The Dynamic Relationship among Bank Credit, House Prices and Carbon Dioxide Emissions in China

Abstract

:1. Introduction

2. Literature Review

2.1. The Impact of Bank Credit on House Prices

2.2. The Impact of Bank Credit on Carbon Dioxide Emissions

2.3. The Impact of House Prices on Carbon Dioxide Emissions

3. Model Description

3.1. TVP-SV-VAR Model

3.2. Bayesian DCC-GARCH Model

4. Empirical Analysis

4.1. Empirical Analysis Based on TVP-SV-VAR Model

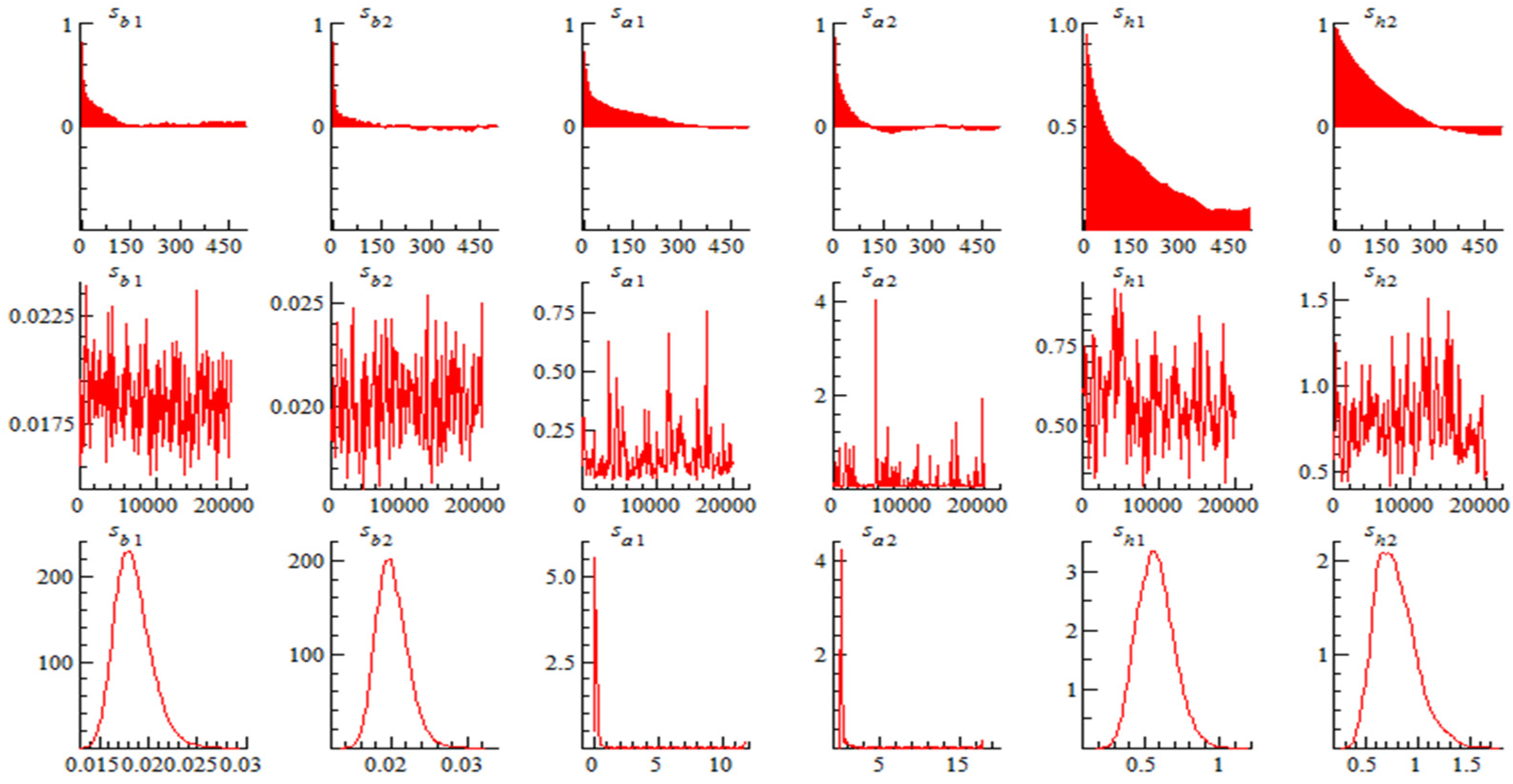

4.1.1. The Analysis of Parameter Regression Results

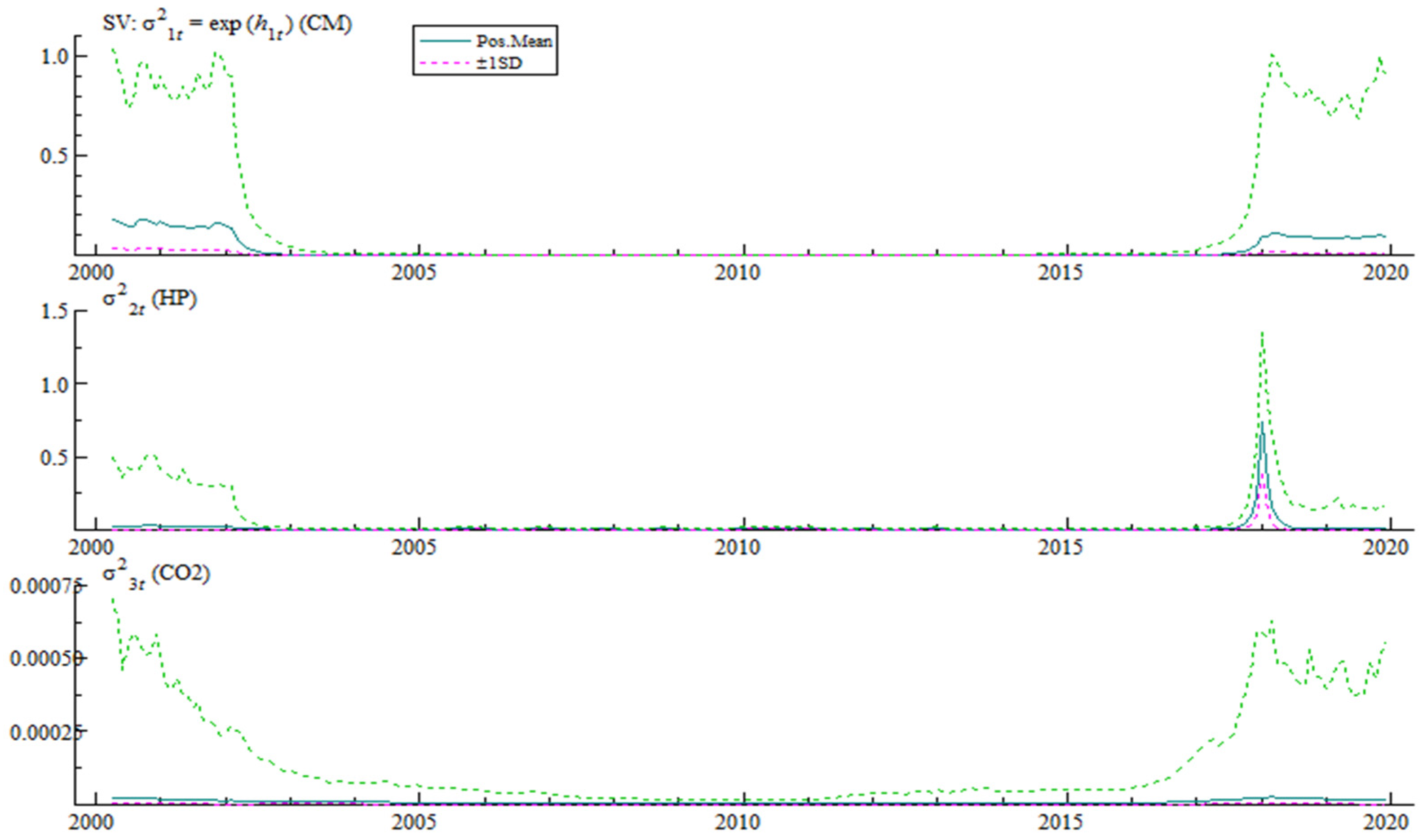

4.1.2. Analysis of Time-Variant Impulse Responses

- (1)

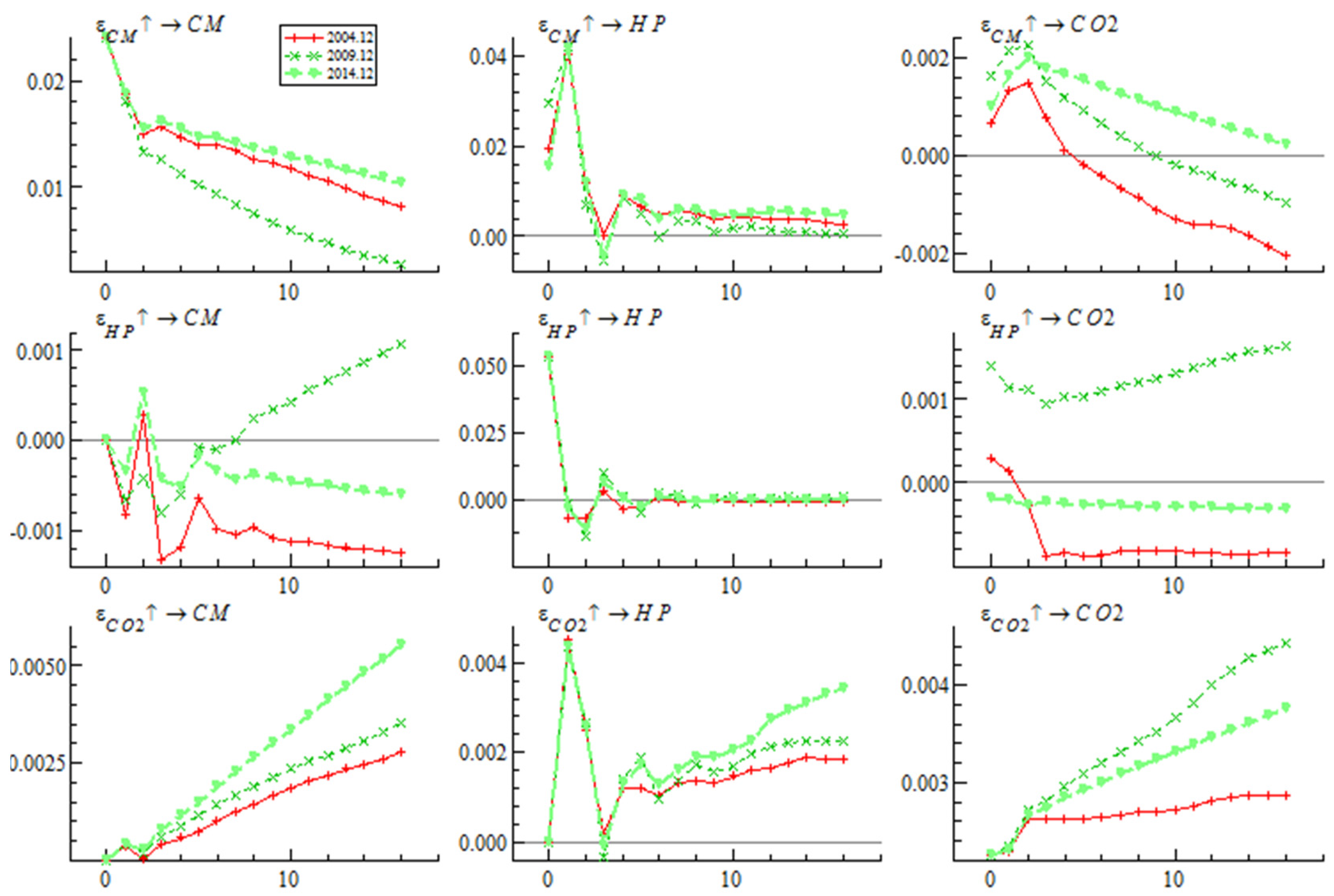

- Analysis of the time-variant characteristics of impulse responses at different time points

- (2)

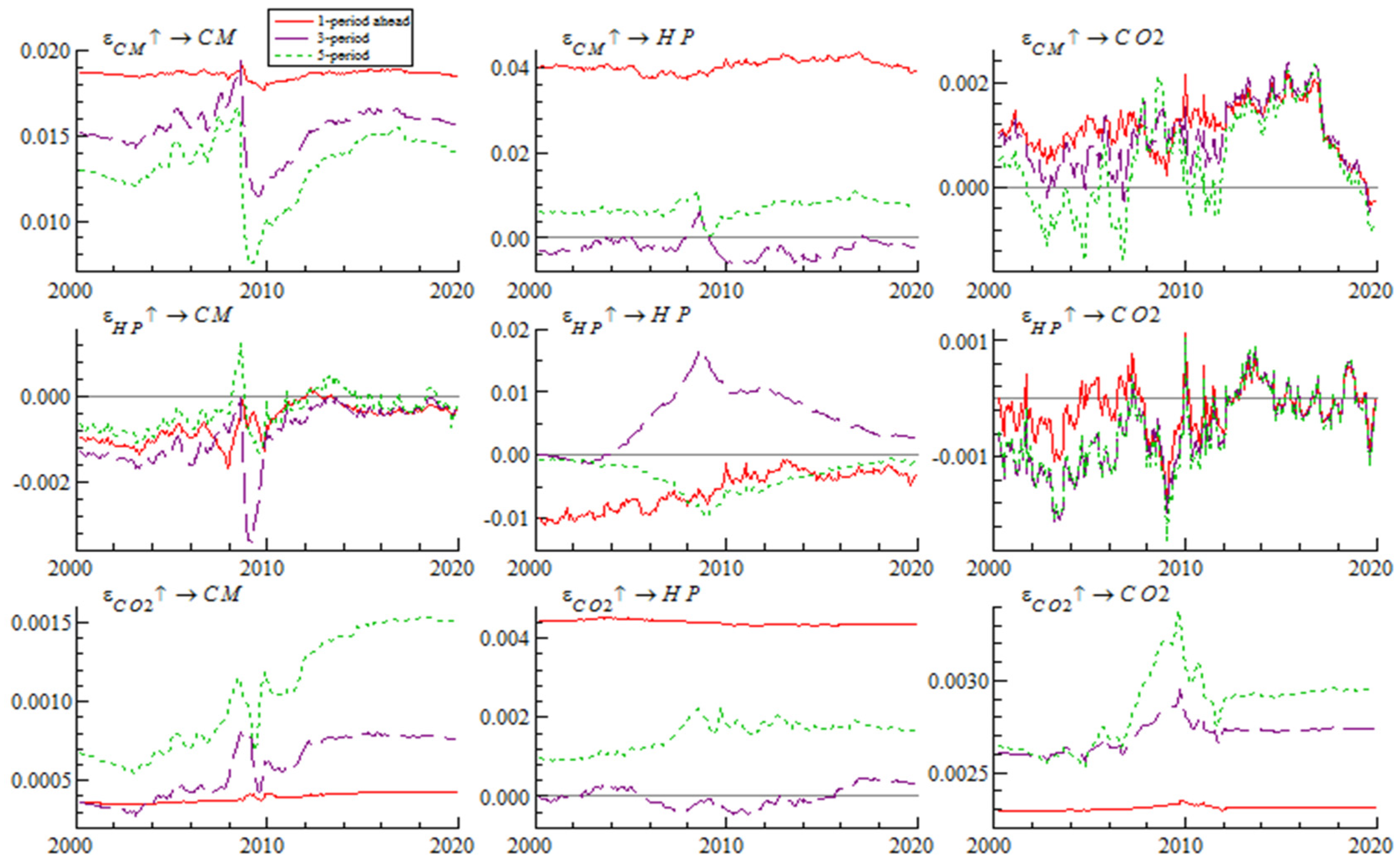

- Analysis of Time-Variant Characteristics of Impulse Response at Different Lead Times

4.2. Empirical Analysis Based on Bayesian DCC-GARCH Model

4.2.1. Estimation Results of the Model

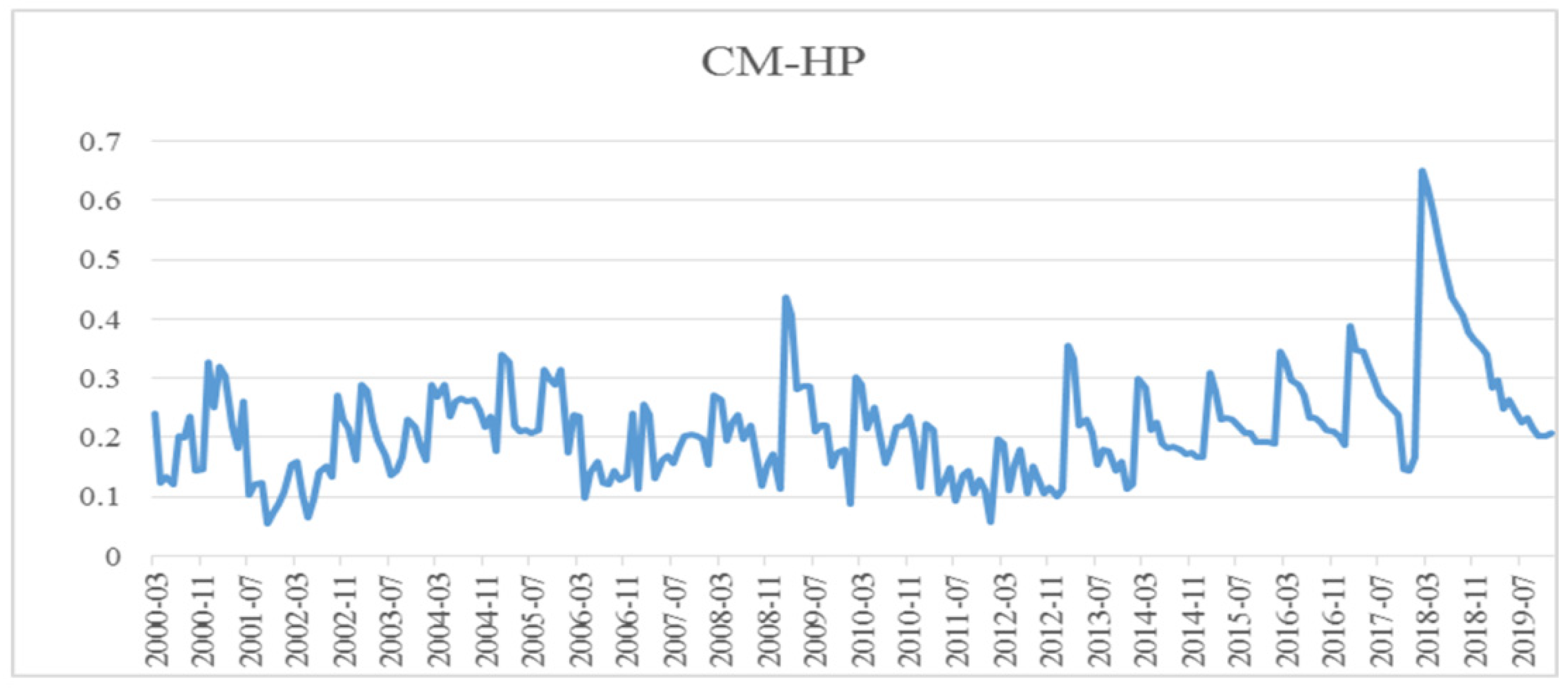

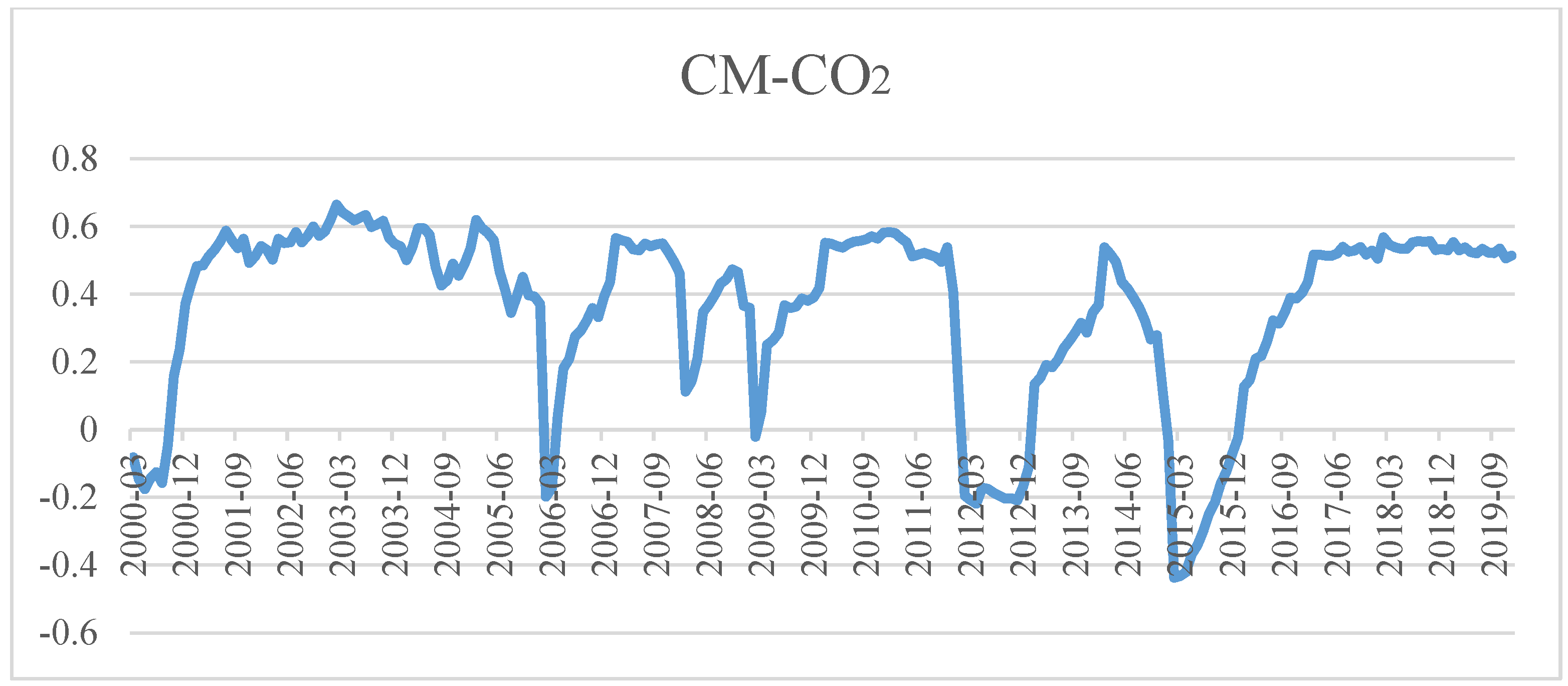

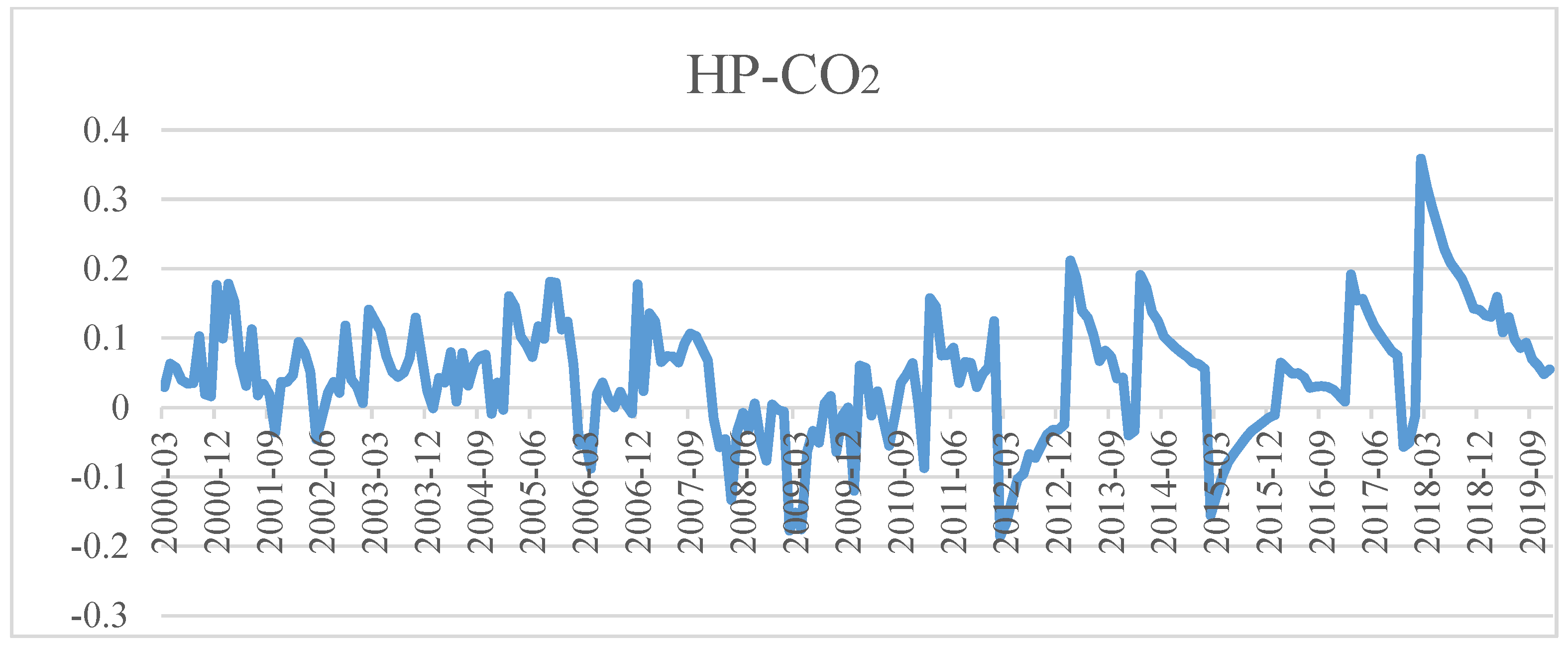

4.2.2. Analysis of Dynamic Correlation Coefficients

5. Conclusions and Recommendations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Qashou, Y.; Samour, A.; Abumunshar, M. Does the real estate market and renewable energy induce carbon dioxide emissions? Novel evidence from Turkey. Energies 2022, 15, 763. [Google Scholar] [CrossRef]

- Wachter, S. The housing and credit bubbles in the United States and Europe: A comparison. J. Money Credit Bank. 2015, 47, 37–42. [Google Scholar] [CrossRef] [Green Version]

- Paramati, S.R.; Mo, D.; Huang, R. The role of financial deepening and green technology on carbon emissions: Evidence from major OECD economies. Financ. Res. Lett. 2021, 41, 101794. [Google Scholar] [CrossRef]

- Davis, M.A.; Heathcote, J. Housing and the business cycle. Int. Econ. Rev. 2005, 46, 751–784. [Google Scholar] [CrossRef] [Green Version]

- Kahn, J.A. What Drives Housing Prices? FRB of New York Staff Report; Federal Reserve Bank of New York: New York, NY, USA, 2008. [Google Scholar]

- Kiyotaki, N.; Michaelides, A.; Nikolov, K. Winners and losers in housing markets. J. Money Credit Bank. 2011, 43, 255–296. [Google Scholar] [CrossRef]

- Lamont, O.; Stein, J.C. Leverage and house-price dynamics in US cities. Rand J. Econ. 1999, 30, 498–514. [Google Scholar] [CrossRef] [Green Version]

- Edelstein, H.; Paul, J. Japanese land prices: Explaining the Boom-Bust Cycle. Asias Financ. Crisis Role Real Estate 2000, 42, 65–82. [Google Scholar]

- Geanakoplos, J.; Zame, W.R. Collateral equilibrium, I: A basic framework. Econ. Theory 2014, 56, 443–492. [Google Scholar] [CrossRef]

- Gete, P.; Reher, M. Two extensive margins of credit and loan-to-value policies. J. Money Credit Bank. 2016, 48, 1397–1438. [Google Scholar] [CrossRef] [Green Version]

- Duca, J.V.; Muellbauer, J.; Murphy, A. What drives house price cycles? International experience and policy issues. J. Econ. Lit. 2021, 59, 773–864. [Google Scholar] [CrossRef]

- Ping, X.Q.; Chen, M.Y. Trends in financing, land price and real estate price. J. World Econ. 2004, 5, 3–10. [Google Scholar]

- Zhang, T.; Gong, L.T.; Bu, Y.X. On the asset return, mortgage lending and property price. J. Financ. Res. 2006, 2, 1–11. [Google Scholar]

- Liang, Y.F.; Gao, T.M. Empirical analysis on real estate price fluctuation in different provinces of China. Econ. Res. J. 2007, 8, 133–142. [Google Scholar]

- Tan, Z.X.; Wang, C. Credit expansion, housing price and financial stability: A DSGE model. J. Financ. Res. 2011, 57–71. [Google Scholar]

- Wang, Y.Q.; Zhu, Q.G.; Tan, Z.D. Research on the fluctuations of housing market in China. J. Financ. Res. 2013, 3, 101–113. [Google Scholar]

- Jia, J.X.; Qin, C.; Zhang, J. Fiscal policy, monetary policy and asset price stability. J. World Econ. 2014, 12, 3–26. [Google Scholar]

- Yu, H.Y.; Huang, Y.F. Regional heterogeneous impacts of monetary policy, housing prices spillovers and the trans-regional impact of housing price on inflation. J. Financ. Res. 2015, 2, 95–113. [Google Scholar]

- Bologna, P.; Cornacchia, W.; Galardo, M. Release of a liquidity regulation: What do we learn for credit and house prices? J. Financ. Stab. 2022, 61, 101021. [Google Scholar] [CrossRef]

- Mian, A.; Sufi, A. Credit supply and housing speculation. Rev. Financ. Stud. 2022, 35, 680–719. [Google Scholar] [CrossRef]

- Iacoviello, M.; Pavan, M. Housing and debt over the life cycle and over the business cycle. J. Monet. Econ. 2013, 60, 221–238. [Google Scholar] [CrossRef] [Green Version]

- Landvoigt, T.; Piazzesi, M.; Schneider, M. The housing market (s) of San Diego. Am. Econ. Rev. 2015, 105, 1371–1407. [Google Scholar] [CrossRef] [Green Version]

- Cox, J.; Ludvigson, S.C. Drivers of the great housing boom-bust: Credit conditions, beliefs or both? Real Estate Econ. 2021, 49, 843–875. [Google Scholar] [CrossRef]

- Park, S.W.; Bahng, D.W.; Park, Y.W. Price run-up in housing markets, access to bank lending and house prices in Korea. J. Real Estate Financ. Econ. 2010, 40, 332–367. [Google Scholar] [CrossRef]

- Glaeser, E.L.; Gottlieb, J.D.; Tobio, K. Housing booms and city centers. Am. Econ. Rev. 2012, 102, 127–133. [Google Scholar] [CrossRef] [Green Version]

- Wei, W.; Chen, J. Does higher mortgage leverage always boost housing price? Evidence from the threshold model of provincial panel data. J. Financ. Res. 2017, 48–63. [Google Scholar]

- Kaplan, G.; Mitman, K.; Violante, G.L. The housing boom and bust: Model meets evidence. J. Political Econ. 2020, 128, 3285–3345. [Google Scholar] [CrossRef] [Green Version]

- Jalil, A.; Feridun, M. The impact of growth, energy and financial development on the environment in China: A cointegration analysis. Energy Econ. 2011, 33, 284–291. [Google Scholar] [CrossRef]

- Umar, M.; Ji, X.; Mirza, N.; Naqvi, B. Carbon neutrality, bank lending, and credit risk: Evidence from the Eurozone. J. Environ. Manag. 2021, 296, 113156. [Google Scholar] [CrossRef]

- Abbasi, F.; Riaz, K. CO2 emissions and financial development in an emerging economy: An augmented VAR approach. Energy Policy 2016, 90, 102–114. [Google Scholar] [CrossRef]

- Zhao, B.; Yang, W. Does financial development influence CO2 emissions? A Chinese province-level study. Energy 2020, 200, 117523. [Google Scholar] [CrossRef]

- Jiang, H.; Wang, W.; Wang, L.; Wu, J. The effects of the carbon emission reduction of China’s green Finance—An analysis based on green credit and green venture investment. Financ. Forum 2020, 11, 39–48. [Google Scholar]

- Kang, H.; Jung, S.Y.; Lee, H. The impact of Green Credit Policy on manufacturers’ efforts to reduce suppliers’ pollution. J. Clean. Prod. 2020, 248, 119271. [Google Scholar] [CrossRef]

- An, S.; Li, B.; Song, D.; Chen, X. Green credit financing versus trade credit financing in a supply chain with carbon emission limits. Eur. J. Oper. Res. 2021, 292, 125–142. [Google Scholar] [CrossRef]

- Al-Mulali, U.; Sab, C.N.B.C. The impact of energy consumption and CO2 emission on the economic growth and financial development in the Sub Saharan African countries. Energy 2012, 39, 180–186. [Google Scholar] [CrossRef]

- Ozturk, I.; Acaravci, A. The long-run and causal analysis of energy, growth, openness and financial development on carbon emissions in Turkey. Energy Econ. 2013, 36, 262–267. [Google Scholar] [CrossRef]

- Zhang, Y.J. The impact of financial development on carbon emissions: An empirical analysis in China. Energy Policy 2011, 39, 2197–2203. [Google Scholar] [CrossRef]

- Haseeb, A.; Xia, E.; Baloch, M.A.; Kashif, A. Financial development, globalization, and CO2 emission in the presence of EKC: Evidence from BRICS countries. Environ. Sci. Pollut. Res. 2018, 25, 31283–31296. [Google Scholar] [CrossRef]

- Ahmad, M.; Khan, Z.; Ur Rahman, Z.; Khan, S. Does financial development asymmetrically affect CO2 emissions in China? An application of the nonlinear autoregressive distributed lag (NARDL) model. Carbon Manag. 2018, 9, 631–644. [Google Scholar] [CrossRef]

- Shahbaz, M.; Destek, M.A.; Dong, K.; Jiao, Z. Time-varying impact of financial development on carbon emissions in G-7 countries: Evidence from the long history. Technol. Forecast. Soc. Change 2021, 171, 120966. [Google Scholar] [CrossRef]

- Boutabba, M.A. The impact of financial development, income, energy and trade on carbon emissions: Evidence from the Indian economy. Econ. Model. 2014, 40, 33–41. [Google Scholar] [CrossRef] [Green Version]

- Kim, D.H.; Wu, Y.C.; Lin, S.C. Carbon dioxide emissions and the finance curse. Energy Econ. 2020, 88, 104788. [Google Scholar] [CrossRef]

- Laquatra, J. Housing market capitalization of thermal integrity. Energy Econ. 1986, 8, 134–138. [Google Scholar] [CrossRef] [Green Version]

- Brounen, D.; Kok, N. On the economics of energy labels in the housing market. J. Environ. Econ. Manag. 2011, 62, 166–179. [Google Scholar] [CrossRef] [Green Version]

- Krozer, Y. Innovative offices for smarter cities, including energy use and energy-related carbon dioxide emissions. Energy Sustain. Soc. 2017, 7, 1–13. [Google Scholar] [CrossRef] [Green Version]

- Glaeser, E.L.; Kahn, M.E. The greenness of cities: Carbon dioxide emissions and urban development. J. Urban Econ. 2010, 67, 404–418. [Google Scholar] [CrossRef] [Green Version]

- Zhang, L.; Wu, J.; Liu, H. Turning green into gold: A review on the economics of green buildings. J. Clean. Prod. 2018, 172, 2234–2245. [Google Scholar] [CrossRef]

- Fuerst, F.; Shimizu, C. Green luxury goods? The economics of eco-labels in the Japanese housing market. J. Jpn. Int. Econ. 2016, 39, 108–122. [Google Scholar] [CrossRef]

- Teotónio, I.; Silva, C.M.; Cruz, C.O. Economics of green roofs and green walls: A literature review. Sustain. Cities Soc. 2021, 69, 102781. [Google Scholar] [CrossRef]

- Dinan, T.M.; Miranowski, J.A. Estimating the implicit price of energy efficiency improvements in the residential housing market: A hedonic approach. J. Urban Econ. 1989, 25, 52–67. [Google Scholar] [CrossRef]

- Gilmer, R.W. Energy labels and economic search: An example from the residential real estate market. Energy Econ. 1989, 11, 213–218. [Google Scholar] [CrossRef]

- Eichholtz, P.; Kok, N.; Quigley, J.M. Doing well by doing good? Green office buildings. Am. Econ. Rev. 2010, 100, 2492–2509. [Google Scholar] [CrossRef] [Green Version]

- Eichholtz, P.; Kok, N.; Quigley, J.M. The economics of green building. Rev. Econ. Stat. 2013, 95, 50–63. [Google Scholar] [CrossRef]

- Primiceri, E. Time varying structural vector autoregressions and monetary policy. Rev. Econ. Stud. 2005, 72, 821–852. [Google Scholar] [CrossRef]

- Engle, F. Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. J. Bus. Econ. Stat. 2002, 20, 339–350. [Google Scholar] [CrossRef]

- Nakajima, J. Time-Varying Parameter VAR Model with Stochastic Volatility: An Overview of Methodology and Empirical Applications; Institute for Monetary and Economic Studies, Bank of Japan: Tokyo, Japan, 2011. [Google Scholar]

- Fioruci, A.; Ehlers, S.; Filho, A. bayesian multivariate GARCH models with dynamic correlations and asymmetric error distributions. J. Appl. Stat. 2014, 41, 320–331. [Google Scholar] [CrossRef]

- Bauwens, L.; Laurent, S. A new class of multivariate skew densities with application to generalized autoregressive conditional heteroscedasticity models. J. Bus. Econ. Stat. 2005, 23, 346–354. [Google Scholar] [CrossRef]

- Ma, M.; Ma, X.; Cai, W.; Cai, W. Carbon-dioxide mitigation in the residential building sector: A household scale-based assessment. Energy Convers. Manag. 2019, 198, 111915. [Google Scholar] [CrossRef]

- Arif, M.S. Residential Solar Panels and Their Impact on the Reduction of Carbon Emissions; University of California: Berkeley, CA, USA, 2013; Available online: https://nature.berkeley.edu/classes/es196/projects/2013final/ArifM_2013.pdf (accessed on 24 June 2021).

- Elias, R.S.; Yuan, M.; Wahab MI, M.; Patel, N. Quantifying saving and carbon emissions reduction by upgrading residential furnaces in Canada. J. Clean. Prod. 2019, 211, 1453–1462. [Google Scholar] [CrossRef]

- Prabatha, T.; Hewage, K.; Karunathilake, H.; Sadiq, R. To retrofit or not? Making energy retrofit decisions through life cycle thinking for Canadian residences. Energy Build. 2020, 226, 110393. [Google Scholar] [CrossRef]

- Balat, H.; Öz, C. Technical and economic aspects of carbon capture an storage—A review. Energy Explor. Exploit. 2007, 25, 357–392. [Google Scholar] [CrossRef]

- Bryan, H.; Ben Salamah, F. Building-integrated Carbon Capture: Development of an Appropriate and Applicable Building-integrated System for Carbon Capture and Shade. Civ. Eng. Archit. 2018, 6, 155–163. [Google Scholar] [CrossRef]

- Pokhrel, S.R.; Hewage, K.; Chhipi-Shrestha, G.; Karunathilake, H.; Li, E.; Sadiq, R. Carbon capturing for emissions reduction at building level: A market assessment from a building management perspective. J. Clean. Prod. 2021, 294, 126323. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Parameter | Mean Value | Standard Deviation | 95% Confidence Interval | Geweke | Non-Effective Factor |

|---|---|---|---|---|---|

| sb1 | 0.0185 | 0.0018 | [0.0154, 0.0226] | 0.061 | 45.17 |

| sb2 | 0.0201 | 0.0020 | [0.0166, 0.0246] | 0.003 | 24.98 |

| sa1 | 0.1469 | 0.1812 | [0.0455, 0.4682] | 0.373 | 74.61 |

| sa2 | 0.2173 | 0.4888 | [0.0384, 1.4980] | 0.176 | 36.62 |

| sh1 | 0.5750 | 0.1183 | [0.3661, 0.8238] | 0.476 | 166.35 |

| sh2 | 0.7852 | 0.1928 | [0.4762, 1.2344] | 0.573 | 174.73 |

| Variable | Parameter | Mean Value | Quantile | ||||

|---|---|---|---|---|---|---|---|

| 2.50% | 25.00% | 50.00% | 75.00% | 97.50% | |||

| CM | γ | 0.5679 | 0.5197 | 0.5511 | 0.5695 | 0.5875 | 0.6216 |

| ω | 0 | 0 | 0 | 0 | 0 | 0 | |

| α | 0.2998 | 0.1376 | 0.2294 | 0.2911 | 0.3571 | 0.5276 | |

| β | 0.5308 | 0.2768 | 0.446 | 0.5388 | 0.621 | 0.7588 | |

| HP | γ | 1.168 | 1.049 | 1.12 | 1.162 | 1.211 | 1.318 |

| ω | 0 | 0 | 0 | 0 | 0 | 0 | |

| α | 0.5832 | 0.2669 | 0.4843 | 0.5984 | 0.6944 | 0.8073 | |

| β | 0.2341 | 0.0891 | 0.1802 | 0.23 | 0.2828 | 0.4017 | |

| CO2 | γ | 0.5634 | 0.5071 | 0.5409 | 0.5625 | 0.5842 | 0.6228 |

| ω | 0 | 0 | 0 | 0 | 0 | 0 | |

| α | 0.7014 | 0.5686 | 0.6527 | 0.6984 | 0.7519 | 0.8307 | |

| β | 0.2811 | 0.153 | 0.2307 | 0.2829 | 0.3295 | 0.4115 | |

| υ | 4.211 | 3.716 | 4.019 | 4.187 | 4.39 | 4.797 | |

| a | 0.0699 | 0.0389 | 0.0568 | 0.0685 | 0.0808 | 0.1105 | |

| b | 0.8372 | 0.7468 | 0.8113 | 0.8409 | 0.8667 | 0.9098 | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, G.; Dong, K.; Wang, S.; Du, X.; Zhou, R.; Yang, Z. The Dynamic Relationship among Bank Credit, House Prices and Carbon Dioxide Emissions in China. Int. J. Environ. Res. Public Health 2022, 19, 10428. https://doi.org/10.3390/ijerph191610428

Chen G, Dong K, Wang S, Du X, Zhou R, Yang Z. The Dynamic Relationship among Bank Credit, House Prices and Carbon Dioxide Emissions in China. International Journal of Environmental Research and Public Health. 2022; 19(16):10428. https://doi.org/10.3390/ijerph191610428

Chicago/Turabian StyleChen, Guangyang, Kai Dong, Shaonan Wang, Xiuli Du, Ronghua Zhou, and Zhongwei Yang. 2022. "The Dynamic Relationship among Bank Credit, House Prices and Carbon Dioxide Emissions in China" International Journal of Environmental Research and Public Health 19, no. 16: 10428. https://doi.org/10.3390/ijerph191610428