Financial Inclusion, Fintech, and Income Inequality in Africa

Abstract

:1. Introduction

2. Literature Review

3. Materials and Methods

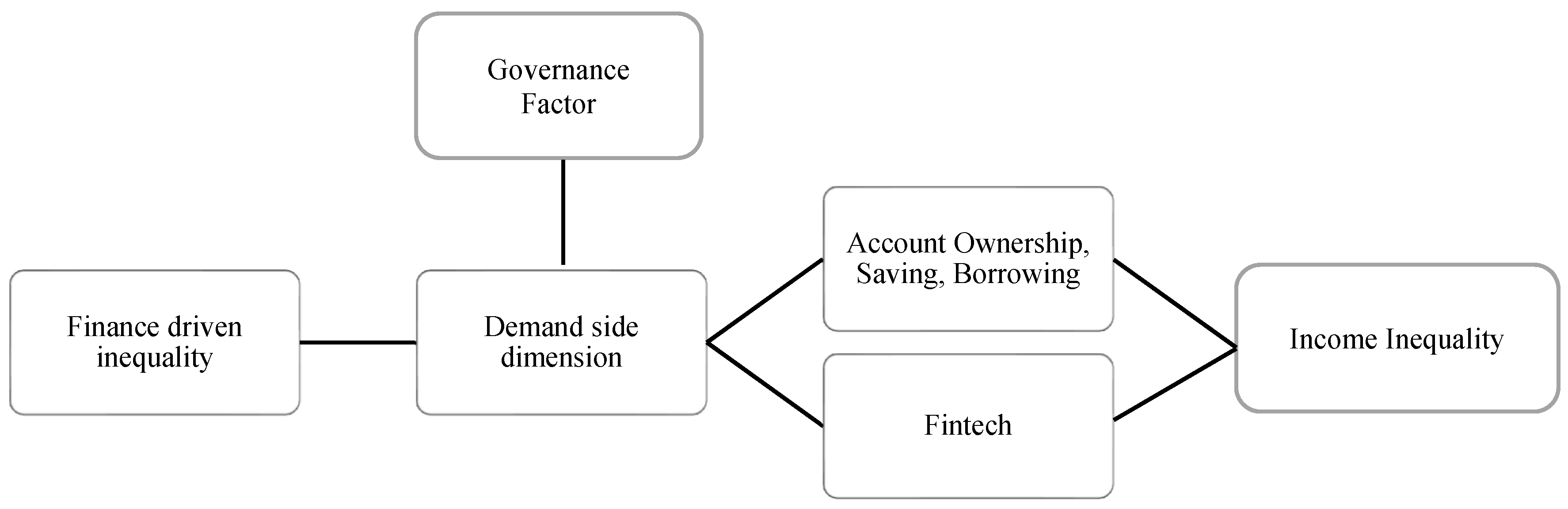

3.1. Model Specification

3.2. Data

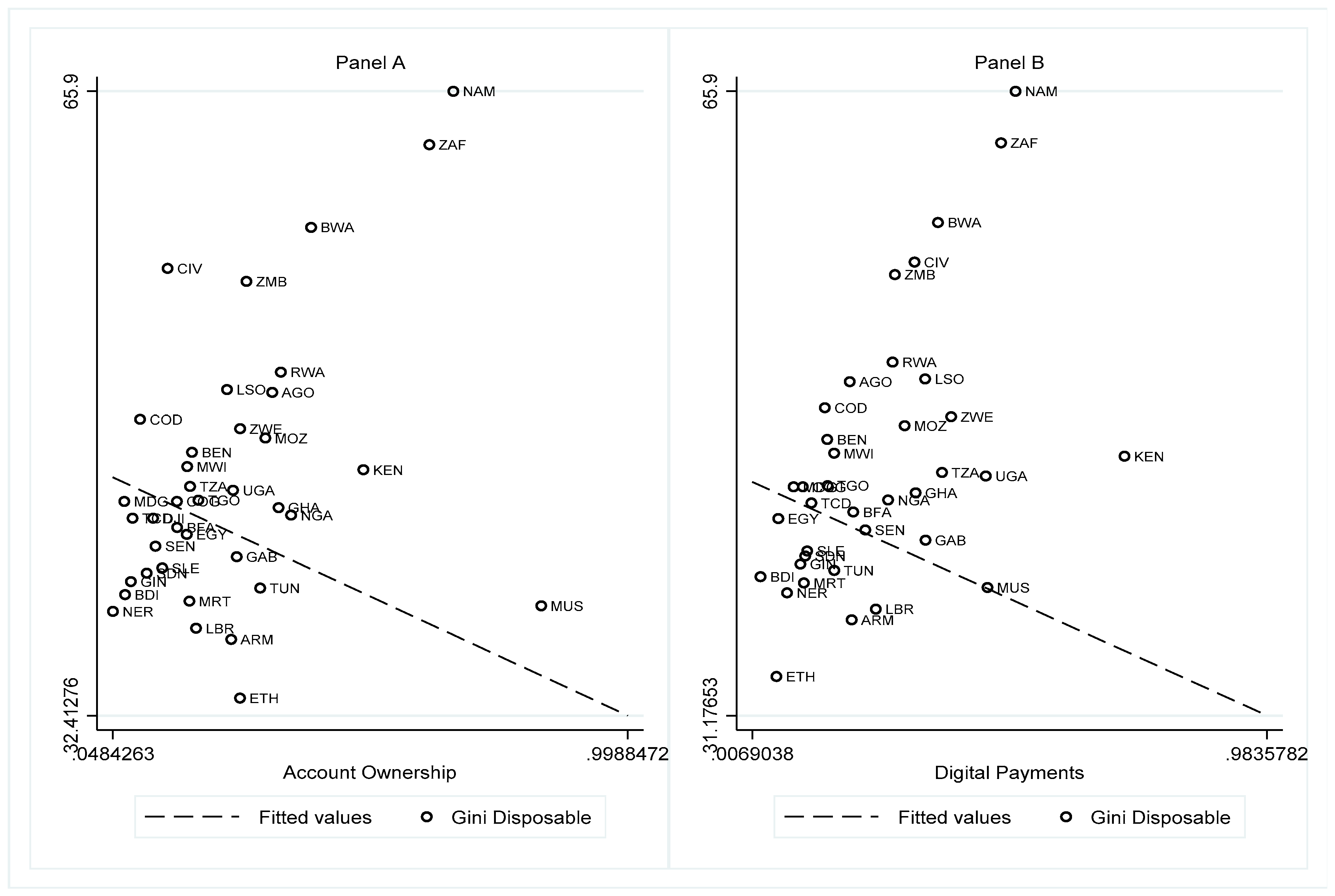

4. Empirical Results

5. Concluding Remark

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Furceri, D.; Ostry, J.D. Robust determinants of income inequality. Oxf. Rev. Econ. Policy 2019, 35, 460–517. [Google Scholar] [CrossRef] [Green Version]

- Alvaredo, F.; Atkinson, A.B.; Piketty, T.; Saez, E. The Top 1 Percent in International and Historical Perspective. J. Econ. Perspect. 2013, 27, 3–20. [Google Scholar] [CrossRef] [Green Version]

- Atkinson, A.B. Top incomes in the UK over the 20th century. J. R. Statist. Soc. A 2005, 168, 325–343. [Google Scholar] [CrossRef]

- Forbes, K.J. A reassessment of the relationship between inequality and growth. Am. Econ. Rev. 2000, 90, 869–887. [Google Scholar] [CrossRef] [Green Version]

- Piketty, T.; Yang, L.; Zucman, G. Capital Accumulation, Private Property, and Rising Inequality in China, 1978–2015. Am. Econ. Rev. 2019, 109, 2469–2496. [Google Scholar] [CrossRef] [Green Version]

- Rehman, F.U.; Islam, M.M. Financial infrastructure—Total factor productivity (TFP) nexus within the purview of FDI outflow, trade openness, innovation, human capital and institutional quality: Evidence from BRICS economies. Appl. Econ. 2022, 1–19. [Google Scholar] [CrossRef]

- IFC. Digital Access: The Future of Financial Inclusion in Africa. In International Financial Corporation 2018, World Bank Group (Issue November); International Finance Corporation: Washington, DC, USA, 2018; Available online: https://www.ifc.org/wps/wcm/connect/aa5e09c7-121e-4588-803a-52ef56b846b2/201805_Digital-Access_The-Future-of-Financial-Inclusion-in-Africa_v1.pdf?MOD=AJPERES (accessed on 1 May 2022).

- Robilliard, A.-S. What’s New About Income Inequality in Africa? In World Inequality Lab (Issue Brief 2020-03); World Inequality Lab, Paris School of Economics: Paris, France, 2020. [Google Scholar]

- Le, Q.H.; Ho, H.L.; Mai, N.C. The impact of financial inclusion on income inequality in transition economies. Manag. Sci. Lett. 2019, 9, 661–672. [Google Scholar] [CrossRef]

- Neaime, S.; Gaysset, I. Financial inclusion and stability in MENA: Evidence from poverty and inequality. Financ. Res. Lett. 2018, 24, 199–220. [Google Scholar] [CrossRef]

- Park, C.Y.; Mercado, R.J. Financial Inclusion, Poverty, and Income Inequality in Developing Asia. In SSRN Electronic Journal (Issue 426); SSRN: Amsterdam, The Netherlands, 2015. [Google Scholar] [CrossRef] [Green Version]

- Demir, A.; Pesqué-Cela, V.; Altunbas, Y.; Murinde, V. Fintech, financial inclusion and income inequality: A quantile regression approach. Eur. J. Financ. 2020, 4364, 86–107. [Google Scholar] [CrossRef]

- Martínez Turégano, D.; García Herrero, A. Financial Inclusion, Rather Than Size, Is the Key To Tackling Income Inequality. Singap. Econ. Rev. 2018, 63, 167–184. [Google Scholar] [CrossRef] [Green Version]

- Omar, M.A.; Inaba, K. Does financial inclusion reduce poverty and income inequality in developing countries? A panel data analysis. J. Econ. Struct. 2020, 9, 37. [Google Scholar] [CrossRef]

- Khan, I.; Khan, I.; Sayal, A.U.; Khan, M.Z. Does financial inclusion induce poverty, income inequality, and financial stability: Empirical evidence from the 54 African countries? J. Econ. Stud. 2021, 49, 303–314. [Google Scholar] [CrossRef]

- Kim, J.H. A study on the effect of financial inclusion on the relationship between income inequality and economic growth. Emerg. Mark. Financ. Trade 2016, 52, 498–512. [Google Scholar] [CrossRef]

- Park, C.Y.; Mercado, R. Financial Inclusion, Poverty, and Income Inequality. Singap. Econ. Rev. 2018, 63, 185–206. [Google Scholar] [CrossRef]

- Kling, G.; Pesqué-Cela, V.; Tian, L.; Luo, D. A theory of financial inclusion and income inequality. Eur. J. Financ. 2020, 28, 137–157. [Google Scholar] [CrossRef]

- Asongu, S.A.; Odhiambo, N.M. How enhancing information and communication technology has affected inequality in Africa for sustainable development: An empirical investigation. Sustain. Dev. 2019, 27, 647–656. [Google Scholar] [CrossRef] [Green Version]

- Tchamyou, V.S.; Asongu, S.A.; Odhiambo, N.M. The Role of ICT in Modulating the Effect of Education and Lifelong Learning on Income Inequality and Economic Growth in Africa. Afr. Dev. Rev. 2019, 31, 261–274. [Google Scholar] [CrossRef]

- Wellen, L.; Van Dijk, M.P. New Financial Technologies and 4Th Industrial Revolution in the Third World (the Example of Customer Care of M-Pesa, Kenya). EUrASEANs J. Glob. Socio-Econ. Dyn. 2018, 2, 7–12. [Google Scholar] [CrossRef] [Green Version]

- Chêne, M. The Impact of Corruption on Growth and Inequality. Transpar. Int. 2014, 1–11. [Google Scholar]

- Ben Ali, M.S.; Fhima, F.; Nouira, R. How does corruption undermine banking stability? A threshold nonlinear framework. J. Behav. Exp. Financ. 2020, 27, 100365. [Google Scholar] [CrossRef]

- Ng, D. The impact of corruption on financial markets. Manag. Finance 2006, 32, 822–836. [Google Scholar] [CrossRef]

- Wei, F.; Kong, Y. Corruption, financial development and capital structure: Evidence from China. China Financ. Rev. Int. 2017, 7, 295–322. [Google Scholar] [CrossRef]

- Adams, S.; Klobodu, E.K.M. Financial development, control of corruption and income inequality. Int. Rev. Appl. Econ. 2016, 30, 790–808. [Google Scholar] [CrossRef]

- Adeleye, N.; Osabuohien, E.; Bowale, E. The Role of Institutions in the Finance-Inequality Nexus in Sub-Saharan Africa. J. Context. Econ. 2017, 137, 173–192. [Google Scholar] [CrossRef]

- Ha, L.T.; Kim, J.; Lee, M. Institutional Quality, Trade Openness, and Financial Sector Development in Asia: An Empirical Investigation. Emerg. Mark. Financ. Trade 2016, 52, 1047–1059. [Google Scholar] [CrossRef] [Green Version]

- Aluko, O.A.; Azeez, B.A. Effectiveness of legal institutions in stock market development in sub-Saharan Africa. Econ. Chang. Restruct. 2019, 52, 439–451. [Google Scholar] [CrossRef]

- Hasan, I.; Horvath, R.; Mares, J. Finance and wealth inequality. J. Int. Money Financ. 2020, 108, 102161. [Google Scholar] [CrossRef] [Green Version]

- Kuznets, S. Economic Growth and Income Inequality. Am. Econ. Rev. 1955, 45, 1–28. Available online: http://links.jstor.org/sici?sici=0002-8282%28195503%2945%3A1%3C1%3AEGAII%3E2.0.CO%3B2-Y (accessed on 1 May 2022).

- Njikam, O. Financial liberalization and growth in African economies: The role of policy complementarities. Rev. Dev. Financ. 2017, 7, 73–83. [Google Scholar] [CrossRef]

- Harrison, A.; McLaren, J.; McMillan, M. Recent perspectives on trade and inequality. Annu. Rev. Econ. 2011, 3, 261–289. [Google Scholar] [CrossRef] [Green Version]

- Tanninen, H. Income inequality, government expenditures and growth. Appl. Econ. 1999, 31, 1109–1117. [Google Scholar] [CrossRef]

- Monnin, P. Inflation and income inequality in developed and developing countries. In CEP Working Pape; SSRN: Amsterdam, The Netherlands, 2014; Volume 1. [Google Scholar] [CrossRef]

- Rougoor, W.; Van Marrewijk, C. Demography, Growth, and Global Income Inequality. World Dev. 2015, 74, 220–232. [Google Scholar] [CrossRef]

- Porta, R.L.; Lopez-de-Silanes, F.; Shleifer, A. Law and Finance. J. Political Econ. 1998, 106, 1113–1155. [Google Scholar] [CrossRef]

- Clarke, G.R.G.; Xu, L.C.; Zou, H.-F. Finance and Income Inequality: What Do the Data Tell Us? South. Econ. J. 2006, 72, 578–596. [Google Scholar] [CrossRef] [Green Version]

- Huang, H.C.; Lin, S.C. Non-linear finance-growth nexus: A threshold with instrumental variable approach. Econ. Transit. 2009, 17, 439–466. [Google Scholar] [CrossRef]

- Roe, M.J.; Siegel, J.I. Political Instability’s Impact on Financial Development. Public Choice 2008, 87, 279–309. [Google Scholar]

- Kaufmann, D.; Kraay, A.; Mastruzzi, M. The Worldwide Governance Indicators Methodology and Analytical Issues. In Hague Journal on the Rule of Law; World Bank Group: Washington, DC, USA, 2010; Volume 5430, Available online: http://ow.ly/JaiU50qDu1Z (accessed on 1 May 2022).

- Solt, F. The Standardized World Income Inequality Database; Versions 8; Harvard Dataverse: Cambridge, MA, USA, 2019. [Google Scholar] [CrossRef]

- Beck, T.; Demirgüç-Kunt, A.; Levine, R. Finance, inequality and the poor. J. Econ. Growth 2007, 12, 27–49. [Google Scholar] [CrossRef]

- Bulíř, A. Income inequality: Does inflation matter? IMF Staff. Pap. 2001, 48, 139–159. [Google Scholar] [CrossRef]

- Law, S.H.; Azman-Saini, W.N.W. Institutional quality, governance, and financial development. Econ. Gov. 2012, 13, 217–236. [Google Scholar] [CrossRef] [Green Version]

- Demirgüç-Kunt, A.; Klapper, L.; Singer, D.; Ansar, S.; Hess, J. The Global Findex Database 2017: Measuring Financial Inclusion and Opportunities to Expand Access to and Use of Financial Services. World Bank Econ. Rev. 2020, 34 (Suppl. 1), S2–S8. [Google Scholar] [CrossRef]

- Matekenya, W.; Moyo, C.; Jeke, L. Financial inclusion and human development: Evidence from Sub-Saharan Africa. Dev. S. Afr. 2021, 38, 683–700. [Google Scholar] [CrossRef]

- Greenwood, J.; Jovanovic, B. Financial Development, Growth, and the Distribution of Income. J. Political Econ. 1990, 98, 1076–1107. [Google Scholar] [CrossRef] [Green Version]

- Dewi, V.I.; Febrian, E.; Effendi, N.; Anwar, M.; Nidar, S.R. Financial literacy and its variables: The evidence from indonesia. Econ. Sociol. 2020, 13, 133–154. [Google Scholar] [CrossRef]

- Poulton, C.; Dorward, A.; Kydd, J. The revival of smallholder cash crops in Africa: Public and private roles in the provision of finance. J. Int. Dev. 1998, 10, 85–103. [Google Scholar] [CrossRef]

- Giudici, P. Fintech Risk Management: A Research Challenge for Artificial Intelligence in Finance. Front. Artif. Intell. 2018, 1, 1–6. [Google Scholar] [CrossRef] [Green Version]

- Ebong, J.; Babu, G. Demand for credit in high-density markets in kampala: Application of digital lending and implication for product innovation. J. Int. Stud. 2020, 13, 295–313. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Variable | Short Definition | Source |

|---|---|---|

| Gini | Gini disposable | The Standardized World Income Inequality Database (SWIID) |

| Account Ownership | Financial institution account (% age 15+) | Global Findex |

| Fintech | Made digital payments in the past year (% age 15+) | Global Findex |

| Savings | Saved at a financial institution (% age 15+) | Global Findex |

| Borrowing | Borrowed from a financial institution (% age 15+) | Global Findex |

| GDP Growth | GDP per capita growth (annual %) | World Development Indicators |

| Schooling | School enrollment, primary and secondary (gross), gender parity index (GPI) | World Development Indicators |

| Trade | Trade (% of GDP) | World Development Indicators |

| Gov’t Expenditure | General government final consumption expenditure (% of GDP) | World Development Indicators |

| Inflation | Inflation, GDP deflator (annual %) | World Development Indicators |

| Population | Population growth (annual %) | World Development Indicators |

| Institutional Quality | Control of corruption, political stability, government effectiveness | World Governance Indicator (WGI) |

| Variable | Obs | Mean | Std. Dev. | Min | Max | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| [26] | Gini | 91 | 45.178 | 7.221 | 33.3 | 65.9 | |||||

| [27] | Account Owners | 102 | 0.264 | 0.188 | 0.015 | 0.895 | |||||

| [29] | Fintech | 69 | 0.243 | 0.171 | 0.022 | 0.764 | |||||

| [2] | Savings | 102 | 0.118 | 0.084 | 0.006 | 0.355 | |||||

| [19] | Borrowing | 102 | 0.065 | 0.045 | 0.013 | 0.284 | |||||

| [3] | GDP Growth | 101 | 2.505 | 3.689 | −6.809 | 24.976 | |||||

| [43] | Schooling | 61 | 0.937 | 0.106 | 0.630 | 1.071 | |||||

| [23] | Trade | 96 | 69.531 | 26.963 | 1.377 | 149.01 | |||||

| [44] | Gov’t Expen | 94 | 14.584 | 6.324 | 4.325 | 39.690 | |||||

| [22] | Inflation | 101 | 7.755 | 9.699 | −11.876 | 60.987 | |||||

| [38] | Population | 102 | 2.440 | 0.878 | −0.027 | 3.899 | |||||

| [26] | [27] | [29] | [2] | [19] | [3] | [43] | [23] | [44] | [22] | [38] | |

| [26] | 1 | ||||||||||

| [27] | 0.388 * | 1 | |||||||||

| [29] | 0.478 * | 0.705 * | 1 | ||||||||

| [2] | 0.385 * | 0.877 * | 0.621 * | 1 | |||||||

| [19] | −0.045 | 0.551 * | 0.455 * | 0.457 * | 1 | ||||||

| [3] | −0.104 | 0.159 | −0.102 | 0.122 | 0.101 | 1 | |||||

| [43] | 0.023 | 0.368 * | 0.311 * | 0.291* | 0.421 * | 0.161 | 1 | ||||

| [23] | 0.147 | 0.177 | −0.031 | 0.056 | 0.033 | 0.024 | 0.023 | 1 | |||

| [44] | 0.396 * | 0.200 | 0.144 | 0.108 | −0.086 | −0.099 | 0.273 * | 0.461 * | 1 | ||

| [22] | 0.025 | −0.041 | −0.025 | −0.034 | −0.053 | 0.013 | −0.013 | −0.111 | −0.155 | 1 | |

| [38] | −0.085 | −0.531 * | −0.271 * | −0.303 * | −0.489 * | −0.216 * | −0.511 * | −0.397 * | −0.352 * | 0.088 | 1 |

| Dependent Variables | Financial Inclusion | Fintech | Financial Inclusion | Fintech | Financial Inclusion | Fintech | |||

|---|---|---|---|---|---|---|---|---|---|

| I. | II. | III. | IV. | V. | VI. | ||||

| Indep Var | Political Stability | 0.076 * | 0.047 | Control of Corruption | 0.176 *** | 0.120 * | Government Effectiveness | 0.230 *** | 0.138 ** |

| (0.032) | (0.037) | (0.046) | (0.048) | (0.036) | (0.043) | ||||

| Observation | 67 | 44 | 67 | 44 | 67 | 44 | |||

| R-Squared | 0.36 | 0.11 | 0.434 | 0.205 | 0.588 | 0.277 |

| Dependent Variables | Financial Inclusion | Savings | Borrowing | Financial Inclusion | Savings | Borrowing |

|---|---|---|---|---|---|---|

| OLS | 2sls | |||||

| I. | II. | III. | IV. | V. | VI. | |

| Fintech | 0.817 *** | 0.331 *** | 0.0226 | 1.455 *** | 0.655 *** | 0.0487 |

| (0.132) | (0.079) | (0.039) | (0.338) | (0.192) | (0.074) | |

| GDP PC Growth | −0.002 | −0.002 | 0.004 * | - | - | - |

| (0.007) | (0.004) | (0.002) | ||||

| Schooling | −0.138 | 0.0155 | 0.0234 | −0.24 | −0.039 | 0.037 |

| −0.197 | −0.118 | −0.0596 | −0.231 | (0.131) | (0.057) | |

| Trade | −0.005 | −0.003 | −0.001 | −0.001 | −0.001 | −0.0006 |

| (0.008) | (0.005) | (0.002) | (0.001) | (0.005) | (0.002) | |

| Government Expen | −0.004 | −0.009 | −0.001 | 0.007 | −0.005 | −0.001 * |

| (0.003) | (0.002) | (0.009) | (0.003) | (0.002) | (0.008) | |

| Inflation | −0.001 | −0.003 | −0.005 | 0.005 | 0.0005 | −0.007 |

| (0.002) | (0.001) | (0.005) | (0.002) | (0.001) | (0.005) | |

| Population Growth | −0.111 *** | −0.0231 | −0.0411 *** | −0.067 | −0.008 | −0.039 *** |

| (0.027) | (0.016) | (0.008) | (0.037) | (0.021) | (0.008) | |

| Constant | 0.539 * | 0.122 | 0.156 * | 0.36 | 0.0312 | 0.149 * |

| (0.254) | (0.152) | (0.076) | (0.308) | (0.174) | (0.076) | |

| N | 44 | 44 | 44 | 44 | 44 | 44 |

| adj. R-sq | 0.703 | 0.389 | 0.584 | 0.521 | 0.122 | 0.544 |

| Sargan Statistics | - | - | - | 0.6853 | 0.566 | 0.0621 |

| Dependent Variable: log[Gini Disposable] | ||||||||

|---|---|---|---|---|---|---|---|---|

| OLS | 2sls | |||||||

| I. | II. | III. | IV. | V. | VI. | VII. | VIII. | |

| Financial Inclusion | 0.284 *** | 0.332 *** | −0.043 | 0.336 * | −0.0153 | |||

| (0.078) | (0.095) | (0.189) | (0.142) | (0.294) | ||||

| Fintech | 0.440 *** | 0.578 *** | 0.616 ** | 0.746 ** | 0.755 | |||

| (0.107) | (0.140) | (0.219) | (0.275) | (0.492) | ||||

| GDP PC Growth | −0.001 | −0.021 | −0.021 | |||||

| (0.006) | (0.011) | (0.012) | ||||||

| Schooling | −0.088 | −0.231 | −0.242 | −0.093 | −0.229 | −0.248 | ||

| (0.190) | (0.239) | (0.248) | (0.176) | (0.295) | (0.252) | |||

| Trade | −0.007 | −0.008 | −0.008 | −0.007 | −0.005 | −0.005 | ||

| (0.007) | (0.001) | (0.001) | (0.006) | (0.001) | (0.001) | |||

| Government Expen | 0.006 * | 0.002 | 0.002 | 0.007 ** | 0.005 | 0.005 | ||

| (0.003) | (0.004) | (0.004) | (0.002) | (0.003) | (0.003) | |||

| Inflation | 0.004 | −0.005 | −0.005 | 0.042 | 0.043 | 0.041 | ||

| (0.002) | (0.002) | (0.003) | (0.027) | (0.035) | (0.037) | |||

| Population Growth | 0.045 | 0.020 | 0.015 | 0.004 | 0.001 | 0.001 | ||

| (0.025) | (0.031) | (0.037) | (0.002) | (0.002) | (0.003) | |||

| Constant | 3.633 *** | 3.896 *** | 3.926 *** | 3.628 *** | 3.688 *** | 3.712 *** | ||

| 91 | (0.243) | (0.310) | (0.341) | (0.234) | (0.319) | (0.319) | ||

| N | 0.119 | 58 | 59 | 36 | 36 | 59 | 35 | 36 |

| adj. R-sq | - | 0.219 | 0.148 | 0.311 | 0.287 | 0.164 | 0.191 | 0.19 |

| Sargan Statistics | - | - | - | - | 0.8099 | 0.0961 | 0.0637 | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ashenafi, B.B.; Dong, Y. Financial Inclusion, Fintech, and Income Inequality in Africa. FinTech 2022, 1, 376-387. https://doi.org/10.3390/fintech1040028

Ashenafi BB, Dong Y. Financial Inclusion, Fintech, and Income Inequality in Africa. FinTech. 2022; 1(4):376-387. https://doi.org/10.3390/fintech1040028

Chicago/Turabian StyleAshenafi, Biruk Birhanu, and Yan Dong. 2022. "Financial Inclusion, Fintech, and Income Inequality in Africa" FinTech 1, no. 4: 376-387. https://doi.org/10.3390/fintech1040028