Does Uncertainty Forecast Crude Oil Volatility before and during the COVID-19 Outbreak? Fresh Evidence Using Machine Learning Models

, , and

, , and

Abstract

:1. Introduction

2. Related Literature

3. Data and Methodology

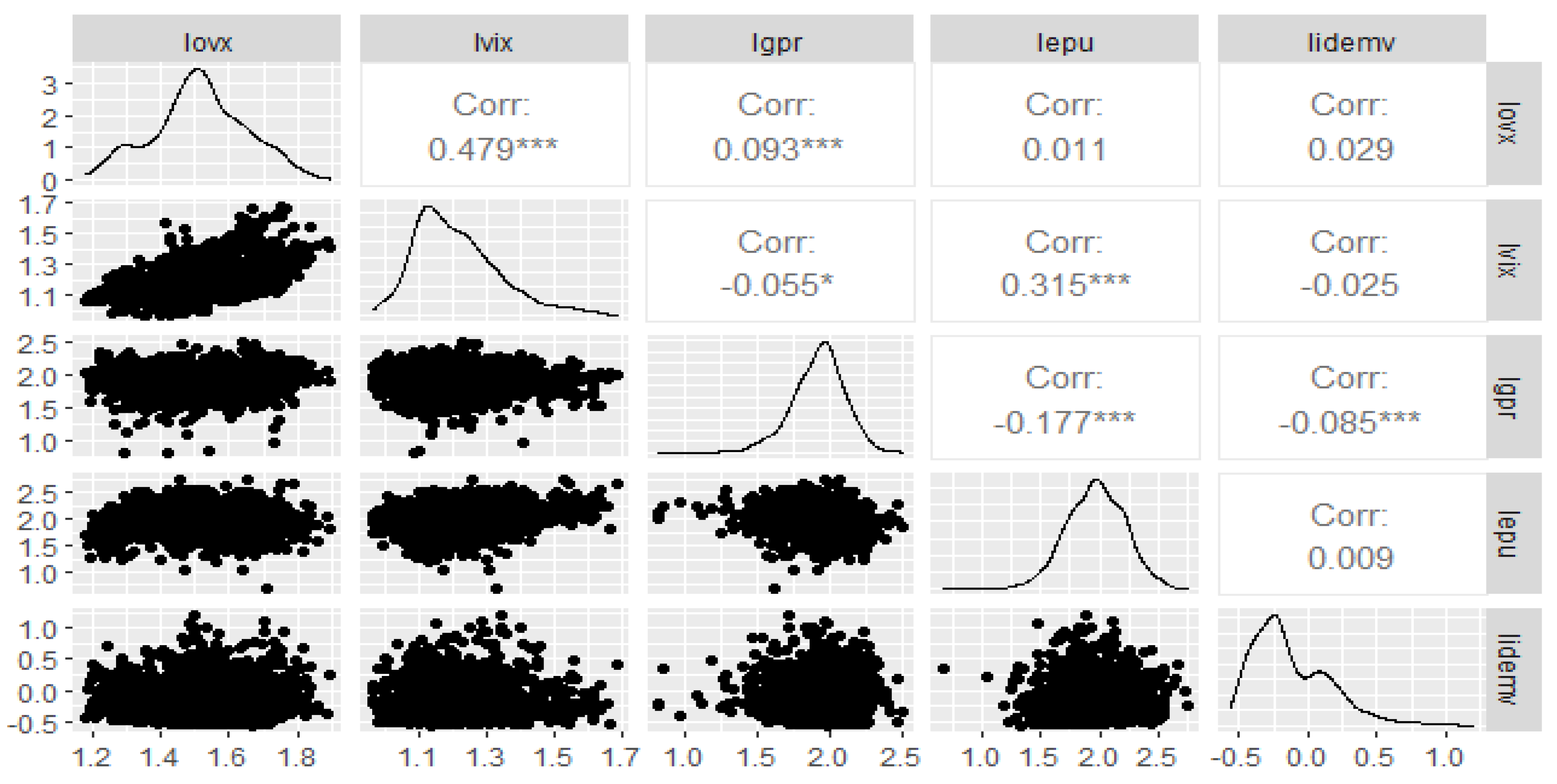

3.1. Data Analysis

3.2. Methodology

3.2.1. Support Vector Machine (SVM)

3.2.2. eXtreme Gradient Boosting (XGBoost)

3.2.3. Autoregressive Integrated Moving Average ARIMAX (p,d,q) Models

3.2.4. The Performance Metrics

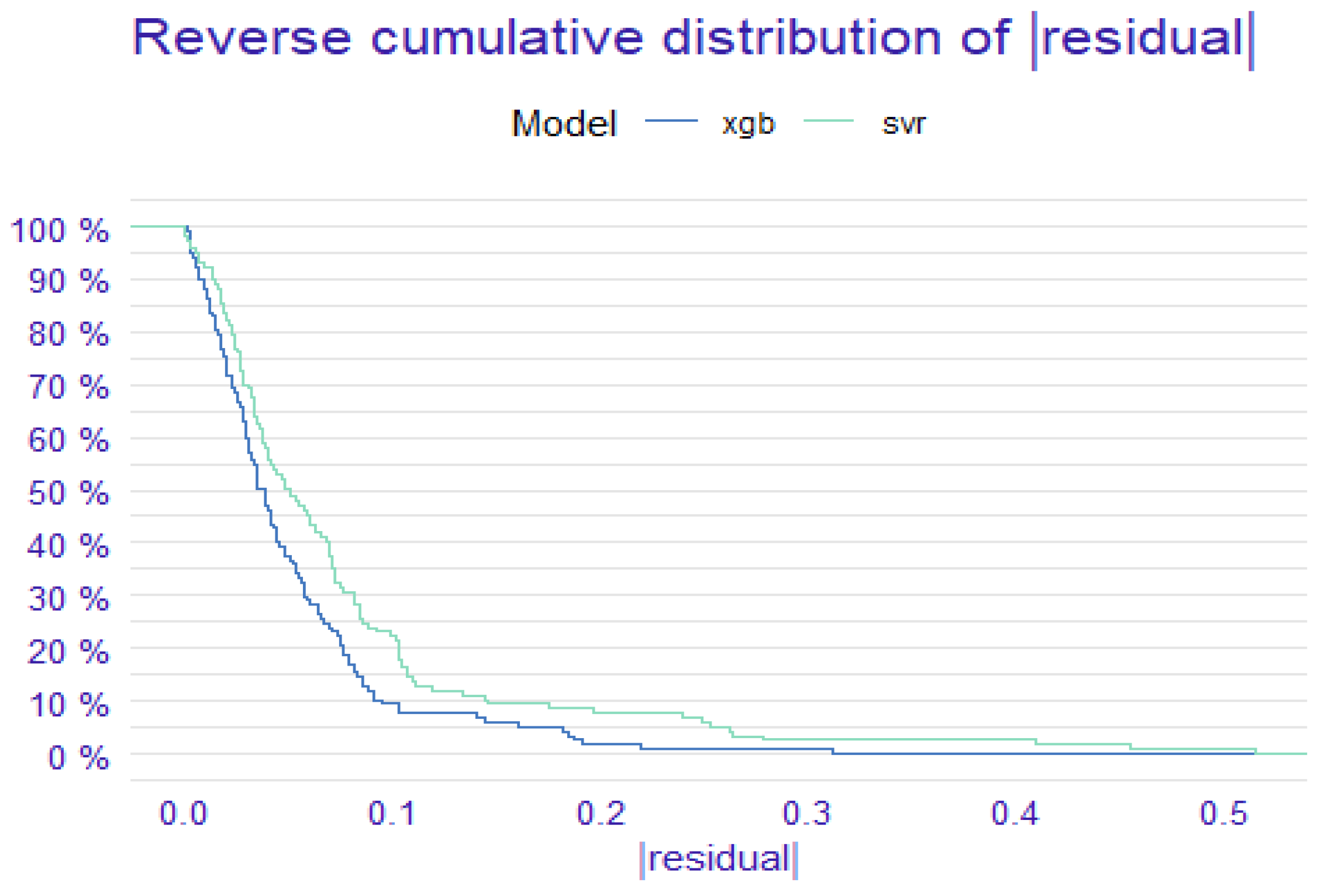

4. Empirical Results

4.1. Forecasting Analysis

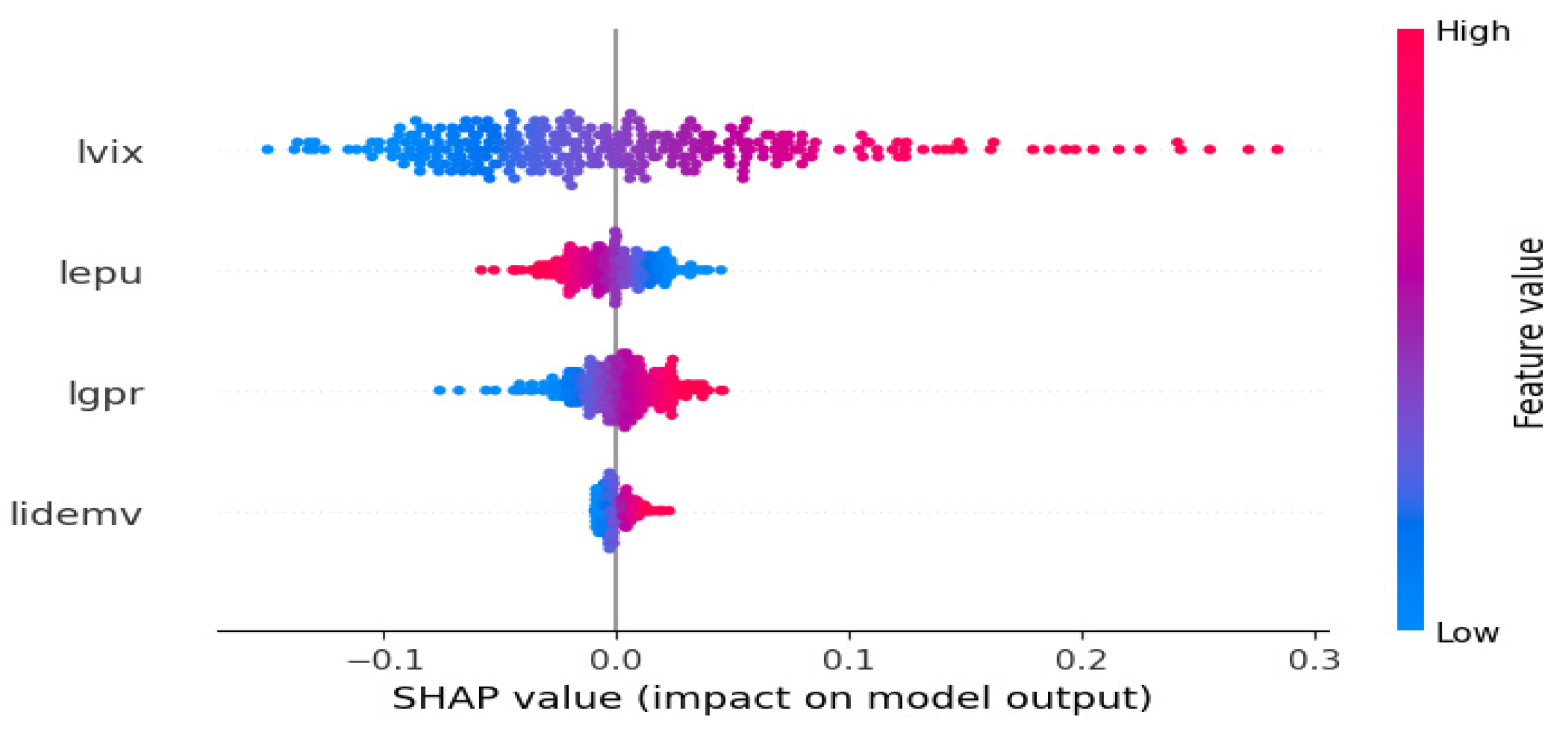

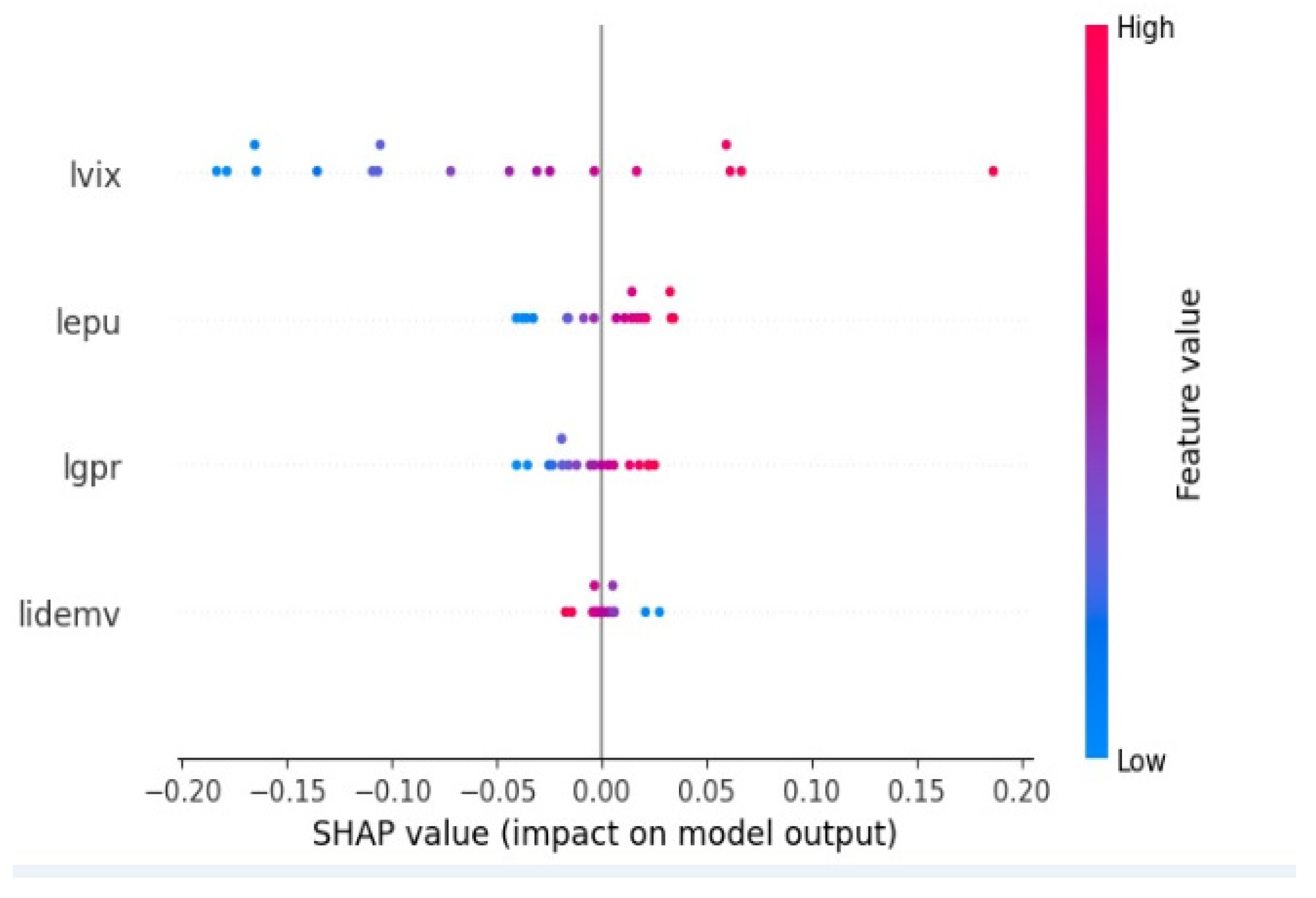

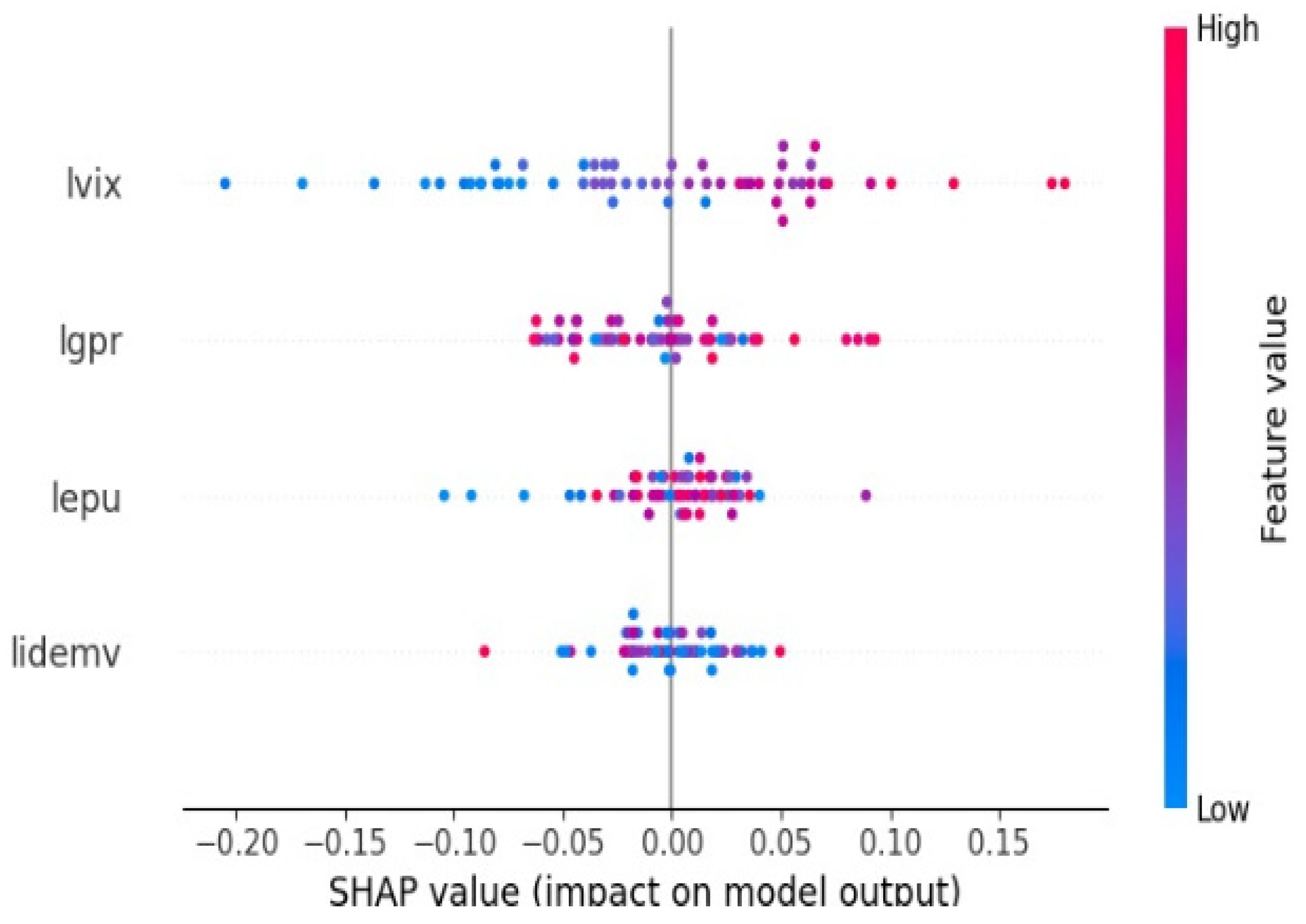

4.2. Feature Importance Analysis

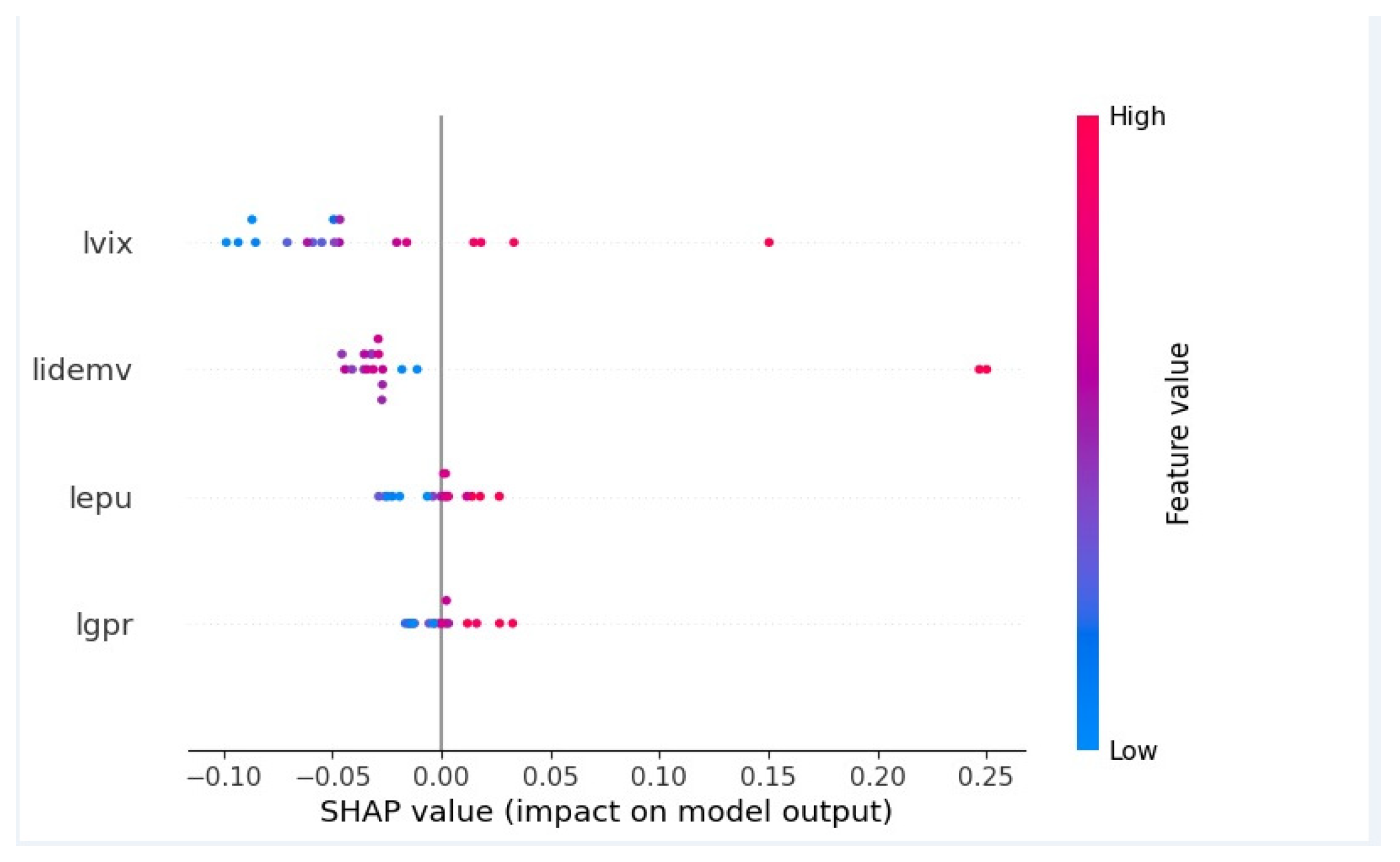

5. Robustness Check

6. Concluding Remarks and Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Le, D.T. Ex-ante determinants of volatility in the crude oil market. Int. J. Financ. Res. 2014, 6, 1–13. [Google Scholar] [CrossRef] [Green Version]

- Narayan, P.K.; Ranjeeni, K.; Bannigidadmath, D. New evidence of psychological barrier from the oil market. J. Behav. Financ. 2017, 18, 457–469. [Google Scholar] [CrossRef]

- Shahzad, S.J.; Naifar, N.H.; Hammoudeh, S.; Roubaud, D. Directional predictability from oil market uncertainty to sovereign credit spreads of oil-exporting countries: Evidence from rolling windows and crossquantilogram analysis. Energy Econ. 2017, 68, 327–339. [Google Scholar] [CrossRef]

- Wheeler, C.M.; Baffes, J.; Kabundi, A.; Kindberg-Hanlon, G.; Nagle, P.S.; Ohnsorge, F. Adding Fuel to the Fire: Cheap Oil during the COVID-19 Pandemic; Policy Research Working Papers 9320; The World Bank: Washington, DC, USA, 2020. [Google Scholar]

- Devpura, N.; Narayan, P.K. Hourly oil price volatility: The role of COVID-19. Energy Res. Lett. 2020, 1, 13683. [Google Scholar] [CrossRef]

- Charles, A.; Darné, O. Forecasting crude-oil market volatility: Further evidence with jumps. Energy Econ. 2017, 67, 508–519. [Google Scholar] [CrossRef]

- Ftiti, Z.; Tissaoui, K.; Boubaker, S. On the relationship between oil and gas markets: A new forecasting framework based on a machine learning approach. Ann. Oper. Res. 2020, 313, 915–943. [Google Scholar] [CrossRef]

- Wu, B.; Wang, L.; Wang, S.; Zeng, Y.-R. Forecasting the U.S. oil markets based on social media information during the COVID-19 pandemic. Energy 2021, 226, 120403. [Google Scholar] [CrossRef]

- Jo, S. The Effects of Oil Price Uncertainty on Global Real Economic Activity. J. Money Credit Bank. 2014, 46, 1113–1135. [Google Scholar] [CrossRef]

- Assaf, A.; Charif, H.; Mokni, K. Dynamic connectedness between uncertainty and energy markets: Do investor sentiments matter? Resour. Policy 2021, 72, 102112. [Google Scholar] [CrossRef]

- Echaust, K.; Just, M. Tail Dependence between Crude Oil Volatility Index and WTI Oil Price Movements during the COVID-19 Pandemic. Energies 2021, 14, 4147. [Google Scholar] [CrossRef]

- Bourghelle, D.; Jawadi, F.; Rozin, P. Oil price volatility in the context of COVID-19. Int. Econ. 2021, 167, 39–49. [Google Scholar] [CrossRef]

- Christopoulos, A.G.; Kalantonis, P.; Katsampoxakis, I.; Vergos, K. COVID-19 and the Energy Price Volatility. Energies 2021, 14, 6496. [Google Scholar] [CrossRef]

- Chen, T.; Guestrin, C. XGBoost: A Scalable Tree Boosting System. In Proceedings of the 22nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, San Francisco, CA, USA, 13–17 August 2016; ACM: New York, NY, USA, 2016; pp. 785–794. [Google Scholar]

- Jabeur, S.B.; Khalfaoui, R.; Arfi, W.B. The effect of green energy, global environmental indexes, and stock markets in predicting oil price crashes: Evidence from explainable machine learning. J. Environ. Manage 2021, 298, 113511. [Google Scholar] [CrossRef] [PubMed]

- Wu, J.; Miu, F.; Li, T. Daily crude oil price forecasting based on improved CEEMDAN, SCA, and RVFL: A case study in WTI oil market. Energies 2020, 13, 1852. [Google Scholar] [CrossRef] [Green Version]

- Hamilton, J.D. Oil and the macroeconomy since World War II. J. Polit. Econ. 1983, 91, 228–248. [Google Scholar] [CrossRef]

- Kilian, L.; Park, C. The impact of oil price shocks on the U.S. stock market. Int. Econ. Rev. 2009, 50, 1267–1287. [Google Scholar] [CrossRef]

- Coleman, L. Explaining crude oil prices using fundamental measures. Energy Policy 2012, 40, 318–324. [Google Scholar] [CrossRef]

- Pan, Z.; Wang, Y.; Wu, C.; Yin, L. Oil price volatility and macroeconomic fundamentals: A regime switching GARCH-MIDAS model. J. Empir. Financ. 2017, 43, 130–142. [Google Scholar] [CrossRef]

- Demirer, R.; Ferrer, R.; Shahzad, S.J.H. Oil price shocks, global financial markets and their connectedness. Energy Econ. 2020, 8, 104771. [Google Scholar] [CrossRef]

- Sadorsky, P. Oil price shocks and stock market activity. Energy Econ. 1999, 21, 449–469. [Google Scholar] [CrossRef]

- Hammoudeh, S.; Huimin, L. Oil sensitivity and systematic risk in oil-sensitive stock indices. J. Econ. Bus. 2005, 57, 1–21. [Google Scholar] [CrossRef]

- Frankel, J.A. Commodity Prices, Monetary Policy, and Currency Regimes. NBER Working Paper No. C0011. 2006. Available online: https://users.nber.org/~confer/2006/apmps06/frankel.pdf (accessed on 20 October 2021).

- Wang, Y.; Wu, C. Energy prices and exchange rates of the US dollar: Further evidence from linear and nonlinear causality analysis. Econ. Model. 2012, 29, 2289–2297. [Google Scholar] [CrossRef]

- Li, R.; Hu, Y.; Heng, J.; Chen, X. A novel multiscale forecasting model for crude oil price time series. Technol. Forecast. Soc. Change 2021, 173, 121181. [Google Scholar] [CrossRef]

- Zhao, L.-T.; Zeng, G.-R.; Wang, W.-J.; Zhang, Z.-G. Forecasting Oil Price Using Web-based Sentiment Analysis. Energies 2019, 12, 4291. [Google Scholar] [CrossRef] [Green Version]

- Orzeszko, W. Nonlinear Causality between Crude Oil Prices and Exchange Rates: Evidence and Forecasting. Energies 2021, 14, 6043. [Google Scholar] [CrossRef]

- Dutta, A.; Bouri, E.; Saeed, T. News-based equity market uncertainty and crude oil volatility. Energy 2021, 222, 119930. [Google Scholar] [CrossRef]

- Baker, S.R.; Bloom, N.; Davis, S.J. Uncertainty and the economy. Policy Rev. 2012, 175, 3. [Google Scholar]

- Bekiros, S.; Gupta, R.; Majumdar, A. Incorporating economic policy uncertainty in US equity premium models: A nonlinear predictability analysis. Financ. Res. Lett. 2016, 18, 291–296. [Google Scholar] [CrossRef] [Green Version]

- Wei, Y.; Liu, J.; Lai, X.; Hu, Y. Which determinant is the most informative in forecasting crude oil market volatility: Fundamental, speculation, or uncertainty? Energy Econ. 2017, 68, 141–150. [Google Scholar] [CrossRef]

- Ma, R.; Zhou, C.; Cai, H.; Deng, C. The forecasting power of EPU for crude oil return volatility. Energy Rep. 2019, 5, 866–873. [Google Scholar] [CrossRef]

- Bakas, D.; Triantafyllou, A. Volatility forecasting in commodity markets using macro uncertainty. Energ. Econ. 2019, 81, 79–94. [Google Scholar] [CrossRef]

- Yang, L. Connectedness of economic policy uncertainty and oil price shocks in a time domain perspective. Energy Econ. 2019, 80, 219–233. [Google Scholar] [CrossRef]

- Qin, Y.; Hong, K.; Chen, J.; Zhang, Z. Asymmetric effects of geopolitical risks on energy returns and volatility under different market conditions. Energy Econ. 2020, 90, 104851. [Google Scholar] [CrossRef]

- Liu, J.; Ma, F.; Tang, Y.; Zhang, Y. Geopolitical risk and oil volatility: A new insight. Energy Econ. 2019, 84, 104548. [Google Scholar] [CrossRef]

- Mei, D.; Ma, F.; Liao, Y.; Wang, L. Geopolitical risk uncertainty and oil future volatility: Evidence from MIDAS models. Energy Econ. 2020, 86, 104624. [Google Scholar] [CrossRef]

- Tiwari, A.K.; Aye, G.C.; Gupta, R.; Gkillas, K. Gold-Oil Dependence Dynamics and the Role of Geopolitical Risks: Evidence from a Markov-Switching Time-Varying Copula Model. Energy Econ. 2020, 88, 104748. [Google Scholar] [CrossRef]

- Nonejad, N. Forecasting crude oil price volatility out-of-sample using news-based geopolitical risk index: What forms of nonlinearity help improve forecast accuracy the most? Financ. Res. Lett. 2021, 46, 102310. [Google Scholar] [CrossRef]

- Lu, X.; Ma, F.; Li, P.; Li, T. Newspaper-based equity uncertainty or implied volatility index: New evidence from oil market volatility predictability. Appl. Econ. Lett. 2022. Available online: https://www.tandfonline.com/doi/abs/10.1080/13504851.2022.2030459. (accessed on 1 June 2022).

- Bouri, E.; Demirer, R.; Gupta, R.; Pierdzioch, C. Infectious diseases, market uncertainty and oil market volatility. Energies 2020, 13, 4090. [Google Scholar] [CrossRef]

- Whaley, R.E. Derivatives on market volatility: Hedging tools long overdue. J. Deriv. 1993, 1, 71–84. [Google Scholar] [CrossRef]

- Tissaoui, K. Forecasting implied volatility risk indexes: International evidence using Hammerstein-ARX approach. Int. Rev. Financ. Anal. 2019, 64, 232–249. [Google Scholar] [CrossRef]

- Hao, X.; Zhao, Y.; Wang, Y. Forecasting the real prices of crude oil using robust regression models with regularisation constraints. Energy Econ. 2020, 86, 104683. [Google Scholar] [CrossRef]

- Vapnik, V.N. The support vector method. In Proceedings of the International Conference on Artificial Neural Networks, Houston, TX, USA, 12 June 1997; Springer: Berlin/Heidelberg, Germany, 1997; pp. 261–271. [Google Scholar]

- Smola, A.J.; Scholkopf, B. A tutorial on support vector regression. Stat. Comput. 2004, 14, 199–222. [Google Scholar] [CrossRef] [Green Version]

- Kuhn, H.W.; Tucker, A.W. Nonlinear Programming. In Proceedings of the 2nd Berkeley Symposium on Mathematical Statistics and Probability, Berkeley, CA, USA, 31 July–12 August 1950; University of California Press: Berkeley, CA, USA, 1951; pp. 481–492. [Google Scholar]

- Ostrowski, K.; Birman, K. Extensible web services architecture for notification in large-scale systems. In Proceedings of the 2006 IEEE International Conference on Web Services (ICWS’06), Chicago, IL, USA, 18–22 September 2006; pp. 383–392. [Google Scholar]

- Singh, N.; Singh, P.; Bhagat, D. A rule extraction approach from support vector machines for diagnosing hypertension among diabetics. Expert Syst. Appl. 2019, 130, 188–205. [Google Scholar] [CrossRef]

- Ma, B.; Meng, F.; Yan, G.; Yan, H.; Chai, B.; Song, F. Diagnostic classification of cancers using extreme gradient boosting algorithm and multiomics data. Comput. Biol. Med. 2020, 121, 103761. [Google Scholar] [CrossRef]

- Lundberg, S.M.; Lee, S.I. A unified approach to interpreting model predictions. In Proceedings of the Advances in Neural Information Processing Systems, Long Beach, CA, USA, 4–9 December 2017; pp. 4765–4774. [Google Scholar]

- Shapley, L.S. A value for n-person games. In Contributions to the Theory of Games; Princeton University Press: Princeton, NJ, USA, 1953; pp. 307–317. [Google Scholar] [CrossRef]

- Tissaoui, K.; Azibi, J. International implied volatility risk indexes and Saudi stock return-volatility predictabilities. N. Am. J. Econ. Financ. 2018, 47, 65–84. [Google Scholar] [CrossRef]

- Biecek, P. DALEX: Explainers for complex predictive models in R. J. Mach. Learn. Res. 2018, 19, 3245–3249. [Google Scholar]

- Tissaoui, K.; Zaghdoudi, T. Dynamic connectedness between the US financial market and Euro-Asian financial markets: Testing transmission of uncertainty through spatial regressions models. Q. Rev. Econ. Financ. 2020, 81, 481–492. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Mean | Median | Max | Min | Std. Dev. | Skewness | Kurtosis | J-B | Obs. | |

|---|---|---|---|---|---|---|---|---|---|

| Panel A. Pre-COVID-19 | |||||||||

| OVX | 33.14 | 31.69 | 78.97 | 14.50 | 10.20 | 0.87 | 3.99 | 614.0960 | 3651 |

| VIX | 16.81 | 15.43 | 48.00 | 9.14 | 5.65 | 1.76 | 6.92 | 4208.202 | 3651 |

| EPU | 109.72 | 94.77 | 586.55 | 3.32 | 63.83 | 1.65 | 7.76 | 5105.250 | 3651 |

| GPR | 93.50 | 88.36 | 361.02 | 6.69 | 39.26 | 1.10 | 5.48 | 1677.320 | 3651 |

| IDEMV | 0.43 | 0.00 | 15.91 | 0.00 | 0.90 | 6.17 | 65.71 | 621,436.5 | 3651 |

| Panel B. COVID-19 | |||||||||

| OVX | 53.38 | 40.15 | 325.15 | 27.66 | 35.86 | 3.07 | 14.06 | 4065.344 | 610 |

| VIX | 25.22 | 22.72 | 82.69 | 12.10 | 10.68 | 2.15 | 9.12 | 1424.659 | 610 |

| EPU | 240.53 | 195.95 | 861.10 | 20.63 | 152.31 | 1.19 | 4.13 | 176.4942 | 610 |

| GPR | 79.54 | 72.75 | 420.29 | 3.73 | 42.54 | 2.18 | 15.01 | 4148.166 | 610 |

| IDEMV | 19.61 | 16.43 | 112.93 | 0.00 | 14.87 | 1.83 | 8.53 | 1115.84 | 610 |

| Pre-COVID-19 | COVID-19 | |||||

|---|---|---|---|---|---|---|

| Models | RMSE | MSE | RMSE | MSE | ||

| XGBoost | 0.120 | 0.014 | 0.210 | 0.070 | 0.005 | 0.840 |

| SVM | 0.112 | 0.013 | 0.260 | 0.100 | 0.012 | 0.710 |

| ARIMAX | 0.149 | 0.022 | 0.320 | 0.151 | 0.023 | 0.319 |

| Pre-COVID-19 | COVID-19 | |||||

|---|---|---|---|---|---|---|

| Models | RMSE | MSE | RMSE | MSE | ||

| XGBoost | 0.148 | 0.021 | 0.391 | 0.110 | 0.012 | 0.717 |

| SVM | 0.128 | 0.016 | 0.041 | 0.153 | 0.023 | 0.451 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tissaoui, K.; Zaghdoudi, T.; Hakimi, A.; Ben-Salha, O.; Ben Amor, L. Does Uncertainty Forecast Crude Oil Volatility before and during the COVID-19 Outbreak? Fresh Evidence Using Machine Learning Models. Energies 2022, 15, 5744. https://doi.org/10.3390/en15155744

Tissaoui K, Zaghdoudi T, Hakimi A, Ben-Salha O, Ben Amor L. Does Uncertainty Forecast Crude Oil Volatility before and during the COVID-19 Outbreak? Fresh Evidence Using Machine Learning Models. Energies. 2022; 15(15):5744. https://doi.org/10.3390/en15155744

Chicago/Turabian StyleTissaoui, Kais, Taha Zaghdoudi, Abdelaziz Hakimi, Ousama Ben-Salha, and Lamia Ben Amor. 2022. "Does Uncertainty Forecast Crude Oil Volatility before and during the COVID-19 Outbreak? Fresh Evidence Using Machine Learning Models" Energies 15, no. 15: 5744. https://doi.org/10.3390/en15155744