Digital Service Tax: Lessons Learned †

1

Faculty of Administrative Sciences, University of Indonesia, Depok 16424, Indonesia

2

Faculty of Economics and Business, Universitas Indonesia, Depok 16424, Indonesia

*

Author to whom correspondence should be addressed.

†

Presented at the 5th International Conference on Vocational Education Applied Science and Technology 2022, Teluk Betung, Indonesia, 26–28 October 2022.

Proceedings 2022, 83(1), 7; https://doi.org/10.3390/proceedings2022083007

Published: 19 December 2022

(This article belongs to the Proceedings of The 5th International Conference on Vocational Education Applied Science and Technology 2022)

{kind=link}

Abstract

:The rapid development of technology and globalization has provided significant business opportunities for digital companies. Digitization has led to changes in traditional structures, where businesses typically have a physical presence and are taxed in jurisdictions where businesses have a real presence. Several countries have made and established regulations on the tax treatment of trade transactions through digital systems. However, there are still pros and cons among the countries concerned. This study uses a qualitative approach to analyze the development of Digital Services Tax regulations in several European countries, including the earliest to make regulations on digital services taxes. The development of regulations in these countries is expected to be a reference for the application of digital services tax in Indonesia. The analysis results show the need for a Digital Service Tax (DST) to be imposed on entities that provide digital services on a specific basis, other than in the form of VAT. DST must consider the applicable international taxation regulations to avoid double taxation. Appropriate strategies and steps are needed to improve voluntary tax compliance. Finally, the government should set a provisional rate for digital taxes in Indonesia until a global consensus is reached.

1. Introduction

Globalization and the rapid development of technology have a significant impact on business patterns and business development [1]. Globalization has removed the barriers of regional boundaries and offers an increasingly widespread investment [2], while technology provides opportunities for businesses to provide internet-based services to their customers around the world so there is no need to establish a physical presence in the country where the customer resides [1]. This massive change in the business world is then better known as the digital economy [3]. Digitization in the economy generates tax revenue potential [4]. Indonesia’s digital economy is predicted to grow to USD 133 million in 2026. E-commerce is also considered to play an important role with a prediction of growing 34% or equivalent to USD 123 million in 2030 [5]. However, this potential can be lost when it cannot be utilized by the tax authorities. Today, markets and societies are increasingly technologically sophisticated. Trading digital content is considered to cause several tax problems. Digital tax management is also becoming progressively difficult, unlike real product sales to easily track [6]. This problem can be exacerbated when the tax system in a country is not able to compete with the digital acceleration, as experienced by Indonesia [7].

Digitization of both goods and the provision of services presents new challenges not only for markets but also for international taxation, where physical presence is no longer an obstacle to the expansion of international trade [7,8]. Over the past few years, there has been concern that the existing international tax system cannot capture and accommodate the proper treatment of digital-based economic transactions [8]. Currently, multinational corporations generally pay corporate income tax to the tax authorities in the jurisdiction where the corporation is incorporated. Meanwhile, the country where the consumer of the company is located, does not obtain any income from the transaction and caused controversy in many countries [1]. To solve this problem, the Organization for Economic Co-operation and Development (OECD) has formulated several rules that adopt the digital economic development. This proposal requires some of the world’s largest multinational businesses to pay some of their income taxes where their consumers are [9,10].

This study will explore the development of regulations from various countries regarding Digital Service Tax (DST), especially European countries which are the initiators of these regulations. We used qualitative method with literature study to collect data and information. The purpose of this study is to provide an overview of how DST is regulated in many countries in the hope that it can be an input for regulators in Indonesia. Finally, we conclude that Indonesia needs to specifically regulate the digital service tax so Indonesian consumers do not run double taxation. In addition, the government must also set temporary tariffs for digital transactions while waiting for a global consensus to be reached.

2. Theoretical Framework and Literature Review

2.1. Tax Optimization Theory

The strategy to increase the tax revenue is indeed necessary yet the policy do not generate economic distortions. Policies built must minimize distortion therefore the convenience of digital transactions for sellers and buyers is not disturbed and minimizes negative marginal effects when viewed from all indicators. There are three criteria that must be fulfilled, namely efficiency, equity, and administration costs. Tax optimization is carried out by designing and implementing tax policies aimed at maximizing the welfare of the community, taking into account various aspects including fair taxes, income distortion and information perfection [11]. It is necessary to add information technology flexibility [12]. A good digital transaction sales tax should not hinder the growth of digital transactions that drive overall economic growth. Some research found a significant relationship between e-commerce and GDP [4]. In the digital age, it is easy for consumers to buy goods and services worldwide as e-commerce reduces borders between countries. Collecting taxes on e-commerce activities requires access to the latest technology by tax authorities, but the latest technology can incur huge costs for the government [12].

2.2. Tax Principles

The effect of taxes and the characteristics of the taxation system in general includes 4 (four) things, including equality, certainty, convenience of payment, and economy in collection. Based on the e-commerce transaction framework, e-commerce tax policies must comply with several principles, including neutrality, efficiency, certainty and simplicity, effectiveness and Fairness, and flexibility. The ideal principle of taxation includes equality, revenue productivity, and ease of administration. The principle of ease of administration include the principle of certainty, the principle of convenience, and the principle of efficiency [13].

3. Result and Discussion

3.1. E-commerce in Indonesia

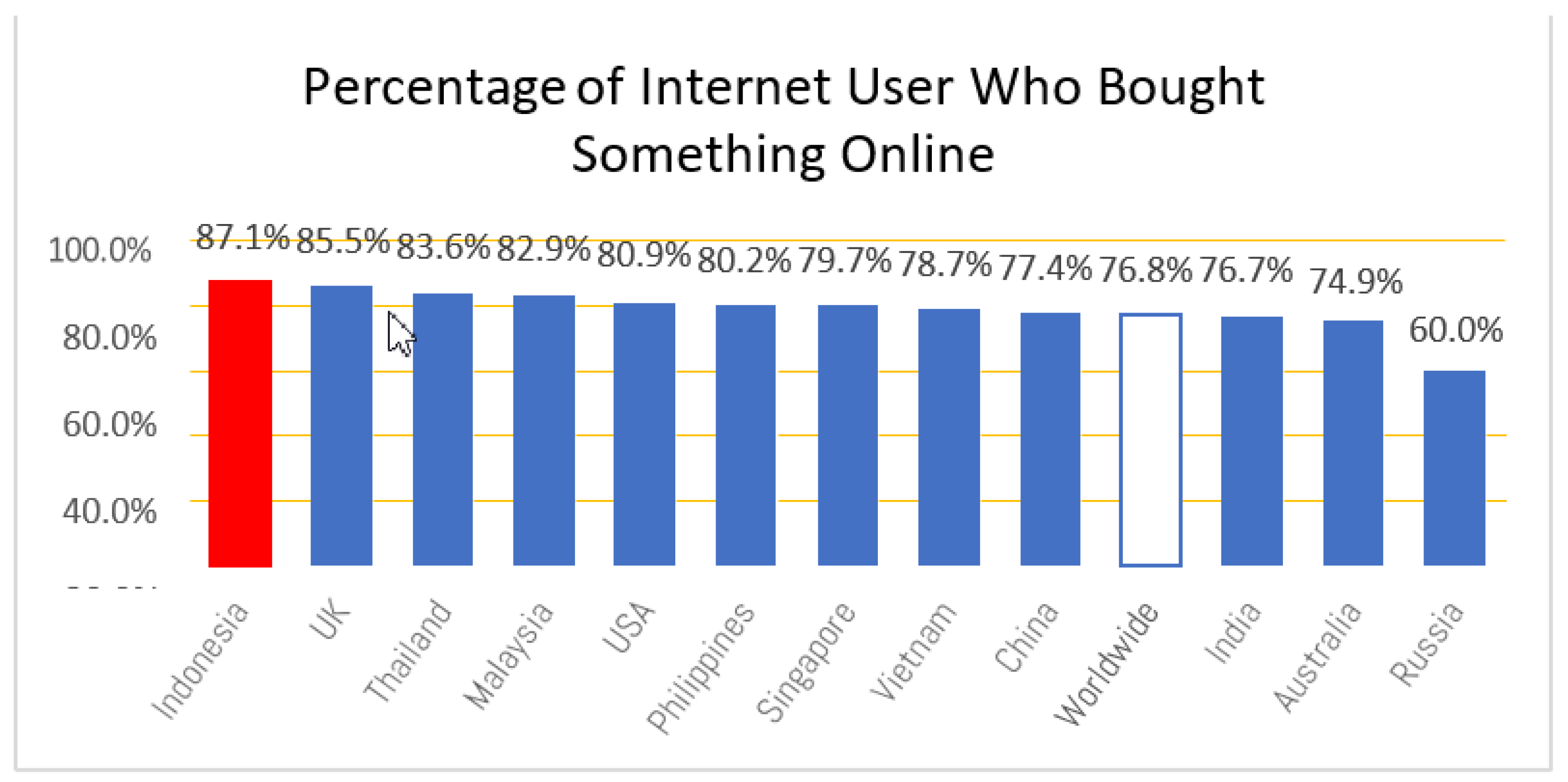

The e-commerce business in Indonesia has been running for a long time, such as buying and selling transactions in marketplaces such as Tokopedia, Bukalapak, Bibli.com, Kaskus, Traveloka, and others. Other forms include internet banking, SMS banking, Internet providers, digital TV, etc. The diversity of products is sold on e-commerce where the product can be in physical form such as clothes or electronics, such as e-books and online learning. E-commerce does not require a physical place for transactions and can be done anywhere, both within one jurisdiction and across jurisdictional borders [1,14]. The growth of e-commerce transactions will certainly have an impact on increasing Indonesia’s economic growth. As shown in Figure 1, Indonesia ranks first in terms of using the internet to buy things.

3.2. Indonesia’s Digital Tax Regulations

In dealing with the growth of e-commerce transactions, the Minister of Finance has issued regulation No.210/PMK.010/2018 concerning tax treatment of trade transactions through electronic systems (e-commerce). in accordance with the provisions of the applicable income tax laws. E-commerce has the duty to collect and deposit taxes. The ministry also requires merchants to have a NPWP and provide the NPWP to e-commerce managers. This regulation drew protests from e-commerce players and was eventually withdrawn.

Then, the government issued Government Regulation (PP/Peraturan Pemerintah) Number 80 of 2019 concerning Trading Through Electronic Systems (PMSE/Perdagangan Melalui Sistem Elektronik) to open the tax base. However, the Indonesian Tax Authorities (DJP/Direktorat Jenderal Pajak) is still hesitant to implement several points in the article for foreign companies that have income in Indonesia. Article 7 PP Number 80/2019 stated that every PMSE from abroad is obliged to appoint representatives domiciled in the jurisdiction of the Republic of Indonesia who can act as and on behalf of business actors, which means that e-commerce originating from abroad is obligated to have a Permanent Establishment (PE) used by foreign tax subjects. The taxation mechanism is regulated in accordance with the applicable laws and regulations. PE is not only defined by how a foreign company’s branch office can appear in Indonesia even without a physical office. Mentioning the Omnibus problem, the DJP has not yet decided on how to issue PE when the omni-bus tax law is enacted. Is the regulation in PP e-commerce still valid or not. The regulation contained in Article 7 of the PP E-Commerce does not have to be a BUT, but the application cannot be implemented because the rules are not technically specific.

Other regulations governing digital transactions are also contained in Government Regulation in Lieu of Law (Perpu) no 1/2020, Law (UU) no 2/2020, Government Regulation No. 9 of 2021 article 20 and UU KUP article 32 paragraphs 1 and 2, and UU HPP. Law number 2/2020 has stipulated that companies that are not registered in Indonesia can still be subject to income tax. However, this law is considered to have inconsistencies with PP number 80/2019 regarding the requirements for the imposition of foreign PMSE taxes. Law no 2/2020 does not make physical presence a requirement, but PP no 80/2019 obliges the organization of trade through foreign electronic systems to establish company representative offices in Indonesia.

The OECD (2017) conducted a study which stated that the tax system must transform and change continuously to adapt to the rapid advances in technology and digitalization, as well as the development of business patterns. The main objective is to increase the effectiveness and efficiency of taxation, or reduces costs and increases voluntary taxpayer compliance, to encourage economic growth and investment. The ideal tax system in the digital era according to the OECD is globally connected, technologically enabled, collaborative and integrated, data and insight led, better information compliance management, enabled workforce, and lastly, continue to transform and continue to change significantly following the latest digital technology and business trends. The Indonesian government has collaborated with the Automatic Exchange of Information (AEol) or the exchange of tax data and information since September 2018 with various world countries in the G20 countries. Information across borders in the era of globalization is unavoidable. With this collaboration, it should be able to assist the government in optimizing taxes, especially for cross-border e-commerce transactions (cross boarders) and compliance with tax compliance.

Jurisdiction for the Imposition of Value Added Tax, the place where VAT is due for cross- border transactions is important. The VAT Law in Indonesia has provisions regarding where VAT is due for cross-border transactions, but they are not formulated specifically and in detail. This is different from what is stated in the International VAT/GAT Guidelines or in the VAT Directive. In Article 12 of the VAT Law, VAT is payable for exports of BKP/JKP, imports of BKP/JKP from outside the customs area within the customs area. In paragraph 1 the location rule does not refer to the location where the BKP/JKP is used, but to the domicile/business activity of the party exporting the BKP/JKP. Article 4 paragraph 1 states that the delivery of which is tax payable is subject to delivery in the customs area. Reviewed closely, the place where VAT is owed for cross-border according to the VAT Law in Indonesia can be said to have not fully fulfilled the destination principle. In the destination principle, VAT is payable where the goods or services are consumed or utilized. The rules for paying VAT with the rules in Indonesia are not a problem for domestic transactions because the location of the BKP/JKP is consumed/used at the same location as the BKP/JKP submission location, which is in the same jurisdiction. However, for cross-border transactions, the location of BKP/JKP is used in different jurisdictions from the location of delivery. VAT regulations in Indonesia focus more on the administrative interests of VAT collection, different from the context of cross- border transactions, the determination of where VAT is due has major implications for determining the allocation of taxation and which country’s VAT system will apply to a transaction. The implications of the rules are absolutely different.

The digitalization of the economy forces tax decision makers to face the basic choice between destination based corporate income taxation and residence based corporate income taxation. On that basis, the USA still maintains the status quo [8]. The rapid growth in e-commerce has changed the ability of jurisdictions to enforce a destination- based commodity tax as appropriate for consumption taxes in cross-border trade [14]. Analysis and comparison are done through tax reform in Europe in response to e- commerce. Bacache Beauvallet (2017) examines the effect of online shopping on taxes and tax competition, eliminates destination-based taxation and origin-based taxation, and finds that tax competition decreases when taxes are imposed on origin based because the presence of the internet helps small countries to increase their taxes, and lead to tax convergence [15].

With the problem of cross-border transactions, there must be rules that are specifically, detailed, clear and different from the rules where domestic VAT is due and these rules must be able to capture the various complexities contained in cross-border transactions. As in several countries, the place where VAT is payable for cross-border transactions in the form of intangible BKP/JKP exports is a complex matter.

Jurisdiction of Income Tax Imposition. Based on income tax article 26, every overseas payment must be subjected to Article 26 Income Tax when the foreign taxpayer has a Permanent Establishment (PE) in Indonesia. In article 2, paragraph 5, the presence in Indonesia is indicated by physical presence. The income earned will be classified as the operating profit of the BUT. This becomes a problem when cross-border e-commerce transactions carried out by business entities abroad to individuals or entities in Indonesia, reviewing the presence or absence of BUT in Indonesia (physical). In fact, with e- commerce, physical presence or the existence of BUT is no longer needed, while e- commerce activities can take place freely. Article 2 (5) of the Income Tax Law states that one of the determinants of BUT is the presence of a server in the source country, but even the current P3B rules do not regulate this. P3B has not regulated income on e-commerce. The current SPT does not yet accommodate e-commerce transactions.

3.3. Learn from European Countries

In recent years, many countries have debated international tax rules which have been considered to have changed significantly. One of the main issues is the digital tax issue, where several European countries such as France, Italy, the UK, Spain, and Austria have unilaterally set a digital service tax (DST) in their respective countries with varying rates. Furthermore, the OECD strives to find the best solution for all countries. The OECD made a proposal for a new taxation rule containing 2 main pillars and was approved by 137 member countries in October 2021 [9]. Pillar 1 requires that multinational companies have an obligation to pay taxes to the countries where their consumers live. Meanwhile, Pillar 2 introduces a global minimum tax. The two pillars in the OECD Proposal are predicted to have an impact on global profits of $275 billion. However, along the way, there is still a lot of debate, some countries even threaten to re-implement DST unilaterally. It is therefore important to analyze why some European countries are eager to re-implement their DST and what lessons Indonesia can learn.

The European Commission has proposed a tax code proposal that would allow European countries to collect taxes from digital companies that take up markets in European countries. This proposal has a long-term goal. However, this proposal also proposes a temporary digital tax rate that can be applied by member countries. The DST rate in this proposal is 3% of the revenue of companies engaged in digital advertising, data sales, and online marketplaces. The proposal was first put forward in March 2018. Although it did not have full support from its member states, the European Commission stated that this work would continue when the proposal from the OECD also did not get full agreement [10].

Neither the EU nor the OECD have so far reached an agreement. This has made several European countries decide to bring this digital taxation proposal into their respective regulations. First, the UK has set a DST rate of 2% and will take effect from 1 April 2020. DST is intended for companies that provide digital services in the form of social media services, online marketplaces, and search engines for users in the UK [16]. Companies that will be subject to DST are those that have revenues of £500 million globally and £25 million from UK users. Unlike DST regulations in other countries, the UK is the first country to pay digital services companies £25 million in fees, meaning the company’s first £25 million in revenue from their digital services coming from UK users will not be taxed [10].

Second, France has introduced DST since July 2019 but will take effect from December 2020. This delay is the result of an investigation by the United States Trade Representative because it considers that the tariffs imposed by the French government are discriminatory. The DST rate imposed on companies providing digital services is 3%, following a proposal from the EU. Companies subject to DST are those that have revenues of more than €750 million or about $840 million globally and €25 million ($28 million) in revenue generated from French users. The potential DST that has been calculated by the French tax authorities is 0.05% of France’s total tax revenue in 2018. Third, Austria only stipulates DST for companies that provide digital services in the form of online advertising. Austria’s DST rate is higher than that of the UK and France because the Austrian tax authorities set the DST rate at 5%. some say that it is almost indistinguishable between traditional and online advertising tax rates. The difference is only in the taxable company threshold. DST is only assigned to companies that have global revenues in excess of €750 million ($840 million) or revenues in excess of €25 million ($28 million), earned from their customers in Austria. Potential tax revenue from DST is estimated at 0.02% of Austria’s total tax revenue in 2018.

3.4. Learn from ASEAN Countries

Most ASEAN countries are studying e-commerce taxation such as Thailand, the imposition of an upper limit tax of 15%, registered, baht currency or transferring money into the country; Indonesia, as discussed previously, Indonesia has issued PMK210/2018 and PP10/2018 and e-commerce is included in the PP74/2017 roadmap for an electronic- based national trading system, but implementation has not yet been implemented, through the use of transaction payment data (National payment Gateway) monitored by BI (Bank of Indonesia) in cooperation with the Ministry of Communication and Informatics; Singapore, applying e-commerce tax of 7% or 0% depending on the destination; Malaysia, will apply 6%; Laos, Cambodia, Brunei Darussalam, Vietnam, Myanmar have not yet implemented e-commerce taxes.

Application of e-commerce taxes ASEAN countries in European countries, e- commerce taxes are applied based on above the threshold and MOSS (mini one stop shop) online service for tax regulation; Australia applies 10% of the total value of online trade, with a lower threshold for online transaction value of one thousand Australian dollars and e-commerce companies whose income value is >75 thousand Australian dollars must register at the tax office and follow tax regulations; South Korea as of June 1 2015 applies 10% and does not have to open a branch office but registers VAT to the electronic taxation system, there is no threshold, paid every 3 months to a Korean bank; India applies 6% B2B in excess of a certain limit. other collections other than PPh, Equalizatio. Levy Rules (EQL); China applies scheduled VAT at various tax rates; The United States applies the Tax Freedom Act, there are no special taxes, e-commerce taxes are treated equally; Japan, there is no special tax for equal treatment but has a PROTECT (Professional team for e- commerce taxation) to hunt e-commerce players who do not carry out tax obligations.

3.5. Recommendations for Indonesian Regulators

Learning from regulatory policies in other countries, tax policy on digital transactions is needed to increase state revenue (revenue productivity). Determination of tax policy must be broad-based, in accordance with long-term policies, and comply with taxation principles. Wrong taxation policies can cause economic distortions, thus hampering efforts to recover the economy and state revenues. Tax policy on digital transactions must be balanced between the goal of increasing state tax revenues and encouraging the growth of digital transactions that meet taxation principles.

Income taxes or taxes on Trading Through Electronic Systems (“PMSE”) activities carried out by foreign tax subjects who meet the provisions of significant economic presence introduced in Article 4 of Perpu No. 1 of 2020, must consider several things in implementing regulations. Law No. 2 of 2020 has accommodated 3 types of tax schemes including Value Added Tax (VAT) for trade through electronic systems, Income Tax (PPh) for trade administration through overseas electronic systems, and taxes on electronic transactions.

The implementation of the imposition of Value Added Tax (VAT) on digital transactions will increase the fees that must be paid by Indonesian consumers (not digital businesses) for the use of subscription fees for Netflix (California, US), Youtube (California, US), Google Cloud (California, US), and others. For companies that are subject to Indonesian tax, the VAT can be used as compensation with VAT input tax, until the net off state revenue may not be as large as expected. It is necessary for the government to set the criteria for VAT for digital transactions input as late as there is no moral hazard from PMSE business actors. Meanwhile, digital taxes through the application of income taxes or through DST are currently not implemented because they are still waiting for global consensus so that there will be no retaliation or policies that weaken tax relations between countries. However, if we learn from other countries, the government needs to set a certain deadline (period) to wait for a global consensus to occur. The longer the global consensus is realized, the more it will cause the loss of potential tax revenue from digital transactions.

The income tax (PPh) imposed on PMSE business actors needs to be implemented using the PMSE Tax (apart from General Income Tax) with the imposition of the type of digital tax that will be imposed, the basis of calculation, threshold, and certain rates taking into account the application of international taxes. The imposition of income tax on digital taxes is temporary until there is a final decision from the OECD, EU and G20, considering that Indonesia is the largest market share for multinational companies in the digital economy.

The Government of Indonesia should define the criteria for “significant economic presence” as stated in Law no. 2 of 2020 article (7) precisely and specifically related to the world’s big digital companies that have users in Indonesia who need to be taxed, in regard to the extensification of tax revenues is achieved by considering the aspect of “fairness” for digital companies that are taxed and, not making perpetrators Businesses have to incur large compliance costs but they are not proportional to the tax revenues that will be received by the government. For example, in France, the regulation on digital tax services with the criteria of significant economic presence will only apply to 17 large companies, of which 16 companies are headquartered in the United States. So, it is recommended that the government should focus more on companies that have the potential to make a significant contribution to state tax revenues.

Learning from European countries, the types of digital services subject to tax include Digital services taxes, Digital advertising taxes, and Unilateral adjustments to PE definitions [1]. Therefore, the PMSE Tax Object on the use of intangible Taxable Goods (BKP) and Taxable Services (JKP) including the use of digital services from outside the customs area within the customs area through PMSE transactions must include various digital business models so that state tax revenues can be received. achieved more optimally. In addition, efforts are needed to improve the capability of DJP human resources who are competent in identifying, analyzing aggressive tax planning through the transfer of profits from PMSE transactions, as well as investigative skills to see potential tax revenues from PMSE transactions, PMSE Tax Administration and optimization of information technology in services, managing the tax system, controlling and collecting PMSE taxes. Designing appropriate strategies and steps in increasing taxpayers’ tax compliance on PMSE transactions by increasing voluntary compliance.

4. Conclusions

Technological developments and globalization have provided business opportunities for digital business actors, both foreign traders, foreign service providers, foreign and domestic PMSE operators, to gain significant profits. The government took a strategic step by implementing the law and its derivative regulations for the taxation of PMSE. Tax policy must comply with all taxation principles. PMSE business actors who have attained certain criteria with a significant economic presence through the value of transactions with buyers and or service recipients that exceed a certain amount, and or the amount of traffic or access exceeds a certain amount will be subjected to PMSE tax.

The PMSE tax imposed by the government in the form of VAT is intended to fulfill the principle of justice in the form of equality in taxation between conventional business actors and digital economy business actors both at home and abroad. However, the VAT burden is a burden borne by Indonesian consumers and will be credited with input tax. The government must impose taxes on the PMSE actors, the imposition of income tax needs to pay attention to the applicable international tax regulations (tax treaty) to avoid double taxation, so it is necessary to consider the use of special taxes for the income of PMSE business actors apart from income taxes in general. The government needs to be careful in calculating the PMSE tax base and cover all digital business models. It is necessary to consider prioritizing potential business actors who can make a significant contribution to state revenues. The Ministry must cooperate with other Ministries and Institutions in implementing digital transaction taxation regulations in order to obtain optimal tax revenues. Policies must be supported by good administration in order to reduce tax compliance costs from the side of digital businesses and the government in an effort to collect taxes. Appropriate strategies and steps are needed to improve voluntary tax compliance.

Finally, learning from countries in the world, especially from European countries, the government must apply temporary tariffs for digital transactions while waiting for the global consensus initiated by the OECD to be reached. This policy is very important to avoid the potential loss of state tax revenue from large digital transactions.

Author Contributions

Conceptualization and Analysis, S.A.; methodology and draft preparation, A.H. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Geringer, S. National Digital Taxes—Lessons from Europe. S. Af. J. Account. Res. 2021, 35, 1–19. [Google Scholar] [CrossRef] [Green Version]

- Qin, Y.; Wang, X.; Xu, Z.; Skare, M. The Effects of Globalization on Family Firms’ Business Model in Europe. Int. J. Entrep. Behav. Res. 2022; ahead of print. [Google Scholar] [CrossRef]

- Brynjolfsson, E.; Kahin, B. Understanding the Digital Economy: Data, Tools, and Research; MIT Press: Cambridge, MA, USA, 2002; ISBN 0262523302. [Google Scholar]

- Iyer, L.S.; Taube, L.; Raquet, J. Global E-Commerce: Rationale, Digital Divide, and Strategies to Bridge the Divide. J. Glob. Inf. Technol. Manag. 2002, 5, 43–68. [Google Scholar] [CrossRef]

- Deloitte. Realising the Potential of Indonesia’s Digital Economy; Deloitte: Jakarta, Indonesia, 2021. [Google Scholar]

- Okah-Avae, T.O.; Mukoro, B. Constructing a Tax Regime for the Regulation of Trade in Digital Content. J. Int. Trade Law Policy 2020, 19, 121–138. [Google Scholar] [CrossRef]

- Tambunan, M.R.U.D.; Rosdiana, H. Indonesia Tax Authority Measure on Facing the Challenge in Taxing Digital Economy. Int. Technol. Manag. Rev. 2020, 9, 1–10. [Google Scholar] [CrossRef] [Green Version]

- Grinberg, I. International Taxation in an Era of Digital Disruption: Analyzing the Current Debate. Int. Tax J. 2019, 97, 73–104. [Google Scholar] [CrossRef] [Green Version]

- OECD. Statement on a Two-Pillar Solution to Address the Tax Challenges Arising from the Digitalisation of the Economy; OECD: Paris, France, 2021. [Google Scholar]

- Bunn, D.; Asen, E.; Enache, C. Digital Taxation Around the World; Tax Foundation: Washington, DC, USA, 2020. [Google Scholar]

- Heady, C. Optimal Taxation as a Guide to Tax Policy: A Survey. Fisc. Stud. 1993, 14, 15–41. [Google Scholar] [CrossRef]

- Udomvitid, K. The e-Commerce Sales Tax: A Case Study of Thailand; Colorado State University PP-United States—Colorado: Ann Arbor, MI, USA, 2003. [Google Scholar]

- Rosdiana, H. Pengantar Ilmu Pajak: Kebijakan Dan Implementasi Di Indonesia; Rajawali Pers: Jakarta, Indonesia, 2018. [Google Scholar]

- Agrawal, D.R.; Fox, W.F. Taxes in an E-Commerce Generation. Int. Tax Public Financ. 2017, 24, 903–926. [Google Scholar] [CrossRef] [Green Version]

- Bacache Beauvallet, M. Tax Competition, Tax Coordination, and e-Commerce. J. Public Econ. Theory 2018, 20, 100–117. [Google Scholar] [CrossRef]

- HMRC. 2020; Policy paper; Digital Services Tax. Available online: https://www.gov.uk/government/publications/introduction-of-the-digi-tal-services-tax/digital-services-tax (accessed on 17 October 2022).

Figure 1.

Percentage of Ecommerce Adoption (Source: We Are Social (2022), selected countries).

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Aulia, S.; Hambali, A. Digital Service Tax: Lessons Learned. Proceedings 2022, 83, 7. https://doi.org/10.3390/proceedings2022083007

AMA Style

Aulia S, Hambali A. Digital Service Tax: Lessons Learned. Proceedings. 2022; 83(1):7. https://doi.org/10.3390/proceedings2022083007

Chicago/Turabian StyleAulia, Sandra, and Ahmad Hambali. 2022. "Digital Service Tax: Lessons Learned" Proceedings 83, no. 1: 7. https://doi.org/10.3390/proceedings2022083007