The Relationship of Fiscal Policy and Economic Cycle: Is Vietnam Different?

Abstract

:1. Introduction

2. Literature Review

2.1. Theories of Fiscal Policy and Economic Cycle

2.2. Relevant Empirical Studies of Pro-Cyclical Fiscal Policy

2.3. Relevant Empirical Studies of Counter-Cyclical Fiscal Policy

2.4. Theoretical Frameworks and Research Gaps on Economic Cycle and Fiscal Policy

3. Methodology and Data

3.1. Methodology

3.2. Data and Model Specifications

4. Results and Discussion

4.1. Stationary Test for Data Series

4.2. Co-Intergration Test

4.3. Granger Causality Test

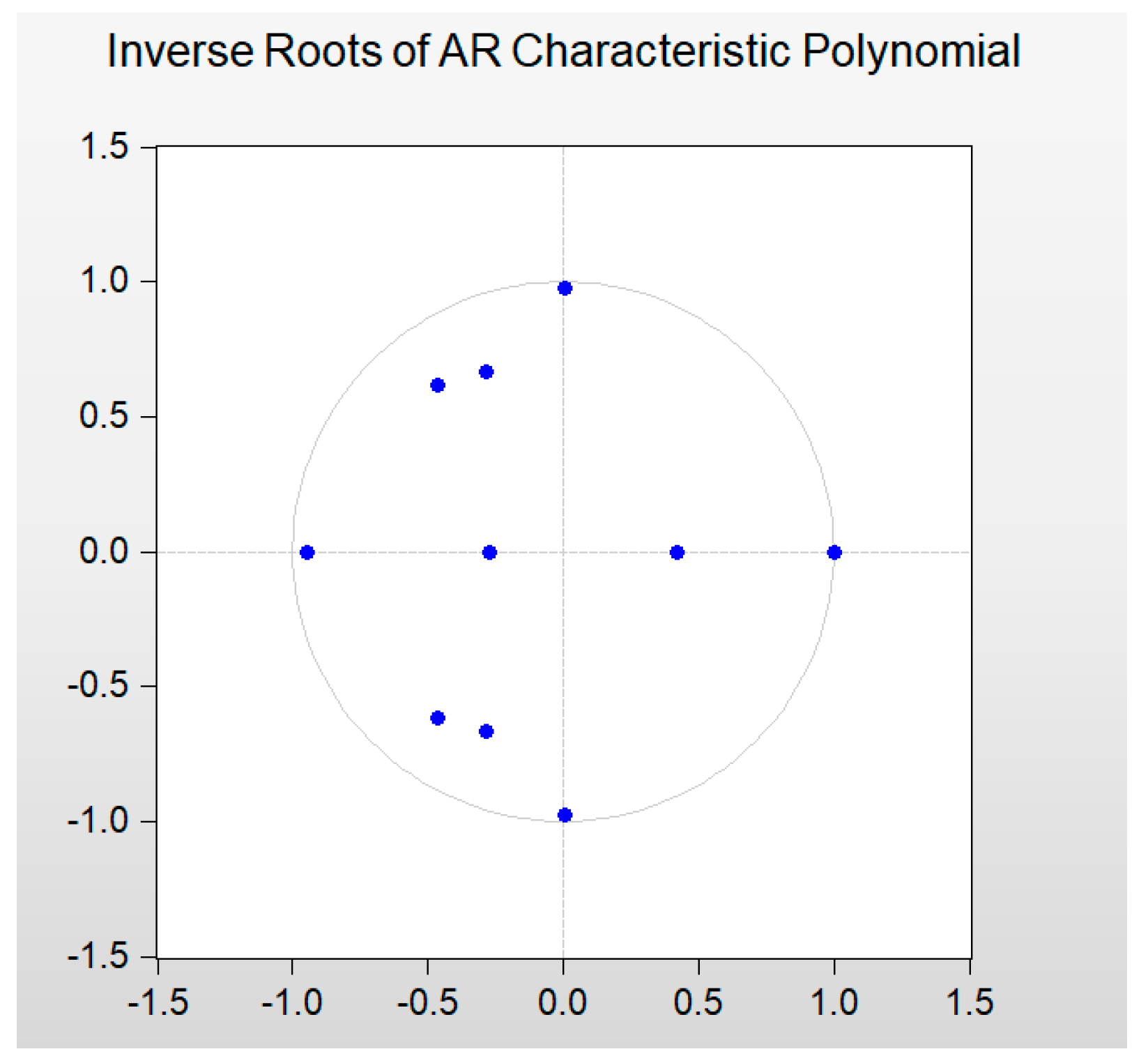

4.4. Stability Test in the Research Model

4.5. The VECM Model

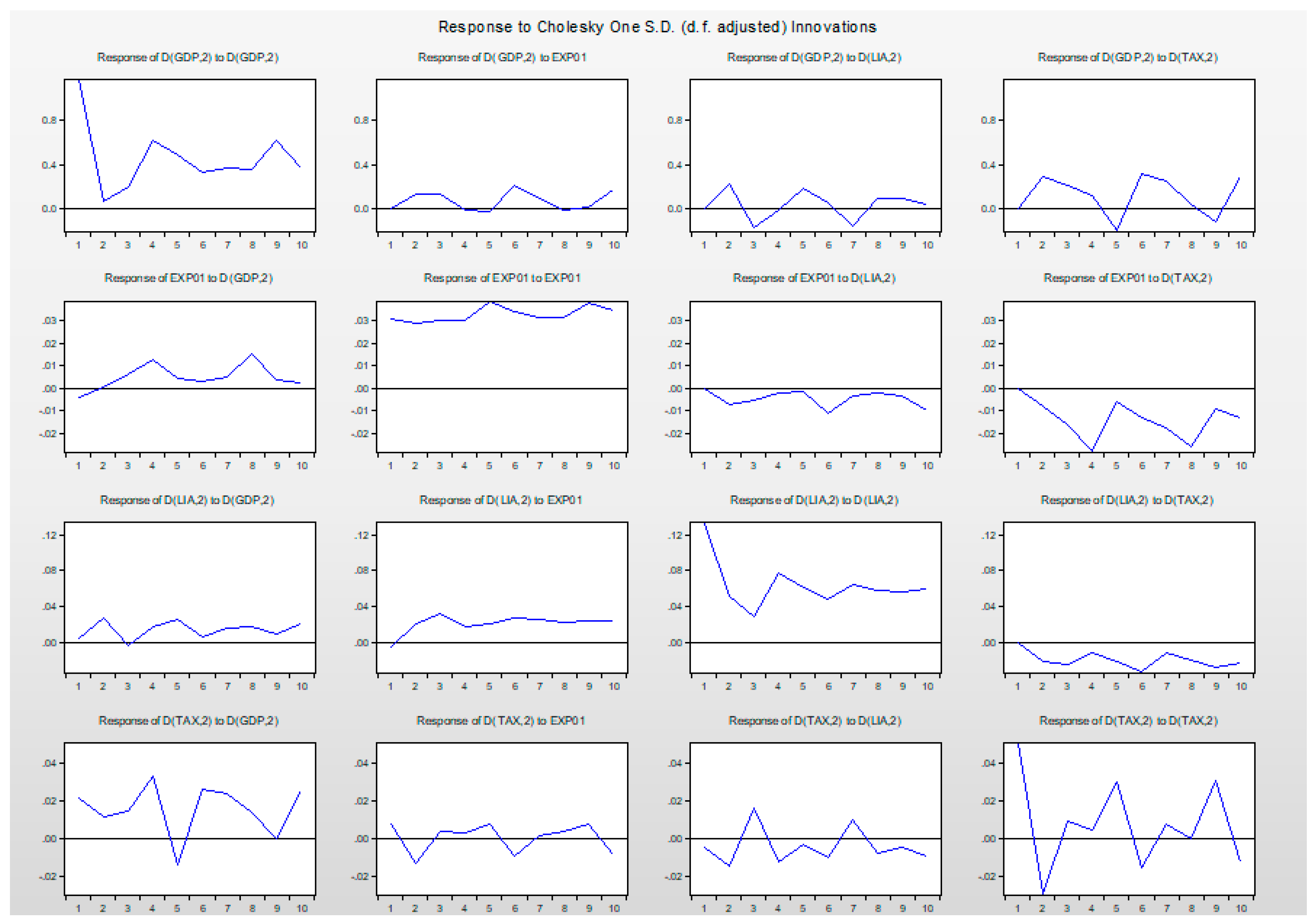

4.6. Impulse Response Function

4.7. The Variance Decomposition

4.8. Discussion

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A. Results of the Johansen Cointegration Test

References

- Acemoglu, Daron, Suresh Naidu, Pascual Restrepo, and James A. Robinson. 2013. Democracy Does Cause Growth. Journal of Political Economy 127: 47–100. [Google Scholar] [CrossRef]

- Afonso, António, and João Tovar Jalles. 2013. The Cyclicality of Education, Health, and Social Security Government Spending. Applied Economics Letters 20: 669–72. [Google Scholar] [CrossRef]

- Aghion, Philippe, David Hemous, and Enisse Kharroubi. 2014. Credit constraints, cyclical fiscal policy and industry growth. Journal of Monetary Economics 62: 41–58. [Google Scholar] [CrossRef]

- Alberola, Enrique, José Manuel Montero, Miguel Braun, and Tito Cordell. 2006. Debt Sustainability and Procyclical Fiscal Policies in Latin America. Economia 7: 157–93. [Google Scholar] [CrossRef]

- Alesina, Alberto, Guido Tabellini, and Filipe R. Campante. 2008. Why is Fiscal Policy Often Procyclical? Journal of the European Economic Association 6: 1006–36. [Google Scholar] [CrossRef]

- Barro, Robert J. 1979. On the Determination of Public Debt. Journal of Political Economy 87: 940–71. [Google Scholar] [CrossRef]

- Bazzaoui, Lamia, and Jun Nagayasu. 2021. Is Inflation Fiscally Determined? Sustainability 13: 11306. [Google Scholar] [CrossRef]

- Blanchard, Olivier, Jean-Claude Chouraqui, Robert P. Hagemann, and Nicola Sartor. 1990. The Sustainability of Fiscal Policy: New Answers to an Old Question. OECD Journal: Economic Studies 15: 7–36. [Google Scholar]

- Caballero, Ricardo J., and Arvind Krishnamurthy. 2004. Fiscal Policy and Financial Depth. NBER Working Paper 10532. Cambridge: MIT Press. [Google Scholar]

- Calderón, César, and Klaus Schmidt-Hebbel. 2008. Business Cycles and Fiscal Policies: The Role of Institutions and Financial Markets. Working Paper No. 481. San Diego: Central Bank of Chile. [Google Scholar]

- Calderón, César, Roberto Duncan, and Klaus Schmidt-Hebbel. 2010. Institutions and Cyclical Proper-Ties of Macroeconomic Policies in the Global Economy. Documentos de Trabajo 372. Santiago: Instituto de Economía PUC, p. 1. [Google Scholar]

- Calderón, César, Roberto Duncan, and Klaus Schmidt-Hebbel. 2016. Do good institutions promote countercyclical macroeconomic policies? Oxford Bulletin of Economics and Statistics 78: 650–70. [Google Scholar] [CrossRef]

- Chakraborty, Lekha, Amandeep Kaur, Divy Rangan, and Jannet Farida Jacob. 2021. COVID-19 and Economic Stimulus Packages: Evidence from the Asia-Pacific Region. New Delhi: National Institute of Public Finance and Policy. Available online: https://www.nipfp.org.in/media/medialibrary/2023/03/Covid19EconomicStimulus.pdf (accessed on 14 May 2023).

- Debrun, Xavier, and Radhicka Kapoor. 2011. Fiscal Policy and Macroeconomic Stability: New Evidence and Policy Implications. Nordic Economic Policy Review 1: 35–70. [Google Scholar] [CrossRef]

- Debrun, Xavier, Jean Pisani-Ferry, and André Sapir. 2008. Government Size and Output Volatility: Should We Forsake Automatic Stabilization? Economic Papers 316. Brussels: European Economy, European Commission. [Google Scholar]

- Easterly, William. 2001. The Elusive Quest for Growth. Cambridge: MIT Press. [Google Scholar]

- Fatas, Antonio, and Ilian Mihov. 2013. Policy Volatility, Institutions, and Economic Growth. Review of Economics and Statistics 95: 362–76. [Google Scholar] [CrossRef]

- Frankel, Jeffrey A., Carlos A. Vegh, and Guillermo Vuletin. 2011. On Graduation from Fiscal Procyclicality. NBER Working Paper No. 17619. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Furceri, Davide, and J. Tovar Jalles. 2016. Determinants and effects of fiscal stabilization: New evidence from time-varying estimates. IMF WP forthcoming. Available online: https://www.ecb.europa.eu/pub/conferences/shared/pdf/20161110_fiscal_policy/paper_4.pdf (accessed on 20 May 2023).

- Gavin, Michael, and Roberto Perotti. 1997. Fiscal Policy in Latin America. In NBER Macroeconomics Annual 1997. Cambridge: MIT Press, vol. 12, pp. 11–72. [Google Scholar]

- Ghosh, Atish R., Jun I. Kim, Enrique G. Mendoza, Jonathan D. Ostry, and Mahvash S. Qureshi. 2013. Fiscal Fatigue, Fiscal Space and Debt Sustainability in Advanced Economies. Economic Policy 28: 365–406. [Google Scholar]

- Granger, Clive W. J., and Paul Newbold. 1987. Spurious regressions in econometrics. Journal of Econometrics 2: 111–20. [Google Scholar] [CrossRef]

- Ilzetski, Ethan, and Carlos A. Végh. 2008. Procyclical Fiscal Policy in Developing Countries: Truth or Fiction? NBER Working Paper 14191. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Johansen, Soren. 1990. Testing for Cointegration Using the Johansen Methodology When Variables are Near-Integrated. Journal of IMF Working paper W07/1041. Washington, DC: International Monetary Fund. [Google Scholar]

- Kaminsky, Graciela L., and Carmen M. Reinhart. 1999. The twin crises: The causes of banking and balance-of-payments problems. The American Economic Review 89: 473–500. [Google Scholar] [CrossRef]

- Kaminsky, Graciela L., Carmen M. Reinhart, and Carlos A. Végh. 2004. When It Rains, It Pours: Procyclical Capital Flows and Macroeconomic Policies. In NBER Macroeconomics Annual. Cambridge: MIT Press, vol. 19, pp. 11–53. [Google Scholar]

- Keynes, John Maynard. 1936. The General Theory of Employment, Interest and Money. New York, Macmillan and Cambridge: Cambridge University Press. [Google Scholar]

- Lane, Philip R. 2003. The Cyclical Behaviour of Fiscal Policy: Evidence from the OECD. Journal of Public Economics 87: 2661–75. [Google Scholar] [CrossRef]

- Le, Mai Trang, and Thi Tue Pham. 2018. Fiscal Policy Status with Vietnam’s Economic Growth. Vietnam Trade and Industry Review 4: 124–28. Available online: https://tapchicongthuong.vn/bai-viet/thuc-trang-chinh-sach-tai-khoa-voi-tang-truong-kinh-te-viet-nam-28998.htm (accessed on 20 May 2023).

- Lewis, John. 2009. Fiscal policy in Central and Eastern Europe with real time data: Cyclicality, inertia and the role of EU accession. Applied Economics 45: 3347–59. [Google Scholar] [CrossRef]

- Manasse, Paolo. 2006. Procyclical Fiscal Policy: Shocks, Rules, and Institutions: A View From Mars. IMF Working Paper 06/27. Washington, DC: International Monetary Fund. [Google Scholar]

- Nguyen, H. T. P., and T. T. T. Nguyen. 2021. The response of fiscal policy to COVID-19 in Vietnam: An analysis of the general government budget. Journal of Asian Public Policy 14: 96–111. [Google Scholar]

- Pham, Duy Linh. 2016. Financial Policy and Economic Cycle In The Economy. Vietnam Finance Journal 634: 57–59. Available online: https://vjol.info.vn/index.php/TC/article/view/24816/21237 (accessed on 20 May 2023).

- Riascos, Álvaro, and Carlos A. Végh. 2004. Procyclical Fiscal Policy in Developing Countries: The Role of Capital Market Imperfections. Los Angeles: University of California at Los Angeles. [Google Scholar]

- Sims, Christopher A. 1980. Macroeconomics and Reality. Econometrica 48: 1–48. [Google Scholar] [CrossRef]

- Stein, Ernesto H., Ernesto Talvi, and Alejandro Grisanti. 1999. Institutional Arrangements and Fiscal Performance: The Latin American Experience. NBER Working Paper No. 6358. Chicago: University of Chicago Press. [Google Scholar]

- Stoian, Andreea, Laura Obreja Brașoveanu, Iulian Viorel Brașoveanu, and Bogdan Dumitrescu. 2018. A Framework to Assess Fiscal Vulnerability: Empirical Evidence for European Union Countries. Sustainability 10: 2482. [Google Scholar] [CrossRef]

- Strawczynski, Michel, and Joseph Zeira. 2011. Procyclicality of Fiscal Policy in Emerging Countries: The Cycle is the Trend. Working Paper 624. San Diego: Central Bank of Chile. [Google Scholar]

- Suzuki, Yui. 2015. Sovereign risk and procyclical fiscal policy in emerging market economies. The Journal of International Trade & Economic Development 24: 247–80. [Google Scholar]

- Talvi, Ernesto, and Carlos A. Vegh. 2005. Tax base variability and procyclical fiscal policy in developing countries. Journal of Development Economics 78: 156–90. [Google Scholar] [CrossRef]

- Temsumrit, Navarat. 2020. Does Democracy Affect Cyclical Fiscal Policy? Evidence From Developing Countries. Bangkok: Puey Ungphakorn Institute for Economic Research, p. 125. [Google Scholar]

- Thornton, John. 2008. Explaining Procyclical Fiscal Policy in African Countries. Journal of African Economies 17: 451–64. [Google Scholar] [CrossRef]

- Tornell, Aaron, and Philip R. Lane. 1999. The voracity effect. American Economic Review 1: 22–46. [Google Scholar] [CrossRef]

- Woo, Jaejong. 2009. Why Do More Polarized Countries Run More Procyclical Fiscal Policy? The Review of Economics and Statistics 91: 850–70. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Variables | Symbol | Ratios | Source |

|---|---|---|---|

| Vietnam production | GDP | GDP index (%) | IMF |

| Government expenditures | LNEXP | EXP index 1 | IMF |

| Government tax revenues | LNTAX | TAX index 1 | IMF |

| Government debts | LNLIA | LIA index 1 | IMF |

| Values | EXP | GDP | LIA |

|---|---|---|---|

| Mean | 32.48437 | 6.536612 | 16.45983 |

| Median | 32.61859 | 6.730000 | 16.86875 |

| Maximum | 33.77033 | 9.261000 | 17.01868 |

| Minimum | 30.84740 | 0.390000 | 15.67639 |

| Std. Dev. | 0.933886 | 1.447579 | 0.519136 |

| Skewness | −0.347415 | −1.114815 | −0.244880 |

| Kurtosis | 1.696106 | 6.125947 | 1.176560 |

| Jarque-Bera | 7.731208 | 52.21407 | 12.62533 |

| Probability | 0.020950 | 0.000000 | 0.001813 |

| Sum | 2761.171 | 555.6120 | 1399.085 |

| Sum Sq. Dev. | 73.26002 | 176.0208 | 22.63819 |

| Observations | 85 | 85 | 85 |

| Augmented Dickey-Fuller Test Statistic | Prob. * |

|---|---|

| Null Hypothesis: LIA has a unit root | 0.5113 |

| Null Hypothesis: EXP has a unit root | 0.1692 |

| Null Hypothesis: TAX has a unit root | 0.1145 |

| Null Hypothesis: GDP has a unit root | 0.0529 |

| Augmented Dickey-Fuller Test Statistic | Prob. * |

|---|---|

| Null Hypothesis: LIA has a unit root | 0.0000 |

| Null Hypothesis: EXP has a unit root | 0.0000 |

| Null Hypothesis: TAX has a unit root | 0.0000 |

| Null Hypothesis: GDP has a unit root | 0.0000 |

| No. of CE(s) | Eigenvalue | Statistic | Critical Value | Prob. ** |

|---|---|---|---|---|

| None * | 0.257683 | 52.00129 | 47.85613 | 0.0194 |

| At most 1 | 0.166278 | 27.56697 | 29.79707 | 0.0885 |

| At most 2 | 0.096903 | 12.65486 | 15.49471 | 0.1281 |

| At most 3 * | 0.051053 | 4.296971 | 3.841466 | 0.0382 |

| Null Hypothesis: | Obs | F-Statistic | Prob. |

|---|---|---|---|

| GDP does not Granger Cause EXP EXP does not Granger Cause GDP | 83 | 2.73114 | 0.0714 |

| 3.31170 | 0.0416 | ||

| LIA does not Granger Cause EXP EXP does not Granger Cause LIA | 83 | 0.00231 | 0.9977 |

| 2.62721 | 0.0787 | ||

| TAX does not Granger Cause EXP EXP does not Granger Cause TAX | 83 | 2.00308 | 0.1418 |

| 0.50411 | 0.6060 | ||

| LIA does not Granger Cause GDP GDP does not Granger Cause LIA | 83 | 2.59160 | 0.0813 |

| 4.15017 | 0.0194 | ||

| TAX does not Granger Cause GDP GDP does not Granger Cause TAX | 83 | 4.09654 | 0.0203 |

| 3.44239 | 0.0369 | ||

| TAX does not Granger Cause LIA LIA does not Granger Cause TAX | 83 | 2.18552 | 0.1193 |

| 0.41915 | 0.6591 |

| Cointegrating Eq: | CointEq1 |

|---|---|

| D(GDP(−1),2) | 1.000000 |

| EXP01(−1) | −0.095912 |

| (0.05522) | |

| [−1.73677] | |

| D(LIA(−1),2) | 1.881209 |

| (0.99337) | |

| [−1.89376] | |

| D(TAX(−1),2) | 26.02291 |

| (2.08690) | |

| [−12.4697] | |

| C | 3.100242 |

| CointEq1 | −0.910403 |

| Period | S.E. | D(GDP,2) | D(EXP,2) | D(LIA,2) | D(TAX,2) |

|---|---|---|---|---|---|

| 1 | 1.168062 | 100.0000 | 0.000000 | 0.000000 | 0.000000 |

| 2 | 1.234664 | 89.86475 | 1.219998 | 3.437062 | 5.478193 |

| 3 | 1.285326 | 85.33336 | 2.133990 | 4.851632 | 7.681021 |

| 4 | 1.435247 | 87.50381 | 1.713810 | 3.900553 | 6.881831 |

| 5 | 1.540345 | 86.19089 | 1.503984 | 4.824023 | 7.481100 |

| 6 | 1.623455 | 81.89801 | 2.980262 | 4.469710 | 10.65202 |

| 7 | 1.692766 | 79.96287 | 3.068010 | 4.954812 | 12.01431 |

| 8 | 1.733458 | 80.53291 | 2.931953 | 5.006654 | 11.52849 |

| 9 | 1.846891 | 82.19460 | 2.592329 | 4.681548 | 10.53152 |

| 10 | 1.913499 | 80.25710 | 3.276754 | 4.415854 | 12.05029 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nguyen, D.X.; Nguyen, T.D. The Relationship of Fiscal Policy and Economic Cycle: Is Vietnam Different? J. Risk Financial Manag. 2023, 16, 281. https://doi.org/10.3390/jrfm16050281

Nguyen DX, Nguyen TD. The Relationship of Fiscal Policy and Economic Cycle: Is Vietnam Different? Journal of Risk and Financial Management. 2023; 16(5):281. https://doi.org/10.3390/jrfm16050281

Chicago/Turabian StyleNguyen, Dung Xuan, and Trung Duc Nguyen. 2023. "The Relationship of Fiscal Policy and Economic Cycle: Is Vietnam Different?" Journal of Risk and Financial Management 16, no. 5: 281. https://doi.org/10.3390/jrfm16050281