1. Introduction

The Electric Reliability Council of Texas (ERCOT) uses locational marginal pricing [

1] to set the spot electricity prices in its day-ahead market (DAM) and real-time market (RTM) [

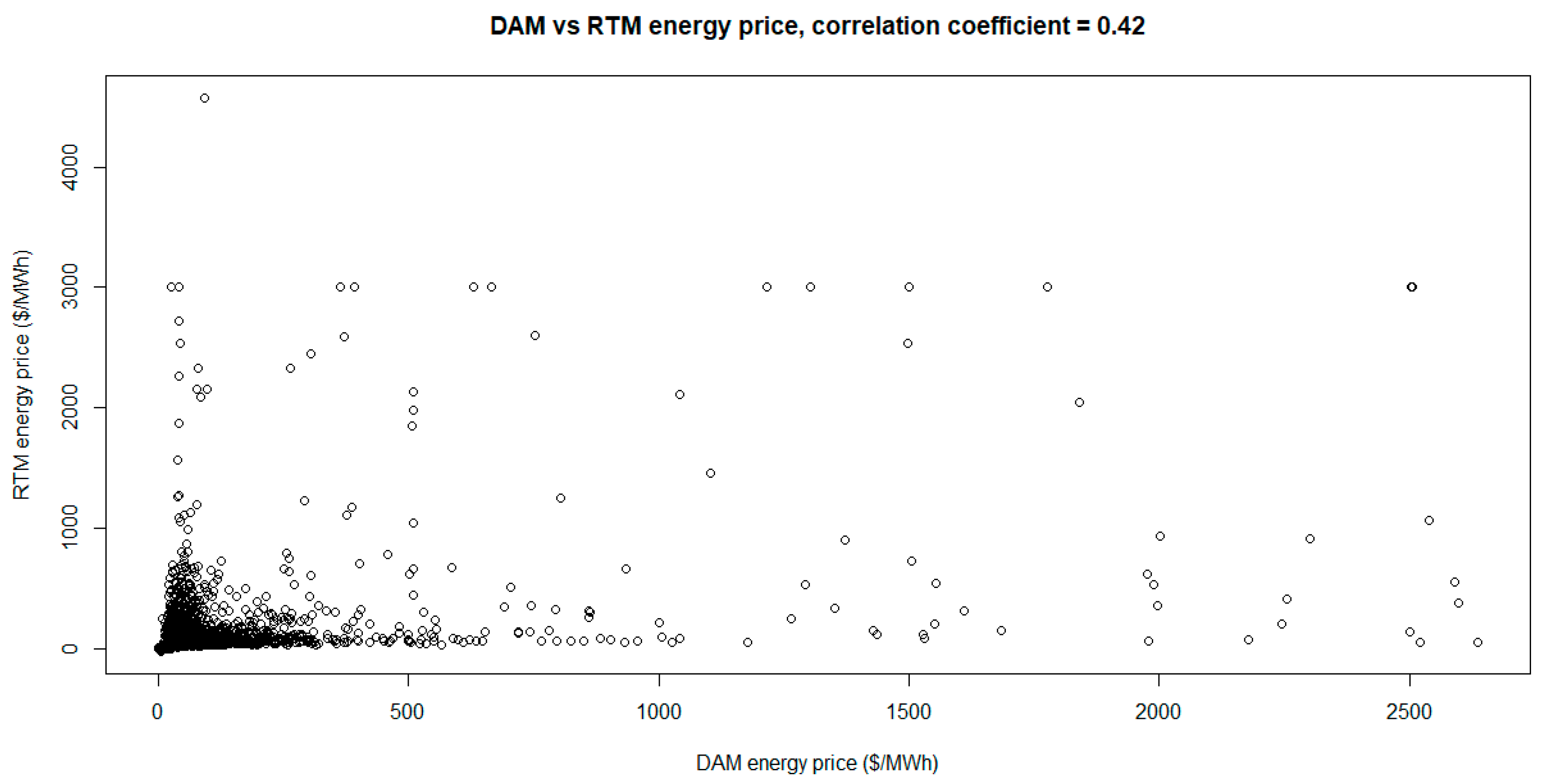

2]. Varying with the day-ahead forecasts of fundamental drivers of natural gas price, system load, ancillary services requirements, nuclear generation, and wind generation, the volatile DAM prices move the even more volatile RTM prices shown in

Figure 1, which is a reproduction from [

3].

When ERCOT’s retail market first opened in 2002, a qualified scheduling entity (QSE) must show that its projected aggregate supply had been procured through bilateral contracts and other means to meet its projected aggregate demand. A balancing energy market was created to resolve the mismatch between the QSE’s projected and actual schedules of aggregate demand and supply. The QSE is responsible for commercial transactions involving multiple retail electric providers (REPs). Hence, the energy shortfall of one REP could be offset by the surplus energy of another REP within the QSE’s portfolio of REPs (

www.ercot.com/files/docs/2005/11/07/360prr_relaxed_balanced_schedules.doc; accessed on 27 May 2022).

The balanced schedule requirement was gradually relaxed, as ERCOT established a DAM in December 2010 that transformed the balancing energy market into today’s RTM (Zarnikau et al., 2014). Hence, a REP in Texas can now decide whether and how to manage its procurement cost risk caused by spot price volatility and sales fluctuation, as exemplified by two case studies of a load serving entity in Florida [

4,

5].

A REP’s procurement cost for serving the unhedged portion of the total load can explode during market conditions of scarcity, exacerbated by the various “adders” that apply to RTM prices (e.g., reliability deployment price adder) and operating reserve demand curve (ORDC) adder [

6]). The reliability deployment price adder is designed to prevent prices from being depressed when ERCOT takes an out-of-market action, such as ordering a power plant to operate to maintain the reliability of the system or orders the deployment of a demand response program. See ERCOT Protocols, Section 6.5.7.3.1 at

https://www.ercot.com/mktrules/nprotocols/current, (accessed on 27 May 2022). In addition, real-time ORDC price adders occur when ERCOT’s physical operating reserve dips below a pre-set threshold. This phenomenon raises a substantive research question: can a small and risk-averse REP insure its procurement cost risk due to large spot price spikes in ERCOT’s energy markets? This question accentuates our paper’s primary focus of designing an insurance scheme to reduce the REP’s procurement cost risk exposure to the price spikes during ERCOT’s critical hours of low physical capacity reserve due to high system demand and/or generation plant outages.

The same question is similarly important and relevant for other regions with volatile wholesale market prices that a competitive retailer inevitably faces. A partial list of these regions includes (a) the states served by the regional transmission organizations of PJM Interconnection, ISO New England, and New York ISO in the US; (b) the provinces of Alberta and Ontario in Canada; (c) Asia-Pacific countries such as Australia, New Zealand, and Singapore; (d) countries in the European Union (

https://www.europarl.europa.eu/factsheets/en/sheet/45/internal-energy-market; accessed on 27 May 2022); and (e) South American countries such as Brazil and Chile [

9,

10].

To answer the question in Texas’s context, we propose an insurance that a small and risk-averse REP may buy to manage its procurement cost risk. Our proposed insurance comes from the first author’s research funded by several electric utilities in North America. As such, it aims for practicality, rather than highly technical details often related to the pricing of electricity derivatives (e.g., [

11,

12]) and recently proposed insurance schemes (e.g., [

13,

14,

15,

16]). While aiding the REP to avoid financial insolvency, our proposed insurance is profitable for insurance sellers voluntarily participating in the REP’s internet-based procurement auction described in

Section 4.2. Hence, it is a newly developed wholesale market product that deserves consideration by REPs in Texas and competitive retailers elsewhere.

Complementing extant studies on electricity risk management (e.g., [

5,

11,

12,

17,

18,

19,

20]), our proposed insurance is, to the best of our knowledge, a newly developed wholesale market product for use by a competitive retailer like those in Texas. Its practical pricing, design and implementation explained in

Section 4 show that it differs from (a) the currently available electricity products described in

Section 3 and (b) the insurance proposals for managing the risks related to system reliability [

13], distributed generation [

14], real-time pricing of energy consumption [

15], power plant performance (

https://www.munichre.com/hsb/en/products.html; accessed on 27 May 2022), and transmission and distribution [

16].

The rest of this paper proceeds as follows.

Section 2 states a REP’s risk management problem. This section purposedly omits a literature review of the voluminous studies on electricity risk management because (a) such a review is an unnecessary distraction from our narrowly focused paper; and (b) general overviews of electricity risk management are already available (e.g., [

12,

17]).

Section 3 describes electricity products currently available for the REP’s risk management.

Section 4 explains our proposed insurance’s design, pricing, and implementation.

Section 5 is an indicative calculation of the insurance per MWh premium, whose empirics are reported in

Section 6.

Section 7 concludes.

2. Risk Management Problem of a Small REP in Texas

To provide a contextual background of our proposed insurance, consider the risk management problem in connection to a small REP’s fixed price plan [

21]. The plan’s fixed price is

$G/MWh for generation, which inevitably differs from the wholesale spot price

$P/MWh after contract signing. For simplicity, we assume that

G is mainly driven by

P because the cost of ancillary services and the cost associated with other charges imposed by ERCOT are relatively small and fully passed through to the REP’s customers. The REP earns ex post profit of

$(

G −

P) for each MWh procured from the spot market for resale. Unfortunately,

Figure 1 shows that

P may surge above

G, resulting in ex post loss of

$(

P −

G)/MWh. Thus, retail fixed pricing can cause the REP to face large financial risk exposure if it decides not to hedge adequately. Parenthetically, this outcome also applies to time-of-use and pre-pay plans with prices that do not closely track the fast-changing spot market prices in their delivery periods.

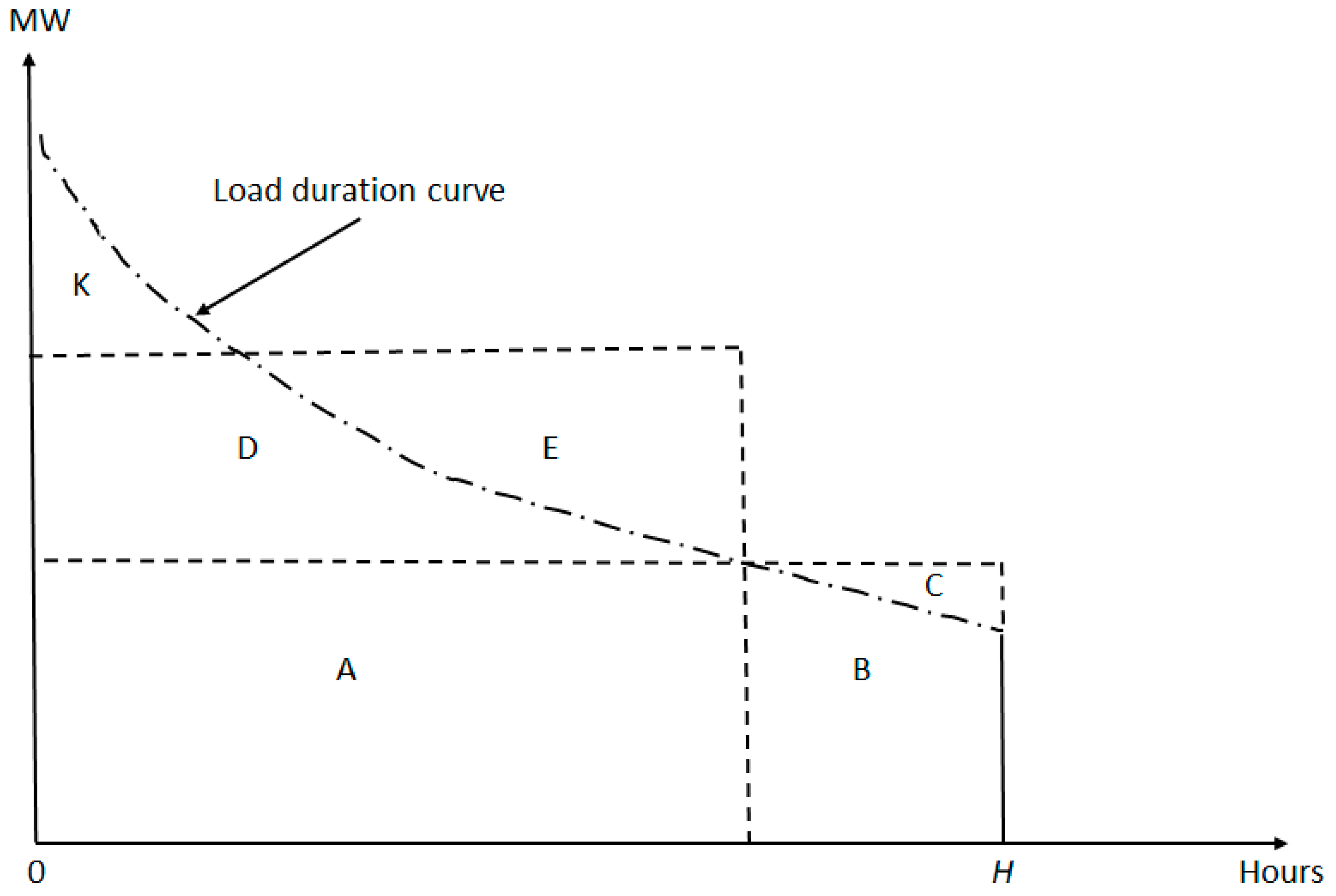

Figure 2 is an illustrative example of the REP’s risk management problem under the assumption that the load duration curve (LDC) can be accurately forecasted [

4,

5]. The LDC forecast can be made using time series modeling of the REP’s aggregate hourly load data. Alternatively, it can be based on a bottom-up approach that uses the data for (1) the average load profiles of customer segments differentiated by consumption size and residence type (e.g., apartment, town house, and single detached home) and (2) each segment’s forecasted number of customers.

Figure 2 assumes that the REP buys a forward contract at fixed price

$F/MWh for a baseload power block given by Areas A, B, and C. Area C is the contract’s excess MWh sold by the REP in the spot market at

$P/MWh. As

F exceeds

E(

P) = expected value of

P [

22,

23,

24,

25] due to the profitable forward premium required by generators and power marketers/traders, the contract’s purchase causes a per MWh expected loss of [

F −

E(

P)] attributable to the REP’s sale of excess MWh. The same line of reasoning applies to the REP’s purchase of a forward contract for the shoulder power block given by Areas D and E to meet the load obligation given by Area D.

When the REP buys ERCOT’s spot energy to meet the peak load obligation given by Area K, it has residual risk exposure. If the REP decides to reduce its procurement of forward contracts, it becomes increasingly vulnerable to large spot price spikes. When lasting multiple days, as in the case of the Texas deep freeze, such spikes can bankrupt the REP.

5. Indicative Calculation of the Insurance’s per MWh Premium

While the values of

μ and

σ2 may come from ERCOT’s least-cost generation dispatch [

3], they are difficult to forecast for determining a forward-looking value for

S. As an illustrative alternative, we calculate

μ and

σ2 based on the per MWh price adder set by ERCOT’s ORDC [

6].

Our indicative calculation presumes that the ORDC price adder is a reasonable approximation of Y, thus bypassing the need to know the threshold level T stipulated in the insurance contract. However, it does not mean that Y is caused by the ORDC adder. We use the ORDC adder solely for circumventing the data unavailability problem in our calculation of S. If more accurate values of μ and σ2 are available from non-ORDC sources, they should replace those presented below.

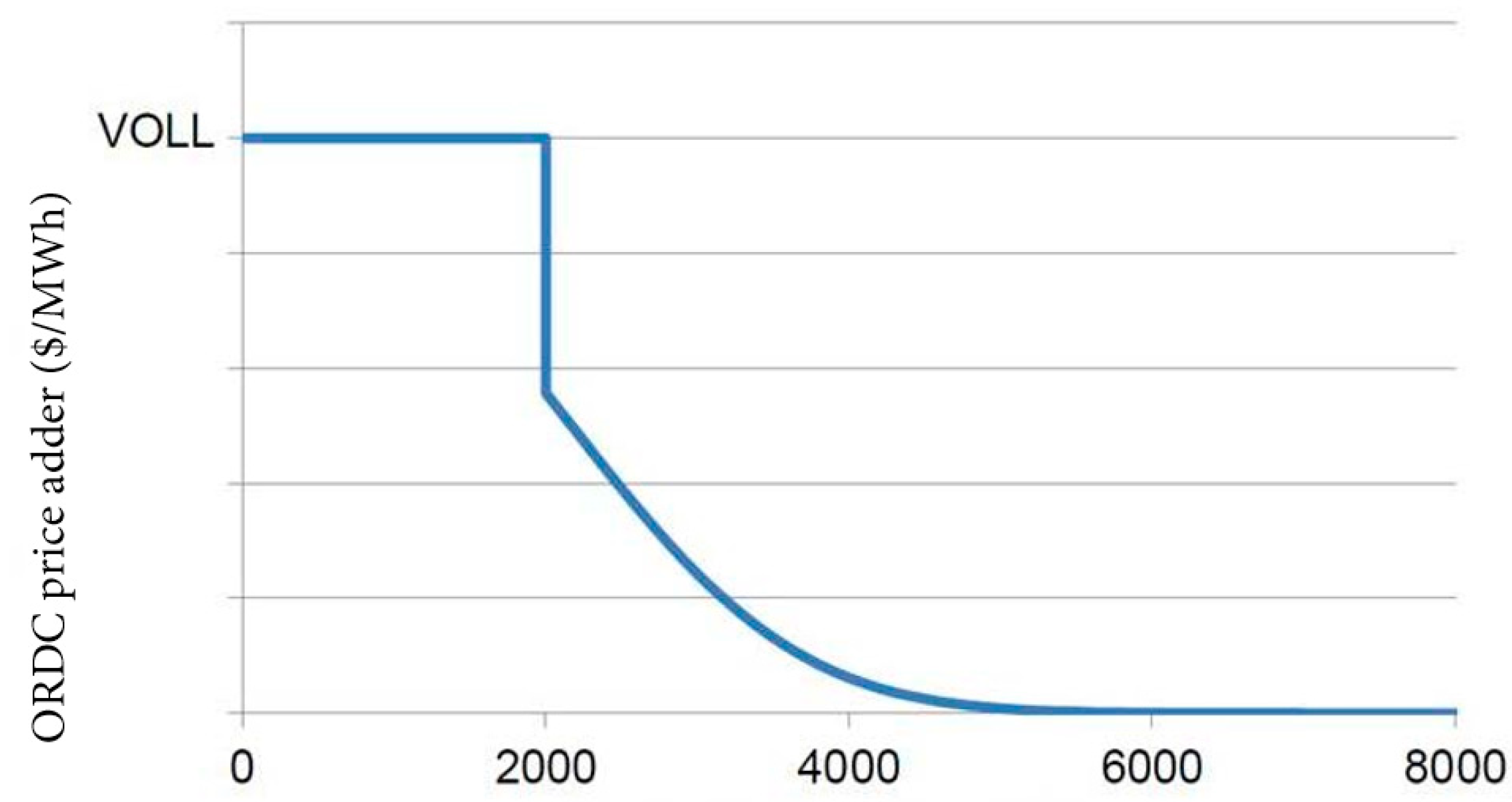

Figure 3 portrays the ORDC adder during ERCOT’s hours of low physical reserve capability [

6]. Hence, these hours correspond to those containing the price spikes on the long right tail of ERCOT’s skewed spot price distribution implied by

Figure 1.

When ERCOT’s physical reserve capability is at or below 2000 MW, the ORDC adder is VOLL = $9000/MWh, which is ERCOT’s value of lost load assumption prior to Winter Storm Uri. Technically, the ORDC adder is always below VOLL. If the system lambda is $X/MWh, the ORDC adder is $(VOLL–X)/MWh to bring the market price up to the systemwide offer cap of VOLL. As will be seen below, this technical adjustment shrinks the size of α used in our calculation of S. In contrast, the ORDC adder is $0/MWh when ERCOT’s physical reserve capability exceeds 5000 MW. As the ORDC adder is used to measure the insurance’s per MWh payoff Y, the insurance’s threshold T is the spot price when ERCOT has over 5000 MW of physical reserve capability.

Replacing the VOLL number with the lower price caps adopted after the deep freeze does not change our calculation process. The price cap was $2000/MWh from March to December 2021 and had been increased to $5000/MWh in January 2022. Importantly, our methodology to estimate μ and σ2 is applicable to any price cap in effect at the time of the per MWh premium’s calculation.

Using

Figure 3, we characterize

Y as follows:

Case 1: Y = 0 if ERCOT’s physical reserve capability is R ≥ RU, where RU = R’s upper threshold at which the ORDC price adder is $0/MWh.

Case 2: Y = α + β R if RU > R > RL, where RL = R’s lower threshold at which the ORDC price adder is strictly positive. The coefficient α > 0 is the VOLL that can be replaced by a lower price cap. The coefficient β = −(α/RU) < 0 is the marginal effect of R on Y.

Case 3: Y = α if RL ≥ R.

Our linear characterization of

Y is necessary to enable our per MWh premium’s calculation based on the information readily available to the REP. Given the convex nature of the ORDC, linearization tends to overstate the ORDC price adder in Case 2. Hence, a nonlinear characterization of the ORDC can improve our premium calculation’s accuracy by reducing the size of the per MWh premium. That said, it is a complication that does not materially enrich the qualitative understanding of our proposed insurance scheme, as further detailed in

Section 6.2 below.

Based on Y’s linear characterization, we can now calculate the conditional expectation and variance of Y for each case:

Case 1: As Y = 0, E(Y|Case 1) = θ1 = 0 and Var(Y|Case 1) = 0.

Case 2: As Y > 0, E(Y|Case 2) = θ2 = α + β μR, where μR = E(R|Case 2). Let σR2 = Var(R|Case 2) for RL < R < RU so that Var(Y|Case 2) = β2 σR2.

Case 3: As Y = α, E(Y|Case 3) = θ3 = α and Var(Y|Case 3) = 0.

The determination of

θ2 and

β2 σR2 requires

μR and

σR2 in Case 2. Hence, we find

μR and

σR2 as follows. Let

R = normally distributed reserve with mean

η and variance

λ2,

ρL = (

RL −

μ)/

μ and

ρU = (

RU −

η)/

λ. As a result,

where

M = [

ϕ(

ρU) −

ϕ(

ρL)]/[

ϕ(

ρU) −

ϕ(

ρL)],

ϕ(

z) = normal density function,

ϕ(

z) = normal probability distribution function, and

z = standard normal variate [

35]. Further,

where

N = [

ρU ϕ(

ρU) −

ρL ϕ(

ρL)]/[

ϕ(

ρU) −

ϕ(

ρL)].

Let

π1 = Prob(

R ≥

RU),

π2 = Prob(

RU >

R >

RL) and

π3 = Prob(

RL ≥

R) = 1 −

π1 −

π2. As indicated in

Section 6, these probabilities can be estimated by an electric grid’s generation reliability criterion and ERCOT’s history of emergency hours.

The unconditional expectation of

Y is:

Finally, the unconditional variance of

Y is:

6. Empirics

6.1. Results

This section reports the empirics from our calculation of

S based on

Figure 3 that shows

α =

$9000/MWh,

RL = 2000 MW,

RU = 5000 MW, and

β = −9000 ÷ 5000 = −1.8. Without invoking Equation (2), we use the midpoint between

RL and

RU as a simple estimate for

μR = 3500 in Case 2, which enables a REP’s quick determination of the value of a competitively priced insurance premium. While this estimate for

μR is less than the appropriately found estimate of 4475 MW based on Equation (2), our sensitivity check indicates that our calculated

S is insensitive to the size of

μR.

Assuming η = 6000 and λ = 1000 based on ERCOT’s 2020 reserve data with mean = 5070 and standard deviation = 1163, we use Equation (3) to find σR = 444.60. This calculation of σR enables an insurer’s determination of the per MWh insurance premium’s probability of profitability.

To complete S’s calculation, we assume π3 = 2.4 h/8760 h = 0.000274 based on the loss-of-load-expectation criterion of 1 day in 10 years, which is commonly used to determine an electric grid’s target of generation reserve margin. We further assume π2 = 12 h/8760 h = 0.00137, which is five times π3 and based on ERCOT’s history of emergency hours of 10 to 20 h per year, excluding Winter Storm Uri’s year of 2021.

We use Equations (4) and (5) to find μ = 6.16 and σ =181.71. Hence, the lower bound for S is SL ≈ $6.16/MWh at z ≈ 0 when there is fierce competition in a REP’s procurement auction. Thanks to Equation (4) that shows μ = π2 (α + β μR) + π3a; a REP can quickly determine SL based on the simple estimate of μR = 0.5 × (RL + RU), the price cap value of a, b = − (a/RU), and the readily available data for π2 and π3. The upper bound for S is SU = $305.98/MWh at z = 1.65, reflecting SU’s profitability for an insurance seller with almost certainty.

Based on Equation (1), an insurance seller’s per MWh profit with a 0.95 probability is SU − SL = $299.82. However, making this large profit with almost certainty is unrealistic because a REP can use SL = $6.16/MWh as the benchmark for selecting the winner of its procurement auction.

Finally, our sensitivity check shows that SL and SU are not materially affected by doubling or halving the values for η and λ. However, reducing α from 9000 to 5000, which is in effect as of 1 January 2022, leads to SL = $3.42/MWh and SU = $170.0/MWh.

6.2. Discussion

Suppose a small REP considers buying insurance based on the insurance’s impact on its fixed price offer. If this impact is deemed excessively large, buying the insurance can harm the REP’s ability to attract customers, despite the insurance’s benefit of pre-empting financial insolvency. This highlights the REP’s trade-off between retail marketing and risk exposure. While offering a low fixed price plan made possible by not buying the insurance can increase customer sign-ups, it enlarges the REP’s risk exposure to spot price spikes that apply to the REP’s residually unhedged load. Underscoring this point are the REP bankruptcies observed in the wake of Texas’s deep freeze in February 2021.

To assess the insurance’s financial impact on the REP’s fixed price offer, we use the average

G value of ~

$60/MWh found by [

21].

Table 1 reports our impact assessment results, which are the percentage changes in

G by per MWh insurance premium and insured amount equal to

γ percent of the REP’s forecast of total fixed price sales.

An example of the REP’s hourly forecast for a given period (e.g., next month or quarter) is (a) the forecasted number of fixed price customers times (b) the estimated hourly kWh sales per customer. Using its marketing and customer data, the REP may find (a) based on n = number of existing customers + number of new customers − number of departed customers. The REP may also find (b) based on the hourly metered kWh sales per customer. The REP’s total forecast can then be found as the sum of hourly forecasts. While there are alternative forecasting approaches (e.g., aggregate time series modeling and disaggregate panel data analysis), their elaboration is beyond our paper’s intent and scope.

Table 1’s calculation details are as follows. We first assume that the insured amount is

γ = 20% of the REP’s total fixed price sales. The price increase based on an insurer’s highly competitive per MWh premium of

SL is ∆

GL = [0.8 × 60 + 0.2 × (60 + 6.16)] − 60 =

$1.23/MWh = 2.05% of the average

G value. The price increase based on an insurer’s highly profitable per MWh premium of

SU is ∆

GU = [0.8 × 60 + 0.2 × (60 + 305.98)] − 60 =

$61.20/MWh = 102.0% of the average

G value. To complete

Table 1, we alternatively assume

γ = 10% (30%). The estimates for ∆

GL and ∆

GU are 1.03% and 51.00% (3.08% and 153.0%) of the average

G value.

The Δ

G estimates shown in

Table 1 suggest that if Area K of the LDC in

Figure 2 is ~30% of the REP’s total fixed price sales, the amount of MWh insured may approach 100% of Area K when the per MWh insurance is highly competitive at

SL.

Informed by the range of ∆

GL and ∆

GU estimates in

Table 1, the REP may consider buying the insurance when its procurement auction’s winning

S quote is close to

SL. However, it should reject

S quotes that resemble

SU. Hence, our ∆

GL and ∆

GU estimates guide the REP’s decision on insurance purchase, notwithstanding that such a decision is ultimately made by the REP’s risk-averse management.

{kind=link}

{kind=link}

{kind=link}