Attaining Standardization in Islamic Banking Institutions in Pakistan: Analysis on Ijarah Financing

,

,

Abstract

:1. Introduction

- (1)

- Do Islamic banks in Pakistan comply with the AAOIFI Shariah Standards on Ijarah financing?

- (2)

- What problems/obstacles (if any) do Islamic banks in Pakistan face in complying with the requirements of the AAOIFI Shariah Standards on Ijarah financing?

- (3)

- How do problems and/or obstacles (if any) faced by Islamic banks in Pakistan resolved to correspond with the AAOIFI Shariah Standards on Ijarah financing?

1.1. Ijarah Financing

- The ownership of an Ijarah asset vests with the lessor, whereas the usufruct remains with the lessee during the Ijarah period.

- The period of the Ijarah contract should be expressed in clear terms.

- A thing which is consumed after usage cannot become the subject matter of Ijarah contract, e.g., food stuff, money, oil, etc.

- The Ijarah asset should be used in the manner specified in the Ijarah contract. If nothing is mentioned in the contract, the Ijarah asset shall be used in accordance with the usage of trade.

- If something bad happens with the Ijarah asset, i.e., if the Ijarah asset is destroyed and loses its intended purpose, then the Ijarah contract stands terminated and the lessor shall bear the entire loss, being the owner of the asset, provided that there is no negligence on the part of the lessee.

- Ownership-related expenditure shall be borne by the lessor, whereas usage-related expenditure shall be borne by the lessee.

- The rentals of the Ijarah asset should be certain, leaving no uncertainty.

- Ijarah rentals should be specified at the time of the Ijarah contract for the whole period.

- Lessor cannot increase the rentals unilaterally without the mutual consent of the lessee.

- If the rent of the subsequent period is not set in advance, the lease stands invalid.

- First year/period rentals should be determined in clear terms; however, subsequent years’ rental may be linked with conventional benchmark provided that the ceiling and floor are set to avoid Gharar kaseer (major uncertainty).

- The Ijarah period shall commence and rentals shall start after the usufruct is made available to the lessee.

- Future Ijarah is permissible, provided that the asset is in existence.

1.2. Brief Account on AAOIFI Standard 9 on Ijarah Financing

2. Literature Review

- The Islamic bank buys a car, say for example INR 2 million, and rents it out to the customer. The amount of total rent that the customer is bound to pay is INR 2.5 million. Thus, an additional 0.5 million is not the rent in its real sense; rather, it is prohibited interest because Ijarah rentals are benchmarked with KIBOR.

- In the contemporary Ijarah transactions of Islamic banks, it is the customer who selects and buys a car from the open market; thus, the Islamic bank deals in paper only, and not in the actual buying of a car.

- While calculating the rent, Islamic banks take into account the element of time taken by the customer to repay the financing amount; thus, effectively, Islamic banks experience the benefit of the time value of money which is forbidden in Islamic Jurisprudence.

- While buying a car from the open market through the customer, Islamic banks bear all the direct and indirect expenses; however, they inculcate the same in Ijarah rentals, which is not allowed in the Shariah viewpoint.

- Islamic banks, after buying a car, do not receive insurance cover from takaful operators; rather, insurance cover is obtained through conventional insurance companies which is forbidden according to the teachings of Islam.

- If the customer delays the payment of rentals, Islamic banks can impose a penalty which is also not allowed in Islam.

3. Methodology

4. Data Analysis, Discussion, and Findings

“A house or chattel may not be leased for the purpose of an impermissible act by the lessee, such as leasing premises to an institution dealing in interest or to a shopkeeper for selling or storing prohibited goods, or leasing a vehicle to transport prohibited merchandise”.

The basis for the requirement that benefit from Ijarah must be permissible is that leasing an asset that will be used in impermissible way makes the lessor an accomplice in doing evil and this is prohibited as per the saying of Allah, the Almighty “[Help ye one another in righteous and piety]9”

“If the purpose of leased asset and contract are correct in Shariah viewpoint, it does not any difference if counterparty is conventional bank”.

“We can finance the car to conventional insurance companies but not the office equipment because office equipment is directly used to facilitate impermissible business but not the vehicle”.

“We don’t provide Ijarah financing to conventional banks because they will use it for facilitation of the conventional banks”.

“No, in accordance with our bank’s compliance regulations, it’s not allowed”.

“There shall be zero acceptability for Shariah non-compliant businesses”.

“The lessor may take out permissible insurance on it whenever possible and may also delegate to the lessee the task of taking out insurance at the lessor’s expense”.

“We prefer to have takaful but when corporate customer wants us to do conventional insurance then in case need we go for conventional insurance”.

“In consumer Ijarah, takaful is 100%, but in corporate, there is 30% takaful and 70% conventional insurance cover”.

- Sometimes, corporate customers received a pre-settled arrangement with the conventional insurance, thus rejecting takaful.

- When the risk exposure is high and the takaful operator is not willing to cover the entire risk, Islamic banks take insurance cover from conventional insurance companies.

- Islamic banks take insurance cover in case of a dire need for instance when it is compulsory for the regulator to take insurance cover from a conventional insurance company.

- Awareness programs regarding takaful operations may be initiated for the corporate customers so that they would not demand for conventional insurance from Islamic banks.

- Every conventional insurance company must have one exclusive wing for takaful operations.

- The SBP develops such policies so that the proportion of takaful operators in the insurance sector may be augmented.

5. Conclusions and Recommendations

“Do not help each other in acts of sinfulness and transgression”.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

| Country | IFDI Value |

|---|---|

| Malaysia | 111 |

| Indonesia | 72 |

| Bahrain | 67 |

| United Arab Emirates | 66 |

| Saudi Arabia | 64 |

| Jordan | 53 |

| Pakistan | 51 |

| Oman | 45 |

| Kuwait | 43 |

| Qatar | 38 |

| Brunei Darussalam | 36 |

| Maldives | 34 |

| Nigeria | 32 |

| Sri Lanka | 30 |

| Syria | 23 |

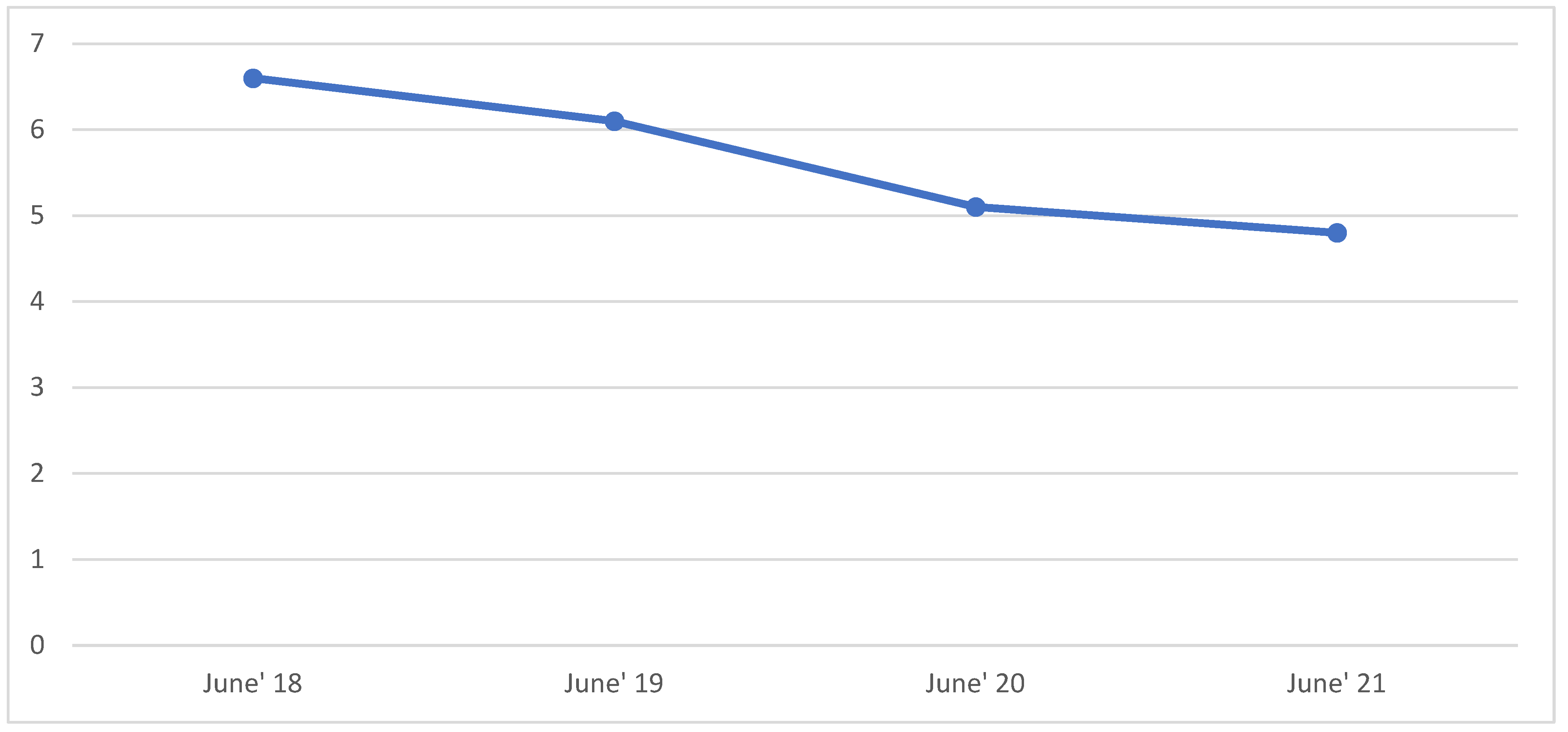

| June’ 18 | June’ 19 | June’ 20 | June’ 21 | % Decrease (From June’ 18 to June’21) |

|---|---|---|---|---|

| 6.6 | 6.1 | 5.1 | 4.8 | 27.3% |

| Full-Fledged Islamic Banks in Pakistan |

|---|

| Meezan Bank Limited |

| Dubai Islamic Bank |

| Bank Al-Barakah Limited |

| Bank Islamic Limited |

| MIB Islamic Bank |

| Clause in Which Deviation Is Explored | Codes from Interviewee’s Responses | Theme | |

|---|---|---|---|

| Clause No 5/1/1—Usage of Ijarah Asset | Interviews: 10 | Codes: 10 | Two (2) out of five (5) Islamic banks undertake Ijarah contract with conventional insurance companies |

| Yes, we do | |||

| Yes, we undertake Ijarah contract with conventional insurance companies | |||

| If the purpose of leased asset and contract are correct in Shariah viewpoint, then if counterparty is conventional bank, it does not make any difference. | |||

| Yes, our bank finance to conventional insurance companies | |||

| I don’t think so that we finance our asset to conventional insurance companies | |||

| We have not such practice till now | |||

| No, not to conventional banks but to conventional insurance companies | |||

| We don’t do it | |||

| No, in accordance with our compliance regulations, it’s not allowed | |||

| We don’t finance to conventional banks and conventional insurance companies | |||

| Clause in Which Deviation Is Explored | Codes from Interviewee’s Responses | Theme | |

|---|---|---|---|

| Clause No 5/1/8—Takaful | Interviews: 10 | Codes: 10 | In corporate Ijarah, Islamic banks take insurance cover from both the conventional insurance companies and takaful operators |

| If the need arises then we also take conventional insurance cover too | |||

| In majority of the cases we take takaful unless there is dire need | |||

| We always go for takaful but in case of need we do take conventional insurance | |||

| 100 percent takaful in consumer Ijarah but we take conventional insurance cover in corporate Ijarah | |||

| In consumer 100% but in corporate there is 30% is takaful and 70% of conventional | |||

| Yes whenever there is a Ijarah asset, we do takaful but in exceptional cases we also go for conventional insurance | |||

| We always go for takaful but when the customer insist we also go for conventional insurance | |||

| 100% takaful | |||

| We prefer to have takaful but when corporate customer want us to do conventional then in case need we do so | |||

| In vehicles there is a 100% takaful. But if the exposure is high then we go for conventional insurance | |||

| 1 | For details, please see page no: 4 of the Islamic Finance Outlook-2019 Edition by S&P Global Rating |

| 2 | See Paragraph No: 3 of IBD Circular No: 1 dated 1 January 2010 at http://www.sbp.org.pk/ibd/2010/C1.htm; (accessed on 5 November 2021) |

| 3 | Second meeting: 22–23 October 1999; Third meeting: 18-22 December 1999; Fourth meeting: April 26-28, 2000; Fifth meeting: 29–31 May 2000; Sixth meeting: 24–28 November 2001 and 11–16 May 2002. |

| 4 | See Paragraph No: 5 of IBD Circular No: 1 dated 1 January 2010 at http://www.sbp.org.pk/ibd/2010/C1.htm; (accessed on 5 November 2021) |

| 5 | Minor uncertainty within the clauses of transaction that does not lead to dispute. |

| 6 | The problem of adverse selection arises when, either of the buyer or seller, has more information than the other. |

| 7 | For details, refer to Islamic Banking Bulletin of the State Bank of Bank (September 2020) |

| 8 | NVivo 9 (QSR International) |

| 9 | Surah al-Ma’idah, verse 2. |

References

- Belwal, Rakesh, and Ahmed Al Maqbali. 2019. A study of customers’ perception of Islamic banking in Oman. Journal of Islamic Marketing 10: 150–67. [Google Scholar] [CrossRef]

- Dakhlallah, Kassim, and Hela Miniaoui. 2011. Islamic Banks vs. Non Islamic Ethical Dimensions. Available online: https://ro.uow.edu.au/dubaipapers/221/ (accessed on 11 February 2021).

- DeLorenzo, Yusuf Talal. 2007. The Total Returns Swap and the ‘Shari’ah Conversion Technology’Stratagem. Available online: https://www.semanticscholar.org/paper/The-Total-Returns-Swap-and-the-%22-Shariah-Conversion-DeLorenzo/15a52194d357bbb0ec7575c2cdb8a6e8a1c388d0 (accessed on 25 June 2021).

- Grummitt, Janis. 1980. Interviewing, Communication Skills Guides. London: Industrial Society Press. [Google Scholar]

- Hanif, Muhammad. 2014. Differences and Similarities in Islamic and Conventional Banking. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1712184 (accessed on 19 December 2020).

- Haqqi, Aji Raden Abdurrahman. 2014. Shariah governance in Islamic financial institution: An appraisal. US-China L. Rev. 11: 112. [Google Scholar]

- Haridan, Nurfarahin Muhammad, Ahamd Hassan, and Yusuf Karbhari. 2018. Governance, religious assurance and Islamic banks: Do Shariah boards effectively serve? Journal of Management and Governance 22: 1015–43. [Google Scholar] [CrossRef]

- Haseeb, Muhammad. 2018. Emerging issues in islamic banking & finance: Challenges and Solutions. Academy of Accounting and Financial Studies Journal 22: 1–5. [Google Scholar]

- Holden, Kelly. 2007. Islamic finance: Legal hypocrisy moot point, problematic future bigger concern. BU Int’l LJ 25: 341. [Google Scholar]

- IBD. 2021. Islamic Banking Bulletin. IBD. Available online: http://www.sbp.org.pk/ibd/bulletin/2021/June.pdf (accessed on 15 December 2021).

- Iqbal, Munawar, and Philip Molyneux. 2016. Thirty Years of Islamic Banking: History, Performance and Prospects. Berlin and Heidelberg: Springer. [Google Scholar]

- Kahf, Monzer. 2004. Success Factors of Islamic Banks. Paper presented at the Brunei Symposium on Islamic Banking and Finance, Brunei, January 5–7. [Google Scholar]

- Khan, Tahreem Noor. 2018. Need of elevating the role of shariah board and portraying them significantly on Islamic bank websites: Why and how? Journal of Emerging Economies & Islamic Research 6: 2–77. [Google Scholar]

- Lee, Kin Ho, and Shakirullah Ullah. 2011. Customers’ attitude toward Islamic banking in Pakistan. International Journal of Islamic and Middle Eastern Finance and Management 4: 131–45. [Google Scholar] [CrossRef]

- Mansoor Khan, Muhammad, and Muhammad Ishaq Bhatti. 2008. Development in Islamic banking: A financial risk-allocation approach. The Journal of Risk Finance 9: 40–51. [Google Scholar] [CrossRef]

- Masruki, Rosnia, Mustafa Muhammad Hanefah, and Bablu Kumar Dhar. 2020. Shariah Governance Practices of Malaysian Islamic Banks in the Light of Shariah Compliance. Asian Journal of Accounting and Governance 13: 91–97. [Google Scholar]

- McLellan, Eleanor, Kathleen MacQueen, and Judith Neidig. 2003. Beyond the qualitative interview: Data preparation and transcription. Field Methods 15: 63–84. [Google Scholar] [CrossRef]

- Miles, Matthew, and Micheal Huberman. 1984. Qualitative Data Analysis. London: Beverly Hills. [Google Scholar]

- Musa, Hussam, Viacheslav Natorin, Zdenka Musova, and Pavol Durana. 2020. Comparison of the efficiency measurement of the conventional and Islamic banks. Oeconomia Copernicana 11: 29–58. [Google Scholar] [CrossRef]

- Musa, Hussam, Zdenka Musova, Viacheslav Natorin, George Lazaroiu, and Martin Martin Boda. 2021. Comparison of factors influencing liquidity of European Islamic and conventional banks. Oeconomia Copernicana 12: 375–98. [Google Scholar] [CrossRef]

- Narayan, Paresh Kumar, and Dinh Hoang Bach Phan. 2019. A survey of Islamic banking and finance literature: Issues, challenges and future directions. Pacific-Basin Finance Journal 53: 484–96. [Google Scholar] [CrossRef]

- Ouerghi, Feryel. 2014. Are Islamic banks more resilient to global financial crisis than conventional banks? Asian Economic and Financial Review 4: 941. [Google Scholar]

- Perveen, Abida. 2018. Does an Islamic Label Indicate Good Corporate Governance? Islamabad: Capital University. [Google Scholar]

- Rabbani, Mustafa Raza, and Shahnawaz Khan. 2020. Agility and fintech is the future of Islamic finance: A study from Islamic banks in Bahrain. International Journal of Scientific and Technology Research. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3783171 (accessed on 21 June 2021). [CrossRef]

- Raza, Muhammad Wajid, Syed Farhan Shah, and Malik Rizwan Khurshid. 2011. Islamic Banking Controversies and Challenges. Available online: https://mpra.ub.uni-muenchen.de/70623/ (accessed on 18 September 2020).

- S&P. 2019. Islamic Finance Outlook. Available online: https://www.spratings.com/documents/20184/984172/Islamic+Finance+2019+Digital.pdf/ca3ed020-a5d5-d01d-14be-ddc828516cd6 (accessed on 22 May 2021).

- Saleem, Shujaat, and Fadillah Mansor. 2020. Exploring compliance of AAOIFI shariah standard on ijarah financing: Analysis on the practices of Islamic banks in Malaysia. Journal of Risk and Financial Management 13: 29. [Google Scholar] [CrossRef] [Green Version]

- Salman, Asma, Huma Nawaz, Syed Muhammad Hassan Bukhari, and Abou Baker. 2018. Growth analysis of Islamic banking in Pakistan: A qualitative approach. Academy of Accounting and Financial Studies Journal 22: 1–8. [Google Scholar]

- Saqib, Luftullah, Muhammad Aitisam Farooq, and Aliya Muneer Zafar. 2016. Customer perception regarding Sharī ‘ah compliance of Islamic banking sector of Pakistan. Journal of Islamic Accounting and Business Research 7: 282–303. [Google Scholar] [CrossRef]

- Saunders, Mark, Lewis Thornhill, and James Wilson. 2009. Business Research Methods. Financial Times. London: Prentice Hall. [Google Scholar]

- Sejiny, Aiman. 2019. Islamic Finance Development Report. Available online: https://www.zawya.com/ifg-publications/report/20191205080154949.pdf/?refKey=IFG-3ab1d3df-09e9-4f10-86e9-b2c499142d58 (accessed on 21 May 2021).

- Shaikh, Salman Ahmed. 2013. Islamic Banking in Pakistan: A Critical Analysis. Available online: https://platform.almanhal.com/Files/Articles/40087 (accessed on 11 May 2022).

- Shiyuti, Hashim, Delil Khairat, Mahamat Mourtada, and Muhammad Ghani. 2012. Critical Evaluation on Al-Ijarah Thummalbai’. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2184296 (accessed on 11 May 2022).

- Siddique, Zahid, and Muhammad Iqbal. 2017. Theory of Islamic Banking: From Genesis to Degeneration. Available online: https://www.torrossa.com/en/resources/an/3187144 (accessed on 22 August 2021).

- Usmani, Muhammad Taqi. 2002. An Introduction to Islamic Finance. Highwood: Brill, vol. 20. [Google Scholar]

- Wilson, Rodney. 1994. Development of Financial Instruments in an Islamic Framework. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3167673 (accessed on 13 May 2021).

- Zubair, Hafiz Muhammad, and Nadeem Chaudhary. 2014. Islamic banking in Pakistan: A critical review. International Journal of Humanities and Social Science 4: 161–76. [Google Scholar]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Saleem, S.; Baig, U.; Meidute Kavaliauskiene, I.; Ul Hassan, M.; Mansor, F. Attaining Standardization in Islamic Banking Institutions in Pakistan: Analysis on Ijarah Financing. J. Risk Financial Manag. 2022, 15, 430. https://doi.org/10.3390/jrfm15100430

Saleem S, Baig U, Meidute Kavaliauskiene I, Ul Hassan M, Mansor F. Attaining Standardization in Islamic Banking Institutions in Pakistan: Analysis on Ijarah Financing. Journal of Risk and Financial Management. 2022; 15(10):430. https://doi.org/10.3390/jrfm15100430

Chicago/Turabian StyleSaleem, Shujaat, Umair Baig, Ieva Meidute Kavaliauskiene, Mehboob Ul Hassan, and Fadillah Mansor. 2022. "Attaining Standardization in Islamic Banking Institutions in Pakistan: Analysis on Ijarah Financing" Journal of Risk and Financial Management 15, no. 10: 430. https://doi.org/10.3390/jrfm15100430