1. Introduction

In this paper, we are interested in the effective numerical schemes for the following time-fractional Black–Scholes (B-S) equation governing European options [

1]:

with the boundary conditions

and terminal condition

. Here,

denotes the price of a European-style double-barrier option with

S being the asset price and

t being the current time. The parameter

is the volatility of the returns,

r is the risk-free interest rate, and

D is the dividend rate. The fractional operator

with the fractional order

is defined by

The functions

P and

Q in the boundary condition are the rebates paid when the corresponding barrier is hit and the function

H in the terminal condition is the payoff function.

The time-fractional B-S model (

1) is derived by assuming that the change in the option price with time is a fractal transmission system. Some scholars have made some achievements in the study of this model or related field; see [

1,

2,

3,

4], just to name a few.

Since the analytical solution of the time-fractional B-S model (

1) is difficult to obtain, we need to resort to numerical methods to better investigate the dynamical behavior of this model. Some efforts on the study of numerical methods have been made so far; see [

5,

6,

7] and the references therein. In [

5], Zhang et al. constructed a discrete implicit difference scheme with accuracy of

, where

and

h are the temporal step size and spatial step size, respectively. Later on, De Staelen and Hendy improved Zhang et al.’s results by proposing a finite difference scheme of spatial fourth-order accuracy while keeping temporal

order accuracy [

6]. Different from the above mentioned central difference method or compact difference method for discretization in space, Roul utilized the collocation method based on quintic B-spline basis functions for spatial discretization and the backward Euler method for temporal discretiztion [

7]. The resulting numerical scheme was shown to be stable with accuracy of

.

It is noted that both theoretical and numerical tests of the above mentioned numerical schemes are discussed under the solution of the time-fractional B-S equation is sufficiently smooth. Generally speaking, the solution of the time-fractional model (

1) has weak singularity near

due to the non-smooth payoff function, which would have certain impact on the accuracy of the derived numerical scheme. This is already a common fact in the fractional community; see the two review papers [

8,

9] or the book [

10] for more discussion of the related topic. One of the most common and effective ways of dealing with the insufficiently smooth solution of time-fractional models is the use of non-uniform meshes; e.g., see [

11,

12,

13,

14].

In [

15], Cen et al. transformed the time-fractional B-S equation into an equivalent integral-differential equation and proposed a finite difference scheme on a temporal adapted mesh. Although the proposed temporal non-uniform meshes-based finite difference scheme takes into account the possible singularity behavior of the analytic solution near

, it has only first-order and second-order accuracy in time and in space, respectively. Similarly, based on the equivalent integral differential equation, Kazmi developed a finite difference scheme with second-order accuracy in both space and time [

16]. The author obtained asymptotic error expansions for numerical solutions of non-smooth problems based on the observation of numerical results and employed the Richardson extrapolation technique to improve the accuracy of the numerical scheme. In [

17], Song and Lyu constructed an efficient finite difference scheme by employing the non-uniform Alikhanov formula. It can be seen that there is some room for improvement in the efficient numerical scheme for time-fractional B-S equation, especially for non-smooth solution problems.

Motivated by the ideas in Li et al. [

11], we develop the efficient finite difference schemes with temporal uniform/non-uniform meshes for solving the time-fractional B-S Equation (

1). More precisely, we first transform the original equation into an equivalent integral-differential equation with a weakly singular kernel and then use the piecewise linear interpolation function to discretize the time integral terms in the equivalent form and use the compact difference method to discretize the spatial direction. Thus, we finally obtain the fully discrete compact difference schemes.

The main contributions of this paper are listed as follows: First, we propose the compact difference schemes with temporal uniform/non-uniform meshes. The derived schemes handle well the effect of the non-smooth payoff function in (

1) and can be easily implemented on the computer. Second, based on Fourier analysis, we provide rigorous proofs of the stability and convergence of the uniform meshes-based compact difference scheme and extend to the theoretical analysis of the temporal non-uniform mesh-based compact difference scheme. Third, we present extensive numerical tests, including comparisons with other existing finite difference schemes, particularly the two schemes presented in [

16,

18], for smooth/non-smooth solution problems to illustrate the advantages of our schemes.

The rest of the paper is organized as follows. The uniform mesh-based compact difference scheme is derived in the next section. Stability and error estimate of the derived numerical scheme are provided in

Section 3. In

Section 4, we extend the results based on the uniform meshes to the non-uniform mesh case and derive the temporal non-uniform mesh-based compact difference scheme and give the corresponding numerical theoretical results. In

Section 5, extensive numerical examples are presented to demonstrate the performance of the derived schemes. Finally, the conclusions are given in

Section 6.

2. The Derivation of the Scheme

For the convenience of numerical solution, we transform the original Equation (

1) into another equivalent form with the help of variable substitution. That is, we set

and denote

and

. After some routine calculations for (

1), one can obtain

which leads to the following equivalent form:

Here,

and

. The Caputo derivative

is defined by

Thus, without loss of generality, we consider the following time-fractional problem:

with the boundary conditions

, and the initial condition

. Here,

is a suitable smooth function and

Remark 1. It is worth noting that the forms of the functions , and h in the boundary and initial conditions of (2) will vary depending on the pricing model. For example, for the European put option, we let and , with K being the strike price of the option. One may refer to [16] or [1] for more discussions. We first introduce some useful notations. For positive integers and , let the spatial step size and temporal step size be and , respectively. The discrete grids in space are given by with the grid points . Let the grid points in time be . Let be a grid function defined on . We define spatial difference operators and .

It is known that the Equation (

2) is equivalent to the Volterra integro-differential equation:

Considering the above Equation (

4) at the grid point

, we have

where

and

.

Suppose that

. Applying the piecewise linear interpolation on each sub-interval

to approximate the integrand

, one has

So, it follows from (

5) that

where the weights are given by

with

, and the truncation error term

.

Next, we consider the compact difference method to obtain the fully discrete numerical scheme for (

6). To this end, we begin with the compact difference method for the following steady state equation:

where

is a suitable smooth function.

Utilizing the Taylor expansion, one can derive the fourth-order compact finite difference scheme to solve Equation (

8) (see Theorem 1 in [

18]), that is,

where

Noting the definition of

in (

6) and so combining Equations (

6) and (

9), one obtains

where

. Dropping the small term

, and replacing

with the approximate solution

, we obtain the following fully discrete compact difference scheme:

with

and

. The corresponding initial and boundary conditions are given by

and

To facilitate code implementation and theoretical analysis, we expand on the original compact difference scheme (

11) below. Observing that the

on the right-hand side of (

11) is unknown, moving it to the left-hand side and using the definitions of

, we obtain

To simplify the above equation, we set

Thus, after some trivial operations, we obtain

The above equations can be written in a more compact matrix-vector form. Denoted by

and

, one has the following matrix form for (

13):

where

. The matrices

,

, and

are all

tridiagonal matrices given by

with

and

. The column vector

with

entries is defined by

It can be readily seen that the compact difference scheme (

13) is uniquely solvable. Indeed, by the definitions of the parameters

and

r, one can observe that the inequality

holds when

and

h are both small. This implies that the coefficient matrix

in the matrix form of (

13) is strictly diagonally dominant and thus it is non-singular. Therefore, the unique solvability of (

13) follows.

4. Extension to the Non-Uniform Meshes

In general, the solution of the time-fractional model (

2) is not sufficiently smooth at the initial time due to the non-smooth initial condition

, and this will lead to an impact on the accuracy of the compact difference scheme (

11). In this section, motivated by the non-uniform mesh technique presented in [

11], we extend the compact difference scheme (

11) to the non-uniform meshes case in time to better deal with the weak singularity of the solution at

.

Set the grid point

with non-equidistant step size

. Here, we choose

, which is the same with that in [

11]. It can be easily seen that the variable step size

satisfies

. Similar to the uniform meshes case, we use the piecewise linear interpolation on each sub-interval

to approximate the integrand

in (

5):

where

.

Then we have the temporal non-uniform meshes-based compact difference scheme as follows.

in which

and

Below, we give a key property of the weights

, which plays important role in stability and error estimate for (

24). This property was mentioned in Lemma 3.1 of [

11], but no detailed proof was given; here we will provide its complete proof.

Lemma 3. If , for and , the weights in (24) have the following property.if , and if . Here, . Proof. We first consider the case and . In view of the definition of , one has .

Since

by utilizing the mean value theorem, we have

where

. It follows that

where

.

When

, we immediately have

Next, we present the proof for the case: and .

For

in the weight

, applying the mean value theorem once again, we have

where

.

For

, we similarly obtain

where

.

Noting that

one obtains

where

and

.

If

, we readily obtain

When

, we obtain

Thus, the proof is completed. □

From Lemma 3, we can see that

for

and

. This together with the Gronwall inequality (see Lemma 2) can lead to the stability and error analysis of the compact difference scheme (

24). Since the proof procedure is analogous to that of the uniform meshes case (see Theorems 1 and 2), we list the conclusions here and omit the detailed proof for the sake of simplicity.

Theorem 3. The temporal non-uniform mesh-based compact difference scheme (24) for numerically solving the problem (2) is unconditionally stable. Theorem 4. Let and be the solutions of compact difference scheme (24) and the Equation (2), respectively. Suppose that with , and for , we have the following error estimate:Specially, we havewhere . Proof. In view of the Lemma 4.3 in [

11] and (

9), we conclude that the truncation error in (

24) is

. So, similar to the proof of Theorem 2, one can obtain the desired result. □

5. Numerical Examples

In this section, we verify the stability and accuracy of the two compact difference schemes (

11) and (

24) derived in the previous sections with numerical examples. We mainly perform numerical tests for the two cases with known and unknown solutions. At the end of this section, we present numerical simulations using specific parameters in order to provide a more intuitive glimpse of the dynamical behavior of the time-fractional model (

1). All numerical tests here are implemented using the Julia language.

We first introduce the following three finite difference schemes.

- Scheme 1

For the equivalent Equation (

4): Using piecewise linear interpolation technique and central difference method in time and space [

16], respectively, one has

where the difference operator

is given by

.

- Scheme 2

For the origin Equation (

2): Using L1 formula and compact difference method in time and space [

18], respectively, one has

where

with

.

- Scheme 3

For the origin Equation (

2): Using L2-1

formula and compact difference method in time and space, respectively, one has

where

,

, and

. Here,

. The weights

in the difference operator

is defined by the following: For

, for

,

Here,

, and

We remark that the third finite difference scheme (

27) is slightly different from [

17] since we consider here only uniform meshes and without fast solver for the sake of discussion.

It can be seen these three stable finite difference schemes (

25)–(

27) have

,

, and

convergence accuracy if the solutions satisfy

,

, and

, respectively.

Example 1 (known solution).

Consider the problem (2) with the following data:and the source termThe exact solution is with the fixed parameters and . Here, the domain .

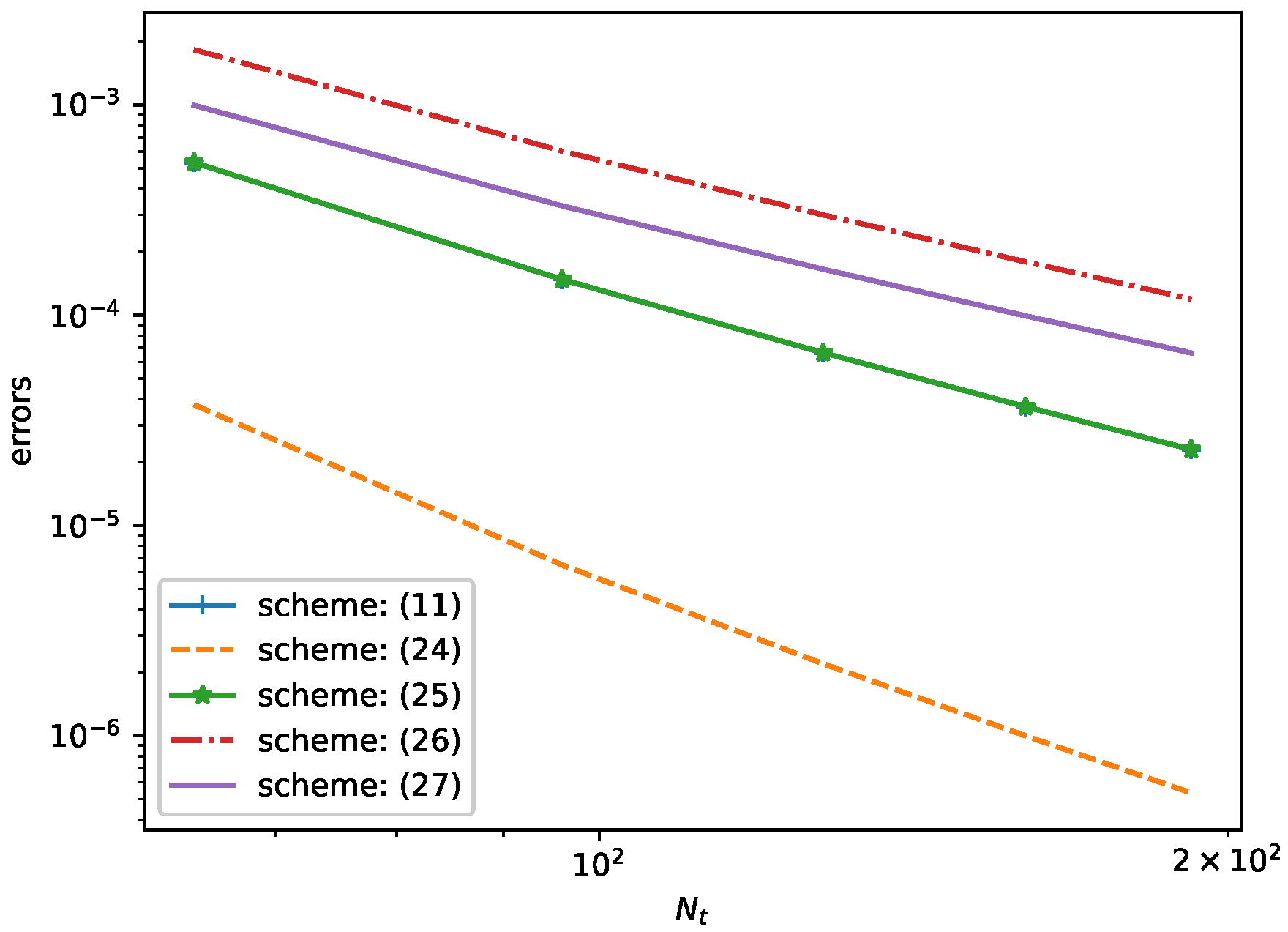

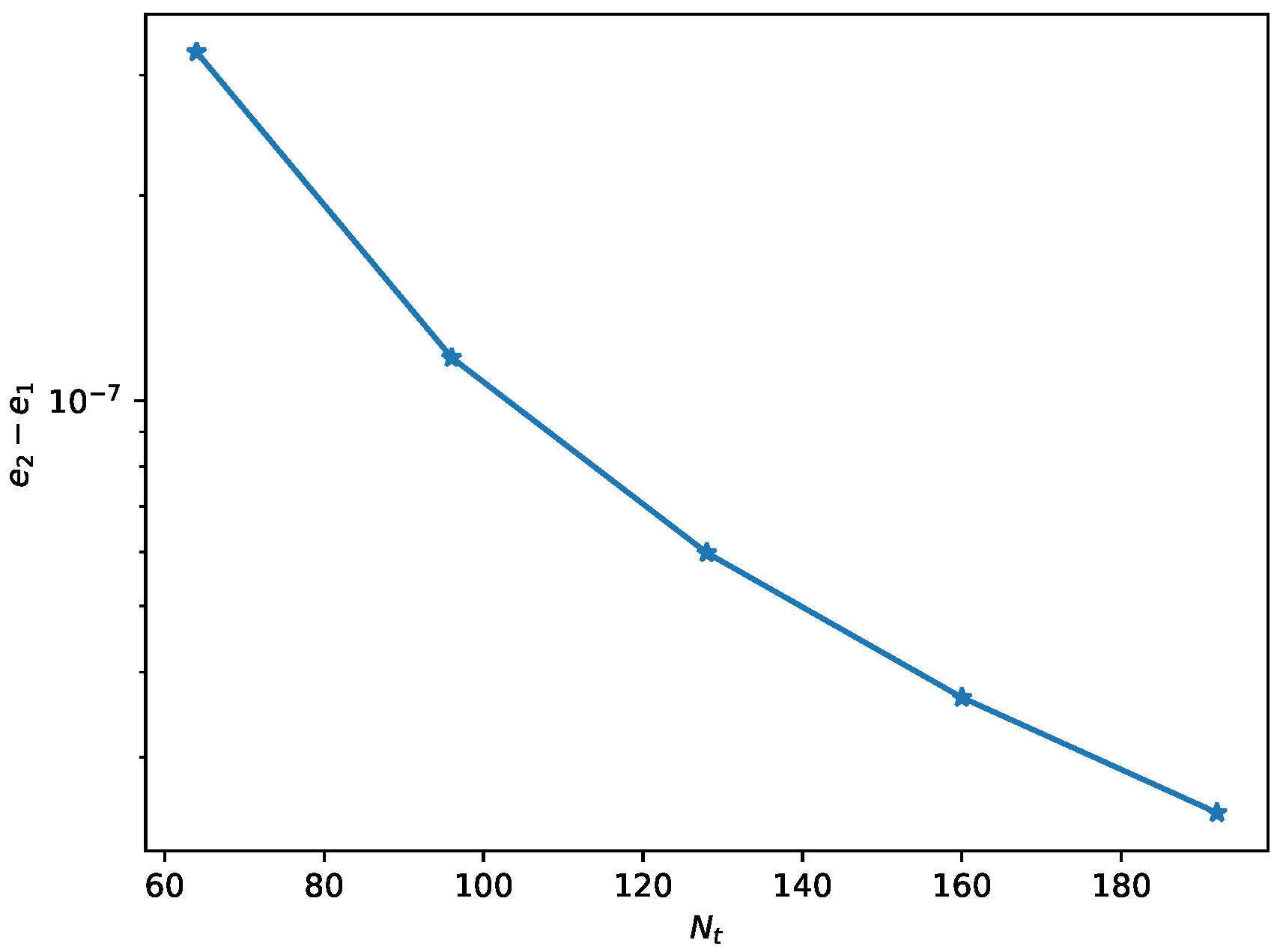

We first consider the smooth case of the above example, i.e., we set and . The errors of the numerical solution at in -norm are measured by . Unless otherwise noted, we always calculated the corresponding temporal and spatial convergence rates by and , respectively. Using the finite difference schemes (11), (25), and (26), one can obtain the numerical results in Table 1 and Table 2. Since the analytic solution u satisfies the smoothness requirement of the compact difference scheme (11), we can theoretically obtain that the scheme (11) has the accuracy of . It is worth noting that when testing the temporal convergence order of (25), the spatial errors contaminate the temporal accuracy as the spatial step size is not small enough. This leads us to not observe the corresponding theoretical temporal convergence order; see the results in the middle rows of Table 1. The similar situation occurs in the test of the spatial convergence order in (26); see the results in last rows of Table 2. One can reduce the corresponding step size so as to observe the theoretical convergence order, but this is not necessary for our scheme (11). The numerical results also illustrate that the accuracy of (11) is more superior to the other two schemes (25) and (26) with the same step sizes τ and h. Next, we consider the case and , i.e., the analytical solution is . Since the first-order partial derivative of the solution u in time does not exist at , we say that the solution is not sufficiently smooth in this case. By applying numerical schemes (11), (24), and (27), we obtain the corresponding numerical results in Table 3 and Table 4. From the data in Table 3 and Table 4, it can be observed that although both (11) and (27) are equally based on the uniform meshes, and the convergence accuracy of the former is higher than that of the latter. In addition, by using the temporal non-uniform meshes-based compact difference scheme (24), we effectively improve the convergence accuracy of the non-smooth solution problem. The numerical results indicate that the convergence orders of (24) in time and space at are two and four, respectively, which verifies the correctness of Theorem 4. Example 2 (unknown solution).

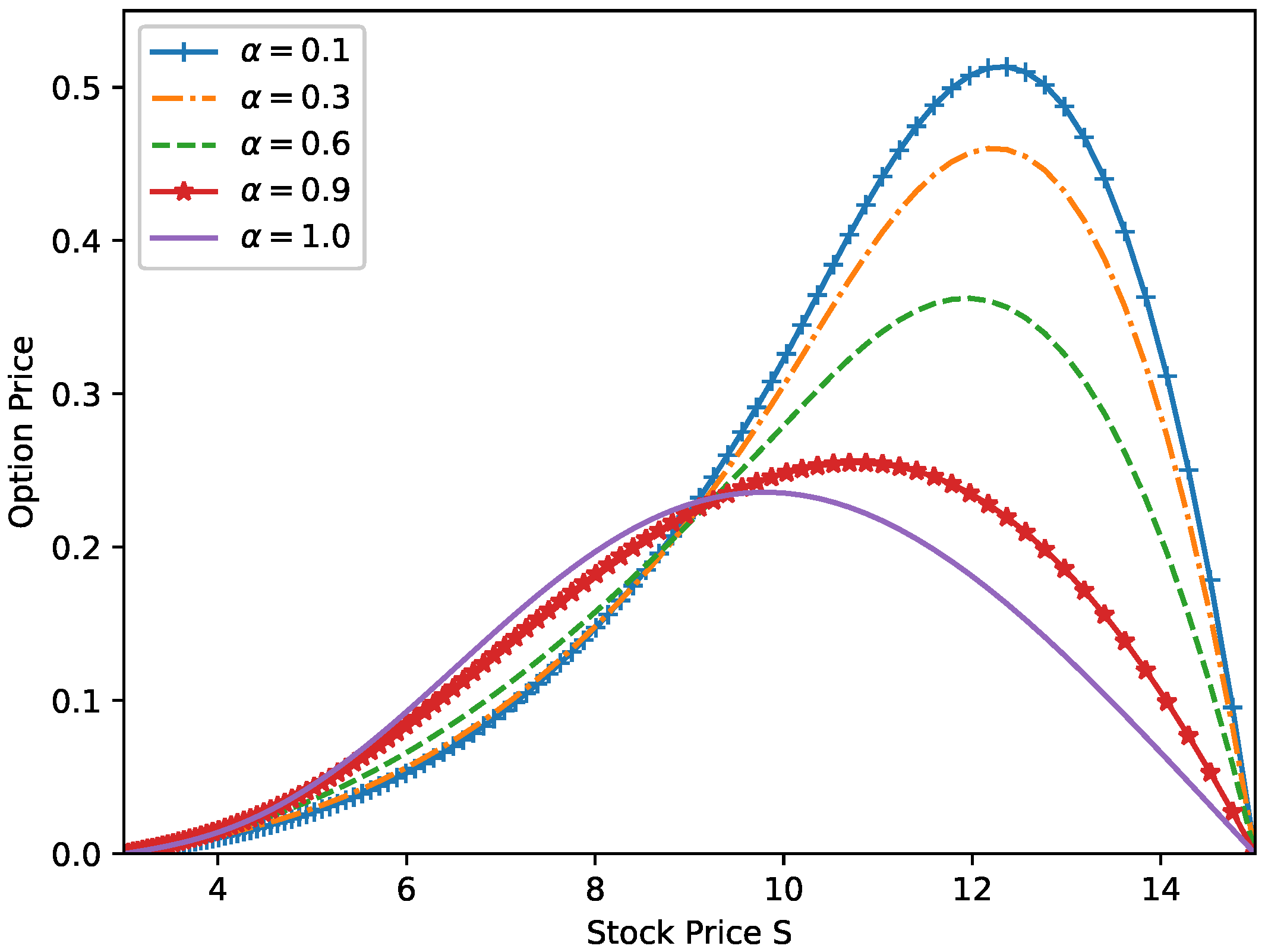

Consider the homogeneous case for the European put option problem (2) with the following data [16]:and the corresponding parameters are chosen as , , and . In this example, we focus on the temporal convergence order. Since the solution is unknown, the errors at are obtained by , and the corresponding temporal convergence rate is computed by . Here, the numbers of the spatial nodes will be taken to be large enough so that the spatial errors do not contaminate the temporal errors. Using the numerical schemes (11), (24), and (27), we obtain the numerical results in Table 5.Unlike the extrapolation technique used in [16] to improve the convergence accuracy, we here adopt the temporal non-uniform meshes. Numerical results in Table 5 show that the temporal non-uniform mesh-based compact difference scheme (24) can maintain the temporal second-order accuracy well, while the uniform mesh-based compact difference schemes (11) and (27) have only about and first-order accuracy, respectively. To further demonstrate the superiority of the temporal non-uniform mesh-based compact difference scheme (24) in handling non-smooth solution problems, we compare the -norm errors for the five finite difference schemes (11) and (24)–(27) by setting fixed and various . Let be the jth value of , e.g., . The numerical results with errors for the case are given in Figure 1. Since the errors of numerical schemes (11) and (25) in Figure 1 are very close to each other, in order to better observe their differences, we let and denote the errors of (11) and (25) respectively, and take their differences as the vertical coordinates of the axes; see Figure 2. As can be seen from Figure 1 and Figure 2, the accuracy of our schemes, particularly the temporal non-uniform mesh-based compact difference scheme (24), is much better than the other three schemes (25)–(27). Similar results are also obtained for the other fractional order α, which are not presented here for the sake of brevity. Remark 2. We remark that for the two non-smooth solution problems Example 2 and the second case of Example 1, the temporal convergence order of the compact difference scheme (11) is different, with Example 2 having the temporal convergence order of , while the second case of the previous example has almost in time (see the top lines in Table 3 and Table 5, respectively). Indeed, using the definition and properties of the Mittag–Leffler function (see, e.g., (1.3) in [19]), one can deduce that the solution in Example 2 has the estimate: For as . It follows that the temporal convergence order of (11) is in view of the error estimate (c) in Theorem 2.5 of [20]. However, the term in the second case of Example 1 has the following form: From the Equations (4) and (6), and reusing the error estimate (c) in Theorem 2.5 of [20], one can see that the temporal convergence order in the second case of Example 1 is when the temporal uniform meshes-based compact difference scheme (11) is applied. Example 3. We perform the numerical simulation to study the dynamical behavior of the following time-fractional B-S model which describes the double-barrier knock-out calls:with the boundary conditions , and terminal condition . The parameters of the above equation are considered as (year), , and the domain are set as . One may refer to [1] for more details. In view of the corresponding equivalent form (2), we employ the temporal non-uniform mesh-based compact difference scheme (24) by setting and to plot the double-barrier option price at different α; see Figure 3. It can be observed from Figure 3 that the fractional order α in the time-fractional B-S Equation (1) has crucial influence on the option price. When the order α is smaller, e.g., , the option price deviates more from that of classical model. This phenomenon is especially significant when the stock price . This coincides with the conclusion of [1] and illustrates the rich expressive power of time-fractional B-S model (1) to characterize option price fluctuations. 6. Conclusions

Since the time-fractional B-S model often has a non-smooth payoff function, i.e., a non-smooth initial condition, the solution to the equation has limited smoothness, making it inherently difficult to construct higher order numerical schemes. In this paper, in order to overcome this difficulty, we investigated the compact difference schemes with temporal uniform/non-uniform meshes. The corresponding stability and error estimate are proved by the method of Fourier analysis. Numerical examples show that the derived schemes are stable with accuracy of

for the smooth/non-smooth solution problem. Thus, we improved some convergence results in the existing literature, in particular the two results presented in [

16,

18] by fourth-order spatial accuracy and second-order temporal accuracy, respectively, especially for the non-smooth solution problem.

It is known that the practical movement of financial markets is more complicated than that described by the one-dimensional time-fractional B-S model (

1). Some researchers have paid close attention to the efficient numerical methods of the high-dimensional B-S model; see [

21,

22] and the references therein. Thus, it is interesting to extend the ideas of our paper to solving high-dimensional problems, which will be one of our upcoming works.

{kind=link}

{kind=link}

{kind=link}