Systematic Contagion Effects of the Global Finance Crisis: Evidence from the World’s Largest Advanced and Emerging Equity Markets

Abstract

:1. Introduction

2. Literature Review

2.1. Definition of Financial Contagion

2.2. Crisis Transmission Mechanisms and Contagion Effects

3. The Modeling Framework

3.1. Motivation

3.2. The Conditional Factor Model

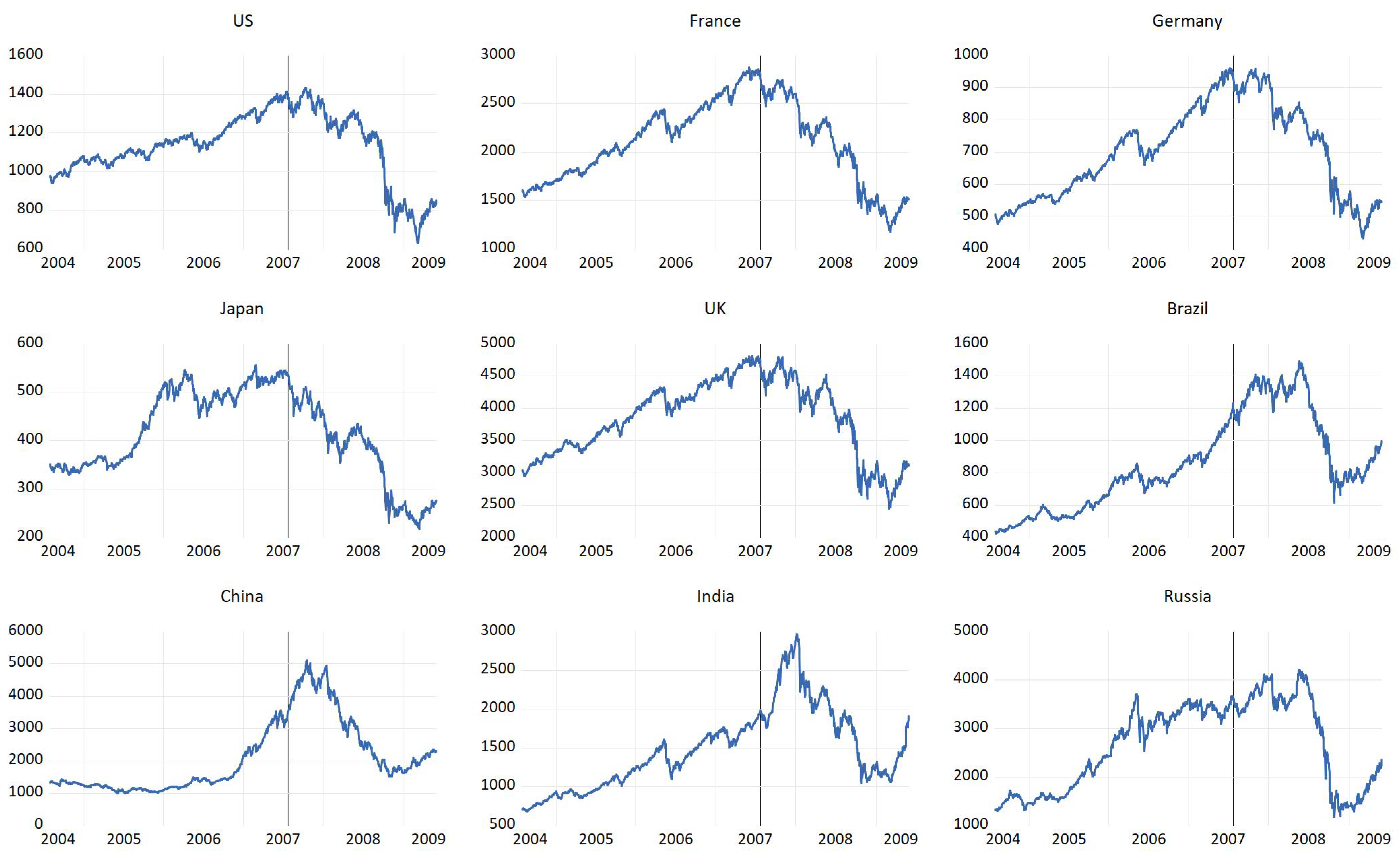

3.3. Sample and Data

Augmented Dickey–Fuller (ADF) Test

3.4. Tests of Contagion

3.4.1. Unadjusted or Naive Correlation Test

3.4.2. Adjusted Correlation Test of Forbes and Rigobon (2002)

3.4.3. Adjusted Beta Test of Dungey et al. (2005)

3.4.4. Conditional Factor Model-Based Test of Dungey and Renault (2018)

3.5. Testing Hypotheses about Model Identification and Structural Stability

3.5.1. Hansen’s J-Test

3.5.2. Ghysels–Hall Test

4. Results and Discussions

4.1. Stylized Facts and Summary Statistics

4.2. Results from the Tests of Contagion

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

| 1 | See Billio and Pelizzon (2003), Corsetti et al. (2005), and Dungey et al. (2005) for limitations of the Forbes and Rigobon (2002) approach. |

| 2 | See Dungey et al. (2005) for a review of different correlation-based empirical methodologies. |

| 3 | See, for example, Phillips et al. (2015), Greenaway-McGrevy and Phillips (2016), Xu and Gao (2019), Mohti et al. (2019), and Samitas et al. (2020) for recent advancement in contagion detection methodologies. |

| 4 | In their actual empirical setting, Forbes and Rigobon (2002) test the following hypotheses:

|

| 5 | Corsetti et al. (2005) offer a similar approach to test for contagion. By relaxing the assumption in Forbes and Rigobon (2002) that the underlying relation between two markets remains constant, Corsetti et al. (2005) provide an adjustment in the unconditional correlation for changes in the variance ratios of the residuals (idiosyncratic factor) and the common factor during the non-crisis and crisis periods, . More specifically, the adjusted correlation coefficient during the crisis period is:

|

| 6 | To overcome the heteroskedasticity issue, some recent studies compute the conditional correlation from the dynamic conditional correlation (DCC) GARCH approach (Engle 2002) and test for a significant increase in the conditional correlation during the crisis period (Chiang et al. 2007; Wang and Nguyen Thi 2012), under the null hypothesis of no contagion, . The DCC approach overcomes the endogeneity issue and omitted variable issues of the Forbes and Rigobon (2002) approach by computing the conditional correlation coefficient from GARCH model residuals. |

| 7 | We have also performed sensitivity analyses for the different values of . As postulated in Dungey and Renault (2018), the results are relatively insensitive to the choice of value for . |

| 8 | The third row of will have a constant term on the righthand side so it does not enter into the estimation process. |

| 9 | Note that the loss was computed as a percentage change in the price index with the highest and lowest values during the crisis period. |

| 10 | The p-values for the coefficients of Brazil and India are 0.11. |

References

- Ait-Sahalia, Yacine, Jochen Andritzky, Andreas Jobst, Sylwia Nowak, and Natalia Tamirisa. 2012. Market response to policy initiatives during the global financial crisis. Journal of International Economics 87: 162–77. [Google Scholar] [CrossRef]

- Aloui, Riadh, Mohamed Safouane Ben Aissa, and Duc Khuong Nguyen. 2011. Global financial crisis, extreme interdependences, and contagion effects: The role of economic structure? Journal of Banking and Finance 35: 130–41. [Google Scholar] [CrossRef]

- Bae, Kee Hong, Andrew Karolyi, and Rene Stulz. 2003. A new approach to measuring financial contagion. Review of Financial Studies 16: 717–63. [Google Scholar] [CrossRef]

- Bago, Jean-Louis, Koffi Akakpo, Imad Rherrad, and Ernest Ouédraogo. 2021. Volatility spillover and international contagion of housing bubbles. Journal of Risk and Financial Management 14: 287. [Google Scholar] [CrossRef]

- Baig, Taimur, and Ilan Goldfajn. 1999. Financial market contagion in the Asian crisis. IMF Staff Papers 46: 167–95. [Google Scholar]

- Baur, Dirk G. 2012. Financial contagion and the real economy. Journal of Banking and Finance 36: 2680–92. [Google Scholar] [CrossRef] [Green Version]

- Bekaert, Geert, and Campbell R. Harvey. 1995. Time-varying world market integration. The Journal of Finance 50: 403–44. [Google Scholar] [CrossRef]

- Bekaert, Geert, Campbell R. Harvey, and Angela Ng. 2005. Market integration and contagion. Journal of Business 78: 39–70. [Google Scholar] [CrossRef] [Green Version]

- Bekaert, Geert, Michael Ehrmann, Marcel Fratzcher, and Arnaud Mehl. 2014. The global crisis and equity market contagion. The Journal of Finance 69: 2597–2649. [Google Scholar] [CrossRef] [Green Version]

- Bhuiyan, Erfan M., and Murshed Chowdhury. 2020. Macroeconomic variables and stock market indices: Asymmetric dynamics in the US and Canada. The Quarterly Review of Economics and Finance 77: 62–74. [Google Scholar] [CrossRef]

- Billio, Monica, and Loriana Pelizzon. 2003. Contagion and interdependence in stock markets: Have they been misdiagnosed? Journal of Economics and Business 55: 405–26. [Google Scholar] [CrossRef]

- Boyson, Nicole M., Christof W. Stahel, and Rene M. Stulz. 2010. Hedge fund contagion and liquidity shocks. The Journal of Finance 65: 1789–816. [Google Scholar] [CrossRef]

- Busetti, Fabio, and Andrew Harvey. 2011. When is a copula constant? A test for changing relationships. Journal of Financial Econometrics 9: 106–31. [Google Scholar] [CrossRef] [Green Version]

- Calvo, Guillermo A., and Enrique G. Mendoza. 2000. Capital-markets crises and economic collapse in emerging markets: An informational-frictions approach. American Economic Review 90: 59–64. [Google Scholar] [CrossRef] [Green Version]

- Chiang, Thomas C., Bang Nam Jeon, and Huimin Li. 2007. Dynamic correlation analysis of financial contagion: Evidence from Asian markets. Journal of International Money and Finance 26: 1206–28. [Google Scholar] [CrossRef]

- Corsetti, Giancarlo, Marcello Pericoli, and Massimo Sbracia. 2005. Some contagion, some interdependence: More pitfalls in tests of financial contagion. Journal of International Money and Finance 24: 1177–99. [Google Scholar] [CrossRef]

- Dickey, David A., and Wayne A. Fuller. 1979. Distribution of the estimators for autoregressive time series with a unit root. Journal of the American Statistical Association 74: 427–31. [Google Scholar]

- Dornbusch, Rudiger, Yung Chul Park, and Stijn Claessens. 2000. Contagion: Understanding how it spreads. World Bank Research Observer 15: 177–97. [Google Scholar] [CrossRef] [Green Version]

- Dungey, Mardi, and Dinesh Gajurel. 2014. Equity market contagion during the global financial crisis: Evidence from the world’s eight largest economies. Economic Systems 38: 161–77. [Google Scholar] [CrossRef] [Green Version]

- Dungey, Mardi, and Dinesh Gajurel. 2015. Contagion and banking crisis–international evidence for 2007–2009. Journal of Banking and Finance 60: 271–83. [Google Scholar] [CrossRef] [Green Version]

- Dungey, Mardi, and Eric Renault. 2018. Identifying contagion. Journal of Applied Econometrics 33: 227–250. [Google Scholar] [CrossRef]

- Dungey, Mardi, and Vance Martin. 2001. Contagion across Financial Markets: An Empirical Assessment. New York Stock Exchange Conference Paper. Cleveland: Econometric Society, pp. 16–17. [Google Scholar]

- Dungey, Mardi, Renee Fry, Brenda Gonzalez-Hermosillo, and Vance Martin. 2005. Empirical modelling of contagion: A review of methodologies. Quantitative Finance 5: 9–24. [Google Scholar] [CrossRef] [Green Version]

- Eichengreen, Barry, Andrew Rose, and Charles Wyplosz. 1996. Contagious currency crises: First tests. Scandinavian Journal of Economics 98: 463–84. [Google Scholar] [CrossRef]

- Engle, Robert F. 2002. Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. Journal of Business and Economic Statistics 20: 339–50. [Google Scholar] [CrossRef]

- Favero, Carlo A., and Francesco Giavazzi. 2002. Is the international propagation of financial shocks non-linear?: Evidence from the ERM. Journal of International Economics 57: 231–46. [Google Scholar] [CrossRef]

- Forbes, Kristin J., and Roberto Rigobon. 2002. No contagion, only interdependence: Measuring stock market comovements. The Journal of Finance 57: 2223–61. [Google Scholar] [CrossRef]

- Fratzscher, Marcel. 2012. Capital flows, push versus pull factors and the global financial crisis. Journal of International Economics 88: 341–56. [Google Scholar] [CrossRef] [Green Version]

- Gajurel, Dinesh, and Akhila Chawla. 2022. International information spillovers and asymmetric volatility in South Asian stock markets. Journal of Risk and Financial Management 15: 471. [Google Scholar] [CrossRef]

- Ghysels, Eric, and Alastair Hall. 1990. A test for structural stability of Euler conditions parameters estimated via the generalized method of moments estimator. International Economic Review 31: 355–64. [Google Scholar] [CrossRef]

- Goldstein, Morris. 1998. The Asian Crisis: Causes, Cures, and Systematic Implications. Washington, DC: Institute for International Economics. [Google Scholar]

- Greenaway-McGrevy, Ryan, and Peter C. B. Phillips. 2016. Hot property in New Zealand: Empirical evidence of housing bubbles in the metropolitan centres. New Zealand Economic Papers 50: 88–113. [Google Scholar] [CrossRef] [Green Version]

- Gurdgiev, Constantin, and Conor O’Riordan. 2021. A wavelet perspective of crisis contagion between advanced economies and the BRIC markets. Journal of Risk and Financial Management 14: 503. [Google Scholar] [CrossRef]

- Hall, Alastair R. 2005. Generalized Method of Moments. London: Oxford University Press. [Google Scholar]

- Hamao, Yasushi, Ronald Masulis, and Victor Ng. 1990. Correlations in price changes and volatility across international stock markets. Review of Financial Studies 3: 281–307. [Google Scholar] [CrossRef]

- Hansen, Lars Peter. 1982. Large sample properties of generalized method of moments estimators. Econometrica 50: 1029–54. [Google Scholar] [CrossRef]

- Hwang, Eugene, Hong-Ghi Min, Bong-Han Kim, and Hyeongwoo Kim. 2013. Determinants of stock market comovements among US and emerging economies during the US financial crisis. Economic Modelling 35: 338–48. [Google Scholar] [CrossRef]

- Jeanne, Olivier. 1997. Are currency crises self-fulfilling?: A test. Journal of International Economics 43: 263–86. [Google Scholar] [CrossRef]

- Kalemli-Ozcan, Sebnem, Elias Papaioannou, and Jose Luis Peydro. 2013. Financial regulation, financial globalization, and the synchronization of economic activity. The Journal of Finance 68: 1179–228. [Google Scholar] [CrossRef] [Green Version]

- Kaminsky, Graciela, and Carmen Reinhart. 1998. Financial crises in Asia and Latin America: Then and now. American Economic Review 88: 444–48. [Google Scholar]

- Kaminsky, Graciela, and Sergio Schmukler. 1999. What triggers market jitters?: A chronicle of the asian crisis. Journal of International Money and Finance 18: 537–60. [Google Scholar] [CrossRef]

- Kaminsky, Graciela, Saul Lizondo, and Carmen M. Reinhart. 1998. Leading indicators of currency crises. IMF Staff Papers 45: 1–48. [Google Scholar] [CrossRef] [Green Version]

- Kangogo, Moses, Mardi Dungey, and Vladimir Volkov. 2022. Changing vulnerability in Asia: Contagion and spillovers. Empirical Economics 1–41. [Google Scholar] [CrossRef]

- Kasch, Maria, and Massimiliano Caporin. 2013. Volatility threshold dynamic conditional correlations: An international analysis. Journal of Financial Econometrics 11: 706–42. [Google Scholar] [CrossRef] [Green Version]

- Kenourgios, Dimitris, Aristeidis Samitas, and Nikos Paltalidis. 2011. Financial crises and stock market contagion in a multivariate time-varying asymmetric framework. Journal of International Financial Markets, Institutions and Money 21: 92–106. [Google Scholar] [CrossRef]

- King, Mervyn, and Sushil Wadhwani. 1990. Transmission of volatility between stock markets. Review of Financial Studies 3: 5–33. [Google Scholar] [CrossRef]

- Klyuev, Vladimir, Phil De Imus, and Krishna Srinivasan. 2009. Unconventional Choices for Unconventional Times: Credit and Quantitative Easing in Advanced Economies. IMF Staff Position Note 27. Washington, DC: International Monetary Fund. [Google Scholar]

- Kyle, Albert S., and Wei Xiong. 2001. Contagion as a wealth effect. The Journal of Finance 56: 1401–40. [Google Scholar] [CrossRef]

- MacKinnon, James G. 1994. Approximate asymptotic distribution functions for unit-root and cointegration tests. Journal of Business & Economic Statistics 12: 167–76. [Google Scholar]

- Masson, Paul. 1999. Contagion: Macroeconomic models with multiple equilibria. Journal of International Money and Finance 18: 587–602. [Google Scholar] [CrossRef]

- Mohti, Wahbeeah, Andreia Dionísio, Isabel Vieira, and Paulo Ferreira. 2019. Financial contagion analysis in frontier markets: Evidence from the US subprime and the Eurozone debt crises. Physica A: Statistical Mechanics and its Applications 525: 1388–98. [Google Scholar] [CrossRef]

- Mondria, Jordi, and Climent Quintana-Domeque. 2013. Financial contagion and attention allocation. The Economic Journal 123: 429–54. [Google Scholar] [CrossRef] [Green Version]

- Moser, Thomas. 2003. What is international financial contagion? International Finance 6: 157–78. [Google Scholar] [CrossRef] [Green Version]

- Pasquariello, Paolo. 2007. Imperfect competition, information heterogeneity, and financial contagion. Review of Financial Studies 20: 391–426. [Google Scholar] [CrossRef]

- Phillips, Peter C. B., Shuping Shi, and Jun Yu. 2015. Testing for multiple bubbles: Historical episodes of exuberance and collapse in the S&P 500. International Economic Review 56: 1043–78. [Google Scholar]

- Polson, Nicholas G., and James G. Scott. 2011. An empirical test for Eurozone contagion using an asset-pricing model with heavy-tailed stochastic volatility. arXiv arXiv:1110.5789. [Google Scholar]

- Rose, Andrew K., and Mark M. Spiegel. 2010. Cross-country causes and consequences of the 2008 crisis: International linkages and American exposure. Pacific Economic Review 15: 340–63. [Google Scholar] [CrossRef] [Green Version]

- Samarakoon, Lalith P. 2011. Stock market interdependence, contagion, and the U.S. financial crisis: The case of emerging and frontier markets. Journal of International Financial Markets, Institutions and Money 21: 724–42. [Google Scholar] [CrossRef]

- Samitas, Aristeidis, Elias Kampouris, and Dimitris Kenourgios. 2020. Machine learning as an early warning system to predict financial crisis. International Review of Financial Analysis 71: 101507. [Google Scholar] [CrossRef]

- Tan, Lin, Thomas C. Chiang, Joseph R. Mason, and Edward Nelling. 2008. Herding behavior in Chinese stock markets: An examination of A and B shares. Pacific-Basin Finance Journal 16: 61–77. [Google Scholar] [CrossRef]

- van Rijckeghem, Caroline, and Beatrice Weder. 2001. Sources of contagion: Is it finance or trade? Journal of International Economics 54: 293–308. [Google Scholar] [CrossRef]

- Wang, Gang-Jin, Chi Xie, Min Lin, and H. Eugene Stanley. 2017. Stock market contagion during the global financial crisis: A multiscale approach. Finance Research Letters 22: 163–68. [Google Scholar] [CrossRef]

- Wang, Kuan Min, and Thanh Binh Nguyen Thi. 2012. Did China avoid the Asian flu? The contagion effect test with dynamic correlation coefficients. Quantitative Finance 23: 471–81. [Google Scholar] [CrossRef]

- Xu, Guoxiang, and Wangfeng Gao. 2019. Financial risk contagion in stock markets: Causality and measurement aspects. Sustainability 11: 1402. [Google Scholar] [CrossRef] [Green Version]

- Yuan, Kathy. 2005. Asymmetric price movements and borrowing constraints: A rational expectations equilibrium model of crises, contagion, and confusion. The Journal of Finance 60: 379–411. [Google Scholar] [CrossRef] [Green Version]

- Zhang, Bing, Xindan Li, and Honghai Yu. 2013. Has recent financial crisis changed permanently the correlations between BRICS and developed stock markets? North American Journal of Economics and Finance 26: 725–38. [Google Scholar] [CrossRef]

{kind=link}

| Country | Aggregate Equity Market | Financial Sector |

|---|---|---|

| U.S. | TOTMKUS | FINANUS |

| France | TOTMKFR | FINANFR |

| Germany | TOTMKBD | FINANBD |

| Japan | TOTMKJP | FINANJP |

| U.K. | TOTMKUK | FINANUK |

| Brazil | TOTMKBR | FINANBR |

| China | TOTMKCA | FINANCA |

| India | TOTMKIN | FINANIN |

| Russia | TOTMKRS | FINANRS |

| Statistics | Advanced Markets | Emerging Markets | |||||||

|---|---|---|---|---|---|---|---|---|---|

| U.S. | France | Germany | Japan | U.K. | Brazil | China | India | Russia | |

| Panel A: Whole sample period (2 August 2004 to 30 May 2009) | |||||||||

| Mean | −0.0106 | −0.0045 | 0.0057 | −0.0192 | 0.0027 | 0.0656 | 0.0428 | 0.0793 | 0.0460 |

| Median | 0.0488 | 0.0432 | 0.0874 | 0.0000 | 0.0417 | 0.0780 | 0.0281 | 0.1390 | 0.0612 |

| Maximum | 10.9019 | 9.9199 | 16.0461 | 12.2917 | 8.8611 | 10.8596 | 9.0409 | 15.0785 | 23.1743 |

| Minimum | −9.4087 | −8.4287 | −6.9133 | −9.6851 | −8.7142 | −9.9400 | −9.3062 | −12.1159 | −19.8503 |

| Std. Dev. | 1.4617 | 1.3285 | 1.2887 | 1.5316 | 1.3355 | 1.7157 | 1.9462 | 1.8383 | 2.4724 |

| Skewness | −0.2748 | 0.0202 | 1.2866 | −0.3039 | −0.1890 | −0.1886 | −0.2103 | −0.2509 | −0.2540 |

| Kurtosis | 14.0983 | 12.4743 | 28.9023 | 11.0001 | 12.0579 | 8.6266 | 5.9864 | 10.3122 | 19.7653 |

| ADF test | −29.7948 ** | −17.1676 ** | −37.5623 ** | −27.2110 ** | −17.3607 ** | −35.2048 ** | −35.8301 ** | −32.8214 ** | −34.9397 ** |

| Observations | 1260 | 1260 | 1260 | 1260 | 1260 | 1260 | 1260 | 1260 | 1260 |

| Panel B: Pre-crisis period (2 August 2004 to 18 July 2007) | |||||||||

| Mean | 0.0477 | 0.0721 | 0.0797 | 0.0545 | 0.0569 | 0.1300 | 0.1151 | 0.1304 | 0.1301 |

| Median | 0.0596 | 0.0910 | 0.1219 | 0.0144 | 0.0701 | 0.1144 | 0.0555 | 0.2108 | 0.1338 |

| Maximum | 2.2614 | 2.6220 | 2.7766 | 3.5518 | 2.8932 | 4.1818 | 8.0492 | 6.2996 | 9.2462 |

| Minimum | −3.4177 | −3.0584 | −4.6597 | −3.6684 | −2.8766 | −5.5808 | −9.3062 | −7.3263 | −10.7884 |

| Std. Dev. | 0.6435 | 0.7368 | 0.7241 | 0.9513 | 0.6612 | 1.1264 | 1.5497 | 1.2813 | 1.7221 |

| Skewness | −0.2474 | −0.4725 | −0.7768 | −0.3647 | −0.4476 | −0.2487 | −0.4860 | −0.7565 | −0.8911 |

| Kurtosis | 4.4435 | 5.0650 | 7.0114 | 4.7469 | 5.5629 | 4.5510 | 7.6762 | 7.3546 | 9.1114 |

| Observations | 773 | 773 | 773 | 773 | 773 | 773 | 773 | 773 | 773 |

| Panel C: Crisis period (19 July 2007 to 30 May 2009) | |||||||||

| Mean | −0.1032 | −0.1259 | −0.1117 | −0.1361 | −0.0833 | −0.0367 | −0.0721 | −0.0019 | −0.0874 |

| Median | 0.0000 | −0.0189 | 0.0021 | 0.0000 | −0.0002 | 0.0000 | 0.0000 | 0.0161 | −0.0008 |

| Maximum | 10.9019 | 9.9199 | 16.0461 | 12.2917 | 8.8611 | 10.8596 | 9.0409 | 15.0785 | 23.1743 |

| Minimum | −9.4087 | −8.4287 | −6.9133 | −9.6851 | −8.7142 | −9.9400 | −8.0253 | −12.1159 | −19.8503 |

| Std. Dev. | 2.2052 | 1.9198 | 1.8565 | 2.1486 | 1.9783 | 2.3650 | 2.4445 | 2.4770 | 3.3310 |

| Skewness | −0.0823 | 0.2220 | 1.3498 | −0.1035 | −0.0082 | −0.0435 | 0.0061 | −0.0274 | 0.0146 |

| Kurtosis | 6.9832 | 7.2817 | 17.4736 | 7.0402 | 6.3743 | 5.8098 | 4.2753 | 7.2795 | 14.5368 |

| Observations | 487 | 487 | 487 | 487 | 487 | 487 | 487 | 487 | 487 |

| Equity Market | France | Germany | Japan | U.K. | Brazil | China | India | Russia | |

|---|---|---|---|---|---|---|---|---|---|

| Panel A. Correlation coefficients | |||||||||

| Pre-crisis period | 0.64 | 0.69 | 0.28 | 0.62 | 0.65 | 0.07 | 0.27 | 0.31 | |

| Crisis period: naive | 0.75 | 0.77 | 0.41 | 0.74 | 0.75 | 0.12 | 0.40 | 0.48 | |

| Crisis period: adjusted | 0.34 | 0.37 | 0.14 | 0.34 | 0.34 | 0.04 | 0.14 | 0.17 | |

| Unadjusted correlation test: | t-stat | 3.63 | 3.20 | 2.64 | 3.89 | 3.36 | 0.82 | 2.63 | 3.42 |

| p-value | 0.02 | 0.03 | 0.04 | 0.02 | 0.02 | 0.24 | 0.04 | 0.02 | |

| Adjusted correlation test: | t-stat | −7.04 | −7.99 | −2.40 | −6.62 | −7.32 | −0.60 | −2.32 | −2.58 |

| p-value | 0.00 | 0.00 | 0.05 | 0.00 | 0.00 | 0.30 | 0.05 | 0.04 | |

| Panel B. Regression coefficients | |||||||||

| Pre-crisis period | 0.74 | 0.78 | 0.41 | 0.64 | 1.17 | 0.19 | 0.55 | 0.81 | |

| se | 0.03 | 0.03 | 0.05 | 0.03 | 0.05 | 0.08 | 0.07 | 0.09 | |

| t-stat | 23.87 | 26.94 | 8.26 | 22.68 | 24.34 | 2.29 | 7.92 | 9.42 | |

| Crisis period: naive | 0.69 | 0.68 | 0.43 | 0.70 | 0.86 | 0.15 | 0.51 | 0.81 | |

| se | 0.03 | 0.03 | 0.04 | 0.03 | 0.03 | 0.05 | 0.05 | 0.07 | |

| t-stat | 25.20 | 27.16 | 10.01 | 24.67 | 25.26 | 2.78 | 9.78 | 12.15 | |

| Crisis period: adjusted | 0.26 | 0.26 | 0.16 | 0.26 | 0.32 | 0.06 | 0.19 | 0.31 | |

| se | 0.01 | 0.01 | 0.02 | 0.01 | 0.01 | 0.02 | 0.02 | 0.03 | |

| t-stat | 25.20 | 27.16 | 10.01 | 24.67 | 25.26 | 2.78 | 9.78 | 12.15 | |

| Panel C: Factor loadings | |||||||||

| Pre-crisis | 2.03 | 1.92 | 2.73 | 1.84 | 3.00 | 0.90 | 4.36 | 4.99 | |

| se | 0.02 | 0.03 | 0.09 | 0.02 | 0.05 | 0.25 | 0.54 | 0.82 | |

| t-stat | 96.68 | 69.54 | 29.87 | 90.32 | 58.33 | 3.68 | 8.15 | 6.08 | |

| Crisis period | 0.91 | 1.15 | 1.29 | 0.90 | 1.05 | 1.16 | 1.57 | 1.31 | |

| se | 0.15 | 0.39 | 0.56 | 0.33 | 0.49 | 0.35 | 0.75 | 1.66 | |

| t-stat | 6.31 | 2.94 | 2.30 | 2.76 | 2.15 | 3.36 | 2.11 | 0.79 | |

| T-test: | t-stat | −170.53 | −43.35 | −56.83 | −64.26 | −88.89 | 14.56 | −72.25 | −45.74 |

| p-value | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| Panel D: Hansen’s J-test for identification | |||||||||

| Pre-crisis | 0.19 | 0.18 | 0.27 | 0.22 | 0.21 | 0.52 | 0.30 | 0.28 | |

| p-value | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | |

| Crisis | 0.59 | 1.05 | 0.72 | 0.64 | 0.73 | 0.48 | 0.80 | 0.88 | |

| p-value | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | |

| Panel E. Tests for structural stability | |||||||||

| Ghysels–Hall test | 110.90 | 108.47 | 88.99 | 121.95 | 106.39 | 84.90 | 106.60 | 109.65 | |

| p-value | 0.07 | 0.09 | 0.51 | 0.01 | 0.11 | 0.63 | 0.11 | 0.08 | |

| Break in factor loadings | 195.86 | 102.28 | 111.27 | 153.25 | 158.50 | 72.79 | 109.34 | 75.09 | |

| p-value | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| Break in number of factors | 0.59 | 1.05 | 0.72 | 0.64 | 0.73 | 0.48 | 0.80 | 0.88 | |

| p-value | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | |

| Equity Market | France | Germany | Japan | U.K. | Brazil | China | India | Russia | |

|---|---|---|---|---|---|---|---|---|---|

| Panel A. Correlation coefficients | |||||||||

| Pre-crisis period | 0.57 | 0.60 | 0.19 | 0.53 | 0.50 | 0.13 | 0.20 | 0.16 | |

| Crisis period: naive | 0.63 | 0.68 | 0.33 | 0.65 | 0.62 | 0.09 | 0.35 | 0.40 | |

| Crisis period: adjusted | 0.17 | 0.19 | 0.08 | 0.17 | 0.16 | 0.02 | 0.08 | 0.09 | |

| Unadjusted correlation test: | t-stat | 1.78 | 2.45 | 2.49 | 3.22 | 3.07 | −0.76 | 2.99 | 4.64 |

| p-value | 0.09 | 0.05 | 0.04 | 0.02 | 0.03 | 0.25 | 0.03 | 0.01 | |

| Adjusted correlation test: | t-stat | −8.23 | −8.74 | −2.16 | −7.18 | −6.68 | −1.98 | −2.09 | −1.18 |

| p-value | 0.00 | 0.00 | 0.06 | 0.00 | 0.00 | 0.07 | 0.06 | 0.16 | |

| Panel B. Regression coefficients | |||||||||

| Pre-crisis period | 0.73 | 0.68 | 0.37 | 0.57 | 0.99 | 0.34 | 0.47 | 0.51 | |

| se | 0.04 | 0.03 | 0.06 | 0.03 | 0.06 | 0.09 | 0.08 | 0.10 | |

| t-stat | 19.77 | 21.67 | 5.8 | 18.01 | 16.35 | 3.98 | 5.79 | 4.96 | |

| Crisis period: naive | 0.52 | 0.44 | 0.28 | 0.56 | 0.47 | 0.07 | 0.36 | 0.49 | |

| se | 0.03 | 0.02 | 0.04 | 0.03 | 0.03 | 0.03 | 0.04 | 0.05 | |

| t-stat | 18.15 | 20.89 | 7.73 | 19.02 | 17.58 | 2.05 | 8.46 | 9.81 | |

| Crisis period: adjusted | 0.12 | 0.10 | 0.07 | 0.13 | 0.11 | 0.02 | 0.08 | 0.11 | |

| se | 0.01 | 0.00 | 0.01 | 0.01 | 0.01 | 0.01 | 0.01 | 0.01 | |

| t-stat | 18.15 | 20.89 | 7.73 | 19.02 | 17.58 | 2.05 | 8.46 | 9.81 | |

| Panel C: Factor loadings | |||||||||

| Pre-crisis | 1.63 | 1.49 | 1.63 | 1.40 | 2.35 | 0.66 | 2.99 | 2.97 | |

| se | 0.06 | 0.05 | 0.15 | 0.04 | 0.19 | 0.46 | 0.42 | 1.98 | |

| t-stat | 26.1 | 30.22 | 10.62 | 38.59 | 12.31 | 1.43 | 7.05 | 1.5 | |

| Crisis period | 0.91 | 0.87 | 1.17 | 0.99 | 0.62 | 0.75 | 1.18 | 1.15 | |

| se | 0.6 | 0.42 | 0.99 | 0.62 | 0.54 | 0.83 | 1.13 | 2.06 | |

| t-stat | 1.52 | 2.06 | 1.19 | 1.59 | 1.17 | 0.91 | 1.05 | 0.56 | |

| T-test: | t-stat | −26.47 | −32.44 | −10.06 | −14.62 | −68.85 | 2.27 | −33.89 | −15.62 |

| p-value | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.05 | 0.00 | 0.00 | |

| Panel D: Hansen’s J-test for identification | |||||||||

| Pre-crisis | 0.21 | 0.19 | 0.35 | 0.22 | 0.23 | 0.46 | 0.35 | 0.43 | |

| p-value | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | |

| Crisis | 0.64 | 0.87 | 0.81 | 0.6 | 0.79 | 0.71 | 0.65 | 0.82 | |

| p-value | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | |

| Panel E. Tests for structural stability | |||||||||

| Ghysels-Hall test | 117.31 | 111.19 | 98.09 | 127.19 | 119.28 | 112.23 | 111.62 | 123.49 | |

| p-value | 0.03 | 0.06 | 0.26 | 0.01 | 0.02 | 0.06 | 0.06 | 0.01 | |

| Break in factor loadings: Hall test | 139.76 | 119.73 | 110.03 | 150.6 | 148.48 | 80.89 | 118.36 | 50.17 | |

| p-value | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.05 | 0.00 | 0.00 | |

| Break in number of factors | 0.64 | 0.87 | 0.81 | 0.6 | 0.79 | 0.71 | 0.65 | 0.82 | |

| p-value | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gajurel, D.; Dungey, M. Systematic Contagion Effects of the Global Finance Crisis: Evidence from the World’s Largest Advanced and Emerging Equity Markets. J. Risk Financial Manag. 2023, 16, 182. https://doi.org/10.3390/jrfm16030182

Gajurel D, Dungey M. Systematic Contagion Effects of the Global Finance Crisis: Evidence from the World’s Largest Advanced and Emerging Equity Markets. Journal of Risk and Financial Management. 2023; 16(3):182. https://doi.org/10.3390/jrfm16030182

Chicago/Turabian StyleGajurel, Dinesh, and Mardi Dungey. 2023. "Systematic Contagion Effects of the Global Finance Crisis: Evidence from the World’s Largest Advanced and Emerging Equity Markets" Journal of Risk and Financial Management 16, no. 3: 182. https://doi.org/10.3390/jrfm16030182