Choice between IEO and ICO: Speed vs. Liquidity vs. Risk

Adam Smith Business School, College of Social Science, University of Glasgow, Glasgow G12 8QQ, UK

FinTech 2022, 1(3), 276-293; https://doi.org/10.3390/fintech1030021

Submission received: 2 August 2022

/

Revised: 31 August 2022

/

Accepted: 5 September 2022

/

Published: 9 September 2022

(This article belongs to the Special Issue Recent Development in Fintech)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:This paper analyzes a financing problem for an innovative firm that is considering launching a web-based platform. The model developed in the paper is the first one that analyzes an entrepreneur’s choice between initial exchange offering (IEO) and initial coin offering (ICO). Compared to ICO, under IEO the firm is subject to screening by an exchange that reduces the risk of investment in tokens; also the firm receives access to a larger set of potential investors; finally tokens become listed on an exchange faster. The paper argues that IEO is a better option for the firm if: (1) the investment size is relatively large; (2) the extent of moral hazard problems faced by the firm is relatively large; (3) the degree of investors’ impatience is relatively small. Furthermore, a non-linear relationship between firm quality and its financing choice is found. Most of these predictions are new and have not been tested so far.

Keywords:

risk in fintech; entrepreneurial finance; initial coin offering; initial exchange offering; moral hazard; utility tokens; listingJEL Classification:

D82; G32; L11; L26; M131. Introduction

Financing strategy is a crucial factor of success for innovative businesses (Wilson (2015) [1]). It is not surprising that these firms use a variety of different strategies to fund their projects including private equity, business incubators, venture capital finance, angel finance, seed accelerators, crowdfunding and most recently initial coin offerings (ICOs) and initial exchange offerings (IEOs). Usually under ICO, a firm sells utility tokens which give their buyers (investors) the right to use the company’s future products or services. (It is very similar to reward-based crowdfunding (see e.g., Belleflamme, Lambert and Schwienbacher (2014) [2] or Baber and Fanea-Ivanovici (2021) [3]) where the participants in entrepreneurial financing (funders) usually count on some services/products/other benefits offered by the firm. Unlike crowdfunding, token holders can also usually sell them on a secondary market.) Under IEO, a company sells tokens using the service of organized exchange for cryptocurrencies such as Binance, LBANK and Coinbene. (Myalo (2019) [4]). The exchange is directly involved in the selection of projects, organization and sale of tokens and becomes the key marketing partner of the project. IEOs had strong momentum in 2019 with largest Bitfinex IEO raising $US1 bln. (ICO and IEO report (2020) [5]).

IEO is designed to minimize risks, liquidity problems and a delay in listing tokens at the end of the token sale. A cryptocurrency exchange distributes digital assets among interested investors who are users of the trading platform. Compared to ICO, in the case of IEO: (1) the fraud risk for investors is lower. The project is launched at the exchange after serious verification. The exchange rejects a suspicious/low quality project to maintain its reputation; (2) listing of new tokens is faster; (3) the investment process is technically more simple for investors; (4) the marketing costs for the project team are reduced because the organizers can reach a large number of exchange users; (5) IEO increases the effectiveness of token promotion on the market. At the same time, all these advantages have some drawbacks. The main one is the price for the IEO (see Beedham (2019) [6] or Myalo (2019) [4] for more details. Furthermore, see among others Lipusch, Dellermann, Ebel, Ghazawneh and Leimeister (2019) [7] or Baber (2019) [8] for an analysis of fintech platforms functions).

ICO and IEO research is quickly growing. Most papers are focused on ICOs. Theoretical papers on ICOs include, among others, Catalini and Gans (2018) [9], Li and Mann (2018) [10], Bakos and Halaburda (2018) [11], Malinova and Park (2018) [12], Garratt and van Oordt (2019) [13], Chod and Lyandres (2021) [14], Cong, Li and Wang (2021) [15], Lee and Parlour (2021) [16], Miglo (2021) [17] and Gan, Tsoukalas and Netessine (2021) [18]. For empirical research on ICO see, for example, Adhami, Giudici and Martinazzi (2018) [19], Amsden and Schweizer (2018) [20], Ante, Sandner and Fiedler (2018) [21], Kher, Terjesen, and Liu (2020) [22], Momtaz (2020) [23], Masiak, Block, Masiak, Neuenkirch, and Pielen (2020) [24], Boreiko and Risteski (2020) [25] and Huang, Meoli, and Vismara (2020)) [26]. Research on IEOs is in its early stages and as we are writing this article it includes several empirical and review papers (e.g., Myalo (2019) [4], Anson (2021) [27], Romero-Castro, Pérez-Pico and Ulrich (2022) [28] and Tran Bui (2022) [29], but no theoretical paper to the best of our knowledge as yet exists. Respectively no paper is focused on the choice between ICO and IEO although this issue has been widely discussed among practitioners. (See, for example, Mathew (2019) [30], Chavez-Dreyfuss (2019) [31], Prosvirkin (2020) [32].

In this article a game-theoretic/contract theory approach (which is common in theoretical literature on optimal financing including token issues (see e.g., Harris and Raviv (1991) [33], Miglo (2022) [34], Chod and Lyandres (2021) [14] etc.) is used to build a model where an entrepreneur with an innovative idea considers launching a web-based platform. In order to finance the development of the platform, the entrepreneur can use ICO or IEO. As was mentioned previously (see also Lee and Parlour (2022)) [16], under token issues (in contrast to reward-based crowdfunding, for example) investors may have different objectives including investments in tokens as financial assets. So in our model, there are two types of investors. Type 1 are interested in using tokens to purchase firm products in the future. Type 2 are interested in reselling tokens and creating capital gain. The number of type 1 investors is crucial because it highlights the market demand for firm products. We first consider the case of a perfect market, i.e., the market without moral hazard and where no difference exists between ICO and IEO regarding promoting effects of early listing. In this case, the choice of financing method is irrelevant because both methods lead to the same result for the firm. The reason is that in either case the number of type 1 investors and respectively the level of demand of firm products/services is crucial (no role exists for a speculation in a perfect market) unless other factors/market imperfections are considered. We then consider our main case when, under IEO, there is promotional effect of listing (Myalo (2019) [14], Romero-Castro et al. (2022) [28]). Moreover, under ICO the entrepreneur is subject to moral hazard problems, i.e., he can be involved in diverting funds/investing in an inefficient project/“stealing” funds from investors (Chod and Lyandres (2021) [14], Gan et al. (2021) [18]). This aspect of token issuing firms has been mentioned/analyzed in the literature but was not analyzed with regard to IEO or/and jointly with ICO. Our analysis shows that IEO will be preferred if the company size is relatively large, the number of type 1 investors is relatively small and if exchange fees for IEO are relatively low.

Most of the model predictions have not been tested so far. Interestingly though, one of our main predictions namely that likelihood of selecting IEO is positively related to project size seems to be consistent with recent data as we discuss later (see e.g., Slyusarev (2020) [35], tokens-economy.com, ICO and IEO report (2019) [5]. The model also predicts that companies for which moral hazard problems is an issue, should prefer IEO. Binance CEO Changpeng Zhao mentioned that “...The goal here (i.e., IEO-author) is to help good projects. There are no specific targets on how quickly we have to grow or expand. We will just help good projects raise funds as we find them...” (Lee (2019) [36].

The rest of the paper is organized as follows. Section 2 provides a literature review. Section 3 describes the basic model and some preliminary results. Section 4 provides an analysis for the model with moral hazard and other factors. Section 5 analyzes the consistency of the model’s predictions with observed empirical evidence. Section 6 discusses the model’s robustness and its potential extensions and Section 7 is a conclusion to the study.

2. Literature Review

This section provides a review of growing literature on ICO and IEO with regard to their aspects related to the present paper. For general reviews see, for example, Cumming, Johan and Pant (2019) [37], Myalo (2019) [4], Bellavitis, Fisch and Wiklund (2021) [38], Romero-Castro, Pérez-Pico and Ulrich (2021) [28] and Miglo (2022) [35].

Uncertainty and risk. As was previously mentioned an ICO is an event of great uncertainty (see also Financial Stability Board (2018) https://www.fsb.org/wp-content/uploads/P101018.pdf, accessed on 1 August 2022). Generally speaking, in the existing literature two main aspects of this uncertainty have been analyzed: one is related to asymmetric information between issuers and potential investors about the content/details/quality of projects and the second one is the post-issue uncertainty/risk related to entrepreneurial actions that is hard to directly control by investors. The issue of asymmetric information has been analyzed mostly through two main channels: one is the so-called direct signalling which is related to the direct information disclosure by the issuers to potential investors and the second one is related to the so-called indirect signalling, i.e., the effort of issuers to signal the quality of their projects indirectly via selecting different actions. Direct signalling related to the quality of information disclosed by the issuers before the issue has not been a particularly popular line of research regarding traditional ways of raising funds such as stocks and bonds mostly because it is a largely regulated area. However unlike traditional ways of raising funds for ICOs there is no mandatory regulated information disclosure requirements for the issuers. Some papers argue that the ICO issuers put effort in preparing quality information about the issue so the ICO team usually publishes a so-called white paper (Yen, Wang and Chen (2021) [39]) with information about the ICO (in some cases, yellow or beige paper can also be issued to give further technical specifications about the project (Yu (2018))) [40]. Some papers find that the quality of information usually improves the chances of success (see e.g., An, Hou and Liu (2018) [41] or Fisch (2019) [42]). Momtaz (2021) [43] argues that a moral hazard problem exists in signaling, and that artificial linguistic intelligence indicates that token issuers systematically exaggerate information disclosed in a white paper. With regard to indirect signalling notes (Chod and Lyandres (2021) [14]) that compare ICO with traditional equity-based financing, there is a focus on several factors including information asymmetry between entrepreneurs and investors. They argue that ICO can be used by high-quality entrepreneurs by retaining more tokens in their own possession (signaling by risk-bearing in the spirit of Leland and Pyle (1977)) [44]. Czaja and Röder (2022) [45] find that media presence and entrepreneurs’ self-efficacy are effective signals in the ICO market that can increase funding success. Moreover, Miglo (2020) [46] analyzes the firm choice between ICO and equity financing based on information problems. The model predicts for example that the message complexity can be beneficial for firms conducting ICOs.

IEOs offer some improvements to ICOs related to risk and uncertainty. Also some authors suggest that during COVID crisis the risk of ICO increased by comparing for example 2021 and 2020 data (see e.g. Leonard (2022) [47]. and also that the number of scams among ICO can be as high as 80%. They also often use the term “Pump and dump” describing some ICOs, which means “pumping” demand for an asset and respectively increasing its price initially, and then a sharp “dumping” of the asset. See e.g., Wu (2020) [48]. As was previously mentioned a cryptocurrency exchange is directly involved in the selection of projects and the launching of the offering, distributing the tokens among verified investors on their trading platform (Myalo (2019) [4]). Some papers argue that the crypto exchange conducts preliminary screening and can reject fraudulent or low-quality projects (Venegas (2017) [49], Doe-Bruce (2019) [50], Myalo (2019) [4], Cumming, Johan and Pant (2019) [38], Anson (2021) [27], Chamorro Domínguez (2021) [51]).

The second aspect of risk is related to entrepreneurial moral hazard after the issue. Several papers analyze this issue in the form of potential firm fund diversion by entrepreneurs with regard to ICOs. See, for example, Garratt van Oordt (2019) [13], Chod et al. (2021) [52], Canidio (2018) [53], Gan et al. (2021) [18] and Gryglewicz, Mayer and Morellec (2021) [54]. Moral hazard in the form of potential diversion of funds by entrepreneur is also a part of the model in this paper. Compared to papers mentioned above, in this paper IEO is also included in the model and the model compares and combines the cost and risk related to moral hazard problem with other aspects related to IEO.

Liquidity and different types of investors. As was previously mentioned, an important feature of ICO/IEO is the liquidity of investments. This also highlights an important difference between ICO/IEO and for example crowdfunding. Some papers argue that the absence of liquidity is one of the major disadvantages of crowdfunding (see e.g., Murray (2015) [55], Schwartz (2012) [56], Signori and Vismara (2016) [57], Lee and Parlour (2022) [16]. Some papers analyze different aspects of market liquidity under ICO and IEO. For example, Kaal and Dell’Erba (2017) [58] and Takahashi (2020) [59] noticed that crypto exchanges allow continuous trading with significant liquidity regardless of market hours and time zone. Further smaller investors are less discriminated against in the process under IEO than under ICO (Boreiko, Ferrarini and Giudici (2019)) [60]. Some papers argue that although under crowdfunding the investors/funders objective is to obtain some rewards/benefits/services from the firm, under ICO different objectives may take place including investments in tokens just as financial assets/speculations etc. It can explain why different types of investors exist under ICO (Fahlenbrach and Frattaroli (2019) [61], Liu (2019) [62], Fisch and Momtaz (2020) [63], Kaal and Dell’Erba (2017) [57], Howell et al. (2019) [64], Romero-Castro et al (2022) [28] and Tran Bui (2022) [29]). Further some research finds that the presence of different types of investors e.g., speculators can play a positive role. For example, Tao, Peng and Ma (2022) [65] analyze the speculator’s risk attitude on the firm’s profitability. They find that the firm will be better off when the speculator is more risk-seeking.

Some research investigates which motive dominates investments in ICOs: buying future firm products or purely financial reward. Some authors find evidence which is consistent with financial reward dominating investments (see e.g., Fahlenbrach and Frattaroli (2019) [60] or Benedetti and Kostovetsky (2021) [66]). On the other hand Ante (2022) [67] investigates liquidity shocks in markets for tokens on the Ethereum blockchain. The paper finds some elements or informed trading and arbitrage. These findings indicate that market capitalization may be an insufficient metric for assessing the liquidity and valuation of (inefficient) crypto assets. Fisch et al. (2018) [68] conducted a survey among investors and suggested that the potential gain of value is not their only incentive (see also Liu (2019)) [61].

Lee and Parlour (2021) [16] compare crowdfunding and ICO. Unlike traditional financial intermediaries, crowdfunding investors/funders/consumers also receive a consumption benefit. The authors then analyze the implications of introducing a resale market for investors, as in the case of ICO, and argue that the speculation necessarily accompanies such markets. As in Lee and Parlour (2021) [16], the model in the present paper uses the liquidity aspect of tokens and different investor types. Because under IEO tokens become circulated quicker (see next subsection) it creates an additional liquidity boost for IEO as compared to ICO. Therefore, unlike Lee and Parlour (2021) [16], IEO is also included in the model and the paper combines the analysis with moral hazard issues mentioned previously.

Speed. During IEOs, exchanges are not just directly involved in the verification and organization of projects, but they are also the key marketing partner of token offerings. The crypto exchange offers help with marketing and promotion and backs the offering with its reputation, increasing fundraising success in exchange for listing fees and a percentage of the tokens sold (Anson (2021) [27], Chamorro Domínguez (2021)) [50]. By conducting the sales through an exchange, all users of the trading platform can participate in the distribution of tokens. Ofir and Sadeh (2020) [69] and Allen, Fatas and Weder di Mauro (2022) [70] suggest that IEOs tokens are almost directly available for trading on the exchange platform. IEOs process underlines a joint effort of the project team and exchange in its promotion, since they both benefit from the offering’s success and immediate exposure to users of the exchange. The duration is often planned for a few days, although some successful projects were concluded within in few minutes depending on the target cap and hype among investors. In contrast, after the launch of ICO, the issued tokens would remain illiquid and unlisted until the organization contact and have their request processed by exchange platforms (Liu (2022) [71]). Some research compares the effectiveness of reaching investors under IEO and IPO. On conventional stock exchanges for secondary markets, a variety of different costs exist, including admission fees, broker commissions or annual exchange fees (Domowitz, Glen and Madhavan (2001) [72]). Furthermore, the complying procedures are often lengthy (Chen (2018) [73]). IEOs can help start-ups with raising funds quickly and more efficiently.

These aspects of ICO and IEO are also related to a similar line of research related to crowdfunding. For example, Schwienbacher (2018) [74] analyzes the marketing effort of entrepreneurs under crowdfunding. The paper argues that under crowdfunding there is a risk that the idea is quickly replicated by others. The presence of professional investors reduces the entrepreneurs’ incentives in their crowdfunding campaign, which leads to more, but on average smaller, crowdfunding campaigns. Unlike crowdfunding, IEOs are subject to a scrutiny by an cryptoexchange so the risk of having a legal dispute between different entrepreneurs is minimized. The size of IEOs are typically larger than that of crowdfunding. The present paper also has aspects of entrepreneurial moral hazard and also marketing aspects of capital-raising fintech platform activity, but it also focuses on ICO and IEO. It is assumed that, because IEO has a marketing advantage compared to ICO (listing effect), that is also mentioned in Myalo (2019) [4].

As this section demonstrates there are several aspects of ICO and IEO that highlights their similarities and differences. Existing empirical literature usually considers some aspects separately but in this paper we build a theoretical model that considers most factors simultaneously.

3. The Model Description and Some Preliminaries

An innovative firm has monopoly power over its idea of creating a website platform for selling a product/service. The initial fixed cost of the project is I (in Section 5 we discuss the model’s assumptions). The variable cost of production of one unit of the product is c. To finance the development of the product the firm can use ICO (initial coin offering) or IEO (initial exchange offering). In both cases, the firm sells utility tokens. Compared to ICO, under IEO: (1) the firm is screened by an exchange that reduces the risk of low-quality campaigns including entrepreneurial fraud (as was previously mentioned, a lot of campaigns fail or turn out to be low quality or even fraud in some cases. See, for example, Cumming, Johan and Pant (2019) [38], OECD (2020) [75]. For traditional exchanges listing requirements and their implications for traditional securities see e.g., Macey and O’Hara (2002) [76]). (2) the firm acquires access to a larger set of potential investors; (3) tokens become listed on an exchange faster (see Myalo (2019) [4]). More specifically, these differences ae modelled as follows. There are three periods in the model. In period 0, tokens are sold for the price . In period 1 under IEO tokens become listed and can be sold on an exchange. In period 2 the firm produces products and tokens can be used to buy products and services offered by the firm and they can be sold on an exchange under both IEO and ICO. There are two types of investors. Type 1 are only interested in products offered by the firm (each investor is interested in consuming one unit of the product). The total number of type 1 investors is . Type 2 are interested in selling tokens and receiving capital gains. The total number of type 2 investors is unlimited. After the initial issue of tokens in period 0, token market participants receive information about token market future prospects. After that, a fraction of randomly chosen type 2 investors who purchased tokens during IEO will sell them in period 1. As was previously discussed, tokens have a two-sided nature: on one hand it is a financial asset but on the other hand it can be used for purchasing goods/services. We assume that in each period some fraction of token holders decides to spend tokens on consumption, i.e., they become short-term investors/consumers (technically one can say that some fraction of token holders is subject to a consumption shock in each period) in this case (for related ideas see e.g., Merello, De la Poza and Jódar (2020) [77] ). The remaining type 2 investors will sell their tokens in period 2. is related to token market uncertainty. In addition to factors affecting the markets for traditional financial assets, token market is also affected by factors affecting blockchain technology development, cryptocurrencies (since payments can be made in cryptotokens) etc. High is associated with token market uncertainty and investors impatience, while low means that token market anticipations are rather positive and investors are patient. The consumption value of tokens is v. All investors are risk-neutral and risk-free interest rate is 0, so investors purchase tokens if the expected payoff covers investment cost. Moreover, the entrepreneur is subject to moral hazard. Under ICO, after funds are collected, the entrepreneur can be involved in some inefficient project instead of continuing with production. More specifically we assume that in the case of success this “inefficient” project brings an amount of profit equal to the amount of funds collected during ICO and in the case of failure it gives the entrepreneur zero. The probability of success is . An interpretation is that funds are stolen and is the probability of being caught. Finally, under IEO, the firm pays a fee F to the exchange. Moreover, information about all issues of tokens is imperfect. More specifically we assume that since under IEO more investors are potentially reached than under ICO and also because under IEO the tokens are listed on an exchange faster, IEO has a promotional effect i.e., under IEO some investors obtain information about new firm and its tokens even though they did not have it otherwise. In the model, an additional number X of type 1 investors are created in case of IEO in period 2. Finally if the number of tokens is smaller than the total number of potential investors when the firm sells tokens in period 0 we assume that type 1 investors will buy first in case of ICO and type 2 investors will buy first in case of IEO. (This assumption is not crucial for our paper result qualitatively and is consistent with the spirit of different types of financing. ICO is more closed compared to IEO so ICO is less attractive for type 2 investors compared to type 1 investors while IEO is more attractive for them. More discussion is provided in Section 5).

Let n be the total number of tokens issued and be the number of type j investors, , , . The value of issued tokens should cover the investment cost and production cost:

First consider perfect information scenarios without moral hazard problems and other market imperfections e.g., exchange fees, i.e., , and .

3.1. ICO

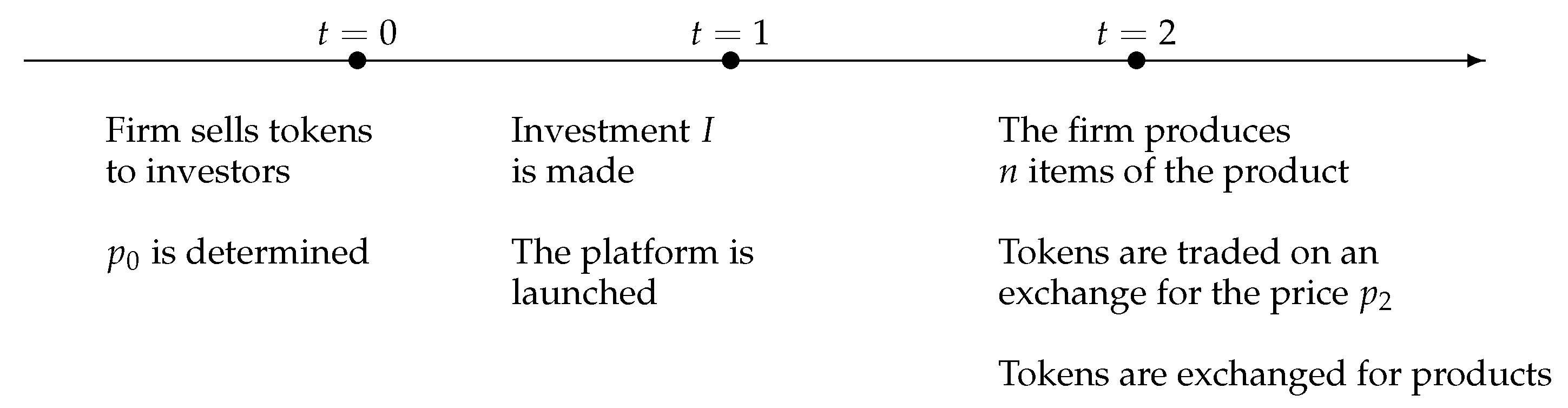

The timing of events is present in Figure 1.

First note that with probability the return for type 2 investors participating in an ICO is zero because they will not be able to sell tokens in period 1 (tokens will not be listed in case of ICO until period 2).

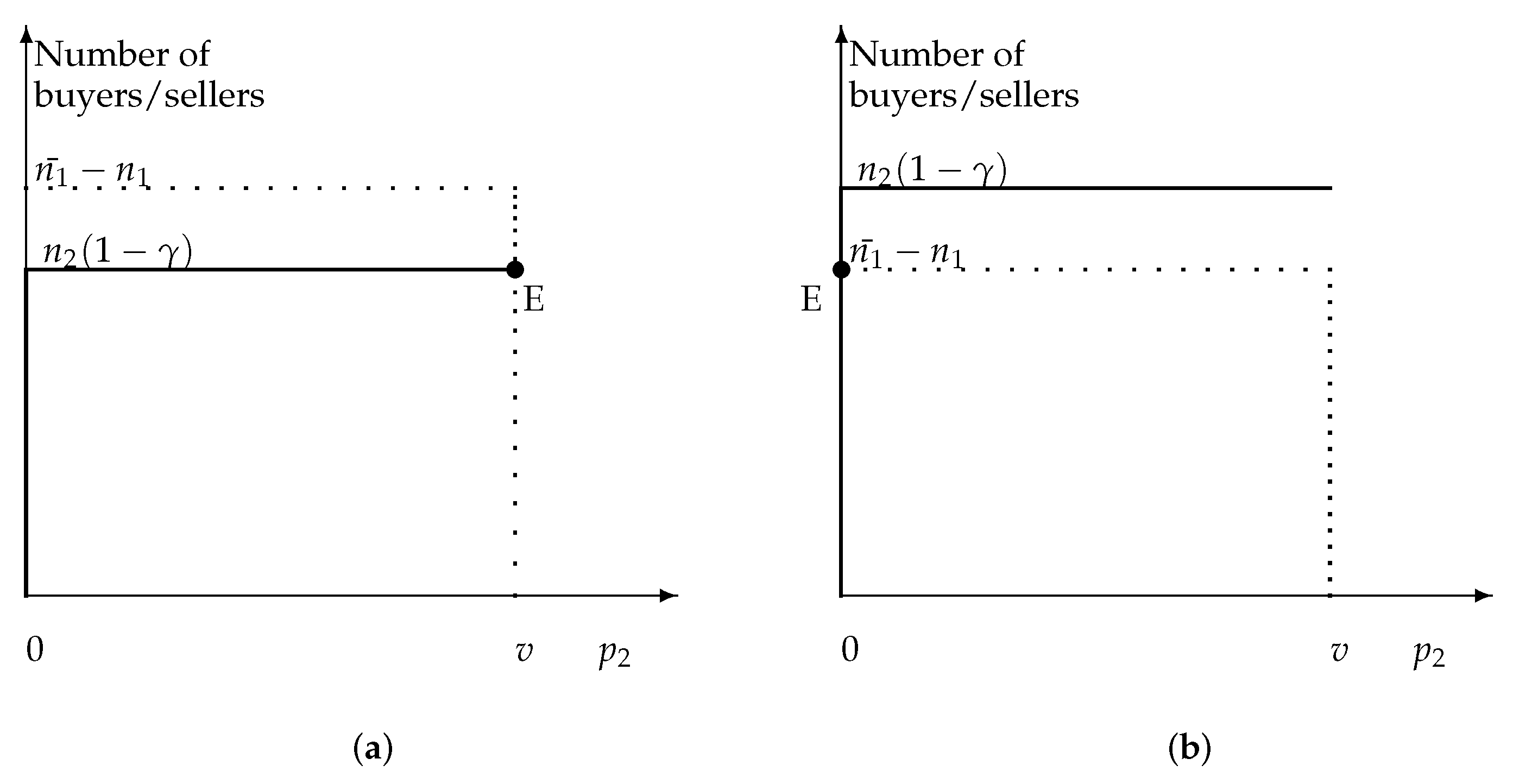

Equilibrium in token market in period 2 depends on the total number of token buyers and sellers. If the number of token buyers is equal or greater than the number of token sellers, equilibrium price is v (see Figure 2a).

Otherwise the price is 0 (see Figure 2b). Indeed in the latter case if the price is greater than zero, it cannot be an equilibrium because any of the sellers who did not sell his tokens could offer a slightly lower price.

In our case the number of token sellers in period 2 is and the number of buyers equals . So if

then . Otherwise . In fact, (2) always holds. Indeed if it does not and , type 2 investors will not be interested in purchasing tokens and implying that (2) holds.

Furthermore, one should have . The firm selects and n to maximize its profit: . The solution is as follows. If , optimal . Otherwise two strategies are possible. First is . In this case type 2 investors are not interested to buy tokens during ICO because their expected payoff () is less than . It implies and

Second is . Even though type 2 investors are interested in purchasing tokens during ICO, the total number of issued tokens can not exceed because type 2 investors will still resell their tokens to type 1 investors and since one consumer is only interested in consuming one good, the total number of produced goods can not be larger than . So and

First strategy is optimal.

3.2. IEO

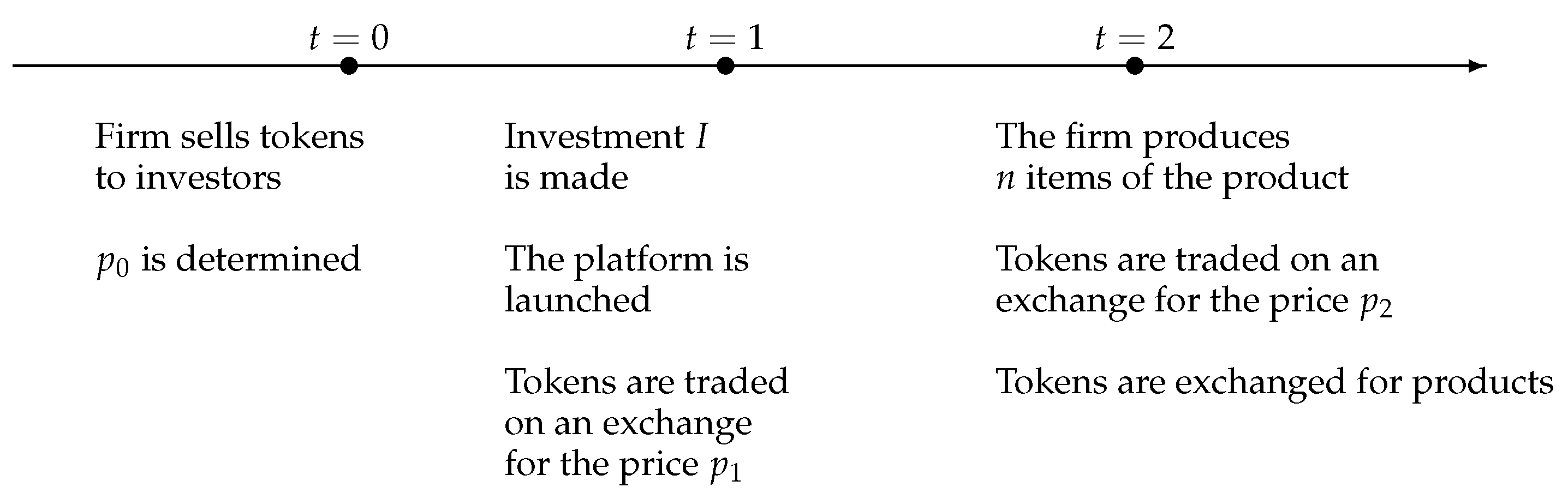

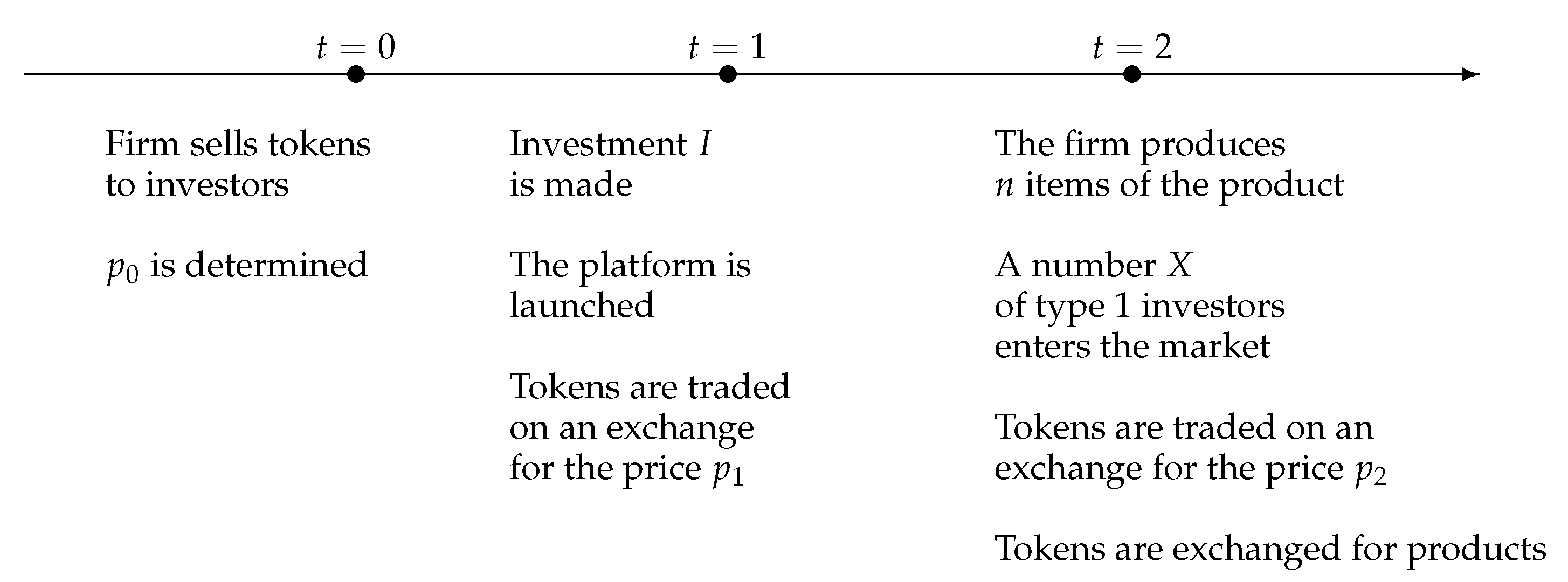

The timing of events is present in Figure 3.

Consider token market equilibrium in period 1. The number of token sellers in period 1 is and the number of buyers equals . So if

then . Otherwise . Suppose (5) holds. In this case ( is the number of type 1 investors who purchased tokens in period 1).

Consider token market equilibrium in period 2. The number of token sellers in period 2 is and the number of buyers equals . So if or

then . Otherwise . Two cases are possible.

1. Suppose that condition (6) holds. The firm maximizes its profit . The solution is as follows. If, optimal . The project is worthless. Otherwise the solution is , and

2. Suppose that (6) does not hold. Then

and . Furthermore, . Otherwise no investor is interested in purchasing tokens. The solution is as follows. If , optimal and . The project is worthless. Otherwise two strategies are possible. First is . In this case type 2 investors are not interested to buy tokens during ICO because their expected payoff () is less than ; that contradicts (8). However, this contradicts our assumption that (6) does not hold. Another strategy is (any price below v but higher than makes no sense for the firm because it reduces firm profit without attracting new token buyers). . Even though type 2 investors are interested in purchasing tokens during ICO, the total number of issued tokens can not exceed because type 2 investors will still resell their tokens to type 1 investors and since one consumer is only interested in consuming one good, the total number of produced goods can not be larger than . So and also . First strategy is optimal.

Now suppose (5) does not hold. In this case .

Consider token market equilibrium in period 2. The number of token sellers in period 2 is and the number of buyers equals 0. So . No type 2 investors will buy tokens initially since their payoff is 0. However, this contradicts that (5) does not hold.

Lemma 1.

Without moral hazard and absence of promoting effect of listing, there are two cases: (1) if , the project is worthless for the entrepreneur; (2) otherwise the firm is indifferent between ICO and IEO.

This result is not surprising given that in the absence of any financial market imperfections every type of financing should have the same result (similar to the Modigliani–Miller proposition (1958)).

4. Moral Hazard and Promoting Effect of Early Listing

In this section the role of moral hazard, promotional effect of IEO and other factors on the firm’s choice of financing strategy is analyzed. Different strategies attract different types of investors. Furthermore, the firm choice affects the incentives of the entrepreneur.

4.1. ICO

The timing of events for ICO is presented in Figure 4.

The difference to the previous case is that now we should consider the entrepreneur’s decision whether to “steal” money from the firm.

If and the entrepreneur continues, his payoff equals according to (3). If he withdraws funds then it is . If

then he continues. Note that RHS (right-hand side) of (9) is less than 1 because of (1).

Funders rationally anticipate an opportunity for stealing and will not provide funds if condition (9) does not hold.

Note that lowering ICO token price does not increase firm credibility in the eyes of investors. Indeed suppose . If the entrepreneur continues, his payoff equals according to (4). If he withdraws funds then it is . If

then he continues. RHS of (10) is greater than RHS of (9) so if (10) does not hold (i.e., the entrepreneur steals money when the price equals v), (10) does hold too and the entrepreneur steals money even if the price is lower. This leads to the following proposition.

Proposition 1.

If , and . If , ICO is not feasible.

Proof.

Follows from above. □

4.2. IEO

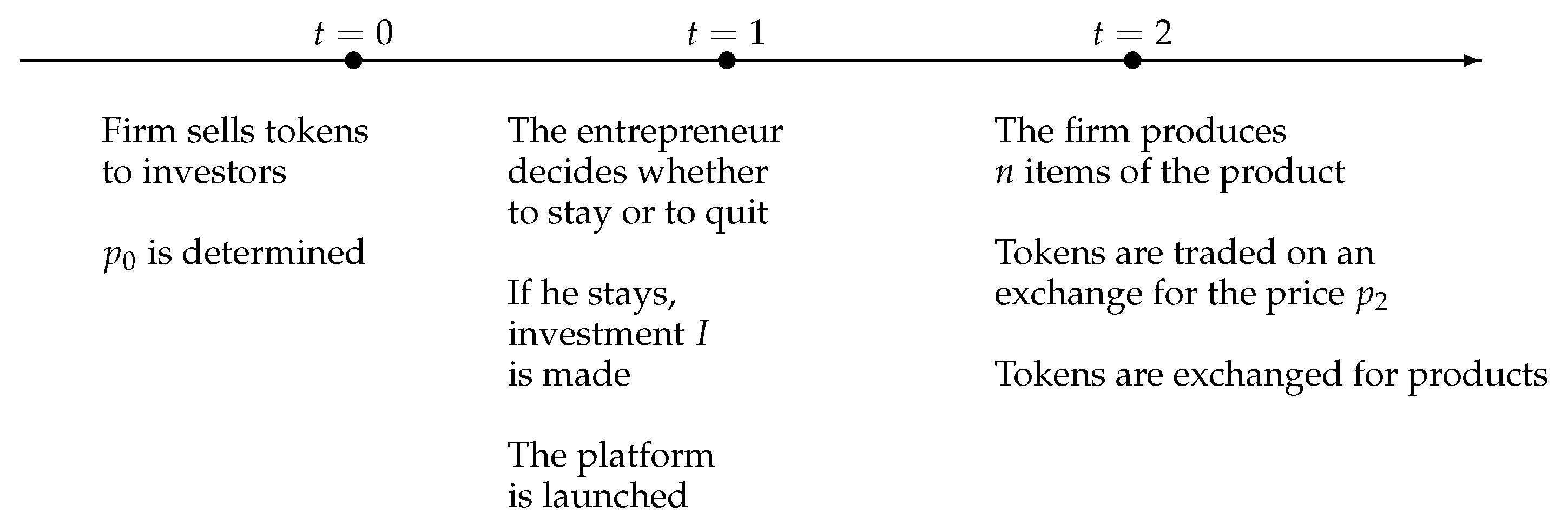

The timing of events for IEO is presented in Figure 5.

The cost of the project does now include an exchange fee F that implies . The firm maximizes its profit:

The number of sellers in period 1 is and the number of buyers equals . Two cases are possible.

If

then . The number of sellers in period 2 is and the number of buyers equals , where is the number of type 1 investors who purchased tokens in period 1 from type 2 investors. Since (12) holds, . So if

or then . Otherwise .

If

then . The number of sellers in period 2 is and the number of buyers equals , where is the number of type 1 investors who purchased tokens in period 1 from type 2 investors. Since (12) does not hold, . So the number of buyers in period 2 is X. If

then . Otherwise . In the latter case type 2 investors are not interested in purchasing tokens during IEO, i.e., leading to a contradiction with (14). So if (14) holds, (15) should hold too.

Suppose (12) holds. Two situations are possible.

(1). (13) holds. When both constraints hold, as was noted previously, and, as follows from (11), the solution for the firm is to find maximal n such that both constraints (12) and (13) hold. Type 2 investors are interested in buying tokens during IEO because both constraints hold, , the expected payoff to type 2 investor equals v and it covers the investment cost. It implies that no type 1 investor will be able to buy a token in period 0: . Condition (12) becomes

and condition (13) becomes

Two cases are possible.

(2). (13) does not hold. Two strategies are possible for the firm. First . In this case type 2 investors will not buy tokens. This leads to a contradiction that (13) does not hold. Another strategy is . If , no n exists that simultaneously satisfies (16) and does not satisfy (17). If the maximal n that satisfies (16) and does not satisfy (17) is .

Now suppose (12) does not hold. If (13) does not hold, then . In this case no type 2 investor would buy tokens leading to a contradiction that (12) does not hold. So (13) holds. Two strategies are possible for the firm. First . In this case type 2 investors will not buy tokens. This leads to a contradiction that (12) does not hold. Another strategy is . Since type 2 investors are interested in buying tokens, type 1 investors will be able to purchase tokens during IEO: . Condition (12) becomes and condition (15) becomes . Two cases are possible. If , the solution is .

If , no solution exists.

Proposition 2.

(1) If , and . (2) If then if

and . Otherwise and .

Proof.

Consider . Two strategies are possible. if then and . If then and which is smaller than previous result.

Consider . Two strategies are possible. If then and . if then and . Comparing these two results leads to the following. If then the former is greater and vice versa. □

The interpretation of these results is as follows. If X is low, the firm will be able to sell tokens equal to the number of all type 1 investors (existing ones () and expected ones in the future (X)). When X increases, a firm is not always able to sell an increasing number of tokens in period 0 in anticipation of future high demand from type 1 investors because of the risk that too many tokens will be offered for sale in period 1 or 2, leading to a low market price for tokens. In order to keep the incentive of type 2 investors to participate in token issue, the firm would then need to consider opportunities for lowering the initial price of tokens. So different scenarios are possible. For example, if the number of existing type 1 investors is relatively high (condition (18)) compared to expected future demand, the firm would prefer to keep the issue price high while otherwise it may consider lowering the issue price.

Now we compare ICO and IEO.

Proposition 3.

(1) If , IEO is preferred. (ICO is not feasible); (2) If then: if , IEO is preferred if . If and , IEO is preferred. If and , IEO is preferred if .

Proof.

Two cases are possible.

- (1)

- IfIEO is preferred (ICO is not feasible according to Proposition 1).

- (2)

- . if then if IEO: and . If ICO then . IEO is preferred if

If and , then if IEO: and . If ICO then . IEO is preferred.

If and , then if IEO: and . If ICO then . IEO is preferred if

□

5. Implications

This paper has several implications for an entrepreneurial firm’s choice of financing strategy.

Proposition 3 implies that IEO is preferred to ICO if the investment cost of the project increases. Indeed, (19) is more likely to hold when I increases and vice versa. If (19) holds, then ICO is not feasible and IEO is the dominant choice for entrepreneurs. As was previously mentioned, this prediction has not been tested directly but is consistent with some data. For example as follows from Slyusarev (2020) the average size of IEO in 2019 was about nine million, and also as follows from tokens-economy.com (accessed on 24 August 2022), the average size of ICOs (all time) is about 6.91 million.

Proposition 3 also implies that the likelihood of IEO is negatively related to . Indeed the derivative of LHS of (21) equals . It means that IEO is better than ICO when the token market participants do not anticipate long-term problems and/or short-term speculation (high volume of token sales in the short run). In the case of IEO it is better to put this kind of pressure on later periods when the promotional effect of IEO will have an impact on a number of potential token buyers and the market pressure coming from token sale by type 2 investors is mitigated. The interpretation of this result is that when the likelihood of liquidity shocks increases then ICO is preferred to IEO. Intutively, under liquidity shocks the negative effect of speculation under IEO increases.

Moreover, the model predicts that under IEO one can have a situation when the price of tokens increases by more than under ICO but not an opposite scenario. Indeed if (21) holds then under IEO and which means that under IEO the extent of underpricing (low token issue price) is larger than under ICO but on the other hand a long-term return on tokens is higher. IEO underpricing is consistent with findings in Tran Bui (2022) although no research has specifically compared the extent of underpricing in ICOs and IEOs to the best of my knowledge.

Moreover the model predicts that the likelihood of IEO is negatively related to the size of exchange fees (F) and the probability of “inefficient project” () success and positively related to the expected increase in the demand from type 1 of investors due to promotional effect of early listing (X).

Finally the model predicts a non-linear relationship between product quality (v) and firm choice. First, when v is too low condition (9) will not hold, implying that IEO will be selected. When v increases and (9) holds then, based on conditions (20) and (21), ICO can be preferred if v is not too high (“intermediate range”) and vice versa. Therefore, when v is very large, IEO is the preferred choice again.

The model’s managerial implications include recommendations related to the choice between ICO and IEO. It suggests different variables that can be used by managers to make this choice. It also describes some basic ideas on qualitative level and mathematical links between different variables. Furthermore the next section discusses possible empirical strategies of testing the paper results that can help with generating more quantitative results for managerial decision-making.

6. The Model Extensions and Robustness

This section first discusses different model assumptions and the model’s results robustness with regard to these assumptions as well as potential lines of research development related to the present model. At the end a general discussion of the research limitations which is mostly related to the approach used in this article is provided.

Other types of moral hazard. In the model of this paper, the moral hazard takes place because the production process is costly for the entrepreneur and he will fully bear this cost while the expected reward in case of quitting may be higher if is sufficiently low. To some extent this approach is similar to the asset substitution effect in financing literature when entrepreneur switches to a socially inefficient project when he is not going to fully enjoy the benefits of socially efficient project because of payoff structure (Jensen and Meckling (1976)). There are many different ways to analyze moral hazard issues, for example, to explicitly assume that the entrepreneurs can issue security token (see, for example, Adhami, Giudici and Martinazzi (2017) [19], Ante and Fiedler (2019) [78] and Miglo (2021)) [17] in addition to utility tokens and then assume that his effort can be socially inefficient because of agency cost of equity. One can also include the cryptocurrency exchange moral hazard problem when conducting a project expertise etc. At this point, however, we do not see which parts of our model results can be affected qualitatively without significantly complicating the model’s solutions so we leave it for future research.

Mixed financing and more types of financing. Unlike capital structure literature (where a debt/equity mix is a very common strategy, as opposed to pure equity or pure debt financing, for a review of capital structure literature see, among others, Harris and Raviv (1991) [34]. For a traditional analysis of the capital structure of internet companies see, for example, Miglo, Lee and Liang (2014) [79]) simultaneously using ICO and IEO has not shown to be common so we do not consider it in the model. One can also include other types of tokens (such as mentioned previously security tokens) or other types of financing (such as bank loans or venture capital). There exists a large spectrum of opportunities here and future evidence would demonstrate which cases are really important for entrepreneurs and which ones deserve to be investigated further. At this point we can see that the choice between ICO and IEO is an important issue in practice as was mentioned previously.

Two stages. One can assume that the firm issues tokens in two stages. As far as we can see, the results will not change with the introduction of this assumption, however, if one introduces for example two development periods in the model with two different stages of investment in each period the results will change at least quantitatively. It is hard to predict the consequences of such a change so it is difficult to judge if it is a promising avenue for future research.

Different priority rules. In the model we assumed that when the number of tokens is smaller when the number of investors then under ICO type 1 investors will buy first and under IEO type 2 investors will buy first. As we mentioned, this assumption is not important qualitatively for the model results. One can further extend the model by assuming, for example, that under IEO a fraction of tokens is purchased by type 1 investors and respectively by type 1 investors. is related to the overall level of market investors reach by an exchange. Our analysis shows that no result of our analysis changes qualitatively although some formulas would change. For example, condition (21) becomes . If it holds, the firm would prefer IEO and vice versa. All predictions remain the same with an addition of a new prediction about the role of changes in . The derivative of LHS in of this condition equals . If is relatively small, it is positive and higher a improves the attractiveness of IEO and vice versa.

Asymmetric information. This paper focuses on ex-post asymmetric information, i.e., an environment where the outcome of a financing strategy depends on the incentives of the entrepreneur. One can consider a model with ex-ante asymmetric information where the entrepreneur initially has some signals about its platform and would like to signal it to the market via tokens issue. It is an interesting avenue for future analysis but it is beyond the scope of present model.

Future empirical tests of this paper results and predictions should be focused on analyzing the connections between the entrepreneur’s choice (that can be a dependent variable) between ICO and IEO and such variables as I (project size), (market uncertainty), c (production costs), (the extent of moral hazard problems) etc. and should also include variable F describing the cost of token issues etc. Our paper suggests that these variables should be important in the choice between ICO and IEO. Some data are not directly observable especially for innovative start-up companies. can be measured for example by using the concept of corporate governance in fintech firms (see the growing literature in this filed e.g., Hernandez-Solis and Herrador-Alcaide (2017) [80], Kashuba (2021) [81] and Najaf, Chin and Najaf (2021) [82] (see also PwC (2020)) [83]. can be measured using similar ideas to e.g., Ante (2022) [67]. We leave the details of econometric analysis for future research.

General limitations of this article include the focus on the ideas which are mostly related to the game-theoretic/contract theory approach used. Basically it is a common approach in theoretical literature dealing with firm financing decisions (see e.g., Harris and Raviv (1991) [34] or Tirole (2006) [84]). ICO and IEO represent examples of financing strategies for firms that however have a lot of new innovative features compared to traditional financing. Some non-traditional elements (for example liquidity shocks or consumption-based financing) are included in the model however more methods can be used to build future models including behavioral finance or network economics. These are promising areas for future research.

7. Conclusions

ICO and IEO are growing areas of interest among practitioners and theorists. They are especially important for innovative businesses and start-up businesses because for them financing is one of the crucial factor of success. Unlike firms in traditional industries, they do not typically own a large amount of tangible assets in order to apply for bank loans and/or do not have an established reputation in order to conduct an IPO for example. Token issues are supposed to be a great help for these firms and they are also considered as a part of Fintech (see e.g., Thakor (2021) [85]) which represents a new area of development in the finance industry that can significantly change the financial landscape in upcoming years. As mentioned by some research, in the last 3–5 years, ICO and IEO have been playing a significant role in enhancing entrepreneurial potential for innovation and economic growth.

Existing literature has discovered many reasons for why raising funds is difficult for entrepreneurial companies including asymmetries of information, high bankruptcy costs, transactions costs, moral hazard issues and many others. Our paper contributes to the growing literature on ICO and IEO, in particular to the branch that focuses on the role of token issues in mitigating moral hazard problems and its trade-off with the advantages and disadvantages of other factors such as liquidity of tokens and the presence of different types of investors. Theoretical literature on token issues usually considers an ICO. It is not surprising given that historically ICO appeared on the market on a large scale several years before IEOs did. This paper offers a model of a choice between ICO and IEO for an entrepreneurial firm that needs to raise funds for financing its innovative project. Our model is based on some important features of IEO. As compared to ICO, under IEO the firm is subject to screening by a cryptocurrency exchange; also the firm acquires access to a larger set of potential investors; finally tokens become listed on an exchange faster.

We first demonstrate that in a perfect market the choice between ICO and IEO is irrelevant. We then show that when markets are imperfect and a moral hazard problem exists then IEO is a better choice for the entrepreneur since it helps with mitigating moral hazard issues via screening of projects by an exchange. On the contrary, when no moral hazard problem exists but the market uncertainty is high and the risk of liquidity shocks and respectively the negative effect of speculation increase then an ICO can be a better choice. The most interesting case is when all market imperfections are present simultaneously. Our model predicts that in this case, the likelihood os using IEO is positively correlated with the project size. Moreover, it is related to the extent of moral hazard problems and the level of market uncertainty. Most of the predictions have not been directly tested while they are consistent with some recent evidence.

Our paper (as most of other theoretical literature on token issues) is related to the area of optimal financing research that connects firm financing decisions and monetary economics since on one hand tokens can be used for an exchange and also for purchasing future firm products/services (similar to the functions of money); on the other hand token issues also represent firms’ financing strategy. To the best of our knowledge there is no direct analogy for this type of research in traditional capital structure literature note for example Bolton and Huang (2018) [86] and Miglo (2020) [87] that analyze the government choice of financing method using microeconomic/game-theoretic ideas that combines financing problem and monetary problems and argue, for example, that the seigniorage (issuing money by the government) is analogous to firm equity issues. The line of research that combines optimal financing research with monetary economics is a promising line for future research.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Acknowledgments

Many thanks to the editor David Roubaud for the invitation to submit the paper to the special issue on Recent Developments in FinTech, and many thanks to four anonymous referees for their excellent comments and suggestions. I am also grateful to Victor Miglo, Sajda Qureshi, Jane Spurr, Chris Yang, Vladimir Zwass and the seminar participants at de Montfort University, London South Bank University, Coventry University London, Edinburgh Napier University and British Accounting and Finance Association 2021 annual meeting for helpful comments and editing assistance.

Conflicts of Interest

The author declares no conflict of interest.

References

- Wilson, K.E. Policy Lessons from Financing Innovative Firms; OECD Science, Technology and Industry Policy Papers, No. 24; OECD Publishing: Paris, France, 2015. [Google Scholar] [CrossRef]

- Belleflamme, P.; Lambert, T.; Schwienbacher, A. Crowdfunding: Tapping the Right Crowd. J. Bus. Ventur. Entrep. Entrep. Innov. Reg. Dev. 2014, 29, 585–609. [Google Scholar] [CrossRef]

- Baber, H.; Fanea-Ivanovici, M. Motivations behind backers’ contributions in reward-based crowdfunding for movies and web series. Int. J. Emerg. Mark. 2021. [Google Scholar] [CrossRef]

- Myalo, A. Comparative Analysis of ICO, DAOICO, IEO and STO. Case Study. Digit. Financ. Assets 2019, 23, 6–25. [Google Scholar] [CrossRef]

- ICO and IEO Report, 6th ed. 2020. Available online: https://www.pwc.ch/en/insights/fs/6th-ico-sto-report.html (accessed on 1 August 2022).

- Beedham, M. Here’s the Difference between ICOs and IEOs. 2019. Available online: https://thenextweb.com/hardfork/2019/03/21/initial-exchange-offering-ieo-ico/ (accessed on 16 August 2021).

- Lipusch, N.; Dellermann, D.; Ebel, P.; Ghazawneh, A.; Leimeister, J.M. Token-Exchanges as a Mechanism to Create and Scale Blockchain Platform Ecosystems. 2019. Available online: https://ssrn.com/abstract=3434941 (accessed on 20 July 2021).

- Baber, H. A Framework for Crowdfunding Platforms to Match Services between Funders and Fundraisers. Int. J. Ind. Bus. 2019, 10, 25–31. [Google Scholar]

- Catalini, C.; Gans, J.S. Initial Coin Offerings and the Value of Crypto Tokens; NBER Working Paper, 24418; NBER: Cambridge, MA, USA, 2018. [Google Scholar]

- Li, J.; Mann, W. Initial Coin Offering and Platform Building. Working Paper. 2018. Available online: https://pdfs.semanticscholar.org/309e/f98741d5da2003df8317fd605e1ac83d6fb9.pdf (accessed on 16 July 2020).

- Bakos, Y.; Halaburda, H. The Role of Cryptographic Tokens and ICOs in Fostering Platform Adoption. Working Paper. 2018. Available online: http://dx.doi.org/10.2139/ssrn.3207777 (accessed on 20 July 2021).

- Malinova, K.; Park, A. Tokenomics: When Tokens Beat Equity. Working Paper. 2018. Available online: https://ssrn.com/abstract=3286825 (accessed on 12 February 2020).

- Garratt, R.; van Oordt, M. Entrepreneurial Incentives and the Role of Initial Coin Offerings. Bank of Canada, Staff Working Paper. 2019. Available online: https://www.bankofcanada.ca/2019/05/staff-working-paper-2019-18/ (accessed on 16 July 2020).

- Chod, J.; Lyandres, E. A theory of ICOs: Diversification, agency, and information asymmetry. Manag. Sci. 2021, 67, 5969–6627. [Google Scholar] [CrossRef]

- Cong, L.W.; Li, Y.; Wang, N. Tokenomics: Dynamic adoption and valuation. Rev. Financ. Stud. 2021, 34, 1105–1155. [Google Scholar] [CrossRef]

- Lee, J.; Parlour, C. Consumers as Financiers: Crowdfunding, Initial Coin Offerings and Consumer Surplus. Rev. Financ. Stud. 2021. forthcoming. Available online: https://www.chapman.edu/research/institutes-and-centers/economic-science-institute/_files/ifree-papers-and-photos/parlour-lee-consumers-as-financiers-2019.pdf (accessed on 16 July 2022). [CrossRef]

- Miglo, A. STO vs. ICO: A Theory of Token Issues Under Moral Hazard and Demand Uncertainty. J. Risk Financ. Manag. 2021, 14, 232. [Google Scholar] [CrossRef]

- Gan, R.; Tsoukalas, G.; Netessine, S. Initial Coin Offerings, Speculation, and Asset Tokenization. Manag. Sci. 2021, 67, 914–931. [Google Scholar] [CrossRef]

- Adhami, S.; Giudici, G.; Martinazzi, S. Why do businesses go crypto? An empirical analysis of Initial Coin Offerings. J. Econ. Bus. 2018, 100, 64–75. [Google Scholar] [CrossRef]

- Amsden, R.; Schweizer, D. Are Blockchain Crowdsales the New “Gold Rush”? Success Determinants of Initial Coin Offerings. Working Paper. 2018. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3163849 (accessed on 12 December 2018).

- Ante, L.; Fiedler, I. Cheap Signals in Security Token Offerings (STOs). BRL Working Paper Series No. 1. 2019. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3356303 (accessed on 1 August 2022).

- Kher, R.; Terjesen, S.; Liu, C. Blockchain, Bitcoin, and ICOs: A review and research agenda. Small Bus. Econ. 2020, 56, 1699–1720. [Google Scholar] [CrossRef]

- Momtaz, P. Initial Coin Offerings, Asymmetric Information, and Loyal CEOs. Small Bus. Econ. 2020, 57, 975–997. [Google Scholar] [CrossRef]

- Masiak, C.; Block, J.H.; Masiak, T.; Neuenkirch, M.; Pielen, K.N. Initial coin offerings (ICOs): Market cycles and relationship with bitcoin and ether. Small Bus. Econ. 2020, 55, 1113–1130. [Google Scholar] [CrossRef]

- Boreiko, D.; Risteski, D. Serial and large investors in initial coin offerings. Small Bus. Econ. 2020, 57, 1053–1071. [Google Scholar] [CrossRef]

- Huang, W.; Meoli, M.; Vismara, S. The geography of initial coin offerings. Small Bus. Econ. 2020, 55, 77–102. [Google Scholar] [CrossRef]

- Anson, M. Initial Exchange Offerings: The Next Evolution in Cryptocurrencies. J. Altern. Invest. 2021, 23, 110–121. [Google Scholar] [CrossRef]

- Romero-Castro, N.; Pérez-Pico, A.M.; Ulrich, K. ICOs, IEOs and STOs: Token Sales as Innovative Formulas for Financing Start-Ups. In Financing Startups: Understanding Strategic Risks, Funding Sources, and the Impact of Emerging Technologies; Lassala, C., Ribeiro-Navarrete, S., Eds.; Springer: Cham, Switzerland, 2022; pp. 117–148. [Google Scholar]

- Tran Bui, M.A. Initial Exchange Offering and the Presence of Underpricing. Bachelor’s Thesis, Fakultät Kommunikation und Umwelt, Kamp-Lintfort, Germany, 2022. Available online: https://opus4.kobv.de/opus4-rhein-waal/frontdoor/index/index/docId/1468 (accessed on 24 August 2022).

- Mathew, G. IEO vs. STO vs. ICO; A Comparison of Tokenized Fundraising. Which One Is Better? 2019. Available online: https://medium.com/hackernoon/ieo-vs-sto-vs-ico-a-comparison-of-tokenized-fundraising-which-one-is-better-ab71b1c2a32b (accessed on 14 February 2020).

- Chavez-Dreyfuss, G. Explainer: Initial Exchange Offerings Flourish in Crypto Market. Reuters. 2019. Available online: https://www.reuters.com/article/us-crypto-currencies-offerings-explainer-iduskcn1tl2e0 (accessed on 12 January 2022).

- Prosvirkin, V. Why Do Projects Need an IEO? Finance Digest. 2020. Available online: https://www.financedigest.com/why-do-projects-need-an-ieo.html (accessed on 19 February 2022).

- Harris, M.; Raviv, A. The Theory of Capital Structure. J. Financ. 1991, 46, 297–355. [Google Scholar] [CrossRef]

- Miglo, A. Theories of Crowdfunding and Token Issues: A Review. J. Risk Financ. Manag. 2022, 15, 218. [Google Scholar] [CrossRef]

- Slyusarev, J. Analytical Report: IEOs in 2019–2020. 2020. Available online: https://blog.coinmarketcap.com/2020/04/15/analytical-report-ieos-in-2019-2020/ (accessed on 1 August 2022).

- Lee, S. Binance CEO on Launchpad and IEOs: “We Encourage Others to Copy our Model”. 2019. Available online: https://www.asiacryptotoday.com/binance-ceo-on-launchpad-and-ieos-we-encourage-others-to-copy-our-model/ (accessed on 17 July 2020).

- Cumming, D.; Johan, S.; Pant, A. Regulation of the Crypto-Economy: Managing Risks, Challenges, and Regulatory Uncertainty. J. Risk. Financ. Manag. 2019, 12, 126. [Google Scholar] [CrossRef]

- Bellavitis, C.; Fisch, C.; Wiklund, J. A comprehensive review of the global development of initial coin offerings (ICOs) and their regulation. J. Bus. Ventur. Insights 2021, 15, e00213. [Google Scholar] [CrossRef]

- Yen, J.; Wang, T.; Chen, Y. Different is better: How unique initial coin offering language in white papers enhances success. Acc. Financ. 2021, 61, 5309–5340. [Google Scholar] [CrossRef]

- Yu, J. Differences between a White Paper, Yellow Paper, and Beige Paper. Medium. 2018. Available online: https://medium.com/@hello_38248/differences-between-a-white-paper-yellow-paper-and-beige-paper-ad173f982237 (accessed on 8 January 2022).

- An, J.; Hou, W.; Liu, X. Initial Coin Offerings: Investor Protection and Disclosure. Technical Report, Working Paper. 2018. Available online: https://www.efmaefm.org/0EFMAMEETINGS/EFMA%20ANNUAL%20MEETINGS/2018-Milan/papers/EFMA2018_0159_fullpaper.pdf (accessed on 1 August 2022).

- Fisch, C. Initial coin offerings (ICOs) to finance new ventures. J. Bus. Ventur. 2019, 34, 1–22. [Google Scholar] [CrossRef]

- Momtaz, P. Entrepreneurial Finance and Moral Hazard: Evidence from Token Offerings. J. Bus. Ventur. 2021, 36, 106001. [Google Scholar] [CrossRef]

- Leland, H.; Pyle, D. Informational Asymmetries, Financial Structure, and Financial Intermediation. J. Financ. 1977, 32, 371–387. [Google Scholar] [CrossRef]

- Czaja, D.; Röder, F. Signalling in Initial Coin Offerings: The Key Role of Entrepreneurs’ Self-efficacy and Media Presence. Abacus-Sydney 2022, 58, 24–61. [Google Scholar] [CrossRef]

- Miglo, A. Pecking-Order Theory For Government Finance. Curr. Econ. US Can. Mex. 2020, 22, 137. [Google Scholar] [CrossRef]

- Leonard, J. Best IEO Crypto to Invest in 2022—Compare Initial Exchange Offerings. 2022. Available online: https://www.business2community.com/cryptocurrency/best-ieo-crypto (accessed on 1 August 2022).

- Wu, P. IEO vs ICO: Advantages and Disadvantages in 2022. 2020. Available online: https://cryptogeek.info/en/blog/ieo-vsico-dis-advantages2020 (accessed on 7 August 2022).

- Venegas, P. Initial Coin Offering (ICO) Risk, Value and Cost in Blockchain Trustless Crypto Markets. Value and Cost in Blockchain Trustless Crypto Markets. 2017. Available online: https://ssrn.com/abstract=3012238 (accessed on 1 August 2017).

- Doe-Bruce, O. Blockchain and Alternative Sources of Financing. In Cryptofinance and Mechanisms of Exchange; Springer: Cham, Switzerland, 2019; pp. 91–111. [Google Scholar]

- Chamorro Domínguez, M.C. Financing of start-ups via initial coin offerings and gender equality. In The Fourth Industrial Revolution and Its Impact Onethics: Solving the Challenges of the Agenda 2030; Miller, K., Wendt, K., Eds.; Springer International Publishing: Cham, Switzerland, 2021; pp. 183–197. [Google Scholar]

- Chod, J.; Trichakis, N.; Yang, S.A. Platform tokenization: Financing, governance, and moral hazard. Manag. Sci. 2021. forthcoming. [Google Scholar]

- Canidio, A. Financial Incentives for Open Source Development: The Case of Blockchain; MPRA Paper; University Library of Munich: Munich, Germany, 2018. [Google Scholar]

- Gryglewicz, S.; Mayer, S.; Morellec, E. Optimal financing with tokens. J. Financ. Econ. 2021, 142, 1038–1067. [Google Scholar] [CrossRef]

- Murray, J. Equity Crowdfunding and Peer-to-Peer Lending in New Zealand: The First Year. JASSA 2015, 2, 5–10. [Google Scholar] [CrossRef]

- Schwartz, A.A. Crowdfunding securities. Notre Dame L. Rev. 2012, 88, 1457. [Google Scholar]

- Signori, A.; Vismara, S. Returns on Investments in Equity Crowdfunding. 2016. Available online: https://ssrn.com/abstract=2765488 (accessed on 26 February 2019).

- Kaal, W.A.; Dell’Erba, M. Initial Coin Offerings: Emerging Practices, Risk Factors, and Red Flags. Verlag CH Beck. U of St. Thomas (Minnesota) Legal Studies Research Paper, (17-18). 2018. Available online: https://ssrn.com/abstract=3067615 (accessed on 1 August 2022).

- Takahashi, K. Prescriptive Jurisdiction in Securities Regulations: Transformation from The ICO (Initial Coin Offering) to The STO (Security Token Offering) and The IEO (Initial Exchange Offering). Ilkam Law Rev. 2020, 45, 31–50. [Google Scholar]

- Boreiko, D.; Ferrarini, G.; Giudici, P. Blockchain Startups and Prospectus Regulation. Eur. Bus. Organ. Law Rev. 2019, 20, 665–694. [Google Scholar] [CrossRef]

- Fahlenbrach, R.; Frattaroli, M.; ICO Investors. Swiss Finance Institute Research Paper No. 19-37, European Corporate Governance Institute—Finance Working Paper No. 618/2019. 2019. Available online: https://ssrn.com/abstract=3419944 (accessed on 17 August 2020).

- Liu, H.M. Why do People Invest in Initial Coin Offerings (ICOs)? Joseph Wharton Scholars. 2019. Available online: https://repository.upenn.edu/joseph_wharton_scholars/70 (accessed on 16 July 2020).

- Fisch, C.; Momtaz, P. Institutional investors and post-ICO performance: An empirical analysis of investor returns in initial coin offerings (ICOs). J. Corp. Financ. 2020, 64, 101679. [Google Scholar] [CrossRef]

- Howell, S.T.; Niessner, M.; Yermack, D. Initial coin offerings: Financial growth with cryptocurrency token sales. Rev. Financ. Stud. 2020, 33, 3925–3974. [Google Scholar] [CrossRef]

- Tao, Z.; Peng, B.; Ma, L. Optimal initial coin offering under speculative token trading. Eur. J. Oper. Res. 2022. forthcoming. [Google Scholar] [CrossRef]

- Benedetti, H.; Kostovetsky, L. Digital tulips? Returns to investors in initial coin offerings. J. Corp. Financ. 2021, 66, 101786. [Google Scholar] [CrossRef]

- Ante, L. Liquidity Shocks, Token Returns and Market Capitalization in Decentralized Finance (DeFi) Markets. BRL Working Paper Series No. 26. 2022. Available online: file:///C:/Users/amm114n/Downloads/BRLWorkingPaper26-LiquidityshockstokenreturnsandmarketcapitalizationinDeFimarkets.pdf (accessed on 1 August 2022).

- Fisch, C.; Masiak, C.; Vismara, S.; Block, J.H. Motives to Invest in Initial Coin Offerings (ICOs). 2018. Available online: https://ssrn.com/abstract=3287046 (accessed on 19 January 2020).

- Ofir, M.; Sadeh, I. ICO vs. IPO: Empirical Findings, Information Asymmetry, and The Appropriate Regulatory Framework. Vand. J. Transnat’l L. 2020, 53, 525. [Google Scholar] [CrossRef]

- Allen, F.; Fatas, A.; Weder di Mauro, B. Was The ICO Boom just a Sideshow of the Bitcoin and Ether Momentum? J. Int. Financ. Mark. I 2022. forthcoming. [Google Scholar] [CrossRef]

- Liu, R. NFT-Related Companies: Token Sale Returns. 2022. Available online: https://scholarship.claremont.edu/cmc_theses/2869 (accessed on 1 August 2022).

- Domowitz, I.; Glen, J.; Madhavan, A. Liquidity, volatility and equity trading costs across countries and over time. Int. Financ. 2001, 4, 221–255. [Google Scholar] [CrossRef]

- Chen, Y. Blockchain Tokens and The Potential Democratization of Entrepreneurship and Innovation. Bus. Horiz. 2018, 61, 567–575. [Google Scholar] [CrossRef]

- Schwienbacher, A. Entrepreneurial Risk-Taking in Crowdfunding Campaigns. Small Bus. Econ. 2018, 51, 843–859. [Google Scholar] [CrossRef]

- OECD. Initial Coin Offerings (ICOs) for SME Financing. 2019. Available online: www.oecd.org/finance/initial-coin-offerings-for-sme-financing.htm (accessed on 12 February 2020).

- Macey, J.; O’Hara, M. The Economics of Stock Exchange Listing Fees and Listing Requirements. J. Financ. Intermediat. 2002, 11, 297–319. [Google Scholar] [CrossRef]

- Merello, P.; De la Poza, E.; Jódar, L. Explaining shopping behavior in a market economy country: A short-term mathematical model applied to the case of Spain. Math. Methods Appl. Sci. 2020, 43, 8089–8104. [Google Scholar] [CrossRef]

- Ante, L.; Sandner, P.; Fiedler, I. Blockchain-based ICOs: Pure Hype or the Dawn of a New Era of Startup Financing? J. Risk Financ. Manag. 2018, 11, 80. [Google Scholar] [CrossRef]

- Miglo, A.; Lee, Z.; Liang, S. Capital Structure of Internet Companies: Case Study. J. Internet Commer. 2014, 13, 253–281. [Google Scholar] [CrossRef]

- Hernandez-Solis, M.; Herrador-Alcaide, T.C. Corporate Governance in FinTech Companies in The United Kingdom: An Exploratory Analysis for E-Disclosure 2017. Available online: https://www.researchgate.net/publication/317351181_Corporate_governance_in_FinTech_companies_in_The_United_Kingdom_An_exploratory_analysis_for_e-disclosure_Forthcoming (accessed on 1 August 2022).

- Kashuba, Y. Challenges of Corporate Governance for FinTech Companies in a pandemic Period. InterConf 2021, 81–87. [Google Scholar] [CrossRef]

- Najaf, K.; Chin, A.; Najaf, R. Conceptualising the Corporate Governance Issues of Fintech Firms. In The Fourth Industrial Revolution: Implementation of Artificial Intelligence for Growing Business Success; Springer: Cham, Switzerland, 2021. [Google Scholar] [CrossRef]

- Available online: https://www.pwc.in/assets/pdfs/consulting/financial-services/fintech/publications/data-governance-in-the-fintech-sector-a-growing-need.pdf (accessed on 1 August 2022).

- Tirole, J. The Theory of Corporate Finance; Princeton University Press: Princeton, NJ, USA, 2006. [Google Scholar]

- Thakor, A. Fintech and banking: What do we know? J. Financ. Intermediat. 2020, 41, 100833. [Google Scholar] [CrossRef]

- Bolton, P.; Huang, H. The Capital Structure of Nations. Rev. Financ. 2018, 22, 45–82. [Google Scholar] [CrossRef]

- Miglo, A. ICO vs. Equity Financing under Imperfect, Complex and Asymmetric Information. Working Paper. 2020. Available online: https://ssrn.com/abstract=3539017 (accessed on 25 July 2022).

Figure 1.

The sequence of events for ICO.

Figure 2.

Token market equilibrium (E). Bold line: token supply; dotted: line-token demand. (a) the number of token buyers is equal to or greater than the number of token sellers; (b) the number of token buyers is smaller than the number of token sellers.

Figure 2.

Token market equilibrium (E). Bold line: token supply; dotted: line-token demand. (a) the number of token buyers is equal to or greater than the number of token sellers; (b) the number of token buyers is smaller than the number of token sellers.

Figure 3.

The sequence of events for IEO.

Figure 4.

The sequence of events for ICO.

Figure 5.

The sequence of events with moral hazard for IEO.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Miglo, A. Choice between IEO and ICO: Speed vs. Liquidity vs. Risk. FinTech 2022, 1, 276-293. https://doi.org/10.3390/fintech1030021

AMA Style

Miglo A. Choice between IEO and ICO: Speed vs. Liquidity vs. Risk. FinTech. 2022; 1(3):276-293. https://doi.org/10.3390/fintech1030021

Chicago/Turabian StyleMiglo, Anton. 2022. "Choice between IEO and ICO: Speed vs. Liquidity vs. Risk" FinTech 1, no. 3: 276-293. https://doi.org/10.3390/fintech1030021