Numerical Investigation of the Three-Dimensional HCIR Partial Differential Equation Utilizing a New Localized RBF-FD Method

Abstract

:1. Introduction

1.1. Background

1.2. PDE Formulation

1.3. Motivation and the Need for Numerical Methods

1.4. Layout

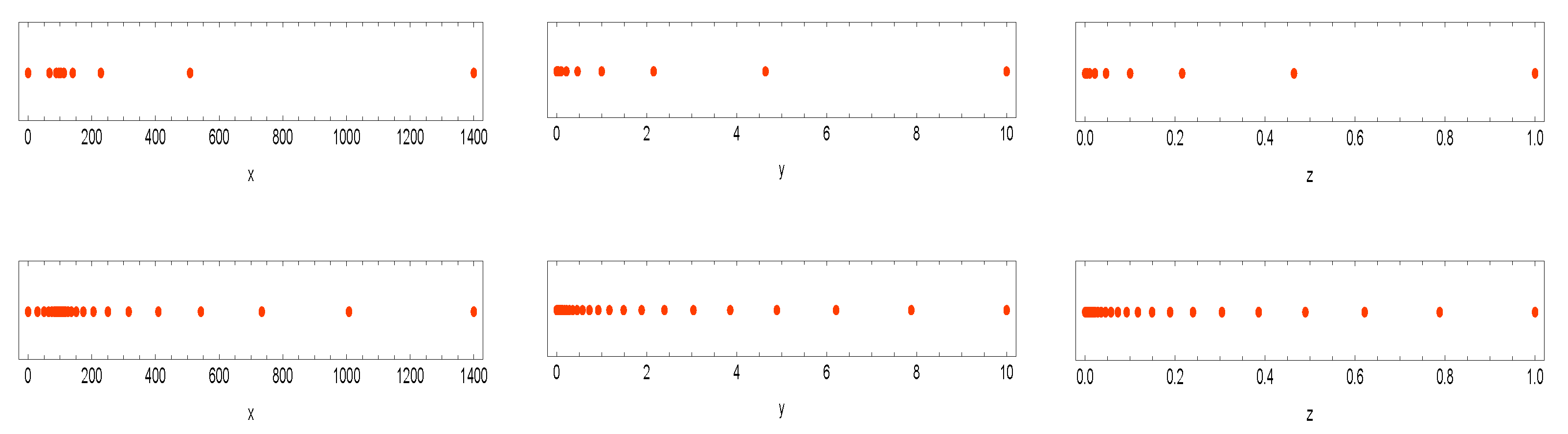

2. The Graded Meshes

3. The Weighting Coefficients for the RBF-FD Methodology

4. Construction of Our Solver

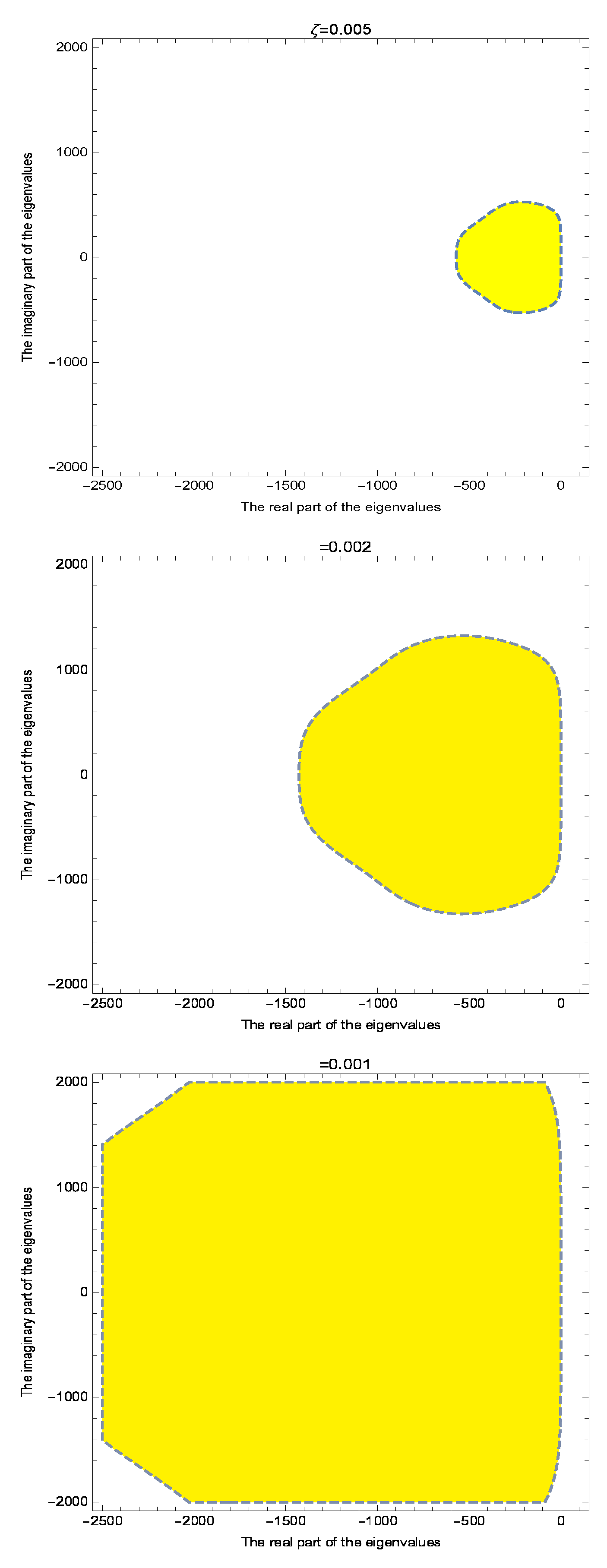

5. The Time-Stepping Solver

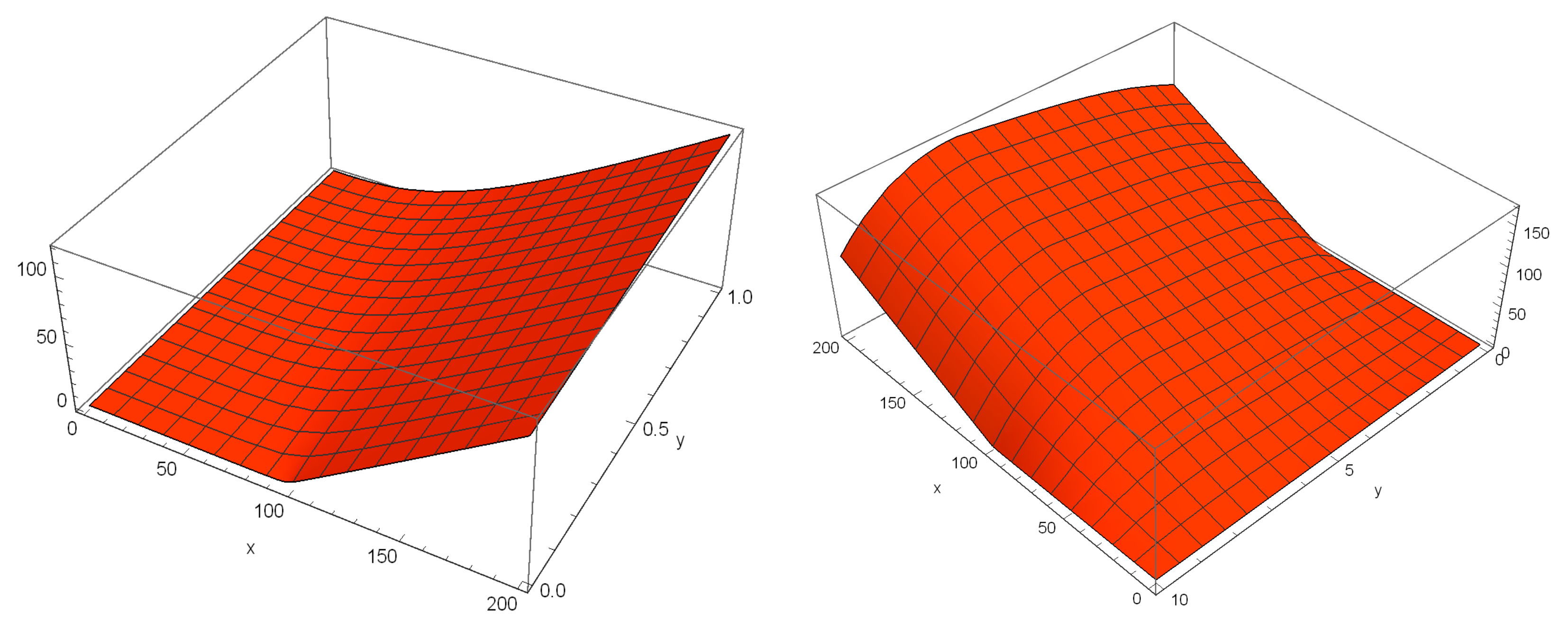

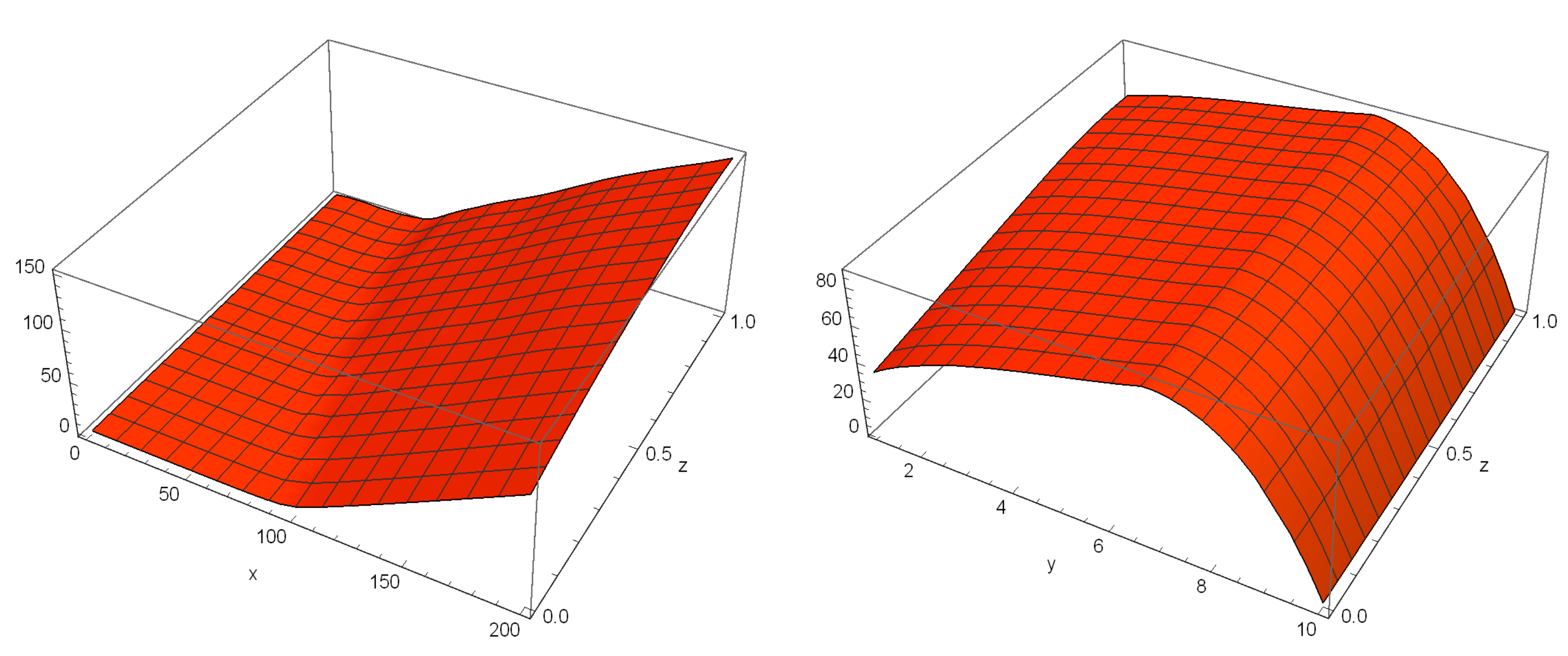

6. Financial Experiments

- The quadratically convergent FD method on uniform meshes and the first-order explicit Euler’s scheme denoted by FDS.

- The scheme with non-equally spaced node distribution (via the Douglas time-stepping method) given in [19], (shown by THM).

- The method presented by Soleymani et al. in [25] and shown by SAM.

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Adhikari, R. Foundations of Computational Finance. Math. J. 2020, 22, 1–59. [Google Scholar] [CrossRef]

- Itkin, A. Pricing Derivatives Under Lévy Models: Modern Finite-Difference and Pseudo–Differential Operators Approach; Birkhäuser: Basel, Switzerland, 2017. [Google Scholar]

- Guo, S.; Grzelak, L.; Oosterlee, C.W. Analysis of an affine version of the Heston-Hull-White option pricing partial differential equation. Appl. Numer. Math. 2013, 72, 143–159. [Google Scholar] [CrossRef] [Green Version]

- Heston, S.L. A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev. Finan. Stud. 1993, 6, 327–343. [Google Scholar] [CrossRef] [Green Version]

- Cao, J.; Lian, G.; Roslan, T.R.N. Pricing variance swaps under stochastic volatility and stochastic interest rate. Appl. Math. Comput. 2016, 277, 72–81. [Google Scholar] [CrossRef]

- Hull, J.; White, A. Using Hull-White interest rate trees. J. Deriv. 1996, 4, 26–36. [Google Scholar] [CrossRef]

- Ampun, S.; Sawangtong, P.; Sawangtong, W. An analysis of the fractional-order option pricing problem for two assets by the generalized Laplace variational iteration approach. Fractal Fract. 2022, 6, 667. [Google Scholar] [CrossRef]

- Zhang, X.; Yang, J.; Zhao, Y. Numerical solution of time fractional Black-Scholes model based on Legendre wavelet neural network with extreme learning machine. Fractal Fract. 2022, 6, 401. [Google Scholar] [CrossRef]

- Cox, J.C.; Ingersoll, J.E.; Ross, S.A. A theory of the term structure of interest rates. Econometrica 1985, 53, 385–407. [Google Scholar] [CrossRef]

- Grzelak, L.A.; Oosterlee, C.W. On the Heston model with stochastic interest rates. SIAM J. Finan. Math. 2011, 2, 255–286. [Google Scholar] [CrossRef] [Green Version]

- Djeutcha, E.; Fono, L.A. Pricing for options in a Hull-White-Vasicek volatility and interest rate model. Appl. Math. Sci. 2021, 15, 377–384. [Google Scholar] [CrossRef]

- Haentjens, T. Efficient and stable numerical solution of the Heston-Cox-Ingersoll–Ross partial differential equation by alternating direction implicit finite difference schemes. Int. J. Comput. Math. 2013, 90, 2409–2430. [Google Scholar] [CrossRef]

- Fornberg, B. A Practical Guide to Pseudospectral Methods; Cambridge University Press: Cambridge, UK, 1996. [Google Scholar]

- Kadalbajoo, M.K.; Kumar, A.; Tripathi, L.P. Radial-basis-function–based finite difference operator splitting method for pricing American options. Int. J. Comput. Math. 2018, 95, 2343–2359. [Google Scholar] [CrossRef]

- Vanani, S.K.; Hafshejani, J.S.; Soleymani, F.; Khan, M. Radial basis collocation method for the solution of differential-difference equations. World Appl. Sci. J. 2011, 13, 2526–2530. [Google Scholar]

- Farahmand, G.; Lotfi, T.; Ullah, M.Z.; Shateyi, S. Finding an efficient computational solution for the Bates partial integro-differential equation utilizing the RBF-FD scheme. Mathematics 2023, 11, 1123. [Google Scholar] [CrossRef]

- Liu, T.; Ullah, M.Z.; Shateyi, S.; Liu, C.; Yang, Y. An efficient localized RBF-FD method to simulate the Heston-Hull-White PDE in finance. Mathematics 2023, 11, 833. [Google Scholar] [CrossRef]

- Milovanović, S.; von Sydow, L. A high order method for pricing of financial derivatives using radial basis function generated finite differences. Math. Comput. Simul. 2020, 174, 205–217. [Google Scholar] [CrossRef] [Green Version]

- Haentjens, T.; In’t Hout, K.J. Alternating direction implicit finite difference schemes for the Heston-Hull-White partial differential equation. J. Comput. Financ. 2012, 16, 83–110. [Google Scholar] [CrossRef]

- Kluge, T. Pricing Derivatives in Stochastic Volatility Models Using the Finite Difference Method. Ph.D. Thesis, Technische Universität Chemnitz, Chemnitz, Germany, 2002. [Google Scholar]

- Milovanović, S.; von Sydow, L. Radial basis function generated finite differences for option pricing problems. Comput. Math. Appl. 2018, 75, 1462–1481. [Google Scholar]

- Fasshauer, G.E. Meshfree Approximation Methods with MATLAB; World Scientific Publishing: Singapore, 2007. [Google Scholar]

- Wright, G.B.; Fornberg, B. Scattered node compact finite difference-type formulas generated from radial basis functions. J. Comput. Phys. 2006, 212, 99–123. [Google Scholar] [CrossRef]

- Soleymani, F.; Zhu, S. RBF-FD solution for a financial partial-integro differential equation utilizing the generalized multiquadric function. Comput. Math. Appl. 2021, 82, 161–178. [Google Scholar] [CrossRef]

- Soleymani, F.; Akgül, A.; Karatas Akgül, E. On an improved computational solution for the 3D HCIR PDE in finance. Analele Stiintifice Ale Univ. Ovidius Constanta Ser. Mat. 2019, 27, 207–230. [Google Scholar] [CrossRef] [Green Version]

- Knapp, R. A method of lines framework in Mathematica. J. Numer. Anal. Indust. Appl. Math. 2008, 3, 43–59. [Google Scholar]

- Meyer, G.H. The Time-Discrete Method of Lines for Options and Bonds, A PDE Approach; World Scientific Publishing: Singapore, 2015. [Google Scholar]

- Sofroniou, M.; Knapp, R. Advanced Numerical Differential Equation Solving in Mathematica; Wolfram Mathematica, Tutorial Collection; Wolfram: Champaign, IL, USA, 2008. [Google Scholar]

- Luther, H.A. An explicit sixth-order Runge-Kutta formula. Math Comput. 1967, 22, 434–436. [Google Scholar] [CrossRef]

- Keskin, A.Ü. Ordinary Differential Equations for Engineers; Springer International Publishing: Cham, Switzerland, 2019. [Google Scholar]

- Shampine, L.F. Numerical Solution of Ordinary Differential Equations; Chapman and Hall: London, UK, 1994. [Google Scholar]

- Wellin, P.R.; Gaylord, R.J.; Kamin, S.N. An Introduction to Programming with Mathematica; Cambridge University Press: Cambridge, UK, 2005. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Case I | Case II | Case III | |

|---|---|---|---|

| 0 | 0 | 2.10 | |

| 0 | 0 | 0.014 | |

| 0.05 | 0.055 | 0.034 | |

| a | 0.20 | 0.16 | 0.22 |

| 0.03 | 0.03 | 0.11 | |

| 0.04 | 0.90 | 1.00 | |

| 0.12 | 0.04 | 0.09 | |

| 0.4 | 0.1 | −0.2 | |

| 0.2 | 0.2 | −0.5 | |

| 0.6 | −0.5 | −0.3 | |

| 3.0 | 0.3 | 1.0 | |

| K | 100 | 100 | 100 |

| T | 1 | 1 | 0.25 |

| Method | m | n | o | N | u | Time | ||

|---|---|---|---|---|---|---|---|---|

| FDS | ||||||||

| 10 | 10 | 10 | 1000 | 0.001 | 21.187 | 0.49 | ||

| 16 | 12 | 12 | 2304 | 0.0005 | 5.887 | 1.07 | ||

| 30 | 16 | 16 | 7680 | 0.0001 | 7.542 | 11.23 | ||

| 40 | 20 | 20 | 16,000 | 0.00005 | 10.698 | 52.96 | ||

| 54 | 22 | 22 | 26,136 | 0.00002 | 10.738 | 382.17 | ||

| THM | ||||||||

| 10 | 10 | 10 | 1000 | 0.001 | 12.216 | 0.68 | ||

| 16 | 12 | 12 | 2304 | 0.0005 | 13.046 | 1.81 | ||

| 30 | 16 | 16 | 7680 | 0.0001 | 13.325 | 15.31 | ||

| 40 | 20 | 20 | 16,000 | 0.00005 | 13.376 | 99.67 | ||

| 54 | 22 | 22 | 26,136 | 0.00002 | 13.404 | 473.52 | ||

| SAM | ||||||||

| 10 | 10 | 10 | 1000 | 0.001 | 14.944 | 0.63 | ||

| 16 | 12 | 12 | 2304 | 0.0005 | 13.804 | 1.68 | ||

| 30 | 16 | 16 | 7680 | 0.0001 | 13.515 | 21.54 | ||

| 40 | 20 | 20 | 16,000 | 0.00005 | 13.477 | 107.49 | ||

| 54 | 22 | 22 | 26,136 | 0.00002 | 13.457 | 499.67 | ||

| RBF-FD-PM | ||||||||

| 10 | 10 | 10 | 1000 | 0.002 | 14.846 | 0.62 | ||

| 16 | 12 | 12 | 2304 | 0.001 | 13.762 | 1.62 | ||

| 30 | 16 | 16 | 7680 | 0.0004 | 13.499 | 20.81 | ||

| 40 | 20 | 20 | 16,000 | 0.0001 | 13.471 | 101.19 | ||

| 54 | 22 | 22 | 26,136 | 0.00004 | 13.455 | 477.28 |

| Method | m | n | o | N | u | Time | ||

|---|---|---|---|---|---|---|---|---|

| FDS | ||||||||

| 8 | 8 | 8 | 512 | 0.002 | 47.829 | 0.27 | ||

| 14 | 10 | 10 | 1400 | 0.0005 | 5.469 | 0.71 | ||

| 20 | 14 | 12 | 3360 | 0.00025 | 14.786 | 2.13 | ||

| 24 | 16 | 14 | 5376 | 0.0001 | 12.960 | 6.91 | ||

| 32 | 18 | 18 | 10,368 | 0.00005 | 8.599 | 28.64 | ||

| 45 | 24 | 20 | 19,800 | 0.000025 | 6.456 | 178.43 | ||

| THM | ||||||||

| 8 | 8 | 8 | 512 | 0.002 | 5.010 | 0.30 | ||

| 14 | 10 | 10 | 1400 | 0.0005 | 6.440 | 0.69 | ||

| 20 | 14 | 12 | 3360 | 0.00025 | 6.672 | 1.97 | ||

| 24 | 16 | 14 | 5376 | 0.0001 | 6.729 | 6.58 | ||

| 32 | 18 | 18 | 10,368 | 0.00005 | 6.797 | 32.44 | ||

| 45 | 24 | 20 | 19,800 | 0.000025 | 6.830 | 180.59 | ||

| SAM | ||||||||

| 8 | 8 | 8 | 512 | 0.002 | 5.794 | 0.35 | ||

| 14 | 10 | 10 | 1400 | 0.0005 | 6.628 | 0.96 | ||

| 20 | 14 | 12 | 3360 | 0.00025 | 6.759 | 3.11 | ||

| 24 | 16 | 14 | 5376 | 0.0001 | 6.776 | 13.37 | ||

| 32 | 18 | 18 | 10,368 | 0.00005 | 6.809 | 57.16 | ||

| 45 | 24 | 20 | 19,800 | 0.000025 | 6.833 | 232.76 | ||

| RBF-FD-PM | ||||||||

| 8 | 8 | 8 | 512 | 0.004 | 5.861 | 0.33 | ||

| 14 | 10 | 10 | 1400 | 0.001 | 6.501 | 0.90 | ||

| 20 | 14 | 12 | 3360 | 0.0004 | 6.760 | 3.03 | ||

| 24 | 16 | 14 | 5376 | 0.0002 | 6.786 | 12.69 | ||

| 32 | 18 | 18 | 10,368 | 0.0001 | 6.826 | 55.84 | ||

| 45 | 24 | 20 | 19,800 | 0.00004 | 6.834 | 224.21 |

| Method | m | n | o | N | u | Time | ||

|---|---|---|---|---|---|---|---|---|

| FDS | ||||||||

| 8 | 8 | 8 | 512 | 0.002 | 0.857 | 0.10 | ||

| 14 | 10 | 10 | 1400 | 0.0005 | 2.124 | 0.27 | ||

| 20 | 14 | 12 | 3360 | 0.00025 | 2.976 | 1.08 | ||

| 24 | 16 | 14 | 5376 | 0.0001 | 3.214 | 3.54 | ||

| THM | ||||||||

| 8 | 8 | 8 | 512 | 0.002 | 3.210 | 0.30 | ||

| 14 | 10 | 10 | 1400 | 0.0005 | 3.528 | 1.01 | ||

| 20 | 14 | 12 | 3360 | 0.00025 | 3.604 | 1.51 | ||

| 24 | 16 | 14 | 5376 | 0.0001 | 3.694 | 4.92 | ||

| SAM | ||||||||

| 8 | 8 | 8 | 512 | 0.002 | 3.329 | 0.26 | ||

| 14 | 10 | 10 | 1400 | 0.0005 | 3.539 | 0.87 | ||

| 20 | 14 | 12 | 3360 | 0.00025 | 3.719 | 1.48 | ||

| 24 | 16 | 14 | 5376 | 0.0001 | 3.924 | 4.76 | ||

| RBF-FD-PM | ||||||||

| 8 | 8 | 8 | 512 | 0.0025 | 3.413 | 0.23 | ||

| 14 | 10 | 10 | 1400 | 0.000625 | 3.610 | 0.78 | ||

| 20 | 14 | 12 | 3360 | 0.0004 | 3.816 | 1.39 | ||

| 24 | 16 | 14 | 5376 | 0.00025 | 3.918 | 4.67 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ma, X.; Ullah, M.Z.; Shateyi, S. Numerical Investigation of the Three-Dimensional HCIR Partial Differential Equation Utilizing a New Localized RBF-FD Method. Fractal Fract. 2023, 7, 316. https://doi.org/10.3390/fractalfract7040316

Ma X, Ullah MZ, Shateyi S. Numerical Investigation of the Three-Dimensional HCIR Partial Differential Equation Utilizing a New Localized RBF-FD Method. Fractal and Fractional. 2023; 7(4):316. https://doi.org/10.3390/fractalfract7040316

Chicago/Turabian StyleMa, Xiaoxia, Malik Zaka Ullah, and Stanford Shateyi. 2023. "Numerical Investigation of the Three-Dimensional HCIR Partial Differential Equation Utilizing a New Localized RBF-FD Method" Fractal and Fractional 7, no. 4: 316. https://doi.org/10.3390/fractalfract7040316