Peer Effects on Farmers’ Purchases of Policy-Based Planting Farming Agricultural Insurance: Evidence from Sichuan Province, China

Abstract

:1. Introduction

2. Materials and Methods

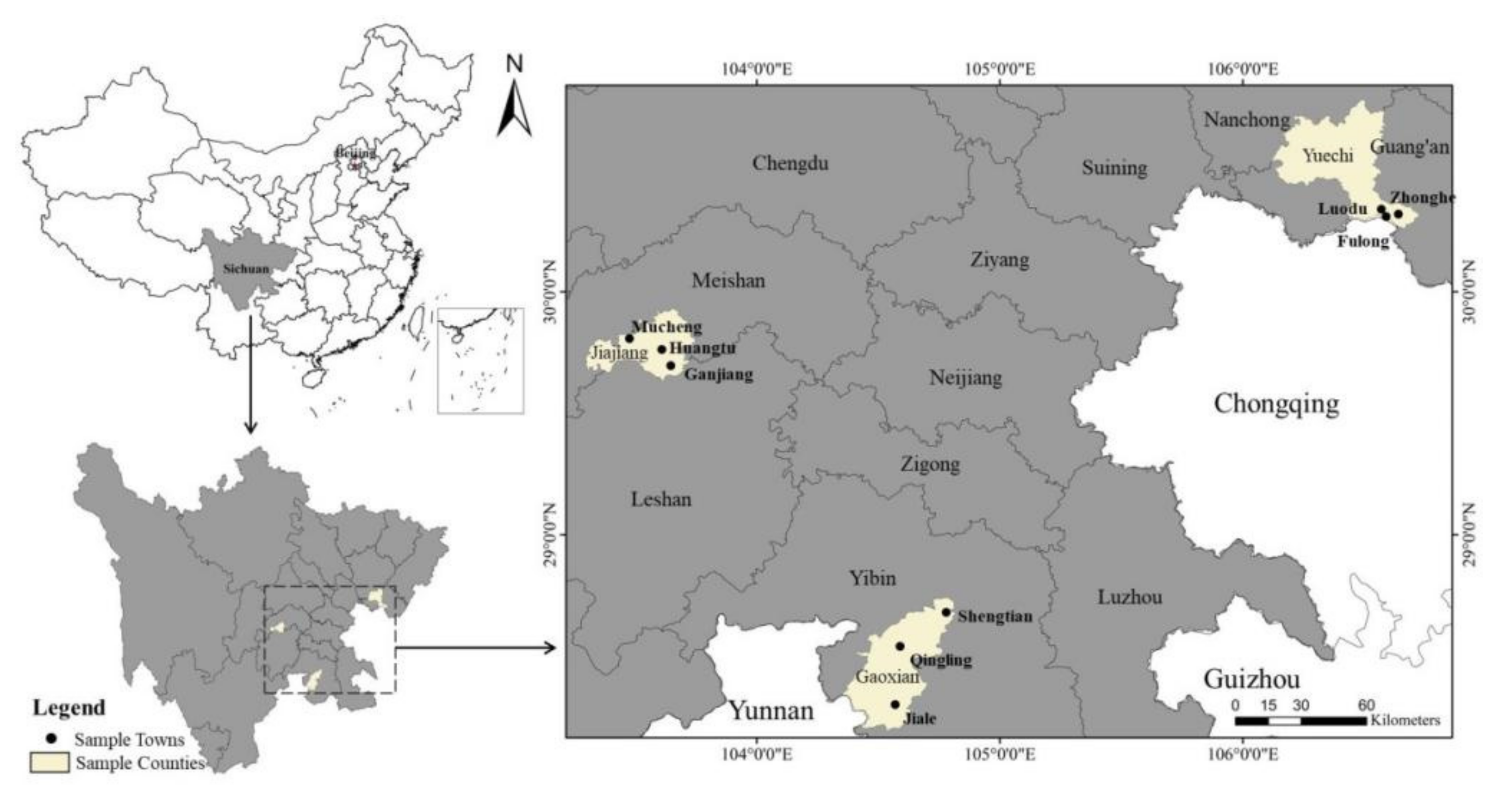

2.1. Data Sources

2.2. Theoretical Analysis and Research Assumptions

2.3. Variable Definitions

2.3.1. Core Variable

2.3.2. Control Variables

2.4. Research Methods and Models

2.4.1. Binary Logistic Regression

2.4.2. Propensity Score Matching Method (PSM Model)

3. Results and Discussion

3.1. Results of the Binary Logistic Model

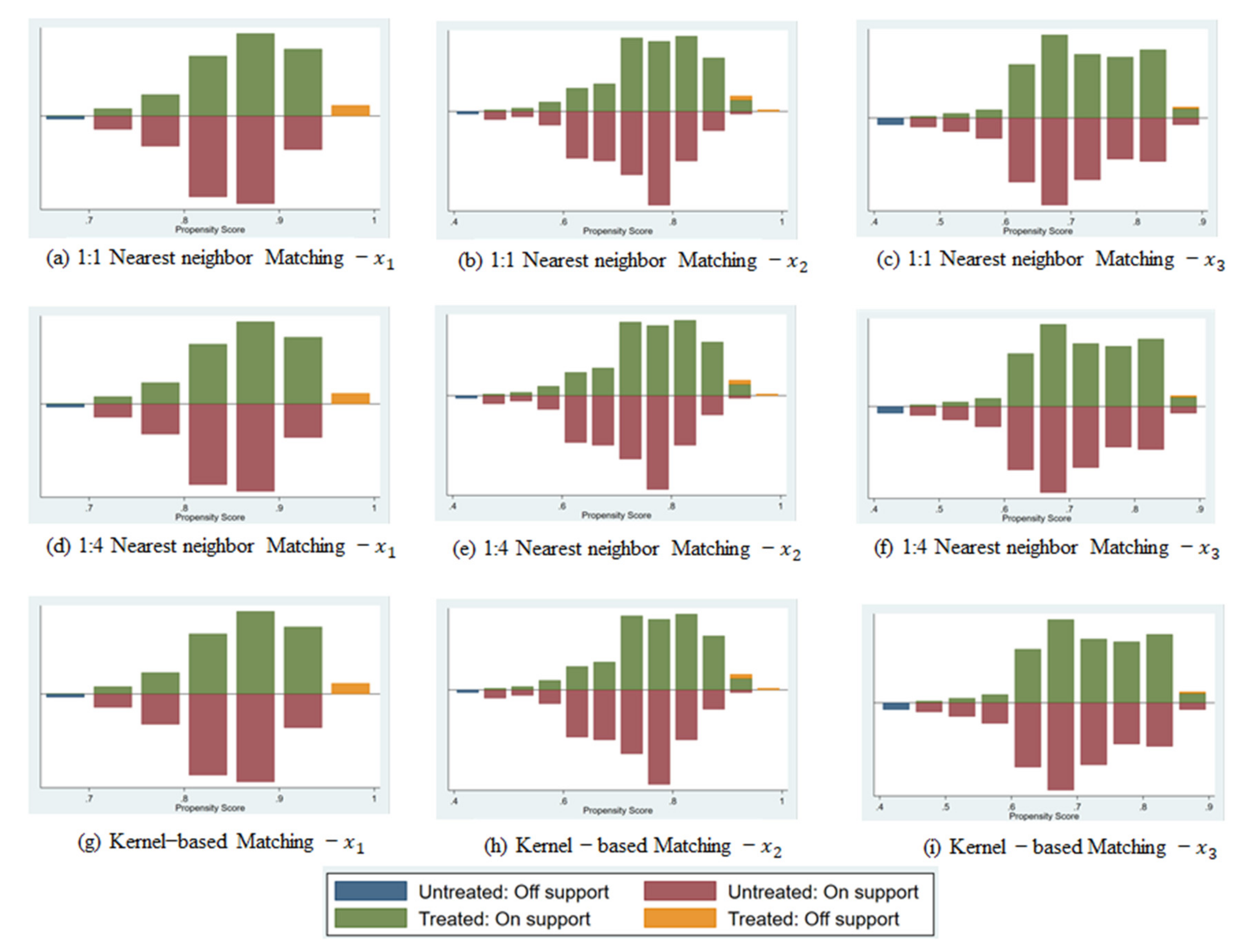

3.2. Correction Results of the PSM Model

3.3. Mechanism Analysis

3.4. Heterogeneity Analysis

4. Conclusions

5. Policy Recommendations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ma, B.; Li, D. Research on Systemic Risk in Hog Price Index Insurance. Agric. Technol. Econ. 2018, 8, 112–123. [Google Scholar] [CrossRef]

- Tuo, G. Looking at the vigorous development of agricultural insurance in my country from 40 years of policy changes. Insur. Res. 2018, 12, 84–87. [Google Scholar]

- Zheng, W.; Zheng, H.; Jia, R.; Chen, G. The evaluation framework of agricultural insurance catastrophe risk dispersion system and its application in international comparison. Agric. Econ. Issues 2019, 9, 121–133. [Google Scholar] [CrossRef]

- Analysis on the Status Quo and Dilemma of China’s Agricultural Development in 2020. Available online: https://www.iimedia.cn/c1020/74133.html (accessed on 15 November 2021).

- Liu, H.; Tao, J. China’s policy agricultural insurance: Development trend, international comparison and path optimization. J. Huazhong Agric. Univ. (Soc. Sci. Ed.) 2020, 6, 67–75, 163–164. [Google Scholar] [CrossRef]

- Bai, Z. Analysis of Influencing Factors of Policy-based Agricultural Insurance Demand: A Literature Review. J. Northwest. Univ. (Philos. Soc. Sci. Ed.) 2012, 4, 32–36. [Google Scholar] [CrossRef]

- Tuo, G. Risks of Agricultural Insurance Operation and Its Prevention and Control. China Insur. 2018, 2, 7–13. [Google Scholar]

- The National Autumn Harvest Has over 80% Progress, Grain Production Will Welcome Eighteen Lian Feng. Available online: http://www.gov.cn/xinwen/2021-10/30/content_5647712.htm (accessed on 14 June 2022).

- Yue, L.; Liu, X. Analysis of Influencing Factors of Agricultural Insurance Demand—Taking Shandong Province as an Example. Rural. Econ. Technol. 2021, 11, 110–112. [Google Scholar]

- Guo, J.; Tan, S.; Kong, X. Regional Differences of Farmers’ Agricultural Insurance Exclusion: Insufficient Supply or Insufficient Demand—Based on the Investigation of Planting Industry Insurance in 12 Counties in 6 Northern Provinces. Agric. Technol. Econ. 2019, 2, 85–98. [Google Scholar] [CrossRef]

- Zheng, W.; Hu, X.; Luo, B. The impact of climate risk on farmers’ purchase of agricultural insurance and its heterogeneity. Stat. Inf. Forum 2021, 8, 66–74. [Google Scholar]

- Zhang, Q.; Chen, X. Empirical analysis of farmers’ willingness to demand agricultural insurance and its influencing factors. N. Hortic. 2019, 23, 157–163. [Google Scholar]

- Yamauchi, T. Actuarial Structure of Crop Insurance in Japan and Appraisal on its Benefits. Bull. Univ. Osaka Prefect. Ser. D Econ. Bus. Adm. Law 1974, 18, 11–42. [Google Scholar]

- Enjolras, G.; Capitanio, F.; Aubert, M.; Adinolfi, F. Direct payments, crop insurance and the volatility of farm income. Some evidence in France and in Italty. In 123. EAAE Seminar: Price Volatility and Farm Income Stabilisation: Modelling Outcomes and Assessing Market and Policy Based Responses; HAL: Rotterdam, The Netherlands, 2012. [Google Scholar]

- Liu, W.; Sun, L.; Tuo, G. Research on the Influence Mechanism of Agricultural Insurance on Farmers’ Income—Based on Moderated Mediating Effect. Agric. Tech. Econ. 2021, 1–15. [Google Scholar] [CrossRef]

- Ren, T.; Zhang, H.; Yang, R. How agricultural insurance coverage affects agricultural production efficiency: Based on survey data from Hubei, Jiangxi, Sichuan and Yunnan provinces. China Popul. Resour. Environ. 2021, 7, 161–170. [Google Scholar]

- Bikhchandani, S.; Hirshleifer, D.; Welch, I. Learning from the behavior of others: Conformity, fads, and informational cascades. J. Econ. Perspect. 1998, 12, 151–170. [Google Scholar] [CrossRef] [Green Version]

- Chen, Y.; Jin, G.Z.; Yue, Y. Peer Migration in China (No. w15671); National Bureau of Economic Research: Cambridge, MA, USA, 2010. [Google Scholar] [CrossRef]

- Duflo, E.; Saez, E. Participation and investment decisions in a retirement plan: The influence of colleagues’ choices. J. Public Econ. 2002, 85, 121–148. [Google Scholar] [CrossRef] [Green Version]

- Manski, C.F. Economic analysis of social interactions. J. Econ. Perspect. 2000, 14, 115–136. [Google Scholar] [CrossRef] [Green Version]

- Bernardi, L.; Klärner, A. Social networks and fertility. Demogr. Res. 2014, 30, 641–670. [Google Scholar] [CrossRef] [Green Version]

- Dahl, G.B.; Løken, K.V.; Mogstad, M. Peer effects in program participation. Am. Econ. Rev. 2014, 104, 2049–2074. [Google Scholar] [CrossRef] [Green Version]

- Liu, H.; Qi, S.; Zhao, Z. Social Learning and Health Insurance Enrollment: Evidence from China’s New Cooperative Medical Scheme. J. Econ. Behav. Organ. 2014, 97, 84–102. [Google Scholar] [CrossRef] [Green Version]

- Lahno, A.M.; Serra-Garcia, M. Peer effects in risk taking: Envy or conformity? J. Risk Uncertain. 2015, 50, 73–95. [Google Scholar] [CrossRef] [Green Version]

- Pool, V.K.; Stoffman, N.; Yonker, S.E. The people in your neighborhood: Social interactions and mutual fund portfolios. J. Financ. 2015, 70, 2679–2732. [Google Scholar] [CrossRef]

- Bernheim, B.D. A theory of conformity. J. Polit Econ. 1994, 102, 841–877. [Google Scholar] [CrossRef]

- Zhang, C.; Zhu, H. Peer Effect in Decision-making of New Rural Social Endowment Insurance. J. Financ. Res. 2021, 9, 111–130. [Google Scholar]

- Banerjee, A.V. A simple model of herd behavior. Q. J. Econ. 1992, 107, 797–817. [Google Scholar] [CrossRef] [Green Version]

- Fei, X. Rural China; Shanghai People’s Publishing House: Shanghai, China, 2019. [Google Scholar]

- Granovetter, M. The Strength of Weak Ties: A Network Theory Revisited. Sociol. Theor. 1983, 1, 201–233. [Google Scholar] [CrossRef]

- Hu, H. The impact of strong and weak relationships in social networks on agricultural technology diffusion: From the perspective of individuals to systems. J. Huazhong Agric. Univ. (Soc. Sci. Ed.) 2016, 5, 47–54, 144–145. [Google Scholar] [CrossRef]

- Li, M.; Zhou, L. Structural holes, strong and weak relationships and private lending organizations: A case study based on the M group in D village. China Rural. Obs. 2018, 1, 84–95. [Google Scholar]

- Sun, X.; Bian, Y. The domestic participation of scientists studying in the United States and the re-examination of the hypothesis of strong and weak relationships in social networks. Society 2011, 2, 194–215. [Google Scholar] [CrossRef]

- Bian, Y.J. Bringing strong ties back in: Indirect ties, network bridges, and job searches in china. Am. Sociol. Rev. 1997, 62, 366–385. [Google Scholar] [CrossRef]

- Harvey, W.S. Strong or weak ties? British and Indian expatriate scientists finding jobs in Boston. Glob. Netw. 2008, 8, 453–473. [Google Scholar] [CrossRef]

- Ramirez, S.; Dwivedi, P.; Ghilardi, A.; Bailis, R. Diffusion of non-traditional cookstoves across western honduras: A social network analysis. Energy Policy 2014, 66, 379–389. [Google Scholar] [CrossRef]

- He, X. Characteristics and functions of Spring Festival culture. J. South.-Cent. Univ. Natl. (Humanit. Soc. Sci. Ed.) 2013, 2, 1–6. [Google Scholar]

- Xiao, F. Cultural Heritage and Cultural Resources—The Significance of Spring Festival Customs in the Modern Context. Jiangxi Soc. Sci. 2006, 2, 11–14. [Google Scholar]

- Zhang, H.; Kong, R. A Study on Influencing Factors of Farmers’ Agricultural Insurance Payment Willingness—A Case Study of 413 Tobacco Farmers in Longyan City, Fujian Province. J. Northwest. AF Univ. (Soc. Sci. Ed.) 2014, 3, 76–82. [Google Scholar] [CrossRef]

- Shang, Y.; Xiong, T.; Li, C. Risk perception, risk attitude and farmers’ willingness to adopt risk management tools: Taking agricultural insurance and “insurance + futures” as examples. China Rural. Obs. 2020, 5, 52–72. [Google Scholar]

- Song, C.; Xiao, X.; Li, C. Research on the Impact of Local Policy Agricultural Insurance on Agricultural Products Market: Taking Wuhan Vegetable Market as an Example. Agric. Mod. Res. 2021, 1, 85–93. [Google Scholar] [CrossRef]

- Ye, M.; Wang, R.; Wu, P. Risk Cognition, Insurance Consciousness and Farmers’ Risk Taking Ability—Based on a Questionnaire Survey of 1554 Farmers in Jiangsu, Anhui and Sichuan Provinces. China Rural. Obs. 2014, 6, 37–48, 95. [Google Scholar]

- Zeng, W. Building a suitable risk prevention and control network for agricultural product price fluctuations. People’s Forum 2020, 4, 90–91. [Google Scholar]

- Zeng, Y.; Zhang, J.; He, K. Effects of conformity tendencies on households’ willingness to adopt energy utilization of crop straw: Evidence from biogas in rural China. Renew Energy 2019, 138, 573–584. [Google Scholar] [CrossRef]

- Song, L.; Han, X.; Wang, Y. A Study on Influencing Factors of my country’s Agricultural Insurance Development—Empirical Analysis Based on Regional Panel Data. Macroecon. Res. 2016, 11, 122–130. [Google Scholar] [CrossRef]

- Zhao, J.; Wang, J.; Qiao, L. Analysis of Influencing Factors of Agricultural Insurance Demand Based on Logit Model: A Survey of 300 Farmers in Hebei Province. Jiangsu Agric. Sci. 2013, 10, 387–389. [Google Scholar] [CrossRef]

- Qin, C.; Wu, Y.; Li, F.; Zhou, X.; Tang, Z. The influence of grassland circulation on herdsmen’s family income: An empirical analysis based on the PSM method. Grass Ind. Sci. 2021, 10, 2087–2095. [Google Scholar]

- Yan, H.; Yang, S. The Relative Poverty Governance Effect of Rural Medical Insurance System—An Empirical Analysis Based on the Perspective of Poverty Vulnerability. J. Hunan Agric. Univ. (Soc. Sci. Ed.) 2021, 1, 48–55. [Google Scholar] [CrossRef]

- Rosenbaum, P.R.; Rubin, D.B. Constructing a control group using multivariate matched sampling methods that incorporate the propensity score. Am. Stat. 1985, 39, 33–38. [Google Scholar]

- Wang, Q.; Guo, X. Perceived interest, social network and farmers’ cultivated land quality protection behavior: Based on the survey data of 410 grain growers in Hua County, Henan Province. China Land Sci. 2020, 7, 43–51. [Google Scholar]

- Wu, J.; Wang, T.; Wang, Z. The influence of social network and perceived value on farmers’ choice of farmland quality protection behavior. J. Northwest. AF Univ. (Soc. Sci. Ed.) 2021, 6, 138–147. [Google Scholar] [CrossRef]

- Yang, Z. Aging, Social Network and Farmers’ Green Production Technology Adoption Behavior: Validation from Farmer’s Data from Six Provinces in the Yangtze River Basin. China Rural. Obs. 2018, 4, 44–58. [Google Scholar]

- Matuschke, I.; Qaim, M. The impact of social networks on hybrid seed adoption in india. Agr. Econ. -Blackwell 2010, 40, 493–505. [Google Scholar] [CrossRef]

- Tumbo, S.D.; Mutabazi, K.D.; Masuki, K.; Rwehumbiza, F.B.; Mahoo, H.F.; Nindi, S.J. Social capital and diffusion of water system innovations in the makanya watershed, tanzania. J. Socio-Econ. 2013, 43, 24–36. [Google Scholar] [CrossRef]

- Genius, M.; Koundouri, P.; Nauges, C.; Tzouvelekas, V. Information transmission in irrigation technology adoption and diffusion: Social learning, extension services, and spatial effects. Work. Pap. 2014, 96, 328–344. [Google Scholar] [CrossRef] [Green Version]

- Wen, Z.; Ye, B. Analysis of Mediating Effect: Method and Model Development. Adv. Psychol. Sci. 2014, 5, 731–745. [Google Scholar] [CrossRef]

- Chen, Y.; Ma, Y. Several notes on farmers’ credit and risk appetite. Financ. Trade Econ. 2009, 1, 18–25. [Google Scholar] [CrossRef]

- Zhang, C.; Hu, Z. Government Trust and Social Public Policy Participation—Taking Grassroots Election Voting and Social Medical Insurance Participation as Examples. Econ. Dyn. 2016, 3, 67–77. [Google Scholar]

- Chen, Z.; Ling, Y.; Li, W. Calculation of farmers’ willingness to pay for agricultural insurance and analysis of its influencing factors: Taking tobacco leaf insurance in Xingshan County, Hubei Province as an example. South. Econ. 2008, 7, 34–44. [Google Scholar]

- Wang, M. Analysis of Factors Influencing Small-scale Farmers’ Participation in Policy-based Agricultural Insurance—Based on the Survey Data of 613 Small-scale Farmers in Zhejiang Province. China Rural. Econ. 2009, 3, 38–44. [Google Scholar]

- Chang, F.; Yang, C.; Wang, A.; Wang, H.; Luo, R.; Shi, Y. Current Situation of New Rural Insurance Implementation and Influencing Factors of Enrollment Behavior—Analysis Based on Survey Data of 101 Villages in 5 Provinces. Manag. World 2014, 3, 92–101. [Google Scholar] [CrossRef]

- Liu, G.; Yang, L.; Guo, S.; Deng, X.; Song, J.; Xu, D. Land Attachment, Intergenerational Differences and Land Transfer: Evidence from Sichuan Province, China. Land 2022, 11, 695. [Google Scholar] [CrossRef]

- Qing, C.; He, J.; Guo, S.; Zhou, W.; Deng, X.; Xu, D. Peer effects on the adoption of biogas in rural households of Sichuan Province, China. Environ. Sci. Pollut. Res. 2022, 1–14. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Variable | Variable Measure | Average | Standard Deviation |

|---|---|---|---|

| Do you have policy-based planting agricultural insurance? a | 0.620 | 0.486 | |

| Have your relatives and friends purchased this type of insurance? a | 0.863 | 0.344 | |

| Have your relatives and friends who visited during New the Year period purchased this type of insurance? a,d | 0.761 | 0.427 | |

| Have your relatives and friends who did not visit during the New Year period purchased this type of insurance? a,d | 0.713 | 0.453 | |

| gender | Your gender (0 = male, 1 = female) | 0.404 | 0.491 |

| age | Your age (years) | 58.480 | 11.840 |

| education | Your education level (years) | 6.552 | 3.443 |

| Farming time | How long have you been farming? (year) | 38.220 | 14.74 |

| Family-owned land area | Land area under operation in 2020 (mu) c | 5.679 | 20.532 |

| income | Annual household income in 2020 (yuan) | 92,992.728 | 168,723.286 |

| Disaster perception | Will crops suffer/reduce production due to disasters/weather in 2020? a | 0.702 | 0.458 |

| Environmental awareness | Are you very concerned about the severe impact of climate change on agricultural production? a | 4.200 | 1.032 |

| Willingness for rural development | Your willingness to continue farming b | 3.644 | 1.393 |

| Risk aversion | Two kinds of investments are available to choose from: if you choose the first, you have a 100% chance of receiving CNY 5000; if you choose the second, you have a 50% chance of receiving CNY 10,000, and a 50% chance of receiving nothing. Which would you choose? (0 = first type,1 = second) | 0.096 | 0.295 |

| county_1 | county_1 a | 0.333 | 0.472 |

| county_2 | county_2 a | 0.333 | 0.472 |

| county_3 | county_3 a | 0.333 | 0.472 |

| Variable | Model 1 | Model 2 | Marginal Effect | ||||

|---|---|---|---|---|---|---|---|

| 2.966 *** (0.388) | 3.091 *** (0.396) | 0.502 *** (0.053) | |||||

| 2.425 *** (0.245) | 2.468 *** (0.270) | 0.384 *** (0.027) | |||||

| 1.537 *** (0.203) | 1.604 *** (0.223) | 0.282 *** (0.031) | |||||

| gender | 0.008 (0.242) | −0.095 (0.248) | −0.068 (0.233) | ||||

| age | −0.022 (0.017) | −0.016 (0.017) | −0.030 * (0.017) | ||||

| education | 0.079 ** (0.037) | 0.080 ** (0.037) | 0.063 * (0.035) | ||||

| Farming time | 0.023 * (0.013) | 0.017 (0.013) | 0.032 ** (0.013) | ||||

| Family-owned land area | 0.399 ** (0.172) | 0.392 ** (0.170) | 0.468 *** (0.164) | ||||

| income | −0.026 (0.099) | 0.015 (0.097) | 0.038 (0.095) | ||||

| Disaster perception | 0.635 *** (0.241) | 0.455 * (0.255) | 0.727 *** (0.233) | ||||

| Environmental awareness | 0.179 (0.109) | 0.212 * (0.110) | 0.109 (0.109) | ||||

| Willingness for rural development | 0.112 (0.079) | 0.144 * (0.082) | 0.074 (0.079) | ||||

| Risk aversion | 0.780 (0.483) | 0.698* (0.414) | 0.856 ** (0.434) | ||||

| county_1 | −0.511 * (0.273) | −0.406 (0.275) | −0.445 * (0.256) | ||||

| county_2 | 1.251 *** (0.309) | 1.290 *** (0.312) | 1.239 *** (0.301) | ||||

| Log likelihood | −309.330 | −297.575 | −327.960 | −265.758 | −258.341 | −283.601 | |

| Prob > chi2 | 0.0000 | 0.0000 | 0.0000 | 0.000 | 0.000 | 0.000 | |

| Pseudo R2 | 0.1371 | 0.1699 | 0.0852 | 0.259 | 0.279 | 0.209 | |

| N | 540 | 540 | 540 | 540.000 | 540.000 | 540.000 | |

| Matching Algorithms | Influencing Factors | ATT | Std. Err. | Treated | Controls |

|---|---|---|---|---|---|

| Nearest neighbor matching (1:1) | 0.552 *** (8.92) | 0.062 | 0.693 | 0.141 | |

| 0.460 *** (7.86) | 0.059 | 0.745 | 0.285 | ||

| 0.329 *** (5.38) | 0.061 | 0. 723 | 0.394 | ||

| Nearest neighbor matching (1:4) | 0.532 *** (10.79) | 0.049 | 0.693 | 0.161 | |

| 0.488 *** (9.92) | 0.049 | 0.745 | 0.257 | ||

| 0.332 *** (6.59) | 0.050 | 0.723 | 0.392 | ||

| Kernel-based matching (bandwidth 0.06) | 0.564 *** (12.73) | 0.044 | 0.693 | 0.129 | |

| 0.502 *** (11.17) | 0.045 | 0.745 | 0.243 | ||

| 0.323 *** (6.83) | 0.047 | 0.723 | 0.400 |

| Variable | Mechanism 1: Peer Effect→Social Network→Purchase Policy-Based Planting Agricultural Insurance | Mechanism 2: Peer Effect→Trust→Buy Policy-Based Planting Agricultural Insurance | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Model 3 | Model 4 | Model 5 | Model 6 | |||||||||

| 0.541 *** | −0.251 | 0.024 * | 0.541 *** | 0.232 | 0.027 * | 0.541 *** | −0.024 | −0.019 | 0.541 *** | 0.212 * | 0.035 * | |

| (0.052) | (0.184) | (0.012) | (0.052) | (0.159) | (0.014) | (0.052) | (0.111) | (0.021) | (0.052) | (0.109) | (0.021) | |

| 0.483 *** | 0.355 ** | 0.017 | 0.483 *** | 0.261 ** | 0.023 | 0.483 *** | −0.127 | −0.007 | 0.483 *** | 0.100 | 0.041 ** | |

| (0.042) | (0.149) | (0.012) | (0.042) | (0.129) | (0.014) | (0.042) | 0.090 | 0.020 | (0.042) | (0.089) | (0.020) | |

| 0.322 *** | 0.279 ** | 0.023 * | 0.322 *** | 0.218 * | 0.028 * | 0.322 *** | 0.187 ** | −0.037 * | 0.322 *** | 0.161 * | 0.039 * | |

| (0.041) | (0.140) | (0.013) | (0.041) | (0.121) | (0.015) | (0.042) | (0.084) | (0.021) | (0.041) | (0.084) | (0.022) | |

| Control | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| County | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Variable | The Size of the Family-Run Land | Respondent’s Educational Level | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| The Average Household Owns 5.679 mu and Below | The Average Household Occupies More than 5.679 mu | 9 Years and Below | Over Nine Years | |||||||||

| 3.038 *** | 3.928 *** | 3.054 *** | 4.916 *** | |||||||||

| (0.438) | (0.964) | (0.419) | (1.443) | |||||||||

| 2.348 *** | 3.366 *** | 2.361 *** | 3.657 ** | |||||||||

| (0.308) | (0.662) | (0.289) | (1.712) | |||||||||

| 1.590 *** | 1.869 *** | 1.636 *** | 3.097 * | |||||||||

| (0.265) | (0.476) | (0.237) | (1.752) | |||||||||

| Control | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| County | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Wald χ2 | 109.62 *** | 97.34 *** | 86.31 *** | 45.01 ** | 42.67 *** | 35.55 *** | 106.84 *** | 103.24 *** | 86.95 *** | 31.25 *** | 28.37 *** | 15.68 |

| Observation | 414 | 414 | 414 | 126 | 126 | 126 | 478 | 478 | 478 | 62 | 62 | 62 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bao, X.; Zhang, F.; Guo, S.; Deng, X.; Song, J.; Xu, D. Peer Effects on Farmers’ Purchases of Policy-Based Planting Farming Agricultural Insurance: Evidence from Sichuan Province, China. Int. J. Environ. Res. Public Health 2022, 19, 7411. https://doi.org/10.3390/ijerph19127411

Bao X, Zhang F, Guo S, Deng X, Song J, Xu D. Peer Effects on Farmers’ Purchases of Policy-Based Planting Farming Agricultural Insurance: Evidence from Sichuan Province, China. International Journal of Environmental Research and Public Health. 2022; 19(12):7411. https://doi.org/10.3390/ijerph19127411

Chicago/Turabian StyleBao, Xueling, Fengwan Zhang, Shili Guo, Xin Deng, Jiahao Song, and Dingde Xu. 2022. "Peer Effects on Farmers’ Purchases of Policy-Based Planting Farming Agricultural Insurance: Evidence from Sichuan Province, China" International Journal of Environmental Research and Public Health 19, no. 12: 7411. https://doi.org/10.3390/ijerph19127411