Industry 4.0 from An Entrepreneurial Transformation and Financing Perspective

Bundesverband Mergers & Acquisitions e.V., 82131 Gauting, Germany

Sci 2022, 4(4), 47; https://doi.org/10.3390/sci4040047

Submission received: 19 April 2022

/

Revised: 7 November 2022

/

Accepted: 8 November 2022

/

Published: 1 December 2022

(This article belongs to the Special Issue Industry 4.0 – The Global Industrial Revolution: Achievements, Obstacles and Research Needs for the Digital Transformation of Industry)

{kind=link}

{kind=link}

{kind=link}

Abstract

:This paper addresses the management of digital–informational transformation of industrial enterprises. Any transformation requires the coordinated action of several independent actors. Similarly, the digital–informational transformation required for the fourth industrial revolution (i.e., Industry 4.0) requires the involvement of multiple actors from the public and private sectors. This applies to an individual company as well as to the entire sector, regardless of the desired level of transformation. The increasing dissolution of boundaries between industrial and non-industrial actors is therefore essential for Industry 4.0. This paper addresses the above dissolution activities, focusing on cross-company networks and management issues. The management aspects of the following factors are examined: culture change, strategies, degree of digitalization, degree of networking, Internet of Things, digital ecosystems, human resources, organizational development, hierarchies, cross-functional collaboration, cost drivers, innovation pressures, supply chains, enterprise resource planning systems and corporate acquisitions/mergers. Based on the findings on the above factors, a management-driven model of the “transformation to Industry 4.0” for manufacturing companies is presented and discussed. This work thus complements the existing literature on Industry 4.0, as the majority of the literature on Industry 4.0 deals with technical problem solving at the field level.

1. Introduction

1.1. General Remarks

This essay provides a complementary view to the analyses focused on technologies and sciences. The perspective presented here is that of the industrial practitioner and thus focuses on the challenges to managing (!) industrial transformation.

The guiding thesis underlying this paper is that the successful, on-target and on-time implementation of Industry 4.0 is less about the availability of necessary technologies than it is about management competencies, the use of adequate processes, appropriate organizational structures, capabilities for profound cultural and structural change, as well as the involvement of the diverse competence bearers required for this.

1.2. Nomenclature

The term “transformation” is understood here as a fundamental reorganization of structures and processes. This sets it apart from the more or less constantly ongoing and mostly marginal reorganizations.

In the broad public discussion, the term “Industry 4.0” is equated with “digitization”. However, this is conceptually incorrect, because according to the German Academy of Science and Engineering (acatech), digitization can be attributed to the “Industry 3.0” development phase. The development spurt, referred to as the “fourth” industrial revolution of modern times after acatech, is characterized by all-encompassing networking. The corporate transformations taking place today include both the complete implementation of digitization and all-encompassing networking. In order to avoid any misunderstandings, the somewhat cumbersome term “digital–informational transformation” is used in this essay as a keyword-like explanation for the implementations according to “Industry 4.0”.

1.3. Logic of the Sequence of Steps in This Paper

In view of the variety of major changes that our society is currently undergoing, this paper starts with a classification of the digital–informational transformation in the transformation landscape that is dominant today (Section 2). Section 3 deepens this consideration through a more precise analysis and presentation of the overarching processes and the industrial participation that takes place in them. Building on this, Section 4 deals with the actual implementation management, i.e., the industrial transformation as such, and explains how this is based on the preceding technology and knowledge management. Section 5 can thus conceptually focus on the purely industrial transformation of “Industry 4.0”. Section 6 builds on this, dedicated to the experiences with digital–informational transformation in industry. For this purpose, a generic model is presented that has its origins in the systematic management of corporate functions. In addition to the management of transformations, their costs, financing and risks must be dealt with, as announced in the title of the article. Section 7 is dedicated to this aspect. This highly exploratory essay implies that a prospective outlook on the further development of the digital–informational transformation is necessary, especially since the present presentation can also demonstrate the previously insufficient performance in corporate restructuring with the help of individual available data. This is covered in Section 8 under the title “Outlook”. The final Section 9 provides summarizing results and their evaluation. The most important findings are that (1) compared to the technical–scientific knowledge about the digital–informational transformation, the empirical knowledge for implementation is far behind; (2) the previous performance in the digital–informational transformation is not satisfactory on average; (3) there are a number of generic models for corporate transformation towards Industry 4.0, which, through combined use, make it possible to develop specific models for implementing the transformation as required; and (4) in view of the unsatisfactory data and study situation, a statistically valid study of failures and success factors in the operational implementation of “Industry 4.0” in companies is recommended. This could support the further orientation of the transformation practice and contribute to a sustainable improvement in performance.

1.4. Radical Change in Management Systems

The change from “classic” corporate management to entirely new management concepts that correspond with the vision of Industry 4.0 is one of the most profound changes that a company can undergo. Thus, the depth of the changes, the all-encompassing readiness of the measures, is most comparable to the fundamental restructuring measures familiar from mergers and major corporate takeovers. As remains to be shown, the degree of verticalization, for example, and the associated concentration of power play a major role. This must be contrasted with new approaches to more horizontally structured management models, which also imply decentralization of power. This primarily involves questions about the degree of autonomy of national organizations and subsidiaries which, according to the “classic model”, tend to be “controlled” by the CEO or corporate headquarters. IT-based structures and networks open revolutionary opportunities through rapid data dialogs based on the “countercurrent principle”—i.e., no longer just “direct top-down” but also bottom-up on an equal footing: based on decentralized market and customer proximity, with their specific requirements. The associated innovation potential for new networked management systems cannot be overstated, because ultimately, a company that was previously managed “as a general staff” can be transformed into an “internal digital entrepreneurial ecosystem”.

1.5. Professionalization through Transfer of Experience

From large M&A projects, especially after their professionalization phase since the turn of the century, we have a lot of experience to draw on [1,2]. Thus, for the field of Industry 4.0 transformation, for which there is significantly less documented and validated experience, the opportunity to draw on M&A experience is given. After a critical view of their “fit”, basic M&A leadership elements can be transferred to digital transformation. However, due to many specifics concerning the reported cases on “digital transformation”, we are not yet able to offer generally applicable generic “transformation management models” despite borrowing from the M&A world of today. In this respect, the approaches presented in this paper are to be understood as attempts and working theses, combined with the invitation to develop them further.

Accordingly, the methods underlying this essay deviate from the deductive technological–scientific approach underlying the essays on the fundamentals of Industry 4.0. As was the case with M&A in the 1990s, today’s implementation on “managing Industry 4.0” is based less on scientific management research and more on management experience that is strongly aligned with the success and value of business outcomes. To substantiate this with a buzzword, we would have to speak of an “art” of transformation management rather than a science, i.e., heuristics [2,3].

2. Localization of the Digital–Informational Transformation within the Current Transformation Areas

As established in the introduction, the thematic treatment starts at this point with a classification of the digital–informational transformation (“Industry 4.0”) in the transformation landscape to which our society is exposed today.

In the following, particular attention is paid to the fact that industrial companies not only represent the “owners” of entire processes, but are also participants in processes in which other partners such as the public sector and private individuals participate. In terms of process optimization for society as a whole, the “non-industrial participants” mentioned would have to be involved in the digital–informational transformation. Industry is to be assigned the role of a pioneer and driver in the digital–informational transformation of our industrial society.

Digital transformations now subsumed under the buzzword “Industry 4.0” involve the most urgent and immediate tasks that industry must address today to secure its future position in international competition. However, the problems facing today’s entrepreneurs go far beyond digital-driven transformation. We are in a phase of the greatest upheaval in the history of modern times. The challenges facing business in particular, in its role as a value-generating force in social society, are manifold and severe. Catastrophes, tensions, wars and mega-accidents of all kinds are accumulating and becoming ever more serious, followed by social and economic crises, some of which are moving around the globe in waves [1,2,3].

The countermeasures required in each case must be taken promptly and, if necessary, simultaneously. Thus, the digital transformation must be integrated into a larger field of transformations.

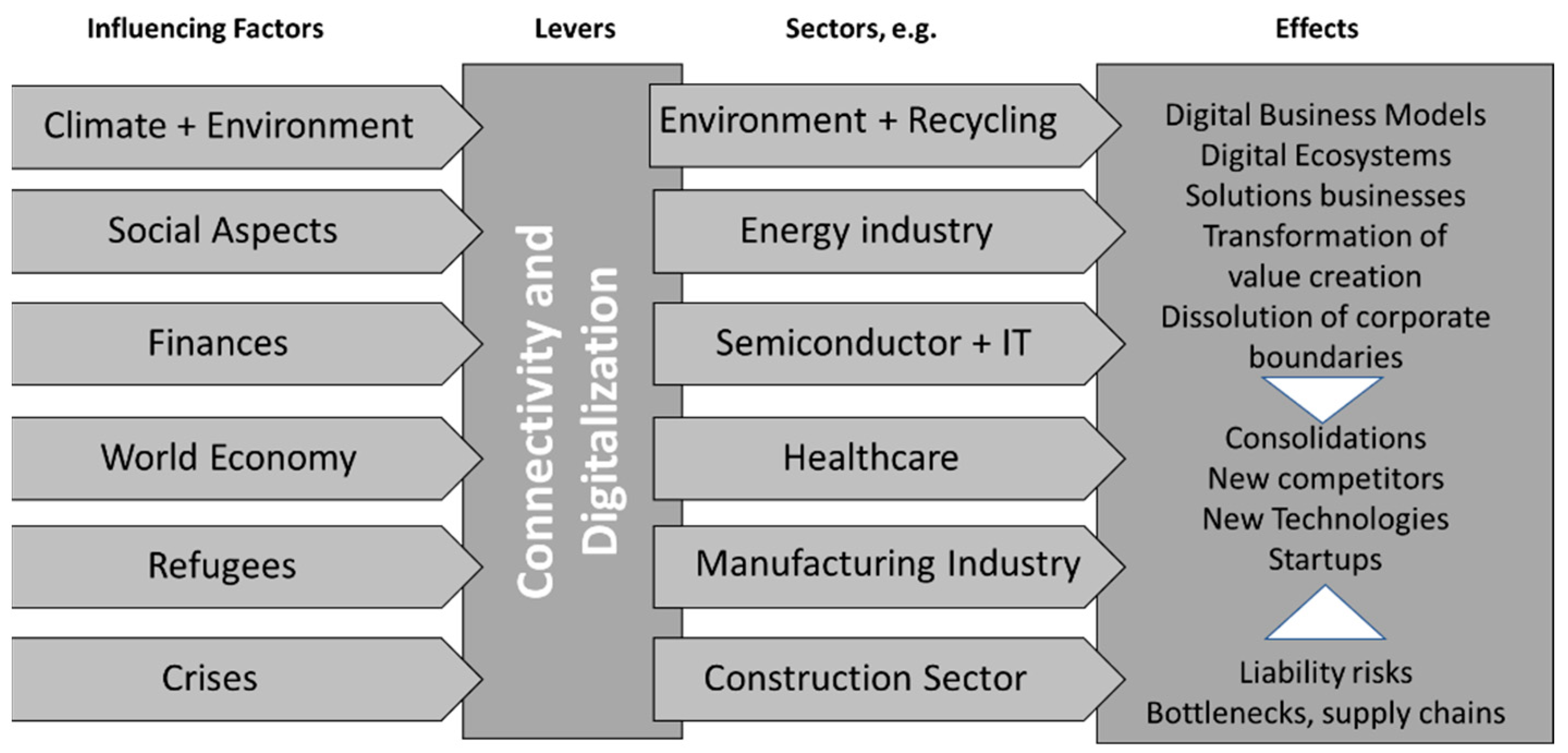

In Figure 1, the more detailed relationships are shown using examples. We distinguish between influencing factors, (mediating) levers, fields of action (“sectors”) and effects. The factors that are occurring simultaneously today include climate change with environmental consequences, social problems (poverty…), finances (inflation…), world economy (inequalities, economic cycles…), refugees (from crisis and war zones, economic refugees…), as well as crises (and disasters of different kinds). The influencing factors can overlap regionally or worldwide and build on each other. All influencing factors can have an immediate effect on companies, and they can also change their mechanisms of action. For example, environmental disasters can result in a national economic crisis. Thus, there are “intermediary” forces between the influencing factors, referred to here as “levers”. The catastrophe theory has a wide variety of explanatory models ready, which are not discussed in detail here.

For the purposes of application and explanation in this essay, the terms “connectivity” (in the sense of all-encompassing networking) and digitalization, which are associated with “Industry 4.0”, were used. These factors have a certain role at this point in the sense that there must be a connection (“connectivity”) for switching and that every form of data and information must be available digitally in order to be able to transmit it via our networks. This is how they are found in the sectors presented here as examples. The most important ones for the industry are currently the management of the energy transition and the supply chain problem, which are addressed in the present picture with the keywords “Semiconductor + IT” (information technology). The effects alone from the combination of energy change (including energy shortages as a result of the Ukraine war) with breaks in supply chains and (!) the claim to also manage the transformation to Industry 4.0 at the same time shows the dramatic situation industrial companies in particular are in, and how high their existential threat is. A single number may illustrate this: the share of intermediate consumption in the production value in the German industrial sector is “very high” at 63 percent. A large part of this is integrated into the supply chains at various points around the world. This size also shows that the necessary restructuring of supply chains is of unprecedented importance in corporate change. According to our definition, this area alone is a matter of real entrepreneurial transformations. These relationships and the variety of transformation fields to be mastered must be taken into account when we implicitly demand the improved implementation of Industry 4.0 models at this point.

These are undoubtedly enormous challenges for entrepreneurs, who are probably facing the greatest pressure since the Second World War. Digitalization and informational restructuring have cross-cutting functions, without which overarching crises cannot be overcome [4]. The digital transformation is not just a matter for the economy, but a task for the whole of society.

The entrepreneurial answers of our time are shown in the right column of Figure 1, such as digital business models. Special liabilities and bottlenecks have a restrictive effect, which, when combined, bring about changes in entire sectors, such as consolidation movements.

With major transformations and downright disruptive changes, the world’s economies are trying to take control over existing ecological, social and economic problems and to counteract escalations that seriously endanger our future.

It is also a favorable circumstance that in the phase of greatest upheavals and radical changes of the modern era, we have those instruments at our disposal, without which none of the pending transformations can be mastered: digitalization and the all-encompassing networking of people, organizations and machines.

Timely deployments of technical solutions are not coincidences but results of extensive research and development. In this paper, we address the challenges, hopes and setbacks to which such processes are fundamentally subject.

In this essay, it is to be shown that “Industry 4.0” not only offers tools for manufacturing industries and specifically their manufacturing processes, but that the so-called fourth industrial revolution encompasses all processes and all stakeholders because all-encompassing communication goes beyond companies. The Internet and data centers, as the informational backbone, connect everyone and everything.

At its core, this paper is dedicated to the drivers of the industry and explores questions about change, deployment factors and structures—but the processes at issue here do not end at virtual “perimeter lines” or “outer boundaries” around commercial enterprises. They extend far beyond that and encompass all organizations, administration, consumption and private citizens, utilities and infrastructures. Thus, if we consider the processes holistically (“end-to-end”), we would have to call them “total societal”. However, even this characteristic does not adequately describe our interconnectedness and process landscape unless the aforementioned infrastructure is also explicitly included—or, more expansively, “all things that surround us and are capable of interconnection.” To express the totality of society and “its networked things”, we choose as working terms the “Integral Processes” that run on the “integral networks of people and things” (i.e., primarily the Internet). This definition also takes into account the basic consideration that needs to maximize benefits while minimizing the use of resources which are not only concerns of the economy but also apply to any organization, the administration, the private citizen, utilities and infrastructure. Integral processes running on integrated digital infrastructure (networks and data processing) promise the greatest benefit for all. Experiences and rules from “Industry 4.0” can be transferred to the aforementioned integral processes. In this respect, we must also deal with our time-typical delimitations of digitalization and networking and not view “industry” in isolation [5,6].

3. On the Embedding of Industry 4.0

After classifying the digital–informational transformation in the overall landscape of transformations, with the driving role that industry plays in the digital–informational transformation (Section 2), the following consideration analyzes the cross-society processes with the industrial processes taking place therein in detail. We begin with a presentation of the overall entrepreneurial situation. This aims to clear up the misunderstanding that “Industry 4.0” only affects the product provision area (procurement, production…). Rather, the company’s internal processes go beyond this and involve all contributors to overall corporate performance, namely management, strategy, purchasing, administration, finance, accounting and human resources.

Administration: Digitalization and networking within a company encompass all activities and do not stop at administration. In this respect, administrations within companies are inseparable parts of “Enterprise Models 4.0”. Nor does the concept of cross-company ecosystems end at industry boundaries or in the form of a perimeter line around industry. Rather, the hallmark of our highly developed industrial society is that the public sector with its offices, administrations and ministries is also part of the “all-encompassing network”. It is common practice for companies to forward their relevant data directly to the tax authorities which use automated processes to calculate taxes and send notices—all paperlessly over the Internet. In this respect, it is time to reinterpret the term “Industry 4.0” in the direction of an “Industrial Society 4.0”.

Public sector ecosystem: In this way, public administration can act as a pioneer for a data-based digital ecosystem that will bring companies and citizens the hoped-for efficiency, effectiveness and reduction in bureaucracy. A number of concepts and projects have been developed to achieve this goal. If it is possible to link this preliminary work across levels and sectors, end-to-end process chains and innovative services could be created at the interface between administration, business and civil society. Data play a key role in this process, enabling synergy potential to be tapped and innovative services to be developed. Concepts for data-based service platforms for public administration already exist. Approaches from Industry 4.0 are being taken up and developed further, for example, under the slogan “Smart Data for Public Services”. Building on this, administrative ecosystems can be developed in which, for example, city halls are connected, whereby a wide variety of services can be harmonized and provided centrally at different locations [7,8]. So much for concepts and potential. Implementation, on the other hand, looks rather critical.

Dangerous backlogs: Compared to the economy, the public sector is still years behind in digitalization, its networking and the standardization and provision of its services. Germany is finding it particularly difficult to innovate because of the diversity of stakeholders (federal states, administrative levels…) due to overregulation, rigidities and fears. All our neighboring countries are further along. Approaches agreed throughout Europe, such as the “once-only principle” agreed 10 years ago, according to which it should be sufficient to give a basic personal information only once to an authority, after which all offices can access this basic information, are not implemented in our country. Optimistic programs for the economy are published at the highest political level. The implementation within their own ranks is often diametrically opposed to this. This also has a knock-on effect on the business community, which must cope with slow administrative procedures and bureaucracies that still largely work with paper and fax [9]. Recent attempts to standardize processes throughout Germany and to get the responsible administrations to work in a network have failed [10].

4. From Knowledge to Implementation

This section describes the decisive step from “advice to action”, namely from the technical–scientific treatment of the digital–informational transformation with its technologies and concepts, to operational implementation. As can be shown, the decisive hurdles today lie in the choice of implementation paths and the actual operationalization. The focus here is therefore the implementation management (in contrast to knowledge management) with the further questions, where do we stand, and where are you going? While knowledge and knowledge management about “Industry 4.0” are dealt with extensively in the literature, we are entering largely new scientific territory with the challenges and solution approaches for the operational implementation of corporate transformations. We do not come across representative scientific investigations. Data are sparse and we have to rely on data published in the trade press. In this inadequate situation, demands for scientific work-up must be made, as they are made at the end of this paper. We start with an analysis of the status quo.

4.1. Political Assessment of the Current Situation

The migration of a classically functioning company to an operation with end-to-end intelligent networking of all processes [11,12,13], with comprehensive integration of people and machines, still poses a major challenge for most players, even if the IT background is already advanced. This applies both to the extent of change to comprehensive information penetration of the processes and to the associated resources required for conversion and risk prevention.

Thanks to the work of acatech, the German government has also recognized the importance of information technology and digital networking as crucial levers for further development of our economy and for safeguarding our prosperity. In its spring 2022 report on “Industry 4.0 for Germany as a business location”, the German Federal Ministry for Economic Affairs and Climate Action stated that:

- 95% of companies see Industry 4.0 as an opportunity;

- 6 out of 10 companies already use Industry 4.0 applications;

- 91% of industrial companies see Industry 4.0 as a prerequisite for maintaining the competitiveness of German industry; and

- 75% of industrial companies believe that Industry 4.0 will reduce CO2 emissions [14].

These opinions raise hopes and ignore implementation hurdles. We may be rich in concepts and technologies—but we are weak when it comes to implementation. Despite all the inventiveness and research funding, the “capitalization” of ideas, concepts and inventions that can be attributed to “Industry 4.0” is taking place primarily and much more quickly among our competitors, especially in the U.S. and China [9,14]. This is particularly critical for the further development of our economy because, as a result of the economic boom and low interest rates, companies were able to remain in the market that would have long since been squeezed out of the market under more difficult boundary conditions. As a result of the COVID-19 waves (at the beginning of the waves, an additional 100,000 company insolvencies were expected), there was also entrepreneurial damage which has not yet taken the form of business closures [15,16].

Projections by economic institutes predict that the pressure to transform and the large wave of insolvencies still to be expected in the medium term, which we are experiencing as a result of a boom in the economy combined with capital costs that are too low for the market, can only be compensated for by new business approaches that are closely linked to high-tech innovations, far-reaching digitalization and all-encompassing communications based on the latest infrastructure technologies (current expansion to 5G; currently, preparatory research and development for 6G in international consortia, mainly from companies in the U.S., Europe and Asia).

4.2. Diagnoses from the Business World

The dimensions of change can be mapped in highly diverse ways. Frequently mentioned are optimization of processes, flexibilization of activities, fundamental changeability, increase in customer value and minimization of the use of resources. To measure change and ensure reproducibility and sustainability, processes and products must be comprehensively mapped and backed up with data.

A more far-reaching concept calls for virtual images of real products and processes. This concept also generates concern among those affected—especially from the older generation—since they mostly come from real, tangible worlds of action and products. Resistance from the ranks of experienced plant foremen against transformation officers only erupts relatively late, when the depth of the change and the personal consequences only really become clear to the representatives of the “old world” after a series of in-depth discussions. By then, however, considerable effort and time have already been invested, which must be practically written off until the disputing parties diplomatically agree on changes in direction that can be supported jointly.

The fact is, consequently, that implementing change in the field of opposing forces will cost much more time, tie up many more resources and involve much greater risks than the preachers of change could have imagined. This also requires coping with setbacks, as is currently being reported by the chemical industry, for example.

Discrepancies: Surveys among larger companies on the international stage reveal discrepancies between high expectations and practical implementation experience in the transformation toward Industry 4.0. In most companies, there is certainly enthusiasm for transformation and ambitious plans for future investments. At the same time, however, gaps in the networking of plans and measures are conspicuous. “While digital transformation is already taking concrete shape in companies, there are lags in terms of strategy, supply chain transformation, workforce preparation and drivers for investment. Inconsistencies between theory and practice are an indication that while there is a pronounced willingness to address digital transformation, organizations are for the most part still struggling to find a way to balance the optimization of their current business with the opportunities created by technologies in the context of Industry 4.0 [17].”

Individual comments corroborate this:

(2019) “Companies tended to focus on steady evolution such as the gradual networking of machinery, a focus on cost reduction and on increasing efficiency—rather than on a disruptive revolution, for example, in the form of complete networking and the implementation of new business models.”[18]

(2020) “Although manufacturing companies recognize the importance of digitalization, there are only a few that have managed a successful digital transformation. Many companies stall in the pilot phase or struggle to achieve enterprise-wide scalability.”[19]

(2020) “digital transformation is still weak at four-fifths of companies in the German economy and is thus still in its infancy.”[20]

(2021) “Overall, the industries have become only slightly more digital compared to the previous year…. The strongest growth is recorded by tourism…. The strongest decline is recorded by the basic materials, chemicals and pharmaceuticals industry group. Its index score drops from 100.6 to 94.5 points.”[21]

(2021) “German SMEs have so far made only slow progress with the digitalization of their business processes. Even the government-provided support programs have only been comprehensively used by around five percent of companies to date.”[22]

(2021) “Even in 2021, processes in small and medium-sized enterprises are still characterized by paper, makeshift solutions, distributed IT tools and a lot of manual intervention…. This means that companies not only give away competitive advantages, but sooner or later even jeopardize their own ability to survive and leave their employees intellectually drained”.[22]

As the quotes make clear, the discussion essentially focuses on the concept of digitalization, but not on comprehensive networking, which—according to the creators of the term—represents the core of “Industry 4.0” [23,24,25,26,27,28].

All-encompassing networking, as the defining criterion of “Industry 4.0”, was made possible by the Internet, which is capable of connecting all people, all things (“Internet of Things”) and all organizations through unique addresses. The basic element is the cyber–physical system (CPS, see Figure 2), which is composed of mechanical components, electronic components and informational components (hardware and software) and includes the data interface to the network. These prerequisites distinguish this element from its predecessors from the previous industrial generation “3.0”, which (like the CPS) have the basic interfaces for energy supply as well as sensors and actuators, which therefore characterize an automaton (robot…) even without integration into a higher-level communication network—just functioning autonomously [29].

5. Industrial Implementation

Building on Section 4, which explains the actual implementation management, i.e., the industrial transformation as such in the context of the preceding technology and knowledge management, Section 5 can now focus conceptually on the purely industrial transformation of “Industry 4.0”. We will deepen the definitions given in the introduction to this paper on transformation in general and on “Industry 4.0” in particular. In doing so, we direct our attention to the inter-entrepreneurial networking that is particularly under discussion today, which is closely linked to the dissolution of entrepreneurial boundaries that can be observed today. Then, we go into the main challenges and levers.

5.1. Definition and Basic Understanding: What Does “Industry 4.0” Entail—What Should It Encompass?

“Industry 3.0” characterizes the development thrust of the years from 1950 to 1960 with the resulting implementations [9]. Industry 4.0, on the other hand, refers to the phase toward all-encompassing networking, starting with the spread of the Internet, the foundations of which were laid from the mid-1960s [9]. In today’s common linguistic usage, the two development phases are smeared together, and the term “digitalization” is used as a quasi-generic term—as is the case in particular with the German federal government, which mostly speaks of “digitalization” in its presentations, although our current industrial–social upheaval is much more strongly characterized by end-to-end communication encompassing all protagonists. Digital technology in the infrastructure (hardware and software infotech in data centers and networks…) provides the technical basis for this. One must be careful here: we may not speak of digital basic technologies if we refer to the informational social transformation.

The networking of companies with each other is to be understood as any form of informational and operational collaboration between companies and thus to be backed up with recommendations drawn from the implementation of “Industry 4.0”. This consequently includes:

- Service chains, for example, from the supplier via production and assembly operations to the logistics provider.

- Competitive relationships: opposing in direct competition, cooperation in associations, committees and across organizations such as chambers of industry and commerce.

- Inclusion of service providers at every stage of the value chain and for all processes.

- Service providers and infrastructures for data and communications technology, data hosting and processing (such as cloud, fog and edge computing).

- Dissolution of boundaries between companies, which are increasingly acting as a combination of manufacturers and customers, so-called prosumers or Xsumers (Xsumer stands, for example, for consumers who step in as manufacturers when demand peaks, such as when electricity generators are switched on by the grid operator via photovoltaics), for example.

- Emergence of so-called digital ecosystems, where every emerging market niche in supply and demand is occupied in a short time, both by diversifications of existing players and by new entrants such as startups, stationary and online-based founders.

- Permanent, temporary and regional forms of entrepreneurial cooperation such as consortia, project companies, purchasing alliances—mostly without capital backing.

- Capital-backed forms of entrepreneurial mergers such as joint ventures.

- Forms of cooperation between business and the public sector, such as public–private partnerships (PPP).

5.2. Levers and Challenges to Digital–Informational Transformation

Important levers and challenges to digital–informational change are discussed below.

Culture change: The digital transformation of organizations requires significant and often painful behavioral changes from those affected. Entire “operating models” (processes, setup, networking, competence management…) are affected as new forms of collaboration and leadership need to be implemented in organizations to keep up with the competition of change. Sustainable changes as well as new demands on strategies, technologies, people and processes require more dynamic and flexible tools to manage, evaluate and track progress of transformation. This should be carried out step by step, with milestone controlling, and iteratively to practice the new ways of doing things. Indeed, experience shows that changing behaviors that add up to a cultural transformation is particularly time-consuming (time, cost…), and that the risk of falling back into old behavior patterns and of reviving old insider relationships is extremely high.

Strategies: The message of the importance of digital transformation has been received by most companies. Most executives state that digital transformation is one of the most important strategic goals in their organization. However, this does not necessarily mean that they are fully exploring the strategic opportunities that digital transformation offers. Indeed, surveys revealed that around two-thirds of executives see the transformation to “Industry 4.0” merely as a means of increasing profitability [30].

Degree of digitalization: Digitalization is gaining massive importance in companies. More than half of the companies report that responses to the COVID-19 pandemic have brought a significant boost in digitalization. Three-quarters of companies are convinced that companies with a digitally driven business model are in a more stable position and state that companies that have already digitized their business processes will better deal with the COVID-19 pandemic [30]. However, if companies continue to focus only on how digital technologies can accelerate digital transformation, cross-functional collaboration is likely to fall short. Entrepreneurs who have successfully implemented digital transformation, however, rank low-friction inter-functional collaboration as elementally important. Alongside efficiency and productivity, this is becoming an increasingly important barometer of success, especially in economically difficult times.

Degree of networking: Industry 4.0-oriented strategies often do not yet fully target the potential of networking. Capabilities to bundle information from interconnected assets and use it to make informed decisions are critical for full implementation of Industry 4.0, but many organizations are not yet able to fully realize this competency in practice. Referring to the fundamental need to restructure management structures—in a departure from general staff planning from headquarters and enforced by the executive board down to the regional units—reference has already been made to the enormous potential offered by IT-backed digital networking, with its fast bi-directional communication options between headquarters and the periphery. As a result, regional units and special business segments, for example, gain many more opportunities to implement their ideas on management, which, after all, know the needs of their particular customers much better and can consequently deviate from central specifications according to the “fit for all model”.

Internet of Things: All-encompassing networking—as mentioned above—includes networking of things. The Internet of Things (IoT) has become a reality in industry and the consumer sector, revolutionizing the entire economy. More and more Internet-enabled “things” such as parts, components, plant areas, finished products and resources are providing automated, efficiency-enhancing control and optimization of manufacturing and logistics processes. “Smart” working factories in Industry 4.0 produce faster and are more resource-efficient, more flexible and scalable.

Digital ecosystems: In a global and highly competitive environment, companies no longer operate autonomously. Instead, they are becoming part of complex, networked and growing ecosystems in which there should be permanent cooperation with the best and most innovative partners. All of this requires new ways of thinking and working: agile and open, flexible and forward-looking. Reference has already been made to the internal digital-backed ecosystems to be formed within the company.

Personnel: Executives are generally confident that suitable personnel are available to shape digital transformation—but they acknowledge that the personnel issue is an ongoing challenge. In fact, only a small minority of top management of internationally active companies see the need to fundamentally change the composition and skills of the workforce in the course of an Industry 4.0 transformation. At the same time, however, the executives rate finding, training and retaining suitable personnel as the greatest organizational and cultural challenge [31].

Organizational development: Traditional inter-functional competition within individual companies inhibits growth and works against the overarching goals of digital transformation. Therefore, digital transformation is also primarily about breaking down functional silos to collaborate better and to be able to drive innovations with higher pressure. Research shows that higher digital transformation investments have seen significantly higher revenue increases than their more conservative competitors. Such “champions” invested 1.1 times more (20.5 percent of their total revenue) than others in digitally transforming their functions. As a result, they achieved twice as much revenue growth as the other companies: 23.7 percent compared with 10.3 percent [31].

Hierarchies: Surveys typically reveal breaks between corporate management and downstream management levels. For example, the management level, which is responsible for managing day-to-day operations, often has little say in the fundamental design of processes. However, during digital transformations, these are quite decisive for success. With increasing informational transformation, hierarchies are becoming less important [32]. Digitalization requires flat hierarchies in which network-like work structures in particular can be implemented. The order of the day is teams with clear role assignments that are not thwarted in their effectiveness, speed of decisions and implementations by hierarchical behaviors [33].

Cross-functional collaboration: It would be a misunderstanding to look for networking under “Industry 4.0” only in the IT infrastructure and the software solutions running on it. The new industrial generation is also based on new forms of interpersonal collaboration as well as on the IT-backed possibilities of human–machine communication. However, cross-functional collaboration is still difficult in many companies. In most companies, different business functions (such as R&D, engineering, production, marketing and sales) are still competing with each other instead of driving the IT transformation forward in a unified and seamless way.

Cost drivers: The problem of functional specialization, with little development of cross-functional careers, which can be observed particularly in Germany (so-called silo structures), is a burden on the informatics transformation. It impairs sales and the success of operational expenditures. This was also reflected in a survey conducted by the management consultancy Accenture for the DACH region:

- Competition between different functions in companies causes superfluous investments in digital projects. In the period studied from 2017 to 2019, actual costs in DACH companies increased by 4.4 percent.

- The digital investments made by function leaders should increase the company’s revenue by 12.9 percent annually. In fact, annual revenue increased by an average of 4.2 percent from 2017 to 2019—only one-third of the expected revenue growth in DACH companies.

- According to three out of four DACH companies (74 percent), digital investments do not increase revenue growth [30].

Innovation pressure: With global networking, access to the Internet, and the lowering of market entry costs via online activities, the pressure on national industry players to perform has increased significantly. This is because national market barriers protect them less and less against companies that attack with innovative service offerings from abroad. This is the critical side to competition. However, anyone who makes full use of the opportunities for digitalization and networking in conjunction with smart data technologies, for example, by virtualizing products and processes, can accelerate their product delivery process by a factor of two to four and reduce costs accordingly. This can take place by working on a virtual twin of the future “real” product and can also be reflected in localized, relatively freely “movable” manufacturing value creation. This can be achieved, for example, by having globally distributed design partners and production service providers who have access to the digital twin via the network. Their designs and productions can be used on a demand-driven basis and in compliance with regulations across the globe. Manufacturing modules must be connected with each other and meet regulatory requirements for compliance with technical standards and for localization of value creation [17]. IIoT [34] applications, as the central core of Industry 4.0, play a fundamental role for digital transformation in this context.

Supply chains can be understood as typical extensions of internal company process chains in value generation. Thus, they should also be included as elements of “Industry 4.0”-based management models. The digital transformation provides decisive impetus for the efficiency of the supply chain. As a result, the interaction between the procurement departments of suppliers and manufacturers is gaining momentum. Thus, the implemented ERP systems should be put to the test, for example, whether they still meet the requirements of production plans, quality criteria and budgets of the purchasing departments in the future. The goal is a fully networked supply chain with which the production status can be viewed in real time at any time [35].

Merchandise Management Systems (MMS): control the flow of goods in terms of quantity and value and can thus be designed as complementary solutions for supply chain management. Purchasing, sales and warehousing must be integrated. A digital MMS offers operational improvements and savings potential through links with finance and accounting, human resources and marketing. To this end, all relevant employees must have access to a common MMS data pool, which they can use to track changes in the flow of goods and values in real time. Thus, a digital MMS is a solution approach that can fulfill the requirement criteria according to “Generation Industry 4.0” [36].

6. Approaches to and Experience with Comprehensive Digital–Informational Transformations in Industry

Following the challenges and levers for the operational implementation of the transformation to organizations according to “Industry 4.0”, explained in Section 5, we take the next step in this section by investigating the question of what the status of digital–informational implementation is today and how it is about the opportunities and barriers to further implementation. We explore this with individual examples. Above all, these shed light on management models and international contexts, which are crucial for successful implementation. A generic framework model for the transformation of manufacturing companies towards “Industry Generation 4.0” is presented for further discussion. In this context, the typical paths for the implementation of “Industry 4.0” are also presented.

As explained, entrepreneurs’ own assessments of the status of their level of digitalization and their ideas about what still needs to be achieved are strongly subjective. Since companies use IT equipment and, as a rule, accounting software, they all believe they are “already somehow in the digital world”. The conceptual impurities in everyday language usage encourage this. For example, the blurring between “digitalization” and “all-encompassing networking”.

6.1. Chances and Limits for the Reorganization of Entrepreneurial Leadership Models

One of the classic leadership conflicts that a board of management faces is the question of the power with which it wants to and must enforce its fundamental experience and ideas on the management of all business and activities in the business units, right down to the periphery (e.g., regional units, business segments). Or, thinking the other way around, how much autonomy (disobedience?) does it concede to peripheral activities in shaping their businesses? After all, these could have good reasons to deviate from the company’s “standard model” because their business partners have different expectations than, say, the “standard customer at the head office”. The resulting leadership dilemma must be recognized and endured by a demanding corporate leader, who must then weigh which direction to take, not just according to one of the two polar basic models, but varying it according to the specific needs to be met.

Reference has already been made to the connection with the “Industry 4.0” approach because decisions made by the management board and executives are directly dependent on each other and require the closest possible bidirectional coordination, which can only be achieved with the help of the latest communication and IT systems. These, in turn, must be embedded in the planning and controlling systems of the company concerned, including, for example, the aforementioned merchandise management system.

Regional peculiarities naturally increase the complexity of planning and controlling processes enormously, especially when one considers that regional peculiarities can be found at several locations and each time in a different form. These would also have to be mapped in higher-level IT systems, unless the corporate headquarters decide that deviations are only to be recorded gradually at headquarters and are to be managed from there.

In addition to the need to keep the complexities of management and controlling low, there are other reasons for (gradual) decoupling the periphery. These include economic policy circumstances, such as tendencies toward deglobalization. In concrete terms, this can result in the decoupling of entire regional markets and countries from the international network. This may be due, for example, to local content requirements, political risks, national technology standards or local purchasing regulations.

Despite all such barriers, internationally valid regulations could take effect, such as the Supply Chain Due Diligence Act, according to which a company based in Germany must also ensure responsible management of supply chains for its local subsidiaries abroad and compliance with human rights, safety and protection of employees also in the locally supplying plants. The fact that this also requires the collection of a great deal of data and that the associated processes should obviously be carried out in accordance with standards that apply uniformly to all regional units worldwide is imperative for reasons of the company’s legal responsibility for all its activities and for the economic application of the procedures [37].

6.2. Dissolution of Boundaries

As shown, the currently observable dissolution of corporate boundaries must be reflected in the fact that the appropriate “dissolved” corporate models must be included for the respective case.

The most important ones are listed here again in the form of buzzwords: digitally driven ecosystems, data-driven services from procurement to the point of sale, including forecasting from the purchasing market to consumer behavior, online business models (B2B, B2C…), new solution businesses (which can displace product manufacturers from their direct relationship with their customers), role changes (such as manufacturer vs. agency) and function changes, such as between producer and consumer (prosumer, xsumer…).

The involvement of third parties, from whatever organization, plays a special role as a driving force for the innovation capability and flexibilization of the respective company. As shown, stability and change are the two poles between which a company must constantly recalibrate itself. The CEO who makes things easiest for himself is the one who always pursues “business as usual…” and thus falls prey to the assumption that his/her company will remain stable. Especially in times of great change, and when new business models driven by Industry 4.0 are being pushed forward, the effect can go exactly in the opposite direction: the market and competitors change, and the company in question loses touch in its seemingly stable position and goes down.

Studies have shown that in-house strategy analyses whose results recommended “continuing as before” were followed in most cases, while studies that concluded that fundamental changes in direction were recommended were factually questioned in large numbers and consequently failed due to internal resistance. (The author, for example, had carried out such investigations in the context of his assignments at Siemens AG and was able to prove such acceptance and implementation resistances.) Navel-gazing and inside views typically obscure rather than reveal new findings, sometimes dramatically. (An example: the Siemens communications division, which required a strategic market analysis after German reunification, provided a negative example of a misleading national internal view. To this end, the leading market supplier Siemens teamed up with its market-dominant customer, Deutsche Telekom. The “consensus result” of the two partners ignored the emerging Internet-based package switching technology. The U.S. competitor Cisco prevailed on the world market with this technology and Siemens had to withdraw from the communications industry.) In this respect, it is particularly important to install early warning systems, to know early alerters and to listen to them. Such “alerters” are most likely to be found in companies positioned quite differently in the (relevant/related) market and pursue highly innovative concepts. For this purpose, it is advisable to set up appropriate networks staffed with “external” people. These can also be researchers [38].

6.3. Modeling Informational Transformation

In the following, a generic model framework for transformations to “Industry Generation 4.0” for manufacturing companies is presented for discussion. This is an attempt to place the paths to this transformation in an operationally oriented system.

A management cockpit consisting of six instruments is used as a basis for steering and controlling. These instruments are used in parallel:

- (I)

- Scope and Goals [39]

A project for the transformation to “Industry Generation 4.0” belongs to the category of fundamental corporate restructuring projects that encompass process organization, organizational structure, competence management, leadership structures, (hard) action programs and cultural change.

Before deriving the goals, the perimeter of the company under consideration must be defined, because size, business breadth and depth of value creation define the earnings potential. Uncertainties in this determination and subsequent changes must be eliminated or corrected during the ongoing work process. (Experience shows that there are often serious omissions here because corporate activities are not recorded correctly. For example, non-core business and regional specifics are often not recorded.)

Before the start of the project, the objectives must be derived based on an outside-in analysis, i.e., in concrete terms, on the basis of a dynamic analysis of the following environment:

- Market today (customers, competitors, suppliers…).

- Drivers for change (technologies, behaviors, market definitions, new players, mergers, fundamental power shifts and changes in the environment, e.g., environment, energy, new evaluation criteria such as ESG (Environmental, Social, Governance) and new evaluation methods [40]).

- Extrapolations to a thus “dynamized” future scenario for the period in which the new corporate model is to be applied (i.e., determination of the period, e.g., time horizon 5–10 years, determination of the dynamizing factors with their size and insertion of the same in the calculation of the future scenario).

- Scenario-based determination of the forces and market positions of leading players in the future market.

- Derivation of the own forces and market positions to be achieved in the dynamized future scenario.

- (II)

- Business Plans

Dynamized top-down objectives in milestones according to time horizon, for the business activities defined according to the perimeter. Nota bene: This can also be used to specifically exclude non-relevant activities. (Hiding is useful where management authority has been relinquished, e.g., outside the scope of consolidation, contract manufacturing based on external specifications, joint ventures in minority positions, support functions performed by third parties.)

Segment plans, where appropriate, each with objectives as above, so that the segment objectives can be consolidated “bottom-up” to the overall objective mentioned above.

- (III)

- Action Plans

Action plans per segment and as needed below. This includes the action plan, consisting of “hard” (thus also financially assessable) measures.

- (IV)

- Culture and Communication

So-called “cultural alignment”, which means motivating and driving behavioral change at all levels and in all functions so that the action plans to be developed ideally become self-perpetuating. This includes a high degree of identification of the participants with the goals, with company-wide and cross-functional overall goals taking precedence and functional sub-goals and support goals being put behind.

Any cultural change requires preparatory and follow-up communication at all levels and in all sectors. In all cases, this needs to be multi-directional, i.e., top-down versus bottom-up and across the organization in different directions. The respective “communication campaign” is not considered complete until all stakeholders have agreed. Forms of unalterable digital documentation should be found for the approval and person-specific commitment. The priority is to achieve the highest possible quality of the goal and the consensus. The time and effort required for this are secondary. In this respect, the time intervals between the defined milestones should be flexible. Priority is given to quality, consensus and securing commitment (documented voluntary commitments).

- (V)

- Teams and Terms

In terms of the transformation discussed here, this is the most important instrument of the cockpit presented. Figure 3 presents a highly simplified “generic” picture of a company organization according to its structure, core process, management structure, value streams and data streams.

Preparatory fit of the organization: The circular shapes indicate the levers to be typically applied for transformation. This is to be determined and combined differently from company to company. As already mentioned, companies with a lower degree of verticalization are better suited to implementing transformations. Consequently, organizations that are as flat as possible are to be preferred. If there is a need for preparatory action in this regard, opportunities for horizontalization should be sought, such as the juxtaposition of organizational units that were previously nested. The resulting increase in management span of top management with the corresponding increase in work and presence in the company can be compensated for by hierarchical mergers at the top levels as well, such as harmonization of the executive board and management. Certain differences in rank and function should be regulated in employment contracts, but these should not permit renewed “verticalization through the back door”. Rather, the top management team should be emotionally and contractually bound to each other by a common “mission & vision document”.

Disruption management: Disruptions can occur at any time, but they should be resolved to the best of their ability in the processes of struggling for the new. In the case of an accumulation of disturbances, however, it can become unavoidable that disruptors and disruptive structures (also insider relationships…), which oppose the agreed change, must be eliminated before too much energy is wasted and perhaps even the agreed overall goal is corrupted. For this purpose, rules and instruments must be kept ready in advance to lead such forces out of the “organization of change” without loss of face and injury.

Crystallization cores: The circular shapes shown in this figure localize most of the drivers of change to be found in today’s world. These can be used in almost any combination and can also be reconfigured over time as needed. There is a lot of individual experience available on which crystallization cores were used in which cases, in which form and how successfully. The specifics of the reported cases, however, only reveal certain measures of generally valid rules for success. Interestingly, these experiences are similar to those made in completely different types of reorganization projects:

- The more far-reaching the conversion, the more difficult it is.

- The more far-reaching the conversion, the higher the increase in value and the longer the positive prospects.

- Project types based on experience patterns and the more common ones have higher potential for success and involve lower risks.

- The more dissimilar the partners to be brought together, the more difficult and the higher the risk of a later rupture. (These are transferred results after evaluations at Siemens AG from strategy projects at the corporate level and mergers and acquisitions (M&A), for which the author had worldwide responsibility until 2008.)

The forces for change described as “crystallization cores” in the figure are briefly characterized below.

- Add-on, e.g., startup

A typical path to change is to merge with a startup. The main reasons for this are found in activity types (overlaps/additions/complementary competencies…) for resource bundling (access to funding for startup/access to competence bearers, especially to IT staff for the company to be transformed/strengthened to improve the position in the race for new developments vis-à-vis the competition…) and for cultural learning (learning promising behaviors and work structures from each other/exploring stress limits through differences/developing migrations to new and promising work models…).

In most cases, this model is applied in the form of test projects and individual projects which, in the best case, turn out to be promising and can be “attached” to the existing organization. In the optimal case, this model can also be transferred to the wider organization of the company in transition and penetrate the entire organization more or less deeply.

Experience shows that the proportion of such pilot projects that lead to sustainable success is relatively low, because working methods, motivations and the forms of incorporation into the organization do not fit. A central reason for failures are “imposed” goals and milestones that correspond to the basic pattern of the parent company but do not meet the expectations of the “young entrepreneurs”. (A few years ago, the author was called in to assess M&A projects by a leading German IT group. Out of 10 “classic” acquisitions, all 10 were classified as “successful”. Of 10 mergers with startups, all 10 were classified as “not promising”. Here it turned out that the success criteria for the startup collaborations were borrowed from classic M&A and were therefore inappropriate. After changing (fitting) the criteria, half of the startup cooperations could be classified as “promising in perspective”. At the same time, the time horizons for the necessary migrations had to be extended considerably.)

The “hype” about startup mergers with medium-sized companies has died down in the meantime. In contrast, successful direct transfers of startup founders and employees to medium-sized companies are more common. In addition to the rather weak success rate of this migration model, the time required to penetrate an entire company is high, so this model is only suitable as a pilot and as a supplement to a top-down approach to managing change [41].

- Buying-in digital business

This describes the “classic M&A path”, namely the acquisition of a digital-driven company by a strategically operating company with a long-term focus (so-called corporate, i.e., less applicable to private equity, which is usually already planning its exit at the time of the acquisition).

Here, the typical M&A processes and work stages come into play. The most important is the entry into the project with the help of a candidate screening, which in the field of digital business approaches is extremely broad, time-consuming and highly updating. Thus, M&A databases can contribute rather little. Most of the data gathering and analytics must be executed in a timely manner by in-house teams. Frequent buyers generate their own target data beacons, which must be constantly updated and adapted to the changing target search. The number of candidates to be captured in an international search can range in size from tens to hundreds of thousands of potential companies.

Integration usually follows the “hang-on” model in the existing organization. Because of cultural and national differences, such integrations are not easy and are “lost” if the hang-on is too low and if management pays too little attention.

A special case is when, due to the low availability of free IT specialists on the labor market, entire IT companies are purchased to then completely dismantle them and assign the individual employees to various organizational units. In terms of costs, this can pay off. However, the risks of dismantling are high, legal hurdles (e.g., § 613a) must be considered and the risk of loss of employees who feel deprived of their colleague network is high.

- Regional acquisition

This is another M&A path, directed at a target region where digitally driven business models are more entrenched and where a suitable pool of companies can be found to choose a target. Strategically, this path would be classified as “diversification or business expansion on a regional level” and typically applied in the Far East, for example.

From such a newly attached unit, which can also be launched as a “trial balloon” according to size and orientation, a new core business can be gradually developed—as in an upgrading process—which even has the potential to substitute older business approaches.

Such a path can turn out to be tolerable for the company because initially it is sufficiently far away from potentially threatened established businesses in the parent company’s region and because such a business can develop well under special “digital-ecological” circumstances. Once this has reached a certain size and a certain threshold of earning power, the proof of success is also given to critics within the company. Once this model has proven itself, further attempts can follow.

- Developments ex IT competencies

Another direction of development is offered by IT competence centers. These can be close to the CIO, more likely to be assigned to IT administration (e.g., for master data), to hardware and software development or to IT service providers. In all of these cases, the key lies with the IT specialists already embedded in the company, who (a) on the one hand, bring specific competencies with them that experience in recent years has shown to be suitable for new management approaches, and (b) are most likely to be able to build bridges between “old” (knowledge of and understanding for outdated business approaches) and “new”: through their own visions and ideas, as well as through their connections to developers and founders.

The specific use of this resource enables simultaneous “Industry 4.0” penetrations of companies at various points—including the possibility of using such IT competence carriers specifically as ambassadors across the company.

- Crystallization centers

In addition to IT, there are many crystallization centers that are suitable for highly innovative business approaches. These include permanently established specialist and staff departments that are predestined for innovations due to their degree of specialization. Temporary project organizations are also suitable—especially if they bring together different competencies from different organizational units, for example, for business development, investment fields, venture capital and basic research. These are particularly noteworthy when it comes to completely new approaches to solutions. These often hold the key to business innovations. They can be triggered by the overall organization committing to higher innovation frequency and having the appropriate tools in place to do so (e.g., measurement at departmental levels, innovation competitions, publication of benchmarks, bonuses, team building across the organization, linking top-down to bottom-up initiatives…).

- Board and management levels

The aforementioned solutions can be used individually or in combination, triggered by senior management, at workshops in factories or through the operational improvement system. Ultimately, the lead-up to an “Industry 4.0” organization is the responsibility of the top management levels. Depending on the size and breadth of the company’s setup, this means the board level plus its managing directors as the second and those responsible for the operational business (divisions, regions…). Because of the many special transformation tasks, this team should be of a certain size, conceivably at least 5 to 15 people, to be able to assign the necessary responsibilities personally. The operative management level must ensure access deep into the organization and thus also prevent (!) that detached decisions are made far away from the business.

Ideally, a coach is appointed for this purpose and assigned a corresponding initiative and leadership role. The CEO can “take” this role (in accordance with management regulations). The entire executive board can dedicate itself to this task as a “top team” and also appoint a “transformation coach” who will be actively and continuously involved personally and at the same time serve as a central contact person in the company. Because of his/her professional qualifications, it makes sense to entrust the chief information officer (CIO) with such a task. The CIO should be a member of the top-level transformation committee, whose members work together as colleagues on an equal footing.

- Network organization

The top team presented, consisting of the aforementioned management levels, should see itself as the driver of a network for implementing the transformation, which is placed on the company as a flexibly positioned “overlay organization”. This network must permeate the entire enterprise by having its named members drive transformation workshops and other initiatives at all levels of the enterprise, in all business segments, at all stages of the value stream. The named (primary) network members ensure that working groups, workshops and other activities occur. The “primary circle” should be allocated a contingent of their working time in which they dedicate themselves to the transformation task. Additional members should be brought in so that larger teams and initiative groups can be formed and meet regularly.

The transformation network must link all transformation activities with each other and can also present individual of the presented paths/models (e.g., startup cooperations) as examples for discussion.

As a brace function and for overarching cohesion, regular town hall meetings for the entire workforce should be scheduled by the management level. A milestone program could provide the clocking for this.

All channels and media of communication should be used; in addition to the face-to-face meetings mentioned above, in-house newspapers, programmatic notices in plant halls, an intranet site, Q&A forums, videos and podcasts are all suitable for this purpose. A special editorial department should be created in the communications and press department for this purpose, in which all productions are coordinated, timed and their content coordinated.

A comprehensive and coordinated stakeholder management system must be developed. This covers not only all internal forces, friends and families but must (!) also be directed to the business partners (customer, suppliers…) and to the general public (press, local representatives, politics,…). Depending on the size and importance of the company, higher levels (district associations, federal state, federal government, international alliances) should also be addressed.

This is not just about informing the immediate or wider environment, but to a much greater extent about a kind of reflection: employees want to know how “their” company is seen from the outside. A positive external image reinforces and confirms their commitment, and they feel appreciated as fellow activists. Pride in one’s own company is an important motivator.

Highly differentiated time management also contributes to success. Messages must first (!) be exchanged within the respective innermost circle, then across the breadth of the company, and only then (!) externally—possibly in cascades to meet external expectations. For example, the mayor might want to be informed about important information firsthand before the department heads are involved. All this can be exercised with military precision with hourly cycles and under role allocation (e.g., who contacts who on the board?). For this to be safe and repeatable, the processes should be standardized and backed up with IT.

- Evaluation

The model presented here should be understood as a generic framework and adapted to each individual case. A fundamental transformation belongs to the most demanding and highest project category that a company can undertake—on a par, for example, with a full takeover by and merger with another company. The change can lead to a kind of “rebirth”. The highest level of attention, the most precise target management, high commitments, the involvement of everyone and the use of a complete set of instruments are called for.

7. Comparison: Empirical Values and Recommendation

This section supplements the operational side of the digital–informational transformation discussed so far with its financing and the management of risks. Because with every fundamental reorientation of a company, special risks arise as a result of temporary uncertainties. After all, the entrepreneurial principle of maintaining the balance between stability and change must always be observed. Stability is often understood as maintaining the status quo. However, in times of great upheaval in the environment, this can pose existential threats to a company. Too radical change can cause losses of corporate identities, employees and established customer relationships. Therefore, even so-called disruptive changes should be approached with caution. The timing is crucial: both when fundamental changes are initiated and at what speed they must be implemented. As shown in Section 6, various generic management models are available.

Potential for improvement: Digitalization in conjunction with networking undoubtedly unlocks enormous potential in terms of cost savings, acceleration and avoidance of work that does not create value. In a recent survey of European companies, most cited increased efficiency as an important benefit resulting from the use of innovative technologies in production. European decision makers also cited potential cost reductions and improved product and service quality as other benefits.

Hurdles: When asked about reasons for the progress of transformation to date, the majority of decision makers in all European survey countries cite the factors of time and money. This assessment cuts across all company segments and is mentioned in every third survey. Around one in four also cite IT security concerns, incompatibility with existing machines and data protection regulations as major challenges in their own company transformation.

Costs and pricing: Motivated by the realization that they cannot bring Industry 4.0 into their own organization on their own due to a lack of expertise, budget or capacity, European company leaders are consciously relying on partnerships. When selecting technology providers, flexible and simple pricing is the most important criterion for one in five companies. The focus is on the ability to flexibly adapt services to specific needs at comprehensible prices. Also particularly important are the aspects of security and the provision of advice and support as well as professional services.

Return on investment expectations: Organizations that focus on innovation or internal transformation report increases in their return on investment. Companies in advanced stages of transformation had invested just over one-fifth of their total revenue in digital projects. The result was profitable growth. Their EBITDA (earnings before interest, taxes, depreciation and amortization) grew by 12.2 percent from 2017 to 2019. By contrast, the EBITDA growth of the other companies in the DACH region shrank by 6.2 percent [41]. Cross-functional collaboration is neither a goal nor a means to an end. Rather, it should be a key organizational and strategic imperative for leaders who want to drive digital transformation. Effective collaboration across functional boundaries not only reduces unnecessary effort and costs—it also leads to measurable improvements in returns [33].

It is almost impossible to put a general figure on the potential savings from the transformation of companies. Nevertheless, individual consultants dare to make overarching statements. According to Accenture, “The optimal technology mix could save large companies up to $16 billion. And yet, only 13 percent of companies have realized the full impact of their digital investments, achieving cost savings and creating growth [41].”

Rules: Companies that have successfully restructured according to Industry 4.0 criteria differ significantly from their non-transformed competitors in several ways:

- They make it clear to function holders what digital transformation means for the organization and why all functions should work together.

- They hold executives accountable for how well they collaborate across organizations in digital transformation projects.

- They prioritize projects that foster cross-functional collaboration.

- They invest in platforms that enable seamless collaboration and scale them rapidly. IT island solutions have become a thing of the past.

- They define clear rules for their information technology and operational processes and make transparent how the two mesh [41].

Risk assessments: The implementation of “Industry 4.0”-based leadership and management concepts to date revealed that the problem lies not in recognizing the benefits and not in the lack of “golden rules” and the lack of advice disseminated via relevant institutions, via ministries and consulting firms. Rather, the crucial problems lie in operational implementation, from the board to the store floor. In addition, it can be observed that mistakes and dead ends that companies run into lead to disappointment and frustration at a variety of levels and across organizational units, so that companies abandon the digital transformation due to exceeding deadlines and budgeted resources, even after part of the implementation process, and even row back when they have to recognize that there are signs of division in the company, that values are being destroyed and that the operational business is being jeopardized.