Literature Study of The Influence of Big Data and Data Analytic on Cost Controls †

Accounting Study Program, Program Pendidikan Vokasi, Universitas Indonesia, Depok 16424, Indonesia

†

Presented at the 5th International Conference on Vocational Education Applied Science and Technology 2022, Teluk Betung, Indonesia, 26–28 October 2022.

Proceedings 2022, 83(1), 52; https://doi.org/10.3390/proceedings2022083052

Published: 12 January 2023

(This article belongs to the Proceedings of The 5th International Conference on Vocational Education Applied Science and Technology 2022)

Abstract

:Cost control is very important for companies in the era of big data because the cost is the main factor affecting a company’s competitiveness. This study aims to examine the impact of big data and data analytics on cost control in companies. This qualitative research uses the literature review method to better understand the influence of big data and data analytics (BDA) on cost control in the company. The results of the study revealed that, with the rapid development of information technology, the integration between data analytics and big data can effectively increase the competitiveness of the company’s market.

1. Introduction

The rapid development of information and communication technology makes the use of mobile devices, such as smartphones, palmtops, tablets, iPads and so on, also increase. The use of these devices generates data in the form of text, images, photos or videos that are increasing in number from day to day. This increasingly large data cannot be handled with conventional devices; instead, it must use big data [1]. Big data is a massive dataset that has a large, more varied, and complex structure with difficulties to store, analyze, and visualize for further processing or results [2]. Big data can be used for things related to information technology and business, including the use of mobile devices, social media, media digitization, application of CRM (customer relationship management), and so on.

Economic globalization that occurs in the world causes the frequency of data exchange between companies to increase significantly. Large amounts of data need to be analyzed in order to produce the right development goals and achieve stable company growth. Big data analysis is the application of computer technology to view large amounts of data using visualization software that helps humans see patterns, trends, exceptions, and anomalies. Big data analysis is also used in real-time to make decisions [3,4].

Economic globalization makes competition between companies more stringent. Companies must be able to compete to maintain their survival by innovating, creating quality products, being responsive to customer needs and following ongoing trends. Business competition makes companies become more concerned with controlling costs that occur in their respective companies [5].

In this era of big data, cost control of companies is very important, as costs are still the main factor affecting the company’s competitiveness [3]. Every company has a goal to reduce costs and increase efficiency, as well as maximize profits. Control over costs that are carried out affects the success of achieving the desired profit of the company [6]. Cost control is how management takes action in directing the activities being carried out so that they run according to the goals that have been set.

The company’s cost control is carried out by analyzing the occurrence of costs and the mechanism of cost formation so that it can find important factors that affect costs, and then control and manage these factors by finding the difference between actual costs and standard costs and taking effective steps to manage so that actual costs can be controlled within a predetermined range. Cost control runs through the entire process and all aspects of the company’s production and operations, and requires all employees to participate [7].

The aim of this study is to examine the impact of big data and big data analytics on corporate cost control. The focus of this study is to answer questions about how companies’ cost management has been impacted by big data and big data analytics. A fundamental question is how BDA affects cost control. What opportunities does big data present for cost control? What are the risks of using big data and big data analytics to control costs? This paper discusses the sources of big data for cost management, the impact of big data analytics on cost management, and the use of big data analytics for cost management decisions.

2. Literature Review

2.1. Big Data

Big data is a massive dataset with a large, more varied, and complex structure with difficulties storing, analyzing and visualizing for further processing or results [1]. Big data is also defined as data that exceeds the processing capacity of existing conventional database systems. The data has a very large size and has a very fast speed or does not match the existing database’s architecture structure. To get the value from the data, an alternative way of processing it must be chosen [8]. The size, variety, and rapid change of that data require new types of big data analysis, as well as different methods of storage and analysis. Such large amounts of data need to be properly analyzed, and related information must be extracted.

In companies, big data will be utilized, among others, for narrower or more specific customer segmentation so that products or services are designed more precisely. Data analytics can improve decision making and big data can be used to enhance the development of next-generation products and services, using big data as the main basis for competition and growth for individual companies, as well as to support a new wave of productivity growth and consumer surplus [9]. Big data also has a role in increasing the understanding of financial market mechanisms for the general public [10].

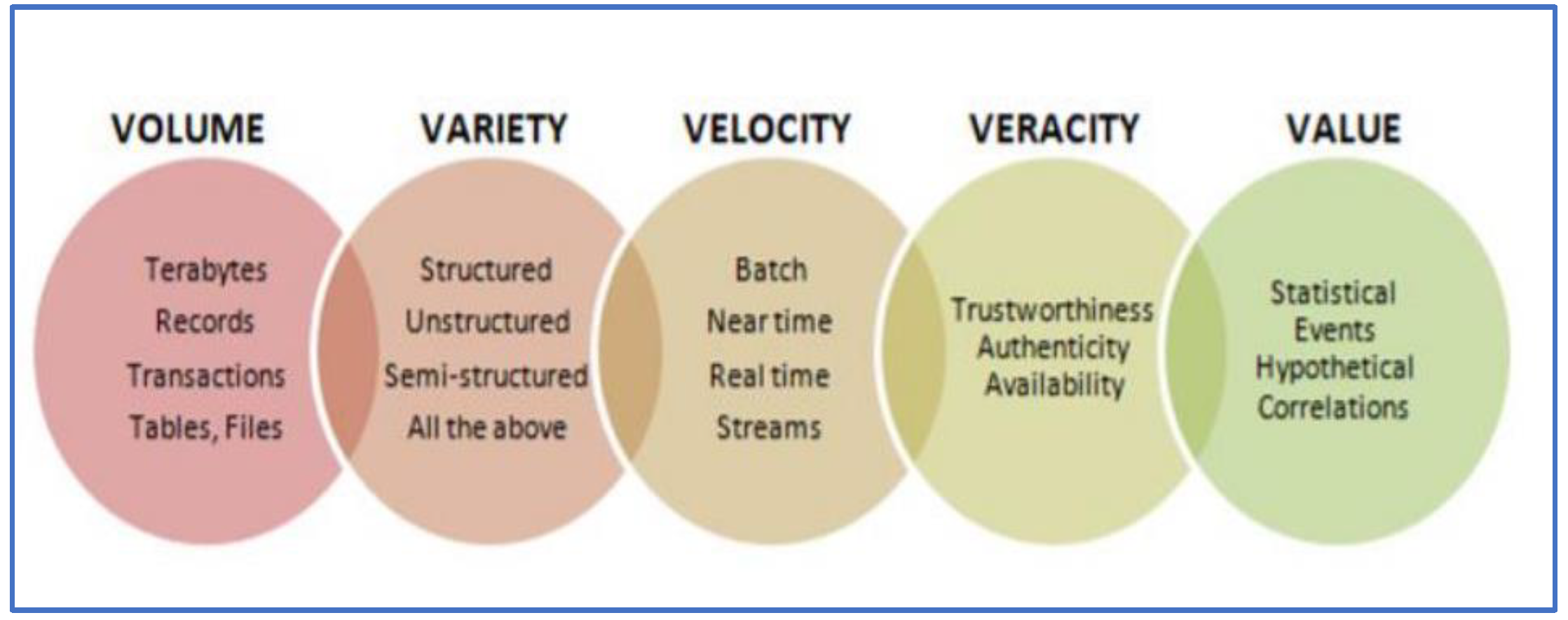

- Volume is a very large and sometimes unstructured collection of data. Files of data are generally very large, reaching terabytes to petabytes.

- Velocity is a very high speed of data reception and processing.

- Variety is the types or forms of data available. If traditional data is generally structured and easy to analyze, big data is generally unstructured and comes from various sources; therefore, it needs to be processed first before being analyzed.

- Veracity is the accuracy of the data, whether it can be trusted or not.

- Value is the level of value, price, or meaning of data.

The larger/higher the volume, variation, speed, level of truth, and value of the existing data, the more feasible it is that the data is categorized as big data.

2.2. Big Data Analytics (BDA)

BDA is defined as a holistic approach to managing, processing, and analyzing the dimensions of big data (characteristics of big data) related to 5V data, namely volume, velocity, variety, veracity, and value.

Cloud computing and storage capabilities that can perform data capture, storage, sharing, and processing regardless of size and complexity enable the use of big data. This causes large amounts of data with various models, programs and technologies to be utilized for in-depth analysis so that decision-makers derive value from the analysis carried out [12].

This is in accordance with the research conducted by Bhimani and Wilcox, which stated that big data analytics related to cloud computing applications are stored in large databases. The cost of using data for decision-making is low. Research indicates that big data analytics apply computational techniques to visualize large amounts of data using visualization software that helps to clearly spot patterns, trends, and anomalies. New insights about data can be gained using data analysis tools. Data analytics also makes it easier for businesses to analyze and use real-time data to make decisions. Businesses’ decisions are facilitated by data analytics, which analyzes and uses real-time data [13].

2.3. Cost Control

Cost control is the process of controlling direct activities so that they do not deviate from predetermined objectives. Cost control can be done through cost budgeting, which is continuously monitored to analyze the deviations, know the causes of the deviations and then follow up to eliminate the resulting losses [14]. Cost control involves the entire process and all aspects of a company’s production and operations, as well as all employees [7]. Cost control has a positive impact on organizational performance. To be successful, the organization must implement cost management and cost-saving systems in its operations, and employees must be engaged and motivated to achieve the desired goals and objectives [15]. Cost control in a project includes cost planning, cost analysis, cost control, and accounting. Appropriate measures must be taken to control costs to an acceptable level, and economical and technical measures must be implemented to realize the potential costs and reduce project costs [16]. Organizations find benefits from business processes by reducing costs, making better operational plans, reducing inventory, utilizing the best people in the organization, and eliminating unnecessary resources, which also increases operational efficiency [17]. Cost control also has a positive impact on the organization and its cost components, such as material, wages, and overhead costs, as well as strategically controlled employee behavior through measures such as proper budgeting standard costing, and responsibility accounting [18].

3. Research Methodology

In this study, the method used was a literature study to gain a better understanding of the research being conducted. This literature review seeks to provide an overview and evaluation of the impact of big data and big data analytics on controlling company costs in various types of industries. The literature study was carried out by analyzing content from various research journals and other scientific references which discuss the influence of BDA on cost control, using Google Scholar in the 2015–2022 period. The keyword or keywords used are as follows: “big data” AND “cost control” OR (“big data analytic” and “cost control”) OR (“big data and data analytic” AND “cost control”).

4. Results and Discussion

As explained in the previous section, this research is a literature study that discusses the results of several studies on the effect of BDA on cost control. There are only seven scientific papers used for discussion, which have been published in 2015–2022, because there is still very little research on this topic. The results of the observations of these scientific studies are shown in Table 1 below.

4.1. Impact of Big Data and Big Data Analytics on Enterprise Cost Control

The impact or influence of big data and data analytics on cost control has been carried out by several researchers and the observations of several research articles on this matter can be seen in Table 1 above. Several studies that have been conducted obtained different results.

The study conducted by Yunsong Gu indicates that an important method of reducing the cost of recycling is to increase the production and culture process per unit. The analysis shows that this method is highly sustainable in controlling the cost of marine water and increasing the profit level of the business. The use of BDA to control costs is in accordance with several other studies, as shown in Table 1 above [20,21,22].

Other impacts or influences of implementing big data technology for enterprise costs apply both to the company’s internal planning and to the company’s external planning. Therefore, big data technology will be one of the most useful methods to comprehensively improve the strength of a business entity, strengthen corporate project cost management to effectively improve corporate economic efficiency and promote long-term development [3,24], and reduce costs [22]. Research on the impact of big data analytics on real estate companies suggests that controlling costs is critical. Companies must have competitiveness in order to compete competitively: cost control systems need to be improved, information technology needs to be applied, cost accounting methods and cost control assessments need to be improved, and an effective accountability system needs to be implemented in order to promote sustainable real estate development [22].

4.2. Importance of Big Data Analytics in Cost Control

Big data analytics help companies in controlling costs. By performing and using data visualization, large amounts of data can be assessed for patterns, trends, exceptions, and outliers, so that decision-making can be better. The company can obtain the possibility of better acceptable results and analyze a large amount of information in order to make better decisions. Companies can focus on recognizing trends to gain a competitive advantage and seize opportunities from the data they have. Many illustrations of business evaluations can be carried out, which lead to the best business decisions. Risks that may arise in the business can be detected early [16]. A company can continue to monitor all costs incurred and compare them with the targets that have been set.

Apart from the positive benefits and opportunities of using big data and big data analytics in controlling corporate costs, there are also risks [17]. These risks are:

- Security risk. Almost all organizations control sensitive information, such as information about customers. This information requires strict protection from being leaked and thus allowing potential cyber-attacks.

- Questionable data quality. Not all data can be analyzed; therefore, data scientists need a more rigorous analytical system in order to gain insight from significant and accurate data.

- Quality of big data analytics. Big data is used to make decisions. If the people who use it do not possess good data processing and analyzing skills, the decisions made are not good for the company.

5. Conclusions

This study found that big data and big data analytics help companies control costs by analyzing cost data, comparing actual and target costs, and making business decisions regarding cost control.

Companies can focus on recognizing trends to gain a competitive advantage and opportunities from the data they have. Many illustrations of business evaluations can be carried out that lead to the best business decisions. Risks that may arise in the business can be detected early.

There are several risks from using big data and big data analytics, including security risks to the data held, questionable data quality, and the quality of big data analytics.

Big data and big data analytics for enterprise cost control are more effective when combined with large databases and cloud service applications. This allows one to gather more information and leverage different types of data from multiple sources to identify specific cost control opportunities in order to generate new insights, manage risks and predict future outcomes.

Funding

This research was funded by Program Pendidikan Vokasi, Universitas Indonesia.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data used to support the findings of this study are included within the article.

Conflicts of Interest

The author declares no conflict of interest.

References

- What is Big Data? Available online: https://www.oracle.com/in/big-data/what-is-big-data/ (accessed on 23 October 2022).

- Sagiroglu, S.; Sinanc, D. Big Data: A Review. In Proceedings of the International Conference on Collaboration Technologies and Systems (CTS), San Diego, CA, USA, 20–24 May 2013. [Google Scholar]

- Xu, Z.; Ji, X.; Wang, J.; Guo, T. Analysis of The Influence of Big Data on The Cost Control of Tianbao Green Food Company. In Proceedings of the 2020 International Conference on Energy Big Data and Low-Carbon Development Management (EBLDM 2020), Nanjing, China, 18–20 December 2020; Volume 214. [Google Scholar] [CrossRef]

- Herath, S.K.; Woods, D. Impacts of Big Data on Accounting. Bus. Manag. Rev. 2021, 12, 195–203. [Google Scholar] [CrossRef]

- Li, K. Research on the Application of Management Accounting Tools in Enterprise Cost Control. In Proceedings of the International Conference on Information Economy, Data Modeling and Cloud Computing, Qingdao, China, 17–19 June 2022. [Google Scholar]

- Ardiani, N.M.S.; Wirasedana, I.W.P. Pengaruh Penerapan Akuntansi Pertanggungjawaban terhadap Efektivitas Pengendalian Biaya. E-J. Akunt. Univ. Udayana 2013, 5, 561–573. [Google Scholar]

- Nartey, E.; Aboagye-Otchere, F.K.; Simpson, S. The contingency effects of supply chain integration on management control system design and operational performance of hospitals in Ghana. J. Account. Emerg. Econ. 2020; ahead-of-print. [Google Scholar]

- Dumbill, E. Big Data Now Current Perspective. O’Reilly Media 2012, 47, 98–115. [Google Scholar]

- Big Data: The Next Frontier for Innovation, Competition, and Productivity. Available online: https://www.mckinsey.com/business-functions/mckinsey-digital/our-insights/big-data the-next-frontier-for-innovation (accessed on 23 October 2022).

- Shen, D.; Chen, S.-H. Big Data finance and financial markets. In Big Data in Computational Social Science and Humanities; Springer: Berlin/Heidelberg, Germany, 2018; pp. 235–248. [Google Scholar]

- Smaya, H. The Influence of Big Data Analytics in the Industry. Open Access Libr. J. 2022, 9, e8383. [Google Scholar] [CrossRef]

- Cockcroft, S.; Russell, M. Big data opportunities for accounting and finance practice and research. Aust. Account. Rev. 2018, 28, 323–333. [Google Scholar] [CrossRef]

- Bhimani, A.; Willcocks, L. Digitisation,‘ Big Data and the transformation of accounting Information’. Account. Bus. Res. 2014, 44, 469–490. [Google Scholar] [CrossRef]

- Trisnawati, S. Hubungan antara Penerapan Akuntansi Pertanggungjawaban Dengan Efektivitas Pengendalian Biaya (Survei Pada 5 Hotel diKota Tasikmalaya). Bachelor Thesis, Universitas Islam Indonesia, Yogyakarta, Indonesia, 2006. [Google Scholar]

- Lawal, B.A. Effect of Cost Control and Cost Reduction Techniques in Organizational Performance. Int. Bus. Manag. 2017, 14, 19–26. [Google Scholar] [CrossRef]

- Chen, L.; Dai, H. Application of Big Data Technology in Cost Management and Control in Construction Project. J. Phys. Conf. Ser. 2021, 1881, 022036. [Google Scholar] [CrossRef]

- Alsghaier, H.; Akour, M.; Shehabat, I.; Aldiabat, S. The Impact of Big Data Analytics on Business Competitiveness. In Proceedings of the New Trends in Information Technology (NTIT-2017), Amman, Jordan, 25–27 April 2017. [Google Scholar]

- Mutya, T. Cost Control: A Fundamental Tool towards Organisation Performance. J. Account. Mark. 2018, 7. [Google Scholar] [CrossRef]

- Gu, Yunsong. Application of Big Data Analysis in Cost Control of Marine Fishery Breeding. Discret. Dyn. Nat. Soc. 2022, 2022. [Google Scholar] [CrossRef]

- Irsyadillah, I.; Indriani, M.; Oktari, R.S. DRG-Based Payment System and Management Accounting Changes in an Indonesian Public Hospital: Exploring Potential Roles of Big Data Analytics. J. Account. Organ. Chang. 2022, 18, 325. [Google Scholar]

- Yu, X.; Zuo, H. Research on Construction Cost Control Technology of Construction Project Based on Big Data Analysis Theory. Mob. Inf. Syst. 2022, 2022. [Google Scholar] [CrossRef]

- Zhang, Y. Cost Control of Real Estate Companies in the Era of Big Data. Int. J. Front. Sociol. 2021, 3, 114–117. [Google Scholar] [CrossRef]

- Mao, H.; Chen, L. E-Commerce Enterprise Supply Chain Cost Control under the Background of Big Data. Complexity 2021, 2021. [Google Scholar] [CrossRef]

- Peng, Y.; Ding, Y.; Yu, Y. Grid Project Cost Control Research Based on Data Mining. In Proceedings of the International Conference on Advanced Material Science and Environmental Engineering (AMSEE 2016), Chiang Mai, Thailand, 26–27 June 2016. [Google Scholar]

Figure 1.

5 Dimensions of big data [11].

Figure 1.

5 Dimensions of big data [11].

{kind=link}

Table 1.

Observation results of the study of the effect of BDA on cost control.

| Author (Year) | Title | Results and Findings |

|---|---|---|

| Gu, Yunsong (2022) [19] | Application of Big Data Analysis in Cost Control of Marine Fishery Breeding | The results of the study (using BDA) indicate that the major method of reducing the cost of recycling is by increasing the production and culture process per unit. The analysis shows that this method is highly sustainable in controlling the cost of marine water and increasing the profit level of the business. |

| Irsyadillah, I., Indriani, M., and Oktari, R.S. (2022) [20] | DRG-Based Payment System and Management Accounting Changes in an Indonesian Public Hospital: Exploring Potential Roles of Big Data Analytics | The results of this study reveal the feasibility of developing case-mix accounting in hospitals and other potential benefits of using BDA simulations. The application of BDA and case-mix accounting in hospitals has the potential to become a catalyst for discussion and mutual learning between managerial and medical staff in controlling patient costs. The regression model shows that LOS (length of stay) is not the only determinant of CRR because the patient’s severity (SEV) and patient age (AGE) also have a significant effect on the CRR of hospitalized cases. Mathematical models can be used to estimate patient costs at the time of admission, as well as evaluate the services provided. |

| Yu, Xiaobing, Zuo, Hengzhong (2022) [21] | Research on Construction Cost Control Technology of Construction Project Based on Big Data Analysis Theory | Based on the characteristics and principles of construction cost control, the two main effects of the theory of big data analysis on construction cost control are proposed: direct and indirect costs and various reasons for construction cost control. Based on this, a system of evaluation indicators was created for controlling the construction costs of construction projects. The accuracy of construction cost management indicators based on big data theory is higher than that of the traditional analytical hierarchy process. |

| Zhang, Y. (2021) [22] | Cost Control of Real Estate Companies in the Era of Big Data | The result shows that for real estate companies, cost control is very important. In the context of big data, in order to compete in the competitive market, real estate companies must have competitiveness, strengthen awareness of cost control, improve cost control systems, apply information technology, improve cost accounting methods, improve cost control assessments, and implement effective accountability systems in order to realize the sustainable development of the real estate. |

| Mao, Haijun, Chen, and Long (2021) [23] | E-Commerce Enterprise Supply Chain Cost Control under the Background of Big Data | This study concludes that many cost control problems can be solved effectively by using big data technology so that it can continue to drive the progress of company management and reduce costs. |

| Xu, Zhou, Ji, Xiaoli, Wang, Junfeng, Guo, Tianyu (2020) [3] | Analysis of The Influence of Big Data on The Cost Control of Tianbao Green Food Company | The results of the study show that the implementation of big data technology for enterprise costs applies both to the company’s internal planning and to the company’s external planning. Therefore, big data technology will be one of the most useful methods to comprehensively improve the strength of a business entity. |

| Peng, Yan, Ding, Yang, Yu, Yuanmei (2016) [24] | Grid Project Cost Control Research Based on Data Mining | The results show that project cost management is an important part of cost management. Strengthen enterprise project cost management to effectively improve the economic efficiency of the enterprise and promote long-term development. Construction project costs: there are still many questions about cost management, especially for high-investment companies such as grid enterprises. One needs to take steps to properly control costs and increase efficiency. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Wahyuni, T. Literature Study of The Influence of Big Data and Data Analytic on Cost Controls. Proceedings 2022, 83, 52. https://doi.org/10.3390/proceedings2022083052

AMA Style

Wahyuni T. Literature Study of The Influence of Big Data and Data Analytic on Cost Controls. Proceedings. 2022; 83(1):52. https://doi.org/10.3390/proceedings2022083052

Chicago/Turabian StyleWahyuni, Titis. 2022. "Literature Study of The Influence of Big Data and Data Analytic on Cost Controls" Proceedings 83, no. 1: 52. https://doi.org/10.3390/proceedings2022083052