1. Introduction

Cryptocurrencies have the potential for higher returns due to their volatility and a wider range of investment opportunities due to the emergence of new tokens and coins. Cryptocurrencies are also global and borderless, allowing anyone with an internet connection to access them from anywhere in the world. Finally, when compared to fiat currency, investing in cryptocurrency can provide greater privacy and security (

Jangir et al. 2022). However, the main risks of investing in cryptocurrency include price volatility, a lack of regulation and liquidity, and the possibility of fraud (

Varma et al. 2022). Furthermore, because cryptocurrencies are decentralized, investors have no recourse if they are scammed or hacked (

Rupeika-Apoga and Wendt 2022). Furthermore, because cryptocurrencies are not supported by governments or other financial institutions, their value can be affected by political and economic events (

Rupeika-Apoga and Wendt 2021). As a result, before investing in cryptocurrency, investors should conduct extensive research.

The cryptocurrency market has a lot of room for growth (

Kumar 2022), but it also has a lot of room for losses. Wins and losses may occur regardless of whether the investor makes an excellent or terrible coin choice (

Toneatto 1999). Timing may have a significant impact on whether or not you succeed (

Tran and Leirvik 2020). According to

Hidajat (

2019), bitcoin is a very illogical investment because the value of each cryptocurrency fluctuates wildly (a trait known on Wall Street as volatility) (

Ammous 2018). The value of cryptocurrency holdings fluctuates dramatically (

Urquhart 2022).

Two principal streams in the literature examine the price fluctuations of cryptocurrencies. The first line of research, which includes foundational papers by

Katsiampa (

2017) and

Urquhart (

2017), is concerned with using GARCH family models to analyze Bitcoin prices and simulate conditional volatility. In the second set of studies, GARCH and other time-series approaches are used to examine the volatility spillover between cryptocurrencies and traditional financial markets.

Kristoufek (

2015) and

Dyhrberg (

2016) describe two illustrious instances. Evidence that Bitcoin price movement and other cryptocurrency price movements are independent was uncovered by

Ciaian et al. (

2016) in their latest research using the ARDL approach. We continue on the premise that the correlation between different cryptocurrency prices signifies a possible volatility persistence.

The study aims to examine the impact of the news (shocks) on the volatility of the cryptocurrency market. The EGARCH model was used to assess the impact of the news and volatility persistence on cryptocurrency return values from 8 March 2019 to 30 November 2022.

This study differs from previous research in three ways. First, the vast majority of published cryptocurrency research focuses on Bitcoin. However, given the current era, many more cryptocurrencies have entered the blockchain technology space. Investors are now pivoting their preference from Bitcoin to other cryptocurrencies, looking at the market’s mood. Hence, this paper covers a large portion of the cryptocurrency market by analyzing the volatility of major currencies based on market capitalization. Second, in this study, the correlation between the return of one cryptocurrency and the return of another is calculated, and the impact of the news (or shocks) on volatility is measured. Third, the current study attempts to estimate and compare the persistence of volatility across currencies. The research conclusion based on data analyses will assist the reader in understanding the orientation of the news (shocks) on volatility in cryptocurrency returns.

Our contribution to the academic literature and its practical implications is threefold. The most effective GARCH model for measuring the impact of shocks, i.e., news, known as EGARCH, was applied for the first time to the volatility in financial returns of the five largest cryptocurrencies (Bitcoin, Binance Coin (BNB), Ethereum, Dogecoin, and XRP) from 8 March 2019 to 30 November 2022. Second, we discovered that the financial returns of all cryptocurrencies throughout the period exhibit volatility clustering, correlation, and generalized autoregressive conditional heteroskedasticity. Third, whether in the stock market, bond market, commodities market, derivatives market, or cryptocurrency market, foreign investors have used a variety of products and techniques. Therefore, the research results provide comprehensive data for global investors to meet their strategic needs concerning investments in the crypto industry.

Section 2 examines what has already been written on the subject of volatility modeling in cryptocurrency markets.

Section 3 contains a brief summary of the data and methods used.

Section 4 presents the analytical findings.

Section 5 provides the discussion and

Section 6 concludes with some final thoughts.

2. Literature Review

Some people are interested in cryptocurrencies such as Bitcoin and Ethereum not because they want to use them as a medium of exchange, but rather because they see them an insurance policy against inflation or as a means of making a profit. Nevertheless, because there is no underlying commodity to underpin crypto (

Smith 2021), its market value depends entirely on speculation (

Hur et al. 2015) and informed guessing (

Tarr 2018). Putting money into a risky investment is a specific method to increase portfolio volatility (

Kallberg et al. 1996;

Roques et al. 2006). In other words, the investment’s price is susceptible to even little changes in investors’ expectations or perceptions because the value is not exceptionally stable (

Alti 2003). As with a hot air balloon trip, the view from the top is nice (

Finkle 2019), but once investors realize that it is just floating in the air, they will be glad to dismount the ride (

Lynch and Rothchild 2000). However, what rises up in the world of speculation typically comes crashing down.

Many people have a negative impression of volatility (

Merkle 2018;

Schwert 2002) because of its bad associations with market turmoil (

BenSaïda 2017), uncertainty (

Arnold and Vrugt 2008), and financial loss (

Arnold and Vrugt 2008). Price volatility increases when markets see large ups and downs because investors and traders are more likely to make wagers on the assumption that the trend will continue (

Covel 2006). The good news is that dramatic price fluctuations like this are uncommon (

Blau 2017). Every day, we see market action that is consistent with healthy volatility (

Barndorff-Nielsen and Shepard 2002). Price fluctuations occur as a result of the reactions of buyers and sellers to new information and events about specific firms, industries, and the general economic climate (

Weske 2013). Investors and traders analyze market circumstances and make buying and selling decisions based on their expectations of the impact of various variables on asset values (

Goldstein et al. 2013). Those who keep tabs on the cryptocurrency market will tell you that the volatility of cryptocurrencies is unprecedented (

Sensoy et al. 2021). Although there are currently no indexes that track the ups and downs of cryptocurrency prices, it just takes a brief look at the charts to notice that cryptocurrency values tend to soar higher and fall lower than those of other assets on the market. Many of the same factors that cause price fluctuations in traditional markets are also at play with cryptocurrencies (

Walther et al. 2019). Cryptocurrency and traditional market price fluctuations are both driven by news and speculation (

Ciaian et al. 2016).

Nevertheless, because crypto markets lack a healthy ecosystem of institutional investors and huge trading businesses, their influence is exacerbated in crypto markets, which have less liquidity than conventional financial markets (

Gomber et al. 2018). Because of their mutual reinforcement, high volatility and low liquidity are a potentially lethal mix (

Schar and Berentsen 2020). Like Bitcoin, most altcoins need more time to develop and gain traction in the market for derivatives (

Back et al. 2014). Cryptocurrency values, subject to the whims of day traders and speculators, may display the same healthy volatility seen in traditional markets (

Golić 2020).

However, the volatility of cryptocurrency markets is decreasing (

Vejačka 2014). As the crypto market develops and expands, institutional investors and trading organizations are increasing their commitment to the asset class, and a future market for cryptocurrencies is taking form (

Giudici et al. 2020).

It remains to be seen whether crypto volatility will ultimately follow the same trends as volatility in traditional markets (

Baur and Dimpfl 2021). However, until the asset class achieves full maturity in the far future, it is expected to continue, consistently exhibiting outsized volatility (

Poon and Granger 2003).

Bitcoin’s value has dropped by more than half since April 2021, from almost USD 45,000 to roughly USD 20,000 (

DataQuest 2021). Other cryptocurrencies have seen much worse declines (

Kumar 2022). There was a total loss of USD 60 billion due to the collapse of the Terra–UST ecosystem in May 2022 (

Sigalos 2022). This ecosystem combined a cryptocurrency with one supposed to be linked to the dollar. Well-known crypto exchanges, such as Coinbase, have announced staff reductions (

Chaturvedi 2022).

Amid the chaos, crypto critics have ramped up their criticisms (

Bhatnagar et al. 2022), focusing mainly on speculative excess and arguing that the crisis has exposed crypto as a Ponzi scheme (

Vasek and Moore 2019). Some point to the high degree of volatility as proof (

Cermak 2017;

Pryzmont 2016;

Fang et al. 2019). How could crypto deliver on its promise if involvement is like riding an unsafe rollercoaster (

Sharma 2021)? While part of the criticism is warranted, it is less compelling an argument than the concentration on price volatility may suggest (

Lesser 2019). Instead, it shows that investors must fully comprehend what various tokens should stand for in the cryptocurrency market (

Lee et al. 2018). The cryptocurrency market is still in its infancy (

Pechman 2022). Although their ultimate purposes will vary, all coins operate essentially as a startup stock with the added benefits of instantaneous liquidity and transparent pricing (

Gazali et al. 2018;

Sukumaran et al. 2022). This one-of-a-kind feature, made possible by new underlying architecture, helps provide a kinder rationale for the volatility.

In the financial market time series, asymmetry in the volatility process in response to shocks is notable (

Ibrahim 2020). The leverage effect describes the tendency for bad news to have a significantly larger impact on the conditional variance of stock returns than good news (

Marquering and de Goeij 2005). As digital currencies have gained popularity, so has the body of research comparing their volatility qualities to those of conventional financial instruments (

Sapuric et al. 2020). The GARCH model is the most effective model used to measure crypto-associated volatility (

Naimy et al. 2021).

The results show an asymmetric impact upon the application of the TGARCH model, in which volatility rises more in reaction to positive shocks than to negative ones, suggesting a pattern of behavior not often seen in stock markets. Uninformed investors’ herding methods may be to blame for the rise in volatility, which has been interpreted as a reaction to positive shocks (

Fakhfekh and Jeribi 2020).

Previous studies shows that Bitcoin, in terms of price, liquidity, and volatility, has some sharing features of other global cryptocurrencies. However, Bitcoin is measured as a highly volatile asset of its class (

Haiss and Schmid-Schmidsfelden 2018).

The GARCH model shows that Bitcoin’s volatility had a statistically significant effect on Ethereum’s and Litecoin’s volatility across the study period. There may be some mild return co-movement across cryptocurrencies, as shown by the conditional correlation metrics in the given research (

Kumar and Anandarao 2019).

A study was conducted to measure the effect of crypto volatility on market return. In the research, using the standard deviation of log values of return, volatility measurements were conducted and high levels of volatility were measured. Hence, Bitcoin is suggested to be suitable for high-risk-endeavor investors (

Almagsoosi et al. 2022).

A VCRIX (volatility index for cryptocurrencies) approach based on the heterogeneous autoregressive (HAR) model was employed for volatility-based forecasting. In the absence of a mature crypto derivatives market, VCRIX fills this gap by providing forecasting capabilities and by acting as a proxy for the expectations of investors. These additions improve the capabilities of monitoring markets, developing trading strategies, and maybe determining the value of options (

Kim et al. 2021).

When analyzing the symmetric and asymmetric information on cryptocurrencies, it was discovered that the return on, or volatility in, the Bitcoin market is symmetrically informative and has a long memory to endure in the future. More so than the fresh shock of market prices, sympatric volatility is observed to be more sensitive to historical values (lagged) (

Othman et al. 2019).

4. Results

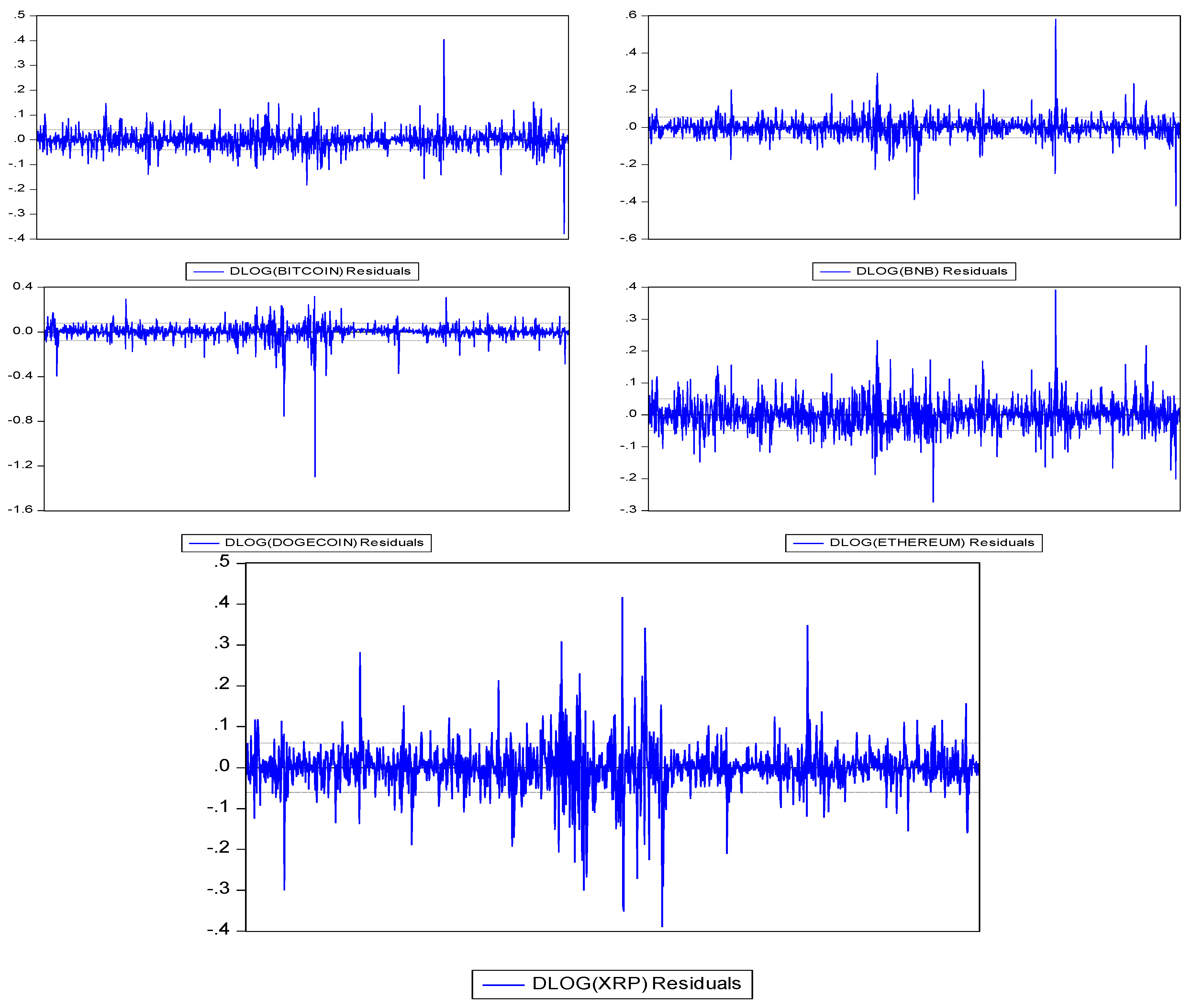

Table 1 incorporates descriptive statistics of the percentage of daily returns. Every statistical parameter mentioned in the table is significant, but the values of maximum loss/gain or minimum loss/gain are quite insightful. Dogecoin shows a maximum loss of 73.7741%, followed by BNB, XRP, Bitcoin, and Ethereum. If you look at the biggest gain in a day, it was 70.2987% for dogecoin, followed by BNB, XRP, Bitcoin, and Ethereum in that order.

Table 3 incorporates the application of ARMA maximum likelihood (OPG − BHHH) on 1291 observations on the returns of the top cryptocurrencies globally. The time-series analyses of the dataset formulated contains the coefficient of covariance computed employing the outer product of gradients. Considering Bitcoin, R-squared shows a value of 0.53 on the application of the ARMA model. The values were obtained on inverted AR roots of −0.5 and inverted MA roots of 1.00. Moreover, the R-squared value of BNB was 0.525070, calculated on inverted AR roots of −0.6 and inverted MA roots of 0.99. Convergence was achieved on BNB after 63 iterations. ARMA modeling also assessed the log returns of Dogecoin on inverted AR roots of −0.08 and inverted MA roots of 0.99. Convergence was achieved in Dogecoin after 121 iterations. Ethereum shows 0.515613 as the value of R-squared, which achieved convergence after 98 iterations on inverted AR roots of −0.03 and inverted MA roots of 1.00. Lastly, the cryptocurrency of XRP showed the second largest R-squared valued on an ARMA application of 0.530665. However, the log returns of XRP exhibited failure to improve non-zero gradients after 71 iterations.

After ARMA, the next step was to check autoregressive conditional heteroskedasticity (ARCH).

Table 4 contains calculations relating to heteroskedasticity, exhibiting F-statistic values, observed R-squared values, and probability values. Probability in the table is based on F-statistics which follow F(k, n − k − 1) distribution. With the exception of Bitcoin, all cryptocurrencies showed significant

p-values as they were less than 0.05. This signifies that after the application of E-GARCH on the framed dataset, there is a high probability that the employed model will not show reliable results for Bitcoin. However, because four out of five currencies showed a positive sign with statistically significant values, it suitable for further analyses. Moreover, the value of R-squares in ARMA modeling was more than 0.5 (

Table 3). Hence, further parameters can be applied to Bitcoin as well.

Table 5 comprises the heteroskedasticity test. ARCH statistics were calculated using RESID

2 as the dependent variable. The analysis is based upon the adjusted sample size of 1292 observations, which changed to 1289 observations after adjustments. The method of least squares was applied to the test to make interpretations.

Table 6 contains the statistics related to

p-values to testify to the significance of the variables and coefficients in the E-GARCH model. C(5), C(6), and C(7) signify size effect, sign effect, and GARCH effect, respectively. From the table, it can be deciphered that AR(1) has a statistically significant result in the case of Dogecoin and XRP only. In comparison, MA(1) shows statistically significant values across all the coins. Moreover, C(5) and C(7) show significant results across all cryptocurrencies. A further assessment based on the E-GARCH statistics concerning the regression variables is made in upcoming sections of the research.

By considering the dependent variable as a log of returns in cryptocurrencies,

Table 7 employs ML ARCH–Student’s t distribution (OPG–BHHH/Marquardt steps). The model runs on an adjusted sample of 1292 observations, including 1290 observations after adjustments.

Coefficient covariance was computed using the outer product of gradients to calculate the regression statistics of the E-GARCH estimations. The calculations in the table are based upon the following:

Table 8 shows the beta coefficient analysis of the EGARCH return (%) application.

5. Discussion

In

Table 8, the value of the size effect of all currencies is statistically significant, which shows that news has a significant impact on volatility. Moreover, volatility persistence was found to be very high and statistically significant in all cryptocurrencies. The high value of volatility persistence signifies that if the market is volatile, it remains volatile for a long time. Considering the sign effect, for Dogecoin there is a positive sign effect, whereas all the other currencies have a negative sign effect. A negative sign effect indicates an inverse relationship between error (

) and

. This signifies that positive information can decrease volatility and negative information can increase volatility. However, the sign effect is significant in the case of only two currencies, i.e., BNB and Dogecoin.

When compared to a similar study conducted during COVID-19 using E-GARCH on cryptocurrencies, it was discovered that the sign effect was significant across the sample. However,

Yang et al. (

2023) used the daily historical closing prices of cryptocurrencies, such as Bitcoin, Ethereum, Ripple, and Cardano, from 2019 to 2020 in their study, whereas we looked at five currencies with a larger market cap over a longer period of time in our study. Furthermore, our study focused on how the news (shocks) affect cryptocurrency market volatility, whereas

Yang et al. (

2023) investigated the correlations between cryptocurrency return volatility, global stock market indices, and the COVID-19 pandemic’s spillover effects.

Gupta and Chaudhary (

2022) also investigated the performance of Bitcoin, Ethereum, XRP, and Litecoin over a 5-year and 6-month period using the GARCH model family. However, when the data analyses measured volatility based on returns of 1 year only, the currency of XRP showed a positive sign effect, unlike the present research (

Gupta and Chaudhary 2022). This signifies that investors in XRP respond negatively in the long run to any adverse news regarding the given currency.

The primary demand for cryptocurrency right now is speculation, and its price is subject to wild swings (

Qi et al. 2020). Because Bitcoin is decentralised, it is impossible to keep tabs on it, which raises the investment risk (

Lee et al. 2018). As a result, traders should exercise extreme caution when trading in the crypto market (

Gandal et al. 2018). Investors should keep their eyes on companies represented by blockchain concept stocks (

Lee and Lee 2016). Therefore, despite the fact that the stocks based on the blockchain idea are rapidly increasing, they are not a good choice for rapidly moving up in the rankings (

Atzori 2017). When evaluating potential investment possibilities, it is important to consider the level of development of the underlying medium to long-term technology, the strength of the driving force, and the magnitude of the benefits to the relevant businesses (

Wheelwright 1984). There is also a cap on the value of “blockchain idea stocks” (

Al-Shaibani et al. 2020), which is an important consideration. Many retail investors become involved with blockchain idea stocks (

Gupta and Shrivastava 2021), such as Bitcoin and Ethereum, before they have a firm grasp of the technology’s underlying fundamentals (

Zachariadis et al. 2019). Before investing in cryptocurrency, investors must conduct due diligence and understand all aspects of the cryptocurrency, including its potential risks and rewards.

According to the current study, the prices of the most widely traded cryptocurrencies respond significantly to shocks i.e., news. While many people are intrigued by cryptocurrencies, others are skeptical due to price volatility. This is evidenced by the fact that the GARCH term has significant value in all five cryptocurrencies. This indicates that volatility remains for a long time in the crypto market. As such, if an investor does not like fluctuations, they can invest in the DAX Performance Index or the Dow Jones Industrial Average Index, which gauges low and insignificant volatility persistence in related research (

Yang et al. 2023), unlike crypto.

6. Conclusions

Cryptocurrency markets are volatile and can be influenced by a variety of factors, such as changing regulations, liquidity issues, technical issues, and market sentiment. As a result, investors should be aware that the value of their investments can fluctuate dramatically, resulting in significant losses or gains. Some people are interested in cryptocurrencies not as a means of exchange, but as a good inflation hedge or an attractive investment vehicle. However, as there are no underlying assets to support the value of crypto, its market value is dependent entirely on speculation. Furthermore, before investing in cryptocurrency, investors should always make sure they understand the risks involved.

This study has limitations in that we investigated only 5 currencies out of over 20,000. It would be interesting to delve deeper into the correlations between these currencies. Furthermore, stochastic volatility methods could be used to improve out-of-sample forecasting power. Furthermore, as our crypto return predictions were calculated using past prices, these projections might be surpassed by market fluctuations or other unforeseen economic developments. Furthermore, the univariate GARCH model has been used in our price-forecasting efforts. Applying multivariate GARCH models, which take into account the micro and macroeconomic factors that influence cryptocurrency demand on the global market, might be a promising avenue for further study.

{kind=link}

{kind=link}

{kind=link}