Study on the Spatial Evolution of China’s Pulp and Paper Product Import Trade and Its Influencing Factors

Abstract

:1. Introduction

2. Research Methods and Data Sources

2.1. Methods

2.1.1. Selection of Econometric Models

2.1.2. Trade Gravity Model

2.2. Index Selection and Data Sources

2.2.1. Major Trading Partners Selection

2.2.2. Theoretical Analysis

- (1)

- Demand side factors

- (2)

- Supply side factors

- (3)

- Price and cost factors

- (4)

- International environmental factors

- (5)

- Domestic policy factors

2.2.3. Data Sources

3. Results

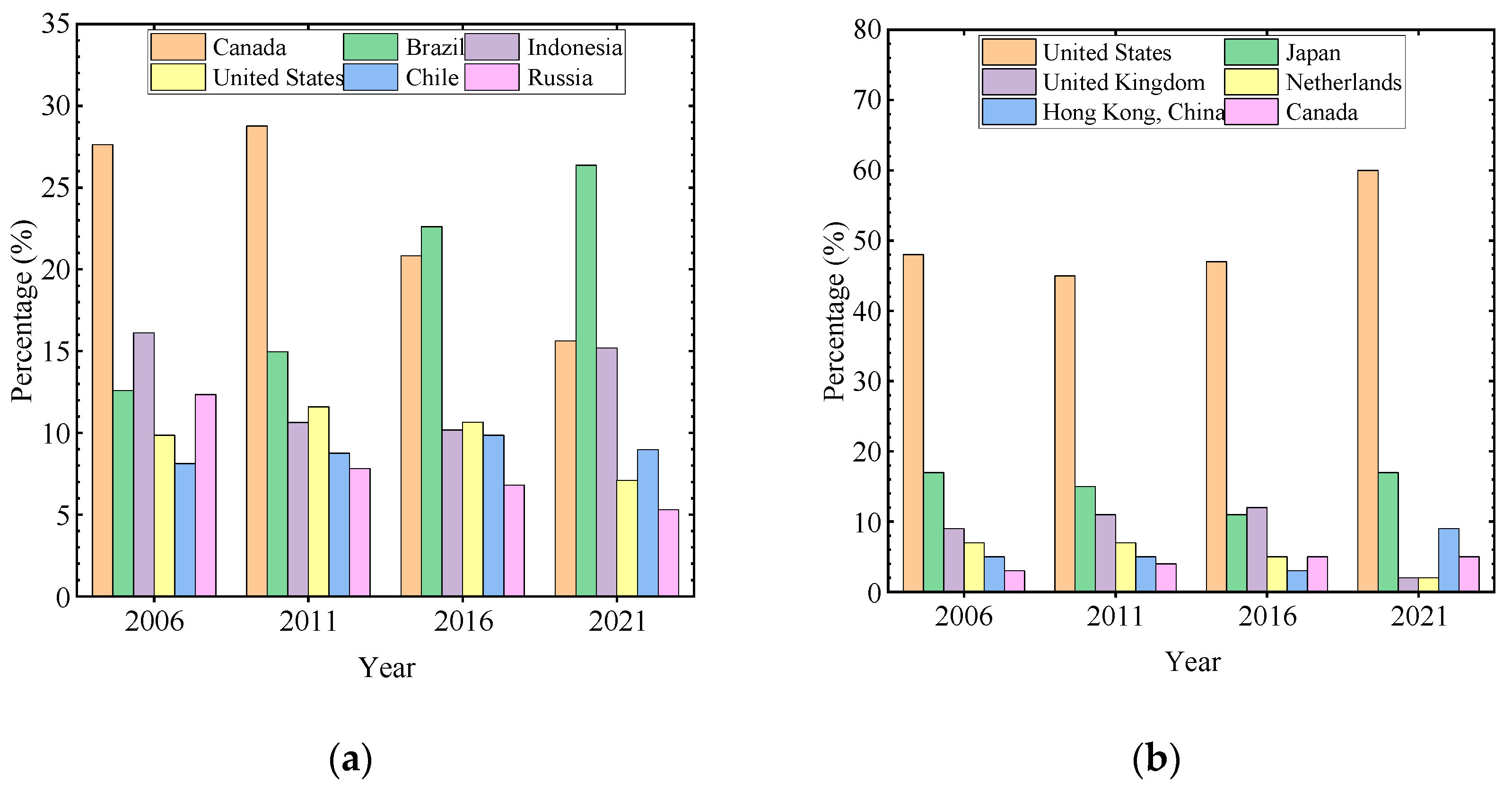

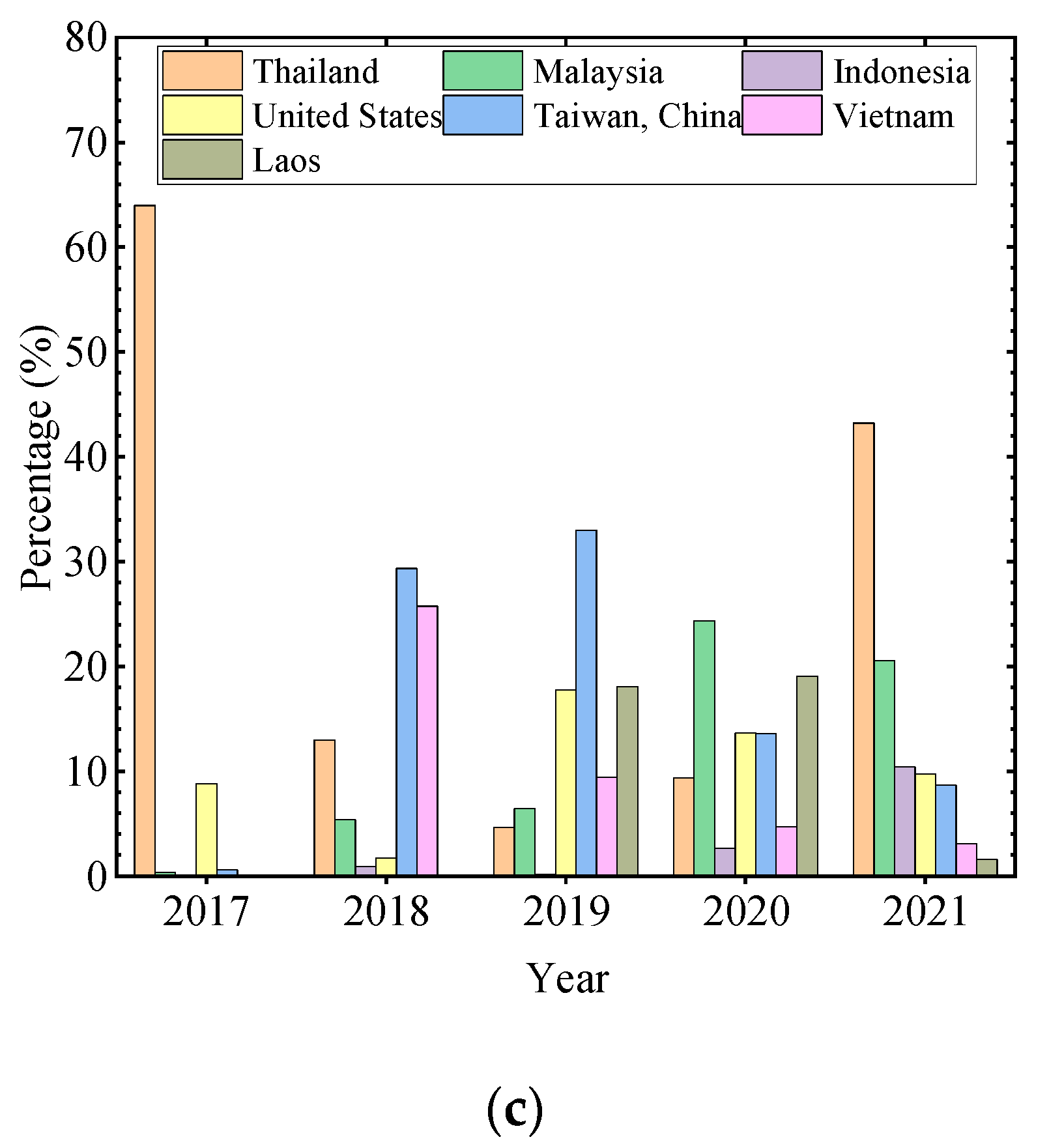

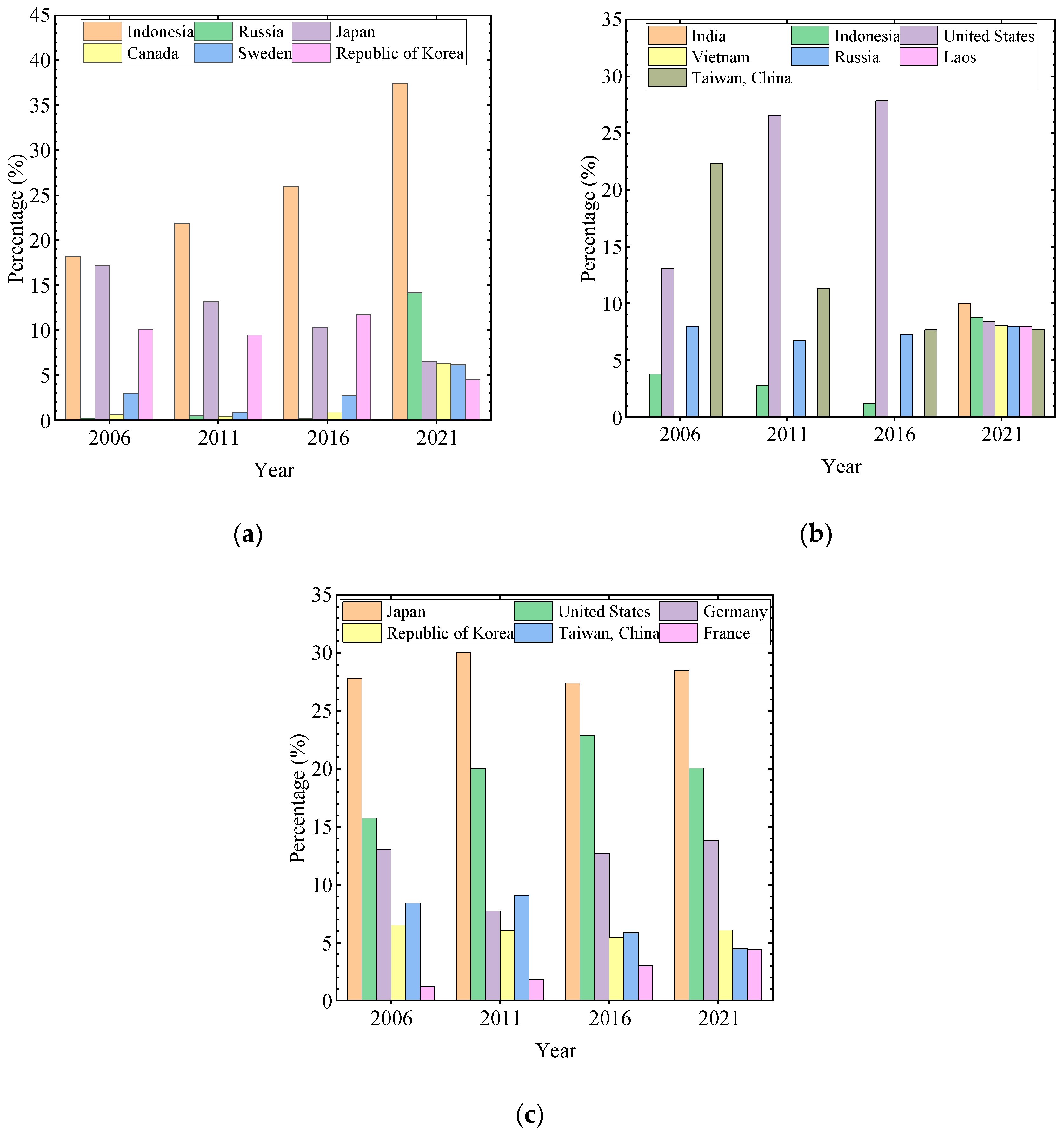

3.1. The Spatial Evolution of China’s Imports of Pulp and Paper Products

3.1.1. The Evolution of the Market Structure of Pulp and Paper Product Imports

3.1.2. The Evolution of the Market Structure of Paper Raw Material Imports

3.1.3. The Evolution of the Structure of the Paper Product Import Market

3.2. Panel Regression Results

3.2.1. Model Identification

3.2.2. Result of Factors Influencing the Spatial and Temporal Evolution of China’s Import Trade in Pulp and Paper Products

3.3. Robustness Tests

4. Discussion

4.1. Supply and Demand Factors

4.2. COVID-19 Pandemic, Waste Paper Restrictions, and US-China Trade Friction

5. Conclusions and Outlook

5.1. Conclusions

- (1)

- The increase in bilateral economic development significantly increases the proportion of wood pulp, waste pulp, and packaging paper products in the import structure of China’s pulp and paper products. The level of economic development on both the supply and demand sides of the trade is very significant. In this paper, the stable economic growth of both sides promotes the consumption of paper products, thus increasing the import of papermaking raw materials and packaging paper products in China.

- (2)

- The import proportion of pulp and paper products is negatively related to the cost factors of trade prices (including import prices, economic distance, and exchange rates). In particular, the increase in import prices significantly reduces the proportion of China’s imports of wood pulp and packaging paper products, while the increase in economic distance significantly reduces the proportion of China’s imports of wood pulp, waste paper, newsprint and printing paper, and industrial paper products. The increase in the exchange rate index significantly reduces the proportion of China’s imports of waste pulp, and China tends to import pulp and paper products with lower trade prices and costs.

- (3)

- The outbreak of the COVID-19 pandemic significantly increased China’s packaging paper product imports, while it showed a non-significant correlation with other pulp and paper product imports. The state of declining demand for packaging paper products at the beginning of the pandemic will improve with the coming of the post-pandemic era and the rapid development of the e-commerce logistics industry. The increase in demand for packaging paper imports has led to a rapid rise in the position of Indonesia as China’s main trading partner for paper imports.

- (4)

- The implementation of import restrictions on waste paper significantly promotes the importation of wood pulp, waste pulp, and various paper products in China. Due to the huge demand for paper products in China, the restriction on waste paper has prompted China’s paper companies to start increasing the importation of wood pulp and waste pulp to replace waste paper to meet China’s demand for paper raw materials. The focus of raw material imports has shifted from North America to South America and the Asia-Pacific region. In addition, for various types of paper products, especially newsprint and printing paper as well as packaging paper products, the proportion of imports will also increase accordingly. The Asia-Pacific region, such as India and Indonesia, is gaining ground as a trading partner with China.

- (5)

- Trade disputes between China and the United States significantly reduce China’s imports of wood pulp, waste paper, and packaging paper products. As the United States was China’s main import trade partner country for wood pulp, waste paper, and packaging paper products, China’s response to trade frictions between China and the United States in the imposition of tariff measures to a certain extent inhibits the normal importation of pulp and paper products, especially the raw materials for paper. Showing a decline in US partner status, the Southeast Asia region has gained importance.

5.2. Limitations and Prospects

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Wang, F.; Wu, M. The Impacts of COVID-19 on China’s Economy and Energy in the Context of Trade Protectionism. Int. J. Environ. Res. Public Health 2021, 18, 12768. [Google Scholar] [CrossRef] [PubMed]

- Gagnon, B.; MacDonald, H.; Hope, E.; Blair, M.J.; McKenney, D.W. Impact of the COVID-19 Pandemic on Biomass Supply Chains: The Case of the Canadian Wood Pellet Industry. Energies 2022, 15, 3179. [Google Scholar] [CrossRef]

- Tian, G. Study on China’s Import Trade and Market in Main Forest Products. Chin. For. Sci. Technol. 2005, 4, 5. [Google Scholar]

- Sun, X.; Katsigris, E.; White, A. Meeting China’s demand for forest products: An overview of import trends, ports of entry, and supplying countries, with emphasis on the Asia-Pacific region. Int. For. Rev. 2004, 3a4, 1–10. [Google Scholar] [CrossRef]

- Muhammad, A. The end of the trade war? Effects of tariff exclusions on US forest products in China. For. Policy Econ. 2021, 1, 1–10. [Google Scholar]

- Turner, J.; Maplesden, F.; Walford, B.; Jacobi, S. Tariff and non-tariff barriers to New Zealand’s exports of wood-based products to China. N. Z. J. For. 2005, 50, 27–33. [Google Scholar]

- Robbins, A.S.T.; Perezgarcia, J. Impacts of Illegal Logging Restrictions on China’s Forest Products Trade. Master’s Dissertation, University of Washington, Seattle, WA, USA, 2014. [Google Scholar]

- Zhang, J.; Li, F.; Liu, Y.; Cheng, B. An Assessment of Trade Facilitation’s Impacts on China’s Forest Product Exports to Countries Along the “Belt and Road” Based on the Perspective of Ternary Margins. Sustainability 2019, 11, 1298. [Google Scholar] [CrossRef] [Green Version]

- Yang, H.; Nie, Y.; Ji, C. Study on China’s timber resource shortage and import structure: Natural Forest Protection Program outlook, 1998 to 2008. For. Prod. J. 2010, 60, 408–414. [Google Scholar] [CrossRef] [Green Version]

- Gan, J.B. Effects of China’s WTO accession on global forest product trade. For. Policy Econ. 2004, 6, 509–519. [Google Scholar] [CrossRef]

- Jiang, H.; Guo, H.; Li, J. Analysis on Market Characteristics of China’s Forest Products Top Trade Partners. For. Econ. 2019, 41, 45–49. [Google Scholar]

- Chen, Y.; Wang, D.; Su, H.; Jiang, H.; Zhang, X. The Impact of Sino-US Trade War on Forest Products Trade and Its Countermeasures. Issues For. Econ. 2019, 39, 1–7. [Google Scholar]

- Bank, T.W. Indonesia—Production Forestry: Achieving Sustainability and Competitiveness. Pre-2003 Economic or Sector Report; Washington, DC, USA. 2015. Available online: http://documents.worldbank.org/curated/en/939711468268800796/Indonesia-production-forestry-achieving-sustainability-and-competitiveness (accessed on 20 February 2023).

- Sharma, R. Indonesian Pulp and Paper Industry. Pap. Asia 2006, 22, 9–11. [Google Scholar]

- Bajpai, P. Future Trends. Pulp Pap. Ind. 2015, 6, 315–320. [Google Scholar]

- Xiong, L.; Cheng, B. Study on Trade Cost of Forest Products in China and Its Influencing Factors. J. Int. Trade 2017, 419, 25–35. [Google Scholar]

- Li, W.; Wan, L.; Yuan, L. Study on the Influencing Factors of China’s Waste Paper Import Trade. Issues For. Econ. 2018, 38, 21–26+101. [Google Scholar]

- Tajdini, A. Estimating the Import Demand Function for Paper and Paper board Products in Iran. Austrian J. For. Sci. 2015, 4, 132–149. [Google Scholar]

- Zhang, D. Tariff and US Paper Products Trade. For. Sci. 2019, 65, 77–86. [Google Scholar] [CrossRef] [Green Version]

- Tang, S. Study on the influential Factors and International Competitiveness of China’s Paper Trade. Ph.D. Dissertation, Beijing Forestry University, Beijing, China, 2015. [Google Scholar]

- Wang, H.; Sui, D. Analysis on the Current Situation, Influencing Factors and Development Countermeasures of Pulp Import Trade in China. Econ. Forum 2019, 2, 116–120. [Google Scholar]

- Zhang, R.; Song, W. An Analysis of the Influencing Factors of Chinese Paper and Paperboard Imports. For. Econ. 2015, 37, 52–57. [Google Scholar]

- Wang, F.; Liu, S.; Cheng, B.; Jiang, Q.; Tian, Y.; Xiong, L. How Can Intra-Industry Trade of Forest Products be Promoted? An Empirical Analysis from China. Forests 2019, 10, 882. [Google Scholar] [CrossRef] [Green Version]

- Cai, X.; Tian, M.; Cai, F.; Wu, C.; Han, M. Empirical Analysis on the Influencing Factors of the Wood Pulp Import in China. For. Econ. 2013, 6, 58–69. [Google Scholar]

- Zhang, D.; Li, Y. Forest endowment, logging restrictions, and China’s wood products trade. Chin. Econ. Rev. 2009, 20, 46–53. [Google Scholar] [CrossRef]

- Sun, L. Research on Interaction Between Foreign Trade of Paper Products and the Development of China’s Paper Industry. For. Econ. 2012, 244, 61–65. [Google Scholar]

- Luo, J. Chinese Newsprint and Printing & Writing Paper Industry. Master’s Dissertation, School of Economics Georgia Institute of Technology, Atlanta, GA, USA, 2003. [Google Scholar]

- Phillips, R.B. Global dynamics of the pulp and paper industry-2013. N. Z. J. For. 2013, 58, 34–42. [Google Scholar]

- Duan, X. The Research of Environment Regulation Effects on Forests Paper Products Trade in China. Master’s Dissertation, South China Agricultural University, Guangzhou, China, 2018; pp. 48–49. [Google Scholar]

- Okoro, S. China’s new policy triggers global change: Capitalization opportunities from imported waste paper policy. China Pap. 2019, 40, 36–39. [Google Scholar]

- Ma, Z.; Yi, Y.; Chen, W.; Wang, P.; Wang, C.; Zhang, C.; Gan, J. Material Flow Patterns of the Global Waste Paper Trade and Potential Impacts of China’s Import Ban. Environ. Sci. Technol. 2021, 55, 8492–8501. [Google Scholar] [CrossRef]

- Shang, D.; Diao, G.; Liu, C.; Yu, L. Study on the Impacts of China’s Waste Paper Import Restrictive Policies on the Cycle Synchronization between the Chinese and International Waste Paper Markets. J. For. Econ. 2022, 37, 295–318. [Google Scholar] [CrossRef]

- Cheng, Y. Impact of China’s New Solid Waste Import Policy on Waste Paper Trade—Based on Historical Data Analysis. J. Hubei Coll. Econ. 2020, 17, 28–30. [Google Scholar]

- Di, S.; Gang, D.; Zhao, X. Have China’s regulations on imported waste paper improved its quality. For. Policy Econ. 2020, 119, 102287. [Google Scholar] [CrossRef]

- Feng, S.; Chen, K. Impact of Environmental Information Disclosure Policy and Trade on Chinese Paper Industry Environmental Effects. Int. J. Environ. Res. Public Health 2022, 19, 11614. [Google Scholar] [CrossRef]

- Zhang, L.; Meng, Z. The impact of carbon peaking and carbon neutrality on the paper industry in the 14th Five-Year Plan period. China Pap. 2021, 42, 9–13. [Google Scholar]

- Yang, Y.C. Environmental Regulation and International Trade. Ph.D. Dissertation, University of Connecticut, Storrs, CT, USA, 2006. [Google Scholar]

- Huang, J.; Wu, Z. Impact of Environmental Regulations on Export Trade—Empirical Analysis Based on Zhejiang Province. Int. J. Environ. Res. Public Health 2022, 19, 12569. [Google Scholar] [CrossRef] [PubMed]

- Tian, G.; Yu, W.; Vu, T.T.H.; Ma, G.-Y. Green Assessment of Imports and Exports of Wooden Forest Products Based on Forest Processing Industry: A Case Study of China. Forests 2021, 12, 166. [Google Scholar] [CrossRef]

- Zhang, F. The Impact of Trade Dispute on Import Demand for Coated Graphic Printing Paper Products in the U.S. In Proceedings of the 2015 Society of American Foresters Annual Convention, Baton Rouge, LA, USA, 3–7 November 2015. [Google Scholar]

- Han, J.; Song, J. Impact of Sino-US Trade Friction on Import and Export Trade Pattern of Soybean in Heilongjiang. Asian Agric. Res. 2019, 3, 4. [Google Scholar]

- Yu, L.; Chen, Y.F.; Han, Y.J. Evolution characteristics and policy implications of the global soybean trade network. Res. Agric. Mod. 2019, 40, 674–682. [Google Scholar]

- Yue, L.; Lou, C.; Du, Y.; Tu, X. An Analysis of the Impact of Sino-US Trade Friction Based on the Tariff Lists. J. Financ. Econ. 2019, 45, 59–72. [Google Scholar]

- Zhang, W.; Zhang, X.; Wang, Y. The Impact of Sino-US Trade Friction on China’s Forest Products Trade—A Simulation Analysis Based on GTAP Model. For. Econ. 2019, 41, 3–9. [Google Scholar]

- Gan, J.B. Forest certification costs and global forest product markets and trade: A general equilibrium analysis. Can. J. For. Res. 2005, 35, 1731–1743. [Google Scholar] [CrossRef]

- Chen, J.; Wang, L.; Li, L.; Magalhães, J.; Song, W.; Lu, W.; Xiong, L.; Chang, W.; Sun, Y. Effect of Forest Certification on International Trade in Forest Products. Forests 2020, 11, 1270. [Google Scholar] [CrossRef]

- Zhang, J.; Zhao, Z.; Zhao, W.; Tao, C.; Cheng, B. The Impact of Forest Certification on the Ternary Margins of China’s Forest Product Export. Forests 2022, 13, 1313. [Google Scholar] [CrossRef]

- Millan. WTO dispute settlement proceeding regarding China-countervailing and anti-dumping duties on grain oriented flat-rolled electrical steel from the United States-recourse by the United States to article 21.5 of the dsu. Fed. Regist. 2009, 79, 13731–13732. [Google Scholar]

- Shen, Y.; Yan, H.; Wei, W.U. Anti-Dumping, Industry Protection and SMEs Development: Reflection on the Case of Chinese Coated Paper. In Proceedings of the 12th West Lake International Conference on Small & Medium Business, Hangzhou, China, 24–26 October 2010. [Google Scholar]

- Qiu, X.; Yu, J. Changes in the rules of the international competitive environment of China’s paper industry and their impact—An analysis based on a low-carbon perspective. Pract. Foreign Econ. Relat. Trade 2014, 9, 40–43. [Google Scholar]

- Buongiorno, J. GFPMX: A Cobweb Model of the Global Forest Sector, with an Application to the Impact of the COVID-19 Pandemic. Sustainability 2021, 13, 5507. [Google Scholar] [CrossRef]

- Zanello, R.; Shi, Y.; Zeinolebadi, A.; Kooten, G. COVID-19 and the Mystery of Lumber Price Movements. Forests 2023, 14, 152. [Google Scholar] [CrossRef]

- Muhammad, A.; Hellwinckel, C.M.; Anosike, E.; Taylor, A. Economic Impact of the COVID-19 Pandemic on Tennessee Forest Product Exports; Extension Report; University of Tennessee: Knoxville, TN, USA, 2022. [Google Scholar]

- Morland, C.; Schier, F.; Weimar, H. The Structural Gravity Model and Its Implications on Global Forest Product Trade. Forests 2020, 11, 178. [Google Scholar] [CrossRef] [Green Version]

- Shen, X.; Lovri, M. Structural determinants of global trade in graphic paper and pulp products. For. Policy Econ. 2022, 134, 102629. [Google Scholar] [CrossRef]

- Jonsson, R. Trends and Possible Future Developments in Global Forest-Product Markets—Implications for the Swedish Forest Sector. Forests 2011, 2, 147–167. [Google Scholar] [CrossRef] [Green Version]

- Nasrullah, M.; Liu, C.; Khan, K.; Rizwanullah, M.; Zulfiqar, F.; Ishfaq, M. Determinants of forest product group trade by gravity model approach: A case study of China. For. Policy Econ. 2020, 113, 102117. [Google Scholar] [CrossRef]

- Guan, Z.; Sheong, J. Determinants of bilateral trade between China and Africa: A gravity model approach. J. Econ. Stud. 2020, 47, 1015–1038. [Google Scholar] [CrossRef]

- Tae-Young, K.; Kyung-Ae, A. The Effects of WTO Trade Facilitation on Bilateral Trade Flows: Spatial Gravity Model Approach. Korea Trade Rev. 2014, 39, 161–183. [Google Scholar]

- Zhang, H. A Review of Extensions and Applications of Trade Gravity Models. Bus. Econ. 2010, 2, 68–70. [Google Scholar]

- Bakouan, M.; Ouedraogo, I.M. Intra-African Trade and Spatial Dependence: Revisiting Africa Intra-Trade Determinants with a Spatial Structural Gravity Model. Theor. Econ. Lett. 2022, 12, 149–171. [Google Scholar] [CrossRef]

- Yue, Y.; Xie, D. Study of Factors Influencing China-ASEAN Agricultural Product Trade Development in the Context of “the Belt and Road”. Asian Agric. Res. 2021, 12, 20–26. [Google Scholar]

- Joseph, B. Gravity models of forest products trade: Applications to forecasting and policy analysis. Forestry 2016, 89, 117–126. [Google Scholar]

- Wu, T.; Zhang, B.; Cao, Y.; Sun, P. Impact of Multi-Dimensional and Dynamic Distance on China’s Exports of Wooden Forest Products to Countries along the “Belt and Road”. Sustainability 2020, 12, 3339. [Google Scholar] [CrossRef] [Green Version]

- Tian, M.; Niu, J.; Chen, K.; Chen, J.; Cheng, J. Analysis of the Impact of Sino-US Trade Friction on International Trade of Chinese Wood Forest Products. Issues For. Econ. 2022, 42, 449–461. [Google Scholar]

- Wang, M. New Changes in the global trade pattern in the post-epidemic era and China’s policy response. Prices Mon. 2022, 5, 34–41. [Google Scholar]

- Shah, P. COVID-19 Impact Analysis on Logistics Industry. 2020. Available online: https://xueshu.baidu.com/usercenter/paper/show?paperid=1b0y00g0jg7r0aw0hy0u0v60c9032591&site=xueshu_se&hitarticle=1%E2%80%9D (accessed on 20 February 2023).

- Niu, Q. Zero imports after the domestic paper recycling industry how to deal with opportunities and challenges. China Pap. Newsl. 2021, 2, 13–16. [Google Scholar]

- Kawasaki, T.; Wakashima, H.; Shibasaki, R. The use of e-commerce and the COVID-19 outbreak: A panel data analysis in Japan. Transp. Policy 2021, 115, 88–100. [Google Scholar] [CrossRef]

- Fang, J. Analysis of the impact of the new crown epidemic on the packaging paper market in 2020. China Pulp Pap. Ind. 2021, 42, 59–60. [Google Scholar]

- Halim, M.A. The Impact of E-commerce on Consumer Purchasing Behavior for the Coronavirus Disease (COVID-19). Sustain. Bus. Econ. 2022, 5, 9. [Google Scholar]

- Zhao, H.; Wangm, L. Global waste paper market: A shifting trade landscape. China Pulp Pap. Ind. 2021, 42, 57–59. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Pulp and Paper Products | Trade Share (%) | Raw Materials | Trade Share (%) | Paper Products | Trade Share (%) | Wood Pulp | Trade Share (%) | Waste Paper | Trade Share (%) |

|---|---|---|---|---|---|---|---|---|---|

| Brazil | 22 | Brazil | 22 | Indonesia | 12 | Brazil | 26 | US | 60 |

| Indonesia | 16 | Indonesia | 16 | Japan | 10 | Canada | 16 | Japan | 17 |

| Canada | 10 | Canada | 14 | US | 9 | Indonesia | 15 | Hong Kong | 9 |

| Chile | 8 | Chile | 9 | Sweden | 7 | Chile | 9 | Canada | 5 |

| US | 7 | US | 8 | Russia | 7 | US | 7 | UK | 2 |

| Sweden | 4 | Finland | 8 | Taiwan | 6 | Russia | 5 | Netherlands | 2 |

| Japan | 3 | Russia | 5 | Republic of Korea | 6 | ||||

| Taiwan | 1 | Thailand | 3 | Laos | 5 | ||||

| Waste Pulp | Trade Share (%) | Newsprint and Printing Paper | Trade Share (%) | Packaging Paper | Trade Share (%) | Industrial Paper | Trade Share (%) | ||

| Thailand | 43 | Indonesia | 37 | India | 11 | Japan | 29 | ||

| Malaysia | 21 | Russia | 14 | Indonesia | 10 | US | 20 | ||

| Indonesia | 10 | Japan | 7 | US | 9 | Germany | 14 | ||

| US | 10 | Canada | 6 | Vietnam | 9 | Republic of Korea | 6 | ||

| Taiwan | 9 | Sweden | 6 | Russia | 9 | Taiwan | 4 | ||

| Vietnam | 3 | Republic of Korea | 5 | Laos | 9 | France | 4 | ||

| Laos | 2 | Taiwan | 9 |

| Variable | Indicator Description | Unit | |

|---|---|---|---|

| Explained variables | IMP | Proportion of pulp imported by trading partners | % |

| IMPP | Proportion of paper products imported by trading partners | % | |

| Explanatory variables | PGDPC | GDP per capita in China | dollar |

| PGDP | GDP per capita of trading partners | dollar | |

| DIS | Economic distance between trade supply and demand | km/dollar | |

| ROE | Exchange rate index | _ | |

| PERM3 | Pulpwood production per capita of trading partners | M3/ | |

| PRICE | Trade price of pulp and paper products | dollar | |

| ANTI | China’s anti-dumping duty on US, Europe, and Japan | ||

| COVID-19 | COVID-19 pandemic | _ | |

| BAN | China’s restrictions on waste paper imports | _ | |

| WAR | Trade disputes between China and the United States | _ |

| Variables | F-Test | LM Test | Hausman Test |

|---|---|---|---|

| Wood pulp | 63.88 *** | 55.94 *** | 55.21 *** |

| 0.00 | 0.00 | 0.00 | |

| Waste pulp | 8.81 *** | 69.62 *** | 34.53 *** |

| 0.00 | 0.00 | 0.00 | |

| Waste Paper | 16.86 *** | 145.38 *** | 26.84 *** |

| 0.00 | 0.00 | 0.00 | |

| Newsprint and printing paper | 7.25 *** | 56.7 *** | 29.14 *** |

| 0.00 | 0.00 | 0.00 | |

| Packaging paper | 11.6 *** | 192.1 *** | 67.78 *** |

| 0.00 | 0.00 | 0.00 | |

| Industrial Paper | 48.30 *** | 55.61 *** | 116.41 *** |

| 0.00 | 0.00 | 0.00 |

| Variables | Wood Pulp | Waste Pulp | Waste Paper | Newsprint and Printing Paper | Packaging Paper | Industrial Paper |

|---|---|---|---|---|---|---|

| LNPGDPC | 1.834 *** | 5.406 *** | 0.930 | 1.042 | 5.016 *** | 0.0329 |

| (0.197) | (1.266) | (0.714) | (0.796) | (1.473) | (0.262) | |

| LNPGDP | 3.090 *** | 17.63 *** | 8.767 ** | 0.134 | 12.98 *** | 1.189 |

| (0.604) | (3.097) | (3.502) | (2.206) | (3.191) | (0.783) | |

| LNDIS | −0.109 * | −0.775 | −5.189 * | −0.614 ** | −0.361 | −0.364 ** |

| (0.0573) | (0.548) | (2.930) | (0.261) | (0.400) | (0.141) | |

| LNROE | −0.0432 | −0.327 * | −0.0468 | −0.0553 | −0.0609 | −0.00336 |

| (0.0318) | (0.175) | (0.0541) | (0.120) | (0.129) | (0.0328) | |

| LNPERM3 | 1.117 *** | 0.415 | 0.203 | 1.448 | 0.217 | 0.0291 |

| (0.219) | (0.479) | (0.308) | (1.207) | (0.595) | (0.219) | |

| LNPRICE | −0.448 * | −0.0195 | −0.00175 | −0.272 | −2.740 *** | −0.00705 |

| (0.252) | (0.323) | (0.418) | (0.258) | (0.606) | (0.0277) | |

| WAR | −0.306 * | −0.942 | −0.667 * | −0.465 | −0.247 * | −0.282 |

| (0.172) | (1.023) | (0.373) | (0.947) | (0.713) | (0.219) | |

| COVID-19 | −0.0169 | −0.326 | −1.407 *** | −0.445 | 1.285 * | −0.0350 |

| (0.153) | (0.891) | (0.349) | (0.812) | (0.715) | (0.224) | |

| BAN | 0.156 *** | 4.643 *** | −0.742 *** | 0.686 ** | 1.816 *** | 0.156 |

| (0.149) | (0.926) | (0.269) | (0.739) | (0.606) | (0.162) | |

| ANTI | −0.741 | −0.152 | ||||

| (0.812) | (0.139) | |||||

| Constant | 32.54 *** | −116.6 *** | −97.48 ** | 0.671 | −46.34 ** | 21.43 *** |

| (5.171) | (24.24) | (45.96) | (17.91) | (20.58) | (7.006) | |

| Observations | 304 | 304 | 304 | 304 | 304 | 304 |

| R-squared | 0.829 | 0.721 | 0.632 | 0.410 | 0.737 | 0.370 |

| p-value | 0.0004 | 0.0006 | 0.000 | 0.0016 | 0.0000 | 0.0013 |

| Variables | Wood Pulp | Waste Pulp | Waste Paper | Newsprint and Printing Paper | Packaging Paper | Industrial Paper |

|---|---|---|---|---|---|---|

| WAR | −0.094 * | −5.064 | −0.521 * | −0.163 | −0.477 * | −0.0324 |

| (0.189) | (1.207) | (0.358) | (0.873) | (0.721) | (0.206) | |

| COVID-19 | −0.321 | −0.619 | −1.192 *** | −0.227 | 0.321 * | −0.274 |

| (0.167) | (0.842) | (0.362) | (0.802) | (0.618) | (0.182) | |

| BAN | 0.0855 *** | 1.770 *** | −0.157 *** | 0.709 ** | 1.940 *** | 0.177 |

| (0.161) | (1.087) | (0.294) | (0.643) | (0.629) | (0.184) | |

| R-squared | 0.821 | 0.660 | 0.611 | 0.420 | 0.762 | 0.380 |

| p-value | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.001 |

| Variables | Wood Pulp | Waste Pulp | Waste Paper | Newsprint and Printing Paper | Packaging Paper | Industrial Paper |

|---|---|---|---|---|---|---|

| L.IMP | 1.405 *** | 0.7447 ** | 1.231 *** | 1.2781 *** | 1.8538 *** | 0.3308 *** |

| (0.1748) | (0.3198) | (0.3838) | (0.0653) | (0.6378) | (0.4095) | |

| LNPGDPC | 1.569 *** | 9.758 *** | 2.410 | 1.14 | 10.15 *** | 2.919 |

| (0.032) | (0.052) | (0.657) | (0.820) | (0.095) | (1.754) | |

| LNPGDP | 2.718 *** | 12.65 ** | 7.92 ** | 5.089 | 10.88 *** | 5.858 |

| (0.846) | (0.403) | (0.076) | (5.365) | (0.091) | (1.956) | |

| LNDIS | −0.275 * | −0.424 | −6.21 ** | −0.345 ** | −2.770 | −1.639 *** |

| (0.154) | (2.182) | (2.451) | (0.722) | (7.126) | (0.243) | |

| LNROE | −0.00178 | −0.235 * | −0.0276 | −0.0525 | −0.159 | −0.0111 |

| (0.0316) | (0.216) | (0.0377) | (0.0929) | (0.131) | (0.0213) | |

| LNPERM3 | 0.518 *** | 0.657 | 0.469 | 1.719 | 0.598 | 0.647 |

| (0.570) | (1.138) | (0.527) | (1.469) | (0.655) | (0.592) | |

| LNPRICE | −0.763 * | −0.330 | −0.659 | −0.373 | −1.478 *** | −0.0129 |

| (0.501) | (0.504) | (0.375) | (0.205) | (1.110) | (0.0144) | |

| WAR | −0.235 * | −0.582 | −0.426 * | −1.901 | −1.932 * | −0.313 |

| (0.334) | (2.150) | (0.395) | (0.874) | (1.323) | (0.291) | |

| COVID-19 | −0.178 | −1.469 | −0.735 ** | −0.419 | 2.805 ** | −0.0292 |

| (0.279) | (1.999) | (0.518) | (0.315) | (1.267) | (0.233) | |

| BAN | 0.270 *** | 3.727 *** | −0.105 *** | 0.320 ** | 3.340 *** | 0.154 |

| (0.235) | (1.522) | (0.237) | (0.499) | (1.066) | (0.138) | |

| ANTI | −3.340 | −0.154 | ||||

| (1.066) | (0.138) | |||||

| Observation | 304 | 304 | 304 | 304 | 304 | 304 |

| AR (1) | −2.517 ** | −2.378 ** | −3.39 *** | −2.11 ** | −2.026 ** | −2.74 *** |

| AR (2) | 1.53 | −0.381 | 0.85 | 1.34 | 1.428 | −0.74 |

| Sargan | 67.64 | 69.07 | 71.46 | 70.25 | 68.8 | 60.16 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cheng, H.; Wang, J.; Hu, M. Study on the Spatial Evolution of China’s Pulp and Paper Product Import Trade and Its Influencing Factors. Forests 2023, 14, 674. https://doi.org/10.3390/f14040674

Cheng H, Wang J, Hu M. Study on the Spatial Evolution of China’s Pulp and Paper Product Import Trade and Its Influencing Factors. Forests. 2023; 14(4):674. https://doi.org/10.3390/f14040674

Chicago/Turabian StyleCheng, Huiying, Jinfang Wang, and Mingxing Hu. 2023. "Study on the Spatial Evolution of China’s Pulp and Paper Product Import Trade and Its Influencing Factors" Forests 14, no. 4: 674. https://doi.org/10.3390/f14040674