1. Introduction

Financial Technology, commonly known as FinTech, has emerged as a transformative force in the financial industry, revolutionizing traditional banking, payments, investment, and other financial services. As the FinTech sector continues to grow rapidly, it becomes increasingly important to understand the research landscape surrounding this dynamic field. According to Kawai et al. [

1], who serves as the General Secretary of the International Association of Insurance Supervisors, a member organization of the Financial Stability Board, a working definition of “FinTech” can be described as a technologically facilitated financial innovation that encompasses new business models, applications, processes, and products. The implementation of FinTech has the potential to significantly affect financial markets, institutions, and the overall provision of financial services.

Financial technology (FinTech) is acknowledged as a highly significant advancement within the financial sector and is rapidly progressing, fueled by factors such as the sharing economy, favorable regulations, and advancements in information technology [

2]. FinTech holds the potential to revolutionize the financial industry by reducing expenses, enhancing the standard of financial services, and fostering a more inclusive and resilient financial environment.

At the same time, the utilization of internet and automated information processing has sparked innovation in the financial industry, resulting in cost savings, enhanced efficiency, speed, creativity, adaptability, and overall improvement in business processes [

3].

FinTech empowers consumers to manage independently their assets by offering automated platforms that utilize robo-advisors and operate on specific algorithms [

4]. These platforms enable individuals to take control of their finances and make informed decisions.

FinTech leverages big data analytics to gain deeper insights into consumer behaviors, needs, and demands, enabling the development of optimal solutions. This capability, previously the domain of big data and cloud technology companies, now resides within the realm of FinTech [

5].

The banking industry has experienced a significant impact from internet technology. From the perspective of banks, online banking offers a range of potential benefits, including reduced operational costs, access to real-time managerial information, improved internal communication, enhanced convenience in interacting with both existing and potential customers, and the provision of value-added services such as access to professional financial management expertise [

6].

On the other hand, the emergence of e-finance and mobile technology for financial companies, following the global financial crisis in 2008, paved the way for FinTech innovation. This progress was marked by the integration of e-finance innovation, internet technology, social networking services, social media, artificial intelligence, and big data analytics. FinTech encompasses six distinct business models: insurance services, crowdfunding, payment systems, lending platforms, wealth management solutions, and capital markets initiatives [

7].

The history of technological innovation in the financial sector commenced with the introduction of checks as a payment method in 1945. This was followed by the Bank of America’s creation of the first credit card in 1958, and the emergence of ATMs for facilitating financial transactions in 1967. Debit cards were subsequently introduced as transaction tools. In the 1990s, the advent of the internet led to the launch of internet banking services. In the 2000s, FinTech advancements such as mobile payments and crowdfunding were introduced. These milestones highlight the rapid growth of the FinTech industry, underscoring the need to review prior research in order to capture the evolution of financial services [

8].

Also, the literature review findings revealed that FinTech research encompassed various business processes, including payments, risk management and investment, financing through crowdfunding and P2P lending, market aggregators, as well as cryptocurrency and blockchain technology. Among these, the most prevalent research theme centered on the adoption of FinTech itself [

9].

Simultaneously, we have observed the emergence of individual FinTech startups that have started to capture specific segments of the financial services value chain and enhance their efficiency. Although FinTech has experienced substantial growth in recent years, it still needs to demonstrate its long-term viability, particularly in markets experiencing a downturn, to establish itself as a sustainable phenomenon [

10].

FinTech has evolved as a continuous process, wherein finance and technology have advanced in tandem, giving rise to a multitude of incremental and disruptive innovations. These innovations include internet banking, mobile payments, crowdfunding, peer-to-peer lending, and online identification [

11].

In terms of innovation, a significant number of FinTech advancements have focused on incremental enhancements, such as optimizing existing business processes through the utilization of mature technologies like mobile phone cameras for mobile payment solutions. Simultaneously, innovations have also affected various facets of FinTech, including the introduction of new services such as chatbots, artificial intelligence-based advisory services, and mobile bank accounts [

12].

FinTech solutions are currently offered not only by traditional banks and insurance companies but also by non-banks and non-insurers as providers of financial services. Moreover, the evolution of FinTech has demonstrated a shift in focus from intra-organizational solutions to customer-centric approaches such as business-to-customer (B2C), customer-to-customer (C2C), and provider-oriented business-to-business (B2B) inter-organizational models [

13,

14,

15,

16].

Presently, the financial industry is undergoing a profound transformation, marked by the emergence of innovative FinTech products that are challenging traditional banking offerings across various areas, including payments and investment advice. Blockchain technology, in particular, is revolutionizing numerous conventional banking services by providing enhanced transaction security, faster money transfers, and reduced costs on both domestic and global scales.

The disruptive nature of FinTech innovation has the potential to reshape the entire financial landscape in the coming years. As with any disruptive force, the true impact of FinTech innovations will become increasingly apparent as the market evolves. This section examines six key challenges faced by both FinTech startups and traditional financial institutions during this era of disruptive innovation: investment management, customer management, regulation, technology integration, security and privacy, and risk management [

7]. The growth of the FinTech market has resulted in the introduction of innovative solutions that significantly enhance the customer experience by offering a wide range of efficient and diverse financial services [

17].

The combination of the global financial crisis in 2008 and the integration of modern technological advancements, including social media, artificial intelligence (AI), and data analytics, propelled FinTech to emerge as a new paradigm. The FinTech ecosystem (FE) encompasses five interconnected elements that collaborate synergistically to drive economic growth, improve customer experiences, and foster social inclusion. These elements include start-ups, technology firms, government bodies, customers, and traditional financial institutions such as banks [

7].

Some other authors categorize FinTech as a disruptive innovation and delve into the primary business models in which FinTech operates. They extensively discuss the roles played by blockchain, crowdfunding, payments, insurance, wealth and asset management, big data analysis, and application programming interface [

18].

FinTech ecosystems exhibit distinct features such as heterogeneity, non-linearity, dynamism, and complexity due to their intricate network of agents. These agents interact with each other to offer a diverse range of financial products and services to end customers. As complementary technologies continue to emerge, the complexity of FinTech ecosystems grows exponentially, with new players entering the scene and new connections being established [

19]. Despite the considerable attention that FinTech ecosystems have garnered from both academia and industry, our understanding of the emergence of such ecosystems remains limited.

At the same time, crowdfunding offers a fresh approach for founders to secure funding for a diverse range of projects. This innovative concept finds its foundation in the broader concept of crowdsourcing, which involves tapping into the collective wisdom of the crowd to acquire ideas, feedback, and solutions to advance corporate endeavors [

20,

21]. In this regard, if there is a need to apply interest on the amount involved in rewards-based crowdfunding, the borrowers have the autonomy to determine the interest rate that suits them best.

Additionally, they can provide assurance of repayment within the specified timeframe [

22]. Entrepreneurs can utilize crowdfunding as a means to secure funding by making an open call on the internet. However, for crowdfunding to become a feasible alternative to the traditional investor- or creditor-based funding methods like banks, business angels, or venture capital, it is crucial to establish a community that derives additional private benefits from participating in the crowdfunding process [

23]. At the same time, investors participating in crowdfunding campaigns are offered assets in exchange for their funds, which can take the form of either regular interest payments or an ownership stake in the funded organization [

24].

On the other hand, it has been suggested that although FinTech firms may capture a portion of the market share from banks, it is not anticipated that they would completely replace banks. Nevertheless, banks are urged to expedite their adoption of innovative technologies in order to remain competitive with FinTech firms. Additionally, it is proposed that strategic partnerships and collaborations between banks and FinTech companies could be established in a mutually beneficial manner, offering advantages to both sides [

25].

Undoubtedly, financial technology (FinTech) stands out as one of the most prominent recent innovations within the financial sector. Its remarkable ability to potentially revolutionize the financial landscape by offering convenience and enhanced security in financial transactions has garnered significant recognition. The advent of this groundbreaking FinTech technology is reshaping the world, creating a distinctive biosphere characterized by streamlined transactions and heightened security [

26].

A cutting-edge FinTech solution is accessible anytime and anywhere for various transactional needs, such as hailing a ride, shopping at a local store, or engaging in online transactions. This innovation is significantly transforming the financial sector by reducing costs, enhancing the quality of financial services, and enabling organizations to manage efficiently their finances while ensuring robust security against cyber-attacks [

27].

The convergence of the digital and physical realms has given rise to new approaches to customer interaction [

28]. Over the past decade, there has been a notable surge in the frequency of customer engagement through various interaction channels. To adapt to this trend, financial service providers have introduced hybrid client interactions, which have contributed to the widespread adoption of FinTech.

In addition, the advent of recent technological innovations has brought about significant changes in financial information flows, resulting in the emergence of novel competitive and cooperative mechanisms that facilitate the creation and distribution of value [

29].

The FinTech industry continues to demonstrate its resilience and growth potential, despite experiencing a decrease in financing during Q2 2022 [

30]. With a 39% decline compared to Q4 2021, it reached its lowest level in the previous five quarters. However, this setback did not deter the global FinTech sector, as it managed to raise an impressive

$21.5 billion during the same period, making it the sector with the highest number of investment rounds worldwide.

The widespread adoption of FinTech services is evident, with approximately 90% of people in the USA currently utilizing these digital financial solutions [

30]. This high level of adoption reflects the shift towards customer-focused digital processes, which have been further accentuated by global quarantines and lockdowns. Looking ahead, the FinTech market is projected to experience substantial growth, with estimates suggesting a value surge from

$110.57 billion in 2020 to a staggering

$698.48 billion by 2030 [

30].

In terms of specific trends, open banking is predicted to witness significant growth, with an estimated 63.8 million users anticipated by 2024, representing a nearly fivefold increase compared to 2020 [

30]. Additionally, the number of individuals holding at least one neobank account is expected to reach 39.1 million by 2025, up from 20 million in 2021 [

30]. The reliance on artificial intelligence (AI) and machine learning within the FinTech industry is also noteworthy, as the global market for AI in FinTech is projected to reach

$26.67 billion by 2026. Moreover, Chime, one of the leading neobanks in the US, has amassed over 13 million users who access their personal banking services through the Chime mobile banking app.

The digitization of financial services has the potential to redirect the flow of financial information away from established incumbents and traditional infrastructures, leading to potential instability in established ecosystems. One example of this is the rise of peer-to-peer payments, which enables individuals to transfer funds directly between themselves, bypassing the payment infrastructures that have been collectively developed and funded by traditional banks. As a result, the introduction of such innovations is affecting the existing competitive and cooperative dynamics among industry participants [

31].

The present study aims to address the existing gaps and provide a novel contribution to the field of FinTech research. Although there is a growing volume of FinTech research, there is a lack of standardized best practices and methodological norms for researchers to rely on [

32]. This study recognizes the early stages of development in the field of FinTech research, suggesting that it is still in its infancy [

13].

To overcome these challenges and provide valuable insights, the study proposes the use of bibliometric analysis. This quantitative method utilizes data from scientific publications to examine various aspects of the FinTech research field. By analyzing publication records, citation patterns, collaboration networks, and other bibliographic indicators, researchers can gain a comprehensive understanding of the intellectual structure and impact of FinTech research.

Through this bibliometric analysis, the study aims to uncover trends, patterns, and influential factors driving advancements in FinTech research. This includes identifying key topics, leading researchers, influential institutions, and emerging trends within the multidisciplinary field of FinTech. By doing so, the study will provide a novel perspective and contribute to the growing body of knowledge in the FinTech research domain.

The objective of this article is to present a comprehensive bibliometric analysis of research on financial technology, exploring the evolution of FinTech literature, identifying influential contributors, and uncovering the most prominent research themes. By examining a vast array of scholarly publications, including academic articles, conference papers, and patents, this analysis aims to provide researchers, industry professionals, and policymakers with valuable insights into the current state and future directions of FinTech research.

This article will proceed by outlining the methodology employed for the bibliometric analysis, including data collection, bibliographic databases, and selection criteria. It will then present an overview of the global research output in FinTech, including publication trends, geographic distribution, and collaboration patterns among researchers and institutions.

Furthermore, the article will delve into the analysis of highly cited papers, top authors, and leading academic journals, elucidating the knowledge hubs and influential figures driving FinTech research. In addition to analyzing the overall landscape, this article will highlight the emerging research themes within FinTech, such as blockchain technology, digital payments, robo-advisors, peer-to-peer lending, and regulatory frameworks. By exploring these thematic clusters and their interconnectedness, we can gain a deeper understanding of the critical areas where research efforts are concentrated, and identify potential avenues for future research and innovation.

Overall, this bibliometric analysis aims to provide a comprehensive overview of the research landscape in financial technology, enabling stakeholders to navigate the vast body of knowledge, identify research gaps, and foster collaborations. Understanding the dynamics of FinTech research is essential for driving advancements in this rapidly evolving field and harnessing the transformative power of technology to shape the future of finance.

This article is structured into several sections to explore bibliometric analysis related to financial technology. The subsequent section focuses on the data and methodology, outlining the sources used and the research approach employed. Following this, the third section presents the data analysis, utilizing statistical tools and algorithms to examine trends and correlations within the collected data. A thematic analysis is then conducted in the fourth section to identify and explore key themes emerging from the findings. The fifth section incorporates a comprehensive document analysis, examining relevant literature and regulations. Finally, the last section provides a concise summary of the study’s main findings, their significance, and recommendations for future research and industry practices, while reflecting on the theoretical implications of the study.

2. Data and Methodology

The methodology employed in this study involved a bibliometric analysis to explore the field of financial technology (FinTech) research. This section provides a detailed overview of the fundamental search key strings, identification criteria, selection criteria, synthesis technique, and quality assessment of the bibliometric data utilized.

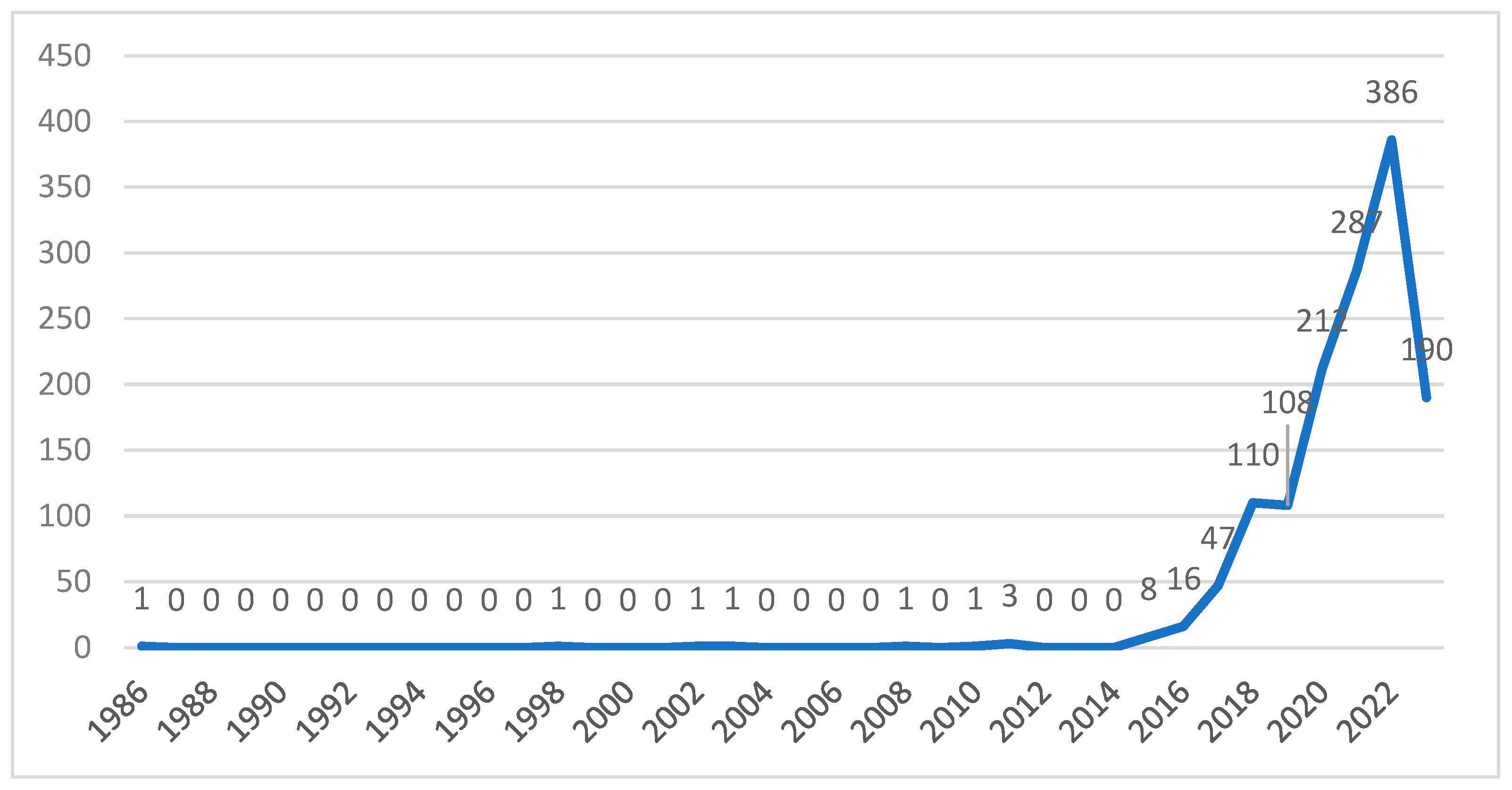

Data Collection: The study used “FINTECH” or “Financial Technology” as the primary search keywords to identify relevant articles for analysis. The initial search yielded a total of 1972 articles that met this criterion. Subsequently, a selection process was implemented to refine the dataset.

Sample Selection: To ensure consistency and focus on a specific linguistic context, only English-language articles were selected for further analysis. This language restriction reduced the dataset to 1945 articles. The final database comprised 1373 publications, covering various disciplines such as business, management and accounting, economics, finance, and social sciences. These disciplines were chosen to align with the research area of FinTech.

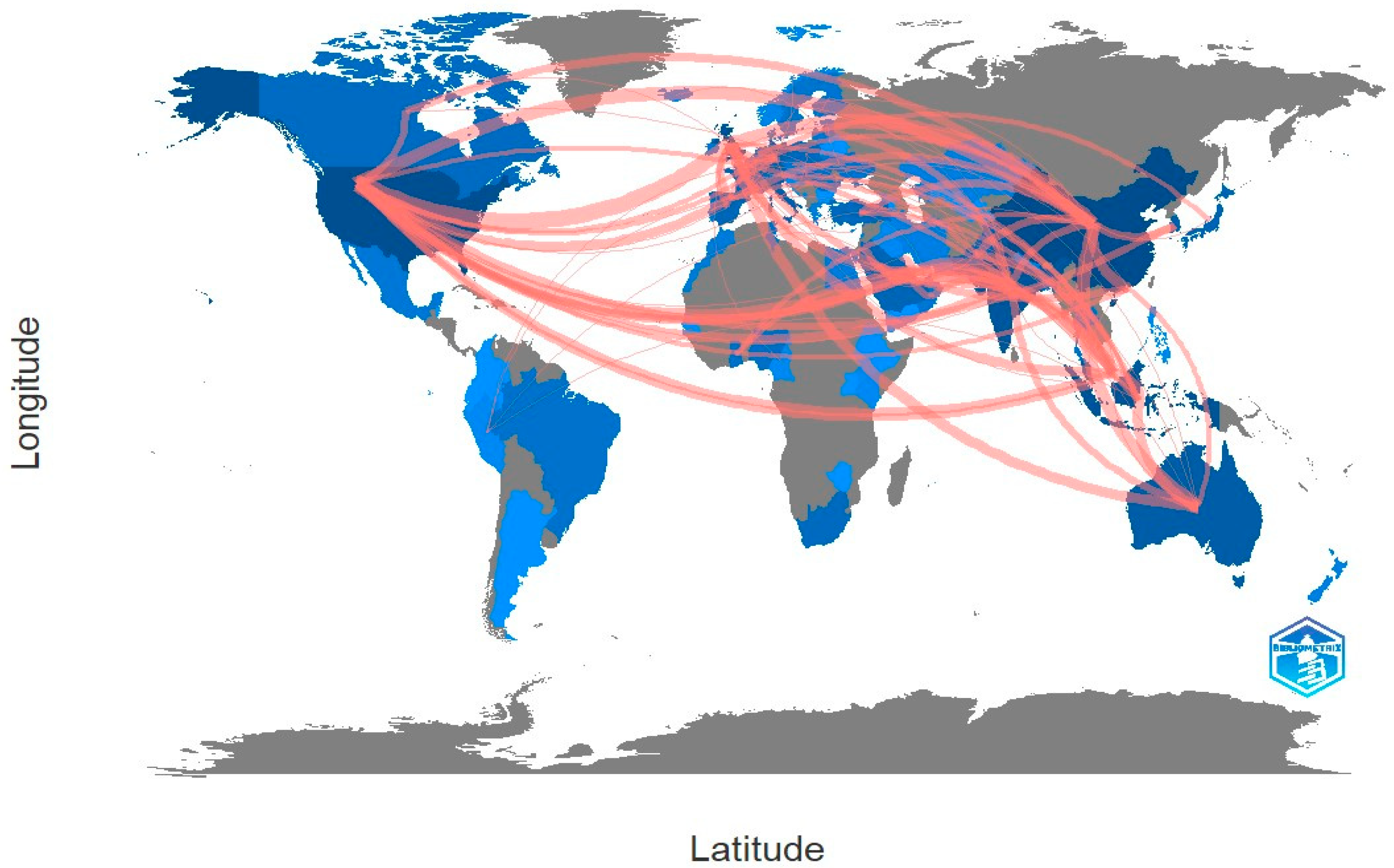

Data Analysis: The study employed a variety of bibliometric analytic approaches to analyze the collected data. Frequency tables were utilized to examine the publications based on different parameters, including year of publication, nation of origin, and authorship. This analysis provided insights into temporal trends, geographic distribution, and prominent authors within the field of FinTech research.

To identify the most influential articles, citation analysis was conducted to determine the citation count and impact of each publication. These influential articles played a crucial role in shaping the field of FinTech research.

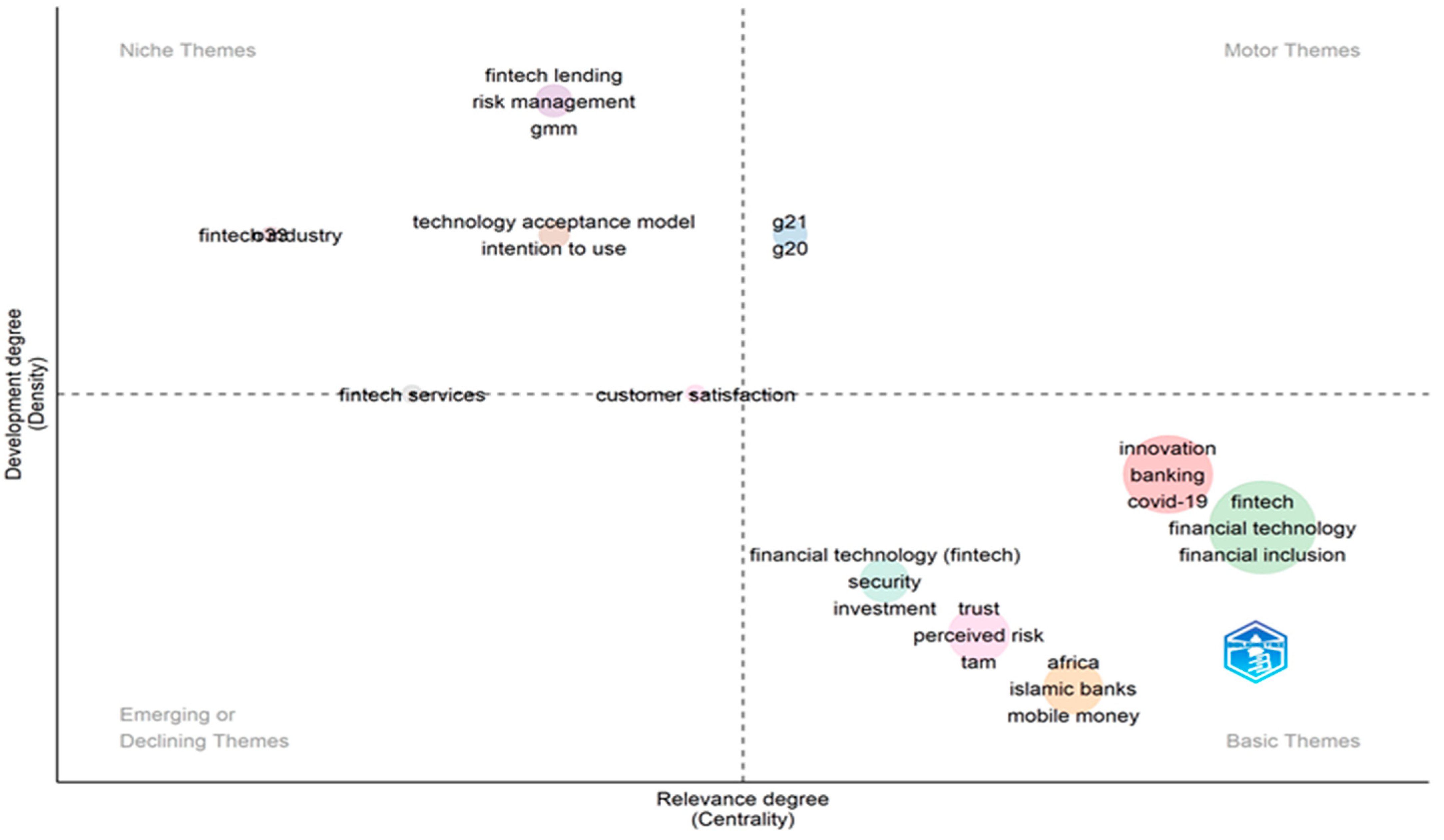

Keyword analysis and thematic mapping techniques were applied to identify prevailing topics and themes within the field. This analysis provided a deeper understanding of the research focus areas and emerging trends in FinTech.

To conduct the synthesis analysis, the study utilized biblioshiny software [

33]. This software facilitated the organization and analysis of the bibliometric data, allowing for a comprehensive synthesis of the findings. Additionally, Lotka’s Law and Bradford’s Law were applied to measure the reliability and distribution patterns of the publications within the dataset, enhancing the quality assessment of the bibliometric analysis.

Table 1 summarized the methodological steps.

The methodology employed in this study provided a rigorous framework for conducting the bibliometric analysis of FinTech research. By specifying the search key strings, identification criteria, selection criteria, synthesis technique, and quality assessment of the bibliometric data, this article ensures transparency and validity in the research process (

Table 2). The utilization of various bibliometric analytic approaches and software tools strengthens the reliability of the findings and contributes to the growing body of knowledge in the field of FinTech research.

5. Documents Analysis

This section summarises the literature related to the highly cited articles related to “Financial Technology”.

Gomber et al. (2018) conducted a study “On the Fintech Revolution: Interpreting the Forces of Innovation, Disruption, and Transformation in Financial Services” and provides a comprehensive examination of the impact of financial technology (FinTech) on the financial services industry [

34]. Through a detailed analysis of innovation, disruption, and transformation, the paper explores the dynamic forces driving the FinTech revolution. It delves into the key aspects of FinTech, including technological advancements, changing consumer behavior, regulatory challenges, and the emergence of new business models. By interpreting these forces, the paper offers valuable insights into the transformative power of FinTech and its implications for the future of financial services.

Additionally, a paper titled “Fintech: Ecosystem, Business Models, Investment Decisions, and Challenges” provides a comprehensive overview of the FinTech landscape, including its ecosystem, various business models, factors influencing investment decisions, and the challenges faced by FinTech companies [

7]. The paper explores the interconnectedness of technology, finance, and entrepreneurship, highlighting the disruptive potential of FinTech in revolutionizing traditional financial services. It examines different business models adopted by FinTech firms, ranging from payment solutions and lending platforms to robo-advisory services and blockchain applications. Additionally, the paper addresses the factors that influence investment decisions in the FinTech sector, such as market trends, regulatory frameworks, and technological advancements. It also identifies and analyzes the challenges faced by FinTech companies, including cybersecurity risks, regulatory compliance, customer trust, and scalability issues. Overall, the paper offers a comprehensive understanding of the FinTech industry, its business models, investment dynamics, and the hurdles it must overcome to thrive in the financial services landscape.

Moreover, Gomber et al. (2017) published “Digital Finance and FinTech: Current Research and Future Research Directions” and provided an overview of the current state of research in digital finance and FinTech while highlighting potential areas for future exploration [

35]. The paper discusses the transformative impact of digital technologies on financial services and the emergence of FinTech as a catalyst for innovation in the industry. It explores various research topics within digital finance and FinTech, including blockchain technology, digital payments, crowdfunding, online lending, and regulatory frameworks. The paper also addresses the importance of interdisciplinary research and collaboration between academia, industry, and policymakers to further advance knowledge in this rapidly evolving field. By identifying research gaps and suggesting future directions, the paper serves as a roadmap for researchers seeking to contribute to the growing body of knowledge in digital finance and FinTech.

Another important paper, entitled “Fintech, Regulatory Arbitrage, and the Rise of Shadow Banks”, examines the relationship between financial technology (FinTech), regulatory arbitrage, and the emergence of shadow banks [

36].

The paper highlights how FinTech companies, by leveraging technological innovations and operating outside traditional regulatory frameworks, have disrupted the financial industry and created new avenues for regulatory arbitrage. It explores the risks and challenges associated with the rise of shadow banks, including potential systemic risks, regulatory loopholes, and consumer protection concerns. The paper sheds light on the evolving regulatory landscape and the need for effective oversight to ensure financial stability and consumer welfare in the context of FinTech and shadow banking activities.

Lastly, the paper “The Economics of Mobile Payments: Understanding Stakeholder Issues for an Emerging Financial Technology Application” delves into the economic aspects of mobile payments and provides insights into the various concerns faced by stakeholders in this emerging field [

37]. The paper explores the economic implications of mobile payment systems, including their impact on transaction costs, efficiency, and consumer behavior. It examines the perspectives of different stakeholders, such as merchants, consumers, financial institutions, and technology providers, shedding light on their concerns regarding security, privacy, interoperability, adoption, and revenue models. By understanding these stakeholder issues, the paper aims to provide a comprehensive understanding of the economics surrounding mobile payments and offers valuable insights for policymakers, industry players, and researchers seeking to navigate this evolving financial technology application.

Together, the above papers provide valuable insights into the transformative power, challenges, and regulatory considerations surrounding FinTech, guiding industry practitioners, policymakers, and researchers in navigating this dynamic field. As a result of the review is presented a table summarizing the main contributions in the field (

Table 8).

6. Conclusions

In conclusion, this article has presented a comprehensive bibliometric analysis of research on financial technology (FinTech), offering valuable insights into the research landscape, trends, and influential factors within this dynamic field.

The findings of this analysis highlight the growing importance of FinTech as a research area, with a substantial increase in the number of publications over the years. The geographic distribution of research output demonstrates a global interest in FinTech, with contributions from various countries and regions. Furthermore, collaboration networks reveal the interconnectedness of researchers and institutions, emphasizing the collaborative nature of FinTech research.

The identification of highly cited papers, top authors, and leading academic journals provides valuable insights into the knowledge hubs and influential figures driving FinTech research. These key contributors serve as a valuable resource for researchers and industry professionals seeking expertise and guidance in the field. Moreover, the analysis of emerging research themes within FinTech has shed light on critical areas of focus, such as blockchain technology, digital payments, robo-advisors, peer-to-peer lending, and regulatory frameworks. These thematic clusters represent areas of active research and innovation, where further exploration and advancements are expected.

Financial advisors can leverage the insights from this analysis to enhance their practices. By staying updated on the latest trends and developments in FinTech, advisors can identify areas of opportunity for integrating FinTech solutions into their advisory services. Understanding the current state and future directions of AI in FinTech can guide advisors in utilizing AI-powered tools to enhance their decision-making processes and provide more accurate and personalized recommendations to clients.

Insights into digital payment solutions can help financial advisors explore and adopt innovative payment technologies, streamlining transactions and enhancing convenience and security for their clients. Furthermore, understanding emerging regulatory frameworks related to FinTech enables advisors to navigate compliance requirements and stay informed about the legal implications of utilizing specific FinTech solutions in their practice.

The analysis also reveals collaboration patterns among researchers and institutions within the FinTech domain. Financial advisors can leverage this information to identify potential collaboration opportunities with academic institutions, FinTech startups, or other industry players. Collaborations can facilitate knowledge exchange, access to cutting-edge technologies, and the development of innovative solutions tailored to the needs of financial advisory clients.

By incorporating these practical implications into their practice, financial advisors can harness the findings of the bibliometric analysis to enhance their service offerings, improve client experiences, and stay competitive in an increasingly technology-driven financial landscape.

In conclusion, the comprehensive understanding gained through this bibliometric analysis serves as a valuable resource for financial advisors, empowering them to leverage FinTech innovations and technologies effectively in their advisory practice and ultimately deliver enhanced value to their clients. As FinTech continues to evolve, further bibliometric analyses will be essential to track and understand emerging trends, technological advancements, and regulatory developments within the field. By leveraging the insights gained from bibliometric analysis, stakeholders can make informed decisions, promote collaboration, and contribute to the advancement of FinTech research and its real-world applications.

{kind=link}

{kind=link}

{kind=link}

{kind=link}