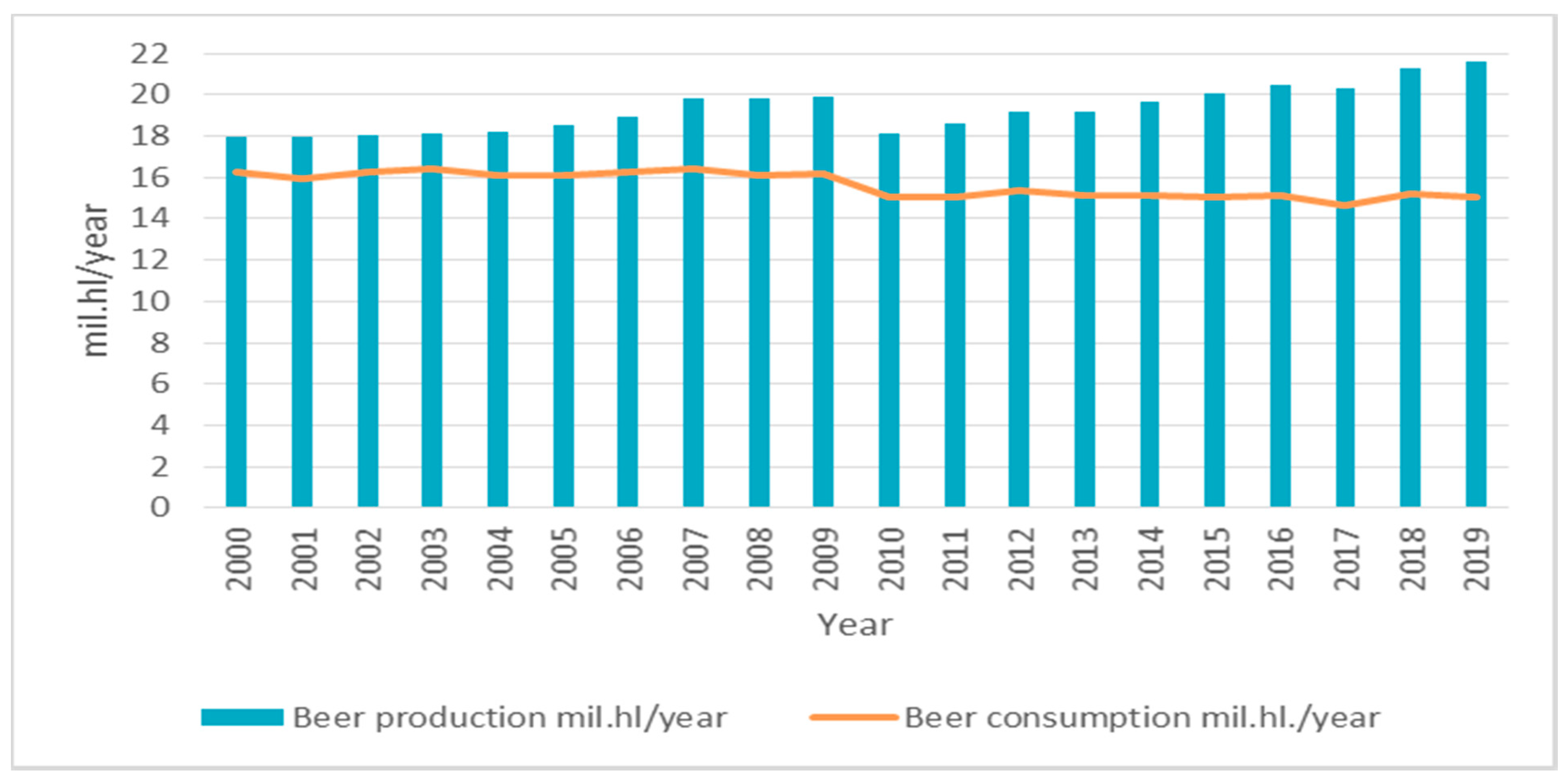

In 2000 the production of the whole brewing industry in the Czech Republic was 17.92 million hectoliters, in 2015 it surpassed the magic number of 20 million hectoliters and this trend of continuous increase still lasts to this day, the last official statement from 2019 states the volume of production was 21.6 million hectoliters [27]. Even though the Czech Republic is still first in beer consumption per inhabitant worldwide, the consumption is continuously declining. It was the highest in 1992 where some sources state consumption of even 169 L per person, another peak was in 2003 where consumption of 161 L per person was stated but since then the decline has continued, to 141 L per person in 2019 [27]. One of the factors influencing the decline in beer consumption is the price, but that is not the only reason; efforts to have a healthy lifestyle, a change of beer drinking habits, the transition from beer to wine and others also play a role. The final price of beer is influenced by excise duty, as well as the increasing labor costs and the price of ingredients. Since 1995, the excise duty in the Czech Republic has been derived from the volume of a brewery’s production and is divided into six zones (mostly in Europe). The basic rate is 32 Kč/hL for every whole weight percentage of the original wort extract, lowered rate for breweries with the production volume of 150,000 to 200,000 hL is 28 Kč/hL, production volume of 100,000 to 150,000 is 25.60 Kč/hL, production volume of 50,000 to 100,000 hL is 22.40 Kč/hL, production volume of 10,000 to 50,000 hL is 19.20 Kč/hL and the last group of production volume is up to 10,000 hL, including tax rate 16 Kč/hL [28]. Czech craft breweries belong in this category.

Even the behavior of consumers is changing—in 2003, Czech consumers drank half of the overall consumption in pubs and restaurants and half at home. In 2019, 66% of the overall consumption was at home (off-trade) and only 34% of the consumption was in restaurants and pubs (on-trade) [29]. The main reason is the different price of draft beer and bottled beer as a consequence of the increasing labor and other costs of restaurants. The evolution of the number of breweries and craft breweries in Czechoslovakia is illustrated in Figure 1.

Among other reasons for the decline in beer consumption is the aforementioned healthier lifestyle of many Czechs who tend to prefer non-alcoholic beverages over alcoholic ones, and the changing preferences of alcohol consumers where some replace beer with wine.

3. Materials and Methods

The goal of the research in this article, which is a follow up of similar research conducted in Slovakia [9], was to identify the main factors influencing the growth of craft breweries but also the challenges to their further development. A method of structured interview with the owners of craft breweries in the Czech Republic was chosen for these purposes. The same method and its implementation were used in Slovakia, so the results can be compared. The research took place during the whole year of 2020, when members of the research team gathered information about the opinions of the owners of craft breweries concerning the development of the brewing industry in the Czech Republic. A minor difference in the methodology would be that we have first established a representative sample within our research using quota selection on which we then carried out the research. Our sample of respondents has the same characteristics as the basic sample, these characteristics are stated in Table 1. The number of respondents (owners or operators) was 48 craft breweries out of 480 existing ones in that time. The research was mostly dealing with the following topics–factors influencing the demand for craft beer, impact of traditional beer market characterized by homogenous products on the demand for differentiated craft beer in the Czech Republic, types of beer produced by craft breweries, motivation for starting a craft brewery, factors influencing the supply of craft beer, accessibility of inputs, know-how of the production of craft beer, regulations of craft beer production, government support for craft beer production.

An advantage of the structured interview method is the opportunity to understand the thoughts forming the development of the craft brewing industry, become acquainted with the expectations of the main representatives, their opinions, interests and former experiences. The method used consisted of the following three phases [30,31]: planning the study thanks to a research method of a structured interview, implementation of the interview itself, analysis of the results and creation of the research report. The method of structured interview is suitable especially when it is needed to understand the behavior, needs and interests of respondents. It was possible to find out the preferences, experiences and opinions during the discussion and from the reactions of the respondents. The interpretation of these results helps to understand the behavior and decisions of the respondents. Key questions for the owners or operators of craft breweries in our research were:

- Does the situation on the market influence the type of beer that you produce?

- What factors determine the demand for craft beer?

- Do the customers react sensitively to changes of your beer’s prices?

- Are the ingredients for brewing craft beer available? Which ingredients are imported and from where?

- Are there enough professionals in craft beer brewing in the Czech Republic? Do you personally (or an appropriate person in your brewery) have previous experience with beer brewing?

- Why did you decide to start a craft-brewery?

- What is your opinion on the relationship between the government and craft-breweries?

- Do you cooperate with other craft-breweries?

- Do you think that there is still space for other craft-breweries on the market?

4. Results

4.1. Beer Market in the Czech Republic and Ownership Structure

In the Czech Republic, the changes described above have manifested in the ownership structure and in the trend of the increased number of craft-breweries. This trend has been significant since 2010 and reached its peak in 2017 when there was essentially a new craft brewery created every week in the Czech Republic [32,33].

Information about production volumes and hence about the distribution of the Czech beer market is not completely accessible, the problem is that breweries are not required to state their production volume. Official statistics and information cannot be considered as precise because of this reason. Production volume and distribution of the Czech beer market were researched from all accessible sources (ČSÚ, Czech–Moravian union of craft-breweries, Czech union of breweries and malt-houses, customs office of the Czech Republic, websites of the respective craft-breweries and personal connections with the owners of craft breweries) in 2019. Detailed information and the most important characteristics are presented in Table 2 and Figure 2.

There are eight large brewing companies in the Czech beer market:

Plzeňský Prazdroj: breweries Pilsner Urquell, Gambrinus, Radegast, Velkopopovický kozel. Owned by Asahi Group Holding, Japan.

Pivovary Staropramen: Staropramen, Ostravar. Owned by MolsonCoors Brewing Co., Canada and USA.

Heineken ČR: breweries Krušovice, Starobrno, Velké Březno. Owned by Heineken N.V., Netherlands.

Budějovický Budvar: national business, owned by the Czech Republic.

Pivovary Lobkowicz Group: breweries Černá Hora, Hlinsko, Vysoký Chlumec, Protivín, Jihlava, Klášter and Hradiště. Owned by CEFC Geoup Company, China.

Pivovary Moravskoslezské Přerov: breweries Hanušovice, Litovel, Přerov. Owned by HSK invest, Czech Republic.

LIV Group: breweries Svijany, Rohozec, Náchod. Owned by the company LIF Group Czech Republic.

AB InBev: brewery Samson. Owned by AB InBev, Belgium. This company owns just the Samson brewery with a production volume of 140,000 hL in the Czech Republic.

Twenty-two independent breweries and 480 craft breweries and restaurant breweries, production volume up to 10,000 hL.

The Czech Republic is a long-term beer exporting country where the consumption of beer is lower than its production volume. The trend of export is continuously increasing—in 2019 the Czech Republic exported 5.4 million hectoliters of beer. Slovakia has the biggest share in the export of Czech beer, over 1.3 million hectoliters has been shipped there in 2019. Then Germany with 1 million hectoliters and Poland, the Russian Federation and Hungary with exports of around 400,000 hectoliters. The import of beer into the Czech Republic is negligible. In 2019, there were only 471,000 hectoliters imported into the Czech Republic which is around 2% of the total production volume. Beers imported into the Czech Republic are mostly special type beers and beers with a higher degree of alcohol [34].

4.2. Opinions of the Owners or Operators of Minibreweries in the Czech Republic and Comparison of Results

According to the opinions of the respondents, the most important factor influencing the demand for craft beer is its sensory expressiveness in its taste, as well as its scent and color, which differentiates these beers from the unified (euro) beers that are produced by industrial breweries. Another factor which supports the demand for craft beers is the return of consumers to local products and experiential gastronomy [34,35]. Even the higher price of craft beers is not a challenge for the increase in demand. Craft beers are perceived as a unique local product and for that, the consumers are willing to pay. All of these factors are behind the significant increase in the number of craft breweries in the Czech Republic and Slovakia. Currently, there are 480 craft breweries out of the 507 breweries that are in the Czech Republic in total. Their layout within the regions of the Czech Republic is not uniform, most of them (13% of the total number) are in South Moravian Region and the least are in the Karlovy Vary Region (only 2% of the total number). Despite the overall high number of craft breweries in the Czech Republic (the most per inhabitant, there is a brewery for every 20,000 inhabitants, in Germany, for example, that ratio is one brewery for every 50,000 inhabitants) more than 65% of respondents think that there is still space for more on the market. According to the questioned owners and operators of craft breweries, it is expected that their number will continue to rise. There are 30 to 50 new craft breweries opened every year in the Czech Republic and since 2010 over 350 new craft breweries were founded. According to the current craft brewers, founding a craft brewery is still considered to be a very good investment opportunity. These conclusions are also confirmed by Swinnen [36] and Materna [37].

The owners of Czech craft breweries expect the demand for craft beer to stay consistent or even increase in the future, which could be caused by the increasing income of the consumers and increasing demand for differentiated, high quality and local products—which craft beer is [29]. It is precisely craft breweries that offer the diversity that consumers look for. According to a supporting survey among consumers, diversity is the thing that is going to interest them in the future. The survey shows that consumers are diverting from being “regulars“, where a customer regularly visits one, usually the closest pub where they consume the permanent menu, in favor of searching for new beer types and tastes in their immediate or distant surroundings. The spread of beer tourism follows this trend, which is another modern trend after wine tourism in the Czech Republic, based on which the so-called beer trails are created that sometimes connect border areas. The demand for diversity is then reflected in the cooperation of craft breweries on joint marketing of their products and mutual product sales.

These changes in the drinking patterns and lifestyle of Czech consumers have a significant impact on the development of craft breweries. The consumption per inhabitant in the Czech Republic is decreasing but its diversity and quality are increasing, which is something that Czech consumers are willing to pay extra for. These conclusions coincide with the conclusions of research carried out in Slovakia [9].

As for the production portfolio, craft breweries focus both on the production of classic lagers and on the different beer styles such as IPA, APA, stout, bitters, porter and more. The diversity of craft beer is a result of differences in production technologies and input variations. The inputs differ depending on the type of beer. Thirty-four percent of craft breweries in the Czech Republic focus only on the production of bottom-fermented beers (lagers), 63% on the production of both bottom-fermented and top-fermented beers and the remaining 3% produce only top-fermented beers (IPA, APA, etc.). In Slovakia, 74% of craft breweries focus on both forms of production, 10% focus only on bottom-fermented beers and 16% of craft breweries focus on top-fermented beers [9]. The difference in the number of breweries focusing only on bottom-fermented beers could be rooted in a long-lasting tradition of Czech lagers and in the effort to preserve this tradition.

Motives for starting a craft brewery are mostly a desire to enrich the Czech beer market, an effort to improve beer culture and it is still a great business opportunity since the return is estimated to be five to seven years depending on the invested resources. The survival rate of the newly established Czech craft breweries is more than 98% (since 2000, only 26 craft breweries have closed down, mainly due to a bad strategy trying to compete with a low price). Some owners of craft breweries (25%) financed their investments themselves, others (75%) used a combination of their own money and bank loans or subsidy titles granted by the Ministry of Agriculture or industry and trade of the Czech Republic. A similar reason is given by Jantyik [5]. Another thing apparent from the results is the fact that only 5% of the current craft brewery owners have worked for an industrial brewery before the craft brewery’s establishment. On the contrary, 45% of the current owners of craft breweries in the Czech Republic were home brewers who decided to make their hobby into a business. The remaining 50% did not have any experience with beer brewing and founded the craft brewery as a form of investment. An interesting fact is that there is 32% of architects or people focusing on construction work in this group. This relatively significant group was motivated to start a craft brewery for other reasons as well, for example, reconstruction of old historical buildings. Their establishments are mostly a part of farmhouses, mills and other originally agricultural buildings.

The accessibility of inputs, know-how of craft beer production was rated as very good by the respondents. There are four main inputs needed for beer production: water, malt, hop and yeast. Based on the conducted research it was found that 90% of malt used for Czech craft beer production comes from the Czech Republic. Water is always from a local source and in 80% of cases the yeast, which is either from an industrial brewery or bought dried from Czech companies, is also locally sourced. This result is also confirmed by the Czech Statistical Office. Hop is a bit more complicated with more than 30% being imported into the Czech Republic [29]. It is mostly American, Australian and Japanese hops that are very aromatic and used mostly for the production of beer types like IPA and APA. Nonetheless, even these imported ingredients will in some cases be replaced with hops that are still of American, Australian or Japanese variety, however, it will be cultivated in the Czech Republic. This is currently the case for the Japanese variety Sorachi ace. This trend also corresponds with increasing shares of cultivated areas of foreign hops varieties in the Czech Republic at the expense of a classic Czech variety—semi-early red-bine hops, which was the only cultivated variety of hops in the Czech Republic until 1995. Currently, it takes up 87% of cultivated areas. Other cultivated varieties are Brewmaster 6%, Premiant 3%, Saaz Late 1%, Agnus 1%, Kazbek 1% and Saaz Special 1%.

We can say that roughly 2% of the total inputs are imported, as the Czech Statistical Office states [29]. In Slovakia, the situation is completely different with roughly 80% of hops and malt being imported [9].

The equipment of breweries is another source of craft beer differentiation. There are a few Czech producers and suppliers of brewing technologies such as Pacovské rolling mill, Mini Brewery System etc. After their success in the Czech Republic, most of them have focused on supplying technology abroad. Foreign subjects are interested not only in Czech beer and hops but also in production technologies and brewers. The biggest identified problem concerning know-how and operating a craft brewery is the lack of qualified brewers. Every craft brewery in the Czech Republic is listed under the so-called craft activity, which must be conducted by a qualified brewer. The qualification for a trade certificate for this activity can be obtained either by graduating from university or high school with documented practice in a brewery or by successfully completing the examinations of full professional qualification in the field “Brewer–malter“. This examination can be taken from 2021 in the Czech Republic. Another option which is widely used is professional supervision where a person with the aforementioned education supervises a craft brewery and is responsible for correct production techniques, the operation of the brewery and even its economy. This option is implemented as a paid service. Currently, one responsible person can supervise up to four craft breweries. Completing the training or graduating in the field itself is expensive and very time-consuming so this situation paired with the limited number of craft breweries that a qualified person can supervise is one of the challenges that prevent further development of craft breweries in the Czech Republic. On the other hand, this process of certification ensures that all medical and hygienic requirements to protect the public are met. The situation is similar in Slovakia, however, the number of breweries that a qualified person can supervise is not limited there. This section may be divided by subheadings. It should provide a concise and precise description of the experimental results, their interpretation, as well as the experimental conclusions that can be drawn.

5. Discussion

The presented results are in compliance with former studies [9,27,30,31,32,37,38,39,40,41], which identified and described similar factors influencing the expansion of craft beer in different countries, however, there are differences because of the diverse history of the countries, levels of income, regional differences, a tradition of drinking beer and its substitutes. Thanks to the gained data we have identified some of the reasons that influence the expansion of craft beer in the Czech Republic as stated above. Those are mostly: increasing demand for diversified beer and various beer styles, increased levels of income, which have a positive influence on the demand for differentiated and high-quality products, craft breweries are still considered to be a good business with the return rate of five to seven years, accessibility of government support (EU subsidies, development funds of the ministry of agriculture or industry and trade). On the contrary, factors identified to hinder this expansion were mostly: substitutes such as wine and other alcohol, bureaucracy, lack of qualified brewers, tax politics (zero excise duty on still wine in the Czech Republic discriminates the whole brewing industry).

The expansion of craft breweries in the Czech Republic seems to be a logical consequence of the consolidation of the brewing industry, just like in many other European and North American countries. There are currently more than 480 craft breweries in the Czech Republic and several others are being built. However, there is still space for more, and it is expected that by 2030 there will be over 1000 active craft breweries. The decision to start a craft brewery was strongly supported by a lack of beer diversity on the market. Different types of beer require different production techniques and inputs. Nonetheless, a vast majority of inputs is from the Czech Republic. The opening of most craft breweries is financed with a combination of own resources and a bank loan or a subsidy.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

All cited sources can be found in “references”.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Cabras, I.; Higgins, D.M. Beer, brewing, and busi-ness history. Bus. Hist. 2016, 58, 609–624. [Google Scholar] [CrossRef]

- Swinnen, J.F.M. The Economics of Beer; Oxford University Press: Oxford, UK, 2011; ISBN 9780199693801. [Google Scholar]

- Sell Foam Like Soap. The Economist [Online]. The Economist Newspaper, 5 May 2011. Available online: http://www.economist.com/node/18651308(accessed on 5 May 2020).

- Hána, D.; Materna, K.; Hasman, J. Winners and losers of the global beer market: European competition in the view of product life-cycle. Camb. J. Econ. 2020, 44, 1245–1270. [Google Scholar] [CrossRef]

- Jantyik, L.; Balogh, J.M.; Török, Á. What Are the Reasons behind the Economic Performance of the Hungarian Beer Industry? The Case of the Hungarian Microbreweries. Sustainability 2021, 13, 2829. [Google Scholar] [CrossRef]

- Madsen, E.S.; Gammelgaard, J.; Hobdari, B. (Eds.) New Developments in the Brewing Industry: The Role of Institutions and Ownership; Oxford University Press: Oxford, UK, 2020. [Google Scholar]

- Acitelli, T. The Audacity of Hops: The History of America’s Craft Beer Revolution; Chicago Review Press: Chicago, IL, USA, 2013. [Google Scholar]

- Tremblay, V.J.; Tremblay, C.H. The US brewing Industry: Data and Economic Analysis; MIT Press: Cambridge, MA, USA, 2004; ISBN 9780262201513. [Google Scholar]

- Pokrivčák, J.; Supeková, S.C.; Lančarič, D.; Savov, R.; Toth, M.; Vašina, R. Development of beer industry and craft beer expansion. J. Food Nutr. Res. 2019, 58, 63–74. [Google Scholar]

- Wessonn, T.; De Figueiredo, J.N. The impor-tance of focus to market entrants: A study of micro brewery performance. J. Bus. Ventur. 2001, 16, 377–403. [Google Scholar] [CrossRef]

- Reid, N.; McLaughlin, R.B.; Moore, M.S. From yellow fizz to big biz: American craft beer comes of age. Focus Geogr. 2014, 57, 114–125. [Google Scholar] [CrossRef]

- Kleban, J.; Nickerson, I. The US craft brew industry. In: Allied Academies International Conference. Int. Acad. Case Stud. Proc. 2011, 18, 33–38. [Google Scholar]

- Mier, T. Minipivovary a Řemeslné Pivovary; Národní Zemědělské Muzeum: Praha, Czech Republic, 2019; ISBN 978-80-88270-10-2. [Google Scholar]

- Carroll, G.R.; Swaminathan, A. Why the micro-brewery movement? Organizational dynamics of resource partitioning in the U.S. brewing indus-try. Am. J. Sociol. 2000, 106, 715–762. [Google Scholar] [CrossRef] [Green Version]

- Photiades, P. Beer Statistics—2017 Edition; Brewers of Europe: Brussels, Belgium, 2017; ISBN 9782960138290. Available online: https://www.brewersofeurope.org/uploads/mycms-files/documents/publications/2017/Statistics-201712-001.pdf (accessed on 25 June 2020).

- Goméz-Corona, C.; Escalona-Buendía, H.B.; Garcia, M.; Chollet, S.; Valentin, D. Craft vs. industrial: Habits, attitudes and motivations towards beer consumption in Mexico. Appetite 2016, 96, 358–367. [Google Scholar] [CrossRef]

- Aquilani, B.; Laureti, T.; Poponi, S.; Secondi, L. Beer choice and consumption determinants when craft beers are tasted: An exploratory study of con-sumer preferences. Food Qual. Prefer. 2015, 41, 214–224. [Google Scholar] [CrossRef]

- Tremblay, V.J.; Iwasaki, N.; Tremblay, C.H. The dynamics of industry concentration for U.S. micro and macro brewers. Rev. Ind. Organ. 2005, 26, 307–324. [Google Scholar] [CrossRef]

- Elzinga, K.G.; Tremblay, C.H.; Tremblay, V.J. Craft beer in the United States: History, numbers, and geography. J. Wine Econ. 2015, 10, 242–274. [Google Scholar] [CrossRef] [Green Version]

- Silberberg, E. Nutrition and the demand for taste. J. Political Econ. 1985, 93, 881–900. [Google Scholar] [CrossRef]

- Gruenewald, P.J.; Treno, A.J.; Nephew, T.M.; Ponicki, W.R. Routine activities and alcohol use: Constraints on outlet utilization. Alcohol. Clin. Exp. Res. 1995, 19, 44–53. [Google Scholar] [CrossRef]

- Voight, J. Big beer brands are fooling us with their crafty looks. In AdWeek [Online]; Adweek Network: New York, NY, USA, 31 March 2013; [cit. 23 October 2017]; Available online: http://www.adweek.com/brand-marketing/big-beer-brands-are-fooling-us-their-crafty-looks-148231/ (accessed on 30 July 2020).

- Hair, J.F.; Bush, P.R.; Ortinau, J.D. Marketing Research: A Practical Approach for the New Milenium; McGraw-Hill Higher Education: New York, NY, USA, 2000; ISBN 9780071164764. [Google Scholar]

- Kratochvíle, A. Pivovarství Českých Zemí v Proměnách 20. Století; Výzkumný Ústav Pivovarský a Sladařský: Praha, Czech Republic, 2005; ISBN 80-86576-16-7. [Google Scholar]

- Kandráčová, V.; Kulla, M. Brewing in Slovakia. In Geography and Geoinformatics: Challenge for Practise and Education: 19th International Conference: Proceedings; Masarykova Univerzita: Brno, Czech Republic, 2012; pp. 278–286. ISBN 9788021057999. [Google Scholar]

- Gow, H.R.; Swinnen, J. How Foreign Direct Investment Has Stimulated Growth in the Central and Eastern European Agri-Food Sectors: Vertical Contracting and the Role of Private Enforcement Capital; Policy Research Group Working Paper No. 18; Wisschenschaftsverlag, Vauk Kiel: Kiel, Germany, 1998. [Google Scholar]

- Czech Statistical Office of the Czech Republic; Czech Government: Praha, Czech Republic, 2020.

- Zákon č. 353/2003 Sb. Zákon o Spotřebních Daních./Act No. 353/2003 Coll. Act on Excise Duties; Czech Government: Praha, Czech Republic, 2003.

- Statistika a my. Časopis Českého Statistického Úřadu. Statistics and Us; Journal of the Czech Statistical Office: Prague, Czech Republic, 2020; Ročník 10; ISSN 1804–7149. [Google Scholar]

- Lantolf, J.P.; Bobrova, L. Happiness is drink-ing beer: A cross-cultural analysis of multimodal metaphors in American and Ukrainian commercials. Int. J. Appl. Linguist. 2012, 22, 42–66. [Google Scholar] [CrossRef]

- Ellis, V.; Bosworth, G. Supporting Rural Entrepre-(PDF) Development of Beer Industry and Craft Beer Expansion; Katholieke Universiteit Lueven: Lueven, Belgium, 1998. [Google Scholar]

- Pokrivčák, J.; Lančarič, D.; Savov, R.; Tóth, M. Craft beer in Slovakia. In Economic Perspectives on Craft Beer: A Revolution in the Global Beer Industry; Garavaglia, C., Swinnen, J., Eds.; Palgrave Macmillan: Cham, Switzerland, 2018; pp. 321–343. ISBN 9783319582344. [Google Scholar] [CrossRef]

- Pícha, K.; Navrátil, J. The factors of Lifestyle of Health and Sustainability influencing pro-environmental buying behaviour. J. Clean. Prod. 2019, 234, 233–241. [Google Scholar] [CrossRef]

- Pícha, K.; Navrátil, J.; Švec, R. Preference to Local Food vs. Preference to “National” and Regional Food. J. Food Prod. Mark. 2018, 24, 125–145, ISSN 1045-4446. [Google Scholar] [CrossRef]

- Euromonitor International. What’s Brewing in Craft Beer? [Analysis]. Research and Markets (the World’s Largest Market Research Store). 2019. Available online: portal.euromonitor.com/ (accessed on 20 September 2020).

- Swinnen, J.; Garavaglia, C. (Eds.) Economic Perspectives on Craft Beer. A Revolution in the Global Beer Industry; Springer: London, UK, 2018; pp. 3–54. [Google Scholar]

- Materna, K.; Hasman, J.; Hána, D. Acquisition of industrial enterprises and its relations with regional identity: The case of the beer industry in Central Europe. Nor. J. Geogr. 2019, 73, 197–214. [Google Scholar] [CrossRef]

- Capitello, R.; Maehle, N. Case Studies in the Beer Sector. Woodhead Publishing Series in Consumer Science and Strategic Marketing; Woodhead Publishing: Sawston, UK, 2020. [Google Scholar]

- Wojtyra, B. How and why did craft breweries “revolutionise” the beer market? The case of Poland. Morav. Geogr. Rep. 2020, 28, 81–97. [Google Scholar] [CrossRef]

- Wojtyra, B.; Kossowski, T.; Březinová, M.; Savov, R.; Lančarič, D. Geography of craft breweries in Central Europe: Location factors and the spatial dependence effect. Appl. Geogr. 2020, 124, 102325. [Google Scholar] [CrossRef]

- Török, Á.; Szerletics, A.; Jantyik, L. Factors Influencing Competitiveness in the Global Beer Trade. Sustainability 2020, 12, 5957. [Google Scholar] [CrossRef]

Figure 1.

Evolution of the number of breweries and craft breweries in Czechoslovakia and the Czech Republic (Czechoslovakia was divided into the Czech Republic and Slovakia in 1992).

Figure 1.

Evolution of the number of breweries and craft breweries in Czechoslovakia and the Czech Republic (Czechoslovakia was divided into the Czech Republic and Slovakia in 1992).

Figure 2.

Development of beer production and consumption in the Czech Republic in 2000–2019.

{kind=link}

{kind=link}

Table 1.

Characteristics of those craft breweries that are in the basic sample (all craft breweries in the Czech Republic) and characteristics of the chosen sample which is the representative sample of respondents.

Table 1.

Characteristics of those craft breweries that are in the basic sample (all craft breweries in the Czech Republic) and characteristics of the chosen sample which is the representative sample of respondents.

| Year of Foundation | Existence of an Establishment | ||

|---|---|---|---|

| Before 2000 | 8% | Yes, craft brewery has its own restaurant | 57% |

| 2000 to 2010 | 15% | No, craft brewery does not have its own restaurant | 43% |

| After 2010 | 77% | Region where brewery is located | |

| Production per year | South Bohemian/South Moravian | 8%/13% | |

| Less than 100 hL | 5% | Karlovy Vary/Hradec Králové | 2%/6% |

| 101–500 hL | 35% | Liberec/Moravian-Silesian | 3%/10% |

| 501–1000 hL | 33% | Olomouc/Pardubice | 7%/4% |

| Over 1000 hL | 27% | Plzeň/Prague | 9%/9% |

| Type of beer produced | Central Bohemian/Ústí | 12%/7% | |

| Only lagers | 34% | Vysočina/Zlín | 6%/4% |

| Only ALE and special beers (Porter, IPA, Bock, etc./Beers which contain more than 5.5% (ABV)) | 3% | Seat of craft brewery | |

| Both | 63% | In the municipality center | 51% |

| Share of lager production | On the outskirts of the municipality | 41% | |

| Less than 25% | 18% | Outside of the municipality | 8% |

| 25–50% | 50% | Number of employees | |

| 51–75% | 22% | 1–9 | 83% |

| Over 75% | 10% | 10 and more | 17% |

Table 2.

Production volume share of breweries, brewery groups and companies in the production volume of the Czech Republic for the year 2019.

Table 2.

Production volume share of breweries, brewery groups and companies in the production volume of the Czech Republic for the year 2019.

| Brewing Company, Group | Production Volume | Share in the Total Production Volume of the Czech Republic |

|---|---|---|

| Plzeňský prazdroj | 9,850,000 hL | 45.6% |

| Pivovary Staropramen | 3,920,000 hL | 20.8% |

| Heineken ČR | 1,924,000 hL | 8.9% |

| Budějovický Budvar | 1,600,000 hL | 4.7% |

| Pivovary Lobkowicz Group | 752,000 hL | 3.5% |

| LIV Group | 694,000 hL | 3.2% |

| AB InBev: | 140,000 hL | 0.6% |

| PMS Přerov | 720,000 hL | 3.3% |

| 22 independent breweries | 1,460,000 hL | 6.8% |

| 480 minibreweries | 540,000 hL | 2.5% |

| Total production volume of the Czech Republic | 21,600,000 hL | 100% |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Březinová, M. Beer Industry in the Czech Republic: Reasons for Founding a Craft Brewery. Sustainability 2021, 13, 9680. https://doi.org/10.3390/su13179680

AMA Style

Březinová M. Beer Industry in the Czech Republic: Reasons for Founding a Craft Brewery. Sustainability. 2021; 13(17):9680. https://doi.org/10.3390/su13179680

Chicago/Turabian StyleBřezinová, Monika. 2021. "Beer Industry in the Czech Republic: Reasons for Founding a Craft Brewery" Sustainability 13, no. 17: 9680. https://doi.org/10.3390/su13179680

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.