Financial Well-Being and Financial Capability among Low-Income Entrepreneurs

Abstract

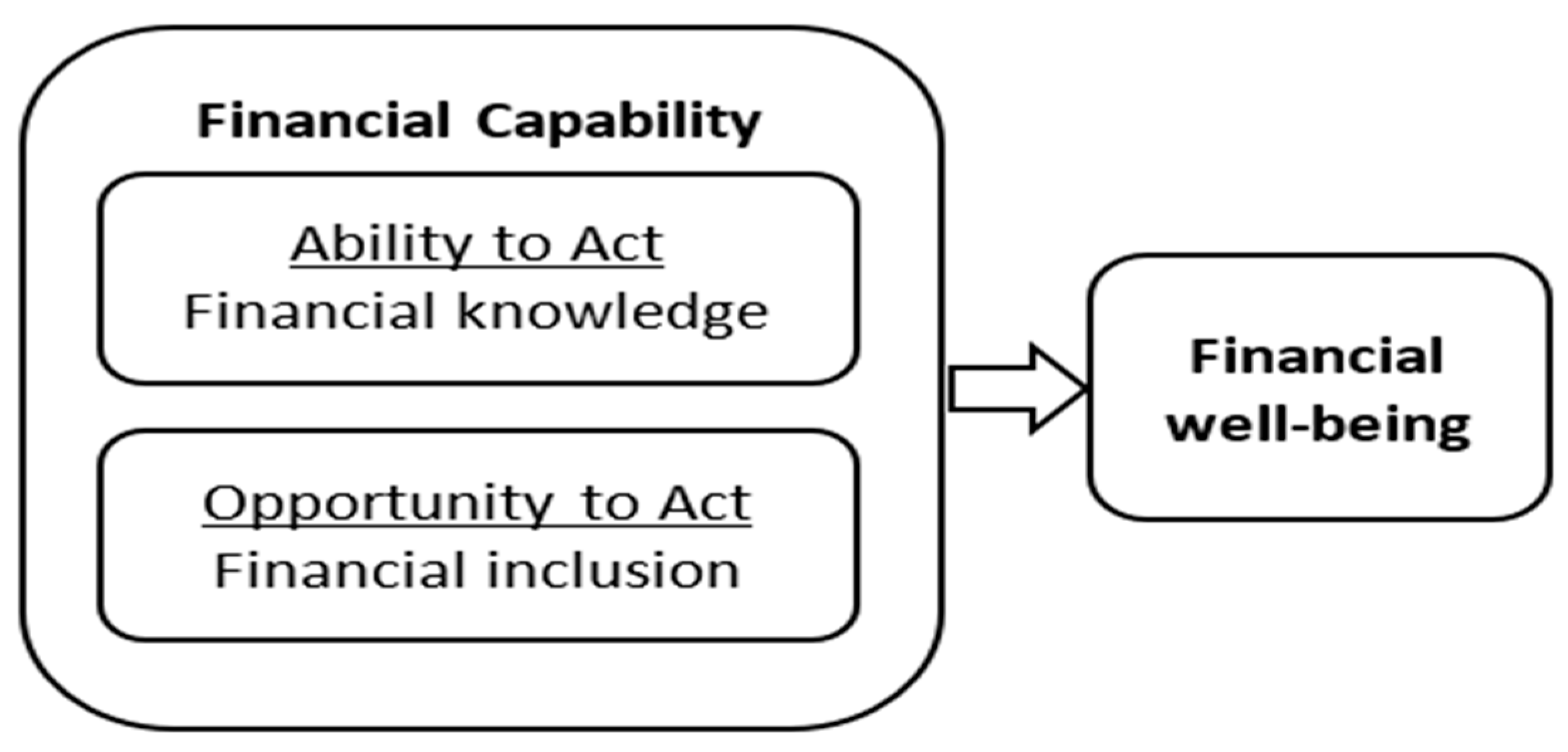

:1. Introduction

2. Methods

2.1. Data and Sample

2.2. Measures

2.3. Analyses

3. Results

3.1. Sample Characteristics

3.2. Financial Well-Being and Financial Capability

3.3. Regression Results

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Acs, Zoltan. 2008. State of literature on small-to medium-sized enterprises and entrepreneurship in low-income communities. In Entrepreneurship in Emerging Domestic Markets. Boston: Springer, pp. 21–45. [Google Scholar]

- Arping, Stefan, Gyöngyi Lóránth, and Alan Morrison. 2010. Public initiatives to support entrepreneurs: Credit guarantees versus co-funding. Journal of Financial Stability 6: 26–35. [Google Scholar] [CrossRef] [Green Version]

- Atkinson, Adele, and Flore-Anne Messy. 2011. Assessing financial literacy in 12 countries: An OECD/INFE international pilot exercise. Journal of Pension Economics & Finance 10: 657–65. [Google Scholar]

- Bartik, Alexander, Marianne Bertrand, Zoe Cullen, Edward Glaeser, Michael Luca, and Christopher Stanton. 2020. The impact of COVID-19 on small business outcomes and expectations. Proceedings of the National Academy of Sciences 117: 17656–66. [Google Scholar] [CrossRef]

- Berglann, Helge, Espen Moen, Knut Røed, and Jens Fredrik Skogstrøm. 2011. Entrepreneurship: Origins and returns. Labour Economics 18: 180–93. [Google Scholar] [CrossRef] [Green Version]

- Bianchi, Milo. 2012. Financial development, entrepreneurship, and job satisfaction. Review of Economics and Statistics 94: 273–86. [Google Scholar] [CrossRef] [Green Version]

- Bloom, Nicholas, Roberts Fletcher, and Ethan Yeh. 2021. The Impact of COVID-19 on US Firms. No. w28314. Cambridge: National Bureau of Economic Research. [Google Scholar] [CrossRef]

- Choguill, Charles. 1999. Community infrastructure for low-income cities: The potential for progressive improvement. Habitat International 23: 289–301. [Google Scholar] [CrossRef]

- Collins, Michael. 2014. Financial Coaching: An Asset Building Strategy (Asset Funders Network Brief). Madison: University of Wisconsin-Madison, Center for Financial Security. Available online: http://cfs.wisc.edu/briefs/AFN_FinacialCoaching_august.pdf (accessed on 20 January 2023).

- Consumer Financial Protection Bureau. 2015. Financial Well-Being: The Goal of Financial Education. Washington, DC: Consumer Financial Protection Bureau. [Google Scholar]

- Consumer Financial Protection Bureau. 2017. National Financial Well-Being Survey: Public Use File User’s Guide. Washington, DC: Consumer Financial Protection Bureau. [Google Scholar]

- Fairlie, Robert. 2020. The Impact of COVID-19 on Small Business Owners: The First Three Months after Social-Distancing Restrictions. NBER Working Paper No. 27462. Cambridge: National Bureau of Economic Research. [Google Scholar] [CrossRef]

- Fang, Shu, and Jin Huang. 2022a. Social workers can help adults with complex needs with financial wellbeing. BMJ 378: o1928. [Google Scholar] [CrossRef]

- Fang, Shu, and Jin Huang. 2022b. Financial incentives for health should be standard practice. BMJ 376: o179. [Google Scholar] [CrossRef]

- Gumus, Gulcin, and Tracy Regan. 2015. Self-employment and the role of health insurance in the U.S. Journal of Business Venturing 30: 357–74. [Google Scholar] [CrossRef]

- Hamilton, Barton. 2000. Does entrepreneurship pay? An empirical analysis of the returns to self-employment. Journal of Political Economy 108: 604–31. [Google Scholar] [CrossRef] [Green Version]

- Huang, Jin, Yunju Nam, and Eun Jeong Lee. 2015. Financial capability and economic hardship among low-income older Asian immigrants in a supported employment program. Journal of Family and Economic Issues 36: 239–50. [Google Scholar] [CrossRef]

- Huang, Jin, Yunju Nam, and Margaret Sherraden. 2013. Financial knowledge and child development account policy: A test of financial capability. Journal of Consumer Affairs 47: 1–26. [Google Scholar] [CrossRef] [Green Version]

- Huang, Jin, Michael Sherraden, Margaret Sherraden, and Lissa Johnson. 2022. Effective finance to increase financial well-being for low-income families: Empirical examination and policy implications. Journal of Consumer Affairs 56: 1638–57. [Google Scholar] [CrossRef]

- Humphries, John Eric, Christopher Neilson, and Gabriel Ulyssea. 2020. The Evolving Impacts of COVID-19 on Small Businesses Since the CARES Act. Cowles Foundation Discussion Paper No. 2230. New York: New York University. [Google Scholar] [CrossRef]

- Idris, Adama, and Kenneth Chukwujioke Agbim. 2015. Micro-credit as a strategy for poverty alleviation among women entrepreneurs in Nasarawa State, Nigeria. Journal of Business Studies Quarterly 6: 122–43. [Google Scholar]

- Joo, Sohyun. 2008. Personal financial wellness. In Handbook of Consumer Finance Research. Edited by J. J. Xiao. New York: Springer, pp. 21–34. [Google Scholar]

- Knoll, Melissa, and Carrie Houts. 2012. The financial knowledge scale: An application of item response theory to the assessment of financial literacy. Journal of Consumer Affairs 46: 381–410. [Google Scholar] [CrossRef]

- Kugler, Maurice, Marios Michaelides, Neha Nanda, and Cassandra Agbayani. 2017. Entrepreneurship in Low-Income Areas. US Small Business Administration Office of Advocacy. Available online: https://www.sba.gov/sites/default/files/437-Entrepreneurship-in-Low-income-Areas.pdf (accessed on 20 January 2023).

- Laney, Kahliah. 2013. Launching Low-Income Entrepreneurs; New York: Center for an Urban Future. Available online: https://files.eric.ed.gov/fulltext/ED555604.pdf (accessed on 20 January 2023).

- Langely, Paul. 2014. Equipping entrepreneurs: Consuming credit and credit scores. Consumption Markets & Culture 17: 448–67. [Google Scholar]

- Larsson, Johan, and Per Thulin. 2019. Independent by necessity? The life satisfaction of necessity and opportunity entrepreneurs in 70 countries. Small Business Economics 53: 921–34. [Google Scholar] [CrossRef] [Green Version]

- Leyshon, Andrew, and Nigel Thrift. 1995. Geographies of financial exclusion: Financial abandonment in Britain and the United States. Transactions of the Institute of British Geographers, 312–41. [Google Scholar] [CrossRef]

- Lin, Ken-Hou, Carolina Aragão, and Guillermo Dominguez. 2021. Firm size and employment during the pandemic. Socius 7: 2378023121992601. [Google Scholar] [CrossRef]

- Ondiek, Benedict Alala, Fredrick Ochieng Deya, and John Busaka. 2013. Cash management techniques adopted by small and medium level enterprises in eldoret town, Kenya. Research Journal of Finance and Accounting 4: 90–96. [Google Scholar]

- Sherraden, Margaret, and Jin Huang. 2019. Financial Social Work. Encyclopedia of Social Work. Available online: https://oxfordre.com/socialwork/view/10.1093/acrefore/9780199975839.001.0001/acrefore-9780199975839-e-923 (accessed on 20 January 2023).

- Sherraden, Margaret. 2013. Building blocks of financial capability. In Financial Education and Capability: Research, Education, Policy, and Practice. Edited by Julie Birkenmaier, Margaret Sherraden and Jami Curley. New York: Oxford University Press, pp. 3–43. [Google Scholar]

- Sherraden, Margaret, Cynthia Sanders, and Michael Sherraden. 2004. Kitchen Capitalism: Microenterprise in Low-Income Households. Albany: SUNY Press. [Google Scholar]

- Sun Sicong, Jin Huang, Darrell Hudson, and Michael Sherraden. 2021. Cash transfers and health. Annual Review of Public Health 42: 363–80. [Google Scholar] [CrossRef] [PubMed]

- Wong, Kuan Yew, and Elaine Aspinwall. 2004. Characterizing knowledge management in the small business environment. Journal of Knowledge Management 8: 44–61. [Google Scholar] [CrossRef]

- Xiao, Jing Jian, Jin Huang, Kirti Goyal, and Satish Kumar. 2022. Financial capability: A systematic conceptual review, extension and synthesis. International Journal of Bank Marketing 40: 1680–1717. [Google Scholar] [CrossRef]

{kind=link}

| Group | Sample Size |

|---|---|

| Low-income entrepreneurs (household income < the 200% federal poverty line) | 134 |

| Low-income non-entrepreneurs (household income < the 200% federal poverty line) | 1342 |

| Higher-income entrepreneurs (household income ≥ the 200% federal poverty line) | 402 |

| Variable | Percentage or Mean (SD) | ||

|---|---|---|---|

| Low-Income Entrepreneurs (n = 134) | Low-Income Non-entrepreneurs (n = 1342) | Higher-Income Entrepreneurs (n = 402) | |

| Age category a | |||

| 18–24 | 8.86 | 10.43 | 4.70 |

| 25–34 | 25.95 | 23.82 | 18.48 |

| 35–44 | 23.39 | 14.19 | 13.98 |

| 45–54 | 24.28 | 14.16 | 28.07 |

| 55–61 | 6.64 | 10.28 | 15.15 |

| 62 and above | 10.87 | 27.11 | 19.62 |

| Female a | 47.34 | 52.56 | 40.89 |

| Race and ethnicity a | |||

| Non-Hispanic white | 34.41 | 48.54 | 69.62 |

| Non-Hispanic black | 19.96 | 17.22 | 7.05 |

| Non-Hispanic other | 3.20 | 7.24 | 6.63 |

| Hispanic | 42.42 | 26.99 | 16.71 |

| Education a | |||

| High school and below | 48.42 | 50.71 | 17.95 |

| Some college | 29.33 | 33.52 | 21.11 |

| College degree and above | 22.25 | 15.78 | 60.94 |

| Married status a | |||

| Married | 37.22 | 38.84 | 61.09 |

| Living with partner | 50.69 | 52.59 | 30.52 |

| Others | 12.09 | 8.58 | 8.40 |

| Household size a | 2.96 (1.55) | 2.85 (1.43) | 2.43 (1.15) |

| Household income a | |||

| Less than $20,000 | 55.62 | 45.68 | 0.00 |

| $20,000–$29,999 | 17.27 | 27.88 | 3.04 |

| $30,000–$39,999 | 14.71 | 16.56 | 6.53 |

| $40,000–$49,999 | 6.96 | 6.21 | 7.71 |

| Above $50,000 | 5.44 | 3.67 | 82.73 |

| Metropolitan resident a | 91.79 | 81.99 | 88.18 |

| Financial Well-Being and Financial Capability | Low-Income Entrepreneurs (n = 134) | Low-Income Non-entrepreneurs (n = 1342) | Higher-Income Entrepreneurs (n = 402) |

|---|---|---|---|

| Financial well-being score | 47.76 | 47.05 | 56.65 a |

| Financial knowledge score | −0.68 | −0.64 | 0.10 a |

| Financial skill score | 47.97 | 46.56 | 52.99 a |

| Mainstream financial products | 1.32 b | 1.73 c | 2.74 |

| Use of risky financial products | 0.64 b | 0.49 c | 0.24 |

| Variables | Low-Income Entrepreneurs (n = 134) | Low-Income Non-entrepreneurs (n = 1342) | Higher-Income Entrepreneurs (n = 402) |

|---|---|---|---|

| Financial knowledge | −3.22 ** | −0.17 | 1.82 * |

| Financial skills | 0.32 *** | 0.28 *** | 0.33 *** |

| Financial access | 1.19 | 0.92 *** | 0.93 ** |

| Use of risky financial products | −3.31 ** | −2.52 *** | −0.80 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Guo, B.; Huang, J. Financial Well-Being and Financial Capability among Low-Income Entrepreneurs. J. Risk Financial Manag. 2023, 16, 181. https://doi.org/10.3390/jrfm16030181

Guo B, Huang J. Financial Well-Being and Financial Capability among Low-Income Entrepreneurs. Journal of Risk and Financial Management. 2023; 16(3):181. https://doi.org/10.3390/jrfm16030181

Chicago/Turabian StyleGuo, Baorong, and Jin Huang. 2023. "Financial Well-Being and Financial Capability among Low-Income Entrepreneurs" Journal of Risk and Financial Management 16, no. 3: 181. https://doi.org/10.3390/jrfm16030181