Does Environmental Credit Rating Promote Green Innovation in Enterprises? Evidence from Heavy Polluting Listed Companies in China

Abstract

:1. Introduction

2. Literature Review and Hypothesis Development

2.1. Research on ECR

2.2. ECR and Green Innovation

2.3. The Impact Mechanism of ECR on Green Innovation

2.3.1. Reputation Mechanism

2.3.2. Financing Mechanism

3. Research Design

3.1. Samples and Data

3.2. Variables and Model

3.2.1. Variable Introduction

3.2.2. Model Specification

4. Empirical Analysis

4.1. Benchmark Regression Analysis

4.1.1. Benchmark Regression Results

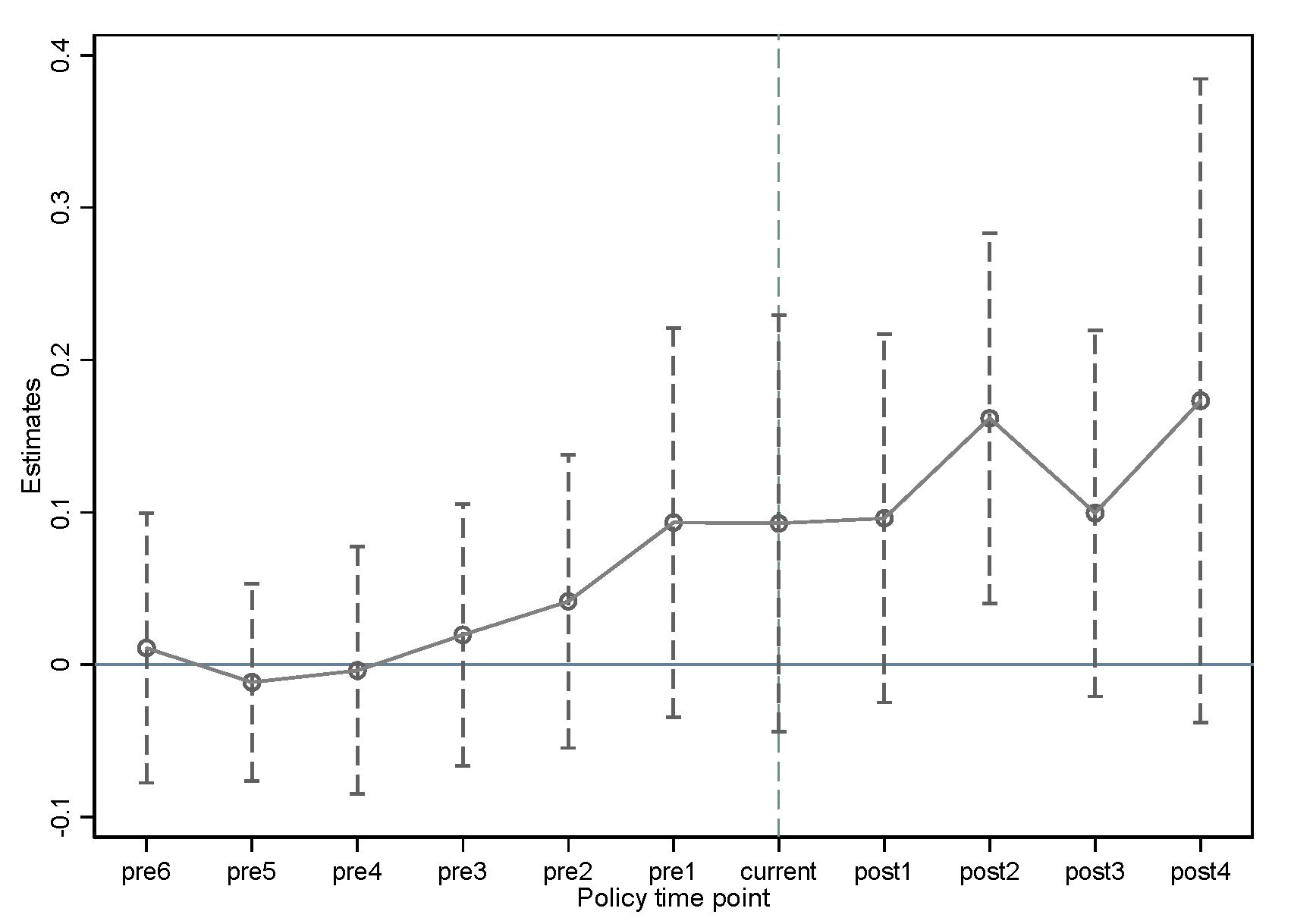

4.1.2. Parallel Trend Test and Dynamic Effect Analysis

4.2. Robustness Check

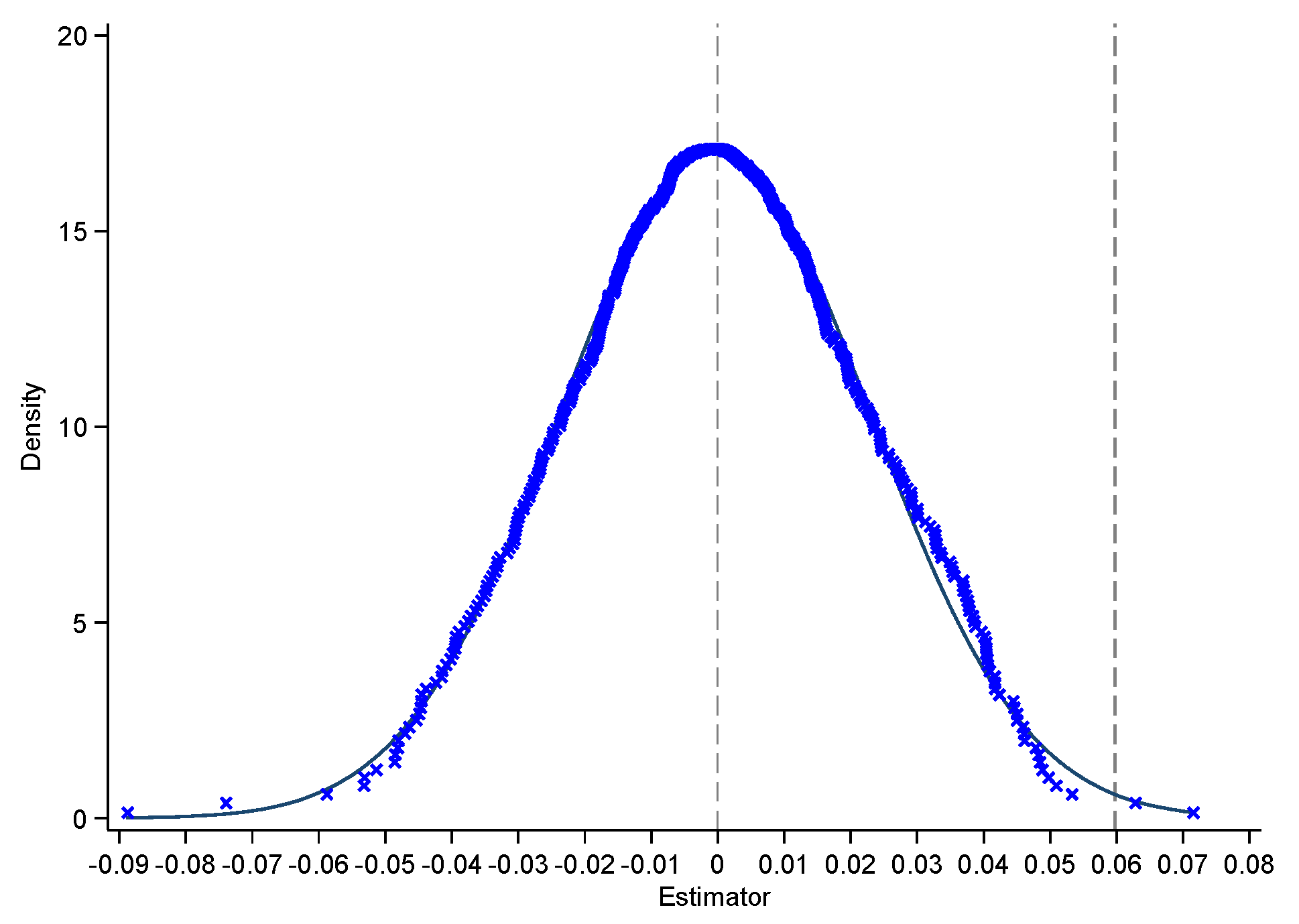

4.2.1. Placebo Test

4.2.2. Counterfactual Test

4.2.3. Change How Green Innovation Is Measured

4.2.4. Delete the Disputed Samples

4.2.5. Consider Possible Missing Variables

4.3. Mechanism Analysis

4.3.1. Reputation Mechanism

4.3.2. Financing Mechanism

5. Heterogeneity Analysis

5.1. Heterogeneity Effects of Enterprise Characteristics

5.1.1. Heterogeneity of Size

5.1.2. Heterogeneity of Ownership

5.2. Heterogeneity Effects of Regional Characteristics

5.2.1. Heterogeneity of Different Financial Development Levels

5.2.2. Heterogeneity of Different Fiscal Pressure Levels

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Rugman, A.M.; Verbeke, A. Corporate strategies and environmental regulations: An organizing framework. Strateg. Manag. J. 1998, 19, 363–375. [Google Scholar] [CrossRef]

- Li, Y.D. The identification of the liability of the Third party to control Secondary Environmental Pollution: An analysis from the perspective of the legal system of enterprise environmental credit Assessment. J. China Univ. Geosci. (Soc. Sci. Ed.) 2019, 19, 35–44, (In Chinese, Wuhan, China). [Google Scholar]

- Wang, L. The legitimacy of improving China’s legal system of enterprise environmental credit evaluation. Bus. Econ. Manag. 2019, 9, 88–96, (In Chinese, Hangzhou, China). [Google Scholar]

- Wang, R.X. Research on Environmental Credit Evaluation System from the Perspective of Public Law. Chin. Public Adm. 2020, 4, 125–129+152, (In Chinese, Beijing, China). [Google Scholar]

- Porter, M.E.; Van der Linde, C. Toward a new conception of the environment-competitiveness relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef] [Green Version]

- Jaffe, A.B.; Palmer, K. Environmental regulation and innovation: A panel data study. Rev. Econ. Stat. 1997, 79, 610–619. [Google Scholar] [CrossRef]

- Chen, J.; Wang, X.; Shen, W.; Tan, Y.; Matac, L.M.; Samad, S. Environmental uncertainty, environmental regulation and enterprises’ green technological innovation. Int. J. Environ. Res. Public Health. 2022, 19, 9781. [Google Scholar] [CrossRef]

- Johnstone, N.; Haščič, I.; Poirier, J.; Hemar, M.; Michel, C. Environmental policy stringency and technological innovation: Evidence from survey data and patent counts. Appl. Econ. 2012, 44, 2157–2170. [Google Scholar] [CrossRef] [Green Version]

- Wang, F.; Feng, L.; Li, J.; Wang, L. Environmental regulation, tenure length of officials, and green innovation of enterprises. Int. J. Environ. Res. Public Health. 2020, 17, 2284. [Google Scholar] [CrossRef] [Green Version]

- Brunnermeier, S.B.; Cohen, M.A. Determinants of environmental innovation in US manufacturing industries. J. Environ. Econ. Manag. 2003, 45, 278–293. [Google Scholar] [CrossRef]

- Greenstone, M.; List, J.; Syverson, C. The Effects of Environmental Regulation on the Competitiveness of U.S. Manufacturing; [NBER Working Paper]; National Bureau of Economic Research: Cambridge, MA, USA, 2012; Volume 18392, (In Chicago, IL, USA). [CrossRef] [Green Version]

- van Leeuwen, G.; Mohnen, P. Revisiting the Porter hypothesis: An empirical analysis of green innovation for The Netherlands. Econ. Innov. New Technol. 2017, 26, 63–77. [Google Scholar] [CrossRef] [Green Version]

- Chen, Z.; Zhang, X.; Chen, F. Do carbon emission trading schemes stimulate green innovation in enterprises? Evidence from China. Technol. Forecast. Soc. Chang. 2021, 168, 120744. [Google Scholar] [CrossRef]

- Kou, Z.L.; Zhang, Y.; Liu, X.Y. Does China’s credit rating really affect the cost of issuing bonds? J. Financ. Res. 2015, 10, 81–98, (In Chinese, Beijing, China). [Google Scholar]

- Wang, R.X. Environmental Credit Rating as a governance Tool Innovation. Lanzhou Acad. J. 2015, 1, 103–110, (In Chinese, Lanzhou, China). [Google Scholar]

- Tietenberg, T. Disclosure strategies for pollution control. Environ. Resour. Econ. 1998, 11, 587–602. [Google Scholar] [CrossRef]

- Berrone, P.; Fosfuri, A.; Gelabert, L.; Gomez-Mejia, L.R. Necessity as the mother of “green” inventions: Institutional pressures and environmental innovations. Strateg. Manag. J. 2013, 34, 891–909. [Google Scholar] [CrossRef]

- Yang, W.P.; Zhao, J.K. Does government. Environmental information disclosure contribute to the improvement of ecological and environmental quality? J. Econ. Manag. 2018, 8, 5–22, (In Chinese, Beijing, China). [Google Scholar]

- Hu, Z.Y.; Li, Y. Evaluation of pollution reduction Effect of environmental information Disclosure. J. Stat. Res. 2020, 4, 59–74, (In Chinese, Beijing, China). [Google Scholar]

- Wang, X.; Wang, Y. A study on the green innovation effect of environmental information disclosure: A quasi-natural experiment based on & LT; Ambient air quality standard & GT. J. Financ. Res. 2021, 10, 134–152, (In Chinese, Beijing, China). [Google Scholar]

- Wang, X.; Wang, Y. Green credit policy promotes green innovation research. J. Manag. World. 2021, 37, 173–188+11, (In Chinese, Beijing, China). [Google Scholar]

- Cai, W.; Li, G. The drivers of eco-innovation and its impact on performance: Evidence from China. J. Cleaner Prod. 2018, 176, 110–118. [Google Scholar] [CrossRef]

- Yu, X.; Xu, Y.; Zhang, J.; Sun, Y. The synergy green innovation effect of green innovation subsidies and carbon taxes. Sustainability 2022, 14, 3453. [Google Scholar] [CrossRef]

- Li, S.J.; Li, J.Q.; Zhang, Y.; Social Trust. Commercial credit financing and enterprise innovation. J. Nankai Econ. Res. 2020, 3, 81–102, (In Chinese, Tianjing, China). [Google Scholar]

- Cellini, R.; Lambertini, L.; Mantovani, A. Persuasive advertising under Bertrand competition: A differential game. Oper. Res. Lett. 2008, 36, 381–384. [Google Scholar] [CrossRef]

- Goss, A.; Roberts, G.S. The impact of corporate social responsibility on the cost of bank loans. J. Bank. Fin. 2011, 35, 1794–1810. [Google Scholar] [CrossRef]

- Dhaliwal, D.S.; Li, O.Z.; Tsang, A.; Yang, Y.G. Voluntary nonfinancial disclosure and the cost of equity capital: The initiation of corporate social responsibility reporting. Acc. Rev. 2011, 86, 59–100. [Google Scholar] [CrossRef]

- Ni, J.; Kong, L.W. Environmental information Disclosure, bank credit decisions and debt financing costs: Empirical evidence from listed companies in Shanghai and Shenzhen A-share Heavy polluting industries. Econ. Rev. 2016, 1, 147–156+160, (In Chinese, Wuhan, China). [Google Scholar]

- Iatridis, G.E. Environmental disclosure quality: Evidence on environmental performance, corporate governance and value relevance. Emerg. Mark. Rev. 2013, 14, 55–75. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Li, Y.; Richardson, G.D. The market valuation of environmental capital expenditures by pulp and paper companies. Acc. Rev. 2004, 79, 329–353. [Google Scholar] [CrossRef]

- Amore, M.D.; Bennedsen, M. Corporate governance and green innovation. J. Environ. Econ. Manag. 2016, 75, 54–72. [Google Scholar] [CrossRef]

- Jia, X.; Jingbo, C. Green technology innovation in low-carbon cities and enterprises. China Ind. Econ. 2020, 12, 178–196. [Google Scholar]

- Popp, D. Induced innovation and energy prices. Am. Econ. Rev. 2002, 92, 160–180. [Google Scholar] [CrossRef] [Green Version]

- Li, W.J.; Zheng, M.N. Substantive innovation or strategic innovation. Econ. Res. J. 2016, 51, 60–73, (In Chinese, Beijing, China). [Google Scholar]

- Qi, S.Z.; Lin, S.; Cui, J.B. Can environmental rights trading market induce green innovation? Based on the evidence of green patent data of listed companies in China. Econ. Res. J. 2018, 53, 129–143, (In Chinese, Beijing, China). [Google Scholar]

- Beck, T.; Levine, R.; Levkov, A. Big bad banks? The winners and losers from bank deregulation in the United States. J. Fin. 2010, 65, 1637–1667. [Google Scholar] [CrossRef] [Green Version]

- Bertrand, M.; Mullainathan, S. Enjoying the quiet life? Corporate governance and managerial preferences. J. Pol. Econ. 2003, 111, 1043–1075. [Google Scholar] [CrossRef] [Green Version]

- Wang, J. The economic impact of Special Economic Zones: Evidence from Chinese municipalities. J. Dev. Econ. 2013, 101, 133–147. [Google Scholar] [CrossRef]

- Jacobson, L.S.; Sullivan, L. Earnings losses of displaced Workerd. Am. Econ. Rev. 1993, 83, 685–709. [Google Scholar]

- McGavock, T. Here waits the bride? The effect of Ethiopia’s child marriage law. J. Dev. Econ. 2021, 149, 102580. [Google Scholar] [CrossRef]

- Wu, Y.Y.; Qi, J.; Xian, Q.; Chen, J.D. A study on the carbon emission reduction effect of China’s carbon market: From the perspective of the synergistic effect of market mechanism and administrative intervention. China Ind. Econ. 2021, 8, 114–132, (In Chinese, Beijing, China). [Google Scholar]

- Chetty, R.; Looney, A.; Kroft, K. Salience and taxation: Theory and evidence. Am. Econ. Rev. 2009, 99, 1145–1177. [Google Scholar] [CrossRef] [Green Version]

- La Ferrara, E.; Chong, A.; Duryea, S. Soap operas and fertility: Evidence from brazil. Appl. Econ. 2012, 4, 1–31. [Google Scholar] [CrossRef] [Green Version]

- Song, H.; Sun, Y.J.; Chen, D.K. Evaluation of the effect of government Air pollution control: An empirical study from the construction of low-carbon cities in China. J. Manag. World 2019, 35, 95–108+195, (In Chinese, Beijing, China). [Google Scholar]

- Zhang, Q.; Zheng, Y.; Kong, D.M. Environmental Governance pressure, Executive experience and corporate environmental investment: A quasi-natural experiment based on & LT; Ambient Air quality Standards (2012) & GT. Econ. Res. J. 2019, 54, 183–198, (In Chinese, Beijing, China). [Google Scholar]

- Shen, F.; Tao, Q.Z.; Zhang, Y. The Impact of directors’ overseas background on corporate green technology innovation: From the perspective of corporate reputation. J. Shanghai Univ. Fin. Econ. 2022, 24, 108–122, (In Chinese, Shanghai, China). [Google Scholar]

- Li, W.; Cui, G.; Zheng, M. Does green credit policy affect corporate debt financing? Evidence from China. Environ. Sci. Pollut. Res. Int. 2022, 29, 5162–5171. [Google Scholar] [CrossRef]

- Deng, Y.P.; Wang, L.; Zhou, W.J. Does environmental regulation promote green innovation capacity? Empirical evidence from China. J. Stat. Res. 2021, 38, 76–86, (In Chinese, Beijing, China). [Google Scholar]

- Hsu, P.; Tian, X.; Xu, Y. Financial development and innovation: Cross-country evidence. J. Financ. Econ. 2014, 112, 116–135. [Google Scholar] [CrossRef] [Green Version]

- Bao, G.X.; Guan, B. Does Financial pressure Reduce the efficiency of Local Government’s environmental Governance: A moderated mediation Model. China Popul. Resour. Environ. 2019, 29, 38–48, (In Chinese, Jinan, China). [Google Scholar]

- Liang, J.; Langbein, L. Performance management, high-powered incentives, and environmental policies in China. Int. Public Manag. J. 2015, 18, 346–385. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Variables | N | Mean | Sd | Min | Max |

|---|---|---|---|---|---|

| 4860 | 0.280 | 0.724 | 0.000 | 6.874 | |

| Size | 4860 | 22.308 | 1.308 | 18.158 | 28.520 |

| Age | 4860 | 2.741 | 0.388 | 0.000 | 3.738 |

| Growth | 4860 | 0.177 | 0.433 | −0.569 | 3.261 |

| Lev | 4860 | 0.445 | 0.228 | 0.007 | 2.992 |

| Roa | 4860 | 0.042 | 0.135 | −1.038 | 7.445 |

| First | 4860 | 26.698 | 18.210 | 0.414 | 69.970 |

| Cash | 4860 | 0.054 | 0.071 | −0.177 | 0.243 |

| Board | 4860 | 2.175 | 0.192 | 1.609 | 2.708 |

| Variables | ||

|---|---|---|

| (1) | (2) | |

| 0.0583 ** (0.0225) | 0.0598 ** (0.0227) | |

| Size | 0.214 *** (0.0658) | |

| Age | −0.141 ** (0.0541) | |

| Growth | −0.0388 ** (0.0188) | |

| Lev | −0.0645 (0.147) | |

| Roa | −0.107 (0.107) | |

| First | 0.00305 ** (0.00149) | |

| Cash | 0.295 ** (0.141) | |

| Board | 0.142 (0.116) | |

| Year-FE | Yes | Yes |

| Province-FE | Yes | Yes |

| N | 4860 | 4860 |

| R2 | 0.066 | 0.227 |

| Variables | ||||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| −0.0050 (0.0277) | 0.0452 * (0.0226) | 0.0599 ** (0.0253) | 0.0580 ** (0.0224) | |

| CVs | Yes | Yes | Yes | Yes |

| Year-FE/Province-FE | Yes | Yes | Yes | Yes |

| Firm-FE | No | No | No | Yes |

| N | 10913 | 4446 | 4257 | 4860 |

| R2 | 0.072 | 0.163 | 0.236 | 0.765 |

| Variables | ||

|---|---|---|

| Reputation Mechanism(1) | Financing Mechanism(2) | |

| 0.0384 *** (0.0130) | ||

| 0.236 ** (0.107) | ||

| Year-FE | Yes | Yes |

| Province-FE | Yes | Yes |

| Firm-FE | Yes | Yes |

| N | 4815 | 4860 |

| R2 | 0.770 | 0.765 |

| Variables | ||||

|---|---|---|---|---|

| Large-Sized Samples | Small-Sized Samples | State-Owned Samples | No State-Owned Samples | |

| 0.116 ** (0.0475) | 0.0318 (0.0306) | 0.0756 * (0.0445) | 0.0291 (0.0249) | |

| CVs | Yes | Yes | Yes | Yes |

| Year-FE/ Province-FE | Yes | Yes | Yes | Yes |

| N | 2430 | 2430 | 2385 | 2475 |

| R2 | 0.332 | 0.060 | 0.289 | 0.072 |

| Variables | ||||

|---|---|---|---|---|

| High Financial Development Level | Low Financial Development Level | High Fiscal Pressure Level | Low Fiscal Pressure Level | |

| 0.0600 ** (0.0281) | 0.0473 (0.0324) | 0.0506 (0.0420) | 0.0914 ** (0.0389) | |

| CVs | Yes | Yes | Yes | Yes |

| Year-FE/ Province-FE | Yes | Yes | Yes | Yes |

| N | 2502 | 2358 | 2515 | 2345 |

| R2 | 0.287 | 0.149 | 0.172 | 0.304 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zuo, M.; Wu, T. Does Environmental Credit Rating Promote Green Innovation in Enterprises? Evidence from Heavy Polluting Listed Companies in China. Int. J. Environ. Res. Public Health 2022, 19, 13617. https://doi.org/10.3390/ijerph192013617

Zuo M, Wu T. Does Environmental Credit Rating Promote Green Innovation in Enterprises? Evidence from Heavy Polluting Listed Companies in China. International Journal of Environmental Research and Public Health. 2022; 19(20):13617. https://doi.org/10.3390/ijerph192013617

Chicago/Turabian StyleZuo, Minxin, and Tao Wu. 2022. "Does Environmental Credit Rating Promote Green Innovation in Enterprises? Evidence from Heavy Polluting Listed Companies in China" International Journal of Environmental Research and Public Health 19, no. 20: 13617. https://doi.org/10.3390/ijerph192013617