In this section, we first present a brief overview of Alberta’s electricity market operation. Moreover, we discuss price volatility and the occurrence of price spikes in Alberta, Ontario, and one representative price zone of New York’s electricity markets. We next review the basic structure of LSTM and XGBoost models and some of their previous applications in time series forecasting. We close this section with a review of a selected number of previous related papers that either have proposed hybrid models for electricity price forecasting, have focused on Alberta’s market, or have developed methods to model and forecast price spikes in electricity markets.

2.1. Alberta’s Electricity Market

The Alberta power system is consists of more than 500 substations and a network of transmission lines that covers 26,000 km in length and transports electric energy in a single control area of around 660,000 km

[

23]. Alberta also transfers electric energy across interties with three neighboring jurisdictions, i.e., British Columbia, Montana, and Saskatchewan. There are close to 350 active generation units that provide electric power to the grid in Alberta. In total, there are close to 200 market participants in both the supply and demand sides.

In Alberta, a must-comply rule exists, which means all energy from generators above 1 MW must be sold through the market. Power generators and importers submit electricity supply offers to the Alberta Electric System Operator (AESO). Exporters of electricity to neighboring jurisdictions submit bids to purchase supply generated in Alberta. Finally, consumers submit demand bids to purchase at or below a specific price [

24]. The offers must be submitted a day ahead (by noon) for each hour and may be updated periodically. These offers cannot change within two hours before the applicable delivery hour [

25]. This means that the offers for the hour running from 8:00 a.m. to 9:00 a.m. (denoted using AESO’s terminology as Hour Ending 9 or HE9) can be changed until 6:00 a.m. (the start of HE7). Note that these power generators are free to choose offer prices between the floor CAD 0/MWh and the cap CAD 999.99/MWh.

The AESO market clearing algorithm essentially sorts all supply (demand) offers (bids) from the lowest (highest) to the highest (lowest) price for each hour of the day into a so-called economic merit order curve. Following the changes in electricity demand throughout the day, the system controller keeps supply and demand in balance, dispatching from the merit order and maintaining, in this way, the reliability of the system. When the system demand increases, the system controller moves up the merit order and dispatches the next eligible supply or accepts the next demand bid. On the other hand, when the system demand declines, the system controller moves down the merit order and instructs suppliers to decrease their supply and/or consumers to increase demand. This way, the demand is always met with the lowest cost option available. The last supply offer used to meet the demand for each minute is called the system marginal price (SMP). The SMP reflects the intersection of supply and demand for each minute in the electricity market, and it is updated in real time. At the end of the hour, the time-weighted average of the sixty one-minute SMPs is calculated and published as the Hourly Alberta Pool Price (HAPP) [

24]. A uniform HAPP applies to all loads and suppliers within the province without any consideration of location.

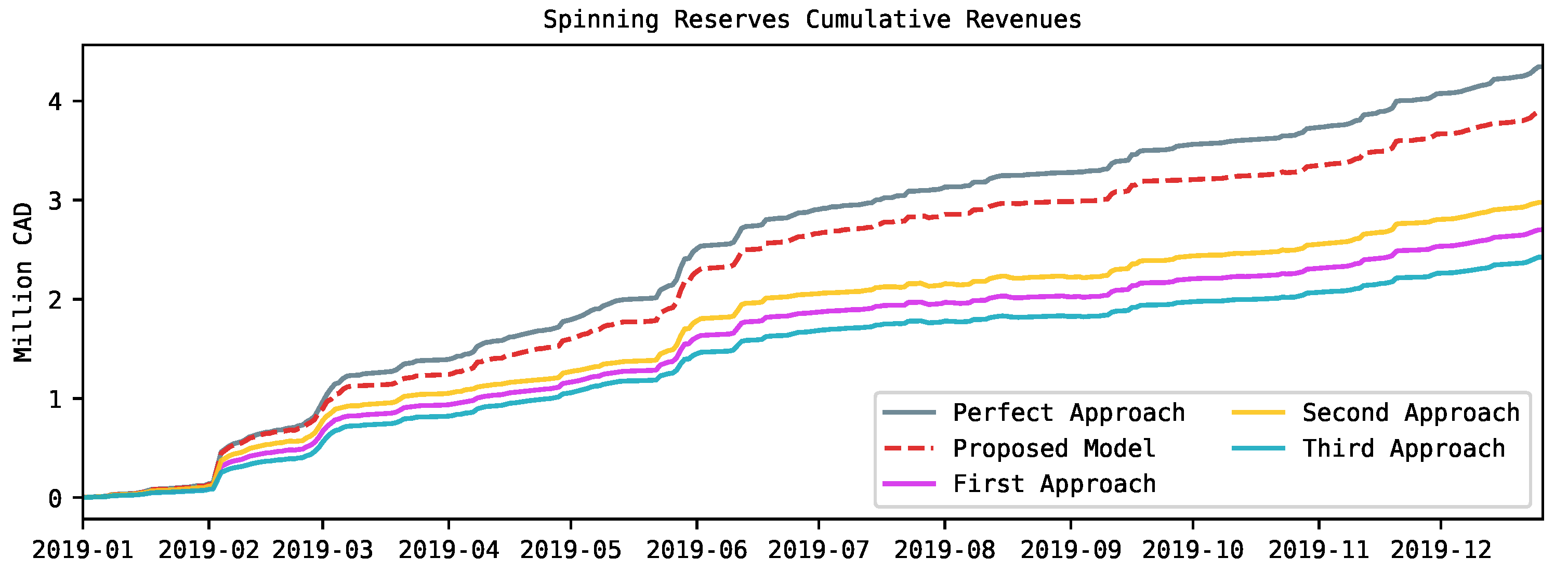

The energy market is run in real time, whereas the Alberta ancillary services (ASs) market is run a day ahead. The AS market includes 10 min spinning, 30 min non-spinning, and frequency regulation reserves. For each reserve, an equilibrium price is determined based on available offers, and the settlement price is the equilibrium price plus the HAPP. The equilibrium price may be positive or negative [

16]. Ancillary services market participants must submit their offers to the market operator before 11:30 a.m. the day before the operation day for all 24 h of the next day. For Mondays, the offers must be submitted before 1:00 p.m. on preceding Fridays. The AESO procures standby and active volumes of each type of operating reserve. The system controller first dispatches the active reserves, which are used to maintain the balance of the electric system under normal operating conditions. When the available resources in the active reserves portfolio are not enough to meet the real-time reliability and operating requirements of the electric system, the system controller proceeds to dispatch the standby reserves [

16].

Given the way the market clearing process is run, and depending on the nature of market participation, multi-hour-ahead electricity price forecasts could be used by market players to optimize their operation. For example, some large load consumers will need a short lead time to cut back their demand. For those, a one-hour-ahead or even a sub-hour-ahead forecast of high prices is often useful. On the other hand, suppliers need at least four hours heads up to change their offers within the permitted window. Furthermore, generators that participate in AS market use day-ahead for Tuesday–Friday (or multi-day-ahead for Mondays or long weekends) price predictions to increase their profits in the AS market.

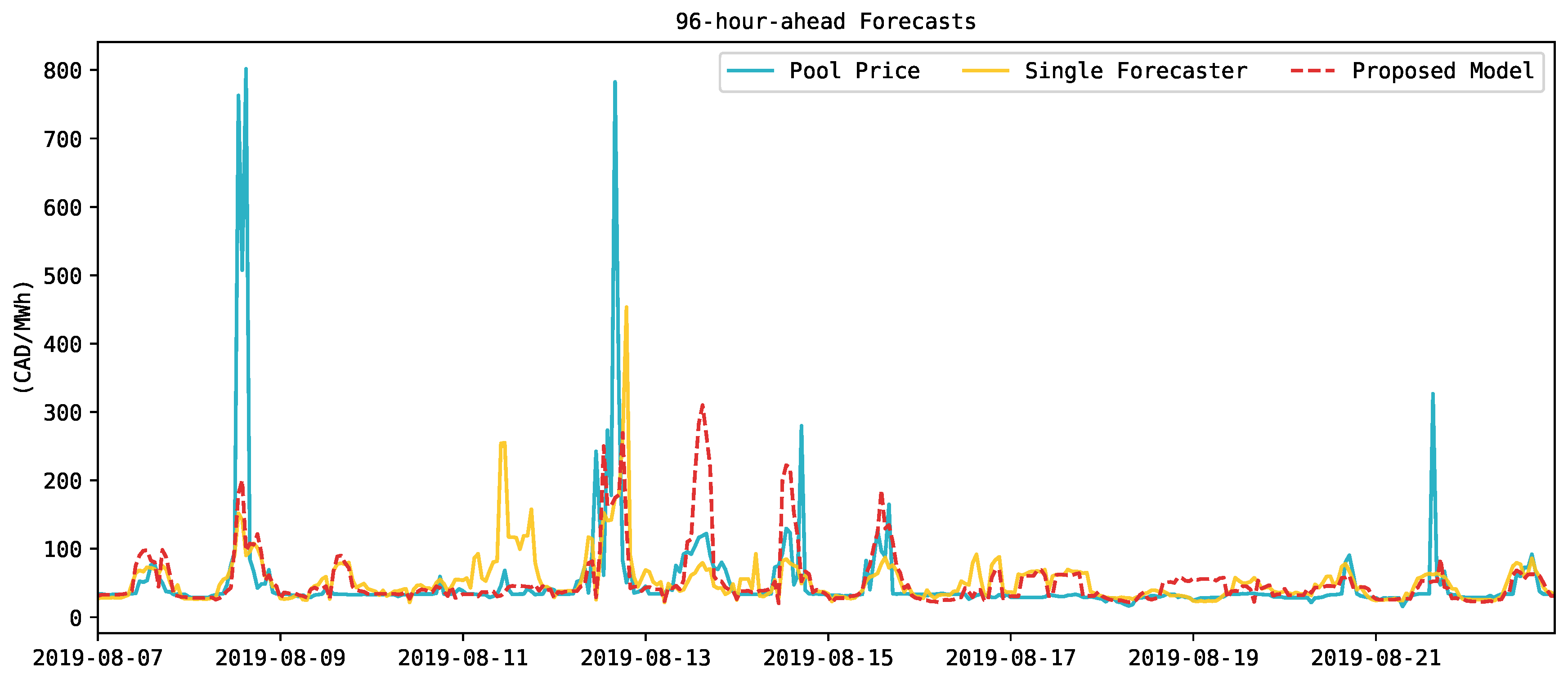

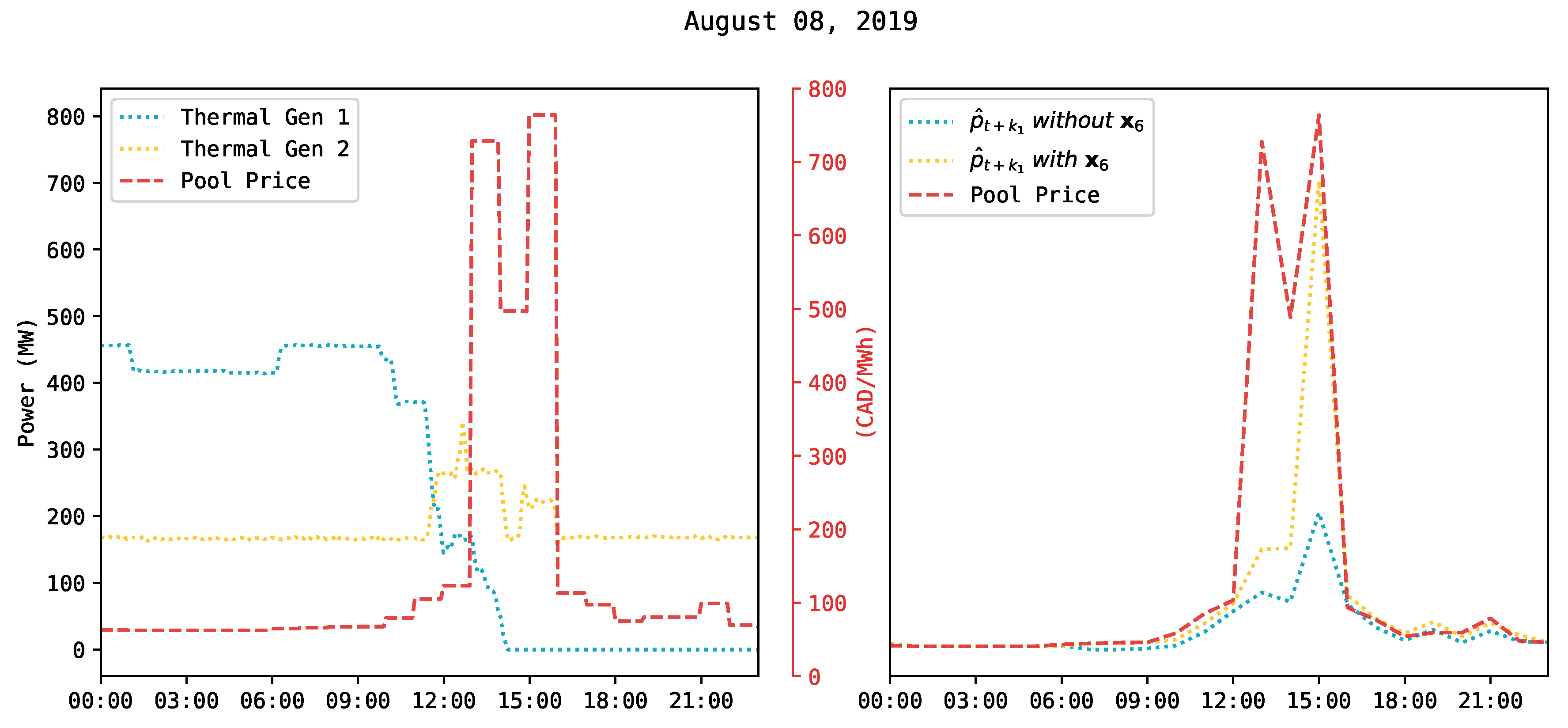

One of the most important features of the Alberta electricity market is that the HAPP fluctuates considerably from hour to hour. The pool price in Alberta can unexpectedly jump to a maximum of CAD 999.99/MWh, mainly due to short-term events, like outages at generation and transmission facilities, along with extreme weather conditions. On the other hand, the pool price can reach a minimum value of CAD 0/MWh due to surplus events.

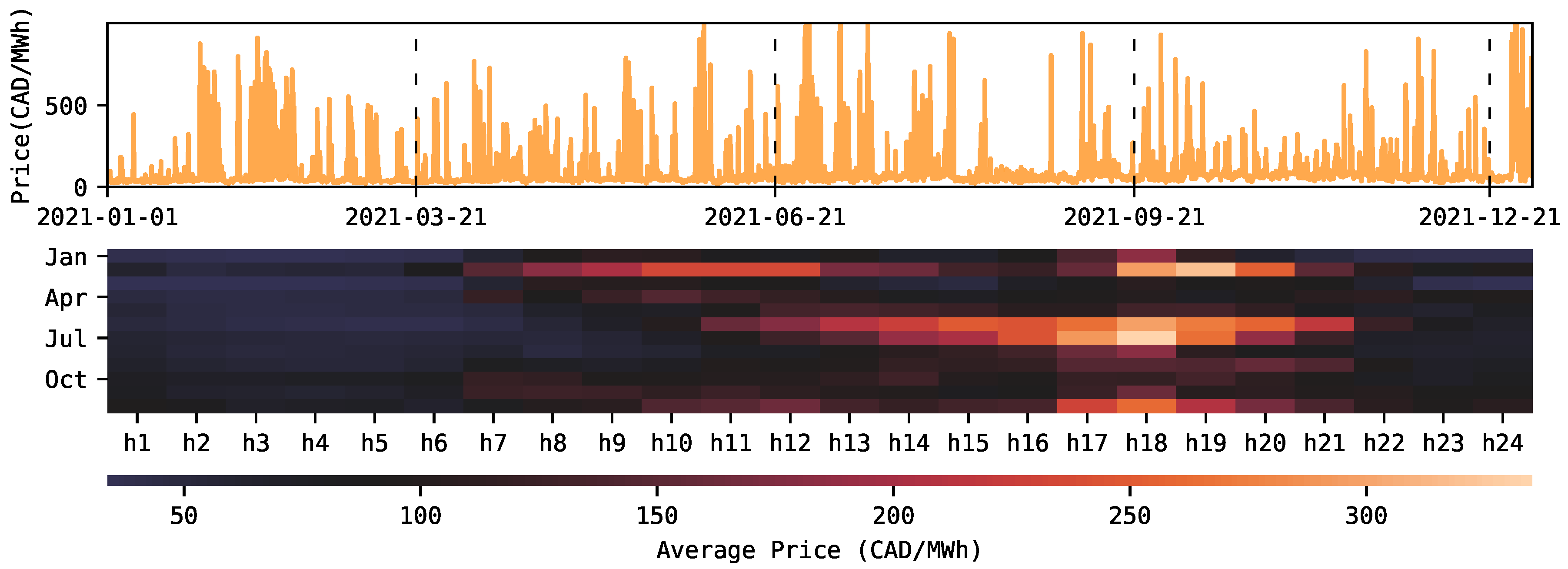

Figure 1 (top) shows the price fluctuations in the Alberta electricity market over the year 2021, where the occurrence of several price spikes can be appreciated. Furthermore, in

Figure 1 (bottom), a heatmap shows the average price for every month of that same year per hour of the day. High monthly average hourly prices, starting at values around CAD 100–150/MWh and up to more than CAD 200/MWh, can be observed during the on-peak period, i.e., from 7 a.m. to 11 p.m. every day [

26]. Furthermore, observe the presence of clusters of very high prices during both the summer and winter seasons.

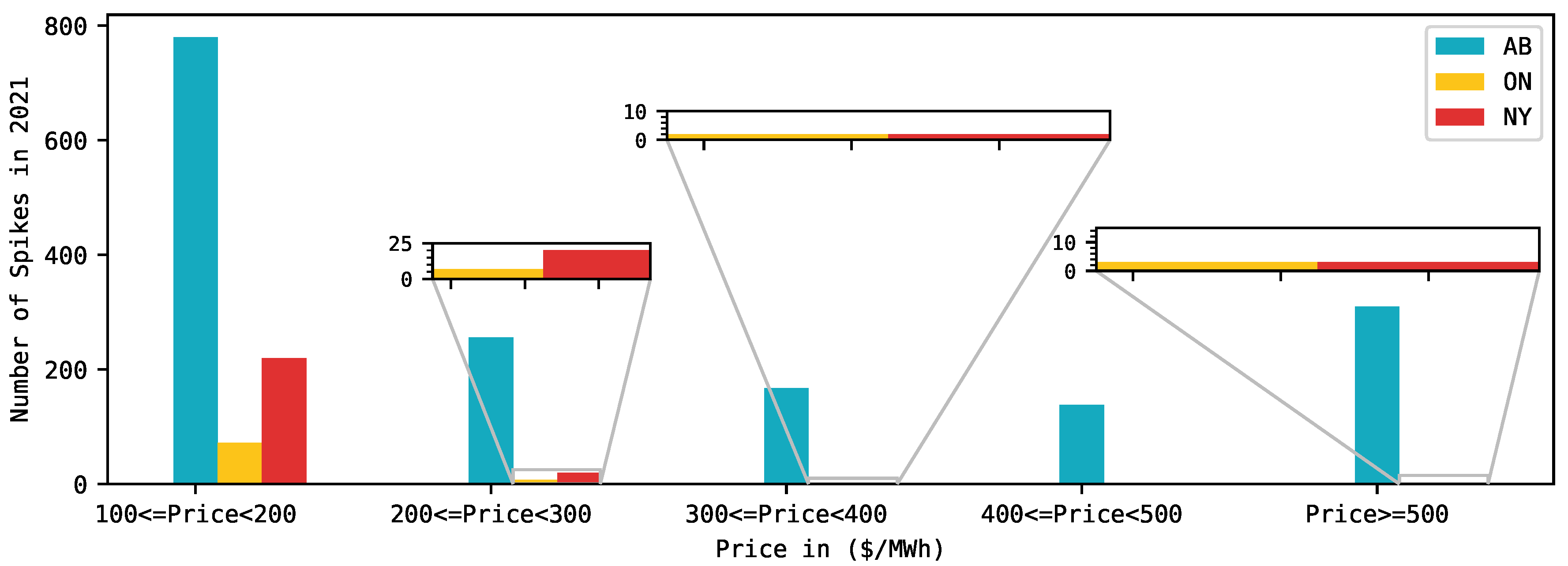

Figure 2 shows a comparison of the occurrence of price spikes between Alberta’s HAPP [

27], Ontario’s Hourly Ontario Energy Price [

28] (HOEP), and New York’s Locational-Based Marginal Price (LBMP) [

29] in 2021. Prices are clustered based on different price thresholds in

$/MWh (CAD/MWh for HAPP and HOEP, and USD/MWh for New York LBMP). Ontario’s electricity market [

28] is also a single-settlement real-time wholesale power pool, while the New York market [

29] is a two-settlement, day-ahead, and real-time market. For the latter, the real-time LBMP of a high-demand zone (i.e., Zone J or the one corresponding to New York City) is considered. Observe from

Figure 2 that the occurrence of price spikes in Alberta’s market surpasses the other two markets at all the different thresholds. Furthermore, as the threshold increases towards

$ 500/MWh, the occurrence of spikes for the Ontario and New York electricity markets dramatically decreases. For example, for the threshold between

$ 400/MWh and

$ 500/MWh, neither of these two markets registered any price spikes, while for that above

$ 500/MWh, the occurrence of three price spikes for both the Ontario and New York markets was detected.

Electricity price spikes can occur for several hours and this occurrence depends upon the system’s available supply and electric demand [

8], but also can depend on the bidding strategies used by different market participants [

30]. Higher-cost operating generators become operative usually when the demand increases, and they normally influence the price causing the occurrence of price spikes [

5]. The increasing number of price spikes in Alberta’s electricity market means that expensive operating generators (usually gas generators) have been required during the on-peak hours to meet demand. Furthermore, among other reasons, like higher demand and higher gas prices, for the year 2021, for example, the occurrence of price spikes is also associated with changes in the bidding strategies of large market participants [

26], following the expiration of their long-term power purchase agreements (PPAs). In other words, those participants are no longer subject to the contractual terms established in their PPAs to recover their fixed and variable operation costs, but now, they are recovered directly from the energy market.

As previously discussed, higher volatility levels can be observed in real-time electricity markets [

31]. Using the measure of return variation,

, presented in [

1], we conduct a comparative analysis of hourly spot price return variations between the Alberta, Ontario, and New York electricity markets. For the latter, again, we selected the load zone J (i.e., New York City zone), being the one having higher load concentration in that market. In this analysis, the time series of spot prices are scaled to zero–one. The return variations are calculated first, as the difference between the spot price at time,

t, and the spot price at

. For example, in [

1], intra-hour return variations are calculated, i.e.,

. Second, each difference is divided by the average value of the spot prices over

T, e.g.,

(2019, 2020, and 2021) years in our case. Finally,

can be estimated as the standard deviation of the price differences over

T. Furthermore, due to the increasing levels of renewable penetration, zero or negative spot prices can frequently be observed in modern electricity markets [

32]; hence, we decide to use

, as defined in [

1], to overcome the associated problems with arithmetic or logarithmic returns. In other words, prices differences,

, are defined as follows:

where

denotes the spot price at time,

t;

the spot price at

; and

T is the overall number of prices (

years in our case). Finally, the return variation,

, can be calculated as follows:

where

is the number of prices differences,

, and

is the simple

average, all of them over the time window,

T. Considering the volatility indices presented in [

31], we extend the analysis for

, i.e., intra-hour, trans-day, and trans-week return variations, respectively.

Table 1 shows the results for the return variations

,

, and

for each electricity market. Higher values are shown in bold letters. From the results observed in

Table 1, Alberta’s market presents the higher three-year return variations for each case, i.e., intra-day, trans-day, and trans-week. For example, Alberta’s intra-day return variations (i.e.,

) are, on average, 5.3 times higher than intra-day return variations from the other analyzed markets. Likewise, Alberta’s trans-day (i.e.,

) and trans-week (i.e.,

) return variations are, on average, 6.5 and 6.1 times higher than those from the other markets, respectively.

Furthermore, we observe from

Table 1 that trans-week variations show the highest value in all markets. For example, on average,

is 2.3 times higher than

for all the analyzed electricity markets; similarly,

is 1.3 times higher than

. As [

31] found in their work, trans-week price fluctuations are wider than those observed intra-hourly. From the analyzed period

T, and based on observations from

Table 1, we can conclude that higher return variations tend to occur in single-settlement electricity markets like Alberta’s and Ontario’s. This is in comparison with two-settlement electricity markets, like the one in New York. Furthermore, Alberta’s market presents higher intra-hour, trans-day, and trans-week return variations, thus, showing the challenging market dynamic faced by the proposed electricity price forecasting model.

2.2. Long Short-Term Memory Networks

Deep learning techniques have recently gained strength in the field of electricity price forecasting, mainly associated with the available computational power, volumes of data, and complexities of modern electricity markets [

20]. Recurrent neural networks (RNNs) are a popular method in time series forecasting. The structure of RNN consists of an input layer, one or more hidden layers, and an output layer. RNNs have a chain-like structure where connections between nodes form a directed graph along a temporal sequence. In contrast to feed-forward neural networks, RNNs include a feedback loop that allows the neural network to receive a sequence of inputs. In other words, in RNNs, the output of

is fed back into the network, having an impact on the outcome of step

t and for each subsequent step, allowing information to persist. For this reason, different types of RNNs, like long short-term memory (LSTM) or gated recurrent units (GRUs) have been used for electricity price forecasting [

20,

33]. In RNN, the backpropagation algorithm is used to calculate gradients and adjust weights between network layers during training [

34]. Nevertheless, the weights update scheme could stop the neural network from further training. The reason is that after a long chain, the gradient could vanish or increase notoriously. In other words, RNNs face many difficulties in learning from a long-term dependency [

35]. Long short-term memory neural networks are a variant of RNNs. They were proposed to address the drawbacks of the RNN on learning long-term dependencies [

18] by including more interactions per module or cell and by remembering information for prolonged periods [

36].

A typical LSTM network consists of memory blocks called cells. The cell state and the hidden state are transferred to the next cell. The main chain of data flow is given by the cell state, which permits the data to flow forward basically unchanged. Nevertheless, some linear transformations can happen and, via sigmoid gates, some data can be removed or added to the cell state. A gate is similar to a series of matrix operations that comprise distinct individual weights. Since the gates control the memorizing process, the LSTM networks can avoid the long-term dependency problem [

36]. The operation of the LSTM network is illustrated in (

3a)–(

3f):

where

is the forget gate that by the sigmoid function decides which information is not required and is going to be omitted or forgotten from the cell. In (

3b),

is the input gate that determines the amount of information of the network input,

, but also the previous hidden state,

that can pass into the memory cell. In (

3c) and (

3d),

is the update gate that creates a vector of new cell values, and

is the output gate that controls the amount of information of the current memory cell that can pass to the hidden state (

) in (

3f). In (

3e),

is the cell state that updates itself recursively by the interaction of its old value (

) with forget and input gates’ values. In addition,

,

,

, and

are the weights matrices of the forget gate, input gate, output gate, and update gate, respectively. The biases of the forget gate, input gate, output gate, and update gate are represented by

,

,

, and

.

Among others, electricity price forecasting is one of the research fields where LSTM neural networks have been used. By analyzing the market coupling impact on electricity price forecasts, different hybrid topologies of autoencoders based on LSTM and convolutional neural networks have been used to forecast the day-ahead electricity prices in the Nord Pool electricity market [

37]. Similarly, considering European market integration, ref. [

20] used different deep learning topologies, one consisting of a hybrid deep learning forecasting model based on an LSTM and a convolutional neural network, to generate day-ahead price forecasts for several European countries. In [

15], different forecasting models consisting of a single LSTM neural network and an LSTM part of one hybrid and two ensemble forecasting models were used to forecast day-ahead prices for the German market at one-, seven-, and thirty-day-ahead forecasting horizons. Similarly, ref. [

38] used a statistical spike filter [

8,

20,

39], Wavelet decomposition on the spot prices time series, in combination with an Adam-optimized LSTM neural network, to forecast electricity prices for the New South Wales region in Australia and French electricity markets. In [

33], shallow and deep architectures of LSTM neural networks were used to forecast day-ahead electricity prices for the Turkish electricity market.

2.3. Extreme Gradient Boosting

Extreme gradient boosting, also called XGBoost, is a scalable machine learning for tree boosting that was proposed by [

19]. XGBoost is optimized under the gradient boosting framework. The concept of boosting is to combine a series of models with low accuracy (weak models) to build a more robust model with better prediction performance. Gradient boosting uses the residual of previous models to correct the next model. It is called gradient boosting because it uses the gradient descent algorithm to minimize the loss function when adding new models. As an improvement, XGBoost adds regularization to the loss function, having, in this way, a better performance against over-fitting.

Let us consider a data set,

, where there are

n samples with

m features or variables. The predicted value of the model is defined as follows:

where

is the

l-th training sample,

represents an independent decision tree,

indicates the prediction score given by the

a-th tree to the

l-th sample, and

F is the space of functions containing all the regression trees. XGBoost uses the same concept of gradient boosting but improves it by a adding regularization to the objective function to measure the model performance:

The

L term represents a training loss function, which measures how well the model fits on training data.

is the regularization term that avoids over-fitting by penalizing the complexity of the model (i.e., the regression tree functions), and is given by [

19]:

where

T is the number of leaves in a decision tree,

is a parameter to scale the penalty,

is the complexity of each leaf, and

w is the vector of scores on leaves. The tree ensemble model is trained in an additive manner. Each time a new tree is added, the score is equal to the previous score plus the new tree’s score. Considering

, the prediction of the

l-th sample at the

b-th iteration, the objective function at the

b-ith iteration is given by the following:

Then, the second-order Taylor expansion is used to optimize the objective in the general setting. Assuming the loss function,

L, is the mean square error (MSE), the objective function can finally be estimated as follows:

where

and

are the first and second gradient of the loss function,

L. The objective function can finally be rewritten as:

where

denotes the instance set of a leaf,

s. For a fixed tree structure,

q, the optimal weight,

, of a leaf,

s, and the corresponding optimal value can be obtained by:

Equation (

10b) can be used as a scoring function to measure the quality of a tree structure,

q. A smaller value

means a better structure of the tree. Since it is impossible to enumerate all the possible tree structures,

q, a greedy algorithm that starts from a single leaf and iteratively adds branches to the tree is used instead.

and

are the instance sets of the left and right nodes after the split, with

. The gain formula, which is often used for evaluating the split candidates, is obtained by enumerating the feasible segmentation points and selecting the maximum gain partition and the minimum target function:

Among others, boosting tree-ensemble-based algorithms have been part of the modeling strategies of leader-board teams in important energy forecasting competitions, e.g., GEFCom2014 [

40,

41]. XGBoost is not the exception, and its robustness postulates it as a good candidate within the energy forecasting research field. For example, [

42] used an ensemble model to generate one-hour-ahead locational marginal price forecasts for the New England day-ahead electricity market. The forecasting model is composed of two “relevance support vector machines” and an XGBoost regressor. Particularly, the latter is used to model the complex behavior of the price spikes. Additionally, [

43] developed a hybrid forecasting model based on ANN with entity embedding to pre-process categorical data and an XGBoost regressor to forecast the day-ahead electricity prices in the PJM market.

2.4. Related Works

Hybrid electricity price forecasting systems consist of a combination of two or more existing price forecasting methods. These systems can be composed of only parametric, non-parametric, or a combination of both types of modeling approaches [

15,

44]. For example, in [

45], a hybrid system consisting of committee machines was employed to recursively generate electricity price forecasts within a 4-hour-ahead forecasting horizon. Each of the two forecasting models is composed of two support vector machines and two multi-layer perceptron Levenberg–Marquardt ANNs. This hybrid system was tested using data from real-time and day-ahead electricity markets, i.e., the Alberta and West Denmark Zone (Nordic) electricity markets, respectively.

A hybrid system composed of a seasonal auto-regressive integrated moving average model and a deep belief network was used by [

46] to forecast half-hourly and hourly electricity normal and spiky prices, respectively. The analyzed markets correspond to the Australian, Spanish, and PJM electricity markets. Similarly, ref. [

8] proposed a hybrid forecasting model purely based on ANNs to forecast normal and spiky prices in the real-time electricity market of Ontario. Forecasts were generated for a 24-hour-ahead forecasting horizon. In [

47], a hybrid mid-term electricity price forecasting system was proposed. Each of the three models consists of an auto-regressive integrated moving average model, along with principal component analysis, and an ANN model. The system is used to recursively generate forecasts of weekly average electricity prices for a 12-week forecasting horizon in the Brazilian electricity market.

Some previous studies have focused on building forecasting models for volatile, real-time markets [

8]. For example, using data from the Ontario electricity market, ref. [

9] forecasted 24-hour-ahead HOEP with ANN and fuzzy logic systems. Similarly, ref. [

48] generated 3- and 24-hour-ahead electricity price forecasts using time series models and ANN in the Ontario market. In [

49], half-hour-ahead forecasts for the Australian electricity market were generated using an extreme learning machine. Using daily electricity spot prices and a higher-order hidden Markov chain model in discrete time, the work in [

50] generated one-step-ahead forecasts on a daily forecasting horizon for the Alberta electricity market. The model estimation was conducted through the decomposition of the time series of spot prices into a seasonal and stochastic component, like in [

51,

52]. The former was modeled as the combination of sinusoidal functions, and the latter as the combination of an Ornstein–Uhlenbeck process and an additive compound Poisson component.

Some of the existing works have focused specifically on modeling and forecasting price spikes in electricity markets. In [

2], the demand-to-capacity ratio was used to estimate the probability of the occurrence of price spikes in the UK electricity market using a forecasting horizon that extends from 2 days up to 2 weeks ahead. The authors in [

53] proposed an auto-regressive Poisson model to forecast one-day-ahead price spikes in different interconnected regions of the Australian electricity market. The model used three exogenous variables and the short-term history of price spike occurrence. In reference [

54], the authors studied the mutual effects of interconnected regions within the Australian electricity market on the occurrence of price spikes. To do so, a dynamic copula-based multivariate discrete choice model generated one-step-ahead predictions of the probability of price spike occurrence using half-hourly historical prices of electricity. In a classification approach, reference [

55] used a variable threshold, along with feature selection via the Fisher score, to classify price spikes using a support vector machine for the Australian electricity market. However, the horizon over which the classification of new spikes was made was not specified.

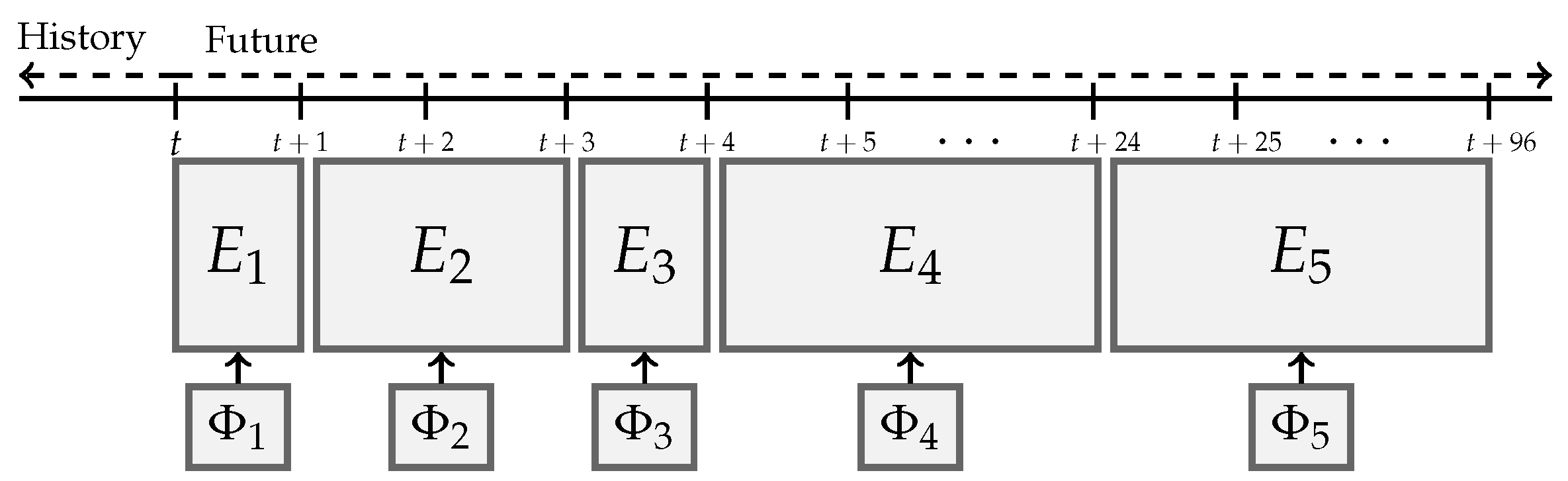

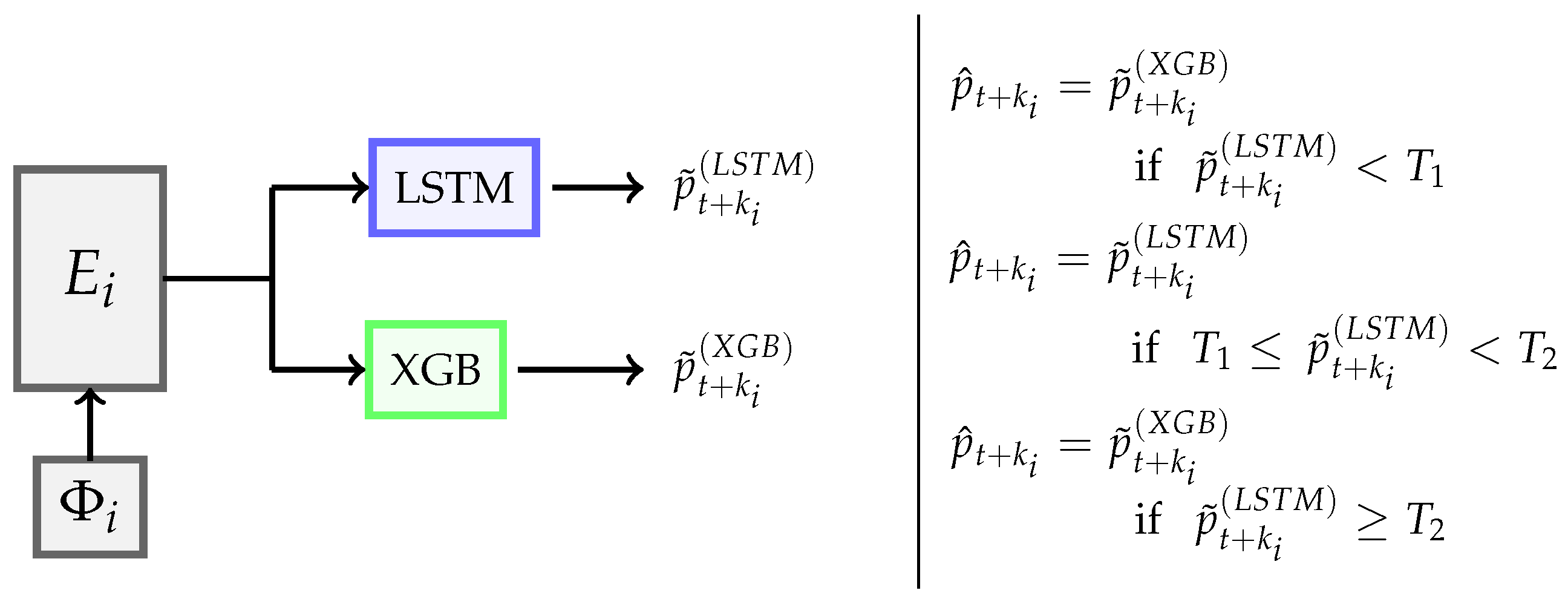

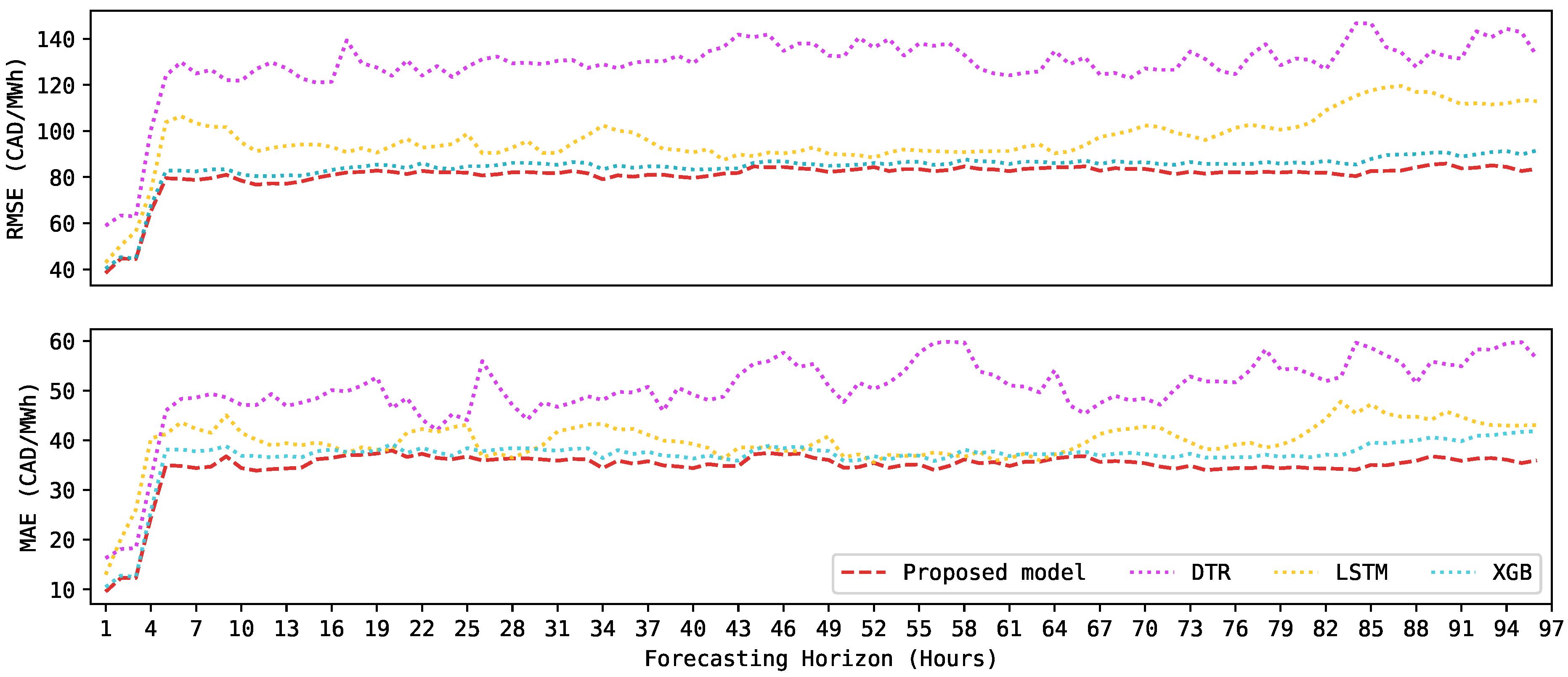

Our proposed method distinguishes itself from the existing approaches by employing a different approach to model combination in two dimensions. Conventional methods typically combine models in a “vertical” dimension, where multiple models are ensembled to generate forecasts for the same fixed forecast horizon. In contrast, our method combines models vertically, specifically focusing on enhancing the predictive ability of our model in detecting and predicting price spikes. Additionally, we combine models at a “horizontal” dimension to take advantage of available market data for each forecast horizon and generate forecasts for an extended 96-hour-ahead forecasting horizon. In other words, we break the forecast horizon into multiple segments and train and build a model for each segment, depending on what explanatory features are available at each horizontal dimension. Furthermore, in the existing works that have used Alberta’s market prices for their base case, no particular emphasis has been made on enhancing the ability of the models to predict the price spikes.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}