A Fast Computational Scheme for Solving the Temporal-Fractional Black–Scholes Partial Differential Equation

Abstract

:1. Introduction

1.1. PDE Formulation

1.2. Initial Conditions

1.3. Boundary Conditions

1.4. Caputo Fractional Derivative

1.5. Time Discretization

1.6. Background on Numerical Methods

1.7. Paper’s Outline

2. Spatial Discretization Nodes

3. A Fast High-Order Discretization

4. Construction of the Solver

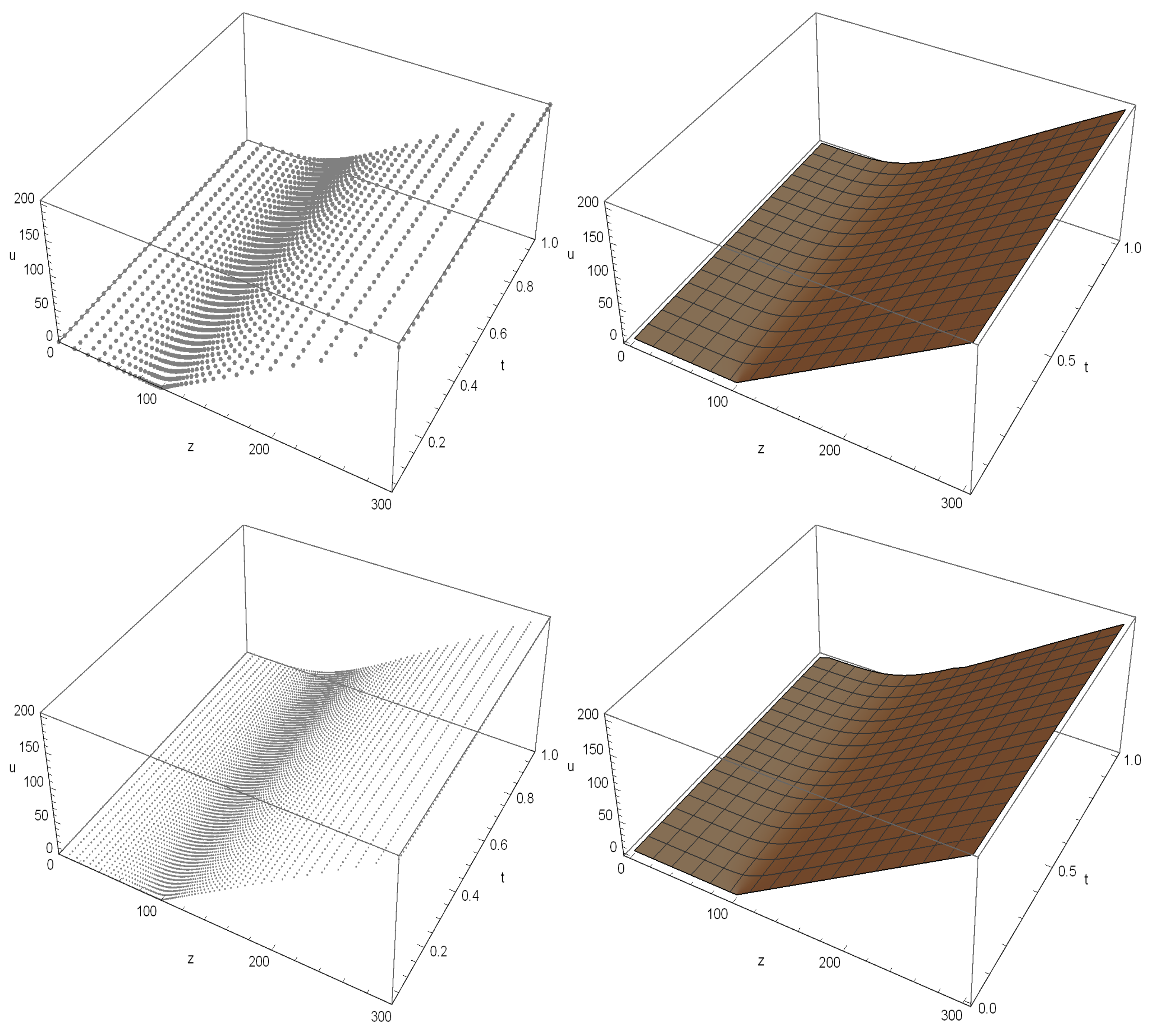

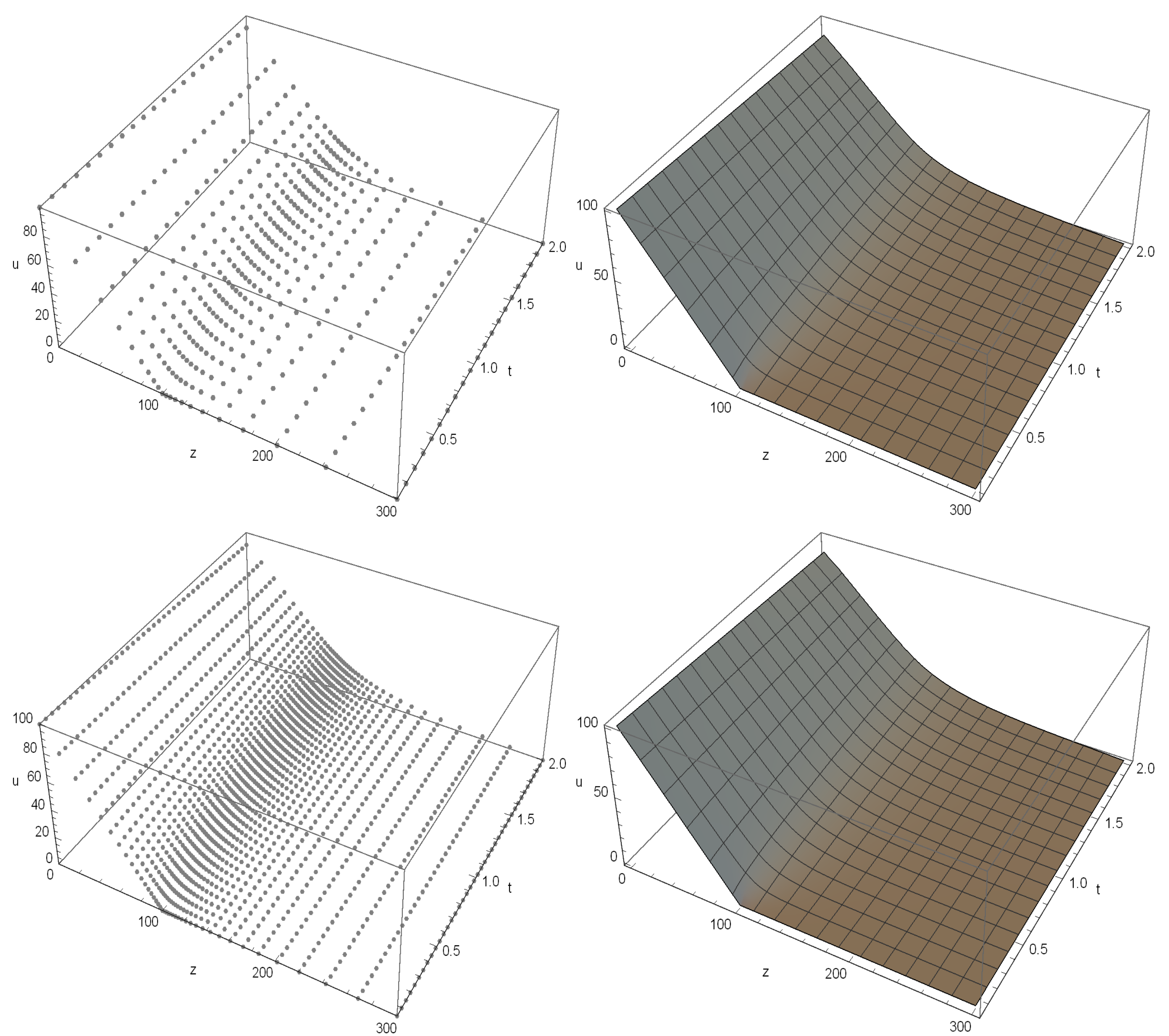

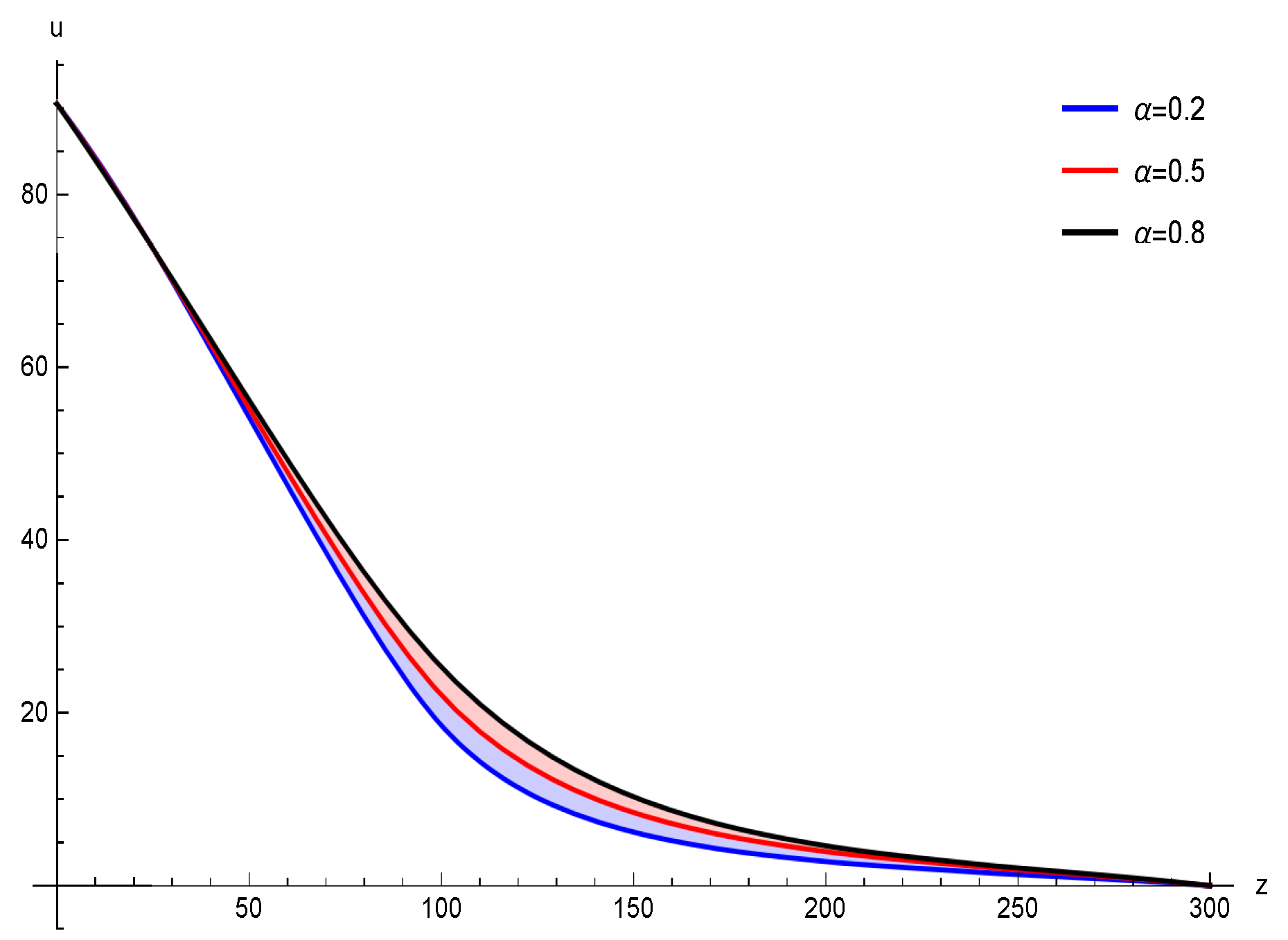

5. Numerical Tests

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Wyss, W. The fractional Black-Scholes equation. Fract. Calc. Appl. Anal. 2000, 3, 51–62. [Google Scholar]

- Jumarie, G. Derivation and solutions of some fractional Black-Scholes equations in coarse-grained space and time: Application to Merton’s optimal portfolio. Comput. Math. Appl. 2010, 59, 1142–1164. [Google Scholar] [CrossRef] [Green Version]

- Hurst, H.E. Long-term storage capacity of reservoirs. Trans. Am. Soc. Civil Eng. 1951, 116, 770–799. [Google Scholar] [CrossRef]

- Seydel, R.U. Tools for Computational Finance, 6th ed.; Springer: London, UK, 2017. [Google Scholar]

- Soleymani, F.; Zhu, S. Error and stability estimates of a time-fractional option pricing model under fully spatial-temporal graded meshes. J. Comput. Appl. Math. 2023, 425, 115075. [Google Scholar] [CrossRef]

- Jumarie, G. Modified Reimann-Liouville derivative and fractional Taylor series of non-differentiable functions further results. Comput. Math. Appl. 2006, 51, 1367–1376. [Google Scholar]

- Caputo, M. Linear model of dissipation whose Q is almost frequency independent II. Geophys. J. Int. 1967, 13, 529–539. [Google Scholar] [CrossRef]

- Diethelm, K. An algorithm for the numerical solution of differential equations of fractional order. Electron. Trans. Numer. Anal. 1997, 5, 1–6. [Google Scholar]

- Soleymani, F.; Barfeie, M. Pricing options under stochastic volatility jump model: A stable adaptive scheme. Appl. Numer. Math. 2019, 145, 69–89. [Google Scholar] [CrossRef]

- Soheili, A.R.; Soleymani, F. Some derivative-free solvers for numerical solution of SODEs. SeMA 2015, 68, 17–27. [Google Scholar] [CrossRef]

- Love, E.; Rider, W.J. On the convergence of finite difference methods for PDE under temporal refinement. Comput. Math. Appl. 2013, 66, 33–40. [Google Scholar] [CrossRef]

- Nikan, O.; Avazzadeh, Z.; Tenreiro Machado, J.A. Localized kernel-based meshless method for pricing financial options underlying fractal transmission system. Math. Meth. Appl. Sci. 2021. [Google Scholar] [CrossRef]

- Roul, P.; Prasad Goura, V.M.K. A compact finite difference scheme for fractional Black-Scholes option pricing model. Appl. Numer. Math. 2021, 166, 40–60. [Google Scholar] [CrossRef]

- Torres-Hernandez, A.; Brambila-Paz, F.; Torres-Martínez, C. Numerical solution using radial basis functions for multidimensional fractional partial differential equations of type Black-Scholes. Comput. Appl. Math. 2017, 40, 1–25. [Google Scholar] [CrossRef]

- He, J.; Zhang, A. Finite difference/Fourier spectral for a time fractional Black-Scholes model with option pricing. Math. Prob. Eng. 2020, 2020, 1393456. [Google Scholar] [CrossRef]

- Kluge, T. Pricing Derivatives in Stochastic Volatility Models Using the Finite Difference Method. Ph.D. Thesis, TU Chemnitz, Chemnitz, Germany, 2002. [Google Scholar]

- Akgül, A.; Soleymani, F. How to construct a fourth-order scheme for Heston-Hull-White equation? In Proceedings of the AIP Conference Proceedings of ICNAAM, Rhodes, Greece, 13–18 September 2018; pp. 1–5. [Google Scholar]

- Henderson, H.V.; Pukelsheim, F.; Searle, S.R. On the history of the kronecker product. Linear Multilinear Algebra 1983, 14, 113–120. [Google Scholar] [CrossRef] [Green Version]

- Zhang, H.; Liu, F.; Turner, I.; Yang, Q. Numerical solution of the time fractional Black-Scholes model governing European options. Comput. Math. Appl. 2016, 71, 1772–1783. [Google Scholar] [CrossRef]

- Song, Y.; Shateyi, S. Inverse multiquadric function to price financial options under the fractional Black-Scholes model. Fractal Fract. 2022, 6, 599. [Google Scholar] [CrossRef]

- Georgakopoulos, N.L. Illustrating Finance Policy with Mathematica; Springer International Publishing: Cham, Switzerland, 2018. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| m,n | T | T | T | ||||||

|---|---|---|---|---|---|---|---|---|---|

| 10 | 16.070 | 2.11 × 10 | 0.01 | 17.378 | 8.1 × 10 | 0.01 | 17.381 | 8.0 × 10 | 0.01 |

| 20 | 17.889 | 2.98 × 10 | 0.02 | 17.694 | 4.94 × 10 | 0.02 | 17.701 | 4.8 × 10 | 0.02 |

| 40 | 17.913 | 2.75 × 10 | 0.16 | 18.003 | 1.85 × 10 | 0.18 | 18.091 | 9.7 × 10 | 0.16 |

| 80 | 18.039 | 1.48 × 10 | 3.96 | 18.213 | 2.46 × 10 | 3.84 | 18.205 | 1.6 × 10 | 3.63 |

| 120 | 18.055 | 1.33 × 10 | 20.02 | 18.190 | 1.64 × 10 | 20.96 | 18.187 | 1.3 × 10 | 19.17 |

| m,n | T | T | T | ||||||

|---|---|---|---|---|---|---|---|---|---|

| 11 | 23.914 | 7.1 × 10 | 0.01 | 23.631 | 9.9 × 10 | 0.03 | 23.712 | 9.1 × 10 | 0.02 |

| 21 | 24.316 | 3.1 × 10 | 0.03 | 24.117 | 5.1 × 10 | 0.05 | 24.239 | 3.9 × 10 | 0.05 |

| 41 | 24.466 | 1.6 × 10 | 0.15 | 24.356 | 2.7 × 10 | 0.21 | 24.546 | 8.3 × 10 | 0.19 |

| 81 | 24.545 | 8.4 × 10 | 4.14 | 24.565 | 6.4 × 10 | 4.69 | 24.601 | 2.8 × 10 | 4.37 |

| 161 | 24.580 | 4.9 × 10 | 63.97 | 24.636 | 6.1 × 10 | 64.01 | 24.624 | 5.9 × 10 | 62.64 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ghabaei, R.; Lotfi, T.; Ullah, M.Z.; Shateyi, S. A Fast Computational Scheme for Solving the Temporal-Fractional Black–Scholes Partial Differential Equation. Fractal Fract. 2023, 7, 323. https://doi.org/10.3390/fractalfract7040323

Ghabaei R, Lotfi T, Ullah MZ, Shateyi S. A Fast Computational Scheme for Solving the Temporal-Fractional Black–Scholes Partial Differential Equation. Fractal and Fractional. 2023; 7(4):323. https://doi.org/10.3390/fractalfract7040323

Chicago/Turabian StyleGhabaei, Rouhollah, Taher Lotfi, Malik Zaka Ullah, and Stanford Shateyi. 2023. "A Fast Computational Scheme for Solving the Temporal-Fractional Black–Scholes Partial Differential Equation" Fractal and Fractional 7, no. 4: 323. https://doi.org/10.3390/fractalfract7040323