1. Introduction

An Equilibrium problem (EP) was originally started in the unifying feature by Blum and Oettli [

1] in 1994 and provided a detailed investigation of their theoretical properties. This study contributes significantly to the advancement of applied and pure science. This problem is primarily related to Ky Fan Inequity due to his early contributions to this field [

2]. It has been established that the equilibrium problem theory has set up an unique approach to investigate an immense range of topics that have appeared in social and physical science. For instance, it might involve physical or mechanical structures, chemical processes [

3], the distribution of traffic over computer, and telecommunication networks or public roads [

4,

5,

6,

7]. In economics, it often refers to production competition [

8] or the dynamics of offer and demand [

9], exploiting the mathematical model of non-cooperative games and the analogous equilibrium concept by Nash [

10,

11]. The problem of equilibrium, as a particular case, includes many mathematical problems as a particular case, such as the variational inequality problems (VIP), problems of minimization, the fixed point problems, Nash equilibrium of non-cooperative games, complementarity problems, and saddle point problem (see e.g., [

1,

12]).

On the other hand, iterative methods are efficient techniques for determining the approximate solution of an equilibrium problem. In that case, two major approaches that are well-known i.e., the proximal point method [

13] and auxiliary problem principle [

14]. The proximal point method strategy was initially developed by Martinet [

15] for the monotone variational inequality problems and later Rockafellar [

16] extends this approach for monotone operators. Moudafi [

13] proposed the proximal point method for monotone equilibrium problems. Konnov [

17] also suggests a different interpretation of the proximal point method with weaker assumptions for equilibrium problems.

In addition, inertial-type methods are additionally significant, depending on the heavy-ball methods of the second-order time dynamic system. Polyak began by considering inertial extrapolation as an acceleration procedure to deal with the problem of smooth convex minimization. Inertial-type algorithms are two-step iterative schemes, and the next iteration is determined by using the previous two iterations and it can be viewed as an accelerating step of the iterative sequence. A large number of methods are the earliest, being set up for solving the problem (EP) in finite and infinite-dimensional spaces, such as the proximal point-like methods [

13,

18], the extragradient methods [

19,

20,

21,

22,

23], the subgradient extragradient methods [

24,

25,

26], the inertia methods [

27,

28,

29,

30,

31,

32] and others in [

33,

34].

In this work, our focus is on the proximal point method, in particular projection methods, which are well established and technically easy to implement due to their convenient numerical computation. This manuscript aims to suggest two modifications of the results that appeared in [

21,

35,

36] by applying the inertial scheme that is useful for speeding up the iteration process. The first result includes the two-step inertial Popov’s extragradient method for determining a numerical solution to the pseudomonotone equilibrium problems and the weak convergence of the suggested method is achieved based on the standard assumptions. We also propose an alternative inertial-type method, the second variant of the first method. The second method does not need any information regarding the Lipschitz-type and strongly pseudomonotone constants of a bifunction. A practical explanation for the second method is that it uses a diminishing and non-summable sequence of non-negative real numbers, which are useful in achieving the strong convergence.

This manuscript is arranged, as follows: in

Section 2, we provide some essential definitions and useful results.

Section 3 and

Section 4 include all of our main methods and corresponding convergence results.

Section 5 provides the methods for variational inequality problems.

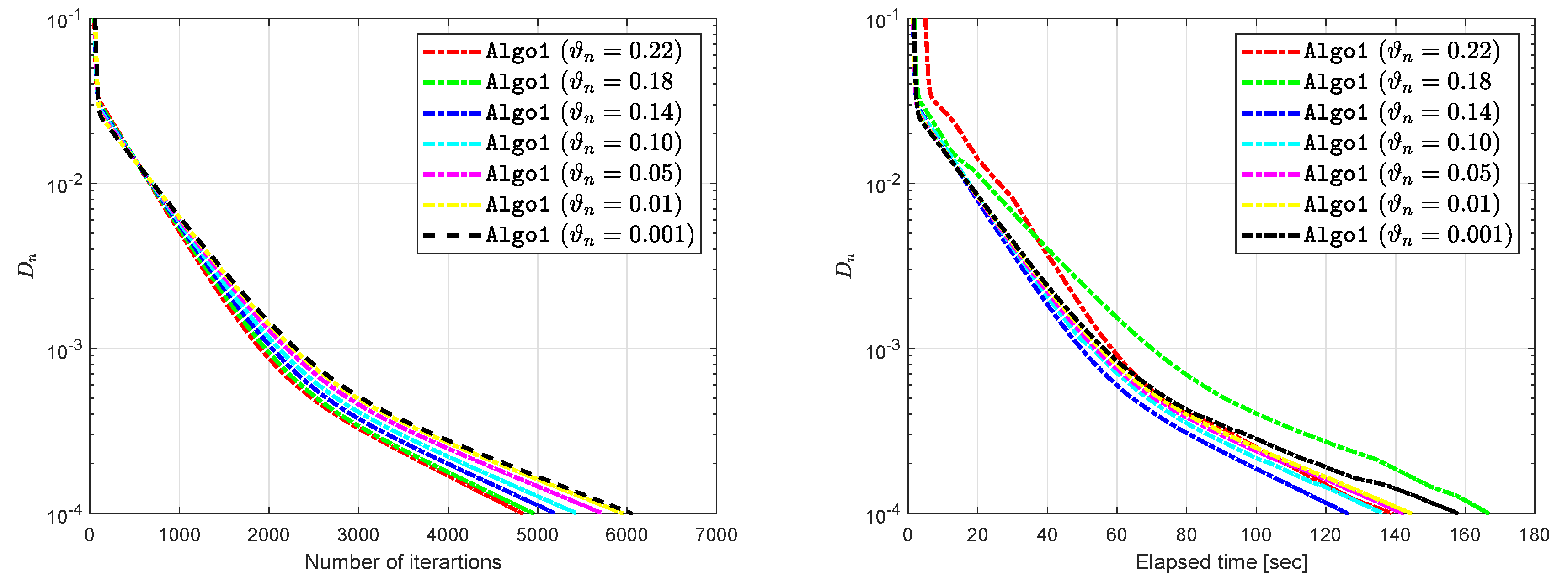

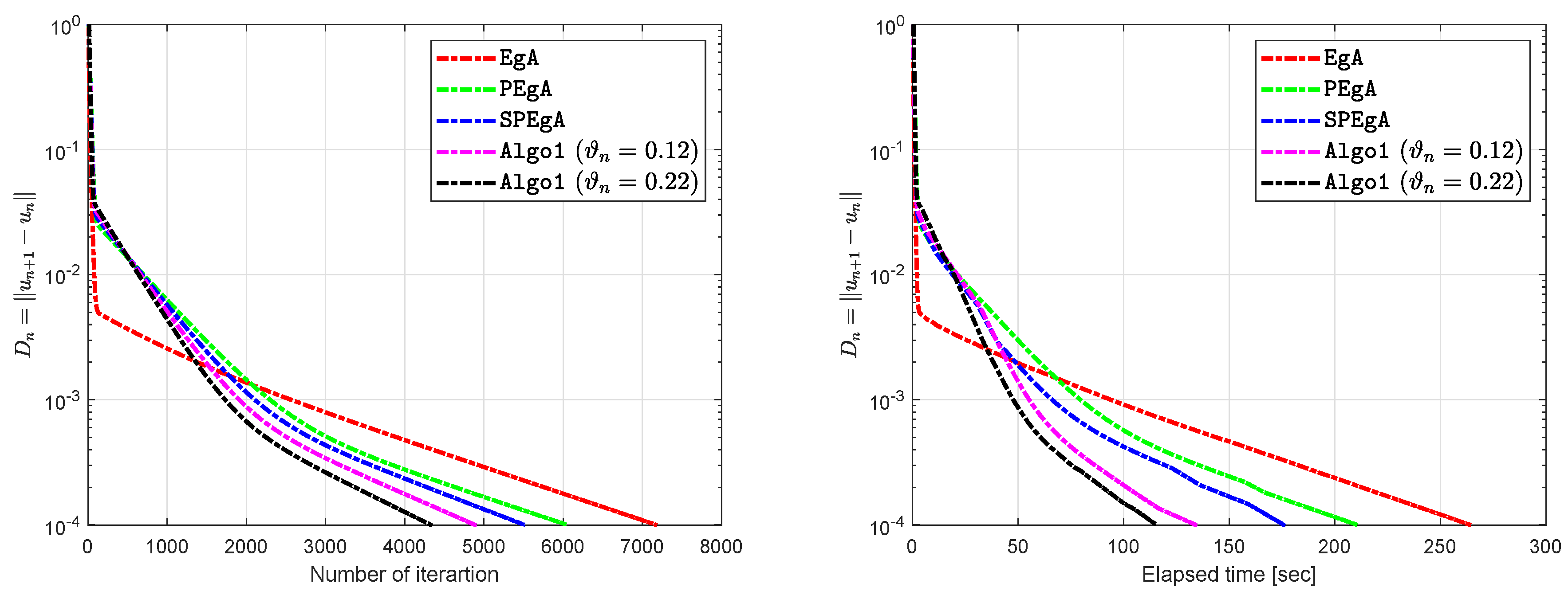

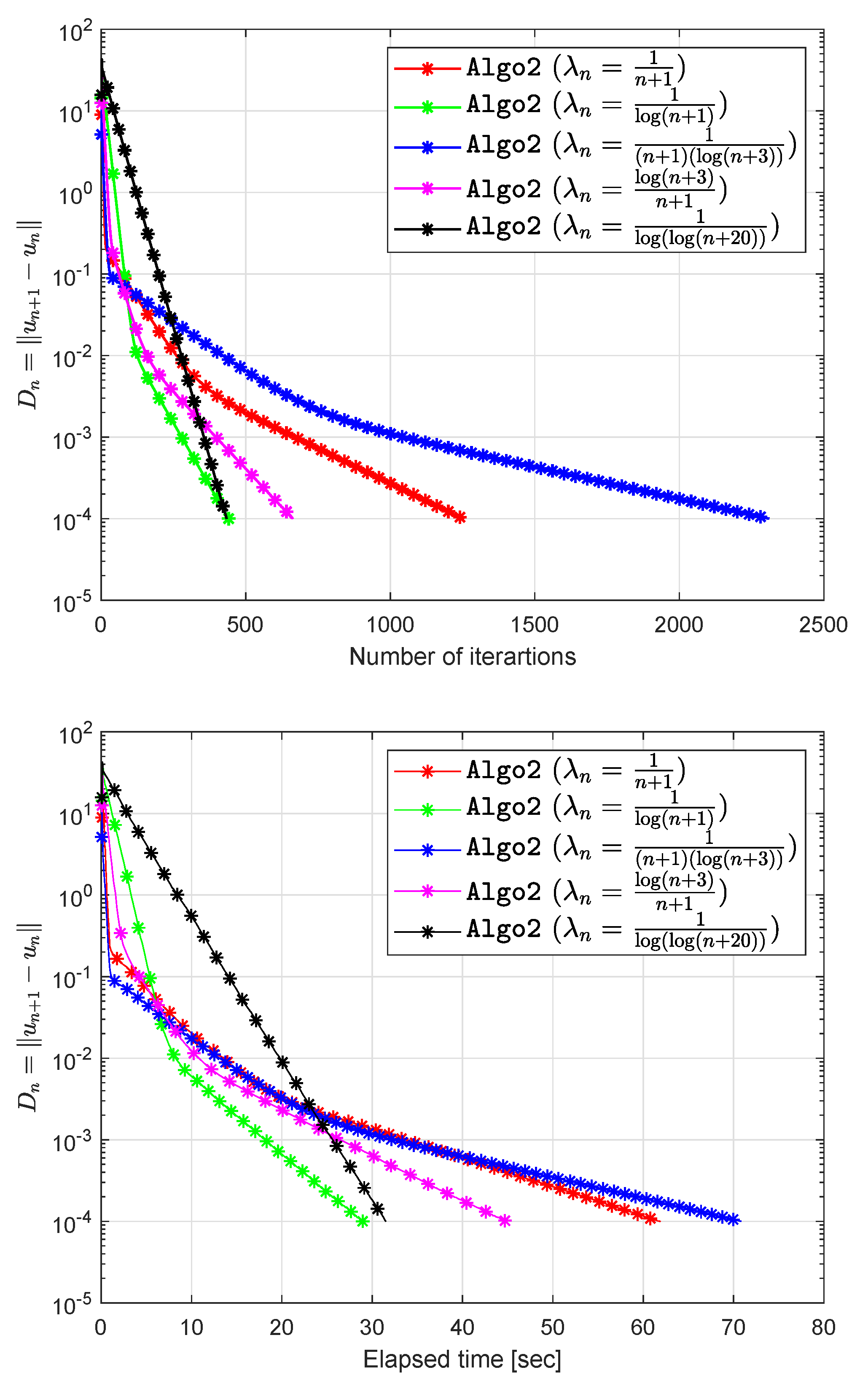

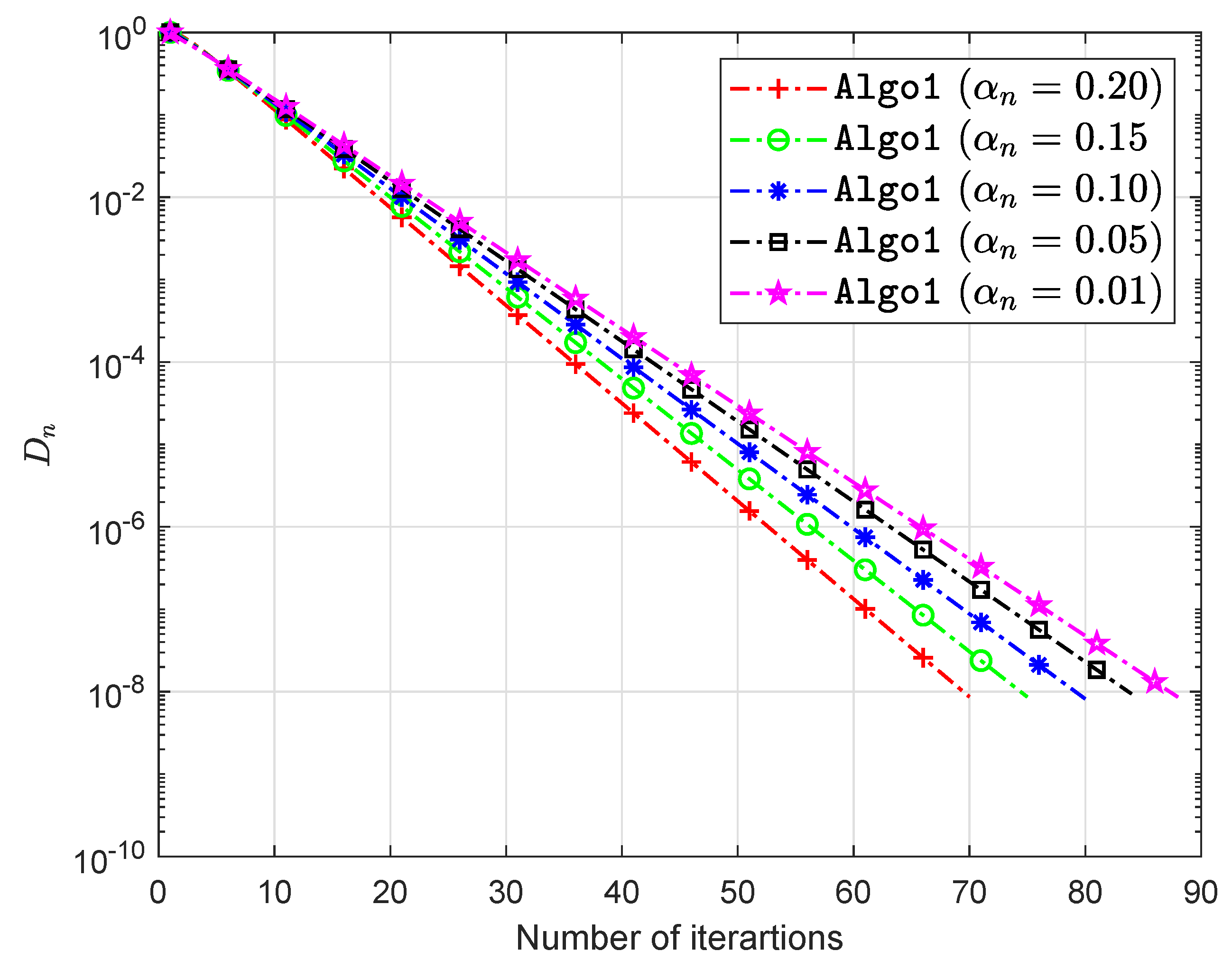

Section 6 sets out the numerical tests to show the numerical efficiency of the proposed methods for the test problems based on the Nash–Cournot equilibrium model compare to other existing methods.

2. Background

Let K be a non-empty, convex, and closed subset of the Hilbert space . Let be an operator and is the solution set of a variational inequality problem relative to the operator H upon the set K. Likewise, denotes the solution set of an equilibrium problem on the set K and is any arbitrary element of the solution set or .

Definition 1. [

1]

Let be a bifunction with , for each . The equilibrium problem for f upon K is defined, as follows: Definition 2. [

37]

The metric projection of on a closed and convex subset K of is determined, as follows: Next, we take the concept of monotonicity of a bifunction into account (see [

1,

38] for details).

Definition 3. Let on K for is

- (1)

- (2)

- (3)

strongly pseudomonotone if - (4)

- (5)

satisfying the Lipschitz-type condition on K if there exist constants such that holds.

This section ends with a few essential lemmas that are useful for examining convergence.

Lemma 1. [

39]

Assume that K is non-empty, convex, and closed subset of Hilbert space and is a convex, subdifferentiable, and lower semi-continuous function on . Furthermore, is a minimizer of g if and only if where and denotes the subdifferential of g at and normal cone of K at , respectively. Lemma 2. [

40]

Let be two sequences and with , then . Lemma 3. [

41]

For and then the following relation is true: Lemma 4. [

42]

Assume that , and are sequences in , such thatand also with , such that for all . Subsequently, the following relations are hold.- (i)

with

- (ii)

Lemma 5. [

43]

Let be a sequence in and such that the following relations are true:- (i)

For each , exists;

- (ii)

Every sequentially weak cluster point of belongs to K;

Subsequently, weakly converges to a point in .

A

normal cone of K at

is defined as:

Let

be a convex function with

subdifferential of g at

is defined as:

3. Inertial Popov’s Two-Step Subgradient Extragradient Algorithm for Pseudomonotone EP

We present our first method to solve the pseudomonotone equilibrium problems involving the Lipschitz-type condition of a bifunction. It uses an inertial term to boost up the iterative sequence, so we referred it as an “Inertial Popov’s Two-step Subgradient Extragradient Algorithm” for a class pseudomonotone equilibrium problems. The detailed algorithm is given below.

| Algorithm 1 (Two-step Subgradient Extragradient Algorithm for Pseudomonotone EP) |

Initialization: Choose , and . Set

where and . Iterative steps: Given , , for and construct a half space

where . Step 1: Compute

where . Step 2: Compute

where . Step 3: If and , then STOP. Otherwise, set and go back to Step 1.

|

Assumption 1. Assume that satisfy the following conditions:

- (A1)

for all and f is pseudomonotone on K;

- (A2)

f satisfy the Lipschitz-type condition on through two positive constants and ;

- (A3)

for all and satisfy ;

- (A4)

is convex and subdifferentiable on for each

Lemma 6. We have the following crucial inequality that results from the Algorithm 1. Proof. By the value

through Lemma 1, we have

For

, there exists

, such that

Because

then

,

It implies that

Due to

and by definition of subdifferentiable, we obtain

From expressions (

1) and (

2), we have the required result. □

Lemma 7. We also have the following inequality from Algorithm 1. Proof. The proof is the same as that of Lemma 6. □

Lemma 8. We have the following inequality from Algorithm 1. Proof. Because

then the definition of

implies that

From

and due to subdifferential definition, we have

Set

in the above expression

From expression (

3) and (

4), we obtain the desired result. □

Now, we are proving the validity of the stopping criterion for Algorithm 1.

Lemma 9. If and in Algorithm 1, then .

Proof. By substituting

in Lemma 6, we have

Because

and

,

, then from Lemma 8, we have

The expression (

5) and (

6) implies that

. □

Remark 1. Two more conditions for stopping criterion are and for Algorithm 1. The validity of these stopping criterion can be shown easily by Lemma 6 and Lemma 7, respectively.

Lemma 10. Let satisfying the Assumption 1. Assume that is nonempty. Afterwards, for each , we have Proof. Substituting

into Lemma 6, we obtain

Since

then

Thus, from (A1) the above expression becomes

Because of the Lipschitz-type condition, we have

The expression (

9) and (

10) implies that

From expression (

11) and Lemma 8, we obtain

We have the following facts:

We also have the following inequality

From the above two facts and last inequality with (

12) provides the required result. □

Now, we are in a position to provide our first convergence result of this work.

Theorem 1. Assume that , and sequences in generated by Algorithm 1, where the sequence is non-decreasing and λ is a positive real number, such that Subsequently, the sequences , and are converges weakly to an element of .

Proof. By the definition of

in Algorithm 1, we have

By the definition of

in Algorithm 1, we also have

Combining the expression (

13)–(

15), we obtain

By substituting

and due to the inequality

From this discussion, the expression (

18) turns into following:

where

By the value

, we have

Combining the expression (

19) and (21) implies that

where

and

Further, we take

It follows from (22) that

The expression (

23) and (

24) with some

, implies that

The above relation (

25) implies that the sequence

is non-increasing. From

, we have

Additionally, from definition

, we have

Combining the expression (

26) and (

27), we obtain

It continues to follow from (

25) and (

28), such that

letting

in (

29) implies that

From the relation (20) and (30), we obtain

Next, the expression (

28) implies that

From the relation (18) we have

Set

and using (

33) for

, gives that

letting

in (

34) implies that

and

The following relation can easily be derived:

By the definition of

and using Cauchy inequality, we have

Now, summing up the expression (38) for

, we obtain

The above expression with (

30) and (

35) implies that

It follows from the relation (

16), we obtain

above expression with (30), (40), (37) and Lemma 4 implies that limit of

and

exists for every

, means that the sequences

,

and

are bounded. Next, we need to show that each weak sequential limit point of the sequence

belongs to

. Let

z be arbitrary weak cluster point of the sequence

, and then there exists a weak convergent subsequence

of

converges to

, this also implies that

also converge weakly to

Now our aim to prove that

By Lemma 6, the bifunction Lipschitz-type condition and Lemma 8, we have

where

y be an any element in

As a result with (31), (36), (37), and due to the boundedness of the sequence

the above inequality tends to zero. By given

, the assumption (A3) and

, we obtain

Due to , we obtain This implies that z belongs to Thus Lemma 5, ensures that , and weakly converges to as

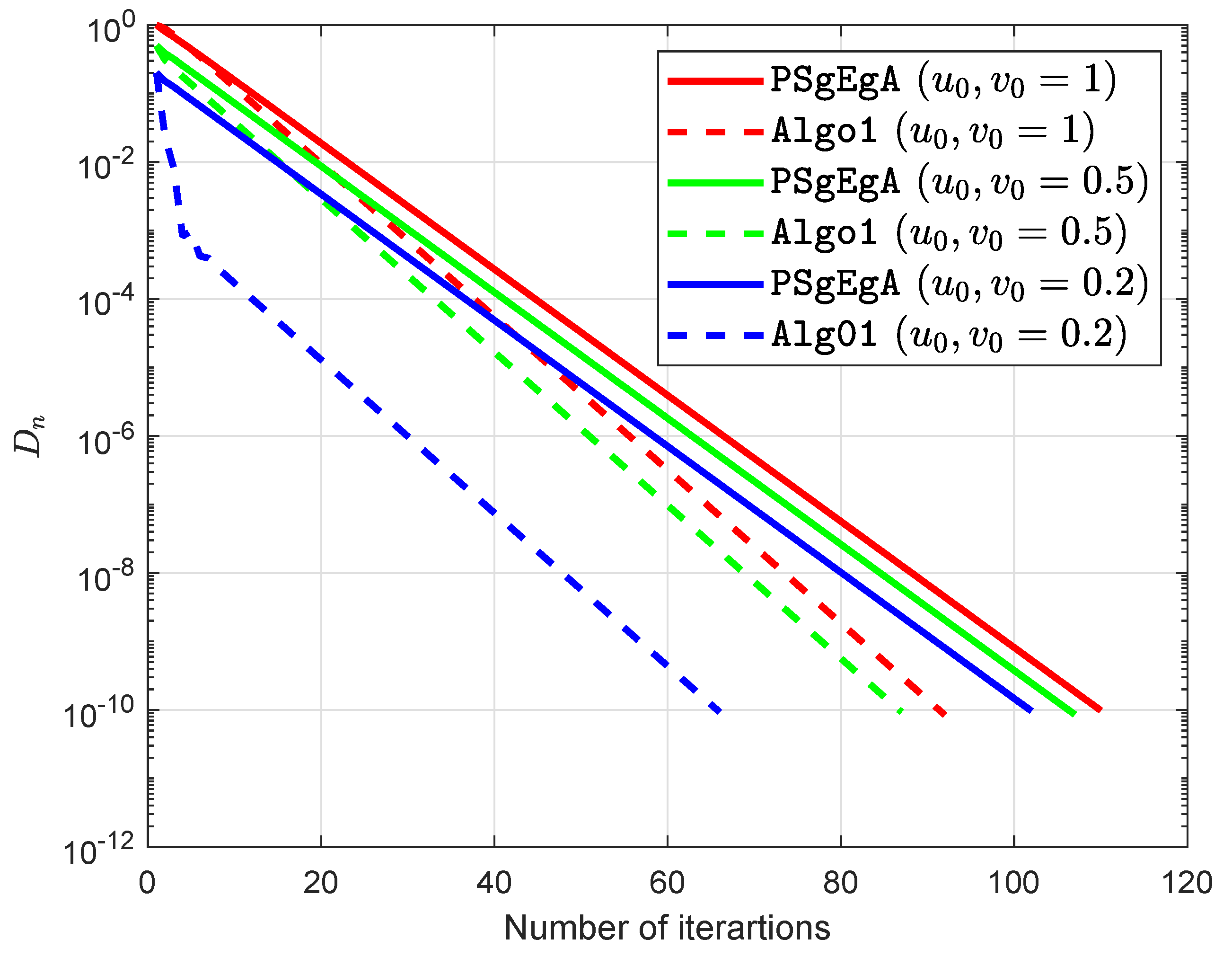

Remark 2. For in Algorithm 1 gives the results as in [35,36]. 4. Inertial Popov’s Two-Step Subgradient Extragradient Algorithm for Strongly Pseudomonotone EP

The second algorithm is also an inertial algorithm that is able to solve the strongly pseudomonotone equilibrium problem. However, the advantage of this algorithm is that there is no need for prior information regarding the strongly pseudomonotone constant

and Lipschitz constants

. Let

be a non-increasing sequence, so that the following conditions are satisfied:

Assumption 2. Let a bifunction satisfies the following conditions:

- (B1)

and f is strongly pseudomontone on K;

- (B2)

f meet the Lipschitz-type condition on with two positive constants and ;

- (B3)

is sub-differentiable and convex on for all

Lemma 11. Assume that satisfies the conditions (B1)–(B3)

. Let the solution set is nonempty. For each , we have Now, we are in a position to provide our second convergence result of this work.

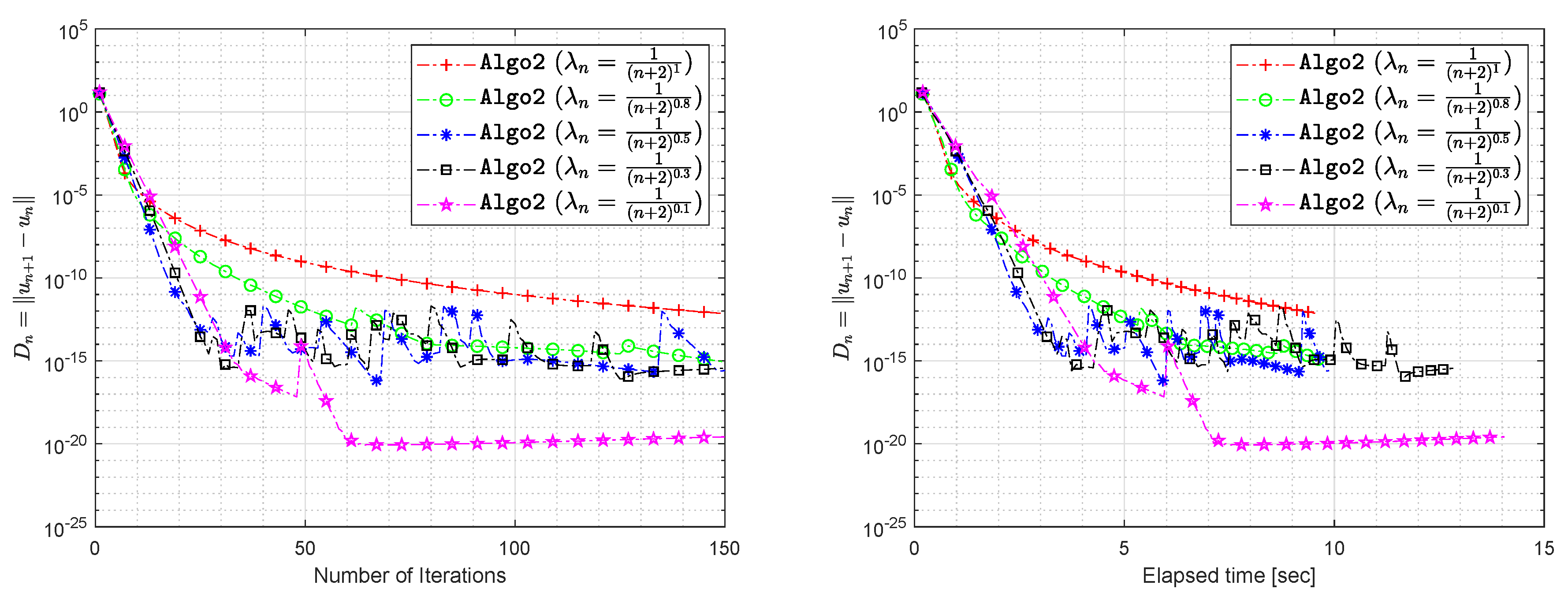

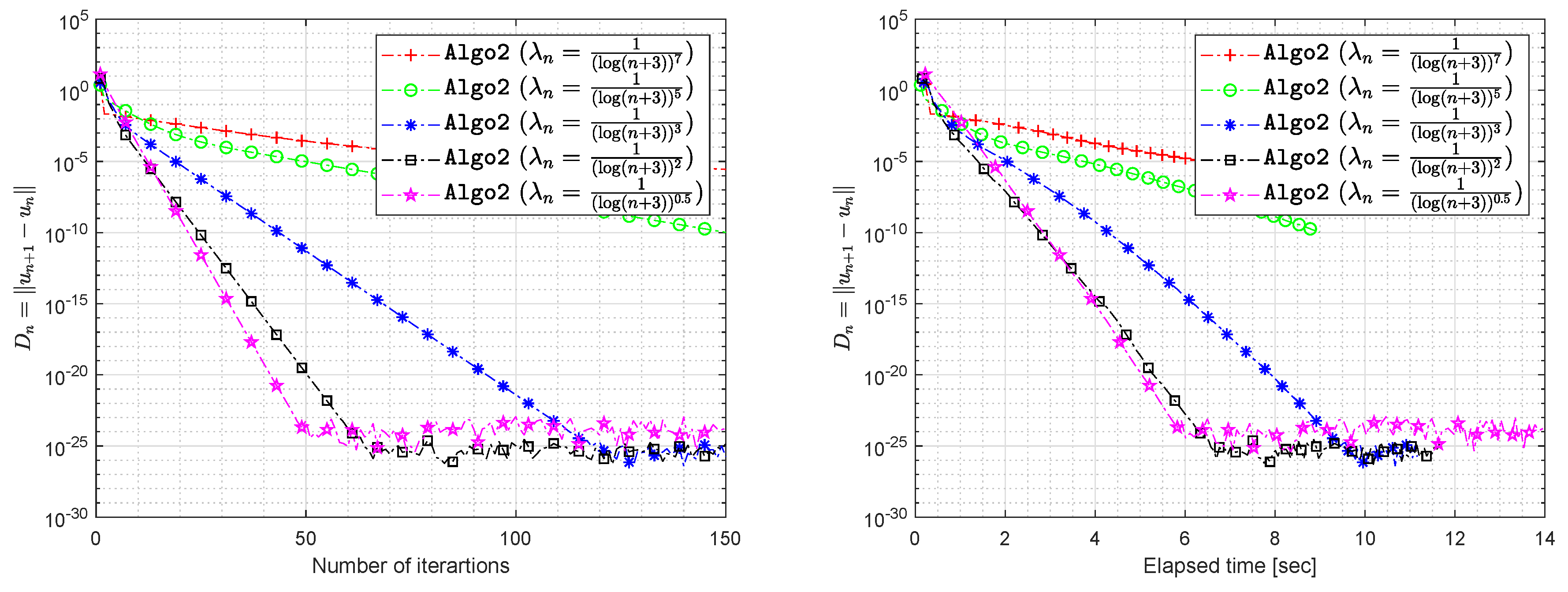

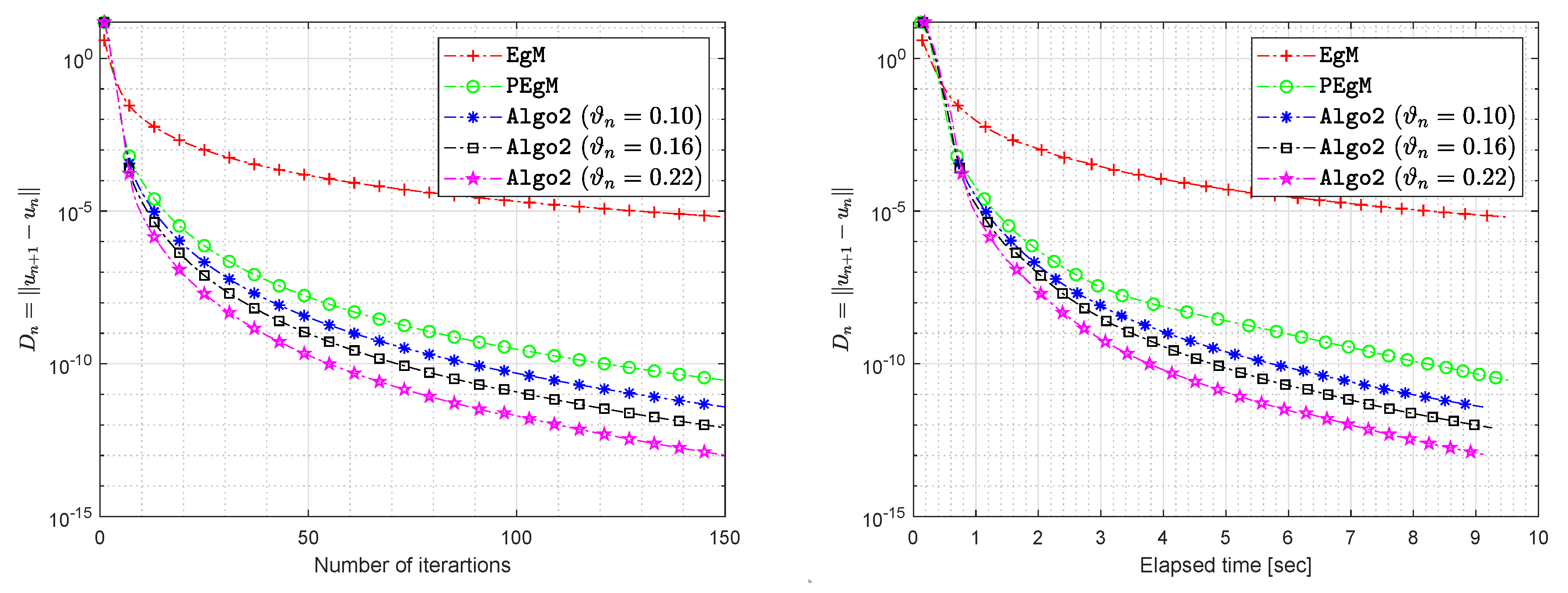

Theorem 2. Assume that satisfies the conditions (B1)–(B3). Let , and are sequences in generated by Algorithm 2 and is non-decreasing sequence with . Subsequently, , and strongly converge to an element in .

| Algorithm 2 (Two-step Subgradient Extragradient Algorithm for Strongly Pseudomonotone EP) |

Initialization: Choose , and a sequence satisfying (43). Set

where and . Iterative steps: Assume that , , and are known for and

where . Step 1: Compute

where . Step 2: Compute

where . Step 3: If and , then STOP. Otherwise set and go to Step 1.

|

Proof. The proof is the identical as the proof of Theorem 1, but there are still few changes. We provide the proof for the readable purpose. By Lemma 11 and adding

in both sides, we have

By using the definition of

in Algorithm 2, we have

By using the definition

in Algorithm 2, we also have

Combining the expression (

44)–(

46), we obtain

Next, we let

and

Due to the above substituting the expression (48) turns into the following:

By the definition

, we have

Combining the expression (49) and (

50), we obtain

where

and

In addition, we also take

It follows from (

51) that

Since

, then there exists a finite number

such that

Similarly, it follows from (

24) and expression (

52) implies that

The above implies that the sequence

is non-increasing for

From the value of

, we have

From the definition of

with the expression (

54), we obtain

It is follows from (

53) and (

55) that

letting

in the expression (

56), we obtain

From the expression (20) and (

57), we obtain

The expression (

55) implies that

It follows from (48) for all

, such that

Consider the expression (

60) for

Summing them up, we obtain

By letting

in the expression (

61) implies that

and

We can easily derive the following relationship:

By using the value

, we obtain

Now, summing up equation (

65) for

, we obtain

The above expression with (

57) and (

62) implies that

Furthermore, the expression (

47) gives that

The above expression through (

57), (

67), and Lemma 4 implies that

The expression (

64) with (

69), we obtain

Now, we are showing that the sequence

converges strongly to

Due to the condition on

for all

, we can easily observe the following inequality:

It follows from Lemma 11, such that

From the expression (45) and (71), we obtain

It follows from expression (

72) that

for

It implies that

By the Lemma 2 and (74) implies that

Finally, expression (69) and (75) provide that This completes the proof. □

5. Application to Variational Inequality Problems

For considering Algorithm 1 and Theorem 1, we can able to write the next result for solving variational inequality problems that involve pseudomonotone and Lipschitz continuous operator.

Corollary 1. Assume that be a Lipschitz continuous with the constant L and pseudomonotone operator. Let , and be sequences generated, as follows:

- (i)

Choose , and Compute - (ii)

Given , and for each and construct the half-space first as - (iii)

where , such thatwith . Subsequently, sequence , and converge weakly to . From the consideration on Algorithm 2 and Theorem 2, we state the following result for the class of variational inequality problems involving strongly pseudomonotone and Lipschitz continuous operator.

Corollary 2. Assume that is a Lipschitz continuous and strongly pseudomonotone operator with the constant . Let , and are the sequences generated as follows:

- (i)

Choose , and a sequence satisfying (43). Compute - (ii)

Given , and create a half space for each such that - (iii)

where , with . The sequence , and converge strongly to .

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}