The Benefits of Local Cross-Sector Consumer Ownership Models for the Transition to a Renewable Smart Energy System in Denmark. An Exploratory Study

Abstract

:1. Introduction

- What is the (theoretical) ability of cross-sector consumer ownership at different locations to address the organisational challenges of SESs in Denmark?

- How does the current Danish institutional incentive system encourage/discourage cross-sector consumer ownership at different locations in the power distribution system?

- Based on 1 and 2, how could the Danish institutional incentive system be improved to better address the organisational challenges of SESs?

- What issues regarding ownership and SESs can be identified for further research?

2. Theoretical Approach and Methods

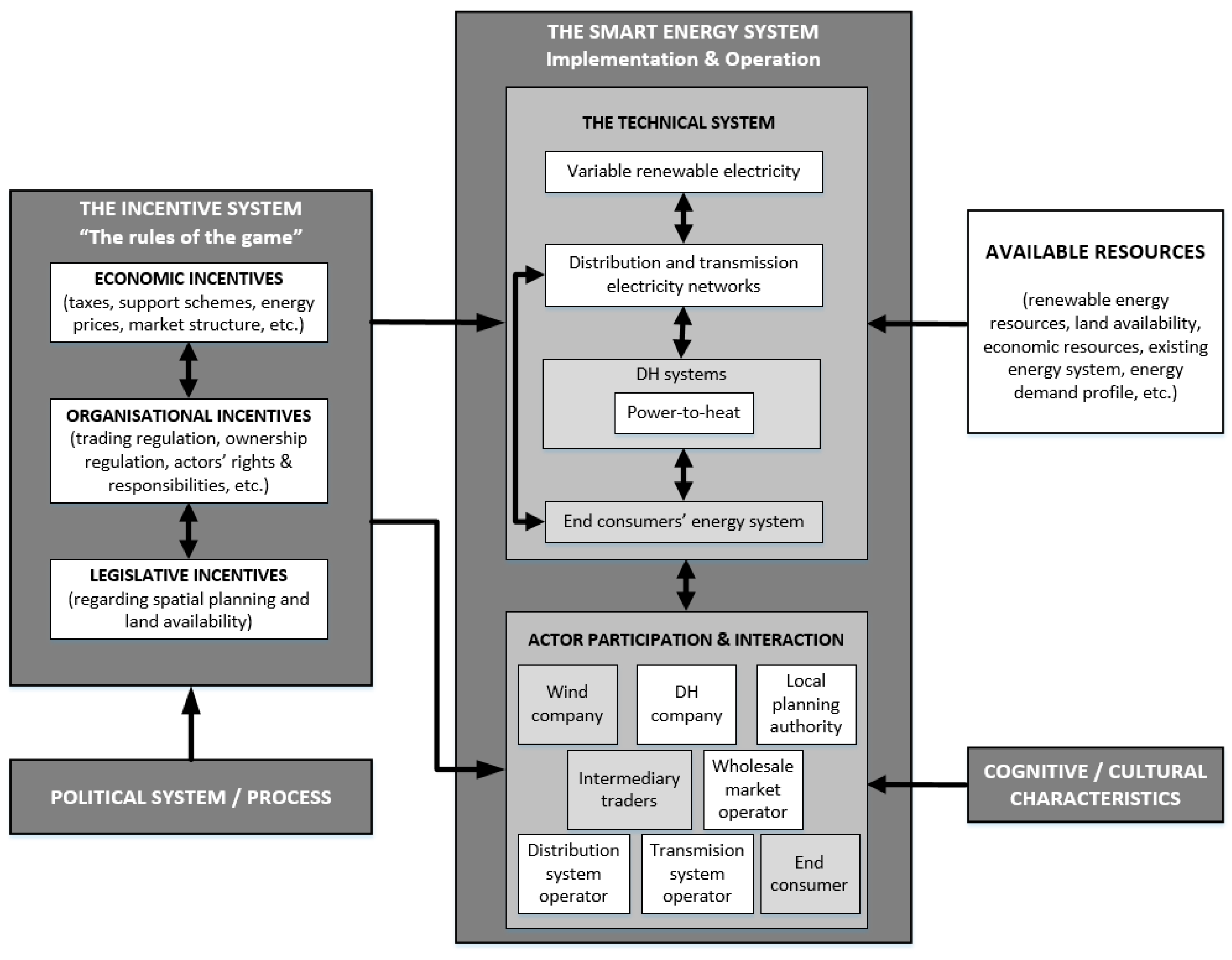

2.1. SESs and their Interrelations

2.2. The Organisational Challenges of SESs, Ownership and Location

2.2.1. Reduction of Overinvestments in the Electricity Grid

2.2.2. Local Opposition to Wind Turbines

2.2.3. Attractiveness of Investments in VRE and P2H in DH Systems

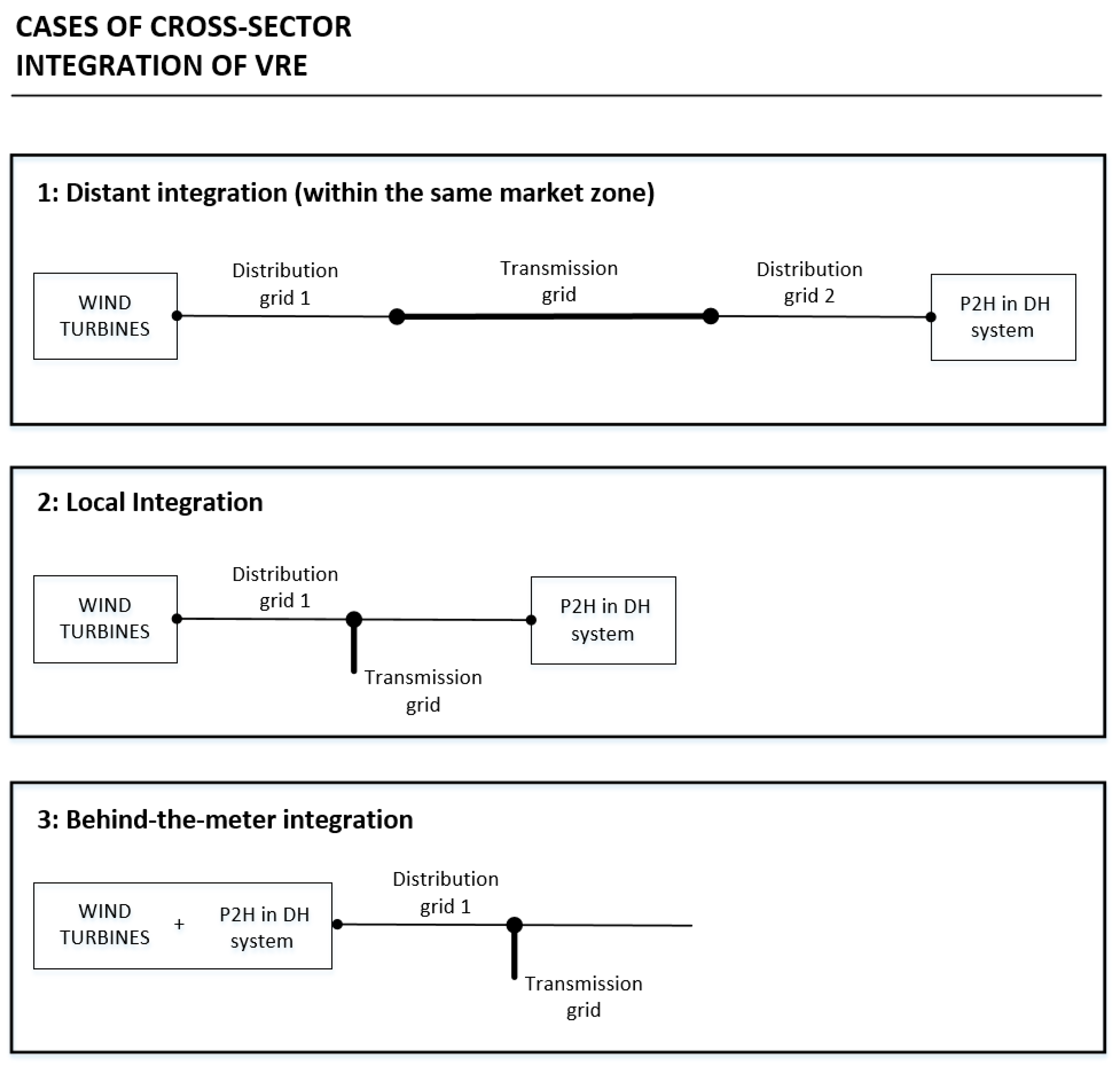

2.2.4. SESs, Cross-sector Ownership and Different Location Cases

2.3. Methodology

3. Results

3.1. The (Theoretical) Ability of the Consumer Cross-sector Ownership Model in Different Location Cases to Address the Organisational Challenges of SESs

3.1.1. The Operation of the Wind Turbines and the DH System in a Co-Ownership Solution

3.1.2. The Location Cases for Cross-Sector Integration and the Reduction of Overinvestments in the Electricity Grid

- (A)

- An increase amount of hours with transmission grid congestions in DK1 and DK2. DK1 and DK2 are the two electricity market zones in Denmark. This problem occurs in moments when the electricity production in DK1 and/or DK2 exceeds the electricity demand in DK1 and/or DK2 and the transmission connections to other market zones are fully utilised. The result is the curtailment of VRE by the power market [7].

- (B)

- The creation of new congestion nodes inside DK1 and DK2. This may occur, e.g., because of congestions in the substations that connect DS1 and DS3 with the transmission voltage cables. Such an issue has already occurred for example in one of the transmission substations in Lolland municipality, where Energinet had to contact the local DSO to achieve down regulation of wind and solar power production. Currently this is only an issue for the transmission system operator (TSO), but it is expected to become a problem for the DSOs as well [46].

- (C)

- Additional electricity grid losses at the distribution level in areas with excess VRE. Grid losses are proportional to the current (i.e., the power flow) and the distance that power is transported. In a centralised fossil fuel energy system (where the electricity is transported from the central power stations to the consumer through the transmission and distribution grids), the power consumption in a given distribution grid can be seen as the cause of the power flow in that given distribution grid and, consequently, of the grid losses in the given distribution grid too. However, in a renewable energy system (where large shares of the power production may be fed directly into the distribution grid and go upstream or downstream) the power flow in a given distribution grid could be caused by power consumption elsewhere in the system. This is the case when the local VRE production exceeds the local power consumption. In this sense, one could say that local excess power production from VRE creates additional grid losses in the local distribution grids where the excess power is produced.

3.1.3. Consumer Ownership and Local Acceptance of Wind Turbines

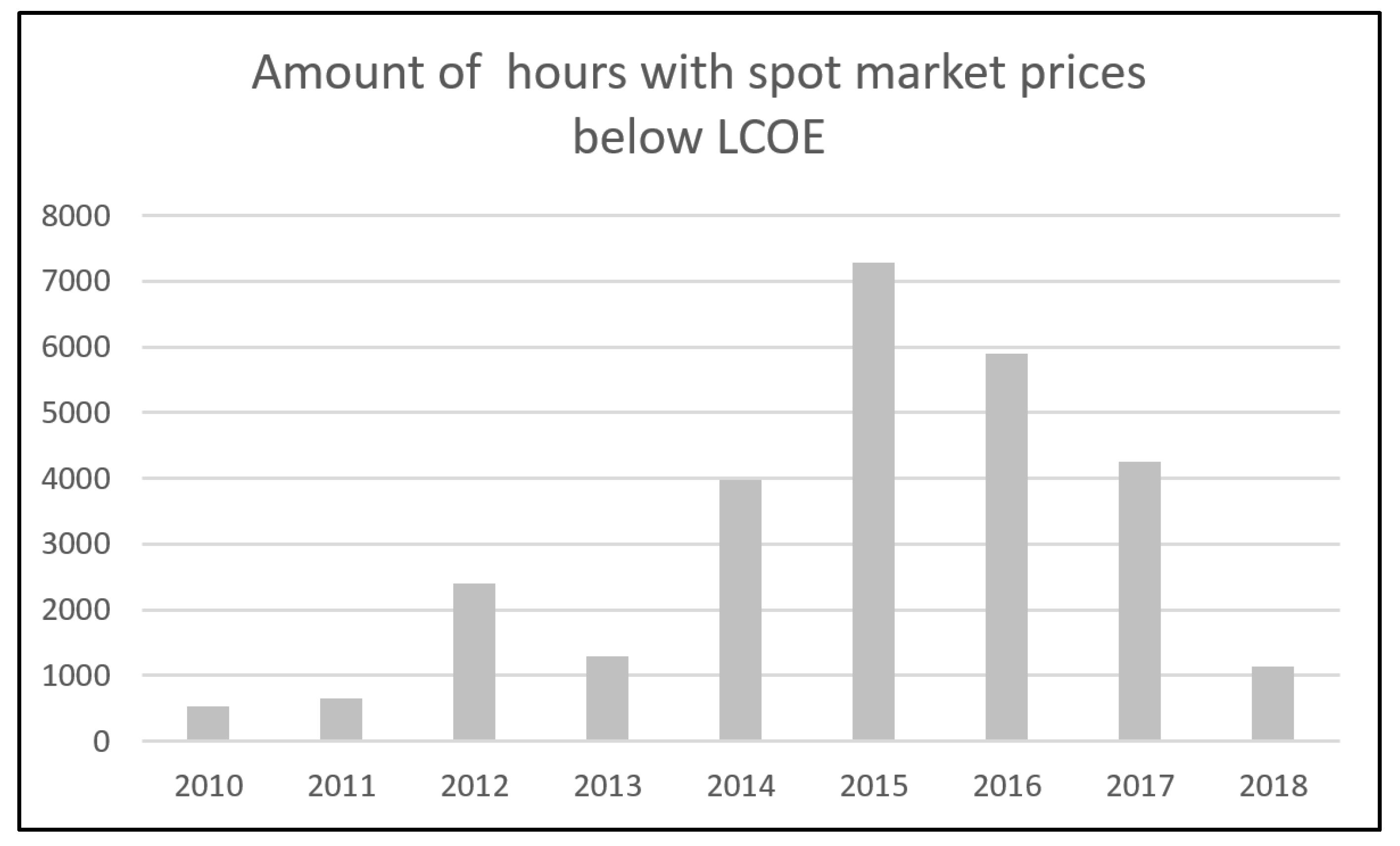

3.1.4. The Attractiveness of VRE and P2H for DH Companies

- Coupling the wind turbines with the flexible demand of the DH system would to some extent resolve the merit-order-effect and the curtailment problems when the wind turbines and the flexible electricity demand are placed in the same congestion node [21].

- Onshore wind turbines are the cheapest source of electricity in Denmark [49]. Therefore, it would be cheaper for a flexible consumer to self-consume electricity from his wind turbines than buy electricity from a wind power producer (either via the spot market or through peer-to-peer trading). This is because, when buying electricity from a producer, the consumer would have to pay for the cost of producing the wind power and for some benefits for the wind power producer. DH companies who owned wind turbines in windy areas would have an additional advantage because the levelised cost of wind power in these areas is even lower.

- The DH system could be entitled to a reduction of electricity grid tariffs for the self-consumed electricity based on the advantages it provides for the reduction of overinvestments in the electricity grid expansion and reinforcement (see Section 3.1.2). In this sense, the co-ownership in the behind-the-meter and local cross-sector integration cases would have an economic advantage over the co-ownership in the distant cross-sector integration case.

3.1.5. Summary

3.2. The Current Institutional Incentive System for Cross-Sector Consumer Ownership in Denmark

3.2.1. The Role and Possibilities of Electricity Grid Operators

3.2.2. Electricity Grid Tariffs, and Taxes

3.2.3. The Design of the Electricity Spot Market

3.2.4. Lack of Specific Incentives for Local Cross-Sector Integration

3.2.5. Summary

3.3. Possibilities for Improving the Current Institutional Incentives

- New (TSO and DSO) grid tariffs to activate flexible demand in a given location in periods of excess electricity generation, as suggested by Ringkøbing DH [30]. “I can prove to them [to the local DSO] mathematically that they would sell more electricity to me [and] make more money and [that] I would make more DH to a lower price on the electrical boiler, if they lowered their price [the electricity distribution tariff]” said Ringkøbing DH [30]. The reconsideration of the waterfall principle for the distribution of grid costs would also be pertinent here.

- Subsidies on investments in VRE and/or P2H in targeted areas. The subsidies could be paid by the savings that would be obtained from not having to reinforce or expand the electricity grid. This could be facilitated by modifying the current legislation so that grid operators could promote the implementation of cross-sector integration technology (on the right time, size and location), when this wasestimated to be a more cost-effective solution from a socio-economic perspective.

3.4. Future Perspectives for Research on Ownership and SESs

4. Discussion

Funding

Acknowledgments

Conflicts of Interest

Abbreviations

| CHP | Combined heat and power |

| DH | District heating |

| H&C | Heating and cooling |

| HP | Heat pump |

| DSO | Distribution system operator |

| LCOE | Levelised cost of energy |

| PPA | Power-purchase-agreement |

| P2H | Power-to-heat |

| SES | Smart energy system |

| TSO | Transmission system operator |

| VRE | Variable renewable energy |

References

- IPCC. Global Warming of 1.5 °C. Summary for Policymakers; IPCC: Geneva, Switzerland, 2018. [Google Scholar]

- European Commission. Roadmap 2050; European Commission: Brussels, Belgium, 2012. [Google Scholar]

- Hvelplund, F.; Djørup, S. Consumer ownership, natural monopolies and transition to 100% Renewable Energy Systems. Energy 2019, 181, 440–449. [Google Scholar] [CrossRef]

- Innovation and Disruption at the Grid’s Edge: How Distributed Energy Resources are Disrupting the Utility Business Model, 1st ed.; Sioshansi, F.P. (Ed.) Academic Press: London, UK, 2017; ISBN 978-0-12-811758-3. [Google Scholar]

- Burger, S.P.; Luke, M. Business models for distributed energy resources: A review and empirical analysis. Energy Policy 2017, 109, 230–248. [Google Scholar] [CrossRef]

- Ladenburg, J. Acceptance of Wind Power: An Introduction to Drivers and Solutions. In Alternative Energy and Shale Gas Encyclopedia; Lehr, J.H., Keeley, J., Eds.; John Wiley and Sons Inc.: Hoboken, NJ, USA, 2016; pp. 3–9. [Google Scholar]

- Bird, L.; Lew, D.; Milligan, M.; Carlini, E.M.; Estanqueiro, A.; Flynn, D.; Gomez-lazaro, E.; Holttinen, H.; Menemenlis, N.; Orths, A.; et al. Wind and solar energy curtailment: A review of international experience. Renew. Sustain. Energy Rev. 2016, 65, 577–586. [Google Scholar] [CrossRef] [Green Version]

- Brown, T.; Schlachtberger, D.; Kies, A.; Schramm, S.; Greiner, M. Synergies of sector coupling and transmission reinforcement in a cost- optimised, highly renewable European energy system. Energy 2018, 160, 720–739. [Google Scholar] [CrossRef] [Green Version]

- Hvelplund, F.; Möller, B.; Sperling, K. Local ownership, smart energy systems and better wind power economy. Energy Strateg. Rev. 2013, 1, 164–170. [Google Scholar] [CrossRef]

- Berka, A.L.; Creamer, E. Taking stock of the local impacts of community owned renewable energy: A review and research agenda. Renew. Sustain. Energy Rev. 2018, 82, 3400–3419. [Google Scholar] [CrossRef] [Green Version]

- Gorroño-Albizu, L.; Sperling, K.; Djørup, S. The past, present and uncertain future of community energy in Denmark: Critically reviewing and conceptualising citizen ownership. Energy Res. Soc. Sci. 2019, 57, 101231. [Google Scholar] [CrossRef]

- Hvelplund, F.; Østergaard, P.A.; Meyer, N.I. Incentives and barriers for wind power expansion and system integration in Denmark. Energy Policy 2017, 107, 573–584. [Google Scholar] [CrossRef]

- Plechinger, M. Dansk Vind Slog Rekord i 2019. Available online: https://energiwatch.dk/Energinyt/Renewables/article11852237.ece (accessed on 11 February 2020).

- Danish Energy Agency. Energistatistiks 2018; Danish Energy Agency: Copenhagen, Denmark, 2019. [Google Scholar]

- Rønne, A.; Nielsen, F.G. Consumer (Co-)Ownership in Renewables in Denmark. In Energy Transition. Financing Consumer Co-ownership in Renewables; Lowitzsch, J., Ed.; Springer Nature Switzerland AG: Cham, Switzerland, 2019; pp. 223–244. [Google Scholar]

- Lund, H.; Østergaard, P.A.; Connolly, D.; Mathiesen, B.V. Smart energy and smart energy systems. Energy 2017, 137, 556–565. [Google Scholar] [CrossRef]

- Djørup, S.; Thellufsen, J.Z.; Sorknæs, P. The electricity market in a renewable energy system. Energy 2018, 162, 148–157. [Google Scholar] [CrossRef]

- Jensen, L.K.; Sperling, K.; Lund, H. Barriers and Recommendations to Innovative Ownership Models for Wind Power. Energies 2018, 11, 2602. [Google Scholar]

- Grashof, K. Are auctions likely to deter community wind projects? And would this be problematic? Energy Policy 2019, 125, 20–32. [Google Scholar] [CrossRef]

- Aagaard, L. Kunne du Overveje en Vindmølle i Baghaven? Available online: https://www.danskenergi.dk/nyheder/kunne-du-overveje-vindmolle-baghaven (accessed on 11 January 2020).

- Gill, S.; Plecas, M.; Kockar, I. Coupling Demand and Distributed Generation to Accelerate Renewable Connections; University of Strathclyde: Glasgow, UK, 2014. [Google Scholar]

- Blanco, I.; Guericke, D.; Andersen, A.N.; Madsen, H. Operational planning and bidding for district heating systems with uncertain renewable energy production. Energies 2018, 11, 3310. [Google Scholar] [CrossRef] [Green Version]

- Larsen, S.V.; Nielsen, H.; Hansen, A.M.; Lyhne, I.; Clausen, N.-E.; Rudolph, D.; Gorroño-Albizu, L.; Forfang, A.S. Integrating social consequences in EIA of renewable energy projects: 11 recommendations; Aalborg University: Aalborg, Denmark, 2017. [Google Scholar]

- IRENA. Renewable Power Generation Costs in 2018; IRENA: Abu Dhabi, United Arab Emirates, 2019. [Google Scholar]

- Berka, A.L.; Harnmeijer, J.; Roberts, D.; Phimister, E.; Msika, J. A comparative analysis of the costs of onshore wind energy: Is there a case for community-specific policy support? Energy Policy 2017, 106, 394–403. [Google Scholar] [CrossRef]

- Yildiz, Ö. Financing renewable energy infrastructures via financial citizen participation - The case of Germany. Renew. Energy 2014, 68, 677–685. [Google Scholar] [CrossRef]

- Chittum, A.; Østergaard, P.A. How Danish communal heat planning empowers municipalities and benefits individual consumers. Energy Policy 2014, 74, 465–474. [Google Scholar] [CrossRef]

- Grøn Energi. Investeringshorisontens indflydelse på fjernvarmesektoren; Grøn Energi: Kolding, Denmark, 2017. [Google Scholar]

- Hvide Sande DH. Personal Communication, 2019.

- Ringkøbing DH. Personal Communication, 2019.

- Ringkøbing-Skjern Municipality. Personal Communication, 2019.

- RAH Net. Personal Communication, 2019.

- Energinet. Personal Communication, 2019.

- EMD International A/S. Personal Communication, 2019.

- Geels, F.W.; Hekkert, M.P.; Jacobsson, S. The dynamics of sustainable innovation journeys. Technol. Anal. Strateg. Manag. 2008, 20, 521–536. [Google Scholar] [CrossRef] [Green Version]

- Seyfang, G.; Smith, A. Grassroots innovations for sustainable development: Towards a new research and policy agenda. Env. Polit. 2007, 16, 584–603. [Google Scholar] [CrossRef]

- Schot, J.; Geels, F.W. Strategic niche management and sustainable innovation journeys: Theory, findings, research agenda, and policy. Technol. Anal. Strateg. Manag. 2008, 20, 537–554. [Google Scholar] [CrossRef]

- Energinet. Energy System Perspective 2035; Energinet: Fredericia, Denmark, 2018. [Google Scholar]

- Energinet Transmission System Data. Available online: https://en.energinet.dk/Electricity/Energy-data/System-data (accessed on 2 January 2020).

- Evonet Net Kort. Available online: https://sekort.dk/Html5/Index.html?viewer=SE_NetWeb.SE (accessed on 11 January 2020).

- State of Green The Future Role of DSOs: Europe’s Energy System is Turned Upside-Down. Available online: https://stateofgreen.com/en/partners/state-of-green/news/the-future-role-of-dsos-europes-energy-system-is-turned-upside-down/,2017/ (accessed on 11 January 2020).

- European Commission Expert Group on electricity interconnection targets. Towards a Sustainable and Integrated Europe; European Commission: Brussels, Belgium, 2017. [Google Scholar]

- Vittrup, C. Denmark as a Bottom-Up Case. Pitch at the Session: “Decarbonisation of the European Energy System”. Available online: https://my.eventbuizz.com/assets/editorImages/1570519706-Workshop1_1150-1300_-_Carsten_Vittrup.pdf (accessed on 2 January 2020).

- NOE Net Historie om NOE. Available online: https://www.noe.dk/noe_s_historie (accessed on 2 January 2020).

- Tornbjerg, J. Vestjyske Elkunder Betaler Overpris for Grøn Omstilling. Available online: https://www.danskenergi.dk/nyheder/vestjyske-elkunder-betaler-overpris-gron-omstilling (accessed on 2 January 2020).

- Energinet. Ny Viden til Sikker Forsyning. F&I Årsrapport 2018; Energinet: Fredericia, Denmark, 2019. [Google Scholar]

- Mathiesen, B.V.; Lund, H.; Hansen, K.; Skov, I.R.; Djørup, S.R.; Nielsen, S.; Sorknæs, P.; Thellufsen, J.Z.; Grundahl, L.; Lund, R.S.; et al. IDA’s Energy Vision 2050: A Smart Energy System Strategy for 100% Renewable Denmark; Aalborg University: Aalborg, Denmark, 2015. [Google Scholar]

- Danish District Heating Association. Nyheder. Nærdemokrati Hvide Sande køber vindmøller. Available online: https://www.danskfjernvarme.dk/nyheder/presseklip/arkiv/2016/160812naerdemokrati-hvide-sande-koeber-vindmoeller (accessed on 20 March 2020).

- Energinet. Systemperspektiv 2035. Baggrundsrapport; Energinet: Fredericia, Denmark, 2018. [Google Scholar]

- Energinet International Infrastructure Projects. Available online: https://en.energinet.dk/Infrastructure-Projects/Projektliste (accessed on 31 January 2020).

- Energinet. Personal Communication, 2020.

- RAH Net Gældende nettariffer og abonnementer. Available online: https://rahnet.dk/priser/nettariffer-og-abonnement/ (accessed on 11 February 2020).

- Energinet TARIFFER OG GEBYRER. Available online: https://energinet.dk/El/Elmarkedet/Tariffer (accessed on 11 February 2020).

- Djørup, S. Competing Market Regimes: When and where are supply and demand able to shake hands? An exploration of demand side policies in the Danish energy transition. In Proceedings of the SWEDES Conference, Palermo, Italy, September 30–Octomber 4 2018. [Google Scholar]

- Smartvarme.dk Homepage. Available online: http://smartvarme.dk/ (accessed on 11 January 2020).

- Danish Government. Energiaftale af 29. June 2018; Danish Government: Copenhagen, Denmark, 2018. [Google Scholar]

- Danish Energy Agency Varmepumper—En God Forretning. Available online: https://presse.ens.dk/news/varmepumper-en-god-forretning-268036 (accessed on 17 January 2020).

- Danish Energy Agency 15 Værker Får Støtte til Store Varmepumper. Available online: https://presse.ens.dk/pressreleases/15-vaerker-faar-stoette-til-store-varmepumper-2562721 (accessed on 17 January 2020).

- Danish Energy Agency Grundbeløbets Ophør og Grundbeløbsindsatsen. Available online: https://ens.dk/ansvarsomraader/varme/grundbeloebets-ophoer-og-grundbeloebsindsatsen# (accessed on 17 January 2020).

- SKAT Bindende Svar. Available online: https://www.rksk.dk/Edoc/Dagsordenspublicering/Økonomi-ogErhvervsudvalget/2016-08-0909.00/Dagsorden/Referat/Hjemmeside/2016-08-0913.10.32/Attachments/1147601-1452497-1.pdf (accessed on 11 January 2020).

- Energinet Markesdata. Available online: http://osp.energinet.dk/_layouts/Markedsdata/framework/integrations/markedsdatatemplate.aspx (accessed on 11 January 2020).

- Mey, F.; Diesendorf, M. Who owns an energy transition? Strategic action fields and community wind energy in Denmark. Energy Res. Soc. Sci. 2018, 35, 108–117. [Google Scholar] [CrossRef]

- Danish Government. Stemmeaftale Mellem Regeringen (Venstre, Liberal Alliance, Det Konservative Folkeparti) og Dansk Folkeparti om ny Støttemodel for Vind og sol i 2018–2019; Danish Government: Copenhagen, Denmark, 2017. [Google Scholar]

- Connolly, D.; Lund, H.; Mathiesen, B.V.; Werner, S.; Möller, B.; Persson, U.; Boermans, T.; Trier, D.; Østergaard, P.A.; Nielsen, S. Heat Roadmap Europe: Combining district heating with heat savings to decarbonise the EU energy system. Energy Policy 2014, 65, 475–489. [Google Scholar] [CrossRef]

- Energy Transition. Financing Consumer Co-ownership in Renewables, 1st ed.; Lowitzsch, J., Ed.; Palgrave Macmillan: Cham, Switzerland, 2019; ISBN 978-3-319-93517-1. [Google Scholar]

- Zeman, J.; Werner, S. District Heating System Ownership Guide; IEE DHCAN project: Watford, UK, 2004. [Google Scholar]

- Werner, S. International review of district heating and cooling. Energy 2017, 137, 617–631. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Stakeholder | Interviewee | Description |

|---|---|---|

| DH Company | Hvide Sande DH [29] | Hvide Sande DH owns wind turbines and an electric boiler in a behind-the-meter solution. |

| DH Company | Ringkøbing DH [30] | Ringkøbing DH owns an electric boiler and a HP. |

| Local Planning Authority | Ringkøbing-Skjern Municipality [31] | Hvide Sande DH and Ringkøbing DH are located in this municipality. Ringkøbing-Skjern is a rural municipality with high shares of VRE and ambitious municipal energy targets. |

| DSO | RAH Net [32] | RAH Net is the local consumer-owned DSO. Hvide Sande DH and Ringkøbing DH are connected to RAH Net’s electricity grid. |

| TSO and Market Operator | Energinet [33] | Energinet is the Danish TSO and market operator. |

| DH Consultant | EMD International [34] | EMD International is an energy systems software company that provides consultancy to DH companies for the improvement of their operations’ strategy. |

© 2020 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gorroño-Albizu, L. The Benefits of Local Cross-Sector Consumer Ownership Models for the Transition to a Renewable Smart Energy System in Denmark. An Exploratory Study. Energies 2020, 13, 1508. https://doi.org/10.3390/en13061508

Gorroño-Albizu L. The Benefits of Local Cross-Sector Consumer Ownership Models for the Transition to a Renewable Smart Energy System in Denmark. An Exploratory Study. Energies. 2020; 13(6):1508. https://doi.org/10.3390/en13061508

Chicago/Turabian StyleGorroño-Albizu, Leire. 2020. "The Benefits of Local Cross-Sector Consumer Ownership Models for the Transition to a Renewable Smart Energy System in Denmark. An Exploratory Study" Energies 13, no. 6: 1508. https://doi.org/10.3390/en13061508