Looking into the Market Behaviors through the Lens of Correlations and Eigenvalues: An Investigation on the Chinese and US Markets Using RMT

, ,

, ,

Abstract

:1. Introduction

2. Literature Review

2.1. RMT and Its Applications

2.2. Applying RMT Approaches in Financial Markets

2.2.1. RMT in Financial Correlation Analysis

2.2.2. RMT in Eigenvalue Analysis

2.2.3. RMT in Eigenvalue Distributions

2.3. Comparative Studies on Different Markets

3. Methodology

3.1. Construction of Correlation Matrices

3.2. Eigenvalue Analysis Using RMT

4. Data and Correlation Matrices

4.1. Data

4.2. Correlation Matrices

5. Eigenvalues and Eigenvectors for CSI163 and S&P468

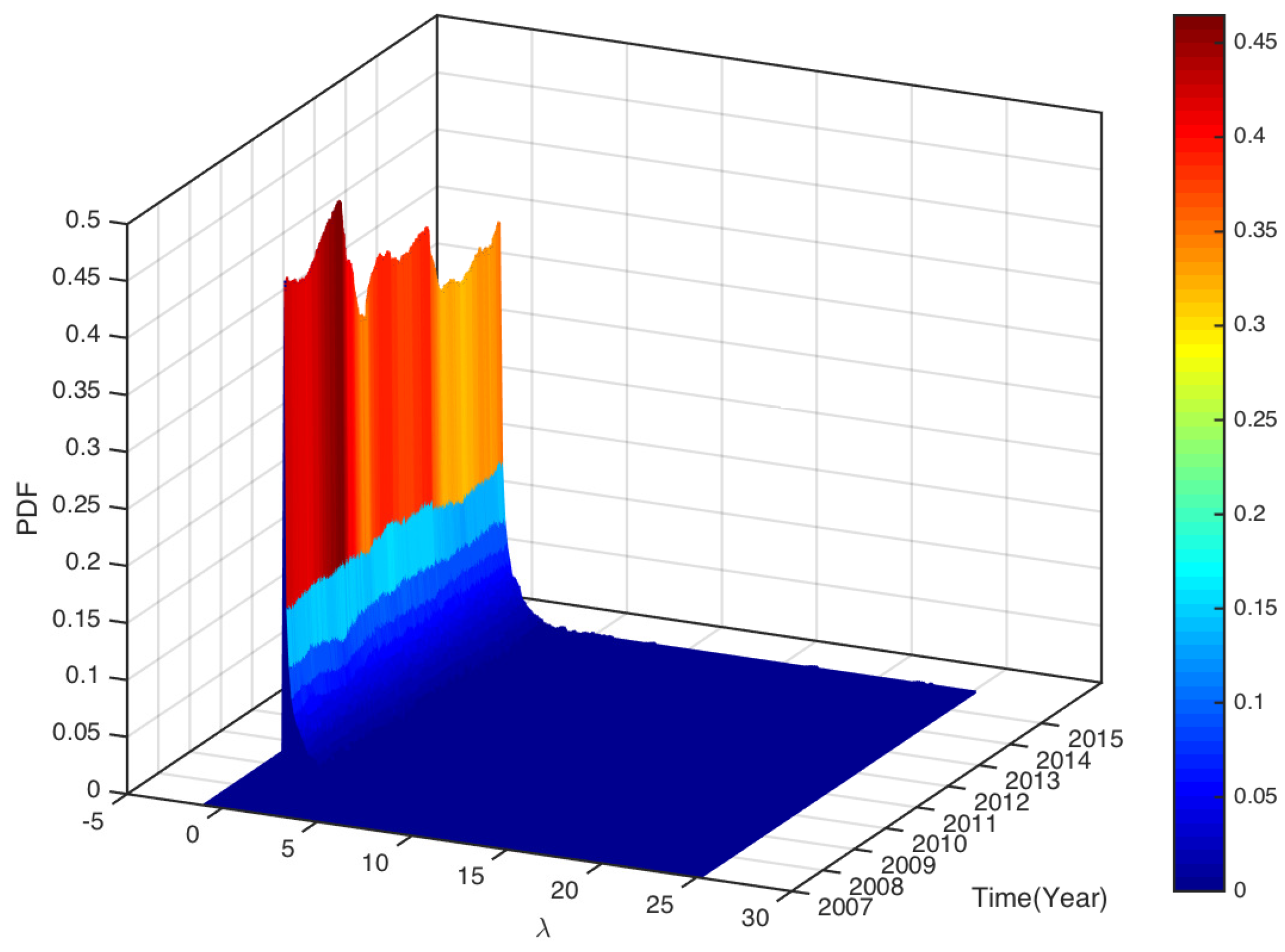

5.1. Eigenvalues

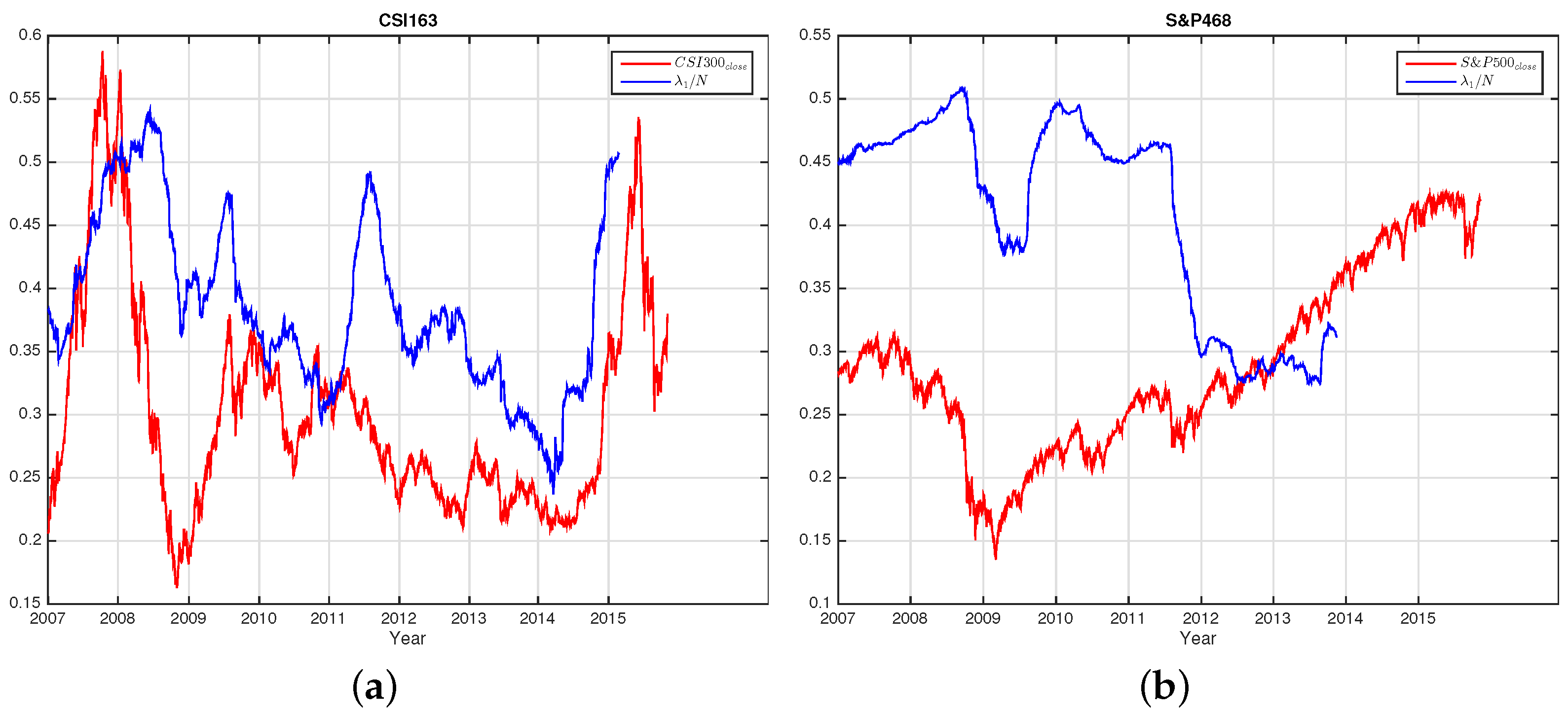

5.2. Largest Eigenvalue

5.3. Second Largest Eigenvalue

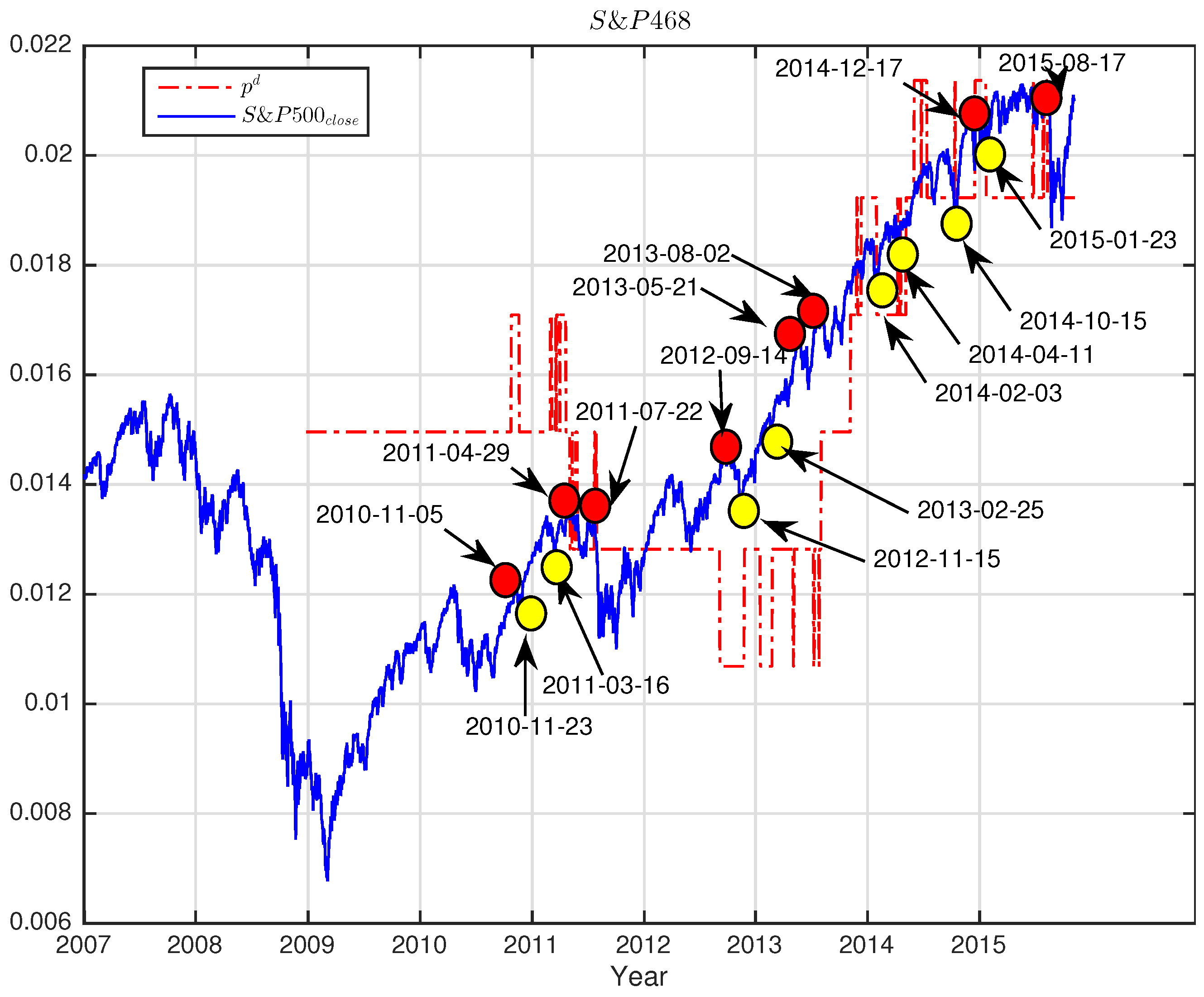

5.4. Market Switching

6. Conclusions and Discussion

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Markowitz, H. Portfolio Selection. J. Financ. 1952, 7, 77–91. [Google Scholar] [CrossRef]

- Sharpe, W.F. Capital Asset Prices: A Theory of Market Equilibrium under Conditions of Risk. J. Financ. 1964, 19, 425–442. [Google Scholar] [CrossRef]

- Livan, G.; Rebecchi, L. Asymmetric correlation matrices: An analysis of financial data. Eur. Phys. J. B—Condens. Matter Complex Syst. 2012, 85, 213. [Google Scholar] [CrossRef]

- Wang, D.; Podobnik, B.; Horvatić, D.; Stanley, H.E. Quantifying and modeling long-range cross correlations in multiple time series with applications to world stock indices. Phys. Rev. E 2011, 83, 046121. [Google Scholar] [CrossRef] [PubMed]

- Fenn, D.J.; Porter, M.A.; Williams, S.; McDonald, M.; Johnson, N.F.; Jones, N.S. Temporal evolution of financial-market correlations. Phys. Rev. E 2011, 84, 026109. [Google Scholar] [CrossRef]

- Di Matteo, T.; Pozzi, F.; Aste, T. The use of dynamical networks to detect the hierarchical organization of financial market sectors. Eur. Phys. J. B—Condens. Matter Complex Syst. 2010, 73, 3–11. [Google Scholar] [CrossRef]

- Tilak, G.; Széll, T.; Chicheportiche, R.; Chakraborti, A. Study of Statistical Correlations in Intraday and Daily Financial Return Time Series. In Econophysics of Systemic Risk and Network Dynamics, New Economic Windows; Abergel, F., Chakrabarti, B.K., Chakraborti, A., Ghosh, A., Eds.; Springer: Milan, Italy, 2013; pp. 77–104. [Google Scholar]

- Mantegna, R.N. Hierarchical structure in financial markets. Eur. Phys. J. B 1999, 11, 193–197. [Google Scholar] [CrossRef]

- Nobi, A.; Maeng, S.E.; Ha, G.G.; Lee, J.W. Network Topologies of Financial Market During the Global Financial Crisis. arXiv 2013, arXiv:1307.6974. [Google Scholar]

- Tumminello, M.; Lillo, F.; Mantegna, R.N. Correlation, hierarchies, and networks in financial markets. J. Econ. Behav. Organ. 2010, 75, 40–58. [Google Scholar] [CrossRef]

- Dimov, I.I.; Kolm, P.N.; Maclin, L.; Shiber, D.Y.C. Hidden noise structure and random matrix models of stock correlations. Quant. Financ. 2012, 12, 567–572. [Google Scholar] [CrossRef]

- Bouchaud, J.P.; Laloux, L.; Miceli, M.A.; Potters, M. Large dimension forecasting models and random singular value spectra. Eur. Phys. J. B—Condens. Matter Complex Syst. 2007, 55, 201–207. [Google Scholar] [CrossRef]

- Dyson, F.J. Statistical Theory of the Energy Levels of Complex Systems. I. J. Math. Phys. 1962, 3, 140–156. [Google Scholar] [CrossRef]

- Wigner, E.P. Characteristic Vectors of Bordered Matrices with Infinite Dimensions I. In The Collected Works of Eugene Paul Wigner: Part A: The Scientific Papers; Wightman, A.S., Ed.; Springer: Berlin/Heidelberg, Germany, 1993; pp. 524–540. [Google Scholar] [CrossRef]

- Potters, M.; Bouchaud, J.P. A First Course in Random Matrix Theory: For Physicists, Engineers and Data Scientists; Cambridge University Press: New York, NY, USA, 2020. [Google Scholar]

- Tao, T. Topics in Random Matrix Theory; American Mathematical Society: Providence, RI, USA, 2023; Volume 132. [Google Scholar]

- Laloux, L.; Cizeau, P.; Bouchaud, J.P.; Potters, M. Noise Dressing of Financial Correlation Matrices. Phys. Rev. Lett. 1999, 83, 1467–1470. [Google Scholar] [CrossRef]

- Chen, H.; Mai, Y.; Li, S.P. Analysis of network clustering behavior of the Chinese stock market. Phys. A Stat. Mech. Appl. 2014, 414, 360–367. [Google Scholar] [CrossRef]

- Jiang, X.F.; Chen, T.T.; Zheng, B. Structure of local interactions in complex financial dynamics. Sci. Rep. 2014, 4, 5321. [Google Scholar] [CrossRef]

- Jamali, T.; Jafari, G.R. Spectra of empirical autocorrelation matrices: A random-matrix-theory-inspired perspective. EPL (Europhys. Lett.) 2015, 111, 10001. [Google Scholar] [CrossRef]

- Kumar, S.; Kumar, S.; Kumar, P. Diffusion entropy analysis and random matrix analysis of the Indian stock market. Phys. A Stat. Mech. Appl. 2020, 560, 125122. [Google Scholar] [CrossRef]

- Saeedian, M.; Jamali, T.; Kamali, M.; Bayani, H.; Yasseri, T.; Jafari, G.R. Emergence of world-stock-market network. Phys. A Stat. Mech. Appl. 2019, 526, 120792. [Google Scholar] [CrossRef]

- Raei, R.; Namaki, A.; Vahabi, H. Analysis of collective behavior of Iran banking sector by random matrix theory. Iran. J. Financ. 2019, 3, 60–75. [Google Scholar] [CrossRef]

- Vahabi, H.; Namaki, A.; Raei, R. Comparing the collective behavior of banking industry in emerging markets versus mature ones by random matrix approach. Front. Phys. 2022, 10, 896303. [Google Scholar] [CrossRef]

- Taştan, B.; Imamoglu, H. The analysis of cross-correlation between Istanbul Stock Exchange and major stock markets and indices: An empirical analysis using Random Matrix Theory. Concurr. Comput. Pract. Exp. 2022, 34, e7113. [Google Scholar] [CrossRef]

- Bun, J.; Bouchaud, J.P.; Potters, M. Cleaning large correlation matrices: Tools from random matrix theory. Phys. Rep. 2017, 666, 1–109. [Google Scholar] [CrossRef]

- Heidari Haratemeh, M. Portfolio Optimization and Random Matrix Theory in Stock Exchange. Innov. Manag. Oper. Strateg. 2021, 2, 257–267. [Google Scholar]

- Namaki, A.; Shirazi, A.H.; Raei, R.; Jafari, G. Network analysis of a financial market based on genuine correlation and threshold method. Phys. A Stat. Mech. Appl. 2011, 390, 3835–3841. [Google Scholar] [CrossRef]

- Tang, Y.; Xiong, J.J.; Jia, Z.Y.; Zhang, Y.C. Complexities in Financial Network Topological Dynamics: Modeling of Emerging and Developed Stock Markets. Complexity 2018, 2018, 4680140. [Google Scholar] [CrossRef]

- Tang, Y.; Xiong, J.J.; Luo, Y.; Zhang, Y.C. How Do the Global Stock Markets Influence One Another? Evidence from Finance Big Data and Granger Causality Directed Network. Int. J. Electron. Commer. 2019, 23, 85–109. [Google Scholar] [CrossRef]

- Pafka, S.; Kondor, I. Noisy covariance matrices and portfolio optimization II. Phys. A Stat. Mech. Appl. 2003, 319, 487–494. [Google Scholar] [CrossRef]

- Laloux, L.; Cizeau, P.; Potters, M.; Bouchaud, J.P. Random matrix theory and financial correlations. Int. J. Theor. Appl. Financ. 2000, 3, 391–397. [Google Scholar] [CrossRef]

- Mantegna, R.N.; Stanley, H.E. An Introduction to Econophysics: Correlations and Complexity in Finance; Cambridge University Press: New York, NY, USA, 2000. [Google Scholar]

- Plerou, V.; Gopikrishnan, P.; Rosenow, B.; Amaral, L.A.N.; Stanley, H.E. A random matrix theory approach to financial cross-correlations. Phys. A Stat. Mech. Appl. 2000, 287, 374–382. [Google Scholar] [CrossRef]

- Plerou, V.; Gopikrishnan, P.; Rosenow, B.; Amaral, L.A.N.; Stanley, H.E. Econophysics: Financial time series from a statistical physics point of view. Phys. A Stat. Mech. Appl. 2000, 279, 443–456. [Google Scholar] [CrossRef]

- Plerou, V.; Gopikrishnan, P.; Rosenow, B.; Amaral, L.A.N.; Stanley, H.E. Collective behavior of stock price movements—A random matrix theory approach. Phys. A Stat. Mech. Appl. 2001, 299, 175–180. [Google Scholar] [CrossRef]

- Tola, V.; Lillo, F.; Gallegati, M.; Mantegna, R.N. Cluster analysis for portfolio optimization. J. Econ. Dyn. Control 2008, 32, 235–258. [Google Scholar] [CrossRef]

- Rosenow, B.; Plerou, V.; Gopikrishnan, P.; Amaral, L.A.N.; Stanley, H.E. Application of random matrix theory to study cross-correlations of stock prices. Int. J. Theor. Appl. Financ. 2000, 03, 399–403. [Google Scholar] [CrossRef]

- Burda, Z.; Jarosz, A.; Nowak, M.A.; Jurkiewicz, J.; Papp, G.; Zahed, I. Applying free random variables to random matrix analysis of financial data. Part I: The Gaussian case. Quant. Financ. 2011, 11, 1103–1124. [Google Scholar] [CrossRef]

- Bai, Z.; Liu, H.; Wong, W.K. Enhancement of the applicability of Markowitz’s portfolio optimization by utilizing random matrix theory. Math. Financ. 2009, 19, 639–667. [Google Scholar] [CrossRef]

- Biely, C.; Thurner, S. Random matrix ensembles of time-lagged correlation matrices: Derivation of eigenvalue spectra and analysis of financial time-series. Quant. Financ. 2008, 8, 705–722. [Google Scholar] [CrossRef]

- Luo, Y.; Xiong, J.; Dong, L.G.; Tang, Y. Statistical correlation properties of the SHIBOR interbank lending market. China Financ. Rev. Int. 2015, 5, 91–102. [Google Scholar] [CrossRef]

- Pafka, S.; Kondor, I. Estimated correlation matrices and portfolio optimization. Phys. A Stat. Mech. Appl. 2004, 343, 623–634. [Google Scholar] [CrossRef]

- Jiang, X.F.; Zheng, B. Anti-correlation and subsector structure in financial systems. EPL (Europhys. Lett.) 2012, 97, 48006. [Google Scholar] [CrossRef]

- Ouyang, F.; Zheng, B.; Jiang, X. Spatial and temporal structures of four financial markets in Greater China. Phys. A Stat. Mech. Appl. 2014, 402, 236–244. [Google Scholar] [CrossRef]

- Lim, K.; Kim, M.J.; Kim, S.; Kim, S.Y. Statistical properties of the stock and credit market: RMT and network topology. Phys. A Stat. Mech. Appl. 2014, 407, 66–75. [Google Scholar] [CrossRef]

- Namaki, A.; Raei, R.; Ardalankia, J.; Hedayatifar, L.; Hosseiny, A.; Haven, E.; Jafari, G.R. Analysis of the Global Banking Network by Random Matrix Theory. Front. Phys. 2021, 8, 586561. [Google Scholar] [CrossRef]

- Glasserman, P.; Young, H.P. Contagion in Financial Networks. J. Econ. Lit. 2016, 54, 779–831. [Google Scholar] [CrossRef]

- Elliott, M.; Golub, B.; Jackson, M.O. Financial Networks and Contagion. Am. Econ. Rev. 2014, 104, 3115–3153. [Google Scholar] [CrossRef]

- Li, F.; Kang, H.; Xu, J. Financial stability and network complexity: A random matrix approach. Int. Rev. Econ. Financ. 2022, 80, 177–185. [Google Scholar] [CrossRef]

- Amini, H.; Cont, R.; Minca, A. RESILIENCE TO CONTAGION IN FINANCIAL NETWORKS. Math. Financ. 2016, 26, 329–365. [Google Scholar] [CrossRef]

- Plerou, V.; Gopikrishnan, P.; Rosenow, B.; Amaral, L.A.N.; Guhr, T.; Stanley, H.E. Random matrix approach to cross correlations in financial data. Phys. Rev. E 2002, 65, 066126. [Google Scholar] [CrossRef]

- Alaoui, M.E. Random matrix theory and portfolio optimization in Moroccan stock exchange. Phys. A Stat. Mech. Appl. 2015, 433, 92–99. [Google Scholar] [CrossRef]

- Sharifi, S.; Crane, M.; Shamaie, A.; Ruskin, H. Random matrix theory for portfolio optimization: A stability approach. Phys. A Stat. Mech. Appl. 2004, 335, 629–643. [Google Scholar] [CrossRef]

- Kwapień, J.; Drożdż, S.; Oświe¸cimka, P. The bulk of the stock market correlation matrix is not pure noise. Phys. A Stat. Mech. Appl. 2006, 359, 589–606. [Google Scholar] [CrossRef]

- Nie, C.X. Analyzing financial correlation matrix based on the eigenvector–eigenvalue identity. Phys. A Stat. Mech. Appl. 2021, 567, 125713. [Google Scholar] [CrossRef]

- Pharasi, H.K.; Sharma, K.; Chakraborti, A.; Seligman, T.H. Complex Market Dynamics in the Light of Random Matrix Theory. In New Perspectives and Challenges in Econophysics and Sociophysics; Abergel, F., Chakrabarti, B.K., Chakraborti, A., Deo, N., Sharma, K., Eds.; Springer International Publishing: Cham, Switaerland, 2019; pp. 13–34. [Google Scholar] [CrossRef]

- Bun, J.; Bouchaud, J.P.; Potters, M. Overlaps between eigenvectors of correlated random matrices. Phys. Rev. E 2018, 98, 052145. [Google Scholar] [CrossRef]

- García-Medina, A.; Sandoval, L.; Bañuelos, E.U.; Martínez-Argüello, A. Correlations and flow of information between the New York Times and stock markets. Phys. A Stat. Mech. Appl. 2018, 502, 403–415. [Google Scholar] [CrossRef]

- Ji, J.; Huang, C.; Cao, Y.; Hu, S. The network structure of Chinese finance market through the method of complex network and random matrix theory. Concurr. Comput. Pract. Exp. 2019, 31, e4877. [Google Scholar] [CrossRef]

- Zitelli, G.L. Random matrix models for datasets with fixed time horizons. Quant. Financ. 2020, 20, 769–781. [Google Scholar] [CrossRef]

- Baruccaand, P.; Kieburg, M.; Ossipov, A. Eigenvalue and eigenvector statistics in time series analysis. EPL (Europhys. Lett.) 2020, 129, 60003. [Google Scholar] [CrossRef]

- Han, R.Q.; Xie, W.J.; Xiong, X.; Zhang, W.; Zhou, W.X. Market Correlation Structure Changes Around the Great Crash: A Random Matrix Theory Analysis of the Chinese Stock Market. Fluct. Noise Lett. 2017, 16, 1750018. [Google Scholar] [CrossRef]

- Yang, Y. Comparison and Analysis of Chinese and United States Stock Market. J. Financ. Risk Manag. 2020, 9, 44. [Google Scholar] [CrossRef]

- Zhang, Y.; Mao, J. COVID-19’s impact on the spillover effect across the Chinese and U.S. stock markets. Financ. Res. Lett. 2022, 47, 102684. [Google Scholar] [CrossRef]

- Jin, Z.; Guo, K. The Dynamic Relationship between Stock Market and Macroeconomy at Sectoral Level: Evidence from Chinese and US Stock Market. Complexity 2021, 2021, 6645570. [Google Scholar] [CrossRef]

- Chen, Y.; Pantelous, A.A. The U.S.-China trade conflict impacts on the Chinese and U.S. stock markets: A network-based approach. Financ. Res. Lett. 2022, 46, 102486. [Google Scholar] [CrossRef]

- Urama, T.C.; Ezepue, P.O.; Nnanwa, C.P. Analysis of Cross-Correlations in Emerging Markets Using Random Matrix Theory. J. Math. Financ. 2017, 7, 18. [Google Scholar] [CrossRef]

- Pharasi, H.K.; Sharma, K.; Chatterjee, R.; Chakraborti, A.; Leyvraz, F.; Seligman, T.H. Identifying long-term precursors of financial market crashes using correlation patterns. New J. Phys. 2018, 20, 103041. [Google Scholar] [CrossRef]

- Batondo, M.; Uwilingiye, J. Comovement across BRICS and the US Stock Markets: A Multitime Scale Wavelet Analysis. Int. J. Financ. Stud. 2022, 10, 27. [Google Scholar] [CrossRef]

- Vuong, G.T.H.; Nguyen, M.H.; Huynh, A.N.Q. Volatility spillovers from the Chinese stock market to the U.S. stock market: The role of the COVID-19 pandemic. J. Econ. Asymmetries 2022, 26, e00276. [Google Scholar] [CrossRef]

- Pan, Q.; Mei, X.; Gao, T. Modeling dynamic conditional correlations with leverage effects and volatility spillover effects: Evidence from the Chinese and US stock markets affected by the recent trade friction. N. Am. J. Econ. Financ. 2022, 59, 101591. [Google Scholar] [CrossRef]

- Ren, F.; Zhou, W.X. Dynamic Evolution of Cross-Correlations in the Chinese Stock Market. PLoS ONE 2014, 9, e97711. [Google Scholar] [CrossRef]

- Said, S.; Heuveline, S.; Mostajeran, C. Riemannian statistics meets random matrix theory: Toward learning from high-dimensional covariance matrices. IEEE Trans. Inf. Theory 2022, 69, 472–481. [Google Scholar] [CrossRef]

- Zhu, W.; Ma, X.; Zhu, X.H.; Ugurbil, K.; Chen, W.; Wu, X. Denoise Functional Magnetic Resonance Imaging With Random Matrix Theory Based Principal Component Analysis. IEEE Trans. Biomed. Eng. 2022, 69, 3377–3388. [Google Scholar] [CrossRef]

- Bouchaud, J.P.; Potters, M. Theory of Financial Risk and Derivative Pricing: From Statistical Physics to Risk Management; Cambridge University Press: New York, NY, USA, 2003. [Google Scholar]

- Rosenow, B.; Gopikrishnan, P.; Plerou, V.; Stanley, H.E. Dynamics of cross-correlations in the stock market. Phys. A Stat. Mech. Appl. 2003, 324, 241–246. [Google Scholar] [CrossRef]

- Giardina, I.; Bouchaud, J.P.; Mézard, M. Microscopic models for long ranged volatility correlations. Phys. A Stat. Mech. Appl. 2001, 299, 28–39. [Google Scholar] [CrossRef]

- Kenett, D.Y.; Huang, X.; Vodenska, I.; Havlin, S.; Stanley, H.E. Partial correlation analysis: Applications for financial markets. Quant. Financ. 2015, 15, 569–578. [Google Scholar] [CrossRef]

- Iori, G.; Masi, G.D.; Precup, O.V.; Gabbi, G.; Caldarelli, G. A network analysis of the Italian overnight money market. J. Econ. Dyn. Control 2008, 32, 259–278. [Google Scholar] [CrossRef]

- Tanaka-Yamawaki, M.; Yang, X.; Kido, T.; Yamamoto, A. Extracting Market Trends from the Cross Correlation between Stock Time Series. In Advanced Techniques for Knowledge Engineering and Innovative Applications: Proceedings of the 16th International Conference, KES 2012, San Sebastian, Spain, 10–12 September 2012; Revised Selected Papers; Tweedale, J.W., Jain, L.C., Eds.; Springer: Berlin/Heidelberg, Germany, 2013; pp. 25–38. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Market | Avg. Number | |||

|---|---|---|---|---|

| CSI163 | 3.0268 | 0.0061 | 0.0368 | 0.0186 |

| S&P468 | 7.2250 | 0.0107 | 0.0214 | 0.0154 |

| Top 10 | |||

|---|---|---|---|

| Rank | Tick | Stock Name | Industry |

| 1 | 2007 | Hualan Biological Engineering Inc. | Pharmaceuticals |

| 2 | 600,867 | Star Lake Bioscience Co., Inc. | Pharmaceuticals |

| 3 | 600,085 | Beijing Tongrentang Co., Ltd. | Pharmaceuticals |

| 4 | 963 | Huadong Medicine Co., Ltd. | Wholesale |

| 5 | 600,332 | Sichuan Hongda Co., Ltd. | Metals |

| 6 | 600,108 | Gansu Yasheng Industrial (Group) Co., Ltd. | Agriculture |

| 7 | 600,535 | Nanjing Chixia Development Co., Ltd. | Real estate |

| 8 | 600,277 | Jiangsu Hengrui Medicine Co., Ltd. | Pharmaceuticals |

| 9 | 600,089 | TBEA Co., Ltd. | Machinery |

| 10 | 999 | Sanjiu Medical & Pharmaceutical Co., Ltd. | Pharmaceuticals |

| Bottom 10 | |||

| Rank | Tick | Stock Name | Industry |

| 154 | 46 | Oceanwide Construction Group Co., Ltd. | Real estate |

| 155 | 601,988 | China Construction Bank | Finance |

| 156 | 2 | China Vanke Co., Ltd. | Real estate |

| 157 | 600,048 | Poly Real Estate Group Co., Ltd. | Real estate |

| 158 | 601,398 | Guangshen Railway | Transportation |

| 159 | 600,016 | China Minsheng Banking Corp. Ltd. | Finance |

| 160 | 600,015 | Hua Xia Bank Co., Ltd. | Finance |

| 161 | 1 | Shenzhen Development Bank Co., Ltd. | Finance |

| 162 | 600,036 | China Merchants Bank Co., Ltd. | Finance |

| 163 | 600,000 | Shanghai Pudong Development Bank | Finance |

| Top 10 | |||

|---|---|---|---|

| Rank | Tick | Stock Name | Industry |

| 1 | 999 | Sanjiu Medical & Pharmaceutical Co., Ltd. | Pharmaceuticals |

| 2 | 2007 | Hualan Biological Engineering Inc. | Pharmaceuticals |

| 3 | 629 | Panzhihua New Steel & Vanadium Co., Ltd. | Metals |

| 4 | 600,089 | TBEA Co., Ltd. | Machinery |

| 5 | 600,085 | Beijing Tongrentang Co., Ltd. | Pharmaceuticals |

| 6 | 538 | Yunnan Baiyao Industry Co., Ltd. | Pharmaceuticals |

| 7 | 963 | Huadong Medicine Co., Ltd. | Wholesale |

| 8 | 729 | Beijing Yanjing Brewery Co., Ltd. | Food & Beverage |

| 9 | 600,535 | Nanjing Chixia Development Co., Ltd. | Real estate |

| 10 | 600,332 | Sichuan Hongda Co., Ltd. | Metals |

| Bottom 10 | |||

| Rank | Tick | Stock Name | Industry |

| 459 | 157 | Changsha Zoomlion Heavy Industry | Machinery |

| 460 | 600,030 | CITIC Securities Co., Ltd. | Finance |

| 461 | 600,585 | Jiangsu Changjiang Electronics Technology | Electronics |

| 462 | 601,988 | China Construction Bank | Finance |

| 463 | 601,398 | Guangshen Railway | Transportation |

| 464 | 1 | Shenzhen Development Bank Co., Ltd. | Finance |

| 465 | 600,015 | Hua Xia Bank Co., Ltd. | Finance |

| 466 | 600,016 | China Minsheng Banking Corp. Ltd. | Finance |

| 467 | 600,036 | China Merchants Bank Co., Ltd. | Finance |

| 468 | 600,000 | Shanghai Pudong Development Bank Co., Ltd. | Finance |

| Top 10 | |||

|---|---|---|---|

| Rank | Tick | Stock Name | Industry |

| 1 | STI | SunTrust Banks | Financials |

| 2 | ZION | Zions Bancorp | Financials |

| 3 | MTB | M&T Bank Corp. | Financials |

| 4 | CMA | Comerica Inc. | Financials |

| 5 | WFC | Wells Fargo | Financials |

| 6 | BBT | BB&T Corporation | Financials |

| 7 | JPM | JPMorgan Chase & Co. | Financials |

| 8 | RF | Regions Financial Corp. | Financials |

| 9 | LEN | Lennar Corp. | Consumer Discretionary |

| 10 | PNC | PNC Financial Services | Financials |

| Bottom 10 | |||

| Rank | Tick | Stock Name | Industry |

| 459 | EOG | EOG Resources | Energy |

| 460 | MUR | Murphy Oil | Energy |

| 461 | OXY | Occidental Petroleum | Energy |

| 462 | HP | Helmerich & Payne | Energy |

| 463 | NBL | Noble Energy Inc. | Energy |

| 464 | XEC | Cimarex Energy | Energy |

| 465 | APC | Anadarko Petroleum Corp. | Energy |

| 466 | DO | Diamond Offshore Drilling | Energy |

| 467 | DVN | Devon Energy Corp. | Energy |

| 468 | APA | Apache Corporation | Energy |

| Top 10 | |||

|---|---|---|---|

| Rank | Tick | Stock Name | Industry |

| 1 | APA | Apache Corporation | Energy |

| 2 | DVN | Devon Energy Corp. | Energy |

| 3 | ETR | Entergy Corp. | Utilities |

| 4 | DO | Diamond Offshore Drilling | Energy |

| 5 | NBL | Noble Energy Inc. | Energy |

| 6 | APC | Anadarko Petroleum Corp. | Energy |

| 7 | FE | FirstEnergy Corp. | Utilities |

| 8 | OXY | Occidental Petroleum | Energy |

| 9 | MUR | Murphy Oil | Energy |

| 10 | XOM | Exxon Mobil Corp. | Energy |

| Bottom 10 | |||

| Rank | Tick | Stock Name | Industry |

| 459 | USB | US Bancorp | Financials |

| 460 | JPM | JPMorgan Chase & Co. | Financials |

| 461 | RF | Regions Financial Corp. | Financials |

| 462 | WFC | Wells Fargo | Financials |

| 463 | BBT | BB&T Corporation | Financials |

| 464 | PNC | PNC Financial Services | Financials |

| 465 | ZION | Zions Bancorp | Financials |

| 466 | CMA | Comerica Inc. | Financials |

| 467 | MTB | M&T Bank Corp. | Financials |

| 468 | STI | SunTrust Banks | Financials |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tang, Y.; Xiong, J.; Cheng, Z.; Zhuang, Y.; Li, K.; Xie, J.; Zhang, Y. Looking into the Market Behaviors through the Lens of Correlations and Eigenvalues: An Investigation on the Chinese and US Markets Using RMT. Entropy 2023, 25, 1460. https://doi.org/10.3390/e25101460

Tang Y, Xiong J, Cheng Z, Zhuang Y, Li K, Xie J, Zhang Y. Looking into the Market Behaviors through the Lens of Correlations and Eigenvalues: An Investigation on the Chinese and US Markets Using RMT. Entropy. 2023; 25(10):1460. https://doi.org/10.3390/e25101460

Chicago/Turabian StyleTang, Yong, Jason Xiong, Zhitao Cheng, Yan Zhuang, Kunqi Li, Jingcong Xie, and Yicheng Zhang. 2023. "Looking into the Market Behaviors through the Lens of Correlations and Eigenvalues: An Investigation on the Chinese and US Markets Using RMT" Entropy 25, no. 10: 1460. https://doi.org/10.3390/e25101460