A Review of Blockchain in Fintech: Taxonomy, Challenges, and Future Directions

Abstract

:1. Introduction

1.1. The Fintech Ecosystem

1.2. What Is Blockchain?

Public vs. Private Blockchains

1.3. Related Work

1.4. Research Methodology

1.4.1. Research Questions

1.4.2. Screening Process and Resources

- Google Scholar

- Scopus

- Web of Science

- IEEE Xplore

- ACM Digital Library

- Science Direct (Elsevier)

- Springer

- Fintech Reports from key financial institutions e.g., KPMG, JP Morgans, PWC, etc.

- Research statements from Central Banks across different countries.

- Medium.com articles from prominent opinion leaders in the industry

- Consensys (https://consensys.net/, accessed 15 March 2022)

- BlockGeeks (https://blockgeeks.com/, accessed 15 March 2022)

- Eth.research (https://ethresear.ch/, accessed 15 March 2022)

- Enterprise Ethereum Alliance (https://entethalliance.org/, accessed 15 March 2022)

- Cointelegraph (https://cointelegraph.com/, accessed on 15 March 2022)

- Websites dedicated to projects discussed in this work

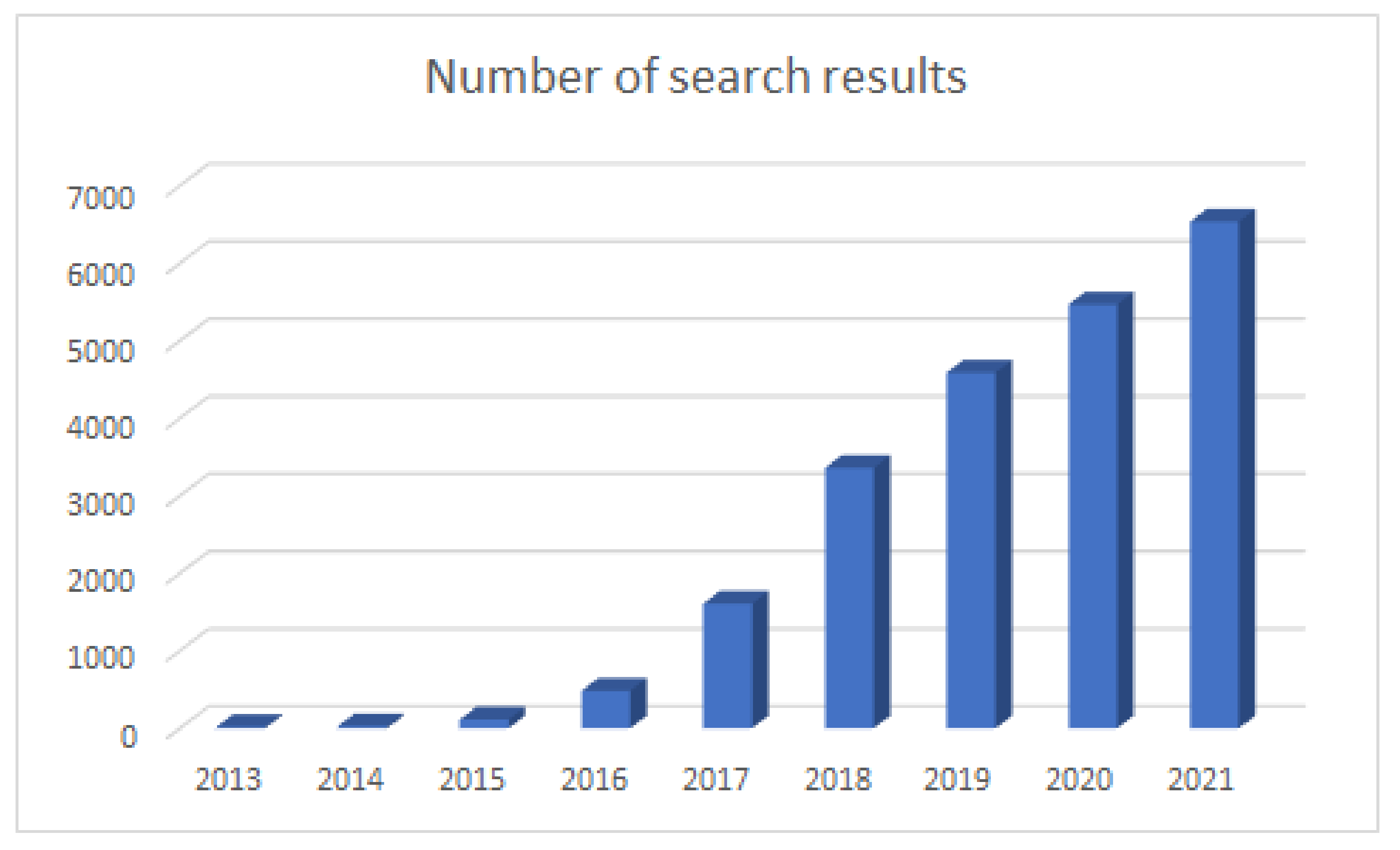

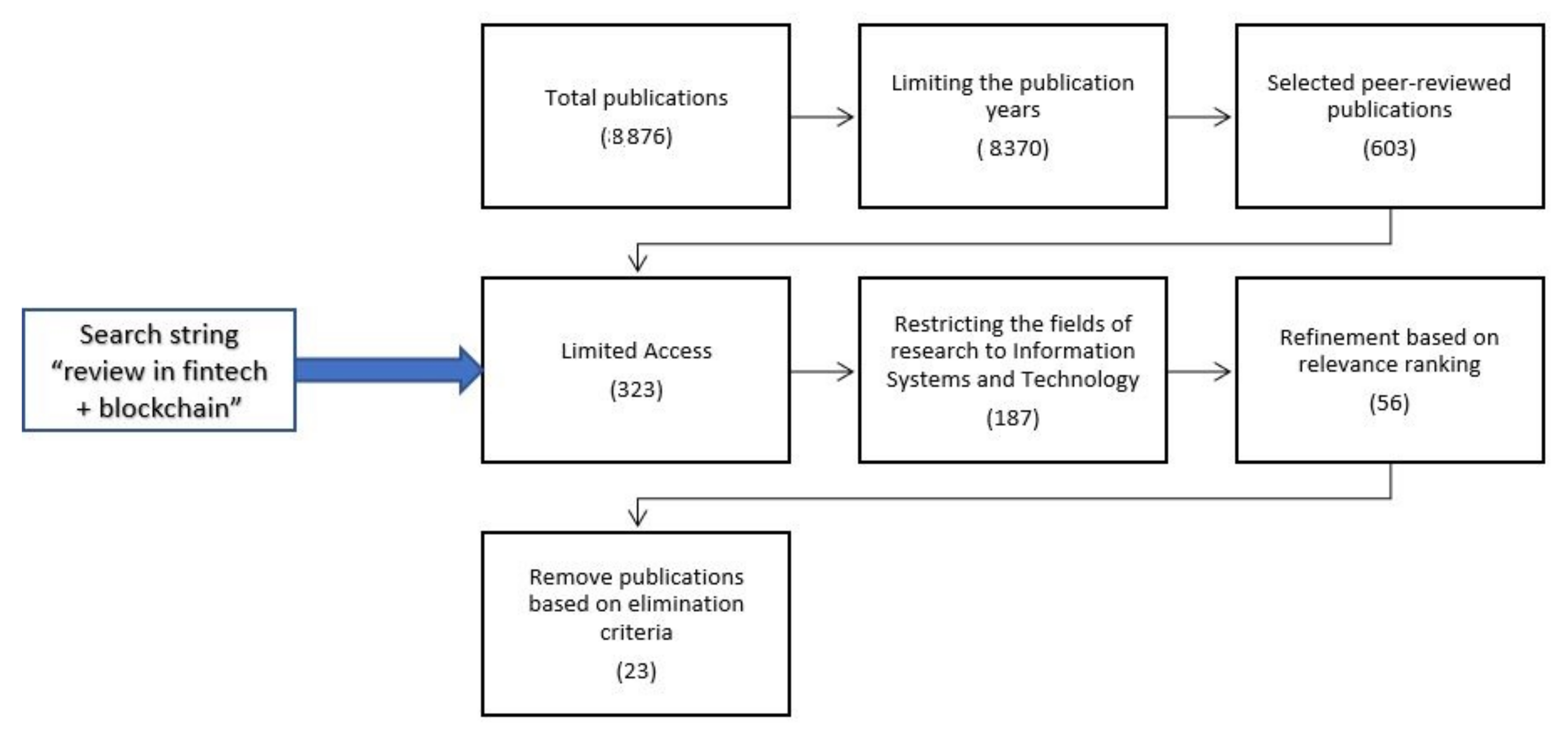

- Figure 2 shows the research trends on Blockchain for Fintech with the number of publications per year. These results are collected by querying “Blockchain for Fintech” from Google Scholar. It showed that the research interests for applying Blockchain to Fintech have been exponentially increasing since 2015. While there were only 18 publications in 2013 (five years after the introduction of Bitcoin), there were 6540 papers published in 2021. Similar pattern can be observed in other indexing sources as well. Hence, our first criterion was to restrict the publishing year between 2016 to 2022.

- Based on keywords found in the publications’ titles and abstracts. These keywords were determined primarily by compiling a list of all Fintech verticals, blockchain-specific phrases, and use cases. Some of the example keywords are listed in Table 1. The search strings were built by combining the keywords using connectors like AND and OR. For example, one of the search strings would be: (Fintech OR Payments OR Banking OR Lending) AND Blockchain.

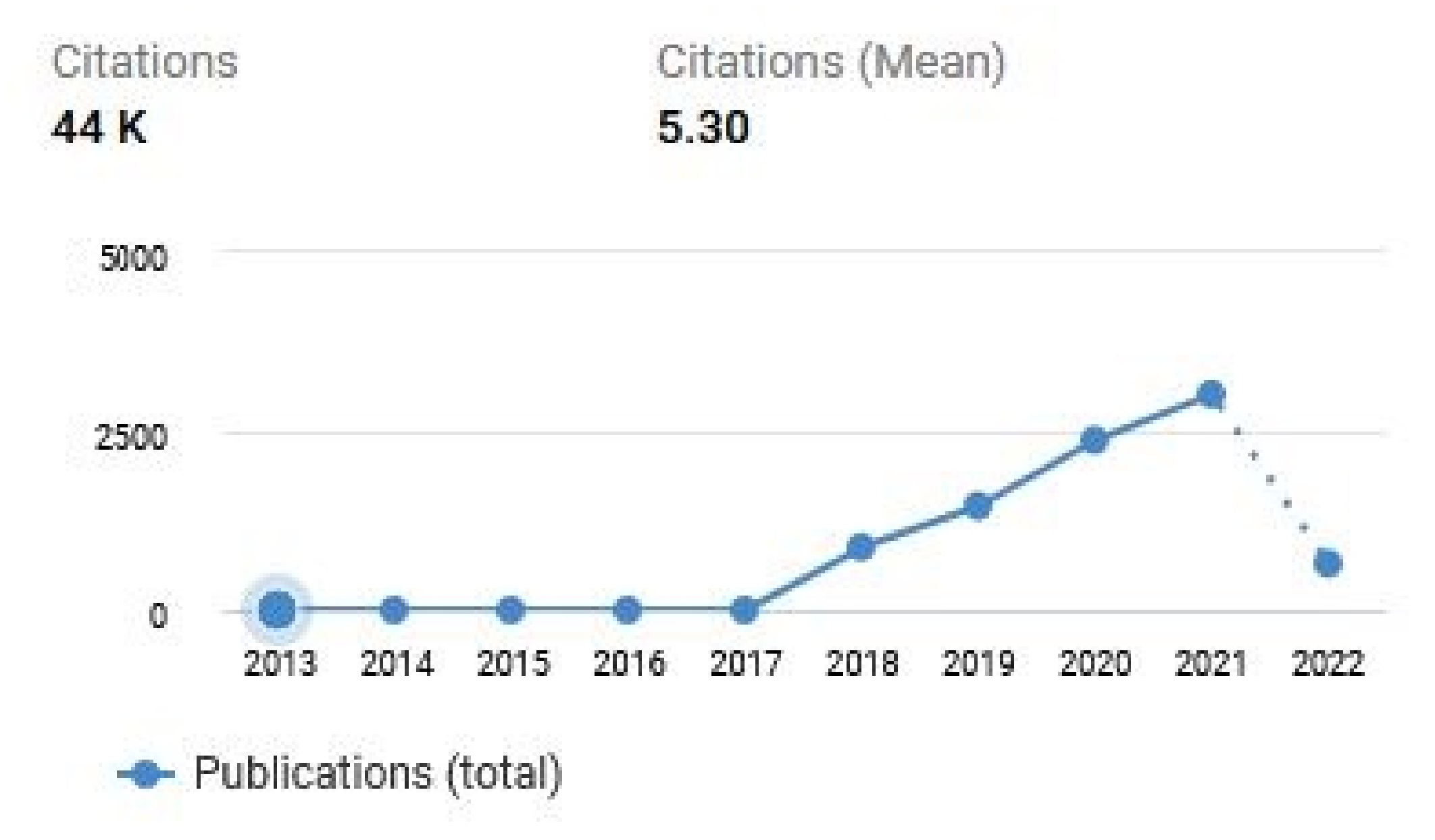

- We were also able to restrict the search results by citation count using a solution for information research datasets in Dimensions AI. We utilized the technique to identify extremely popular works in this field. This was accomplished by first searching the tool using various search terms and then selecting references with a citation count greater than 5 for each year beginning in 2018. Figure 3 shows the increase in the citation count for the works since 2013 with mean citation around 5.30.

- Additionally, Dimensions AI delivers a search rank based on the publication’s relevance. We chose resources with a rank greater than 100 for all search keywords.

- Apart from the search restrictions, we additionally eliminated several entries using the criteria listed below:

- (a)

- Papers written in other languages than English.

- (b)

- Master and doctoral dissertations.

- (c)

- Duplicated articles obtained from all four indexing databases.

2. Background

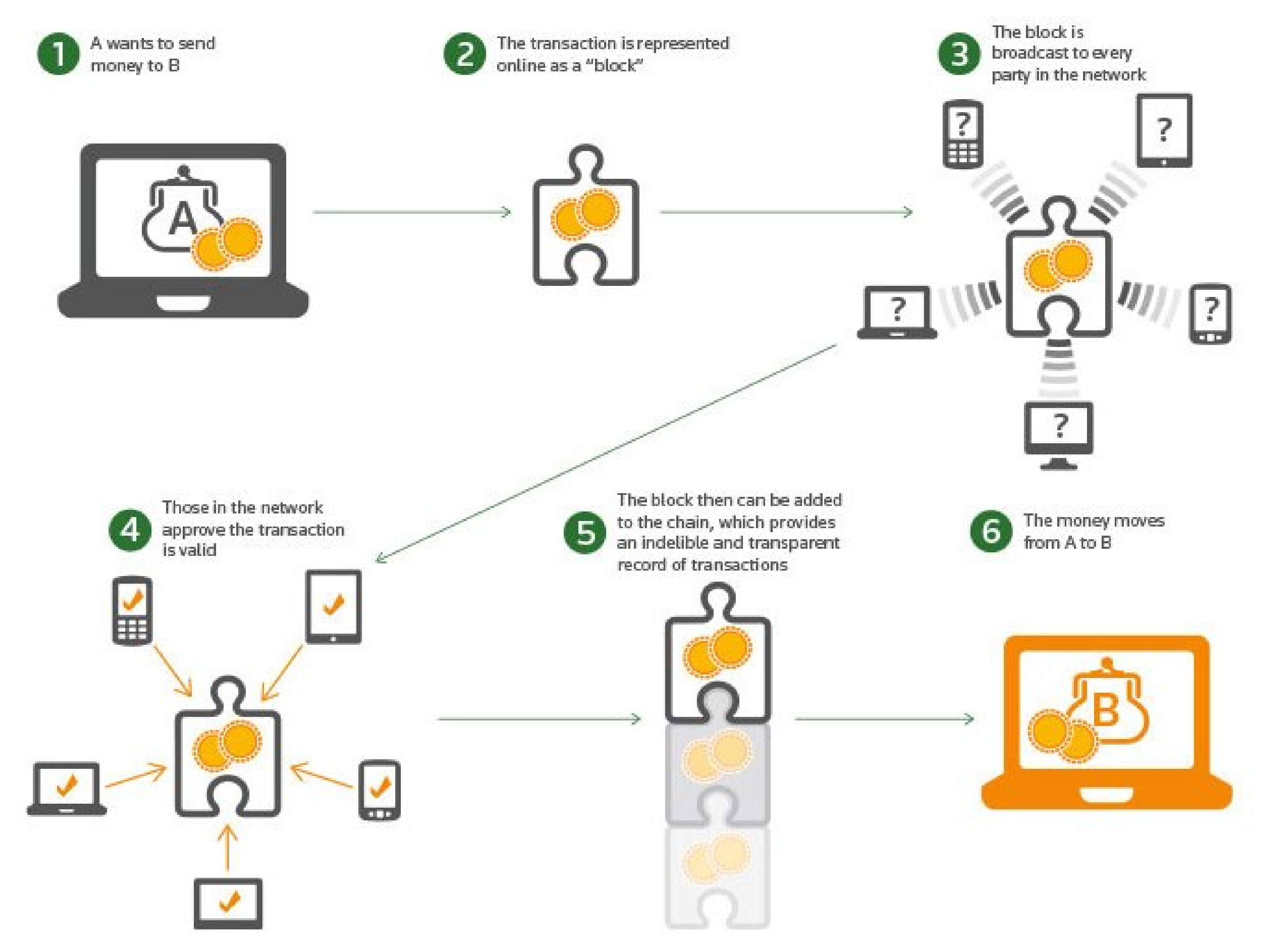

2.1. How Does a Blockchain Work?

- Cryptography: In the first blockchain system, Bitcoin, the main purpose of cryptography is to provide the integrity and authenticity of transactions [20]. While the former is ensured by using hash functions [50], the latter is ensured by secure digital signatures [51]. The signatures play a double role additionally serving as an identity due to the properties of public-private key pairs. Only one who possesses the private key can generate a digital signature for a document. This digital signature hence ensures the strong control of ownership. In subsequent developments, with new found focuses around digital privacy, new cryptographic primitives such as special digital signatures [52], zero-knowledge proofs [53] or cryptographic commitments [54] have been developed to provide solutions in blockchain systems.

- Smart Contract: Bitcoin was initially designed for peer-to-peer (P2P) money transfer only. However, it soon showed the potential to be used for any kind of P2P value transaction on top of the Internet. The concept of smart contracts [55] was later introduced but ignited significant interest and popularity. Typically the contract layer is decoupled from the blockchain layer, where the ledger itself is used by smart contracts that trigger transactions automatically when certain pre-defined conditions are met. By decoupling the smart contract layer from the blockchain layer, blockchains like Ethereum aim to provide a more flexible development environment than the Bitcoin blockchain.

- A Distributed Network: Blockchain technology functions via a peer-to-peer network where information is stored in all participant nodes [20]. Validators (i.e., nodes) work come to a consensus about a fact witnessed by all parties in a common epoch. To secure the network against majority attacks, the network must have enough competing entities who are large enough to weather sudden arrivals/departures of competitors.

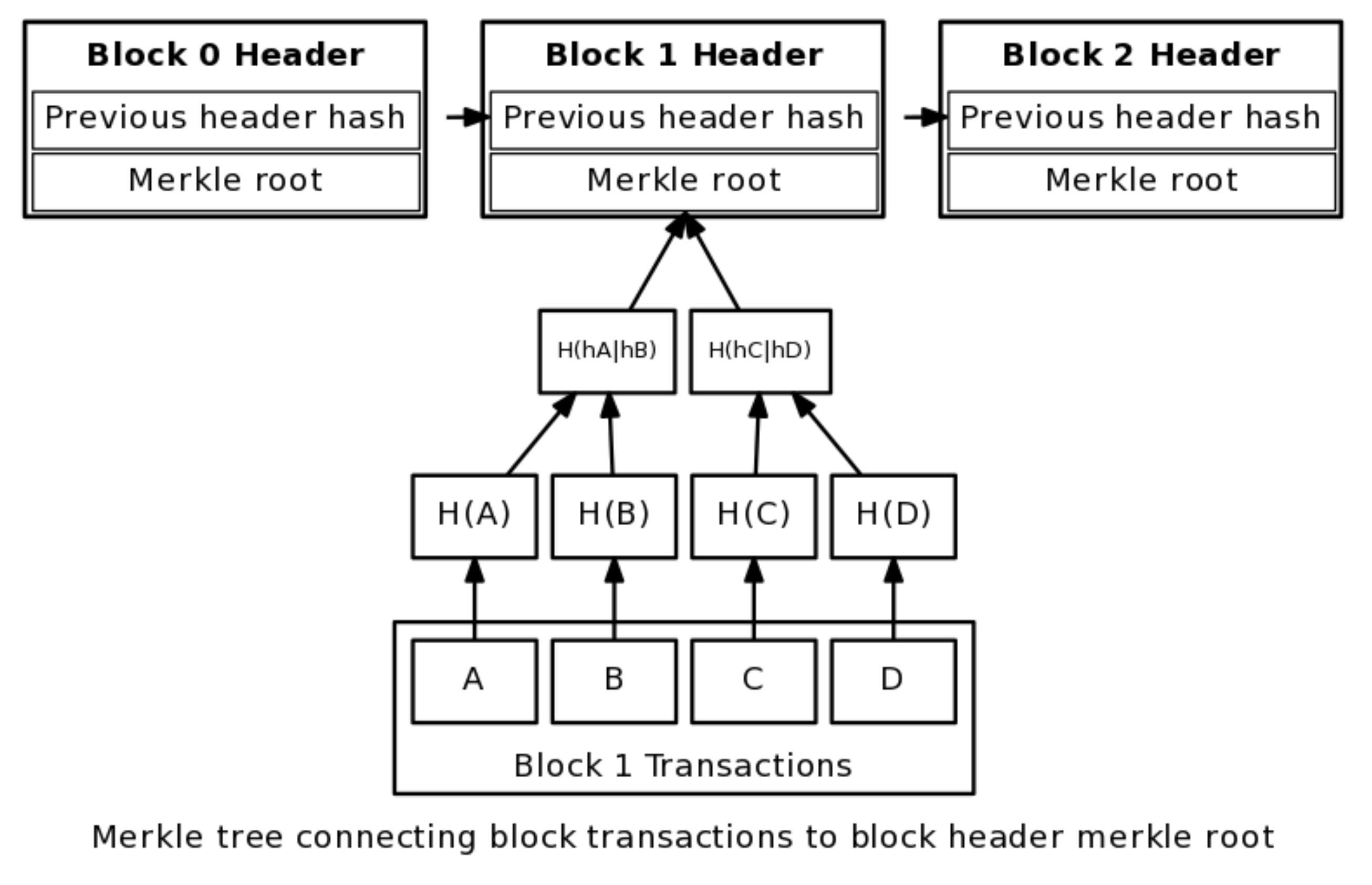

- Network servicing protocol: A block containing a list of transactions, a Merkle root value, previous block’s hash value, timestamp, etc., is broadcast to and maintain on participants in the network. Public blockchain such as Bitcoin usually offers an available reward for computing power that serves the network [20]. The nodes serving the network create and maintain a history of transactions by working to solve proof-of-work mathematical problems. More serving nodes the blockchain is more secure.

- First, the consistency of the global state is probabilistic. In most decentralised consensus mechanisms, it is not possible to determine which entity will update and solve the challenge next or at any given time. To obtain a good chance to be chosen as the next block’s creator, an attacker must own more than 50% computing power of the total network.

- Second, all transactions’ integrity and authenticity are protected by using hash functions and digital signatures.

- Third, consistency and correctness is enhanced because of the block history. Each block is chained by the hash of the previous block in the chain. Tampering with a transaction would make the hash value of all subsequent blocks in the chain wrong. This would be immediately noticed by other validators in the network who are continuously keeping verifying the transactions and refusing to accept transactions that are not consistent with the known longest chain.

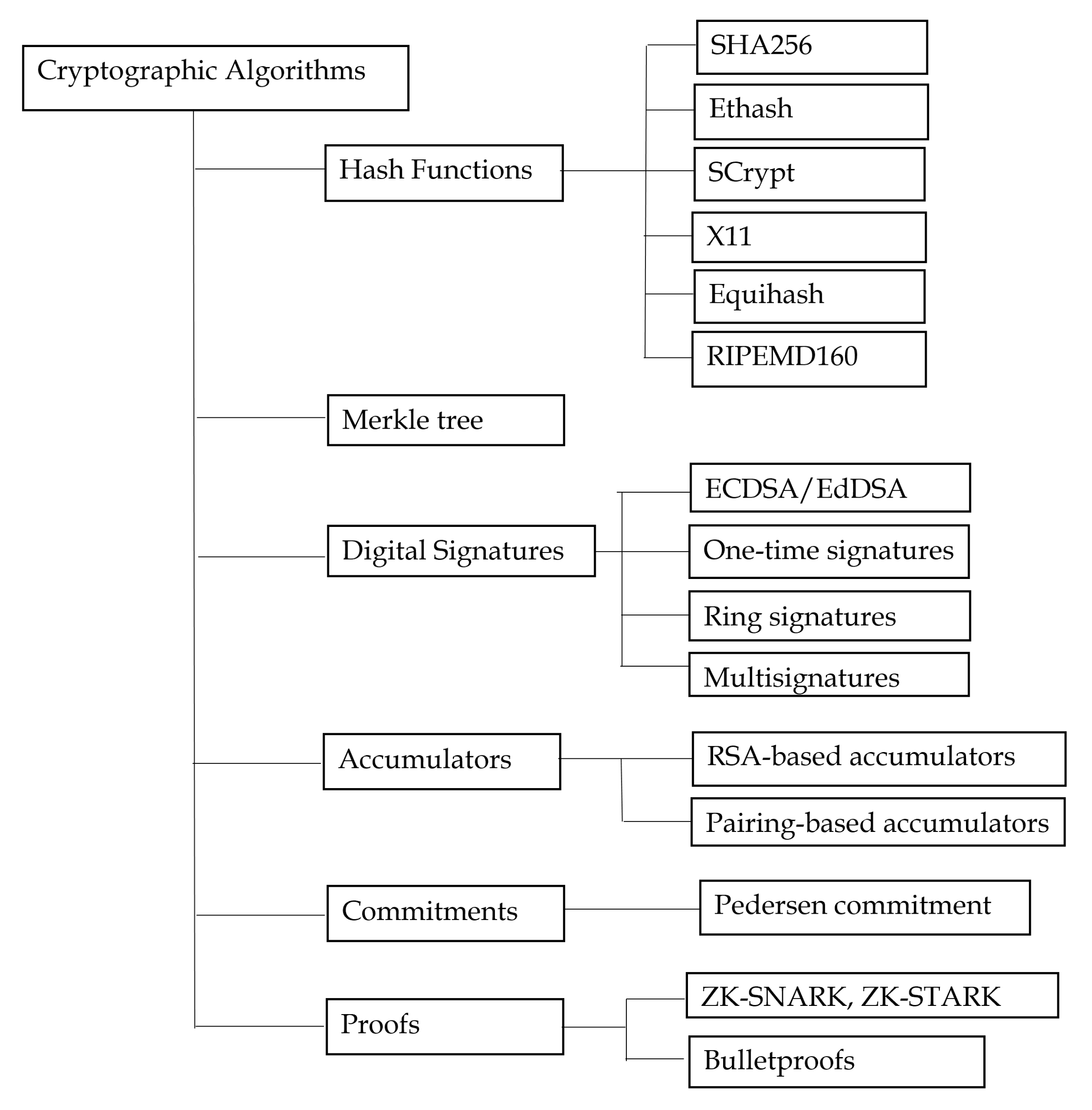

2.2. Cryptographic Primitives

2.2.1. Hash Functions

- First-preimage resistant or one-way: Given a hash value , it should be impossible to recover the message m.

- Second-preimage resistant: Given a message m, it should be infeasible to find a message such that .

- Collision resistant: For a hash function , it should be infeasible to find two messages such that .

- Zero resistant: It is infeasible to find a message m such that .

2.2.2. Merkle Tree

2.2.3. Digital Signature

ECDSA

Special Signatures

2.2.4. Accumulators

2.2.5. Homomorphic Commitments

- Hiding: one party wants to commit the message m without revealing the content of m itself.

- Binding: if one party makes a commitment to m, she/he cannot open it to a different message .

Pedersen Commmitment

2.2.6. Zero-Knowledge Proofs

2.3. Smart Contracts

2.3.1. Hashed Timelock Contracts

2.3.2. Cross-Chain Swap

- Alice generates a secret and sends the hash of the secret to Bob out of band while negotiating the details for the secure escrows on both chains;

- Alice generates an HTLC with her funds and the hash of the secret;

- Bob generates an HTLC with his funds and the hash of the secret;

- Alice reveals the secret to collect the funds from Bob’s HTLC thereby revealing the secret to Bob who also collects the funds from Alice’s HTLC;

2.3.3. Bridges

- Trusted bridges: These bridges are backed by a central authority that guarantees the integrity of the activities that pass over them. This means that users of this bridge must develop a relationship of trust with the entity that manages it. Multichain is an example of this sort of bridge.

- Trustless Bridges: These are bridges that are not controlled by a third party. Smart contracts or their own consensus algorithms regulate the bridge. Connext, cBridge, and Hop are a few examples.

3. Overview of Blockchain Platforms in Fintech

3.1. How Blockchain Transforms Fintech Industry?

3.1.1. Disintermediation

3.1.2. Immutability and Transparency

3.1.3. Timeliness

3.1.4. Cost Optimization

3.1.5. Privacy and Security

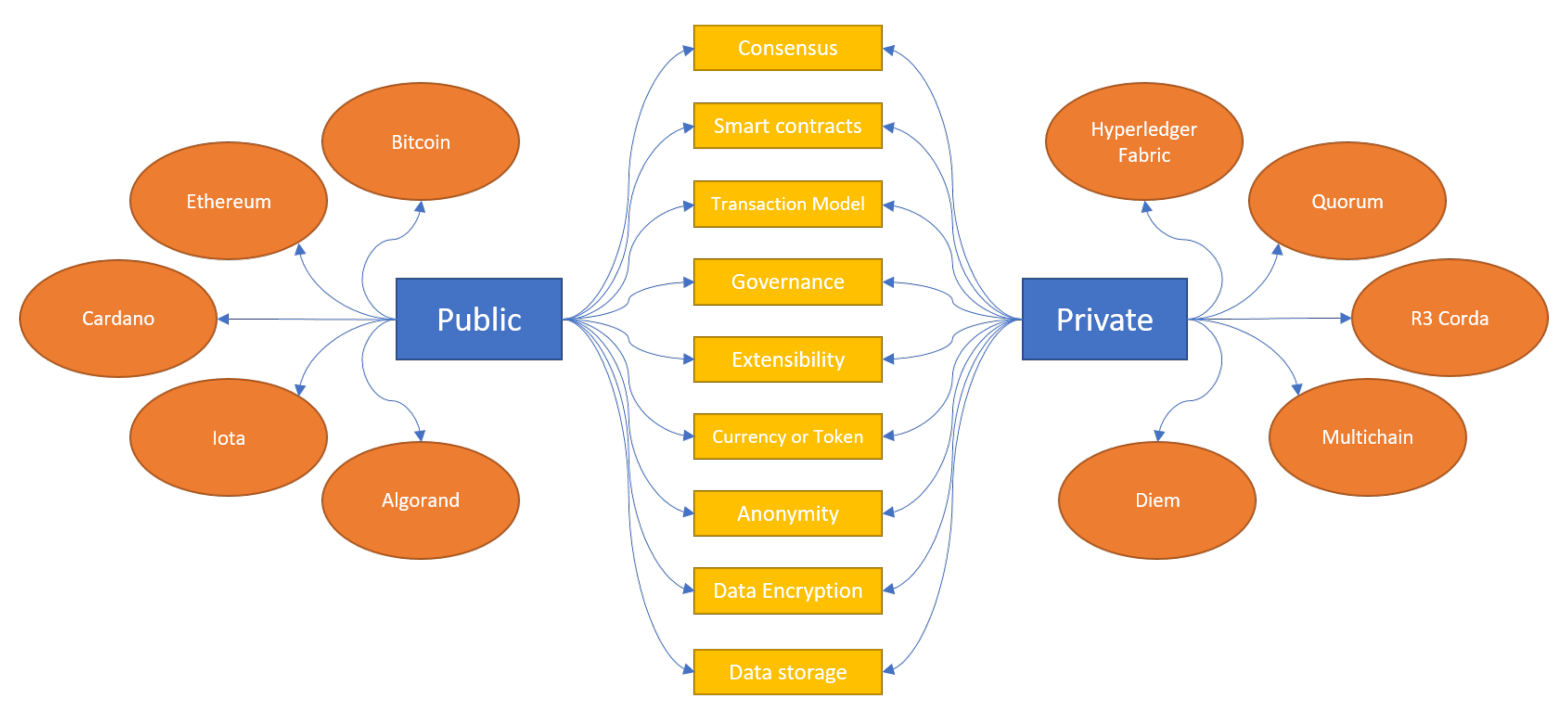

3.2. Classification of Blockchain Platforms

3.3. Comparison between Platforms

3.3.1. Bitcoin

3.3.2. Ethereum

3.3.3. Cardano

3.3.4. IOTA

3.3.5. Algorand

3.3.6. Hyperledger Fabric

3.3.7. R3 Corda

3.3.8. Quorum

3.3.9. Multichain

3.3.10. Diem

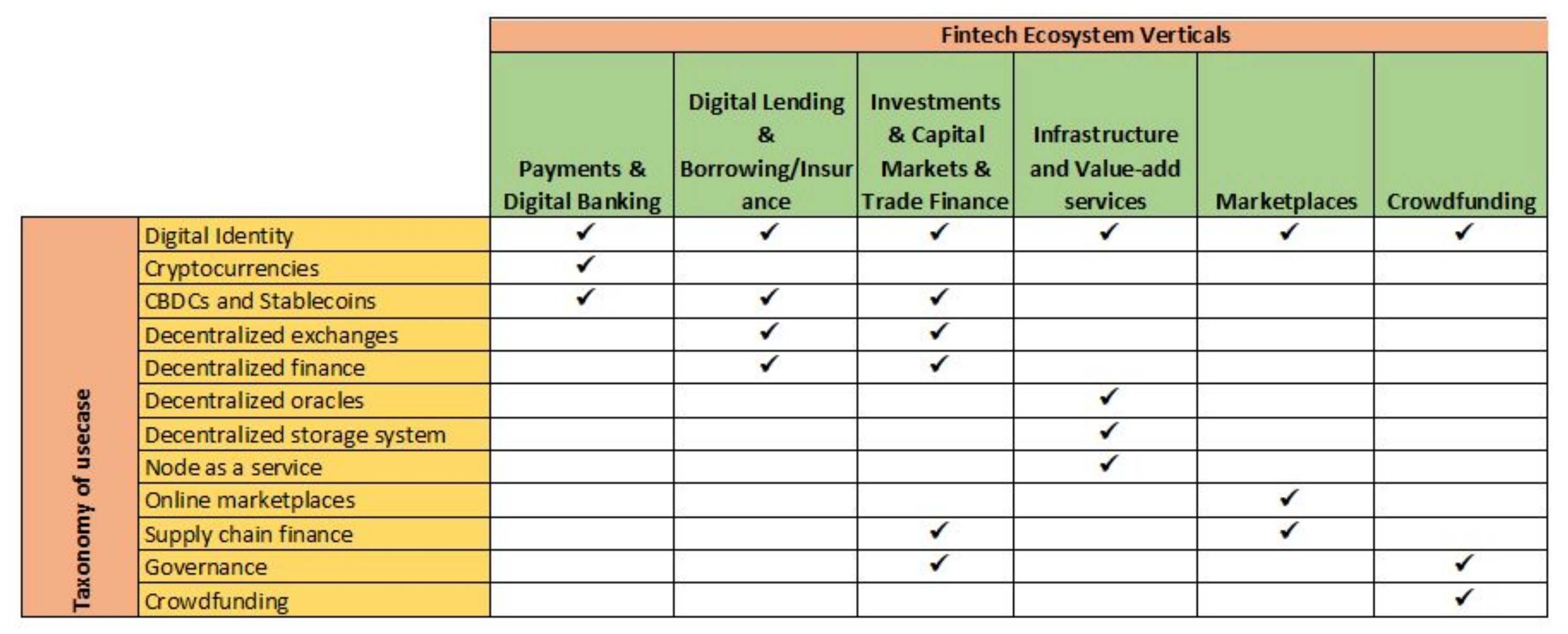

4. Taxonomy of Use Cases

4.1. Digital Identity

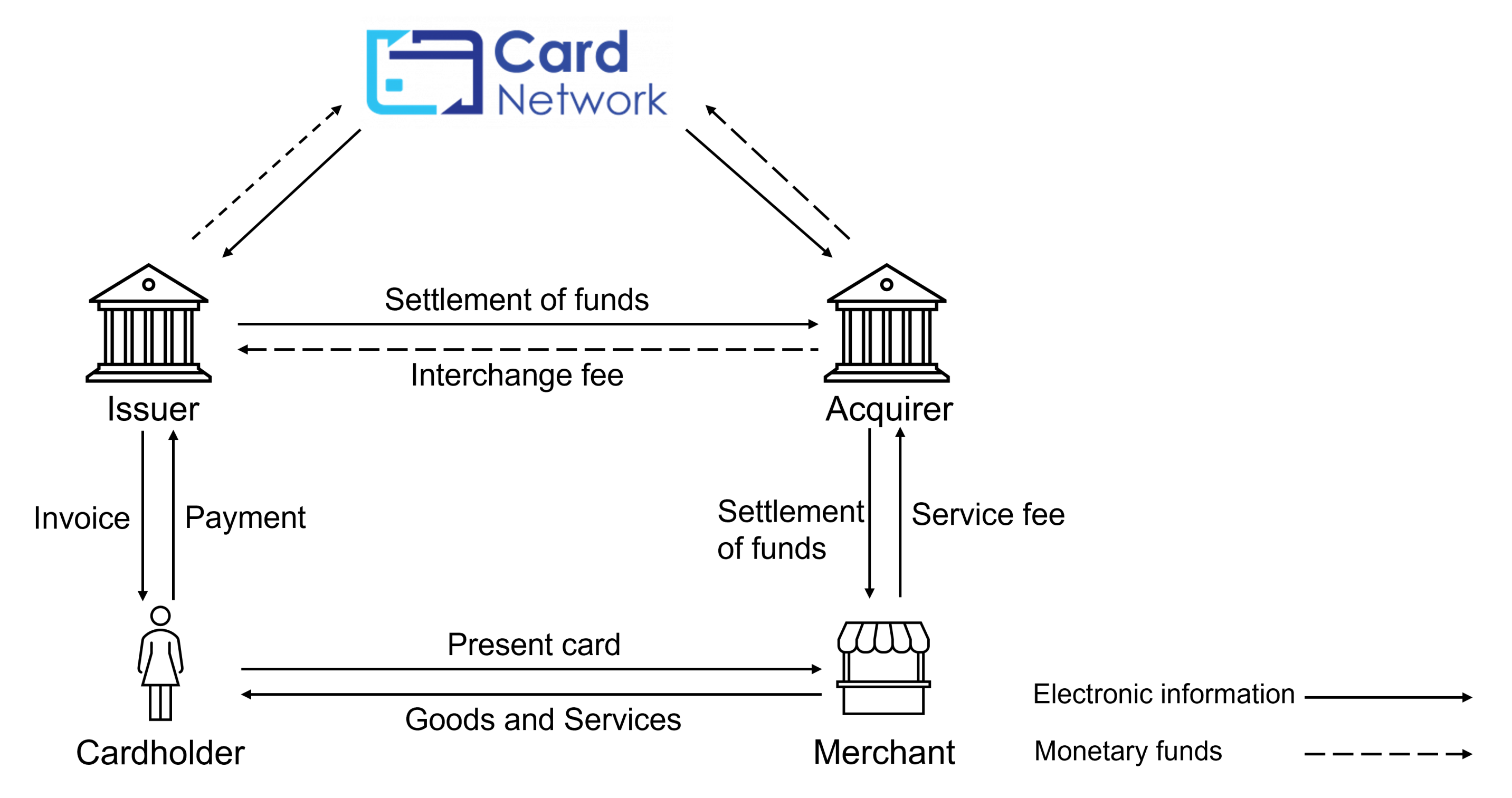

4.2. Payments

- Use an inherently privacy-preserving cryptocurrency;

- Atomically swap to a privacy-preserving cryptocurrency and transact there;

- Use a mixing service;

- Use an on-chain privacy token/service

- Reduce transaction fees

- Faster transactions, especially transactions performed across different countries

- Offer transparency and tractability

- Indisputable and immutable after finality

4.3. Digital Currencies

4.4. Investing

4.4.1. Decentralised Exchanges

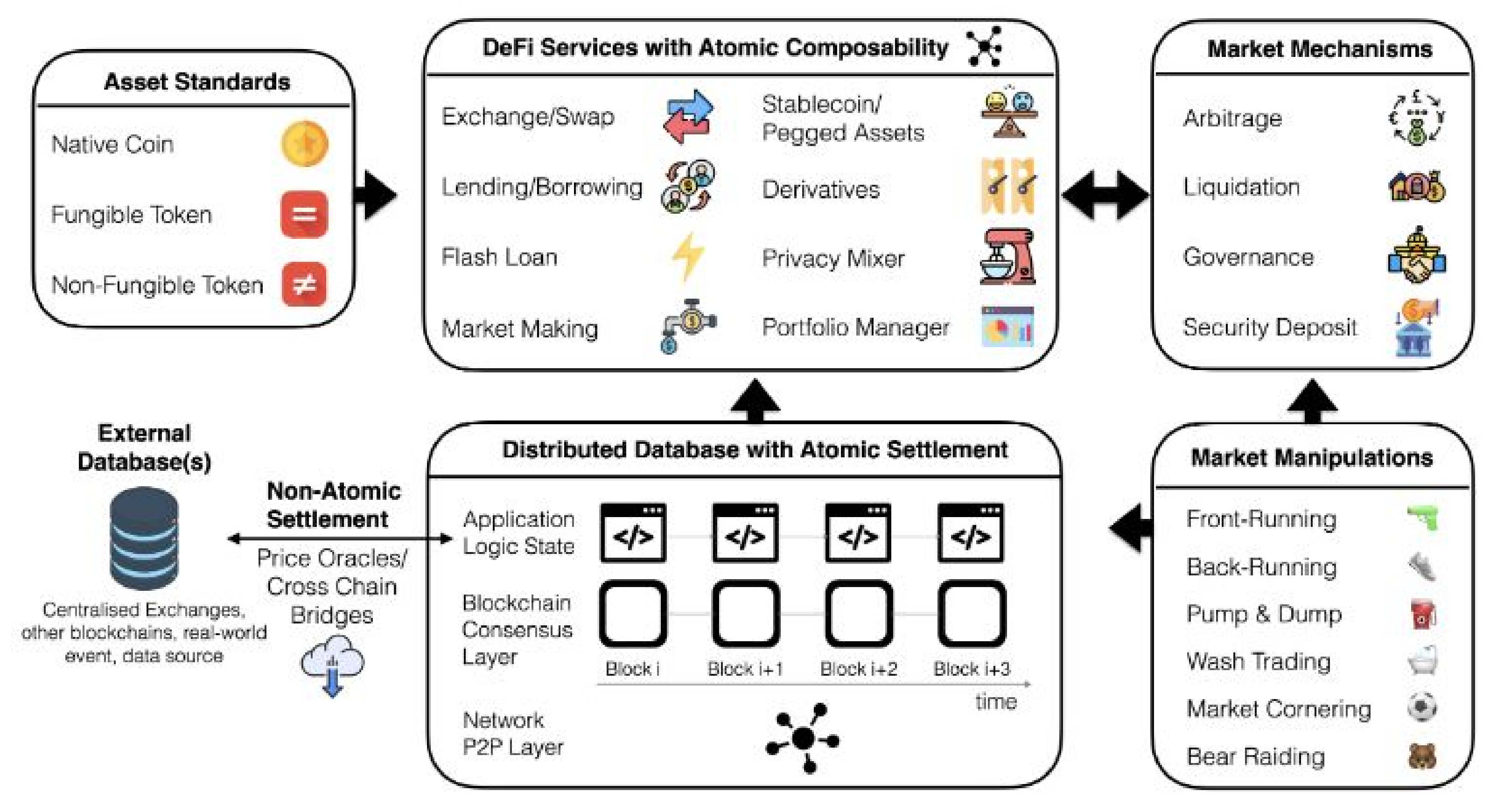

4.4.2. Decentralised Finance

4.5. Infrastructure/Value-Add Services

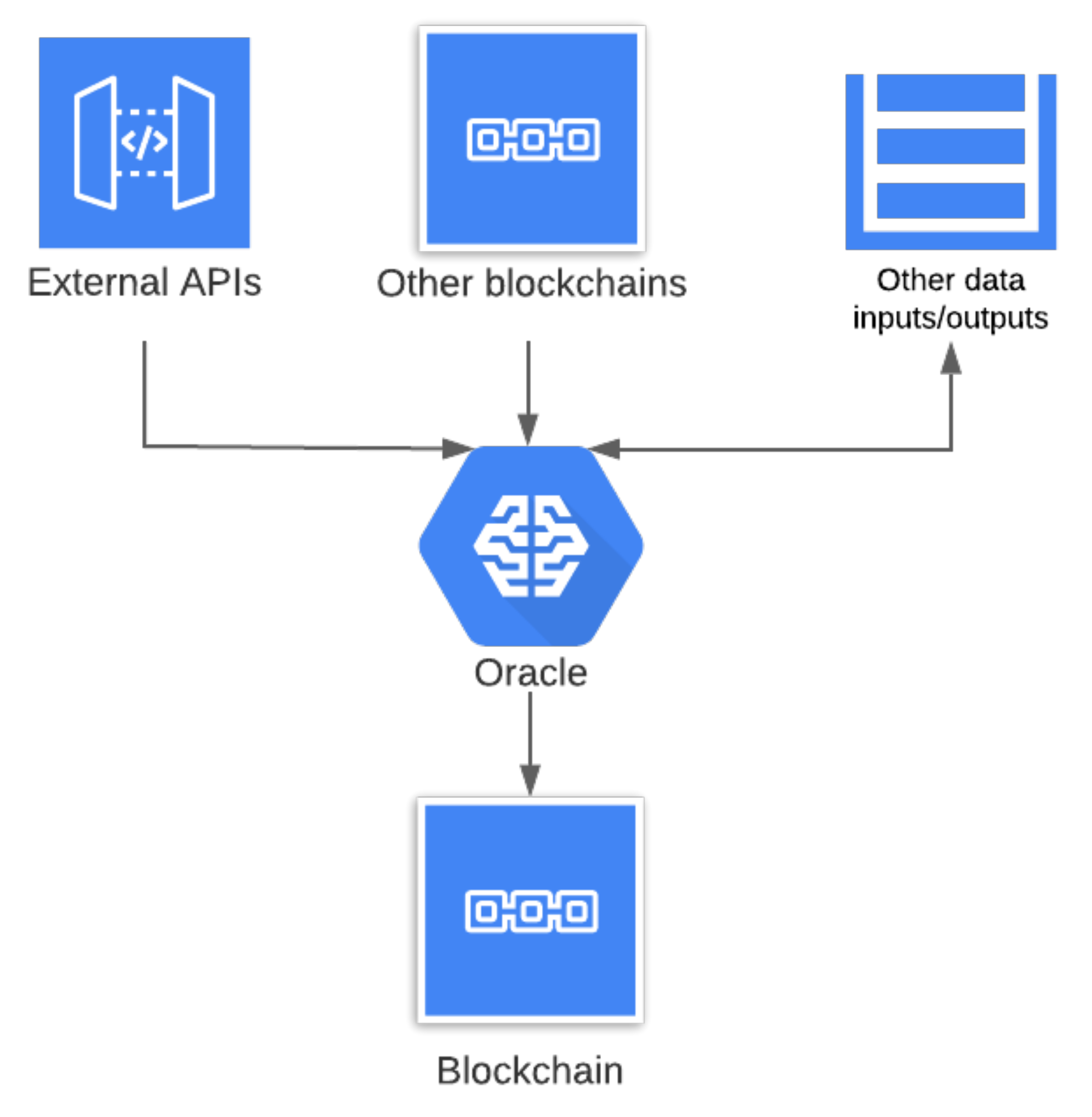

4.5.1. Decentralized Oracles

4.5.2. Decentralized Storage

4.5.3. Node-as-a-Service

4.6. Online Marketplaces and Supply Chains

4.6.1. Online Marketplaces

4.6.2. Supply Chain Finance

4.7. Corporate Governance

4.8. Crowdfunding

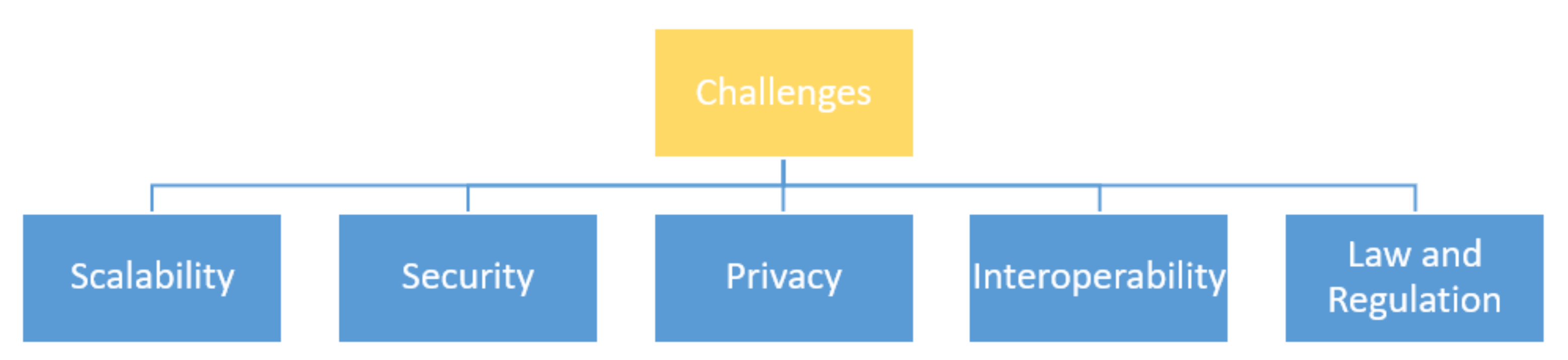

5. Open Research Challenges

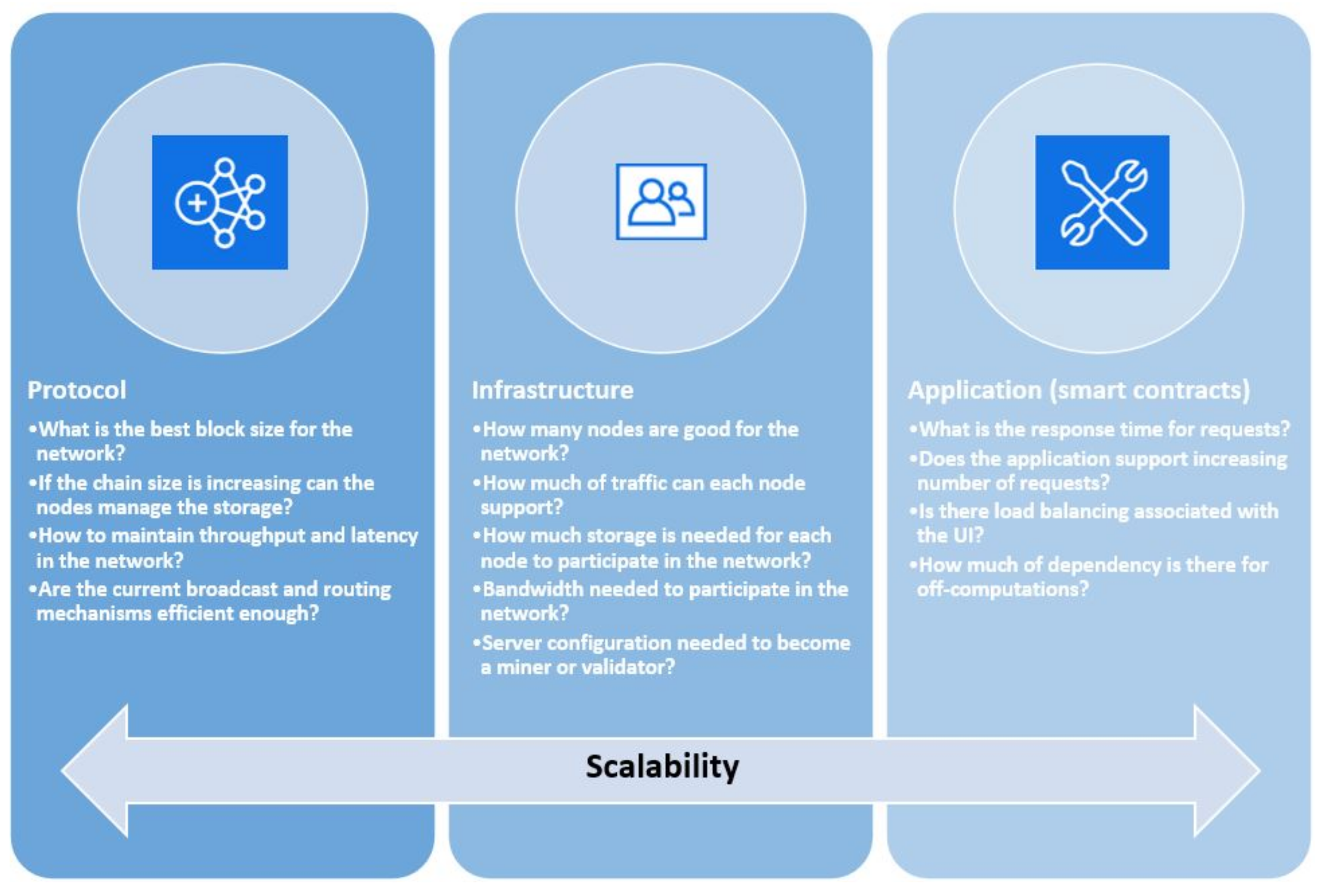

5.1. Scalability

- ORQ1: How should we design scalable protocols from the ground up when developing a blockchain-based financial services platform?

- ORQ2: Which characteristics (block size, network size, etc.) should be used to ensure that a network maintains consistent throughput and latency?

- ORQ3: What is the optimal throughput and latency required for a financial application to run on blockchain?

- ORQ4: How much centralization should be permitted (if scalability is increased) while using blockchain in enterprise scenarios?

- ORQ5: On which layer of the architecture should we place a premium on scalability? Is it Layer 1 (at the protocol-level) or Layer 2?

- ORQ6: Is reliance on multi-layered architectures a disadvantage, or is it more beneficial for the community to host a variety of applications?

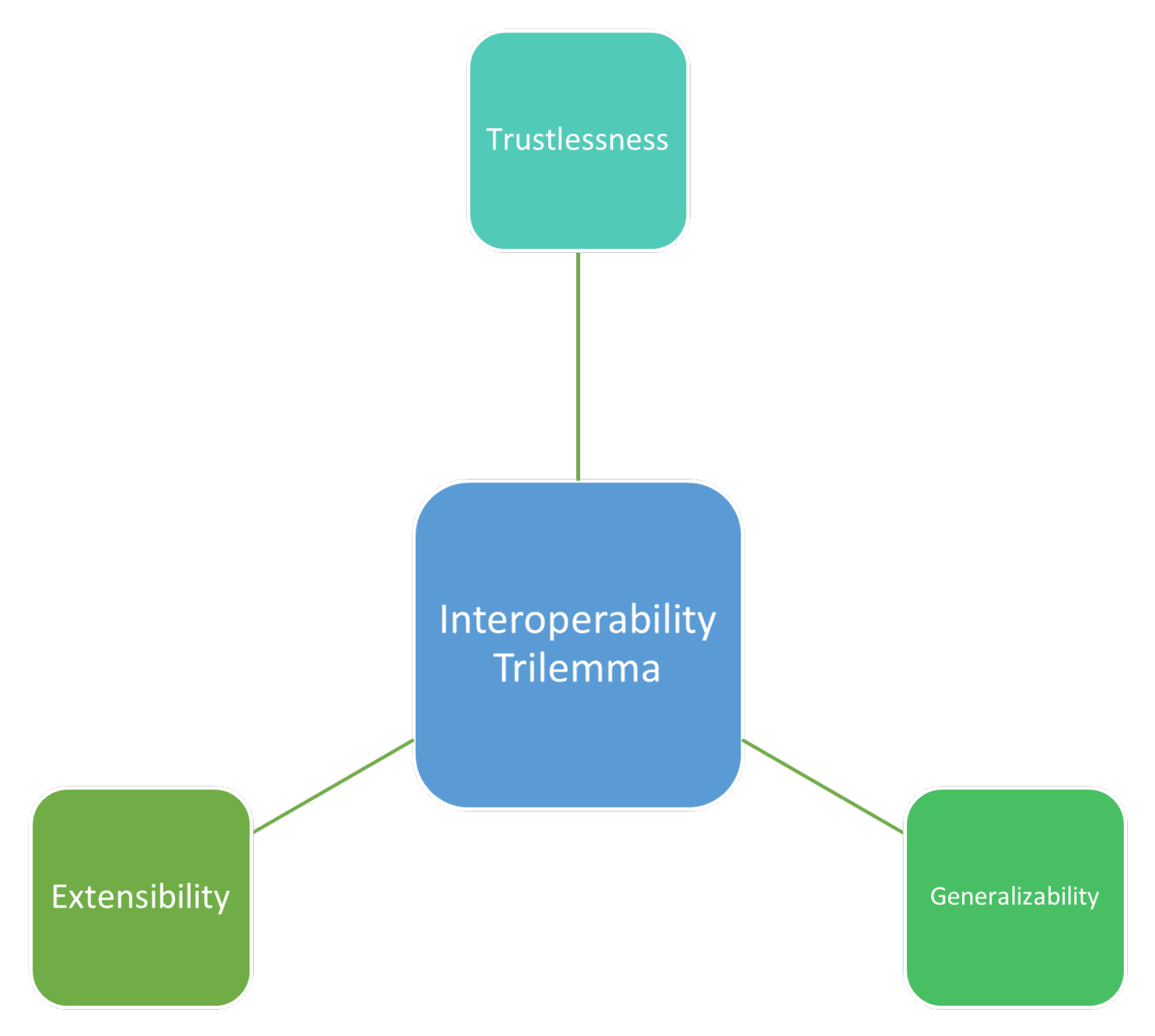

5.2. Interoperability

- ORQ1: How do we transfer data between platforms while maintaining an identical level of privacy and security?

- ORQ2: How can we ensure that data are valid across platforms?

- ORQ3: What safeguards and protocols should be used when communicating between public and private/consortium blockchains?

- ORQ4: What are the dangers associated with implementing interoperability between platforms with varying degrees of trust?

- ORQ5: If the platform is application-specific, for example, supply chain blockchain, how do you transfer data in a way that other platforms can interpret it?

- ORQ6: Using financial services as an example, how do you model the value of assets across numerous platforms?

- ORQ7: From a programming standpoint, how can we execute a smart contract developed for one platform on another?

- ORQ8: How can developers compete in terms of becoming familiar with the semantics of many platforms that use different languages?

- ORQ9: In terms of usability and accessibility, is the end-user experience consistent across platforms?

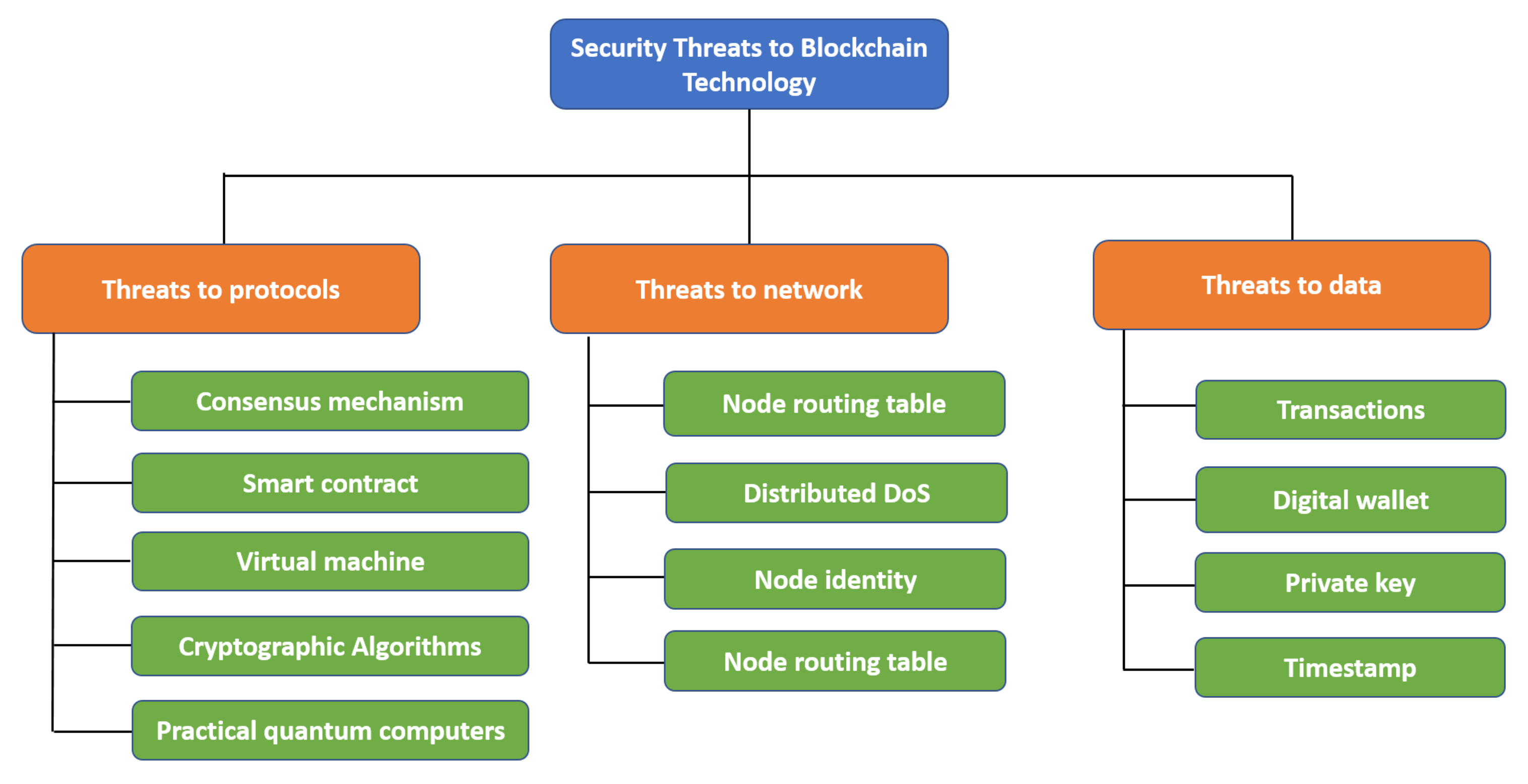

5.3. Security

- Threats to protocols: A security breach in this group would impact the system integrity. Depending on protocols that drive system and network behaviors, hackers could be able to fork the blockchain, perform unauthorized transactions, double-spending, violate the privacy, etc. Threat targets include the following:

- Consensus mechanisms: The integrity of an blockchain relies on the assumption that the majority of miners are honest in mining and in maintaining the network. In the proof-of-work (PoW), if there is a chance that the majority of the miners are colluding together, these miners would be capable of compromising the integrity of the transactions. An successful attack against consensus mechanism provably the most harmful to the system. The study of effective and secure consensus mechanisms is still a open problem.

- Cryptographic algorithms: While blockchain can provide the tamper-proof of transactions due to the use of cryptographic hash functions, attackers are still able to exploit other vulnerabilities. A collision in the hash functions could allow a malicious adversary to replace or modify the input data without changing its digest. A signature forgery could lead to unauthorized transactions. A security breach in other asymmetric cryptographic algorithms, such as ring signatures, zero-knowledge proofs or homomorphic commitment will result in loosing confidentiality and privacy. Last but not least, practical quantum computers would break all cryptosystems based on integer factorization and discrete-logarithm.

- Smart contracts: Since smart contracts are encoded as a part of a “creation” transaction, and written on the blockchain, it is difficult to update. In case a vulnerability is exploited in a smart contract, a malicious adversary could gain profit without respecting agreements between related parties.

- Virtual machine: As this platform provides an execution environment for smart contracts, vulnerabilities exploited also allow a malicious adversary to gain profit without an agreement from related parties in the smart contracts.

- Threats to networks: Various kind of attacks against networking services exist. For instance, Ethereum suffered a DoS attack in 2016 (https://blog.ethereum.org/2016/09/22/ethereum-network-currently-undergoing-dos-attack/, accessed on 2 February 2022). In Dos attacks, an attacker will flush data to a node. This may make the node cannot process normal transactions, that is, aims at the availability of a system. Other network attacks could be carried out on the node routing table or note identity. Designing and provisioning a secure blockchain-based Fintech system against network attacks is crucial.

- Threats to data on the blockchain: Users’ addresses, data transactions, digital wallets, smart contracts, etc. are visible to all participants on the blockchain system to some extent. A blockchain-based system must provide security features to the data, including its integrity, confidentiality and availability. Loosing private key is a significant security concern of participants on the blockchain as without his private key, a participant will have no longer control on his digital assets on the blockchain. Loosing could be caused by a carelessness or by a compromised device holding the digital wallet. How could we design a user-friendly, but digital wallet?

- ORQ1: How can a public blockchain network detect false network identities to prevent Sybil attacks?

- ORQ2: How can a public blockchain network provide the confidentiality of blockchain’s data?

- ORQ3: How do we provide the same level of security in a private blockchain compared to the public blockchain networks with a higher level of decentralization?

- ORQ4: How does a private blockchain network provide a secure access control?

- ORQ5: How can we prevent double-spending in private blockchains, where transactions are not publicly verified?

5.4. Privacy

- ORQ1: Many contracts performed in a business context is done in confidence. How can we implement private smart contracts?

- ORQ2: How can we perform an KYC/AML compliance in blockchain-based Fintech applications whilst offering users and transactions privacy?

- ORQ3: How can blockchain-based Fintech applications comply with privacy requirements such as the right to be forgotten, or other data rights under the GDPR framework?

- ORQ4: The current cryptographic primitives being used to ensure privacy such as Zero-Knowledge Proofs or special signatures are not suitable for use in a tap-pay user experience. Can we design efficient cryptographic algorithms for low resource devices?

5.5. Law and Regulation

- Inter-Continental

- Due to the fact that blockchain applications span multiple countries, legal and regulatory requirements within those countries may become ineffective.

- Financial services have a tendency to migrate to less restrictive jurisdictions when they are prohibited in one. If there are no legal safeguards in place for these scenarios, it will be hard to manage hostile activity.

- At the moment, the majority of designs being offered are being tested in siloed environments, which do not fully simulate working with many entities.

- When it comes to payments, states and governments must collaborate to develop shared regulatory sandboxes in which new technologies can be tested. Particularly for use cases such as cross-border payments, it is critical to thoroughly examine the risks associated with employing blockchain as the underlying technology.

- Numerous usecases for blockchain are being evaluated within country-specific regulatory domains, but again, this is limited to usecase-specific circumstances.

- Users must be assured of the stability of the system under consideration. This is because the majority of blockchain applications entail high-value transactions.

- Priority should be directed to educating the public on both the benefits and risks. For instance, when customers register with centralized exchanges, are they aware that their private keys are not in their control?

- When code becomes law, it is critical to understand how difficulties should be handled when the semantics of code are not specified and learned uniformly by all.

- Within specified areas, a mechanism for incorporating legal documents into the code should exist. R3 Corda is the more well-known protocol that implements this concept. However, this should be consistent across platforms.

- Multiple protocols may be working to improve processes within a single domain, and we have identified interoperability as a critical topic of research. If the platforms are distinct, how are compliance and regulatory challenges addressed? Is there a standardized legal template to which all of these platforms can relate is a critical research subject that has to be addressed.

- ORQ1: Can smart contracts’ compliance and adherence with local regulations be validated?

- ORQ2: How can compliance and regulatory challenges be handled across different platforms that are bridged together?

- ORQ3: How should legal disputes be handled if a platform spans across jurisdictions that have legally divergent consequences?

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Statista. Investments into Fintech Companies Globally 2010–2021. 2022. Available online: https://www.statista.com/statistics/719385/investments-into-fintech-companies-globally/ (accessed on 25 February 2022).

- Insider, B. Overview of the Fintech Industry: Stats, Trends, and Companies in the Ecosystem Market Research Report. 2022. Available online: https://www.businessinsider.com/fintech-ecosystem-report (accessed on 15 March 2022).

- Lee, I.; Shin, Y.J. Fintech: Ecosystem, business models, investment decisions, and challenges. Bus. Horiz. 2018, 61, 35–46. [Google Scholar] [CrossRef]

- Franco-Riquelme, J.N.; Rubalcaba, L. Innovation and SDGs through Social Media Analysis: Messages from FinTech Firms. J. Open Innov. Technol. Mark. Complex. 2021, 7, 165. [Google Scholar] [CrossRef]

- Gomber, P.; Kauffman, R.J.; Parker, C.; Weber, B.W. On the fintech revolution: Interpreting the forces of innovation, disruption, and transformation in financial services. J. Manag. Inf. Syst. 2018, 35, 220–265. [Google Scholar] [CrossRef]

- Jakšič, M.; Marinč, M. Relationship banking and information technology: The role of artificial intelligence and FinTech. Risk Manag. 2019, 21, 1–18. [Google Scholar] [CrossRef]

- Belanche, D.; Casaló, L.V.; Flavián, C. Artificial Intelligence in FinTech: Understanding robo-advisors adoption among customers. Ind. Manag. Data Syst. 2019, 119, 1411–1430. [Google Scholar] [CrossRef]

- Ashta, A.; Herrmann, H. Artificial intelligence and fintech: An overview of opportunities and risks for banking, investments, and microfinance. Strateg. Chang. 2021, 30, 211–222. [Google Scholar] [CrossRef]

- Meng, S.; He, X.; Tian, X. Research on Fintech development issues based on embedded cloud computing and big data analysis. Microprocess. Microsystems 2021, 83, 103977. [Google Scholar] [CrossRef]

- Trelewicz, J.Q. Big data and big money: The role of data in the financial sector. It Prof. 2017, 19, 8–10. [Google Scholar] [CrossRef]

- Pant, S.K. Fintech: Emerging Trends. Telecom Bus. Rev. 2020, 13, 47–52. [Google Scholar]

- Tan, S.; Yang, Y.; Leopold, C.; Robeller, C.; Weber, U. Augmented Reality and Virtual Reality: New Tools for Architectural Visualization and Design. In Research Culture in Architecture; Walter De Gruyter: Berlin, Germany, 2019; pp. 301–310. [Google Scholar]

- Fernandez-Vazquez, S.; Rosillo, R.; De La Fuente, D.; Priore, P. Blockchain in FinTech: A mapping study. Sustainability 2019, 11, 6366. [Google Scholar] [CrossRef] [Green Version]

- Imerman, M.B.; Fabozzi, F.J. Cashing in on innovation: A taxonomy of FinTech. J. Asset Manag. 2020, 21, 167–177. [Google Scholar] [CrossRef]

- Sardana, V.; Singhania, S. Digital technology in the realm of banking: A review of literature. Int. J. Res. Financ. Manag. 2018, 1, 28–32. [Google Scholar]

- BusinessWire. 2022. Available online: https://www.businesswire.com/news/home/20220218005233/en/Global-Digital-Payment-Market-is-Expected-to-Grow-at-a-CAGR-of-over-20.5-During-2022-2030—ResearchAndMarkets.com (accessed on 7 March 2022).

- Federal Reserve Bank of St Louis. 2022. Available online: https://www.stlouisfed.org/education/tools-for-enhancing-the-stock-market-game-invest-it-forward/episode-1-understanding-capital-markets (accessed on 7 March 2022).

- Biery, M.E. What Is Digital Lending and How Can Community Banks, Credit Unions Benefit. 2018. Available online: https://www.abrigo.com/blog/what-is-digital-lending-and-how-can-community-banks-credit-unions-benefit/ (accessed on 3 March 2022).

- Arner, D.W.; Barberis, J.; Buckley, R.P. FinTech and RegTech in a Nutshell, and the Future in a Sandbox; CFA Institute Research Foundation: Charlottesville, VA, USA, 2017; Volume 3, pp. 1–20. [Google Scholar]

- Nakamoto, S. Bitcoin: A Peer-to-Peer Electronic Cash System. Technical Report. 2008. Available online: https://bitcoin.org/bitcoin.pdf (accessed on 3 March 2022).

- Wood, G. Ethereum: A Secure Decentralised Generalised Transaction Ledger; Technical Report; Ethereum & ETHCore: New York, NY, USA, 2016; Volume 151, pp. 1–32. [Google Scholar]

- Foundation, L. Hyperledger Fabric. 2015. Available online: https://hyperledger-fabric.readthedocs.io (accessed on 15 March 2022).

- Greenspan, G. MultiChain Private Blockchain—White Paper. 2015. Available online: https://www.multichain.com/white-paper/ (accessed on 15 March 2022).

- Lee, S.H.; Lee, D.W. Review on Fintech Industry in Oversea. In Proceedings of the Conference on Circuits, Control, Communication, Electricity, Electronics, Energy, System, Signal and Simulation, Ho Chi Minh City, Vietnam, 12–19 October 2016. [Google Scholar]

- Hendershott, T.; Zhang, X.; Zhao, J.L.; Zheng, Z. FinTech as a game changer: Overview of research frontiers. Inf. Syst. Res. 2021, 32, 1–17. [Google Scholar] [CrossRef]

- Suryono, R.R.; Budi, I.; Purwandari, B. Challenges and trends of financial technology (Fintech): A systematic literature review. Information 2020, 11, 590. [Google Scholar] [CrossRef]

- Li, B.; Xu, Z. Insights into financial technology (FinTech): A bibliometric and visual study. Financ. Innov. 2021, 7, 1–28. [Google Scholar] [CrossRef]

- Bollaert, H.; Lopez-de Silanes, F.; Schwienbacher, A. Fintech and access to finance. J. Corp. Financ. 2021, 68, 101941. [Google Scholar] [CrossRef]

- Takeda, A.; Ito, Y. A review of FinTech research. Int. J. Technol. Manag. 2021, 86, 67–88. [Google Scholar] [CrossRef]

- Sangwan, V.; Prakash, P.; Singh, S. Financial technology: A review of extant literature. Stud. Econ. Financ. 2019, 37, 71–88. [Google Scholar] [CrossRef]

- Knewtson, H.S.; Rosenbaum, Z.A. Toward understanding FinTech and its industry. Manag. Financ. 2020, 46, 1043–1060. [Google Scholar] [CrossRef]

- Milian, E.Z.; Spinola, M.D.M.; de Carvalho, M.M. Fintechs: A literature review and research agenda. Electron. Commer. Res. Appl. 2019, 34, 100833. [Google Scholar] [CrossRef]

- Xu, M.; Chen, X.; Kou, G. A systematic review of blockchain. Financ. Innov. 2019, 5, 1–14. [Google Scholar] [CrossRef] [Green Version]

- Ali, O.; Ally, M.; Dwivedi, Y. The state of play of blockchain technology in the financial services sector: A systematic literature review. Int. J. Inf. Manag. 2020, 54, 102199. [Google Scholar] [CrossRef]

- Rabbani, M.R.; Khan, S.; Thalassinos, E.I. FinTech, Blockchain and Islamic Finance: An Extensive Literature Review. Int. J. Econ. Bus. Adm. 2020, VIII, 65–86. [Google Scholar]

- Cao, S.; Cao, Y.; Wang, X.; Lu, Y. A review of researches on blockchain. In Proceedings of the Wuhan International Conference on e-Business, Wuhan, China, 29–28 May 2017. [Google Scholar]

- Da Luz, M.A.; de Oliveira, K.S.F. The Use of Blockchain in Financial Area: A Systematic Mapping Study. In Proceedings of the Anais do XVI Simpósio Brasileiro de Sistemas de Informação; SBC: São Bernardo do Camp, Brazil, 2020. [Google Scholar]

- Frizzo-Barker, J.; Chow-White, P.A.; Adams, P.R.; Mentanko, J.; Ha, D.; Green, S. Blockchain as a disruptive technology for business: A systematic review. Int. J. Inf. Manag. 2020, 51, 102029. [Google Scholar] [CrossRef]

- Pal, A.; Tiwari, C.K.; Behl, A. Blockchain technology in financial services: A comprehensive review of the literature. J. Glob. Oper. Strateg. Sourc. 2021, 14, 61–80. [Google Scholar] [CrossRef]

- Trivedi, S.; Mehta, K.; Sharma, R. Systematic Literature Review on Application of Blockchain Technology in E-Finance and Financial Services. J. Technol. Manag. Innov. 2021, 16, 89–102. [Google Scholar] [CrossRef]

- Gamage, H.; Weerasinghe, H.; Dias, N. A survey on blockchain technology concepts, applications, and issues. SN Comput. Sci. 2020, 1, 1–15. [Google Scholar] [CrossRef] [Green Version]

- Gan, Q.; Lau, R.Y.K.; Hong, J. A critical review of blockchain applications to banking and finance: A qualitative thematic analysis approach. Technol. Anal. Strateg. Manag. 2021, 1–17. [Google Scholar] [CrossRef]

- Osmani, M.; El-Haddadeh, R.; Hindi, N.; Janssen, M.; Weerakkody, V. Blockchain for next generation services in banking and finance: Cost, benefit, risk and opportunity analysis. J. Enterp. Inf. Manag. 2021, 34, 884–899. [Google Scholar] [CrossRef]

- Gorkhali, A.; Chowdhury, R. Blockchain and the Evolving Financial Market: A Literature Review. J. Ind. Integr. Manag. 2021, 1–35. [Google Scholar] [CrossRef]

- Maiti, M.; Ghosh, U. Next generation Internet of Things in fintech ecosystem. IEEE Internet Things J. 2021. [Google Scholar] [CrossRef]

- Maiti, M.; Kotliarov, I.; Lipatnikov, V. A future triple entry accounting framework using blockchain technology. Blockchain Res. Appl. 2021, 2, 100037. [Google Scholar] [CrossRef]

- Javaid, M.; Haleem, A.; Singh, R.P.; Khan, S.; Suman, R. Blockchain technology applications for Industry 4.0: A literature-based review. Blockchain Res. Appl. 2021, 2, 100027. [Google Scholar] [CrossRef]

- Chondrogiannis, E.; Andronikou, V.; Karanastasis, E.; Litke, A.; Varvarigou, T. Using blockchain and semantic web technologies for the implementation of smart contracts between individuals and health insurance organizations. Blockchain Res. Appl. 2022, 3, 100049. [Google Scholar] [CrossRef]

- Six, N.; Herbaut, N.; Salinesi, C. Blockchain software patterns for the design of decentralized applications: A systematic literature review. Blockchain Res. Appl. 2022, 3, 100061. [Google Scholar] [CrossRef]

- NIST-FIPS. FIPS Publication 180-2: Secure Hash Standard; Technical Report; Federal Information Processing Standard Publication: Gaithersburg, MD, USA, 2002. [Google Scholar]

- America National Standard Institute. Public Key Cryptography for the Financial Services Industry: The Elliptic Curve Digital Signature Algorithm (ECDSA); ANSI: San Fransisco, CA, USA, 1998. [Google Scholar]

- Rivest, R.L.; Shamir, A.; Tauman, Y. How to Leak a Secret; Springer: Berlin/Heidelberg, Germany, 2001; pp. 552–565. [Google Scholar]

- Blum, M.; Feldman, P.; Micali, S. Non-Interactive Zero-Knowledge and Its Applications. In Proceedings of the Twentieth Annual ACM Symposium on Theory of Computing (STOC ’88); Association for Computing Machinery: New York, NY, USA, 1988; pp. 103–112. [Google Scholar] [CrossRef]

- Pedersen, T.P. Non-interactive and information-theoretic secure verifiable secret sharing. In Proceedings of the Annual International Cryptology Conference, Santa Barbara, CA, USA, 11–15 August 1991; pp. 129–140. [Google Scholar]

- Szabo, N. Formalizing and securing relationships on public networks. First Monday 1997, 2. [Google Scholar] [CrossRef]

- Bosselaers, A.; Preneel, B. Integrity Primitives for Secure Information Systems: Final Ripe Report of Race Integrity Primitives Evaluation; Number 1007; Springer Science & Business Media: New York, NY, USA, 1995. [Google Scholar]

- Dobbertin, H.; Bosselaers, A.; Preneel, B. RIPEMD-160: A strengthened version of RIPEMD. In Proceedings of the International Workshop on Fast Software Encryption; Springer: Cambridge, UK, 1996; pp. 71–82. [Google Scholar]

- Litecoin. Litecoin—Open Source P2P Digital Currency. Technical Report. 2011. Available online: https://litecoin.org/ (accessed on 30 November 2012).

- Percival, C.; Josefsson, S. The Scrypt Password-Based Key Derivation Function. 2016. Available online: http://tools.ietf.org/html/josefsson-scrypt-kdf-00.txt (accessed on 7 March 2022).

- Biryukov, A.; Khovratovich, D. Equihash: Asymmetric proof-of-work based on the generalized birthday problem. Ledger 2017, 2, 1–30. [Google Scholar] [CrossRef] [Green Version]

- Merkle, R.C. A digital signature based on a conventional encryption function. In Proceedings of the Conference on the Theory and Application of Cryptographic Techniques, Santa Barbara, CA, USA, 16–20 August 1987; pp. 369–378. [Google Scholar]

- Diffie, W.; Hellman, M. New Directions in Cryptography. IEEE Trans. Inf. Theor. 2006, 22, 644–654. [Google Scholar] [CrossRef] [Green Version]

- National Institute of Standards and Technology. Digital Signature Standard; NIST: Washington, DC, USA, 1994. [Google Scholar]

- Vanstone, S. Responses to NIST’s Proposal. Commun. ACM 1992, 35, 50–52. [Google Scholar]

- International Standard Organization. Information Technology—Security Techniques—Cryptographic Techniques Based on Elliptic Curves—Part 2: Digital Signatures. 2002. Available online: https://www.iso.org/standard/31076.html (accessed on 7 March 2022).

- IEEE Computer Society. IEEE Std 1363-2000; IEEE Standard Specifications for Public-Key Cryptography; IEEE Computer Society: Washington, DC, USA, 2000; pp. 1–228. [Google Scholar] [CrossRef]

- Lamport, L. Constructing Digital Signatures from a One Way Function; Technical Report CSL-98; IEEE: New York, NY, USA, 1979; This paper was published by IEEE in the Proceedings of HICSS-43 in January 2010. [Google Scholar]

- Chaum, D. Blind signatures for untraceable payments. In Advances in Cryptology; Springer: Santa Barbara, CA, USA, 1983; pp. 199–203. [Google Scholar]

- Van Saberhagen, N. CryptoNote v 2.0; Technical Report. 2013. Available online: https://bytecoin.org/old/whitepaper.pdf (accessed on 7 March 2022).

- Maxwell, G.; Poelstra, A. Borromean ring signatures. Comput. Sci. 2015, 8, 2019. [Google Scholar]

- Valenta, L.; Rowan, B. Blindcoin: Blinded, accountable mixes for bitcoin. In Proceedings of the International Conference on Financial Cryptography and Data Security, San Juan, Puerto Rico, 26–30 January 2015; pp. 112–126. [Google Scholar]

- Itakura, K.; Nakamura, K. A Public-Key Cryptosystem Suitable for Digital Multisignatures; NEC Research & Development: Kanagawa, Japan, 1983; pp. 1–8. [Google Scholar]

- Le, D.P.; Yang, G.; Ghorbani, A. A new multisignature scheme with public key aggregation for blockchain. In Proceedings of the 2019 17th International Conference on Privacy, Security and Trust (PST), Fredericton, NB, Canada, 26–28 August 2019; pp. 1–7. [Google Scholar]

- Benaloh, J.; Mare, M.D. One-way accumulators: A decentralized alternative to digital signatures. In Proceedings of the Workshop on the Theory and Application of of Cryptographic Techniques; Springer: Lofthus, Norway, 1993; pp. 274–285. [Google Scholar]

- Nguyen, L. Accumulators from bilinear pairings and applications. In Proceedings of the Cryptographers’ Track at the RSA Conference, San Francisco, CA, USA, 14–18 February 2005; pp. 275–292. [Google Scholar]

- Boxall, J.; El Mrabet, N.; Laguillaumie, F.; Le, D.P. A Variant of Miller’s Formula and Algorithm. In Proceedings of the 4th International Conference on Pairing-Based Cryptography (Pairing’10); Springer: Berlin/Heidelberg, Germany, 2010; pp. 417–434. [Google Scholar]

- Sun, S.F.; Au, M.H.; Liu, J.K.; Yuen, T.H. Ringct 2.0: A compact accumulator-based (linkable ring signature) protocol for blockchain cryptocurrency monero. In Proceedings of the European Symposium on Research in Computer Security, Oslo, Norway, 11–15 September 2017; pp. 456–474. [Google Scholar]

- Miers, I.; Garman, C.; Green, M.; Rubin, A.D. Zerocoin: Anonymous distributed e-cash from bitcoin. In Proceedings of the 2013 IEEE Symposium on Security and Privacy, Berkeley, CA, USA, 19–22 May 2013; pp. 397–411. [Google Scholar]

- Sasson, E.B.; Chiesa, A.; Garman, C.; Green, M.; Miers, I.; Tromer, E.; Virza, M. Zerocash: Decentralized Anonymous Payments from Bitcoin. In Proceedings of the Symposium on Security and Privacy, Berkeley, CA, USA, 18–21 May 2014. [Google Scholar]

- Ben-Sasson, E.; Chiesa, A.; Riabzev, M.; Spooner, N.; Virza, M.; Ward, N.P. Aurora: Transparent succinct arguments for R1CS. In Proceedings of the Annual International Conference on the Theory and Applications of Cryptographic Techniques, Darmstadt, Germany, 19–23 May 2019; pp. 103–128. [Google Scholar]

- Bünz, B.; Bootle, J.; Boneh, D.; Poelstra, A.; Wuille, P.; Maxwell, G. Bulletproofs: Short proofs for confidential transactions and more. In Proceedings of the 2018 IEEE Symposium on Security and Privacy (SP), Berkeley, CA, USA, 21–23 May 2018; pp. 315–334. [Google Scholar]

- Cong, L.W.; He, Z. Blockchain disruption and smart contracts. Rev. Financ. Stud. 2019, 32, 1754–1797. [Google Scholar] [CrossRef]

- Dcunha, S.; Patel, S.; Sawant, S.; Kulkarni, V.; Shirole, M. Blockchain Interoperability Using Hash Time Locks. In Proceedings of the Fifth International Conference on Microelectronics, Computing and Communication Systems, Ranchi, India, 12–13 May 2021; pp. 475–487. [Google Scholar]

- Han, J.; Huang, S.; Zhong, Z. Trust in DeFi: An Empirical Study of the Decentralized Exchange. 2021. Available online: https://ssrn.com/abstract=3896461 (accessed on 7 March 2022).

- Poon, J.; Dryja, T. The Bitcoin Lightning Network: Scalable Off-Chain Instant Payments. White Paper, 14 January 2016. Available online: https://lightning.network/lightning-network-paper.pdf (accessed on 7 March 2022).

- Besedin, S.; Mitrokhin, A. Decentralized Escrow Whitepaper. Technical Report. 2017. Available online: https://descrow.com/images/WP_en.pdf (accessed on 7 March 2022).

- Goldfeder, S.; Bonneau, J.; Gennaro, R.; Narayanan, A. Escrow protocols for cryptocurrencies: How to buy physical goods using bitcoin. In Proceedings of the International Conference on Financial Cryptography and Data Security, Sliema, Malta, 3–7 April 2017; pp. 321–339. [Google Scholar]

- Herlihy, M. Atomic cross-chain swaps. In Proceedings of the 2018 ACM Symposium on Principles of Distributed Computing, Egham, UK, 23–27 July 2018; pp. 245–254. [Google Scholar]

- Hardjono, T. Blockchain gateways, bridges and delegated hash-locks. arXiv 2021, arXiv:2102.03933. [Google Scholar]

- Blockchain Bridges. 2022. Available online: https://ethereum.org/en/bridges/ (accessed on 3 March 2022).

- Kfoury, B. The Role of Blockchain in Reducing the Cost of Financial Transactions in the Retail Industry. Technical Report. 2021. Available online: http://ceur-ws.org/Vol-2889/PAPER_02.pdf (accessed on 15 March 2022).

- Mori, T. Financial technology: Blockchain and securities settlement. J. Secur. Oper. Custody 2016, 8, 208–227. [Google Scholar]

- Tasca, P.; Tessone, C.J. Taxonomy of blockchain technologies. Principles of identification and classification. arXiv 2017, arXiv:1708.04872. [Google Scholar] [CrossRef]

- Zhang, C.; Wu, C.; Wang, X. Overview of Blockchain consensus mechanism. In Proceedings of the 2020 2nd International Conference on Big Data Engineering, Shanghai, China, 29–31 May 2020; pp. 7–12. [Google Scholar]

- Vukolić, M. The Quest for Scalable Blockchain Fabric: Proof-of-Work vs. BFT Replication. In Open Problems in Network Security. iNetSec 2015. Lecture Notes in Computer Science; Camenisch, J., Kesdoğan, D., Eds.; Springer: Cham, Switzerland, 2015; Volume 9591. [Google Scholar] [CrossRef] [Green Version]

- Saleh, F. Blockchain without waste: Proof-of-stake. Rev. Financ. Stud. 2021, 34, 1156–1190. [Google Scholar] [CrossRef]

- Nair, P.R.; Dorai, D.R. Evaluation of performance and security of proof of work and proof of stake using blockchain. In Proceedings of the 2021 Third International Conference on Intelligent Communication Technologies and Virtual Mobile Networks (ICICV), Virtual, 4–6 February 2021; pp. 279–283. [Google Scholar]

- Reijers, W.; Wuisman, I.; Mannan, M.; De Filippi, P.; Wray, C.; Rae-Looi, V.; Cubillos Vélez, A.; Orgad, L. Now the Code Runs Itself: On-Chain and Off-Chain Governance of Blockchain Technologies. Topoi 2021, 40, 821–831. [Google Scholar] [CrossRef] [Green Version]

- Chohan, U.W. The Decentralized Autonomous Organization and Governance Issues. 2017. Available online: https://ssrn.com/abstract=3082055 (accessed on 7 March 2022).

- Zhang, R.; Xue, R.; Liu, L. Security and privacy on blockchain. ACM Comput. Surv. (CSUR) 2019, 52, 1–34. [Google Scholar] [CrossRef] [Green Version]

- Chen, X.; Hasan, M.A.; Wu, X.; Skums, P.; Feizollahi, M.J.; Ouellet, M.; Sevigny, E.L.; Maimon, D.; Wu, Y. Characteristics of bitcoin transactions on cryptomarkets. In Proceedings of the International Conference on Security, Privacy and Anonymity in Computation, Communication and Storage, Atlanta, GA, USA, 14–17 July 2019; pp. 261–276. [Google Scholar]

- Guides, T.S. Why Cardano ADA Deserves Your Attention—Cardano Cryptocurrency Strategy. 2018. Available online: https://tradingstrategyguides.com/cardano-cryptocurrency-strategy/ (accessed on 7 March 2022).

- Silvano, W.F.; Marcelino, R. Iota Tangle: A cryptocurrency to communicate Internet-of-Things data. Future Gener. Comput. Syst. 2020, 112, 307–319. [Google Scholar] [CrossRef]

- Chen, J.; Micali, S. Algorand: A secure and efficient distributed ledger. Theor. Comput. Sci. 2019, 777, 155–183. [Google Scholar] [CrossRef]

- Brown, R.G.; Carlyle, J.; Grigg, I.; Hearn, M. Corda: An introduction. R3 CEV 2016, 1, 14. [Google Scholar]

- Baliga, A.; Subhod, I.; Kamat, P.; Chatterjee, S. Performance evaluation of the quorum blockchain platform. arXiv 2018, arXiv:1809.03421. [Google Scholar]

- Consensys. Quorum Blockchain. 2022. Available online: https://github.com/ConsenSys/quorum (accessed on 15 March 2022).

- Diem. Diem Blockchain. 2022. Available online: https://www.diem.com/en-us/ (accessed on 15 March 2022).

- Kelley, M.; Mahdi, D. Innovation Insight for Decentralized Identity and Verifiable Claims; Technical Report; Gartner Research: Stamford, CT, USA, 2021. [Google Scholar]

- Foundation, H. Decentralized ID and Access Management (DIAM) for IoT Networks; Technical Report; Linux Foundation: San Francisco, CA, USA, 2021. [Google Scholar]

- Lyons, T.; Courcelas, L.; Timsit, K. Blockchain and Digital Identity; Technical Report; The European Union Blockchain Observatory & Forum: Washington, DC, USA, 2019. [Google Scholar]

- Pertsev, A.; Semenov, R.; Storm, R. Tornado Cash Privacy Solution Version 1.4. 2019. Available online: https://tornado.cash/Tornado.cash_whitepaper_v1.4.pdf (accessed on 15 March 2022).

- Hopwood, D.; Bowe, S.; Hornby, T.; Wilcox, N. Zcash Protocol Specification; GitHub: San Francisco, CA, USA, 2016; p. 1. [Google Scholar]

- Ali, R.; Barrdear, J.; Clews, R.; Southgate, J. The economics of digital currencies. Bank Engl. Q. Bull. 2014, 54, 276–286. [Google Scholar]

- Allen, F.; Gu, X.; Jagtiani, J. Fintech, Cryptocurrencies, and CBDC: Financial Structural Transformation in China. J. Int. Money Financ. 2022, 124, 102625. [Google Scholar] [CrossRef]

- Calcaterra, C.; Kaal, W.A.; Rao, V. Stable cryptocurrencies: First order principles. Stan. J. Blockchain L. Pol’y 2020, 3, 62. [Google Scholar] [CrossRef]

- Bogoni, G. Cryptocurrencies Stabilization Systems: A Focus on the MakerDAO Case. 2019. Available online: https://www.politesi.polimi.it/handle/10589/152447?mode=full (accessed on 15 March 2022).

- Acker, A.; Murthy, D. What is Venmo? A descriptive analysis of social features in the mobile payment platform. Telemat. Inform. 2020, 52, 101429. [Google Scholar] [CrossRef]

- Tsepeleva, R.; Korkhov, V. Implementation of the Cross-Blockchain Interacting Protocol. In Computational Science and Its Applications—ICCSA 2021. Lecture Notes in Computer Science; Springer: Cham, Switzerland, 2021; Volume 12952. [Google Scholar] [CrossRef]

- Fung, B.; Halaburda, H. Understanding platform-based digital currencies. Bank Can. Rev. 2014, 2014, 12–20. [Google Scholar]

- Meta. 2022. Available online: https://about.facebook.com/meta/ (accessed on 6 March 2022).

- Amazon. 2022. Available online: https://www.aboutamazon.com/ (accessed on 6 March 2022).

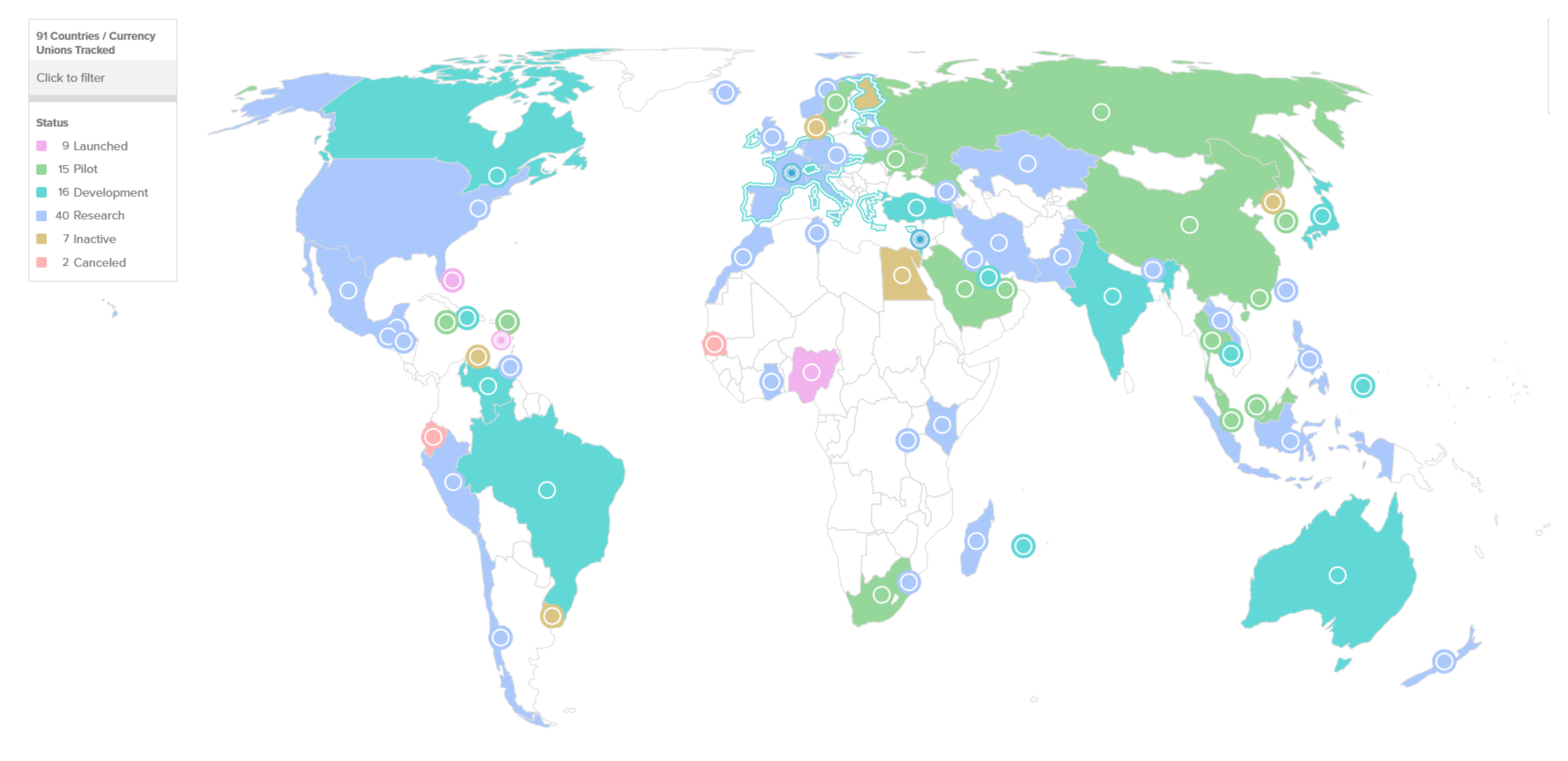

- Kiff, M.J.; Alwazir, J.; Davidovic, S.; Farias, A.; Khan, M.A.; Khiaonarong, M.T.; Malaika, M.; Monroe, M.H.K.; Sugimoto, N.; Tourpe, H.; et al. A Survey of Research on Retail Central Bank Digital Currency. 1 July 2020. Available online: https://ssrn.com/abstract=3639760 (accessed on 15 March 2022).

- Zhang, T.; Huang, Z. Blockchain and central bank digital currency. ICT Express 2021. [Google Scholar] [CrossRef]

- Bank of International Settlements. 2022. Available online: https://www.bis.org/publ/othp33.pdf (accessed on 14 March 2022).

- Atlantic Council. 2022. Available online: https://www.atlanticcouncil.org/blogs/econographics/a-report-card-on-chinas-central-bank-digital-currency-the-e-cny/ (accessed on 6 March 2022).

- MIT Media Lab. 2022. Available online: https://dci.mit.edu/project-hamilton-building-a-hypothetical-cbdc (accessed on 7 March 2022).

- Liu, Y.; Vogel, S.; Zhang, Y. Electronic trading in OTC markets vs. centralized exchange. In Proceedings of the Finance Meeting EUROFIDAI-AFFI, Paris, France, 20 December 2018. [Google Scholar]

- Xu, J.; Paruch, K.; Cousaert, S.; Feng, Y. Sok: Decentralized exchanges (dex) with automated market maker (AMM) protocols. arXiv 2021, arXiv:2103.12732. [Google Scholar]

- Capponi, A.; Jia, R. The adoption of blockchain-based decentralized exchanges. arXiv 2021, arXiv:2103.08842. [Google Scholar]

- Uniswap. 2022. Available online: https://uniswap.org/ (accessed on 7 March 2022).

- Sushiswap. 2022. Available online: https://www.sushi.com/ (accessed on 7 March 2022).

- Balancer. 2022. Available online: https://balancer.fi/ (accessed on 7 March 2022).

- Qin, K.; Zhou, L.; Afonin, Y.; Lazzaretti, L.; Gervais, A. CeFi vs. DeFi–Comparing Centralized to Decentralized Finance. arXiv 2021, arXiv:2106.08157. [Google Scholar]

- Werner, S.M.; Perez, D.; Gudgeon, L.; Klages-Mundt, A.; Harz, D.; Knottenbelt, W.J. Sok: Decentralized finance (defi). arXiv 2021, arXiv:2101.08778. [Google Scholar]

- Qin, K.; Zhou, L.; Livshits, B.; Gervais, A. Attacking the DeFi Ecosystem with Flash Loans for Fun and Profit. In Financial Cryptography and Data Security. FC 2021. Lecture Notes in Computer Science; Borisov, N., Diaz, C., Eds.; Springer: Berlin/Heidelberg, Germany, 2021; Volume 12674. [Google Scholar] [CrossRef]

- Compound. 2022. Available online: https://compound.finance/ (accessed on 7 March 2022).

- Aave. 2022. Available online: https://aave.com/ (accessed on 7 March 2022).

- dYdX. 2022. Available online: https://dydx.exchange/ (accessed on 7 March 2022).

- Gudgeon, L.; Werner, S.; Perez, D.; Knottenbelt, W.J. Defi protocols for loanable funds: Interest rates, liquidity and market efficiency. In Proceedings of the 2nd ACM Conference on Advances in Financial Technologies, New York, NY, USA, 21–23 October 2020; pp. 92–112. [Google Scholar]

- Synthetix. 2022. Available online: https://synthetix.io/ (accessed on 7 March 2022).

- Nexus. 2022. Available online: https://nexusmutual.io/ (accessed on 7 March 2022).

- Erasure. 2022. Available online: https://erasure.world/ (accessed on 7 March 2022).

- Jumpcrypto.com. 2022. Available online: https://jumpcrypto.com/state-of-crypto-derivatives-market/ (accessed on 7 March 2022).

- Beniiche, A. A study of blockchain oracles. arXiv 2020, arXiv:2004.07140. [Google Scholar]

- Egberts, A. The Oracle Problem—An Analysis of how Blockchain Oracles Undermine the Advantages of Decentralized Ledger Systems. 13 December 2017. Available online: https://ssrn.com/abstract=3382343 (accessed on 7 March 2022).

- Pasdar, A.; Dong, Z.; Lee, Y.C. Blockchain Oracle Design Patterns. arXiv 2021, arXiv:2106.09349. [Google Scholar]

- Zhang, F.; Maram, D.; Malvai, H.; Goldfeder, S.; Juels, A. Deco: Liberating web data using decentralized oracles for tls. In Proceedings of the 2020 ACM SIGSAC Conference on Computer and Communications Security, Virtual Event, 9–13 November 2020; pp. 1919–1938. [Google Scholar]

- Liu, B.; Szalachowski, P.; Zhou, J. A First Look into DeFi Oracles. In Proceedings of the 2021 IEEE International Conference on Decentralized Applications and Infrastructures (DAPPS), London, UK, 23–26 August 2021; pp. 39–48. [Google Scholar] [CrossRef]

- Adler, J.; Berryhill, R.; Veneris, A.; Poulos, Z.; Veira, N.; Kastania, A. Astraea: A Decentralized Blockchain Oracle. In Proceedings of the 2018 IEEE International Conference on Internet of Things (iThings) and IEEE Green Computing and Communications (GreenCom) and IEEE Cyber, Physical and Social Computing (CPSCom) and IEEE Smart Data (SmartData), Dalian, China, 20–21 October 2018; pp. 1145–1152. [Google Scholar] [CrossRef] [Green Version]

- Goel, N.; Filos-Ratsikas, A.; Faltings, B. Decentralized Oracles via Peer-Prediction in the Presence of Lying Incentives. 2019. Available online: https://arisfilosratsikas.com/papers/decentralized_oracles.pdf (accessed on 7 March 2022).

- Merlini, M.; Veira, N.; Berryhill, R.; Veneris, A. On Public Decentralized Ledger Oracles via a Paired-Question Protocol. In Proceedings of the 2019 IEEE International Conference on Blockchain and Cryptocurrency (ICBC), Seoul, Korea, 14–17 May 2019; pp. 337–344. [Google Scholar] [CrossRef]

- Cai, Y.; Fragkos, G.; Tsiropoulou, E.E.; Veneris, A. 2020 A Truth-Inducing Sybil Resistant Decentralized Blockchain Oracle. In Proceedings of the 2020 2nd Conference on Blockchain Research & Applications for Innovative Networks and Services (BRAINS), Paris, France, 28–30 September 2020; pp. 128–135. [Google Scholar] [CrossRef]

- Peterson, J.; Krug, J.; Zoltu, M.; Williams, A.K.; Alexander, S. Augur: A decentralized oracle and prediction market platform. arXiv 2015, arXiv:1501.01042. [Google Scholar]

- De Pedro, A.S.; Levi, D.; Cuende, L.I. Witnet: A decentralized oracle network protocol. arXiv 2017, arXiv:1711.09756. [Google Scholar]

- Breidenbach, L.; Cachin, C.; Chan, B.; Coventry, A.; Ellis, S.; Juels, A.; Koushanfar, F.; Miller, A.; Magauran, B.; Moroz, D.; et al. Chainlink 2.0: Next Steps in the Evolution of Decentralized Oracle Networks. 2021. Available online: https://research.chain.link/whitepaper-v2.pdf (accessed on 7 March 2022).

- Benisi, N.Z.; Aminian, M.; Javadi, B. Blockchain-based decentralized storage networks: A survey. J. Netw. Comput. Appl. 2020, 162, 102656. [Google Scholar]

- Casino, F.; Politou, E.; Alepis, E.; Patsakis, C. Immutability and decentralized storage: An analysis of emerging threats. IEEE Access 2019, 8, 4737–4744. [Google Scholar] [CrossRef]

- Shah, M.; Shaikh, M.; Mishra, V.; Tuscano, G. Decentralized Cloud Storage Using Blockchain. In Proceedings of the 2020 4th International Conference on Trends in Electronics and Informatics (ICOEI)(48184), Tirunelveli, India, 16–18 April 2020; pp. 384–389. [Google Scholar] [CrossRef]

- Lakshman, A.; Malik, P. Cassandra: A decentralized structured storage system. ACM SIGOPS Oper. Syst. Rev. 2010, 44, 35–40. [Google Scholar] [CrossRef]

- Vorick, D.; Champine, L. Sia: Simple decentralized storage. Retrieved May 2014, 8, 2018. [Google Scholar]

- Churyumov, A. Byteball: A Decentralized System for Storage and Transfer of Value. 2016. Available online: https://byteball.org/Byteball.pdf (accessed on 7 March 2022).

- Haeberlen, A.; Mislove, A.; Druschel, P. Glacier: Highly durable, decentralized storage despite massive correlated failures. In Proceedings of the 2nd Conference on Symposium on Networked Systems Design & Implementation, Boston, MA, USA, 2–4 May 2005; Volume 2, pp. 143–158. [Google Scholar]

- Wilkinson, S.; Lowry, J.; Boshevski, T. Metadisk a Blockchain-Based Decentralized File Storage Application; Technical Report, hal; Storj Labs Inc.: Atlanta, GA, USA, 2014; pp. 1–11. Available online: http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.692.8781&rep=rep1&type=pdf (accessed on 7 March 2022).

- Ali, S.; Wang, G.; White, B.; Cottrell, R.L. A Blockchain-Based Decentralized Data Storage and Access Framework for PingER. In Proceedings of the 2018 17th IEEE International Conference on Trust, Security And Privacy in Computing and Communications/12th IEEE International Conference on Big Data Science and Engineering (TrustCom/BigDataSE), New York, NY, USA, 1–3 August 2018; pp. 1303–1308. [Google Scholar] [CrossRef]

- Ruj, S.; Rahman, M.S.; Basu, A.; Kiyomoto, S. BlockStore: A Secure Decentralized Storage Framework on Blockchain. In Proceedings of the 2018 IEEE 32nd International Conference on Advanced Information Networking and Applications (AINA), Krakow, Poland, 16–18 May 2018; pp. 1096–1103. [Google Scholar] [CrossRef]

- Filecoin. 2022. Available online: https://filecoin.io/ (accessed on 7 March 2022).

- Medium. 2022. Available online: https://blog.sia.tech/a-deep-dive-into-skynet-a0fa037feea (accessed on 7 March 2022).

- Alchemy. 2022. Available online: https://www.alchemy.com/ (accessed on 7 March 2022).

- Ankr. 2022. Available online: https://www.ankr.com/ (accessed on 7 March 2022).

- BlockDaemon. 2022. Available online: https://blockdaemon.com/ (accessed on 7 March 2022).

- ChainStack. 2022. Available online: https://chainstack.com/ (accessed on 7 March 2022).

- Subramanian, H. Decentralized blockchain-based electronic marketplaces. Commun. ACM 2017, 61, 78–84. [Google Scholar] [CrossRef]

- Klems, M.; Eberhardt, J.; Tai, S.; Härtlein, S.; Buchholz, S.; Tidjani, A. Trustless Intermediation in Blockchain-Based Decentralized Service Marketplaces. In Service-Oriented Computing. ICSOC 2017. Lecture Notes in Computer Science; Maximilien, M., Vallecillo, A., Wang, J., Oriol, M., Eds.; Springer: Cham, Switzerland, 2017; Volume 10601. [Google Scholar] [CrossRef]

- Gnosis. 2022. Available online: https://gnosis.io/ (accessed on 7 March 2022).

- Lawrenz, S.; Sharma, P.; Rausch, A. Blockchain technology as an approach for data marketplaces. In Proceedings of the 2019 International Conference on Blockchain Technology, Atlanta, GA, USA, 14–17 July 2019; pp. 55–59. [Google Scholar]

- Banerjee, P.; Ruj, S. Blockchain Enabled Data Marketplace—Design and Challenges. arXiv 2018, arXiv:1811.11462. [Google Scholar]

- Xu, R.; Ramachandran, G.S.; Chen, Y.; Krishnamachari, B. BlendSM-DDM: BLockchain-ENabled Secure Microservices for Decentralized Data Marketplaces. In Proceedings of the 2019 IEEE International Smart Cities Conference (ISC2), Casablanca, Morocco, 14–17 October 2019; pp. 14–17. [Google Scholar] [CrossRef] [Green Version]

- Vousinas, G. Supply chain finance: Definition, modern aspects and research challenges ahead. In Supply Chain Finance: Risk Management, Resilience and Supplier Management; Tate, W., Bals, L., Ellram, L., Eds.; Kogan Page: London, UK, 2019; pp. 63–95. Available online: https://www.researchgate.net/publication/327981053_Supply_chain_finance_definition_modern_aspects_and_research_challenges_ahead (accessed on 7 March 2022).

- Wang, R.; Wu, Y. Application of Blockchain Technology in Supply Chain Finance of Beibu Gulf Region. Math. Probl. Eng. 2021, 2021, 5556424. [Google Scholar] [CrossRef]

- Yaksick, R. Overcoming Supply Chain Finance Challenges Via Blockchain Technology. In Disruptive Innovation in Business and Finance in the Digital World (International Finance Review, Vol. 20); Choi, J.J., Ozkan, B., Eds.; Emerald Publishing Limited: Bingley, UK, 2019; pp. 87–100. [Google Scholar] [CrossRef]

- Contour. 2022. Available online: https://contour.network/ (accessed on 7 March 2022).

- Skuchain. 2022. Available online: https://www.skuchain.com/ (accessed on 7 March 2022).

- Etradeconnect. 2022. Available online: https://www.etradeconnect.net/ (accessed on 7 March 2022).

- Kongo. 2022. Available online: https://www.komgo.io/ (accessed on 7 March 2022).

- Marco Polo. 2022. Available online: https://marcopolonetwork.com/ (accessed on 7 March 2022).

- UAE Trade Connect. 2022. Available online: https://avanzainnovations.com/blog/portfolio/utc/ (accessed on 7 March 2022).

- We.trade. 2022. Available online: https://we-trade.com/ (accessed on 7 March 2022).

- Singh, H.; Jain, G.; Munjal, A.; Rakesh, S. Blockchain technology in corporate governance: Disrupting chain reaction or not? Corp. Gov. Int. J. Bus. Soc. 2019, 20, 67–86. [Google Scholar] [CrossRef]

- Yermack, D. Corporate governance and blockchains. Rev. Financ. 2017, 21, 7–31. [Google Scholar] [CrossRef] [Green Version]

- Wiśniewska, A. The initial coin offering—Challenges and opportunities. Copernic. J. Financ. Account. 2018, 7, 99–110. [Google Scholar] [CrossRef]

- Jentzsch, C. Decentralized Autonomous Organization to Automate Governance. White Paper, November 2016. Available online: https://lawofthelevel.lexblogplatformthree.com/wp-content/uploads/sites/187/2017/07/WhitePaper-1.pdf (accessed on 7 March 2022).

- Fenwick, M.; Vermeulen, E.P. Technology and corporate governance: Blockchain, crypto, and artificial intelligence. Tex. J. Bus. L. 2019, 48, 1. [Google Scholar] [CrossRef] [Green Version]

- Aragon. 2022. Available online: https://aragon.org/ (accessed on 7 March 2022).

- DAOStack. 2022. Available online: https://daostack.io/ (accessed on 7 March 2022).

- Colony. 2022. Available online: https://colony.io/ (accessed on 7 March 2022).

- Oguama, L. Fintech Credit Market—Crowdfunding: An Evaluation of Market Models. 20 September 2020. Available online: https://ssrn.com/abstract=3696044 (accessed on 7 March 2022).

- Shneor, R.; Zhao, L.; Flåten, B.T. (Eds.) Advances in Crowdfunding; Springer International Publishing: Berlin, Germany, 2020. [Google Scholar] [CrossRef]

- LendingClub. 2022. Available online: https://www.lendingclub.com/ (accessed on 7 March 2022).

- GoFundMe. 2022. Available online: https://www.gofundme.com/ (accessed on 7 March 2022).

- AngelList. 2022. Available online: https://angel.co/ (accessed on 7 March 2022).

- Kickstarter. 2022. Available online: https://www.kickstarter.com/ (accessed on 7 March 2022).

- Lacasse, R.; Lambert, B.; Roy, N.; Sylvain, J.; Nadeau, F. A digital tsunami: FinTech and crowdfunding. In Proceedings of the International Scientific Conference on Digital Intelligence, Quebec City, QC, Canada, 4–6 April 2016; pp. 1–5. [Google Scholar]

- Baber, H. Blockchain-Based Crowdfunding. In Blockchain Technology for Industry 4.0. Blockchain Technologies; Rosa Righi, R., Alberti, A., Singh, M., Eds.; Springer: Singapore, 2020. [Google Scholar] [CrossRef]

- RealBlocks. 2022. Available online: https://www.realblocks.com/home (accessed on 7 March 2022).

- Meridio. 2022. Available online: https://medium.com/@Meridio (accessed on 7 March 2022).

- QuantmRE. 2022. Available online: https://www.quantmre.com/ (accessed on 7 March 2022).

- Gitcoin. 2022. Available online: https://gitcoin.co/ (accessed on 7 March 2022).

- Brickblock. 2022. Available online: https://www.brickblock.io/ (accessed on 7 March 2022).

- RealtyBits. 2022. Available online: https://www.realtybits.com/ (accessed on 7 March 2022).

- Zhou, Q.; Huang, H.; Zheng, Z.; Bian, J. Solutions to scalability of blockchain: A survey. IEEE Access 2020, 8, 16440–16455. [Google Scholar] [CrossRef]

- Medium. 2022. Available online: https://aakash-111.medium.com/the-scalability-trilemma-in-blockchain-75fb57f646df (accessed on 7 March 2022).

- Nasir, M.H.; Arshad, J.; Khan, M.M.; Fatima, M.; Salah, K.; Jayaraman, R. Scalable blockchains—A systematic review. Future Gener. Comput. Syst. 2022, 126, 136–162. [Google Scholar] [CrossRef]

- Zheng, Z.; Xie, S.; Dai, H.N.; Chen, X.; Wang, H. Blockchain challenges and opportunities: A survey. Int. J. Web Grid Serv. 2018, 14, 352–375. [Google Scholar] [CrossRef]

- Medium. 2022. Available online: https://blog.connext.network/the-interoperability-trilemma-657c2cf69f17 (accessed on 7 March 2022).

- Goldberg, I. On the security of the Tor authentication protocol. In Proceedings of the International Workshop On Privacy Enhancing Technologies, Cambridge, UK, 28–30 June 2006; pp. 316–331. [Google Scholar]

- Feng, Q.; He, D.; Zeadally, S.; Khan, M.K.; Kumar, N. A survey on privacy protection in blockchain system. J. Netw. Comput. Appl. 2019, 126, 45–58. [Google Scholar] [CrossRef]

- Androulaki, E.; Karame, G.O.; Roeschlin, M.; Scherer, T.; Capkun, S. Evaluating user privacy in bitcoin. In Proceedings of the International Conference on Financial Cryptography and Data Security, Okinawa, Japan, 1–5 April 2013; pp. 34–51. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Criterion | Keywords |

|---|---|

| General | Fintech, Blockchain, DLT, Enterprise blockchains |

| Fintech Verticals | payments, banking, investments, capital markets, lending, crowdfunding, insurance services, loyalty programs, supply chain |

| Blockchain related | Public or private blockchains, permissioned, permissionless, bitcoin, ethereum, hyperledger, smart contracts |

| Use cases | Decentralized Applications, stablecoins, digital currency, exchanges, oracles, decentralized finance |

| Search String | Count |

|---|---|

| Decentralized applications | 5 |

| Payments OR Digital Banking | 4 |

| Capital markets | 3 |

| Insurance | 2 |

| Health | 4 |

| Stablecoins | 2 |

| Digital currency | 2 |

| Oracles | 2 |

| Decentralized Finance | 2 |

| Smart contracts | 5 |

| Digital lending | 7 |

| Digital Borrowing | 3 |

| Regtech | 1 |

| Law AND Regulation | 3 |

| Governance | 1 |

| Identity | 2 |

| CBDC | 1 |

| Decentralized Exchanges | 3 |

| Storage | 5 |

| Marketplaces | 1 |

| Concept | Definition |

|---|---|

| AMM | Automated Market Makers, a type of decentralized exchange (DEX) protocol that relies on a mathematical formula to automatically price assets. |

| Block | A data structure within the blockchain database that collects transactions in a period of time and permanently recorded on the blockchain |

| Blockchain | A distributed ledger stored across a peer-to-peer (P2P) network. A blockchain consists of blocks where transactions are permanently recorded by appending blocks. |

| Consensus | A mechanism that is used in blockchain systems to reach an agreement on the network’s current state for the network’s nodes. |

| Cross-chain | Complete decentralisation cannot be achieved unless people on different blockchains are interconnected with each other through one common protocol. Cross-chain technology aims to solve this problem by adding interoperability between different blockchains. It means they will all be able to communicate with each other and share data. |

| dApps | Decentralized Applications that can operate autonomously, typically through the use of smart contracts, that runs on a decentralized computing, blockchain system. |

| DAO | A decentralized autonomous organization (DAO) is a software running on a blockchain that offers users a built-in model for the collective management of its code. |

| Ethereum | A decentralized, open-source blockchain with smart contract functionality |

| Fork | A change of blockchain protocol or data in a public blockchain. It can be a hard fork, resulting in two blockchains or a soft fork, still maintaining one blockchain. |

| Genesis Block | Also called Block 0, is the very first block upon which additional blocks in a blockchain are added. |

| Node | A copy of the ledger operated by a user on the blockchain. |

| Mining | The process of creating a new valid block of transactions to the blockchains. Nodes mining are called miners. |

| Mining pool | A collection of miners who come together to share their processing power over a network and agree to split the rewards of a new block found within the pool. |

| Smart Contract | A contractual governance of transactions between two or more parties that is enforced and verified programmatically with blockchain technology instead of by a central authority. |

| UTXO | UTXO stands for Unspent Transaction Output. The remaining amount of digital currency after executing a cryptocurrency transaction. |

| Wallet | A digital wallet that allows users to store and manage their digital assets such as Bitcoin, Ether, and other cryptocurrencies. Basically, it includes an wallet address derived from the user’s public key, and a private key authenticating for transactions related to the wallet. |

| Platform | Consensus | Transaction Model | Throughput | Private Transactions | Currency/Token | Applications |

|---|---|---|---|---|---|---|

| Bitcoin | Proof of work | UTXO | 7 TPS | Shadow Addresses and Mixing | BTC | Payments |

| Ethereum | Proof of work | Account | 15 TPS | ZK Proofs | ETH | Dapps |

| Cardano | Ouroboros Proof of stake | UTXO | 257 TPS | ZK proofs | ADA | Dapps |

| IOTA | Fast Probabilistic Consensus | UTXO | 1500 TPS | CoinMixing | IOTA | IoT devices |

| Algorand | Pure proof of stake | Account | 1000 TPS | None | ALGO | Payments |

| Hyperledger Fabric | CFT & BFT | Account | 3000 TPS | Channels & ZK proofs | None | Enterprise |

| R3 Corda | Validity & Uniqueness consensus | UTXO | 15-1678 TPS | Inherent support | None | Enterprise |

| Quorum | RAFT and IBFT | Account | 900 TPS | ZK proofs | ETH | Dapps |

| Multichain | PBFT | UTXO | 1000 TPS | Streams | Custom | Enterprise |

| Diem | DiemBFT | Account | 3 TPS | None | DIEM | Payments |

| Company | Platform | Summary |

|---|---|---|

| Contour [182] | R3 Corda | Rebranded from Voltron, targetted towards letters of credit usecase. Revenue model will include monthly subscription fees and transaction fees in the platform. Participants in the network currently include: Bangkok Bank, BNP Paribas, CTBC, Citi, ING, HSBC, SEB, and Standard Chartered. |

| Skuchain [183] | Hyperledger Fabric | Provides end-to-end solution for supply chain finance and not restricted to a particular usecase. Firms pay subscription and transaction fees for using the platform. Currently, the platform is operating across countries including USA, Asia, Europe etc., It is fully interoperable with Corda and Ethereum. |

| eTradeConnect [184] | Hyperledger Fabric | Operated by the Hong Kong Trade Finance Platform Company Limited. Offers multiple products for SCF including purchase order and invoice creation, pre-shipment trade finance and post-shipment trade finance. Current participants include various banks from Australia, Hong Kong and Asia. |

| komgo [185] | Quorum blockchain | Around 150 companies are using this platform. Along with SCF solutions this platform also offers Know-Your-Customer(KYC) and certification feature. They generate revenue through subscription fees and professional services charges for activities like integration. |

| Marco Polo [186] | R3 Corda | Is a network for SCF consisting of over 30 banks globally. The platform is compatible with APIs and legacy systems allowing banks to easily integrate. Marco Polo operates following a license and transaction fee model. |

| UAE Trade Connect [187] | Hyperledger Fabric | 8 banks participated in the product launch. UAE Trade Connect addresses several of the issues with duplicate and fraudulent invoice financing that have posed considerable problems to banks in the industry.It will generate revenue by charging banks for each transaction that they verify. |

| We.trade [188] | Hyperledger Fabric | Through a license fee and transaction fee model, we.trade currently has a number of products that are live, including: Auto-Settlement: automation of payment based on pre-agreed conditions; Bank Payment Undertaking (BPU): confirmation of buyer’s bank to make a payment to the seller; BPU Financing: a financing option for the seller based on the BPU; and Invoice Financing: a financing option for the seller based on a single sales invoice. |

| IPO | ICO | |

|---|---|---|

| Legal status | Detailed regulation | No regulation or insufficient one |

| Securities type | Stocks and bonds | Tokens that may have features of particular types of securities or being vouchers or having no additional attributes at all |

| Risk level | Moderate | High (for the company and investors) |

| Accessibility | For large enterprises, For investors | May be used by almost any company. Anyone who have internet access can become an investor |

| Costs | High | Moderate or low |

| Platform | Launch | DAOs | Token | Market Cap | Features |

|---|---|---|---|---|---|

| Aragon | Oct 2018 | 1700 | ANT | $ 3 billion USD |

|

| DAOStack | Apr 2019 | 22 | GEN | $ 1.6 million USD |

|

| Colony | Jan 2022 | - | CLNY | - |

|

| Name | Launch Year | Summary |

|---|---|---|

| RealBlocks [205] | 2015 | RealBlocks is a decentralized platform built on distributed ledger technology which enables retail and institutional investors to invest in real estate projects. Tokenizes the physical assets and thus allows retail investors to own a part of the project. |

| Meridio [206] | 2017 | Meridio is an online crowdfunding platform for real estate investments. The SaaS solution uses blockchain based technology to convert individual properties into digital shares. Investors can directly connect with landlords by circumventing all traditional intermediaries and co-own properties. The company claims to verify all investors and properties registered on the platform. |

| QuantmRE [207] | 2017 | QuantmRE is an online crowdfunding platform based on blockchain technology. It enables property owners/investors to create a portfolio of assets, receive investments from other investors, and more. It enables homeowners to gain additional value of their homes by enabling others to invest in it. Investors can purchase tokens to begin the process. |

| Gitcoin [208] | 2017 | On-demand requirement for open source software development. Features of gitcoin are fund issues, tip developers, project search, gith hub integrations, and hackathons. It allows freelancers to work on Python, Rust, Ruby, JavaScript, Solidity, HTML, CSS, and Design. |

| Brickblock [209] | 2016 | Brickblock claims to be creating an investment platform that allows individuals to invest directly into ETFs and real estate funds using their cryptocurrency balances. The goal of the project is to create a system that facilitates cross-border investments and access to capital markets round the clock. Enabled by smart contracts, the platform will allow routine dispersion of dividends, reduce entry barriers in terms of paperwork and foreign exchange, and function relatively transparently. |

| RealtyBits [210] | 2018 | It is one of the decentralized crowdfunding platforms that allow investing in American commercial real estate. Real estate investment funds are raised via verified investors. It uses RBX tokens to raise its fund and make investments. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nelaturu, K.; Du, H.; Le, D.-P. A Review of Blockchain in Fintech: Taxonomy, Challenges, and Future Directions. Cryptography 2022, 6, 18. https://doi.org/10.3390/cryptography6020018

Nelaturu K, Du H, Le D-P. A Review of Blockchain in Fintech: Taxonomy, Challenges, and Future Directions. Cryptography. 2022; 6(2):18. https://doi.org/10.3390/cryptography6020018

Chicago/Turabian StyleNelaturu, Keerthi, Han Du, and Duc-Phong Le. 2022. "A Review of Blockchain in Fintech: Taxonomy, Challenges, and Future Directions" Cryptography 6, no. 2: 18. https://doi.org/10.3390/cryptography6020018