Technological Progress and Supply Base under Uncertain Market Conditions: The Case Study of the Taiwanese c-Si Solar Industry 2016–2019

Abstract

:

1. Introduction

2. Global PV Market Dynamics: The Taiwanese Perspective

- (1)

- Lagging technological progress. An absence of adequate supervision results in low standards, which lead to nonspecific demand. Particular members of the industry network were weakly affiliated, which negatively affected R&D diffusion. Although impressive in scale, the industry was underdeveloped from the technological aspect, leading to low-end processing. The main reason for this situation was the uncontrolled pace of growth and the lack of consistent national policies for manufacturers. In effect, the industry relied on technology transfers, which positioned China behind the EU, the US, Japan, and also Taiwan. In the later stages, due to the leapfrogging strategy, the technological gap gradually diminished. Therefore, the technological advancements of Chinese companies became acknowledged [23].

- (2)

- Overcapacity. A chaotic system led to structural imperfections. Chinese companies witnessed a negative correlation between the scale effect and profit. The production capacities overlapped since the products competed mostly with the lower costs obtained through improved managerial and production efficiency. The diffusion of the innovation was too low, and the products were rather homogeneous than diversified [24]. Overall, in 2014, PV manufacturing in China was composed of around 1000 entities in which a majority were active in the low entry barrier module assembling. Although the total capacity was estimated at around 70 GW, the line utilization did not surpass 50% [25]. In their research, Zhao and Zhang concluded that growth relied on cheap labour rather than on the positive average level of the frontier technological progress while the growth rate of the total productivity was negative until 2013 [7].

- (3)

- The local markets of the underdeveloped capacities absorbed the number of installations, which could not ensure the producers’ profits. As a result, Chinese and Taiwanese PV companies were overexposed to significant business risks associated with fluctuations in demand. Previous literature mainly focuses on the aftermath of the financial crisis of 2008 (followed by the relative stabilization), and the uncertainty caused by the anti-dumping regulations introduced by the EU and the US in 2014 at a time when Taiwan exported around 90% of its PV output [12].

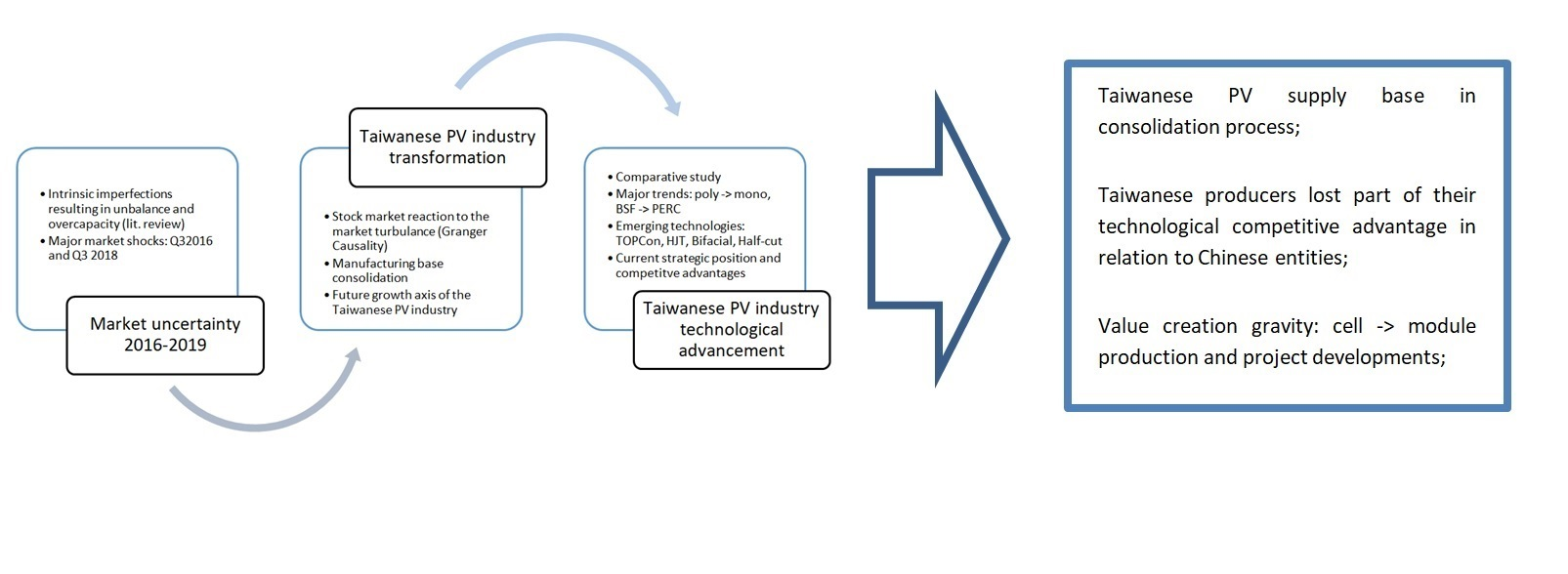

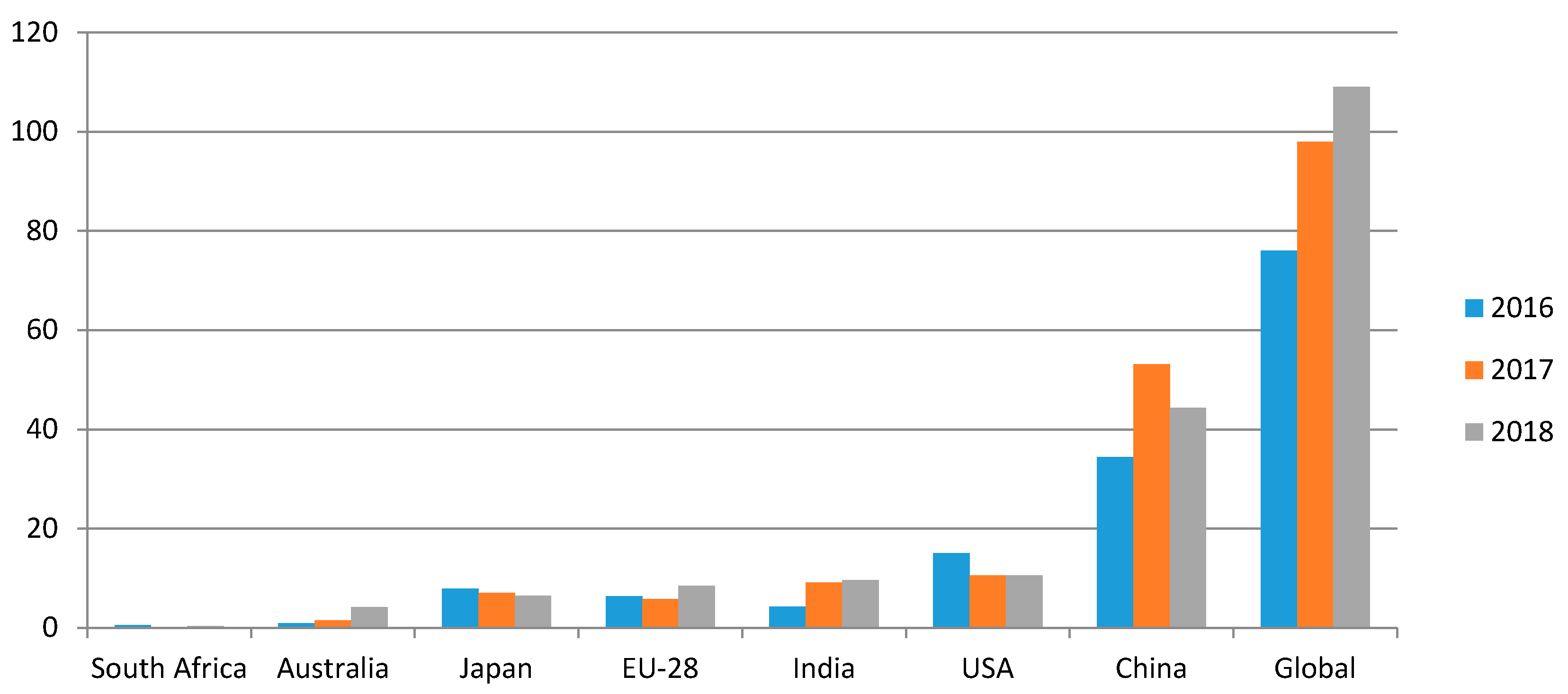

3. Taiwanese PV Industry under Uncertain Market Conditions

3.1. Research Logic and Objective

3.1.1. Market Uncertainty 2016–2019

3.1.2. Taiwanese PV Industry Transformation

- -

- Null Hypothesis: X does not Granger Cause Y

- -

- Alternative Hypothesis: Y does Granger Cause X

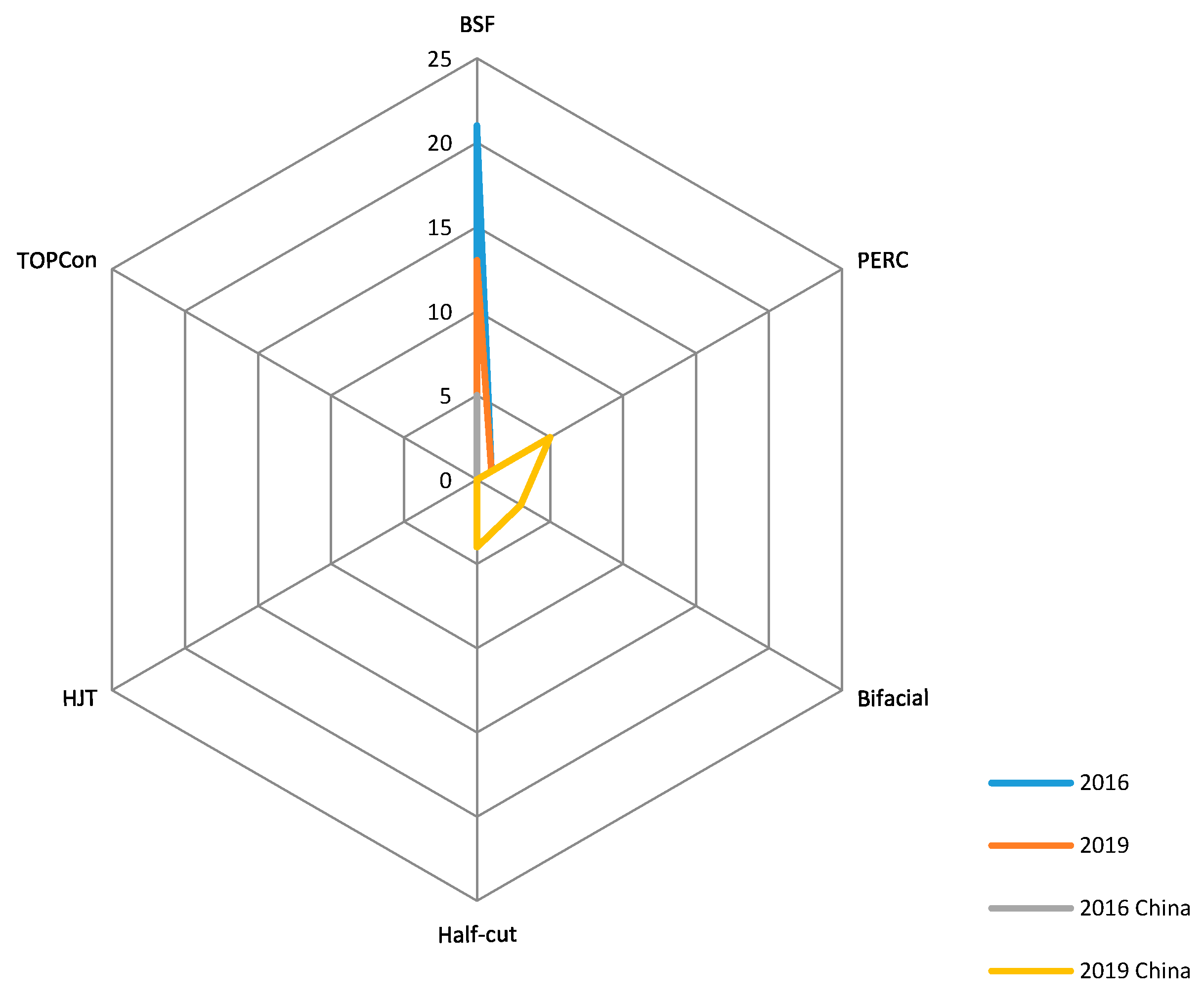

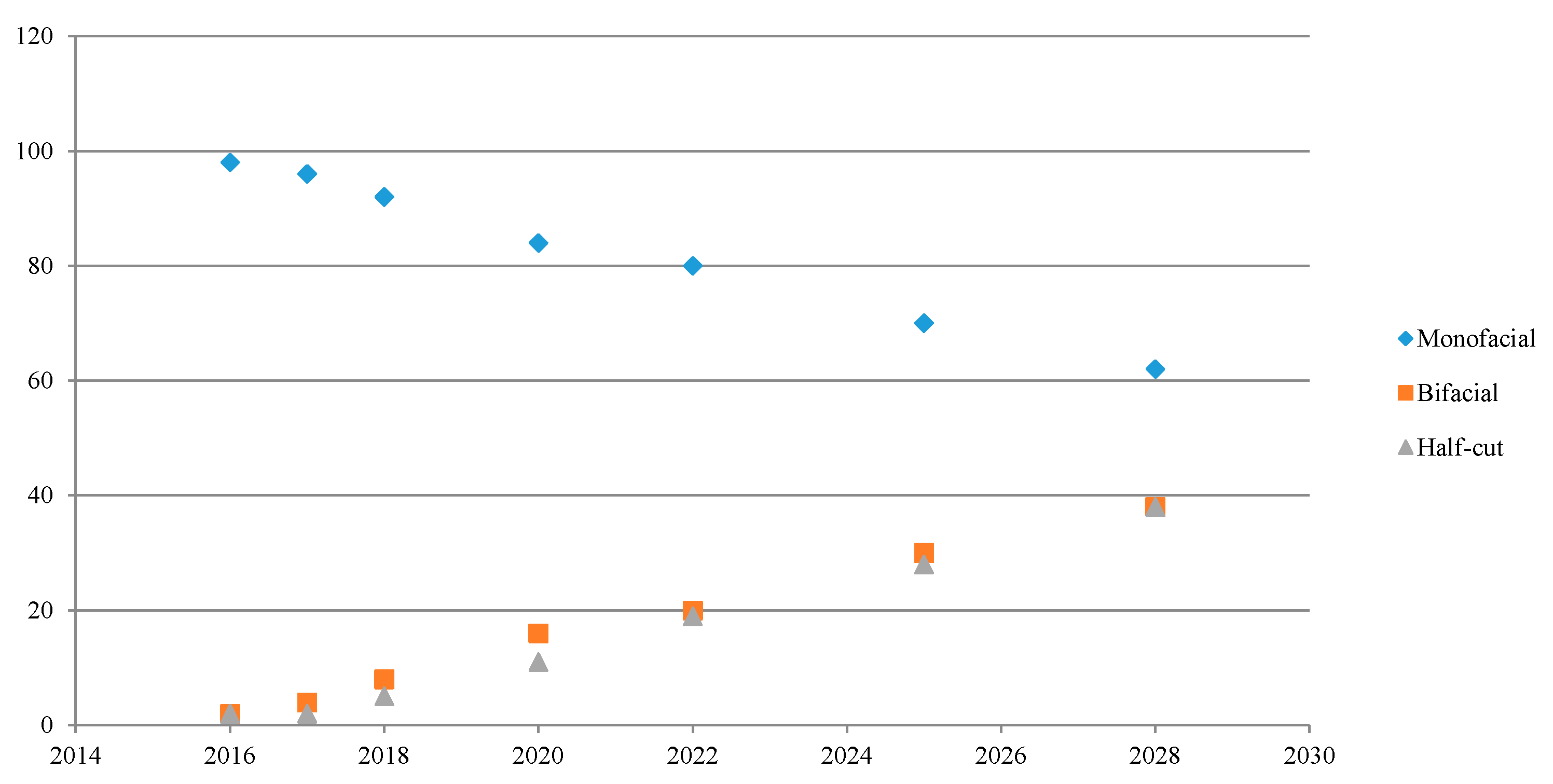

3.1.3. Taiwanese PV Industry Technological Advancement

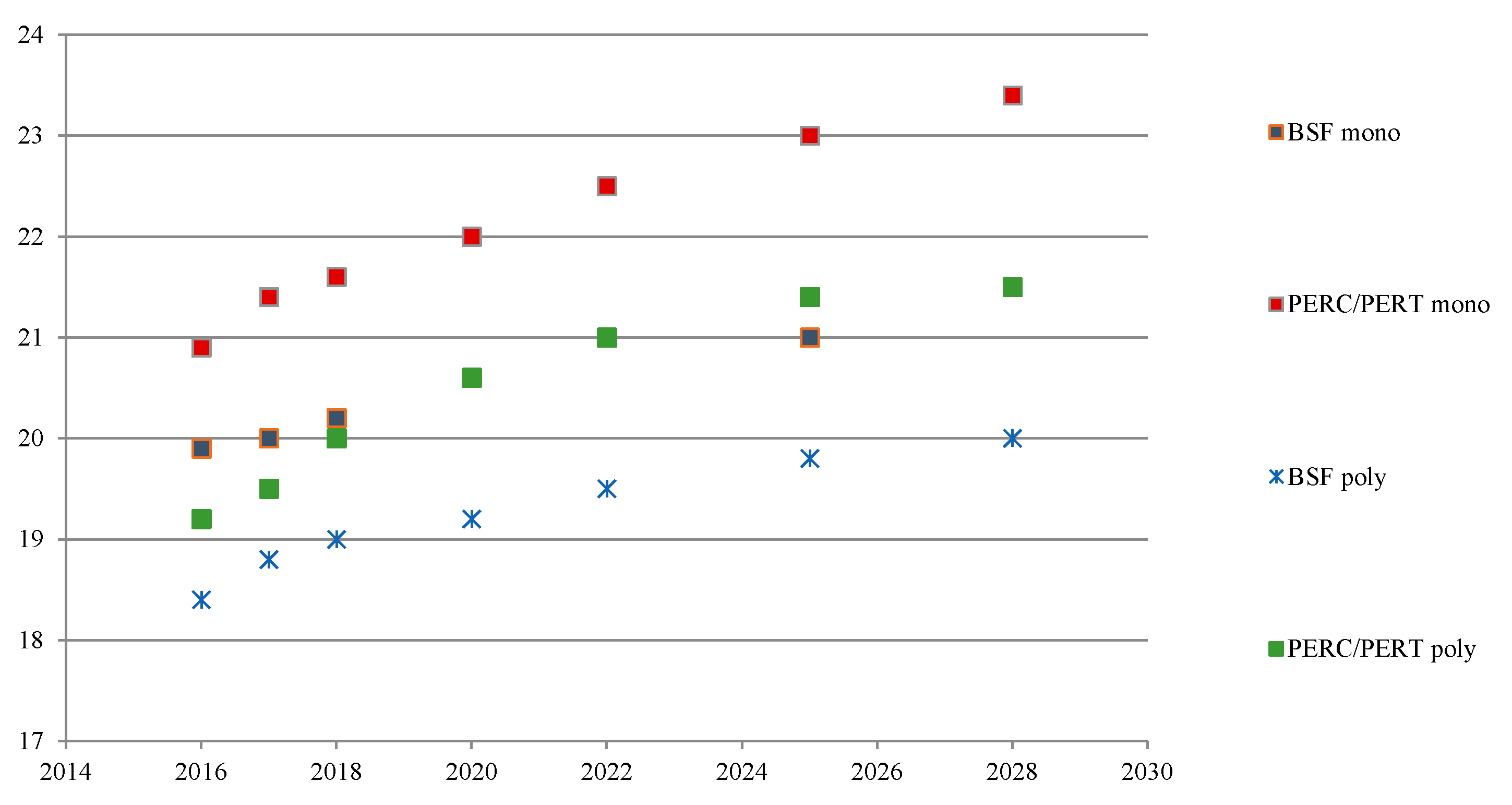

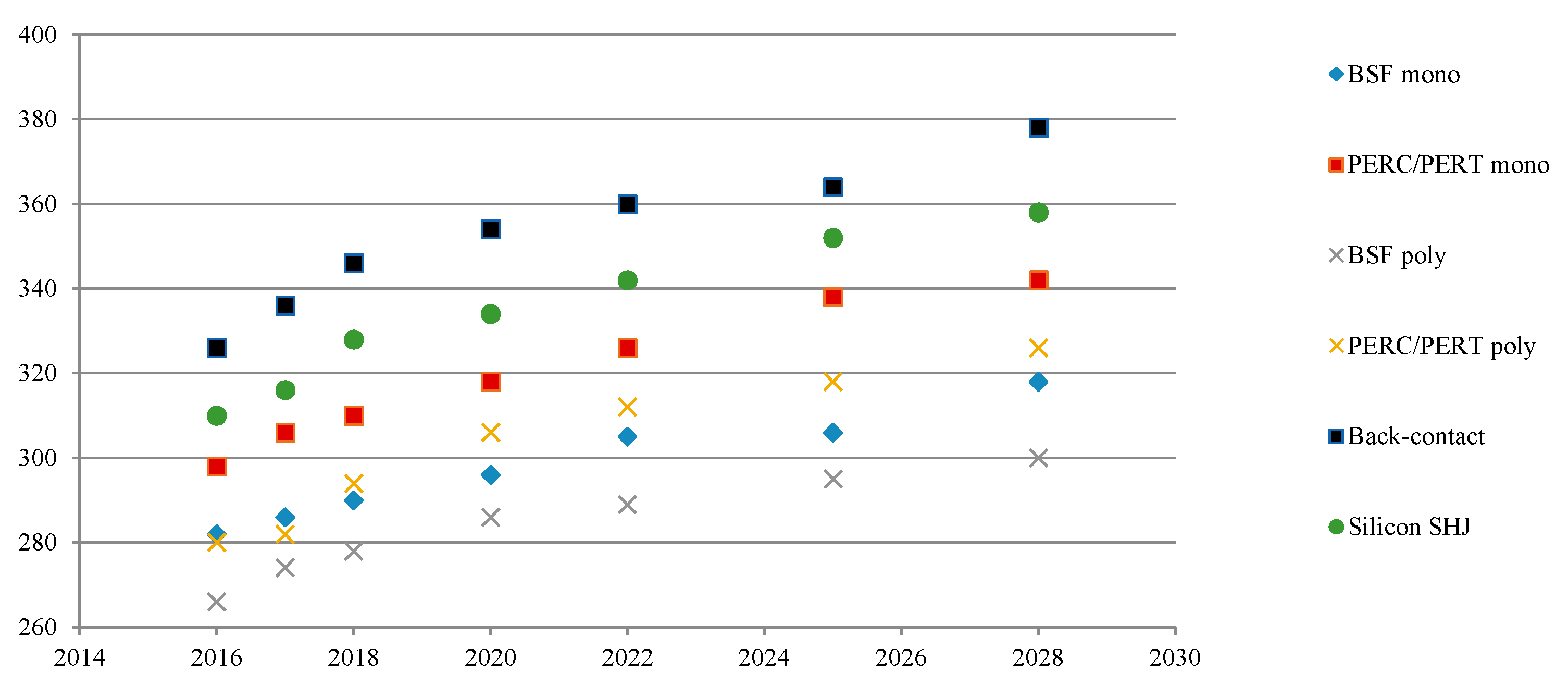

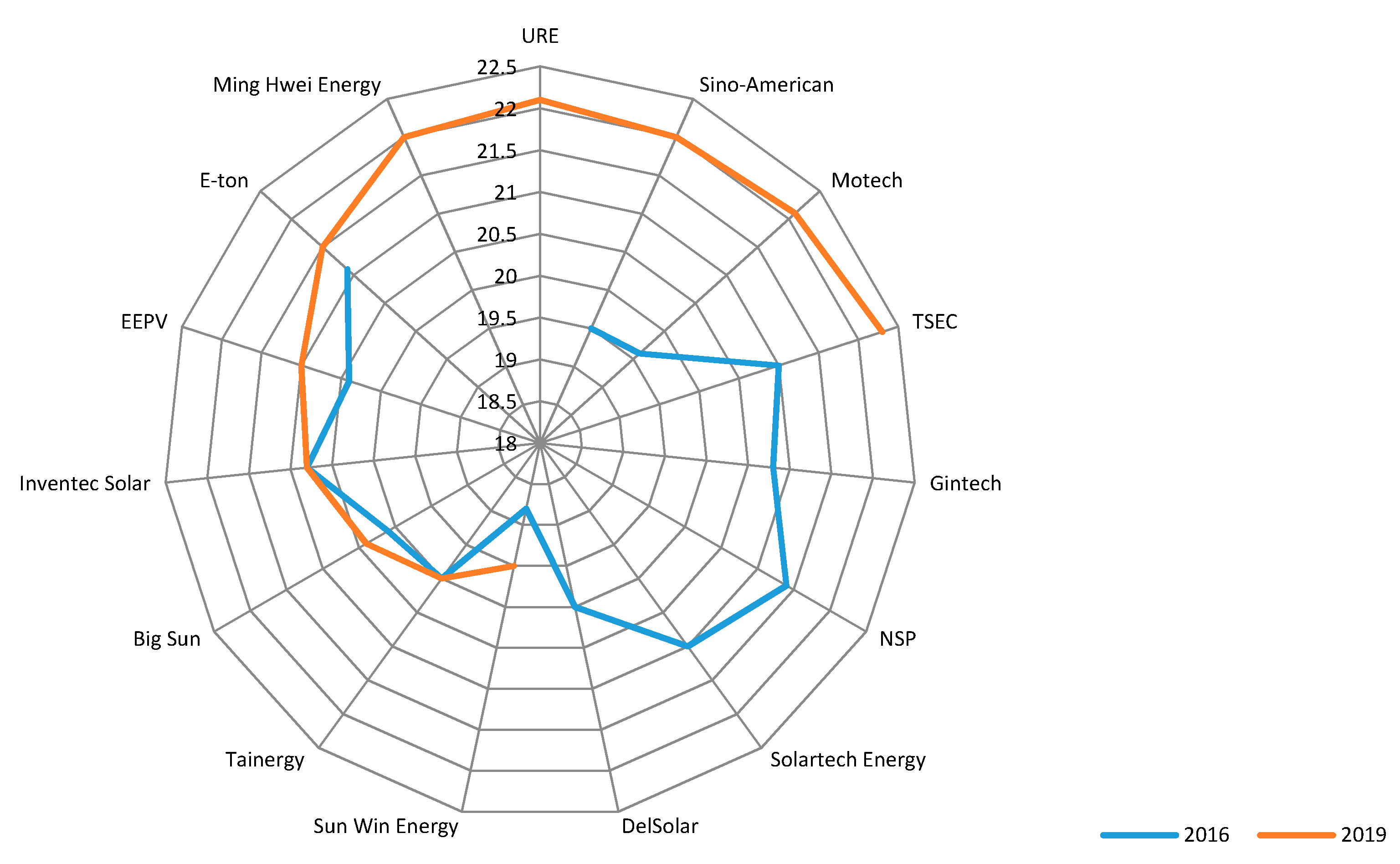

- (1)

- Quantitative: cell and module efficiencies, efficiency, and power progress noted in cell and module categories.

- (2)

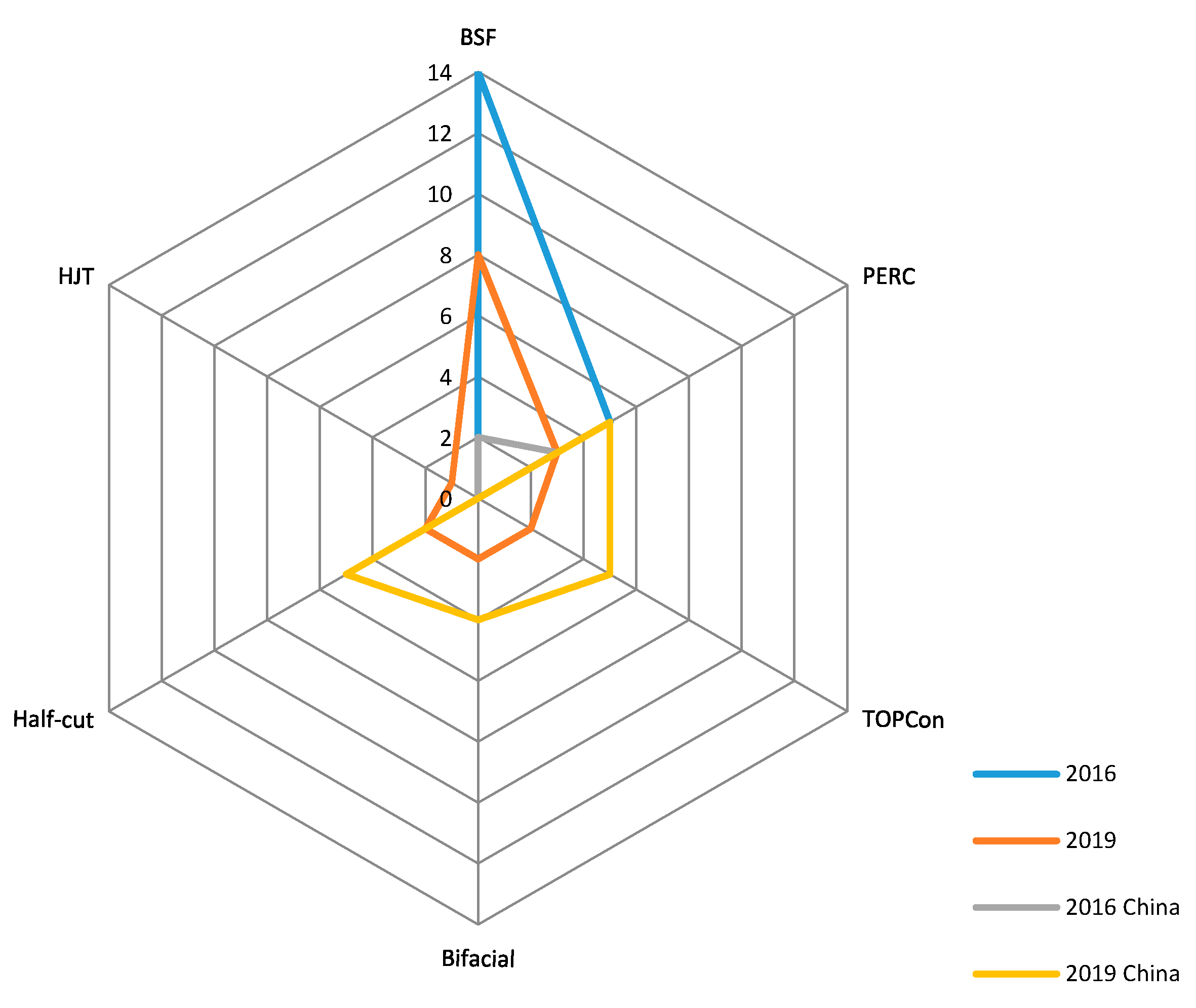

- Qualitative: cell and module technologies of the main categories of mono and poly, cell, and module technologies of the sub-categories of PERC, TOPCon, HJT, Bifacial, and Half-cut.

3.2. Results

3.2.1. Market Uncertainty 2016–2019

3.2.2. Taiwanese PV Industry Transformation

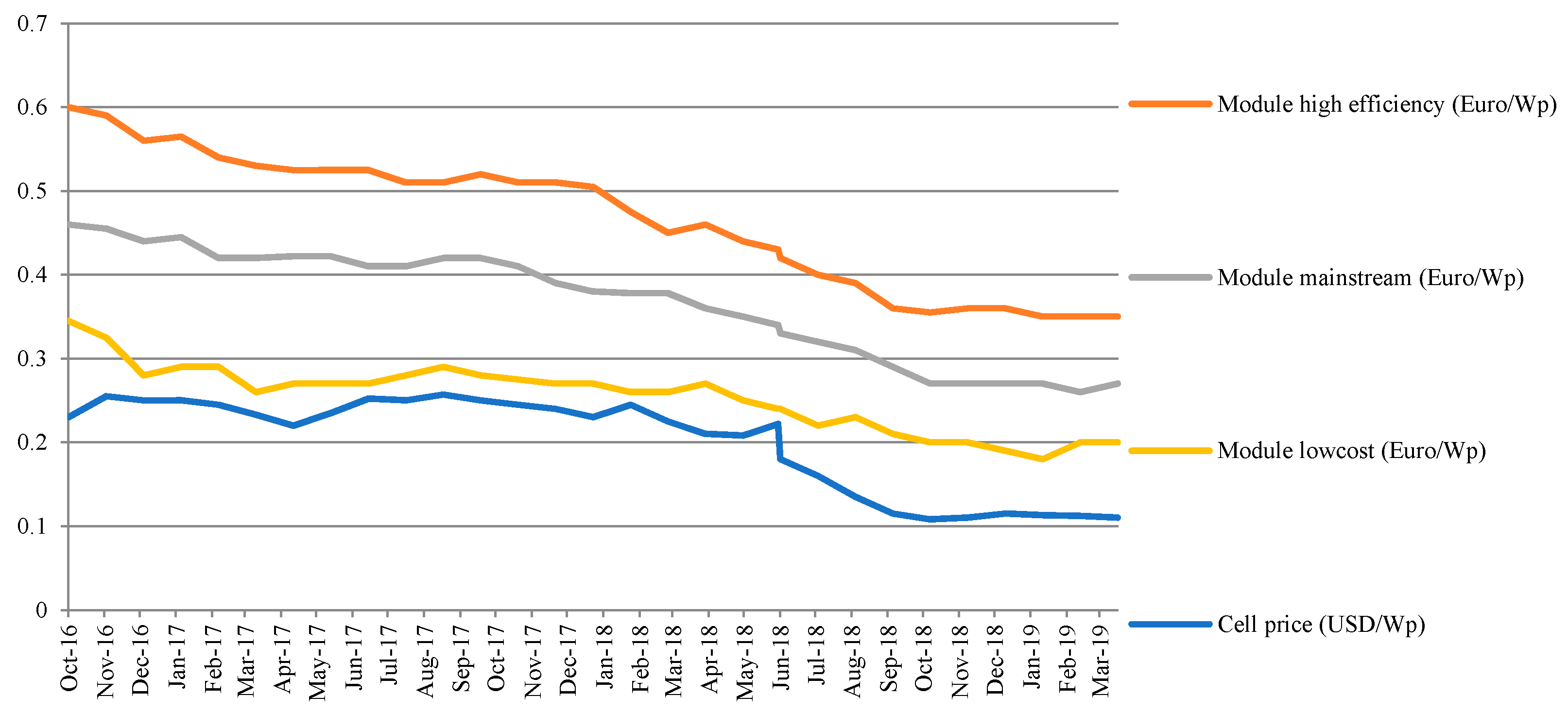

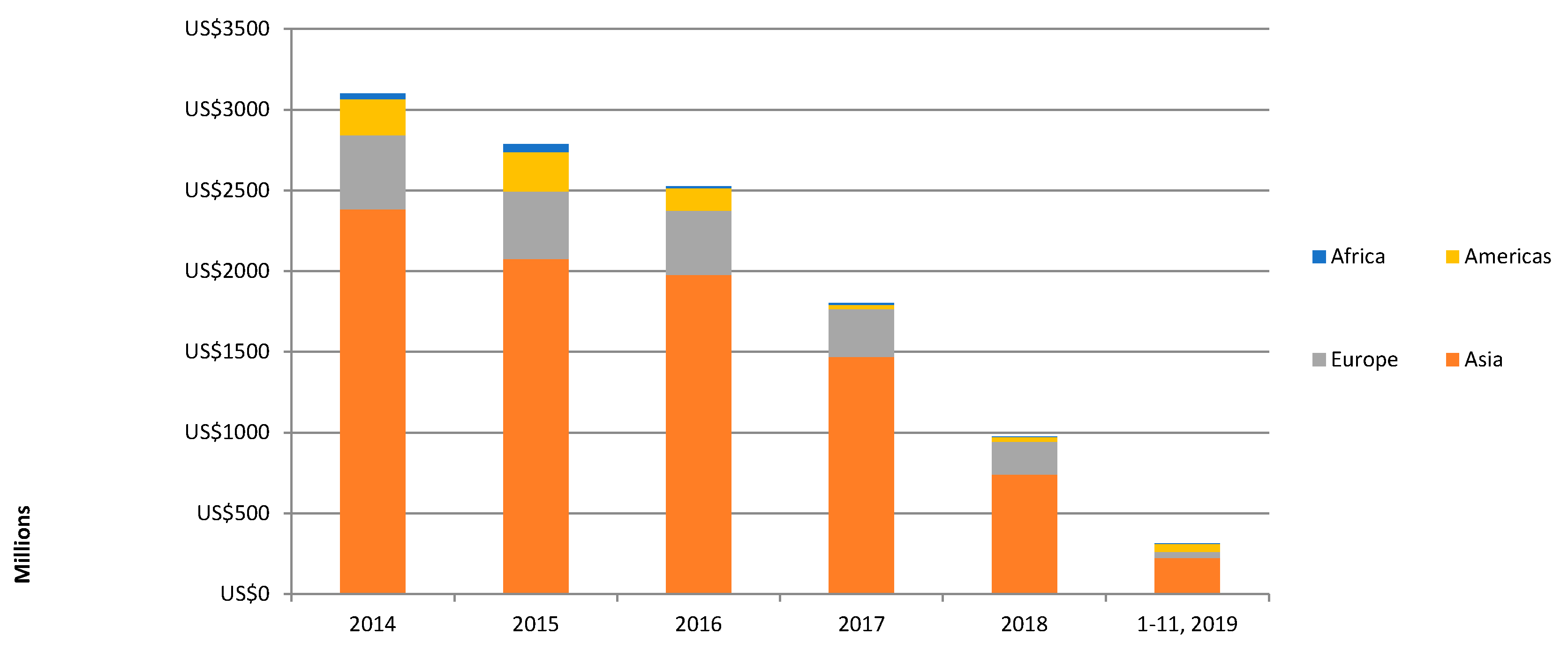

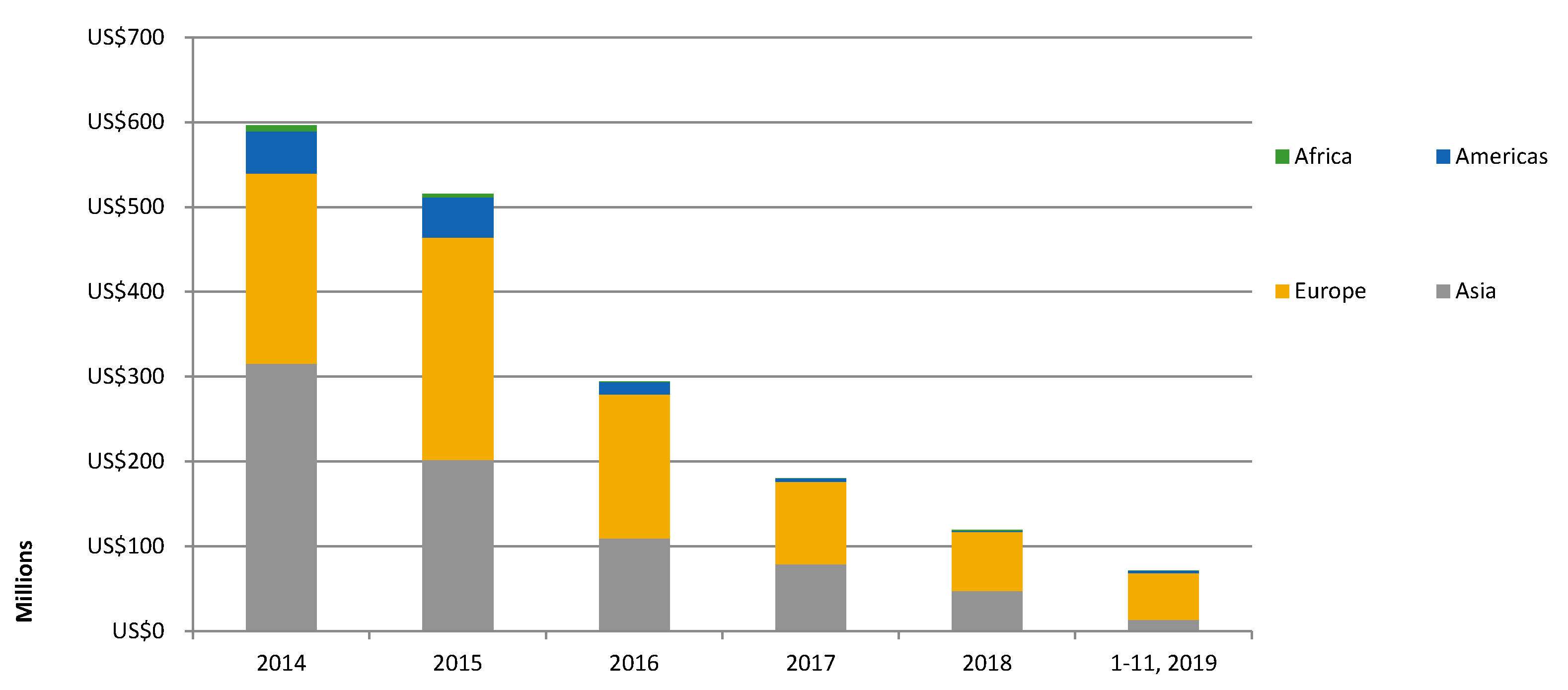

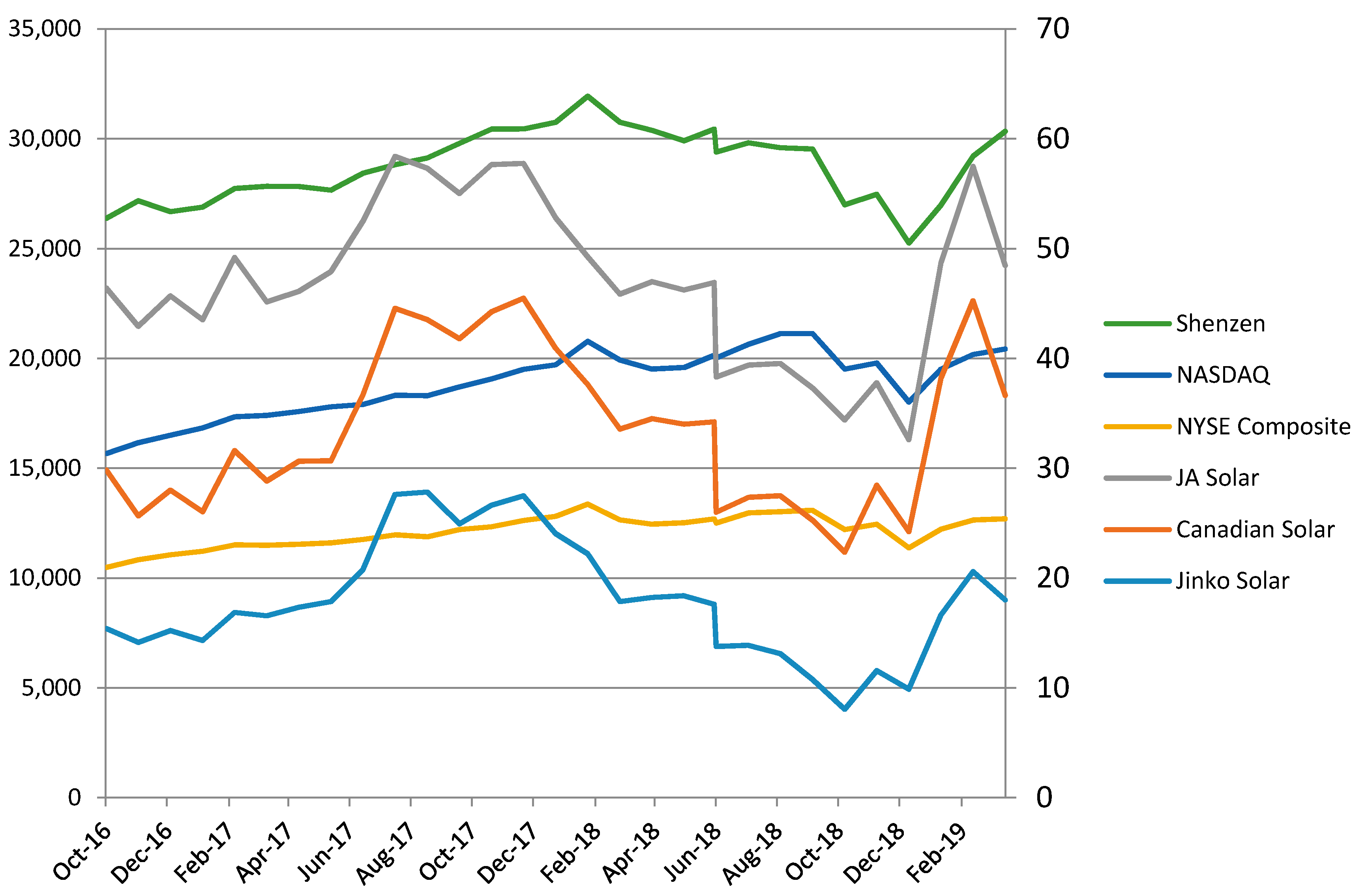

Sales and Operation

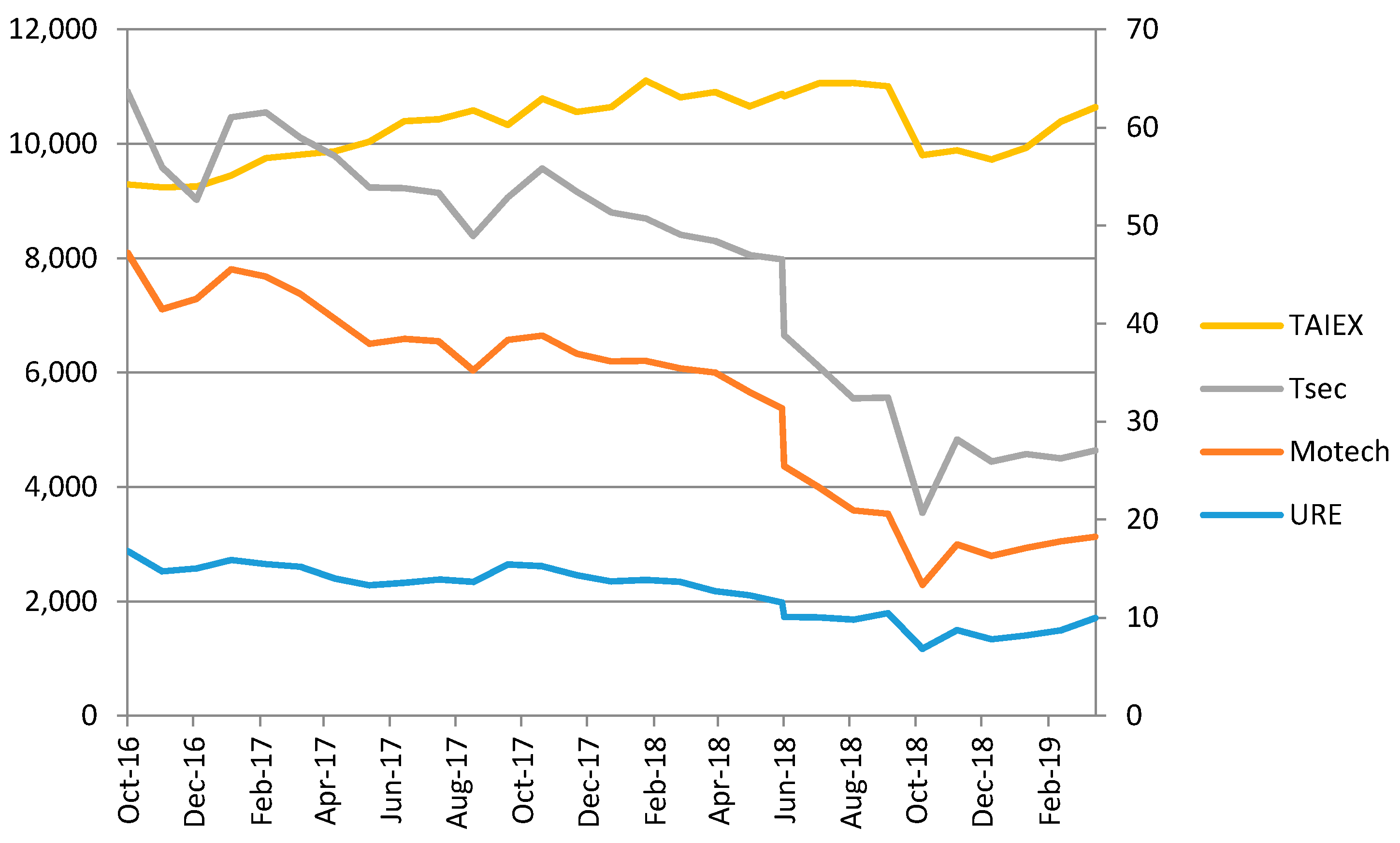

Stock Market Performance

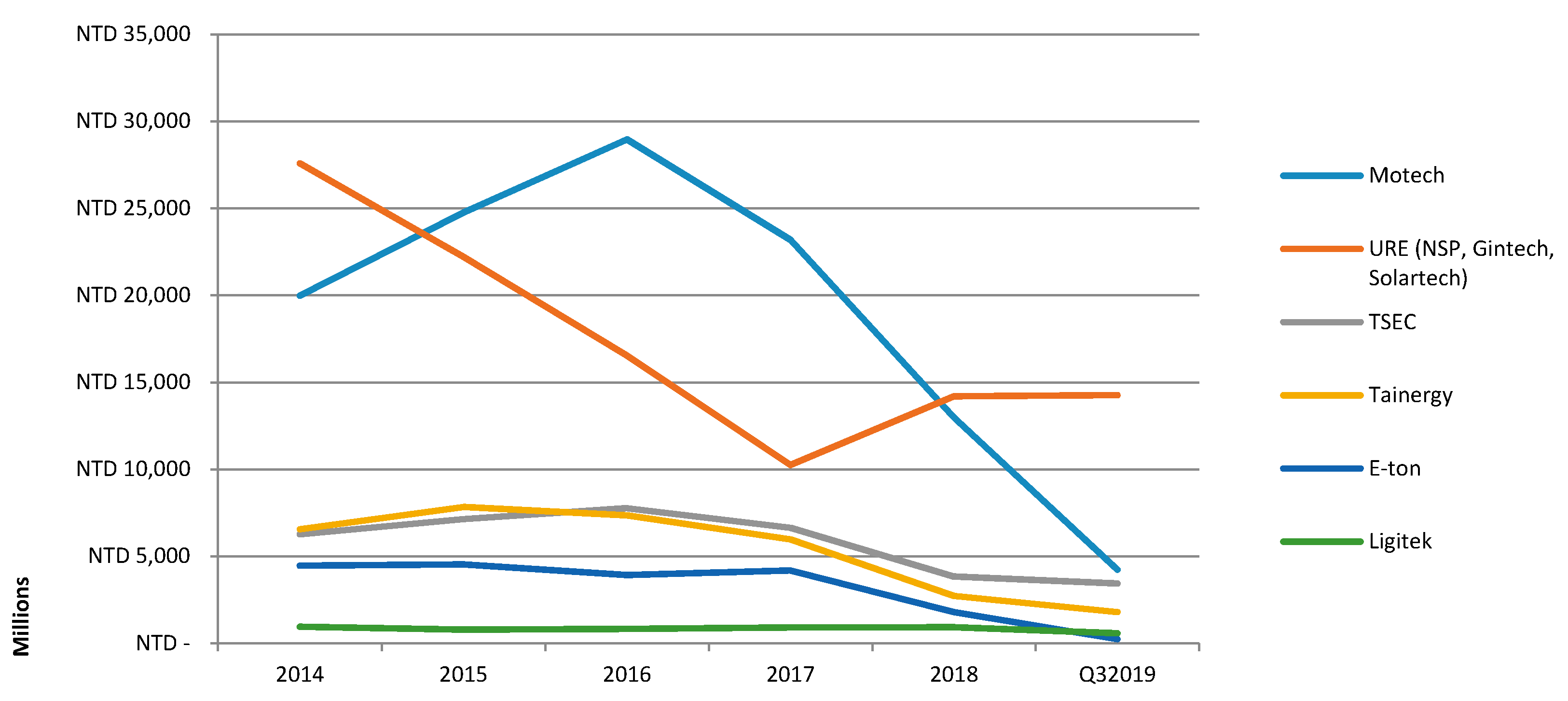

Industry Consolidation

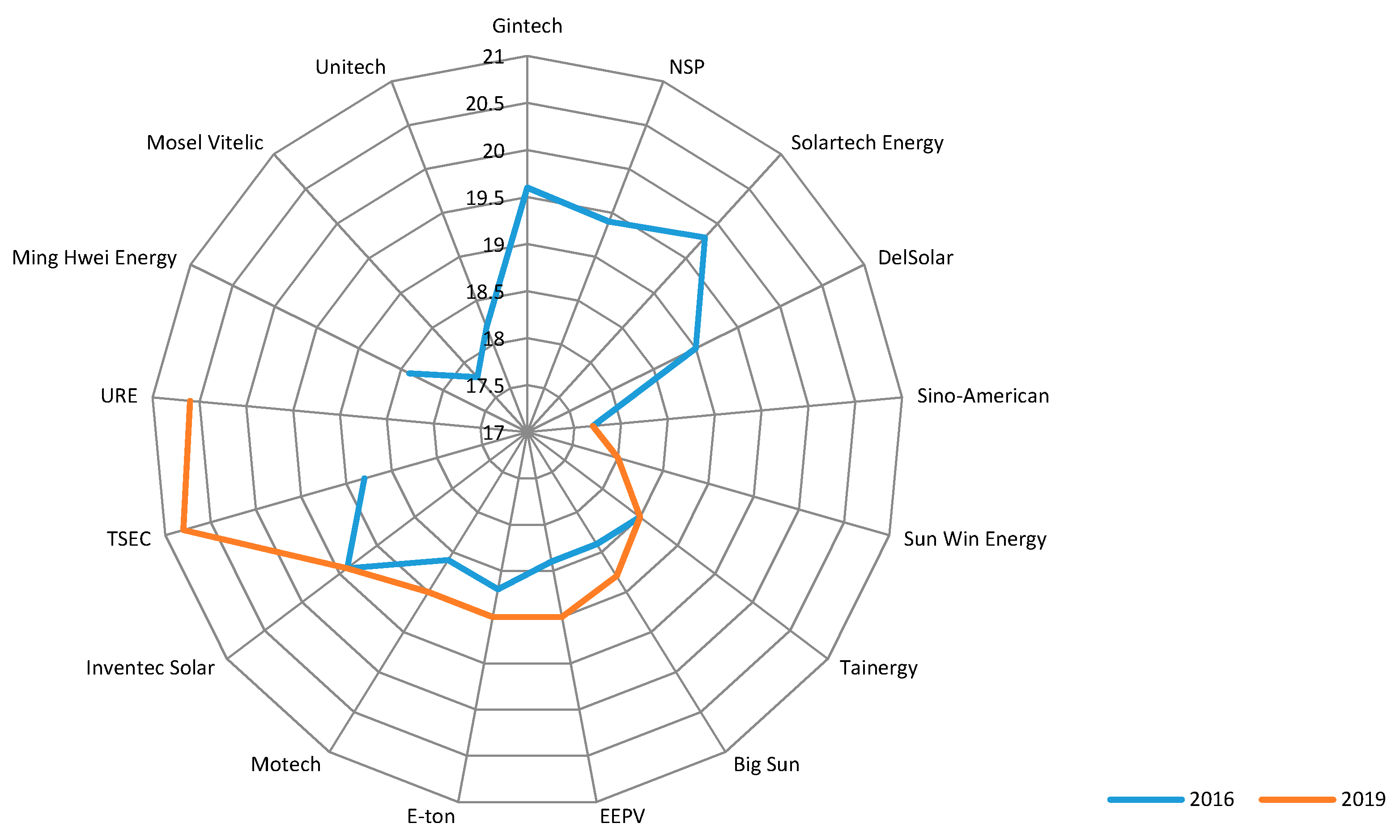

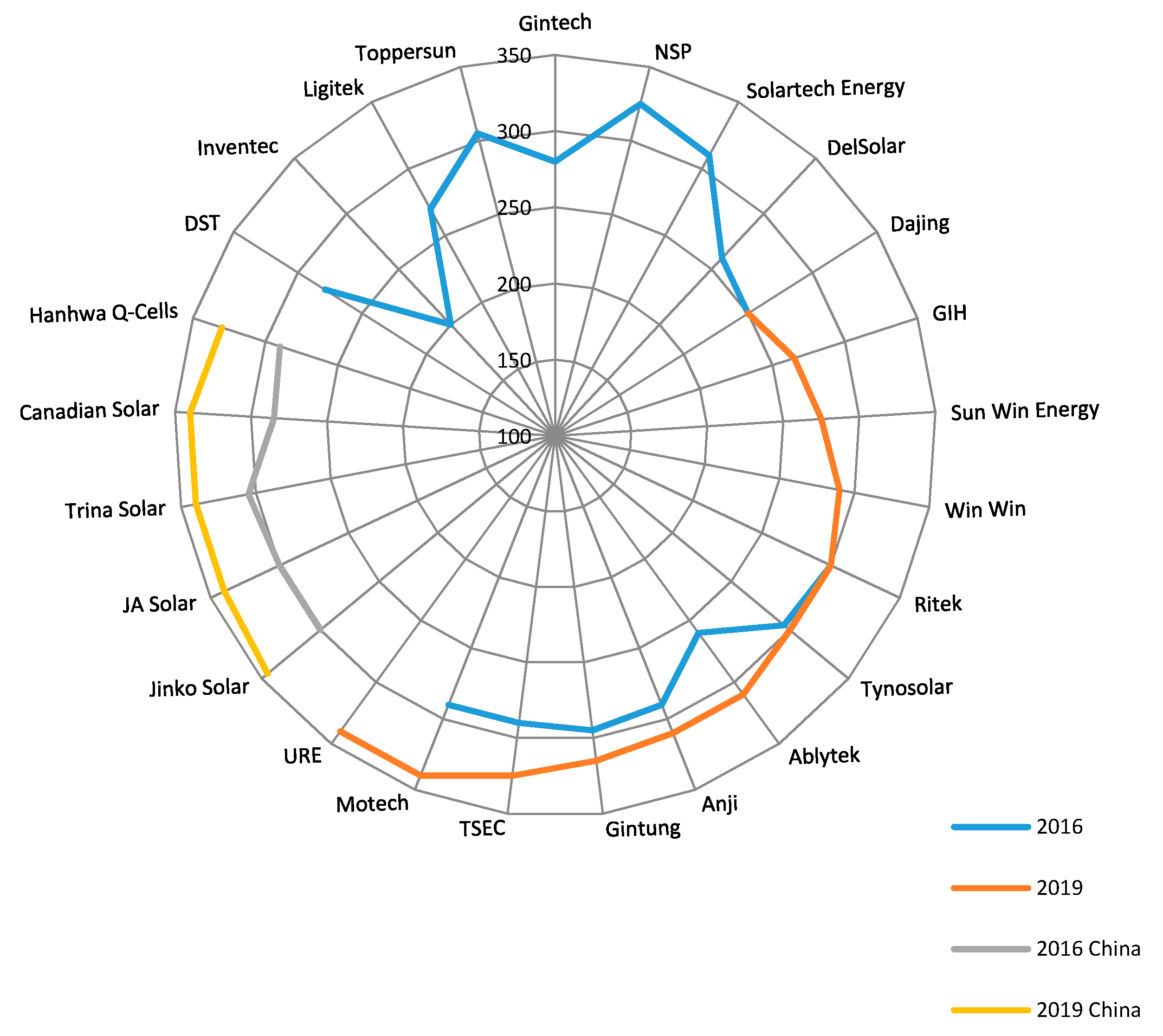

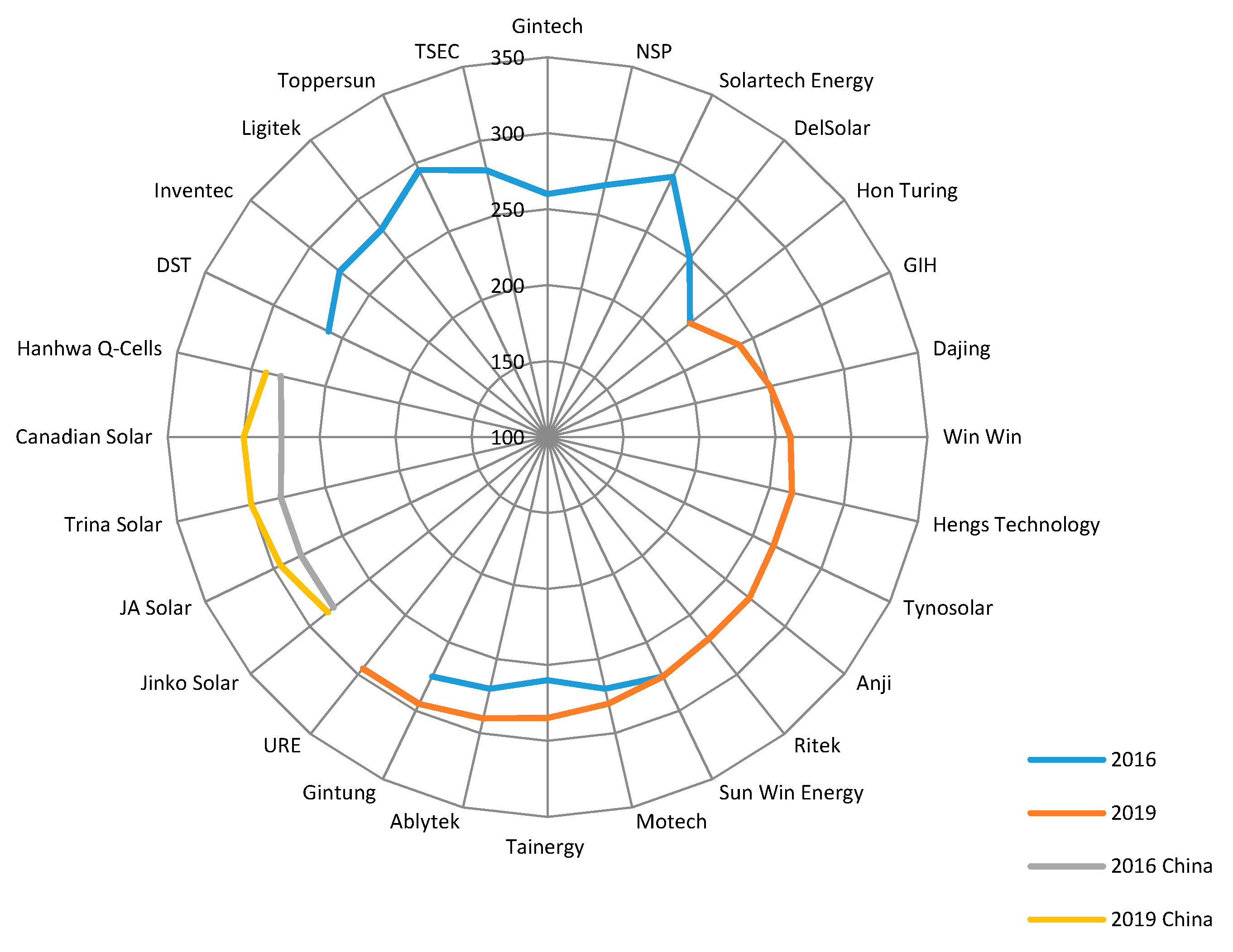

3.2.3. Taiwanese PV Industry Technological Advancement

3.3. Discussion

3.3.1. Industry Transformation

3.3.2. Technological Advancement

4. Conclusions

Author Contributions

Funding

Conflicts of Interest

Abbreviations

| PV | Photovoltaics |

| FDP | Foreign Direct Investment |

| R&D | Research and Development |

| PERC | Passivated Emitter and Rear Cell |

| ASP | Average Selling Price |

| BSF | Back Surface Field |

| HJT | Heterojunction Technology |

| TOPCon | Tunnel Oxide Passivated Contact |

| IBC | Interdigitated Back Contact |

| LCOE | Levelized Cost of Electricity |

Appendix A

| Company Name | Cell Type | Q32016 | Q22019 | Efficiency Progress (%) | ||||

|---|---|---|---|---|---|---|---|---|

| Cell Technology | Power/Cell (W) | Top Efficiency (%) | Cell Technology | Power/Cell (W) | Top Efficiency (%) | |||

| Big Sun | Mono | BSF | 4.91 | 20.1 | BSF | 4.984 | 20.4 | 0.3 |

| Poly | BSF | 4.48 | 18.4 | BSF | 4.619 | 18.8 | 0.4 | |

| DelSolar | Mono | BSF | 4.78 | 20 | BSF | 4.78 | 20 | 0 |

| Poly | BSF | 4.62 | 19 | BSF | 4.62 | 19 | 0 | |

| EEPV | Mono | BSF | 4.98 | 20.4 | BSF | 5.13 | 21 | 0.6 |

| Poly | BSF | 4.48 | 18.4 | BSF | 4.67 | 19 | 0.6 | |

| E-ton | Mono | PERC | 4.55 | 21.1 | PERC | 5.25 | 21.5 | 0.4 |

| Poly | BSF | 5.16 | 18.7 | BSF | 4.67 | 19 | 0.3 | |

| Gintech | Mono | PERC | 5.55 | 21.44 | PERC | 5.35 | 21.9 | 0.46 |

| Poly | PERC | 4.77 | 19.6 | BSF | 4.62 | 18.8 | -0.8 | |

| Inventec Solar | Mono | PERC | 4.94 | 20.8 | PERC, Bifacial | 4.94 | 20.8 | 0 |

| Poly | PERC | 4.64 | 19.4 | PERC | 4.64 | 19.4 | 0 | |

| Ming Hwei Energy | Mono | PERC | 5.682 | 22 | ||||

| Poly | BSF | 4.48 | 18.4 | |||||

| Mosel Vitelic | Mono | |||||||

| Poly | BSF | 4.34 | 17.79 | |||||

| Motech | Mono | BSF | 4.68 | 19.6 | PERC, Bifacial | 5.4 | 22.1 | 2.5 |

| Poly | BSF | 4.53 | 18.6 | BSF | 4.67 | 19 | 0.4 | |

| NSP | Mono | PERC | 5.228 | 21.4 | PERC, Bifacial | 5.351 | 21.9 | 0.5 |

| Poly | PERC | 4.721 | 19.4 | PERC | 4.914 | 20 | 0.6 | |

| Sinco american | Mono | BSF | 4.65 | 19.5 | TOPcon | 4.65 | 22 | 0 |

| Poly | BSF | 4.3 | 17.7 | BSF | 4.3 | 17.7 | 0 | |

| Solartech Energy | Mono | PERC | 5.11 | 21 | PERC | 5.326 | 21.9 | 0.9 |

| Poly | PERC | 4.79 | 19.8 | PERC, Half-cut | 5.037 | 20.6 | 0.8 | |

| Sun Win Energy | Mono | BSF | 4.505 | 18.8 | BSF | 4.66 | 19.5 | 0.7 |

| Poly | BSF | 4.38 | 18 | BSF | 4.38 | 18 | 0 | |

| Tainergy | Mono | BSF | 4.86 | 20 | BSF | 4.86 | 20 | 0 |

| Poly | BSF | 4.5 | 18.5 | BSF | 4.5 | 18.5 | 0 | |

| TSEC | Mono | PERC | 5.13 | 21 | PERC | 5.45 | 22.3 | 1.3 |

| Poly | BSF | 4.58 | 18.8 | PERC | 5.11 | 20.8 | 2 | |

| Unitech | Mono | |||||||

| Poly | BSF | 4.38 | 18.2 | |||||

| Company Name | Type | Q32016 | Q22019 | Module Power Progress (W) | ||||

|---|---|---|---|---|---|---|---|---|

| Cell Technology | Power/Module (W) | Top Efficiency (%) | Cell Technology | Power/Module (W) | Top Efficiency (%) | |||

| Ablytek | Mono | BSF | 260 | 15.93 | BSF | 310 | 19.05 | 50 |

| Poly | BSF | 270 | 16.59 | BSF | 290 | 17.83 | 20 | |

| Anji | Mono | BSF | 290 | 17.9 | BSF | 310 | 19.9 | 20 |

| Poly | BSF | 270 | 16.6 | BSF | 270 | 16.6 | 0 | |

| Dajing | Mono | BSF | 250 | 15.26 | BSF | 250 | 15.26 | 0 |

| Poly | BSF | 250 | 15.26 | BSF | 250 | 15.26 | 0 | |

| DelSolar | Mono | BSF | 260 | 15.9 | BSF | 260 | 15.9 | 0 |

| Poly | BSF | 250 | 15.3 | BSF | 250 | 15.3 | 0 | |

| DST | Mono | BSF | 279 | 16.57 | ||||

| Poly | BSF | 260 | 15.95 | |||||

| GIH | Mono | BSF | 265 | 16.17 | BSF | 265 | 16.17 | 0 |

| Poly | BSF | 240 | 14.64 | BSF | 240 | 14.64 | 0 | |

| Gintech | Mono | BSF | 280 | 17.2 | ||||

| Poly | BSF | 260 | 16 | |||||

| Gintung | Mono | BSF | 295 | 18.31 | BSF | 315 | 19.55 | 20 |

| Poly | BSF | 275 | 17.07 | BSF | 295 | 18.31 | 20 | |

| Hengs Technology | Mono | |||||||

| Poly | BSF | 265 | 16.29 | BSF | 265 | 16.29 | 0 | |

| Hon Turing | Mono | |||||||

| Poly | BSF | 220 | 13.26 | BSF | 220 | 13.26 | 0 | |

| Inventec | Mono | PERC | 300 | 18.4 | ||||

| Poly | PERC | 275 | 16.9 | |||||

| Ligitek | Mono | BSF | 270 | 16.8 | ||||

| Poly | BSF | 275 | 17.1 | |||||

| Motech | Mono | BSF | 290 | 17.5 | PERC, Bifacial | 340 | 19.6 | 50 |

| Poly | BSF | 270 | 16.5 | BSF | 280 | 17.2 | 10 | |

| NSP | Mono | PERC | 325 | 20 | PERC, Bifacial, Half-cut | 335 | 20.2 | 10 |

| Poly | BSF | 270 | 16.6 | PERC | 295 | 18.1 | 25 | |

| Ritek | Mono | BSF | 300 | 18.44 | BSF | 300 | 18.44 | 0 |

| Poly | BSF | 270 | 16.6 | BSF | 270 | 16.6 | 0 | |

| Solartech | Mono | PERC | 310 | 18.91 | PERC | 310 | ||

| Poly | BSF | 290 | 17.69 | PERC | 295 | 5 | ||

| Sun Win Energy | Mono | BSF | 275 | 16.87 | BSF | 275 | 16.87 | 0 |

| Poly | BSF | 275 | 16.87 | BSF | 275 | 16.87 | 0 | |

| Tainergy | Mono | |||||||

| Poly | BSF | 260 | 16.4 | BSF | 285 | 17.5 | 25 | |

| Toppersun | Mono | BSF | 305 | 18.7 | ||||

| Poly | BSF | 295 | 18.1 | |||||

| TSEC | Mono | PERC | 290 | 20.23 | PERC, Half-cut | 325 | 19.9 | 35 |

| Poly | BSF | 280 | 19.53 | |||||

| Tynosolar | Mono | BSF | 295 | 18.1 | BSF | 300 | 18.44 | 5 |

| Poly | BSF | 265 | 16.18 | BSF | 265 | 16.29 | 0 | |

| Win Win | Mono | PERC | 290 | 17.46 | PERC | 290 | 17.46 | 0 |

| Poly | BSF | 260 | 15.65 | BSF | 260 | 15.65 | 0 | |

| Jinko Solar (CN) | Mono | PERC | 300 | 18.33 | PERC, Half-cut, Bifacial | 345 | 20.45 | 45 |

| Poly | BSF | 280 | 17.11 | PERC, Half-cut, Bifacial | 285 | 17.41 | 5 | |

| JA Solar (CN) | Mono | PERC | 300 | 18.35 | PERC, Half-cut, Bifacial | 340 | 20.2 | 40 |

| Poly | BSF | 280 | 17.2 | PERC, Half-cut, Bifacial | 295 | 17.5 | 15 | |

| Trina Solar (CN) | Mono | PERC | 305 | 18.6 | PERC, Half-cut, Bifacial | 340 | 19.9 | 35 |

| Poly | BSF | 280 | 17.1 | PERC, Half-cut, Bifacial | 300 | 17.6 | 20 | |

| Canadian Solar (CN) | Mono | BSF | 285 | 17.41 | PERC, Half-cut | 340 | 19.86 | 55 |

| Poly | BSF | 275 | 16.8 | PERC | 300 | 18.05 | 25 | |

| Hanhwa Q-Cells (KR) | Mono | BSF | 290 | 17.7 | PERC, Half-cut | 330 | 19.6 | 40 |

| Poly | BSF | 280 | 17.1 | PERC, Half-cut | 290 | 17.4 | 10 | |

References

- Cao, J.; Groba, F. Chinese Renewable Energy Technology Exports: The Role of Policy, Innovation and Markets. SSRN Electron. J. 2013, 60, 243–283. [Google Scholar] [CrossRef] [Green Version]

- Xiong, Y.; Yang, X. Government subsidies for the Chinese photovoltaic industry. Energy Policy 2016, 99, 111–119. [Google Scholar] [CrossRef]

- Wu, C.-Y.; Mathews, J.A. Knowledge flows in the solar photovoltaic industry: Insights from patenting by Taiwan, Korea, and China. Res. Policy 2012, 41, 524–540. [Google Scholar] [CrossRef]

- Zhang, F.; Gallagher, K. Innovation and technology transfer through global value chains: Evidence from China’s PV industry. Energy Policy 2016, 94, 191–203. [Google Scholar] [CrossRef]

- Calantone, R.J.; Garcia, R.; Droge, C. The Effects of Environmental Turbulence on New Product Development Strategy Planning. J. Prod. Innov. Manag. 2003, 20, 90–103. [Google Scholar] [CrossRef]

- Yun, S.; Lee, J.; Lee, S. Technology development strategies and policy support for the solar energy industry under technological turbulence. Energy Policy 2019, 124, 206–214. [Google Scholar] [CrossRef]

- Zhao, X.; Zhang, Y. Technological progress and industrial performance: A case study of solar photovoltaic industry. Renew. Sustain. Energy Rev. 2018, 81, 929–936. [Google Scholar]

- Hu, M.; Mathews, J. Taiwan’s Green Shift—Prospects and Challenges. Asia Pac. J. Jpn. Focus 2016, 14, 4960. [Google Scholar]

- Hu, J.-L.; Yeh, F.-Y. The Value Migration and Innovative Capacity of Taiwan’s Photovoltaic Industry. Energy Sources Part B Econ. Plan. Policy 2013, 8, 190–199. [Google Scholar] [CrossRef]

- Jia, F.; Sun, H.; Koh, L. Global solar photovoltaic industry: An overview and national competitiveness of Taiwan. J. Clean. Prod. 2016, 126, 550–562. [Google Scholar] [CrossRef]

- Liou, H.M. Policies and legislation driving Taiwan’s development of renewable energy. Renew. Sustain. Energy Rev. 2010, 14, 1763–1781. [Google Scholar] [CrossRef]

- Liu, C.-S.; Hsiao, C.-T.; Chang, D.-S.; Hsiao, C.-H. How the European Union’s and the United States’ anti-dumping duties affect Taiwan’s PV industry: A policy simulation. Renew. Sustain. Energy Rev. 2016, 53, 296–305. [Google Scholar] [CrossRef]

- Lo, C.-C.; Wang, C.-H.; Huang, C.-C. The national innovation system in the Taiwanese photovoltaic industry: A multiple stakeholder perspective. Technol. Forecast. Soc. Chang. 2013, 80, 893–906. [Google Scholar] [CrossRef]

- Wang, C.-T.; Chiu, C.-S. Competitive strategies for Taiwan’s semiconductor industry in a new world economy. Technol. Soc. 2014, 36, 60–73. [Google Scholar] [CrossRef]

- Ruhang, X. Characteristics and prospective of China׳s PV development route: Based on data of world PV industry 2000–2010. Renew. Sustain. Energy Rev. 2016, 56, 1032–1043. [Google Scholar] [CrossRef]

- Available online: m.energytrend.com/news/20150515-8776.html (accessed on 6 October 2019).

- Available online: renewableenergyworld.com/articles/2015/02/the-top-ten-pv-manufacturers-in-2014-and-why-this-list-can-lack-meaning.html (accessed on 6 October 2019).

- Quitzow, R.; Huenteler, J.; Asmussen, H. Development trajectories in China’s wind and solar energy industries: How technology-related differences shape the dynamics of industry localization and catching up. J. Clean. Prod. 2017, 158, 122–133. [Google Scholar] [CrossRef]

- Chen, W.-M.; Kim, H.; Yamaguchi, H. Renewable energy in eastern Asia: Renewable energy policy review and comparative SWOT analysis for promoting renewable energy in Japan, South Korea, and Taiwan. Energy Policy 2014, 74, 319–329. [Google Scholar] [CrossRef]

- Mathews, J.A.; Hu, M.-C.; Wu, C.-Y. Fast-Follower Industrial Dynamics: The Case of Taiwan’s Emergent Solar Photovoltaic Industry. Ind. Innov. 2011, 18, 177–202. [Google Scholar] [CrossRef]

- Tsai, K.-H.; Yang, S.-Y. Firm innovativeness and business performance: The joint moderating effects of market turbulence and competition. Ind. Mark. Manag. 2013, 42, 1279–1294. [Google Scholar] [CrossRef]

- Zheng, C.; Kammen, D.M. An innovation-focused roadmap for a sustainable global photovoltaic industry. Energy Policy 2014, 67, 159–169. [Google Scholar] [CrossRef]

- Wang, Y.-H.; Luo, G.-L.; Guo, Y.-W. Why is there overcapacity in China’s PV industry in its early growth stage? Renew. Energy 2014, 72, 188–194. [Google Scholar] [CrossRef]

- Zou, H.; Du, H.; Ren, J.; Sovacool, B.; Zhang, Y.; Mao, G. Market dynamics, innovation, and transition in China’s solar photovoltaic (PV) industry: A critical review. Renew. Sustain. Energy Rev. 2017, 69, 197–206. [Google Scholar] [CrossRef] [Green Version]

- Wu, Y. Analysis and reflection on the situation of Chinese PV industry. Energy Technol. 2016, 58. [Google Scholar]

- VDMA. International Technology Roadmap for Photovoltaics 2018, Ninth Edition, September 2018. Available online: pv.vdma.org/documents/105945/26776337/ITRPV%20Ninth%20Edition%202018%20including%20maturity%20report%2020180904_1536055215523.pdf/a907157c-a241-eec0-310d-fd76f1685b2a (accessed on 13 October 2019).

- Chen, S. Supply Barriers and Supply Distribution under Trend of Market Decentralization. [in Chinese]. Energytrend, 9 April 2019. Available online: www.energytrend.com.tw/research/20190403-14314417.html (accessed on 1 October 2019).

- Schachinger, M. August 2017: Origin Must Not Be a Factor—Only Quality Should Count! pv-Magazine, Module Price Index, August 2017. Available online: www.pv-magazine.com/module-price-index/ (accessed on 5 October 2019).

- Schachinger, M. August 2018: Greetings from the Madhouse…, pv-Magazine, Module Price Index, August 2018. Available online: www.pv-magazine.com/module-price-index/ (accessed on 5 October 2019).

- Schachinger, M. July 2019: Everyone’s Talking about Higher Module Prices…, pv-Magazine, Module Price Index, August 2019. Available online: www.pv-magazine.com/module-price-index/ (accessed on 5 October 2019).

- Feldman, D.; Hoskins, J.; Margolis, R. Q4 2017/Q1 2018 Solar Industry Update, National Renewable Energy Laboratory, May 2018. Available online: www.nrel.gov/docs/fy18osti/71493.pdf (accessed on 15 October 2019).

- Hoskins, J.; Margolis, R. Q4 2018/Q1 2019 Solar Industry Update, National Renewable Energy Laboratory, May 2019. Available online: www.nrel.gov/docs/fy19osti/73992.pdf (accessed on 15 October 2019).

- Engle, R.F.; Granger, C.W.J. Co-Integration and Error Correction: Representation, Estimation, and Testing. Econ. 1987, 55, 251. [Google Scholar] [CrossRef]

- Chinese National Renewable Energy Center (CNREC). Chinese Energy Policy Newsletter: June 2018. Available online: http://boostre.cnrec.org.cn/wp-content/uploads/2018/06/China-Energy-Policy-Newsletter_June-2018.pdf (accessed on 1 October 2019).

- European Commission. Commission Decides Not to Extend Trade Defense Measures on Solar Panels from China. Brussels, August 2018. Available online: www.trade.ec.europa.eu/doclib/press/index.cfm?id=1904 (accessed on 3 October 2019).

- Available online: https://www.irena.org/statistics.html (accessed on 2 October 2019).

- Shuai, J.; Chen, C.-F.; Cheng, J.; Leng, Z.; Wang, Z. Are China’s solar PV products competitive in the context of the Belt and Road Initiative? Energy Policy 2018, 120, 559–568. [Google Scholar] [CrossRef]

- Zhu, L.; Xu, Y.; Pan, Y. Enabled comparative advantage strategy in China’s solar PV development. Energy Policy 2019, 133, 110880. [Google Scholar] [CrossRef]

- Green, M.A.; Hishikawa, Y.; Dunlop, E.D.; Levi, D.H.; Hohl-Ebinger, J.; Yoshita, M.; Ho-Baillie, A.W. Solar cell efficiency tables (Version 53). Prog. Photovoltaics: Res. Appl. 2018, 27, 3–12. [Google Scholar] [CrossRef] [Green Version]

- JinkoSolar. JinkoSolar Breaks World Record for Cell Efficiency and Module Output., 3 June 2018. Available online: www.jinkosolar.com/press_detail_1821.html?lan=en (accessed on 4 November 2019).

- Parnel, J. PV Innovation Can Drive European Market Forward, Says JA Solar. pv-Tech, 3 July 2019. Available online: www.pv-tech.org/news/pv-innovation-can-drive-european-market-forward-says-ja-solar (accessed on 7 November 2019).

- Fraunhofer Institute for Solar Energy Systems, ISE. Photovoltaics Report. Freiburg, 14 March 2019. Available online: https://www.ise.fraunhofer.de/content/dam/ise/de/documents/publications/studies/Photovoltaics-Report.pdf (accessed on 12 October 2019).

- Sino-American Silicon Products Inc. (SAS). SAS Launches "CelcoN" N-type High-efficiency Solar Cell/60-cell Modules Output Achieves 350W, 27 June 2019. Available online: www.saswafer.com/pages/sas/en/news/detail.aspx?ArticleId=9E190A4E32974E2F9548B1E70AA29D04 (accessed on 8 November 2019).

- Motech. Motech Announces Organization Optimization Plan, 28 November 2018. Available online: http://www.motechsolar.com/en/latestnews_20181128.php (accessed on 4 November 2019).

- Motech. Enhancing Financial Structure through Non-cash Impairment Adjustment., 18 March 2019. Available online: http://www.motechsolar.com/en/latestnews_20190318.php (accessed on 4 November 2019).

- Energy Metal News. SAS Reportedly to Invest in TOPCon Solar Cell Production. 24 December 2018. Available online: www.energymetalnews.com/2018/12/24/sas-reportedly-to-invest-in-topcon-solar-cell-production/ (accessed on 23 October 2019).

- Louwen, A.; Van Sark, W.; Schropp, R.R.; Faaij, A. A cost roadmap for silicon heterojunction solar cells. Sol. Energy Mater. Sol. Cells 2016, 147, 295–314. [Google Scholar] [CrossRef] [Green Version]

- Lin, C. Market Outlook of N-Type Technology. Infolink Report, December 2018. Available online: www.en.pvinfolink.com/userfiles/files/20181205-PVInfoLink-Market%20Outlook%20of%20N-Type%20Technology_En.pdf (accessed on 4 November 2019).

- Liu, J.; Lin, X. Empirical analysis and strategy suggestions on the value-added capacity of photovoltaic industry value chain in China. Energy 2019, 180, 356–366. [Google Scholar] [CrossRef]

- Corwin, S.; Johnson, T.L. The role of local governments in the development of China’s solar photovoltaic industry. Energy Policy 2019, 130, 283–293. [Google Scholar] [CrossRef]

- Chenavaz, R. Dynamic pricing, product and process innovation. Eur. J. Oper. Res. 2012, 222, 553–557. [Google Scholar] [CrossRef]

- Liu, W.; Atuahene-Gima, K. Enhancing product innovation performance in a dysfunctional competitive environment: The roles of competitive strategies and market-based assets. Ind. Mark. Manag. 2018, 73, 7–20. [Google Scholar] [CrossRef]

- Sun, H.; Zhi, Q.; Wang, Y.; Yao, Q.; Su, J. China’s solar photovoltaic industry development: The status quo, problems and approaches. Appl. Energy 2014, 118, 221–230. [Google Scholar] [CrossRef]

- Zoco, E. The Sun Rises on the Bifacial Module Market, pv-Magazine, IHS Markit, 10 June 2019. Available online: www.pv-magazine.com/2019/06/10/the-sun-rises-on-the-bifacial-module-market/ (accessed on 15 November 2019).

- Sun, X.; Khan, M.R.; Deline, C.; Alam, M.A. Optimization and performance of bifacial solar modules: A global perspective. Appl. Energy 2018, 212, 1601–1610. [Google Scholar] [CrossRef] [Green Version]

- Qian, J.; Thomson, A.; Blakers, A.; Ernst, M. Comparison of Half-Cell and Full-Cell Module Hotspot-Induced Temperature by Simulation. IEEE J. Photovoltaics 2018, 8, 834–839. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Company | Mainstream Module Price Granger Cause Test on Stock Valuation | Cell Price Granger Cause Test on Stock Valuation | |

|---|---|---|---|

| Taiwan | |||

| URE | p-value | 0.002 | 0.005 |

| F-value | 11.911 | 9.258 | |

| MOTECH | p-value | 0.022 | 0.148 |

| F-value | 5.902 | 2.224 | |

| TSEC | p-value | 0.006 | 0.001 |

| F-value | 9.010 | 13.602 | |

| TAIEX | p-value | 0.887 | 0.484 |

| F-value | 0.021 | 0.504 | |

| China | |||

| Jinko | p-value | 0.491 | 0.599 |

| F-value | 0.488 | 0.284 | |

| NYSE | p-value | 0.654 | 0.980 |

| F-value | 0.205 | 0.001 | |

| Canadian Solar | p-value | 0.132 | 0.171 |

| F-value | 2.415 | 1.979 | |

| NASDAQ | p-value | 0.453 | 0.966 |

| F-value | 0.581 | 0.002 | |

| JA Solar | p-value | 0.150 | 0.659 |

| F-value | 2.196 | 0.199 | |

| Shenzhen | p-value | 0.386 | 0.313 |

| F-value | 0.777 | 1.059 | |

| Based on data collected from the Taiwanese Stock Exchange, yahoo finance number of observations = 27 | |||

| lag = 1 based on ACF | |||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, W.L.; Kryszak, M. Technological Progress and Supply Base under Uncertain Market Conditions: The Case Study of the Taiwanese c-Si Solar Industry 2016–2019. Energies 2020, 13, 5841. https://doi.org/10.3390/en13215841

Wang WL, Kryszak M. Technological Progress and Supply Base under Uncertain Market Conditions: The Case Study of the Taiwanese c-Si Solar Industry 2016–2019. Energies. 2020; 13(21):5841. https://doi.org/10.3390/en13215841

Chicago/Turabian StyleWang, Wang Lai, and Marek Kryszak. 2020. "Technological Progress and Supply Base under Uncertain Market Conditions: The Case Study of the Taiwanese c-Si Solar Industry 2016–2019" Energies 13, no. 21: 5841. https://doi.org/10.3390/en13215841