1.1. Background

The continuing increase in per-capita energy demand, coupled with the planet’s increasing population, is bringing critical threats to both the fight against global climate change and energy security issues. The COVID-19 pandemic and the consequent lockdown periods all over the world have emphasized the importance of secure, stable, and resilient electricity networks [

1].

The process of decarbonization, which is the progressive shift from fossil fuels to renewable energy technologies, requires on one hand a rapid growth of renewables, namely solar photovoltaic and wind power, and on the other hand an optimization of the role of natural gas as a transition medium [

2].

Solar photovoltaic energy (solar PV) is considered a very attractive solution among renewable energy sources (RES), especially for households. According to the most recent IEA report on renewables [

3], the growth of renewable power capacity at the world level has reached another record in 2021, driven by solar photovoltaic energy; solar PV alone has accounted for more than half of all renewable power expansion in 2021, followed by wind and hydropower.

Despite this rapid growth, some key challenges and market barriers remain and hinder a faster RES diffusion process. As highlighted by [

4], social acceptance and political feasibility are crucial elements for low-carbon transitions. The diffusion of renewable energy technologies is a complex process that involves multiple agents, with the interaction of firms and economic agents, public and private institutions, and final consumers (see, for instance, [

5,

6]). All these subjects may have different needs and expectations, different attitudes towards change, and respond to different economic and social incentives.

Focusing on PV adoption, a study on Switzerland aiming to explain the differences in PV growth at the subnational level [

7] showed that solar PV is more spread in areas with higher technoscientific knowledge, higher education institutions, and widespread innovation activity. Moreover, the critical role of local authorities, dedicated citizens, and energy companies has been highlighted for its ability to accelerate the uptake of this technology through locally based strategies.

A recent analysis of barriers and enablers for PV installation in [

8] identified economic, information, and administrative barriers, while enablers included subsidies, climate change concerns, as well as the opportunity to earn money. The analysis especially focused on the importance of the use of nonresidential buildings to strengthen the diffusion process. A meta-analysis of studies on residential PV adoption in [

9] suggested that measures should focus on enhancing the perception of benefits.

However, many other aspects may be accounted for when dealing with the diffusion of a renewable energy such as PV. For example, a study on Greece by [

10] highlighted the role of technological and demographic changes, in combination with climatic factors, to explain the differences among regions in terms of energy conservation and emissions reduction. The work by [

11] took a broader perspective, considering European countries, and assessed the sustainability of rooftop PV systems by taking into consideration the different solar potential of countries as well as the variety of electricity mix throughout Europe. The results of such analysis show that PV systems may be a viable solution for the future, but this depends on location and the local electricity mix. A more technical assessment on the sustainability and performance of PV systems comparing five different technologies, conducted by [

12], confirmed that overall, these technologies proved to be sustainable and environmentally friendly. As a general observation, these studies suggest that PV diffusion is characterized by many sources of heterogeneities, resulting from natural, technological, economic, social, and behavioral specificities.

Bearing in mind the multifaceted nature of a transition to PV systems and the multiplicity of agents and factors involved, in this paper we focus on the diffusion of solar PV in the United Kingdom, one of the top ten countries in terms of solar PV cumulative installed capacity according to the IEA-PVPS 2020 report [

13].

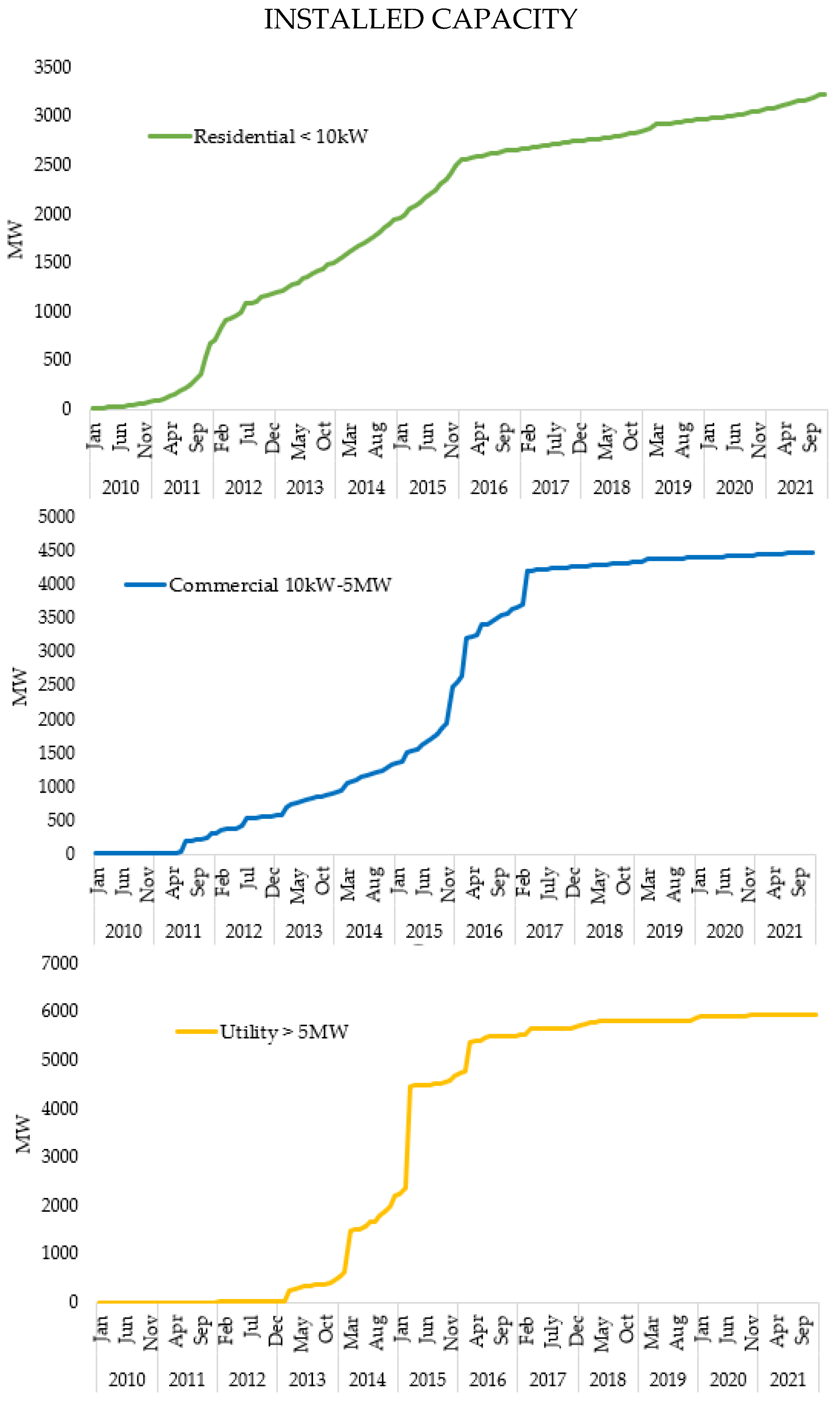

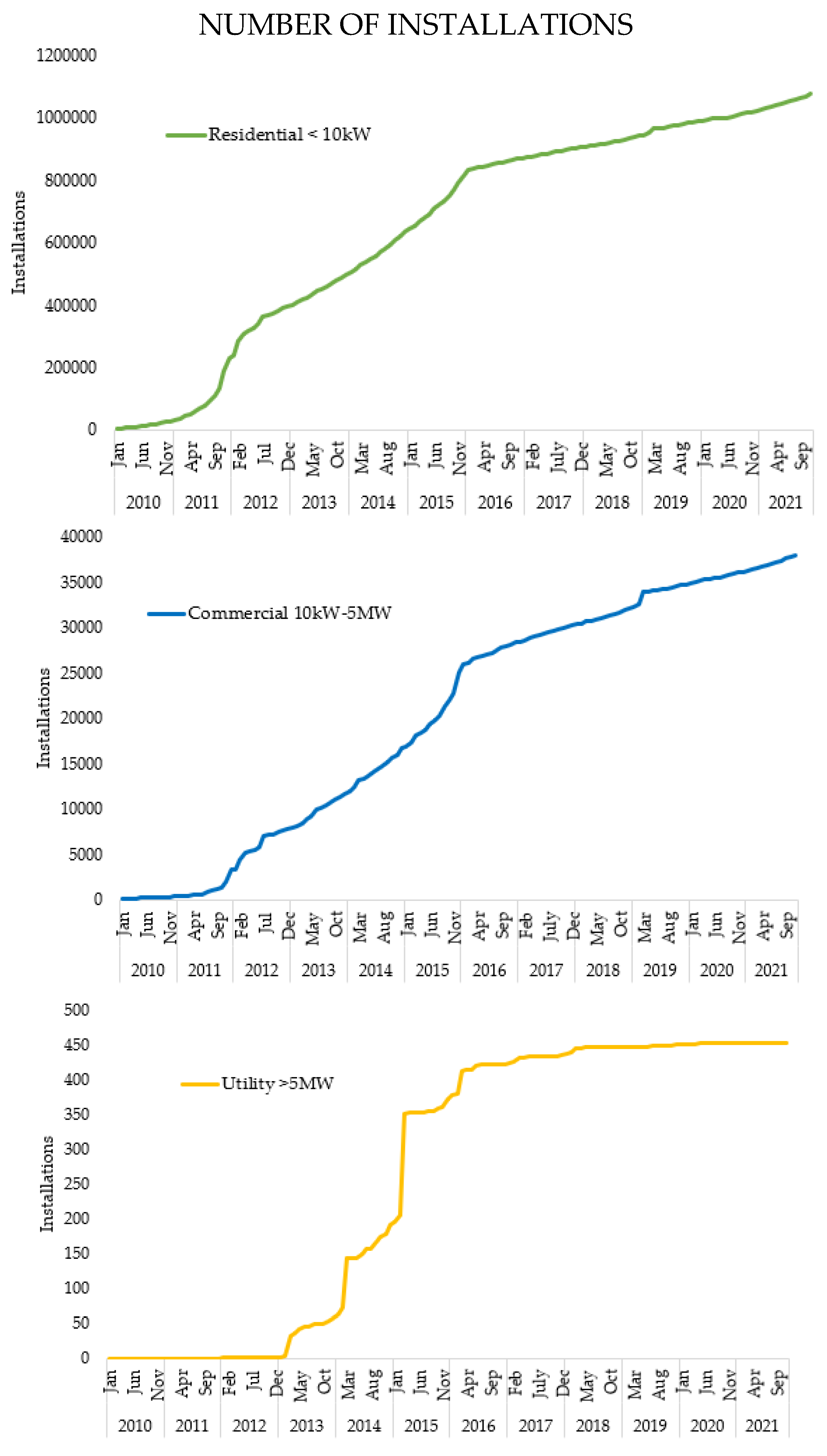

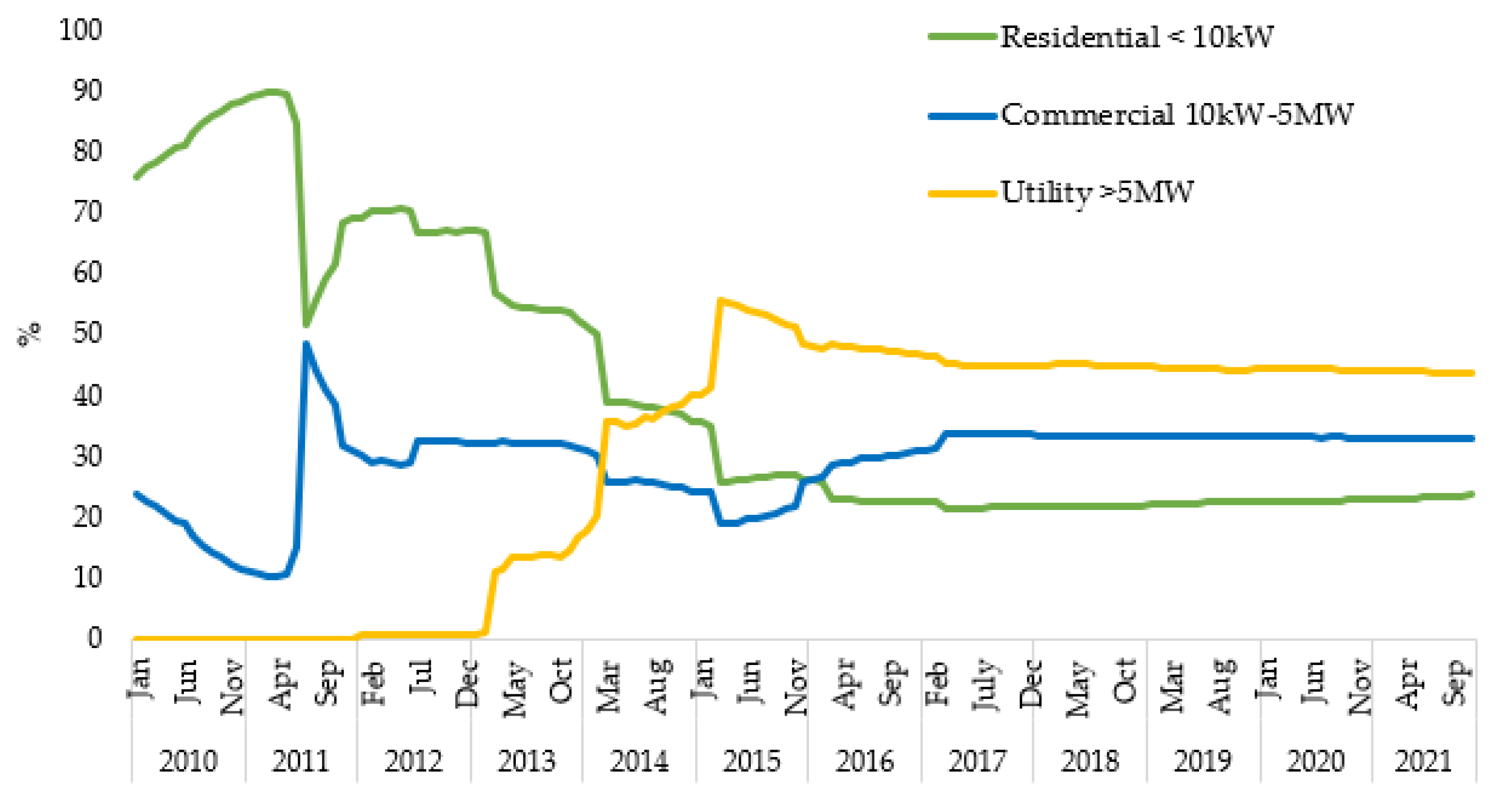

Compared with standard public data on energy diffusion, typically available only in a highly aggregated form, the UK case is of tantamount importance for the understanding of RES diffusion patterns, in view of the availability of highly disaggregated data, with time-granular (i.e., monthly) information on both installed capacity and number of installations of solar PV from January 2010 to November 2021, concerning three different and largely heterogeneous market categories: residential, commercial, and utility (i.e., licensed electricity suppliers).

1.2. Modelling the Diffusion of RES: A Short Review

The mathematical modelling of the temporal trends of diffusion processes has proved valuable in many applied sciences [

14]. Innovation diffusion models, extensively used after the seminal work of [

15], have also proved critically useful for describing and forecasting the growth of an energy source over the years, considering it as a technology that must be accepted in a market.

For recent reviews on the applications of innovation diffusion models for renewable energy technologies see [

16,

17]. Among the studies using innovation diffusion models for energy markets, [

18] proposed an innovative application of the so-called Generalized Bass model (GBM) [

19] to energy diffusions, whereby the GBM—thanks to the inclusion of suitable shock terms—was used as a diagnostic tool for describing the impact that external shocks (from, e.g., a war, a price shock or wave of policy incentives) exerted on diffusion trends.

In [

20], the GBM was applied to yearly time series of national solar PV capacity in eleven countries up to 2006, finding that public incentives had a key role in stimulating the growth of this technology. A recent cross-country study on 26 countries by [

21] has updated the findings of [

20] by including the dramatic incentive-triggered adoption waves since 2007. Both these works exploited the ability of the GBM to capture the effect of policy interventions and ad hoc incentives in driving the diffusion of solar energy. In [

21], the important role of the GBM as a parsimonious tool to capture the impact of “structured” shocks, i.e., shocks characterized by a precise pattern—as it might be the case of a policy intervention aiming to incentivize a market—on diffusions was noted. Structured shocks have a fully different nature compared, e.g., to standard stochastic perturbations. A complementary perspective based on the use of innovation diffusion models was proposed in [

22,

23], trying to understand the adoption of solar PV at the household level. In particular, the analysis proposed in [

23] suggested that information from the media should explain more about investment criteria, feed-in tariffs (FIT), and environmental attributes.

1.3. Contribution and Paper Organization

Most modelling studies of the diffusion of solar PV based on the well-accepted methodological approach of innovation diffusion models, initiated by the Bass model, have typically relied on yearly, highly aggregated data, generally at the national level. This paper aims to contribute to the growing literature on the diffusion of solar PV technology by considering sectoral diffusion patterns in the UK as allowed by the high degree of granularity of data available for this country.

Some recent works have considered solar PV diffusion in the UK [

24,

25,

26]. The authors of [

24] conducted an analysis of PV adoption data, along with a study of implemented policies, finding that areas of similar installed PV capacity are clustered, indicating a strong dependence on local conditions for PV adoption. In [

25], an interesting spatial analysis was performed in order to understand the socio-economic variables that help the adoption of solar PV and explain the spatial heterogeneity in the diffusion of such technology. In [

26], a simulation study evaluated the effects of a cautious reduction in FIT in the UK solar PV market. Their results suggest the counterintuitive effect by which a reduction in incentives (i.e., in the FIT), while reducing the adoption of solar PV, could incentivize battery storage.

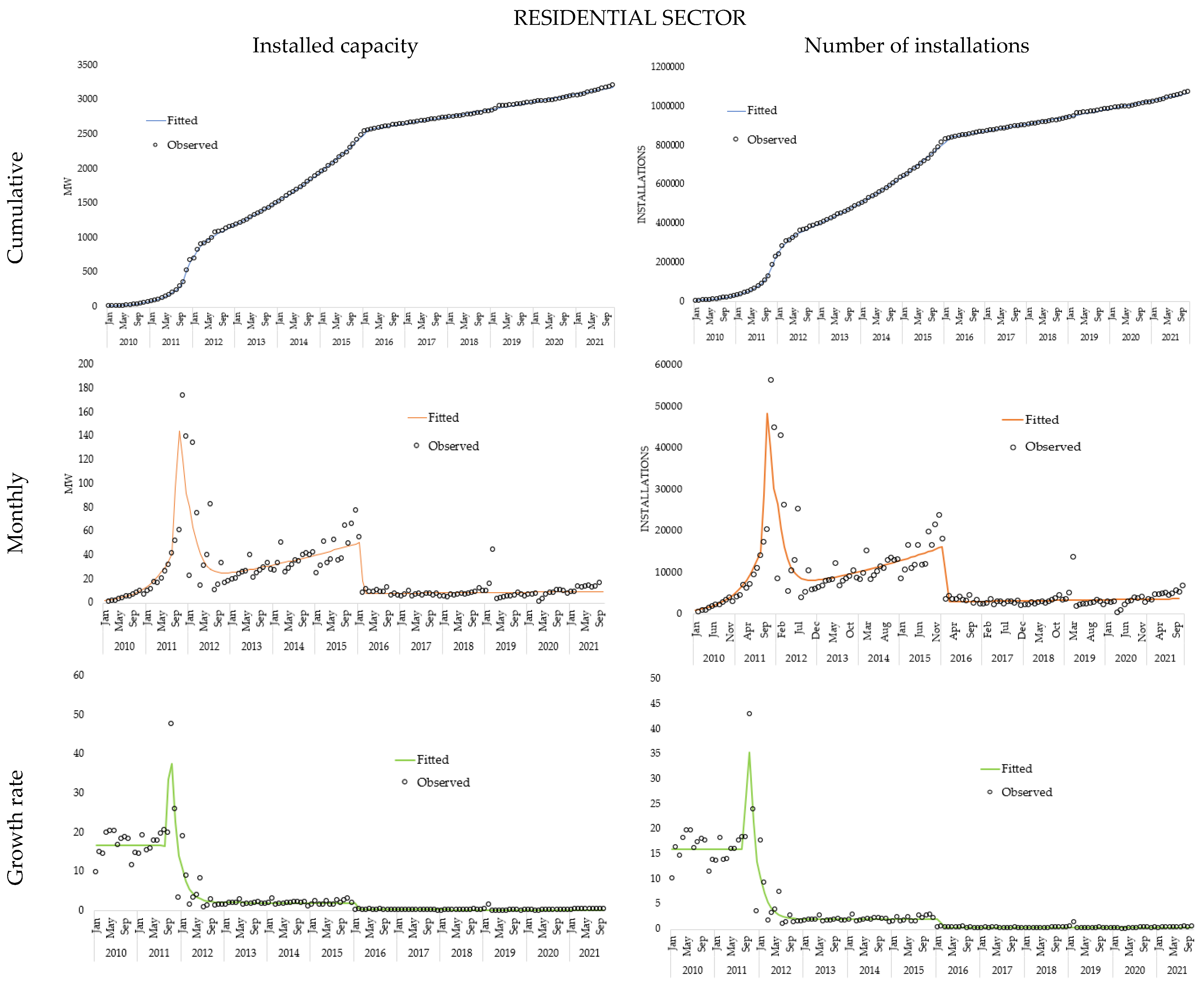

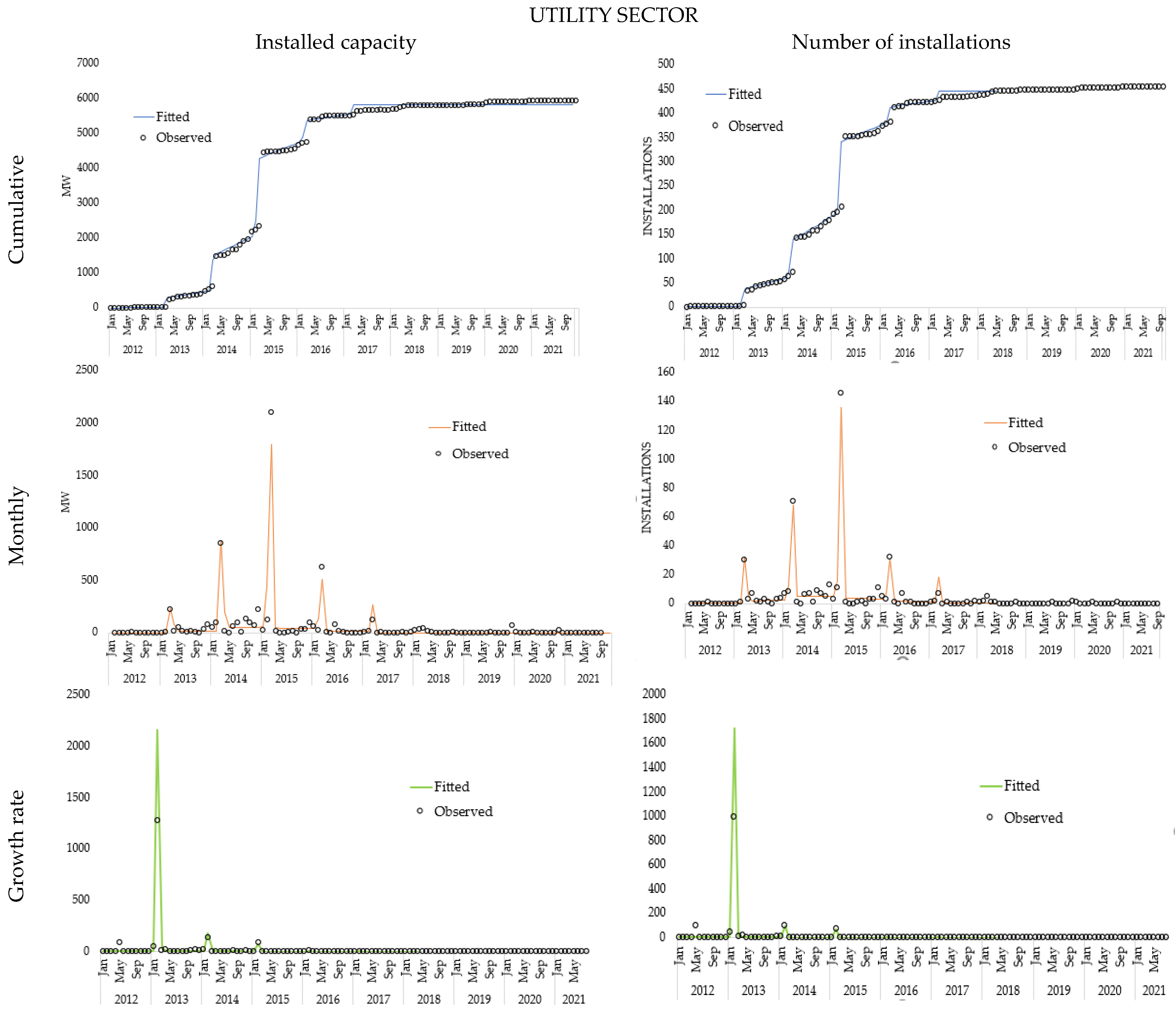

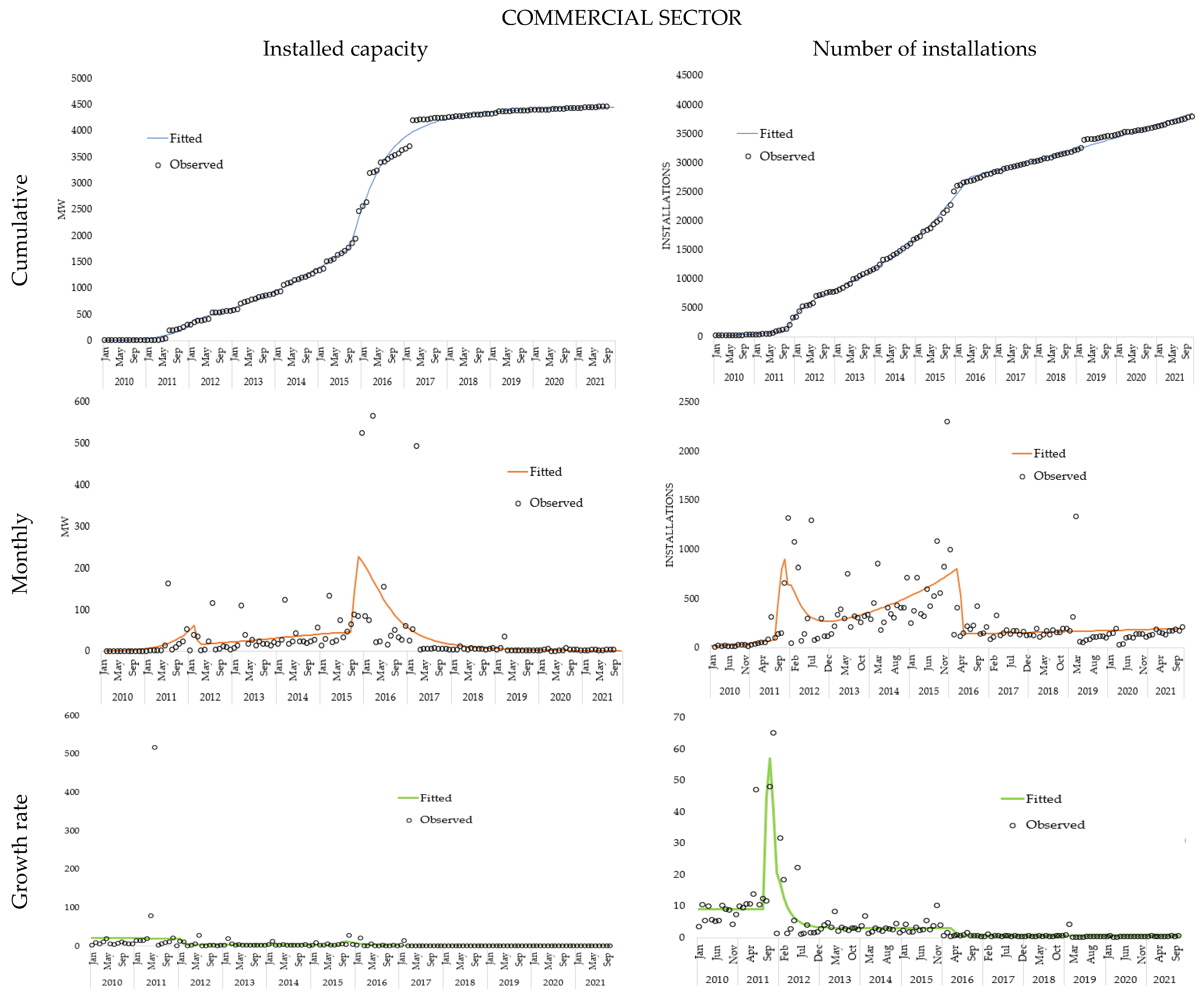

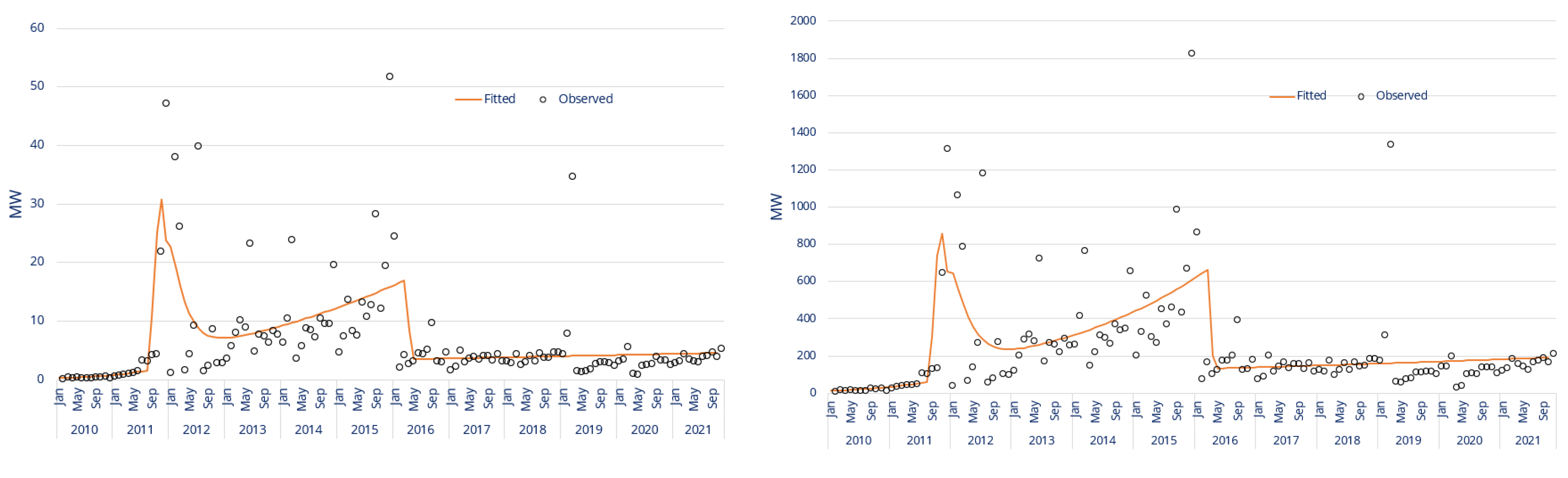

The present article uses the GBM to describe the heterogeneity in adoption behavior among different types of agents and on the related role played by the incentive measures provided by the UK government. To this end, we carried out separate nonlinear regressions with the GBM to the monthly time series of data on PV adoptions for each of the three sectors considered, namely residential, commercial, and utility. This allowed us to offer insights on how the UK government’s policies influenced the solar PV diffusion across these sectors in terms of persistence and intensity of the shocks emerging in the adoption trajectories. Additionally, we also highlighted the differences between these three categories in terms of the two main communication channels typical of Bass-type innovation diffusion models, i.e., the spontaneous communication among individuals (“word of mouth” or “imitation”) and the publicly available information supplied by the media. Moreover, as a by-product, we took advantage of the dual nature of the UK data, providing both the numbers of individual installations (which is the appropriate figure for diffusion models) and the installed capacity (which is the typically available figure), to discuss the appropriateness of installed capacity data.

Overall, our results indicate a general weakness of media support and a key role of incentives as the main drivers of the solar PV diffusion across sectors in the UK. Moreover, the imitation effect differs largely among the three sectors: while the residential market grows primarily because of public support, the commercial and utility sectors have an estimated imitation effect ten times larger. All in all, companies seem to make more rational decisions based on economic factors rather than being led by perceptions. Last, the results also highlight some nice regularities between the sectors analyzed, and situations where data by installed capacity and number of installations exhibit similar patterns, thus justifying the use of the former to predict the latter, at least in terms of trend.

The structure of the paper is as follows.

Section 2 presents the data employed for our study and the methodology, based on the GBM and its reduced version, the Generalized Internal model (GIM).

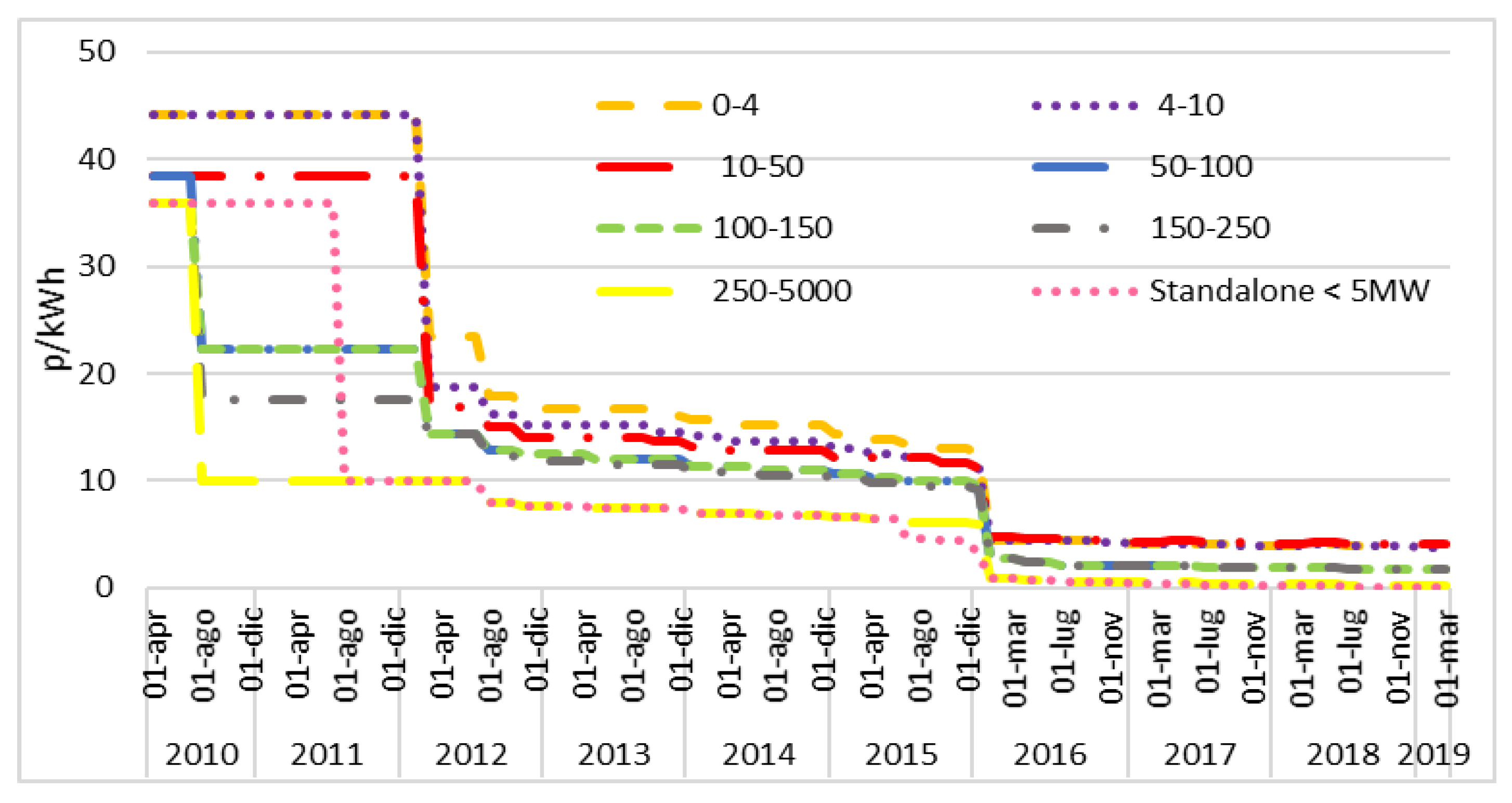

Section 3 presents an overview of the policies implemented in the UK for stimulating solar PV growth.

Section 4 applies the GBM and GIM to the data concerning the three categories and discusses the results obtained.

Section 5 is devoted to some discussion and

Section 6 to general conclusions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}