COVID-19 Media Chatter and Macroeconomic Reflectors on Black Swan: A Spanish and Indian Stock Markets Comparison

Abstract

:1. Introduction

2. Past Research

2.1. Impact of Social Media, News, and Sentiment

2.2. Predictive Modeling of Stock Markets during COVID-19

3. Methodology

3.1. Isometric Mapping (ISOMAP)

3.2. Gradient Boosting Regression (GBR)

3.3. Performance Indicators

3.4. Explainable Artificial Intelligence (XAI)

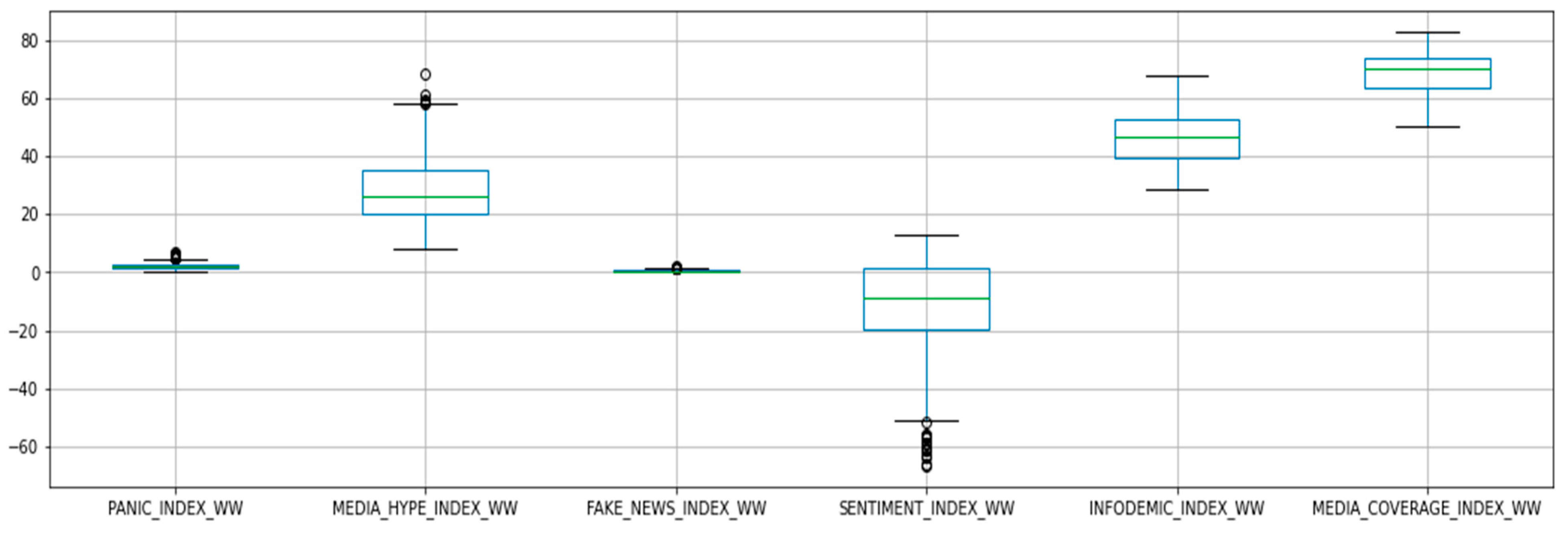

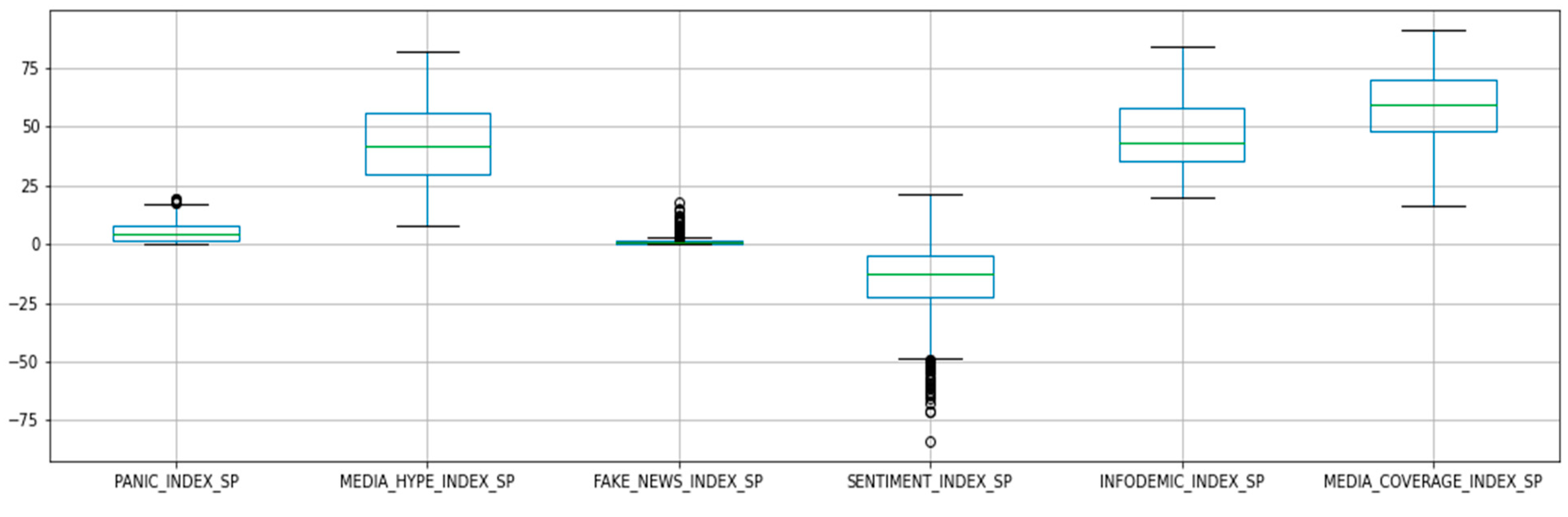

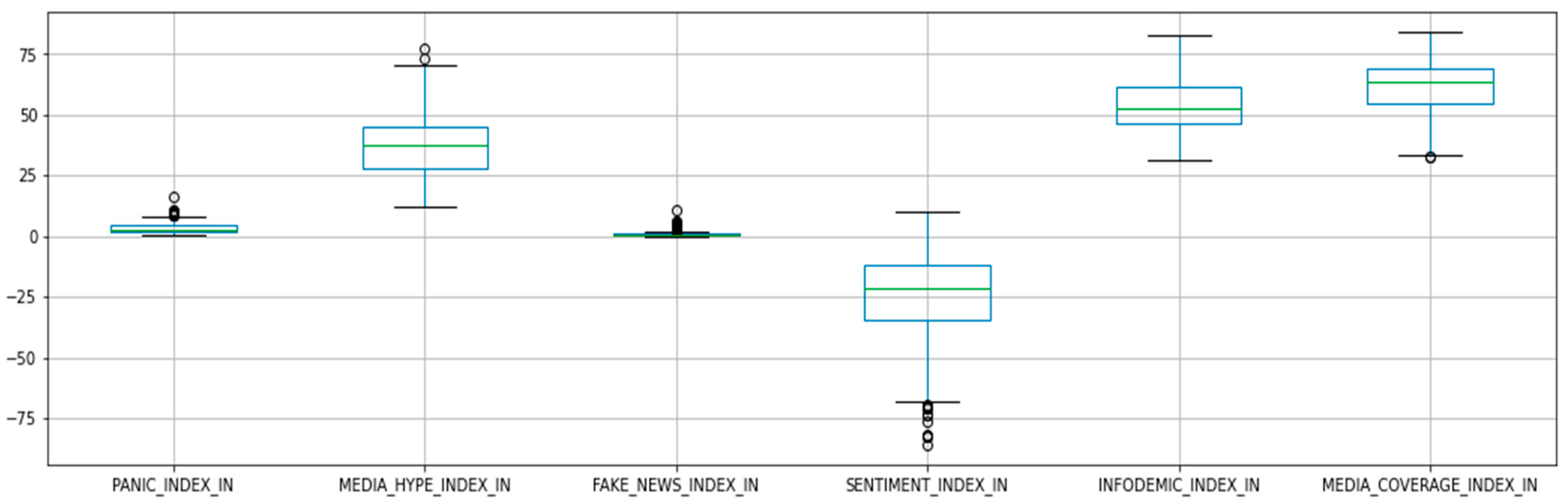

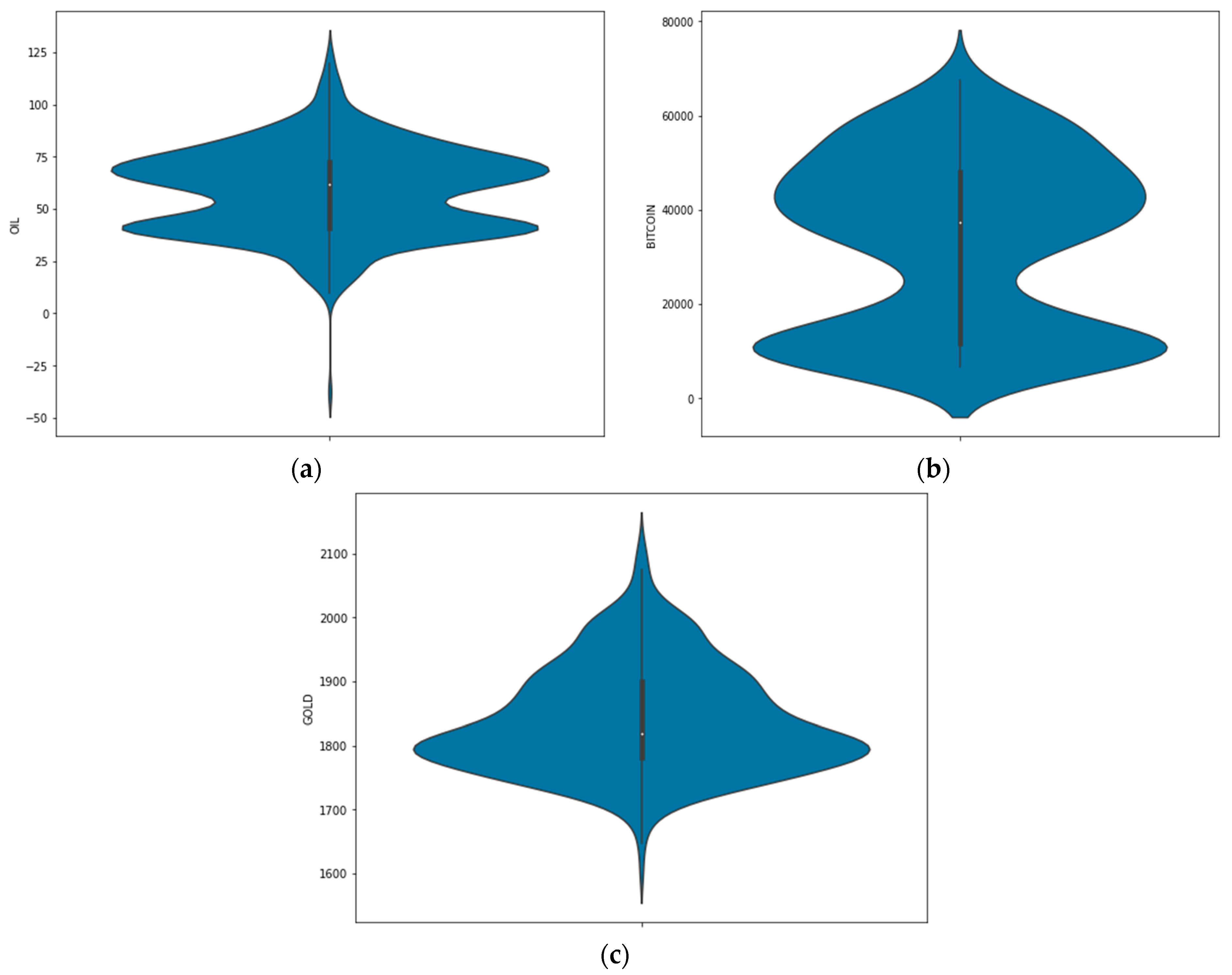

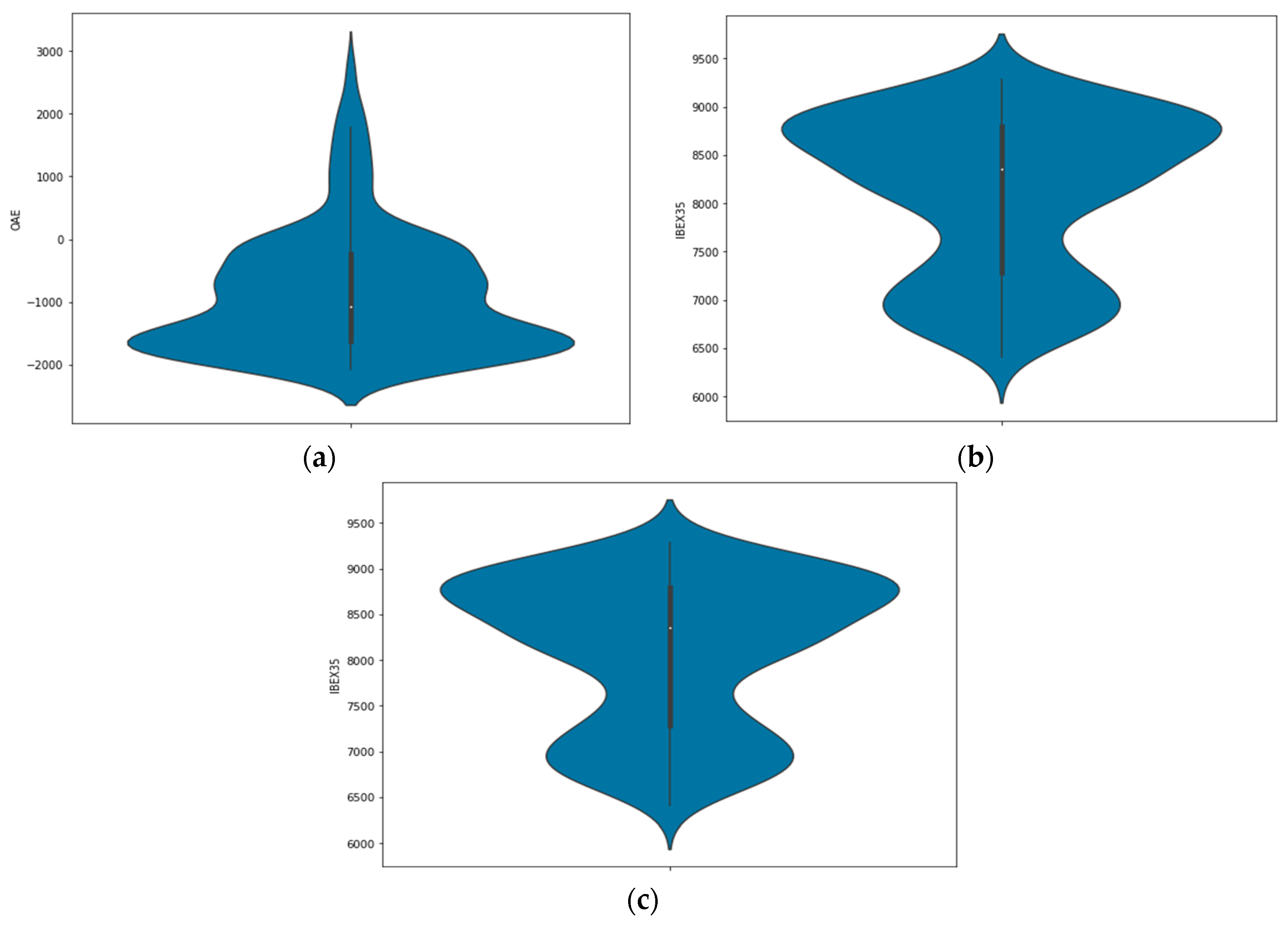

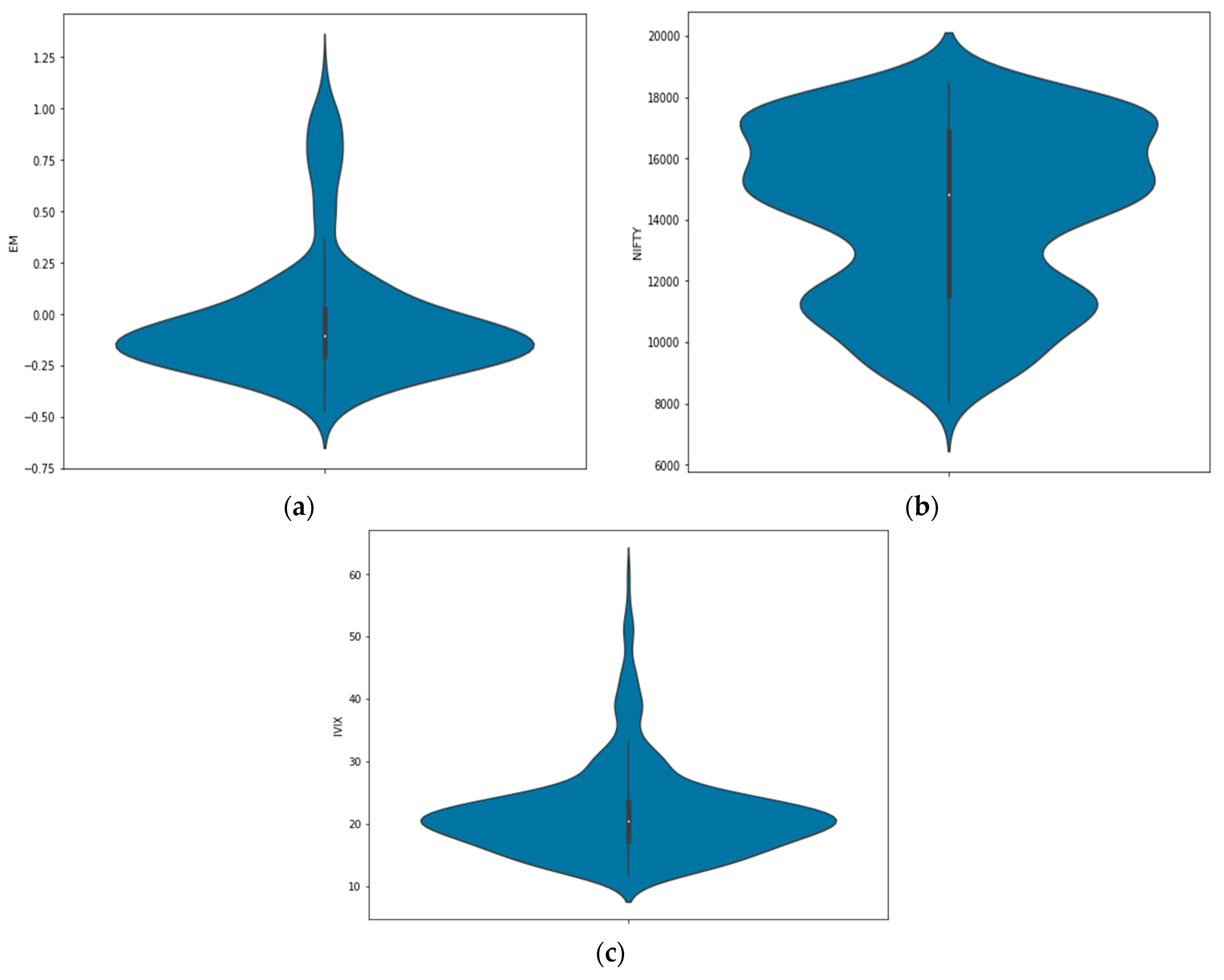

4. Data Description

5. Results & Discussion

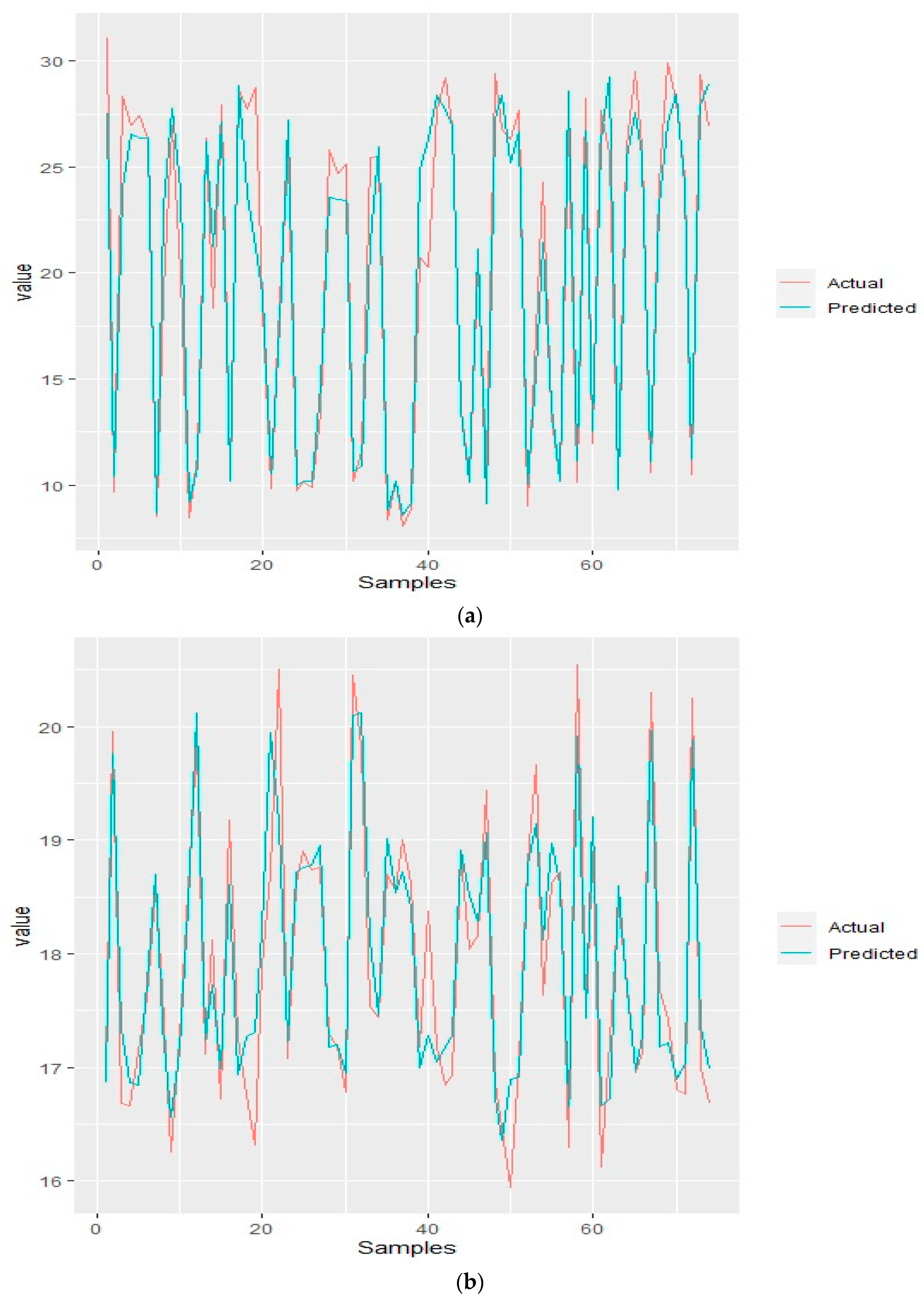

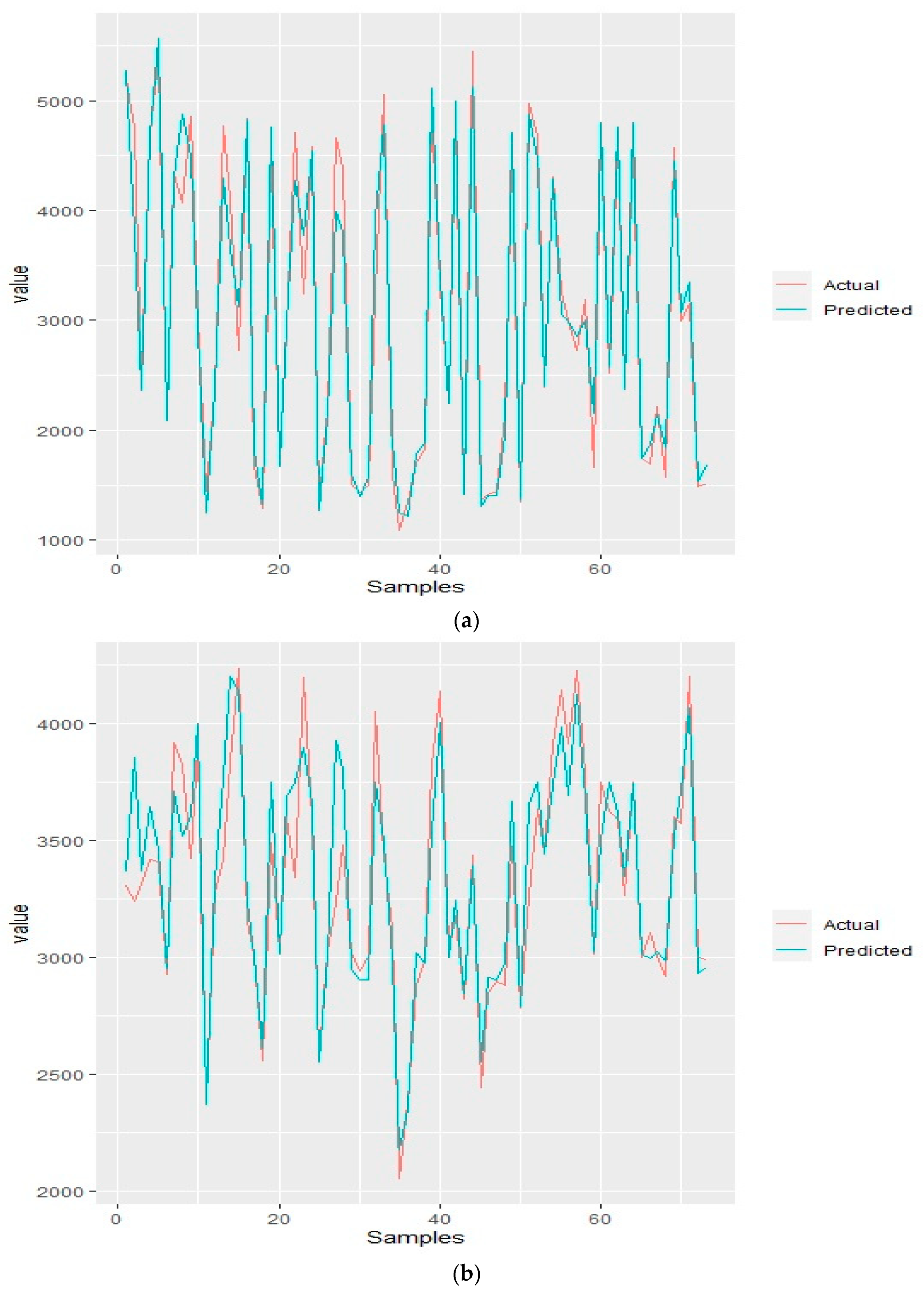

5.1. Predictive Outcome

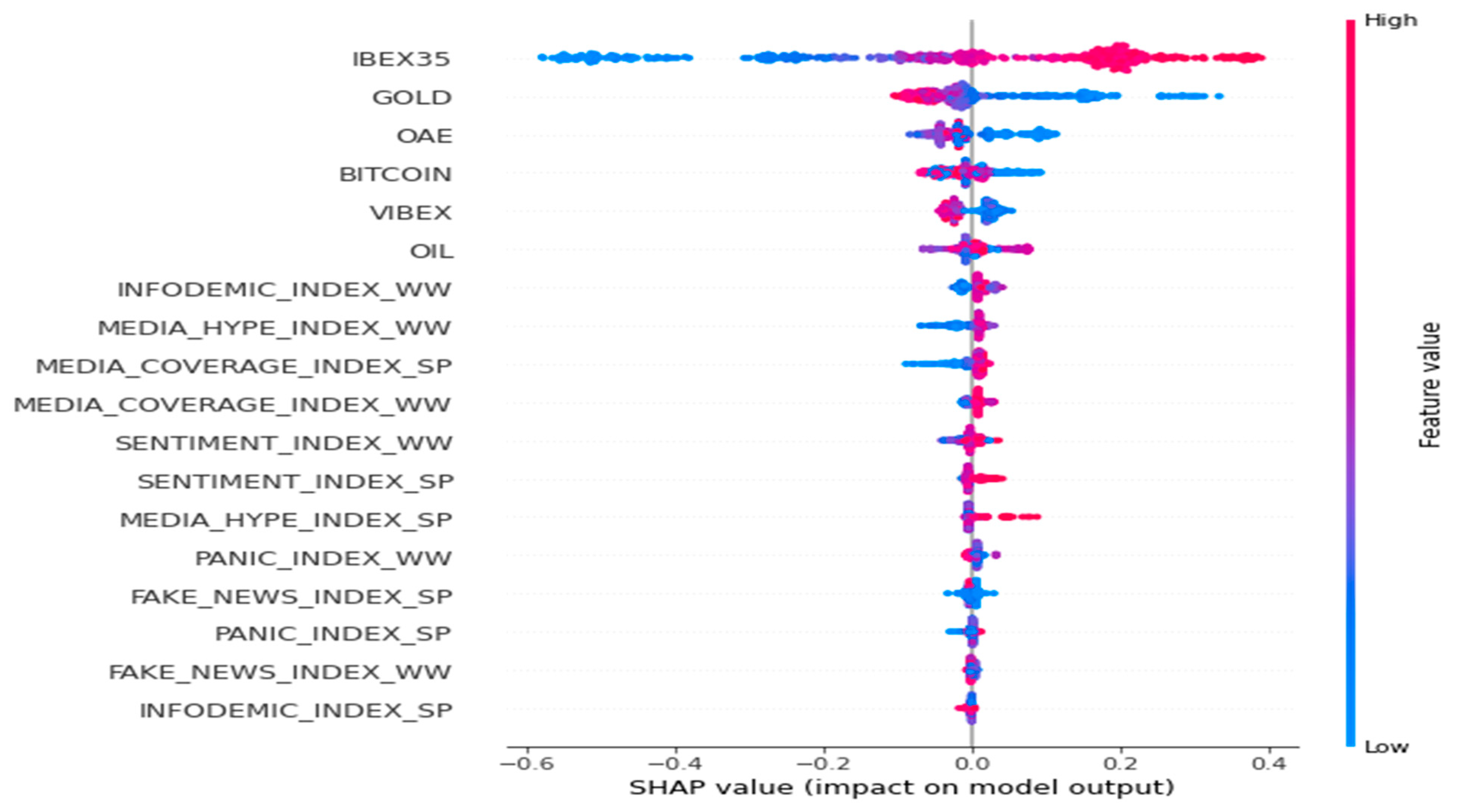

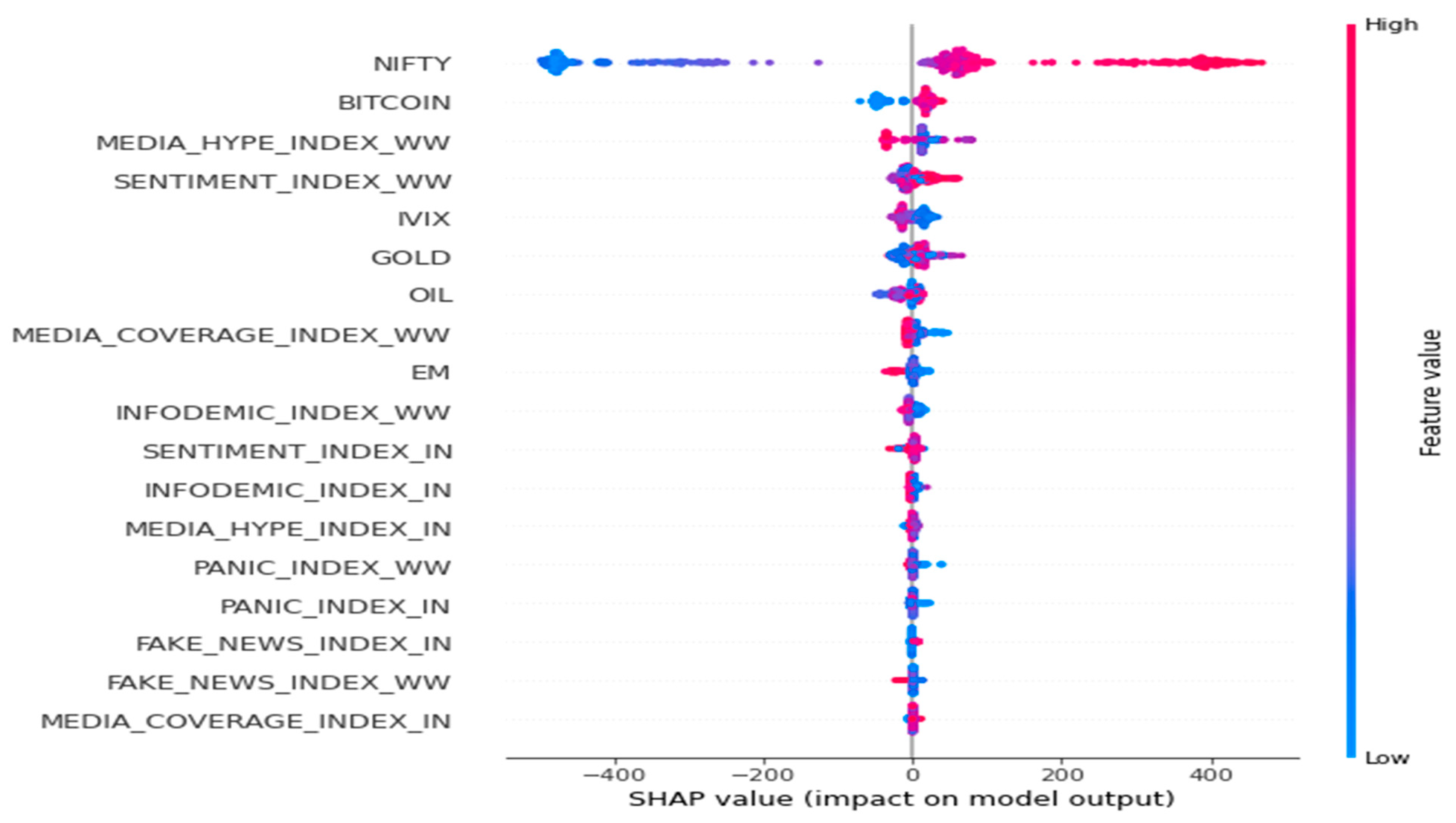

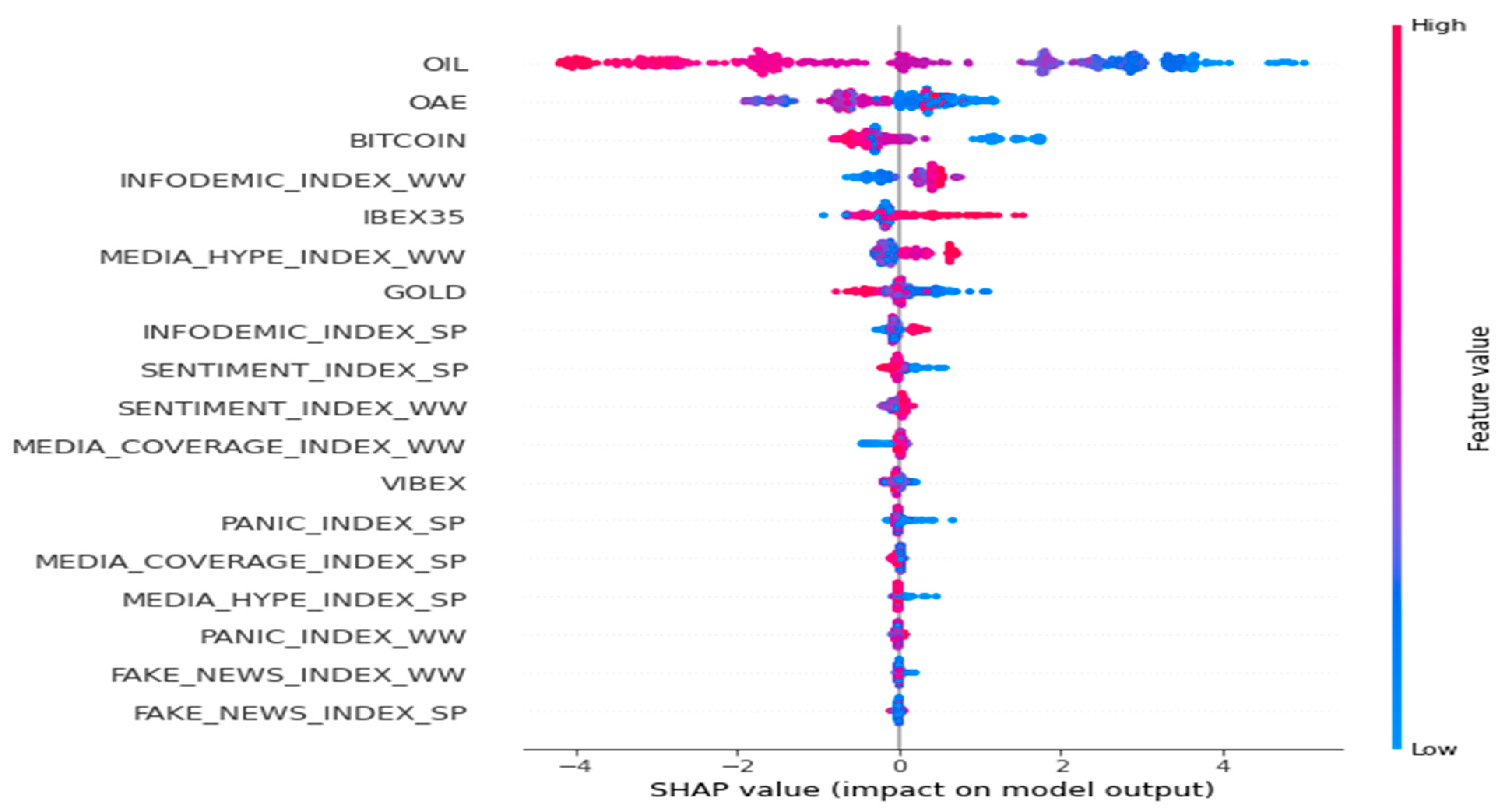

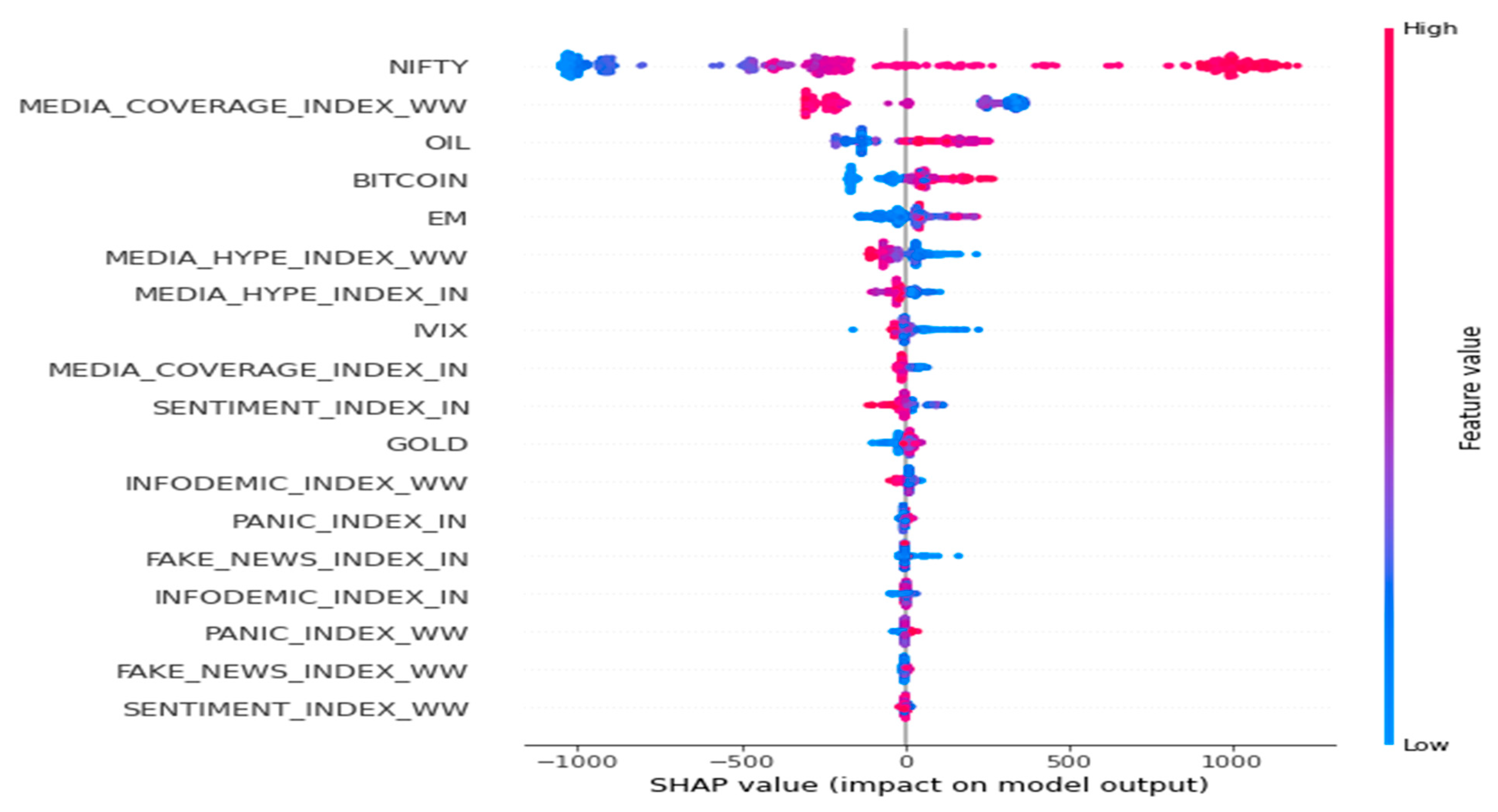

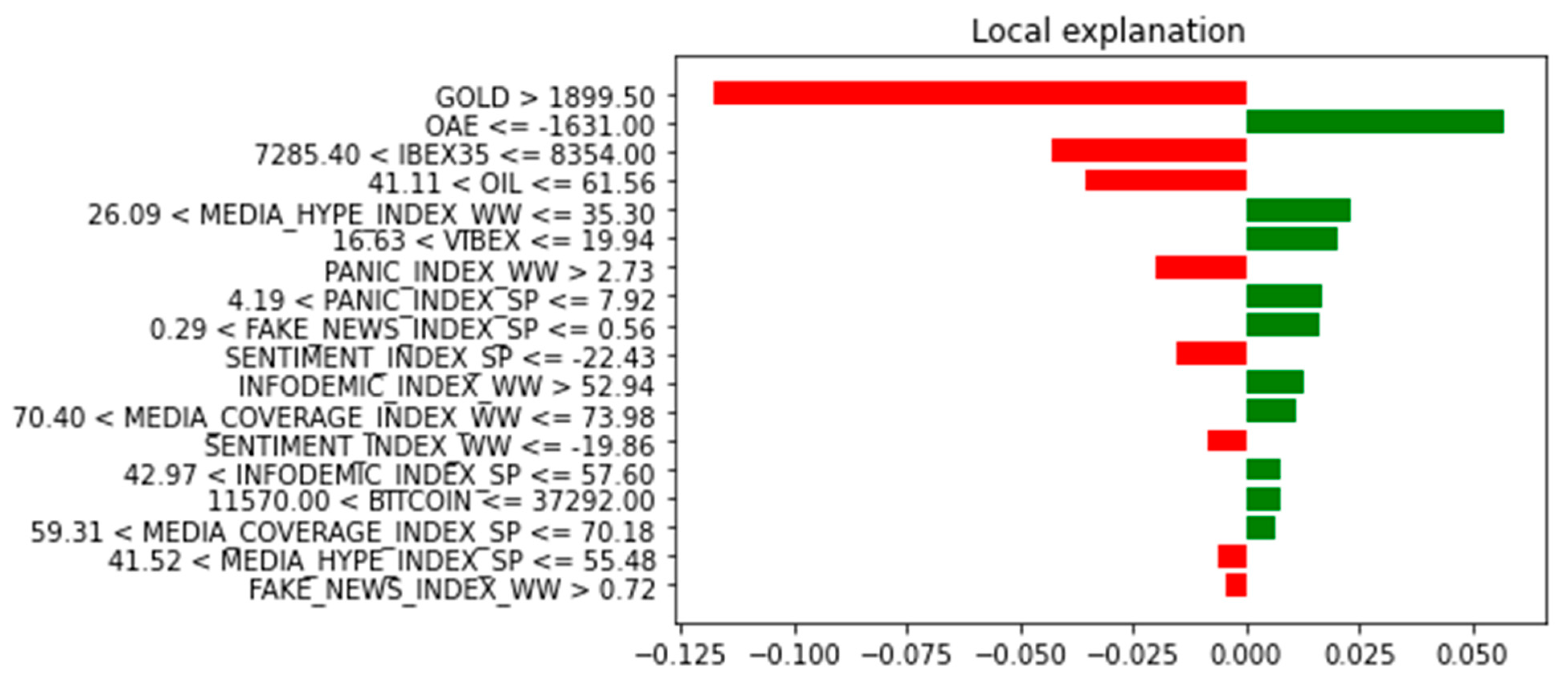

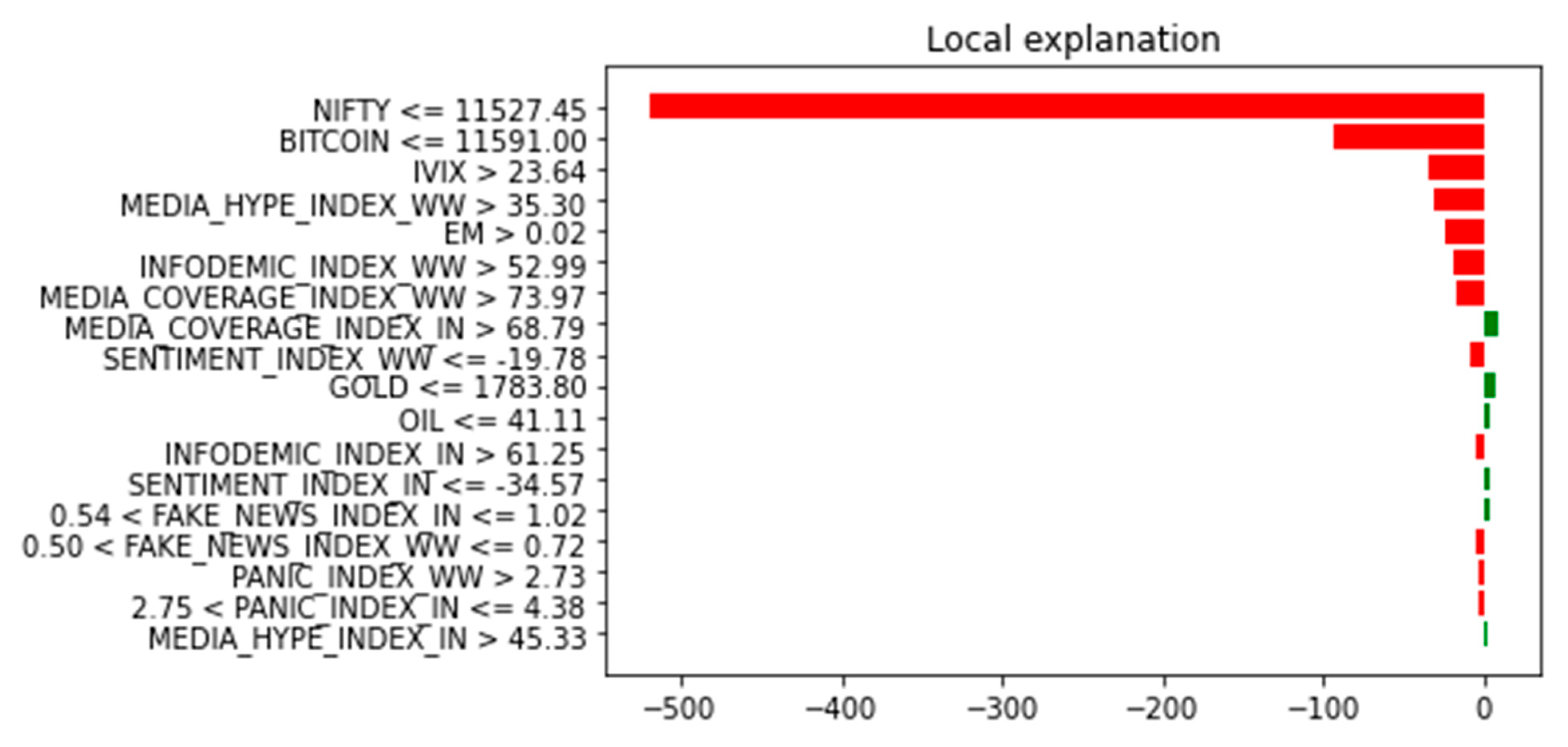

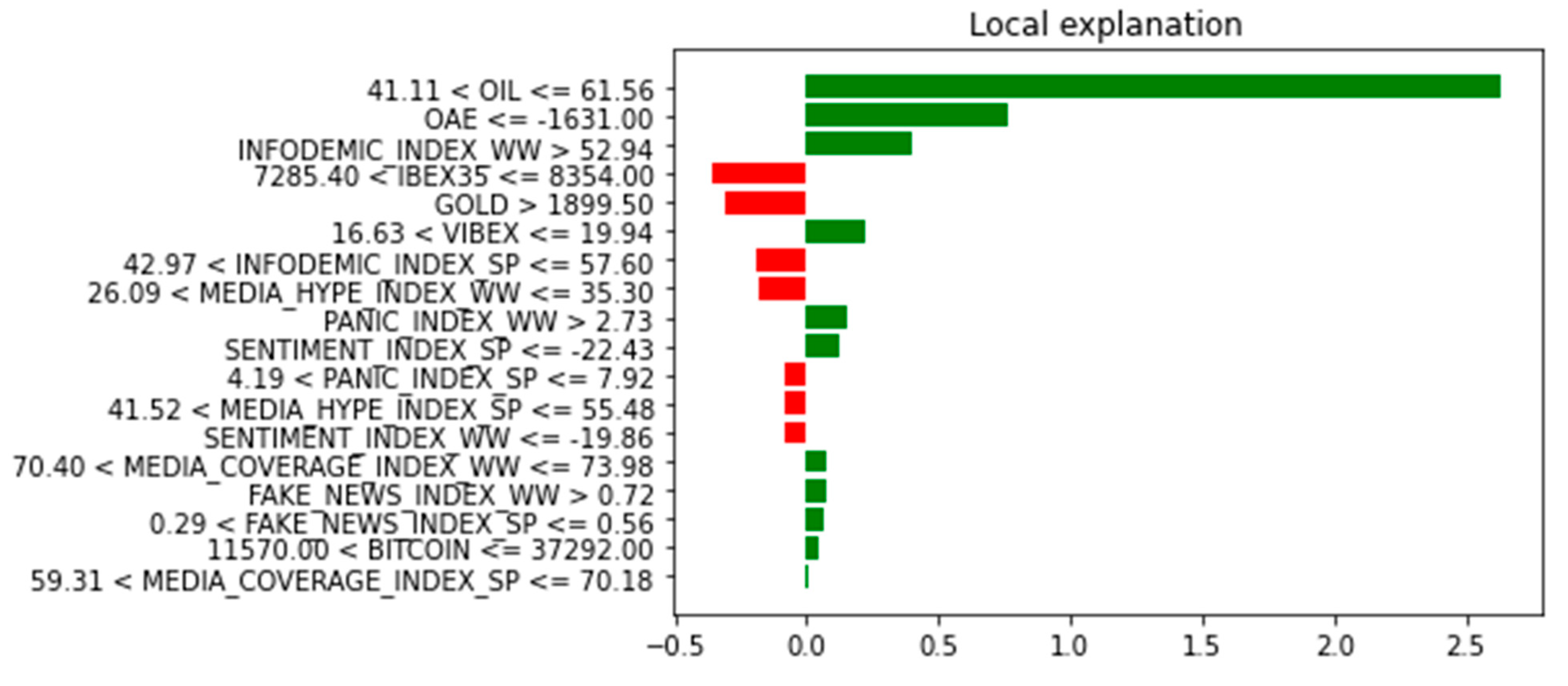

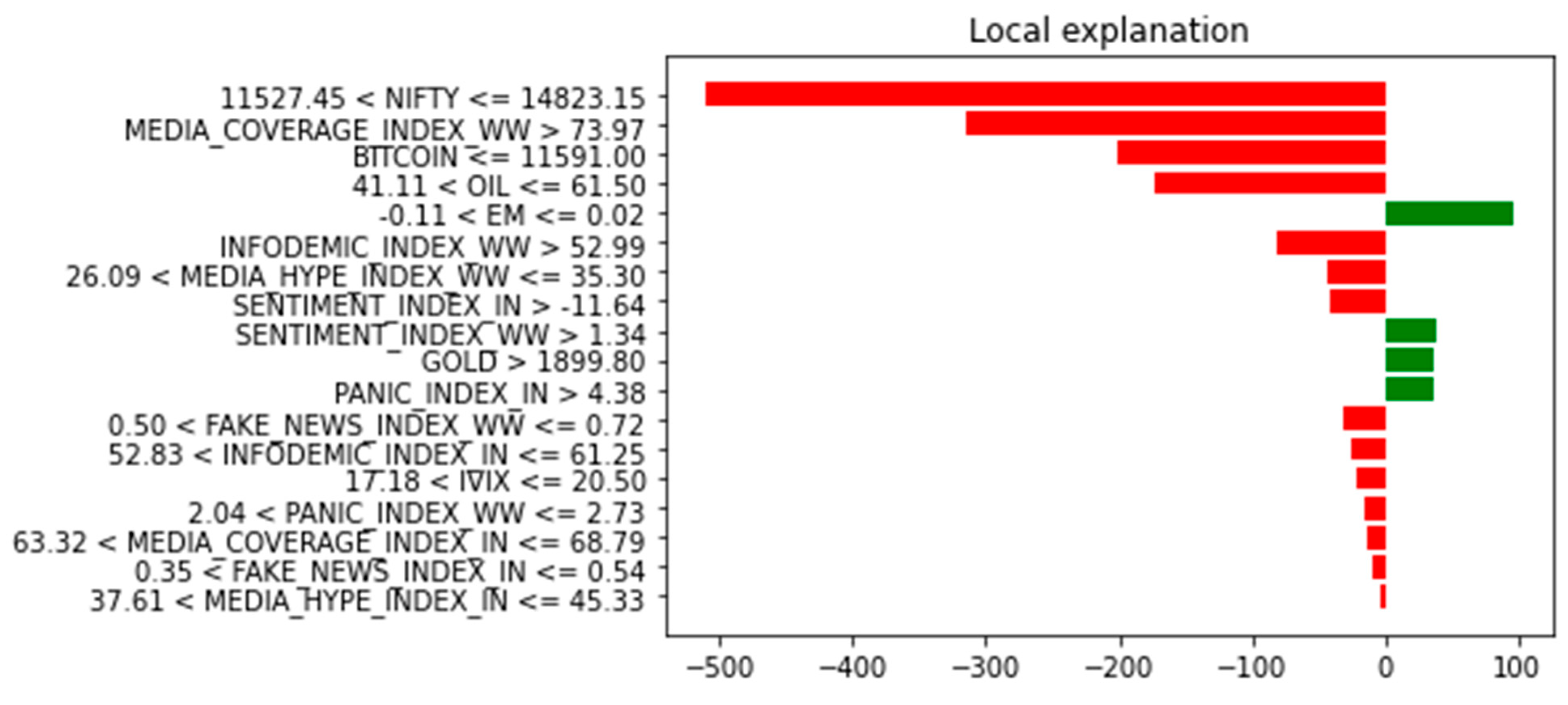

5.2. Model Interpretation

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Ahmar, Ansari Saleh, and Eva Boj Del Val. 2020. SutteARIMA: Short-term forecasting method, a case: COVID-19 and stock market in Spain. Science of The Total Environment 729: 138883. [Google Scholar] [CrossRef]

- Ahmed, W. M. A. 2022. What Drives US Stock Markets during the COVID-19 Pandemic? A Global Sensitivity Analysis. Borsa Istanbul Review 22: 939–60. [Google Scholar] [CrossRef]

- Albaity, Mohamed, Ray Saadaoui Mallek, and Hasan Mustafa. 2022. Bank Stock Return Reactions to the COVID-19 Pandemic: The Role of Investor Sentiment in MENA Countries. Risks 10: 43. [Google Scholar] [CrossRef]

- Albulescu, Claudiu Tiberiu, Aviral Kumar Tiwari, and Phouphet Kyophilavong. 2021. Nonlinearities and Chaos: A New Analysis of CEE Stock Markets. Mathematics 9: 707. [Google Scholar] [CrossRef]

- Ali, Kashif, Muhammad Ashfaque, Adil Saleem, Judit Bárczi, and Judit Sági. 2022a. Did the Islamic Stock Index Provide Shelter for Investors during the COVID-19 Crisis? Evidence from an Emerging Stock Market. Risks 10: 109. [Google Scholar] [CrossRef]

- Ali, Syez Riaz Mahmood, Walid Mensi, Kaysul Islam Anik, Mishtakur Rahman, and Sang Hoong Kang. 2022b. The impacts of COVID-19 crisis on spillovers between the oil and stock markets: Evidence from the largest oil importers and exporters. Economic Analysis and Policy 73: 345–72. [Google Scholar] [CrossRef]

- Araújo, Ricardo De A., Nadia Nedjah, José M. de Sexias, Adriano L. I. Oliveira, and Silvio R. De Meira. 2018. Evolutionary-morphological learning machines for high-frequency financial time series prediction. Swarm and Evolutionary Computation 42: 1–15. [Google Scholar] [CrossRef]

- Asawa, Parth, Manas Gaur, Kaushik Roy, and Amit Sheth. 2020. COVID-19 in Spain and India: Comparing Policy Implications by Analyzing Epidemiological and Social Media Data. arXiv. [Google Scholar] [CrossRef]

- Asl, Mahdi Ghaemi, Oluwasegun Babatunde Adekoya, Muhammad Mahdi Rashidi, Mohammad Ghasemi Doudkanlou, and Ali Dolatabadi. 2022. Forecast of Bayesian-based dynamic connectedness between oil market and Islamic stock indices of Islamic oil-exporting countries: Application of the cascade-forward backpropagation network. Resources Policy 77: 102778. [Google Scholar] [CrossRef]

- Bai, Chenjiang, Yuejiao Duan, Xiaoyun Fan, and Shuai Tang. 2023. Financial market sentiment and stock return during the COVID-19 pandemic. Finance Research Letters 54: 103709. [Google Scholar] [CrossRef]

- Barky, Walid, Peter John Kavalmthara, Vivienne Saverimuttu, Yiyang Liu, and Sajan Cyril. 2022. Response of stock market volatility to COVID-19 announcements and stringency measures: A comparison of developed and emerging markets. Finance Research Letters 46: 102350. [Google Scholar] [CrossRef]

- Benlagha, Noureddine, and Salaheddine El Omari. 2022. Connectedness of stock markets with gold and oil: New evidence from COVID-19 pandemic. Finance Research Letters 46: 102373. [Google Scholar] [CrossRef] [PubMed]

- Bhatnagar, Mukul, Ercan Özen, Sanjay Taneja, Simon Grima, and Ramon Rupeika-Apoga. 2022. The Dynamic Connectedness between Risk and Return in the Fintech Market of India: Evidence Using the GARCH-M Approach. Risks 10: 209. [Google Scholar] [CrossRef]

- Çelik, Taha Buğra, Özgür İcan, and Elif Bulut. 2023. Extending machine learning prediction capabilities by explainable AI in financial time series prediction. Applied Soft Computing 132: 109876. [Google Scholar] [CrossRef]

- Cepoi, Cosmin Octavian. 2020. Asymmetric dependence between stock market returns and news during COVID-19 financial turmoil. Finance Research Letters 36: 101658. [Google Scholar] [CrossRef]

- Chen, Qian, Xiang Gao, Jianming Mo, and Zhouling Xu. 2022. Market Reaction to Local Attention around Earnings Announcements in China: Evidence from Internet Search Activity. International Journal of Financial Studies 10: 97. [Google Scholar] [CrossRef]

- Chundakkadan, Radeef, and Elizabeth Nedumparambil. 2021. In search of COVID-19 and stock market behavior. Global Finance Journal 54: 100639. [Google Scholar] [CrossRef]

- Das, Debojyoti, M. Kannadhasan, and Malay Bhattacharyya. 2019. Do the emerging stock markets react to international economic policy uncertainty, geopolitical risk and financial stress alike? The North American Journal of Economics and Finance 48: 1–19. [Google Scholar] [CrossRef]

- Dash, Rajashree, P. K. Dash, and Ranjeetha Bisoi. 2014. A self adaptive differential harmony search based optimized extreme learning machine for financial time series prediction. Swarm and Evolutionary Computation 19: 25–42. [Google Scholar] [CrossRef]

- Dash, Saumya Ranjan, and Debasish Maitra. 2022. The COVID-19 pandemic uncertainty, investor sentiment, and global equity markets: Evidence from the time-frequency co-movements. The North American Journal of Economics and Finance 62: 101712. [Google Scholar] [CrossRef]

- Dey, Asim K., G. M. Tofiqul Hoque, Kumer P. Das, and Irina Panovska. 2022. Impacts of COVID-19 local spread and Google search trend on the US stock market. Physica A: Statistical Mechanics and Its Applications 589: 126423. [Google Scholar] [CrossRef] [PubMed]

- Ding, Guangyu, and Liangxi Qin. 2020. Study on the prediction of stock price based on the associated network model of LSTM. International Journal of Machine Learning and Cybernetics 11: 1307–17. [Google Scholar] [CrossRef]

- Drake, Pamela Peterson. 2022. The gold-stock market relationship during COVID-19. Finance Research Letters 44: 102111. [Google Scholar] [CrossRef] [PubMed]

- Elliott, D. L., K. C. Santosh, and Charles Anderson. 2020. Gradient boosting in crowd ensembles for Q-learning using weight sharing. International Journal of Machine Learning and Cybernetics 11: 2275–87. [Google Scholar] [CrossRef]

- Gao, Xiaofang, Jiye Liang, Wenjian Wang, Xuefei Bai, and Lina Jia. 2022. An unsupervised multi-manifold discriminant isomap algorithm based on the pairwise constraints. International Journal of Machine Learning and Cybernetics 13: 1317–36. [Google Scholar] [CrossRef]

- Garcia-Vega, Sergio, Xiao Jun Zeng, and John Keane. 2020. Stock returns prediction using kernel adaptive filtering within a stock market interdependence approach. Expert Systems with Applications 160: 113668. [Google Scholar] [CrossRef]

- Ghosh, Indranil, and Tamal Datta Chaudhuri. 2021. FEB-Stacking and FEB-DNN Models for Stock Trend Prediction: A Performance Analysis for Pre and Post COVID-19 Periods. Decision Making: Applications in Management and Engineering 4: 51–84. [Google Scholar] [CrossRef]

- Ghosh, Indranil, and Tamal Datta Chaudhuri. 2022. Integrating Navier-Stokes equation and neoteric iForest-BorutaShap-Facebook’s prophet framework for stock market prediction: An application in Indian context. Expert Systems with Applications 210: 118391. [Google Scholar] [CrossRef]

- Ghosh, Indranil, Esteban Alfaro-Cortés, Matías Gámez, and Noelia García-Rubio. 2023. Role of proliferation COVID-19 media chatter in predicting Indian stock market: Integrated framework of nonlinear feature transformation and advanced AI. Expert Systems with Applications 219: 119695. [Google Scholar] [CrossRef]

- Ghosh, Indranil, Rabin K. Jana, and Manas K. Sanyal. 2019. Analysis of temporal pattern, causal interaction and predictive modeling of financial markets using nonlinear dynamics, econometric models and machine learning algorithms. Applied Soft Computing 82: 105553. [Google Scholar] [CrossRef]

- Ghosh, Indranil, Tamal Datta Chaudhuri, Esteban Alfaro-Cortés, Matías G. Martínez, and Noelia García-Rubio. 2021. Estimating the relative effects of raw material prices, sectoral outlook and market sentiment on stock prices. Resources Policy 73: 102158. [Google Scholar] [CrossRef]

- Ghosh, Indranil, Tamal Datta Chaudhuri, Esteban Alfaro-Cortés, Matías Gámez, and Noelia García. 2022. A hybrid approach to forecasting futures prices with simultaneous consideration of optimality in ensemble feature selection and advanced artificial intelligence. Technological Forecasting and Social Change 181: 121757. [Google Scholar] [CrossRef]

- Hasan, Md Bokhtiar, M. Kabir Hassan, Md Mamunur Rashid, and Yasser Alhenawi. 2021. Are safe haven assets really safe during the 2008 global financial crisis and COVID-19 pandemic? Global Finance Journal 50: 100668. [Google Scholar] [CrossRef]

- Hsu, Yu Lin, and Leilei Tang. 2022. Effects of investor sentiment and country governance on unexpected conditional volatility during the COVID-19 pandemic: Evidence from global stock markets. International Review of Financial Analysis 82: 102186. [Google Scholar] [CrossRef]

- Huang, Qi An, Jun Chan Zhao, and Xiao Qun Wu. 2022. Financial risk propagation between Chinese and American stock markets based on multilayer networks. Physica A: Statistical Mechanics and its Applications 586: 126445. [Google Scholar] [CrossRef]

- Inglada-Perez, Lucia. 2020. A Comprehensive Framework for Uncovering Non-Linearity and Chaos in Financial Markets: Empirical Evidence for Four Major Stock Market Indices. Entropy 22: 1435. [Google Scholar] [CrossRef]

- Jana, Rabin K., and Indranil Ghosh. 2022. A residual driven ensemble machine learning approach for forecasting natural gas prices: Analyses for pre-and during-COVID-19 phases. Annals of Operations Research. [Google Scholar] [CrossRef]

- Jana, Rabin K., Indranil Ghosh, Fred Jawadi, Gazi Salah Uddin, and Ricardo M. Sousa. 2022. COVID-19 news and the US equity market interactions: An inspection through econometric and machine learning lens. Annals of Operations Research. [Google Scholar] [CrossRef]

- Kamal, Javed Bin, and Mark Wohar. 2023. Heterogenous responses of stock markets to covid related news and sentiments: Evidence from the 1st year of pandemic. International Economics 173: 68–83. [Google Scholar] [CrossRef]

- Kamaludin, Kamilah, Sheela Sundarasen, and Izani Ibrahim. 2021. COVID-19, Dow Jones and equity market movement in ASEAN-5 countries: Evidence from wavelet analyses. Heliyon 7: e05851. [Google Scholar] [CrossRef]

- Kamdem, Jules Sadefo, Rose. Bandolo Essomba, and James Njong Berinyuy. 2020. Deep learning models for forecasting and analyzing the implications of COVID-19 spread on some commodities markets volatilities. Chaos, Solitons & Fractals 140: 110215. [Google Scholar] [CrossRef]

- Khalfaoui, Rabeh, Salma Mefteh-Wali, Buhari Dogan, and Sudeshna Ghosh. 2023. Extreme spillover effect of COVID-19 pandemic-related news and cryptocurrencies on green bond markets: A quantile connectedness analysis. International Review of Financial Analysis 86: 102496. [Google Scholar] [CrossRef] [PubMed]

- Kubiczek, Jakub, and Marcin Tuszkiewicz. 2022. Intraday Patterns of Liquidity on the Warsaw Stock Exchange before and after the Outbreak of the COVID-19 Pandemic. International Journal of Financial Studies 10: 13. [Google Scholar] [CrossRef]

- Lange, Petter Eilif de, Borger Melsom, Christian Bakke Vennerød, and Sjur Westgaard. 2022. Explainable AI for Credit Assessment in Banks. Journal of Risk and Financial Management 15: 556. [Google Scholar] [CrossRef]

- Li, Cong, Shiwei Lin, Yihan Sun, Sahar Afshan, and Tanzeela Yaqoob. 2022. The asymmetric effect of oil price, news-based uncertainty, and COVID-19 pandemic on equity market. Resources Policy 77: 102740. [Google Scholar] [CrossRef] [PubMed]

- Lúcio, Francisco, and Jorge Caiado. 2022. COVID-19 and Stock Market Volatility: A Clustering Approach for S&P 500 Industry Indices. Finance Research Letters 49: 103141. [Google Scholar] [CrossRef]

- Lundberg, Scott, and Su In Lee. 2017. A Unified Approach to Interpreting Model Predictions. arXiv. [Google Scholar] [CrossRef]

- Ma, Feng, Xinjie Lu, Jia Liu, and Dengshi Huang. 2022. Macroeconomic attention and stock market return predictability. Journal of International Financial Markets Institutions and Money 79: 101603. [Google Scholar] [CrossRef]

- Makatjane, Katleho, and Ntebogang Moroke. 2021. Predicting Extreme Daily Regime Shifts in Financial Time Series Exchange/Johannesburg Stock Exchange—All Share Index. International Journal of Financial Studies 9: 18. [Google Scholar] [CrossRef]

- Melis, Marco, Michele Scalas, Ambra Demontis, Davide Maiorca, Battista Biggio, Giorgio Giacinto, and Fabio Roli. 2021. Do gradient-based explanations tell anything about adversarial robustness to android malware? International Journal of Machine Learning and Cybernetics 13: 217–32. [Google Scholar] [CrossRef]

- Nguyen, Khanh Quoc. 2022. The correlation between the stock market and Bitcoin during COVID-19 and other uncertainty periods. Finance Research Letters 46: 102284. [Google Scholar] [CrossRef] [PubMed]

- Noreen, Umara, Attayah Shafique, Usman Ayub, and Syed Kashif Saeed. 2022. Does the Adaptive Market Hypothesis Reconcile the Behavioral Finance and the Efficient Market Hypothesis? Risks 10: 168. [Google Scholar] [CrossRef]

- Polamuri, Subba Rao, Kudipudi Srinivas, and A. Krishna Mohan. 2021. Multi-Model Generative Adversarial Network Hybrid Prediction Algorithm (MMGAN-HPA) for stock market prices prediction. Journal of King Saud University - Computer and Information Sciences 34: 7433–44. [Google Scholar] [CrossRef]

- Qiu, Mingyue, Yu Song, and Fumio Akagi. 2016. Application of artificial neural network for the prediction of stock market returns: The case of the Japanese stock market. Chaos, Solitons & Fractals 85: 1–7. [Google Scholar] [CrossRef]

- RavenPack. 2023. Coronavirus Media Monitor. Available online: https://www.ravenpack.com/solutions/research/coronavirus-media-monitor (accessed on 3 May 2022).

- Ravi, Vadlamani, Dadabada Pradeepkumar, and Kalyanmoy Deb. 2017. Financial time series prediction using hybrids of chaos theory, multi-layer perceptron and multi-objective evolutionary algorithms. Swarm and Evolutionary Computation 36: 136–49. [Google Scholar] [CrossRef]

- Ribeiro, Marco Tulio, Sameer Singh, and Carlos Guestrin. 2016. “Why should I trust you?” Explaining the predictions of any classifier. Paper presented at 22nd ACM SIGKDD Conference, San Francisco, CA, USA, August 13–17. [Google Scholar] [CrossRef]

- Ronaghi, Farnoush, Mohammad Salimibeni, Farnoosh Naderkhani, and Arash Mohammadi. 2022. COVID19-HPSMP: COVID-19 adopted Hybrid and Parallel deep information fusion framework for stock price movement prediction. Expert Systems with Applications 187: 115879. [Google Scholar] [CrossRef]

- Saetia, Kittipob, and Jiraphat Yokrattanasak. 2023. Stock Movement Prediction Using Machine Learning Based on Technical Indicators and Google Trend Searches in Thailand. International Journal of Financial Studies 11: 5. [Google Scholar] [CrossRef]

- Salisu, Afees A., and Xuan Vinh Vo. 2020. Predicting stock returns in the presence of COVID-19 pandemic: The role of health news. International Review of Financial Analysis 71: 101546. [Google Scholar] [CrossRef]

- Schapire, Robert E., and Yoram Singer. 1999. Improved boosting algorithms using confidence-rated predictions. Machine Learning 37: 297–336. [Google Scholar] [CrossRef]

- Sharma, Gagan Deep, Aviral Kumar Tiwari, Mansi Jain, Anshita Yadav, and Burak Erkut. 2021. Unconditional and conditional analysis between COVID-19 cases, temperature, exchange rate and stock markets using wavelet coherence and wavelet partial coherence approaches. Heliyon 7: e06181. [Google Scholar] [CrossRef]

- Sinlapates, Parichat, Tanit Sriwong, and Surachai Chancharat. 2023. Risk Spillovers between Bitcoin and ASEAN+6 Stock Markets before and after COVID-19 Outbreak: A Comparative Analysis with Gold. Journal of Risk and Financial Management 16: 103. [Google Scholar] [CrossRef]

- Spulbar, Cristi, Jatin Trivedi, and Ramona Birau. 2020. Investigating abnormal volatility transmission patterns between emerging and developed stock markets: A case study. Journal of Business Economics and Management 21: 1561–92. [Google Scholar] [CrossRef]

- Tenenbaum, Joshua B., Vin De Silva, and John C. Langford. 2000. A Global Geometric Framework for Nonlinear Dimensionality Reduction. Science 290: 2319–23. [Google Scholar] [CrossRef] [PubMed]

- Thangamuthu, Mohanasundaram, Suneel Maheshwari, and Deepak Raghava Naik. 2022. Volatility Spillover Effects during Pre-and-Post COVID-19 Outbreak on Indian Market from the USA, China, Japan, Germany, and Australia. Journal of Risk and Financial Management 15: 378. [Google Scholar] [CrossRef]

- Thorbecke, Willem. 2022. Understanding the transmission of COVID-19 news to French financial markets in early 2020. International Economics 170: 103–14. [Google Scholar] [CrossRef]

- World Bank. 2022. The World Bank/Data/Countries and Economies. Available online: https://data.worldbank.org/country (accessed on 3 May 2022).

- WTO. 2022. World Trade Organization. Trade Profiles. Available online: https://www.wto.org/english/res_e/statis_e/trade_profiles_list_e.htm (accessed on 3 May 2022).

- Yousfi, Mohamed, Younes Ben Zaied, Nidhaleddine Ben Cheikh, Béchir Ben Lahouel, and Houssem Bouzgarrou. 2021. Effects of the COVID-19 pandemic on the US stock market and uncertainty: A comparative assessment between the first and second waves. Technological Forecasting and Social Change 167: 120710. [Google Scholar] [CrossRef]

- Yu, Xiaoling, and Kaitian Xiao. 2022. Dependencies and Volatility Spillovers among Chinese Stock and Crude Oil Future Markets: Evidence from Time-Varying Copula and BEKK-GARCH Models. Journal of Risk and Financial Management 15: 491. [Google Scholar] [CrossRef]

- Yu, Xiaoling, Kaitian Xiao, and Junping Liu. 2022. Dynamic co-movements of COVID-19 pandemic anxieties and stock market returns. Finance Research Letters 46: 102219. [Google Scholar] [CrossRef]

- Zeng, Qing, Xinjie Lu, Tao Li, and Lan Wu. 2022. Jumps and stock market variance during the COVID-19 pandemic: Evidence from international stock markets. Finance Research Letters 48: 102896. [Google Scholar] [CrossRef]

- Zhang, Hongwei, Huojun Hong, Yaoqi Guo, and Cai Yang. 2022. Information spillover effects from media coverage to the crude oil, gold, and Bitcoin markets during the COVID-19 pandemic: Evidence from the time and frequency domains. International Review of Economics & Finance 78: 267–85. [Google Scholar] [CrossRef]

- Zhang, Yongmin, and Jiaying Mao. 2022. COVID-19’s impact on the spillover effect across the Chinese and U.S. stock markets. Finance Research Letters 47: 102684. [Google Scholar] [CrossRef]

- Zheng, Songfeng. 2011. Gradient descent algorithms for quantile regression with smooth approximation. International Journal of Machine Learning and Cybernetics 2: 191–207. [Google Scholar] [CrossRef]

- Zhou, Yang, Xiaoxiao Wang, Rebecca Kechen Dong, Ruihui Pu, and Xioa Guang Yue. 2022. Natural resources commodity prices volatility: Evidence from COVID-19 for the US economy. Resources Policy 78: 102895. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Series | Mean | Std. Dev. | Frosini Test | ADF Test | Terasvirta’s NN Test | Hurst Exponent |

|---|---|---|---|---|---|---|

| Spanish stocks | ||||||

| ARCELORMITTAL | 20.229 | 7.703 | 54.312 *** | 1.000 # | 105.88 *** | 0.872 *** |

| EBRO | 18.00 | 1.188 | 1.087 *** | −0.707 # | 649.94 *** | 0.862 *** |

| GESTAMP | 4.946 | 0.871 | 1.59 *** | 0.105 # | 553.51 *** | 0.867 *** |

| GRIFOLS | 22.59 | 4.012 | 0.649 *** | −1.855 # | 518.02 *** | 0840 *** |

| IAG | 1.823 | 0.359 | 0.258 * | −0.390 # | 449.19 *** | 0.828 *** |

| INDRA | 7.885 | 1.276 | 0.911 *** | 0.333 # | 533.46 *** | 0.853 *** |

| REPSOL | 9.277 | 1.745 | 0.839 *** | 0.373 # | 548.13 *** | 0.862 *** |

| ROVI | 46.11 | 15.164 | 1.027 *** | 1.534 # | 704.01 *** | 0.868 *** |

| SIEMENS | 23.39 | 5.745 | 0.268 * | −0.140 # | 542.21 *** | 0.853 *** |

| TELEFONICA | 3.847 | 0.380 | 0.831 *** | −0.150 # | 644.9 *** | 0.832 *** |

| Indian stocks | ||||||

| APOLLO | 3118.197 | 1308.941 | 1.056 *** | 1.397 # | 773.12 *** | 0.865 *** |

| BAJAJ | 3416.201 | 497.143 | 0.654 *** | 0.896 # | 464.44 *** | 0.855 *** |

| EXIDE | 172.989 | 16.748 | 0.468 *** | 0.161 # | 482.16 *** | 0.848 *** |

| HAVELL | 978.459 | 296.130 | 1.043 *** | 0.890 # | 649.04 *** | 0.863 *** |

| INFOSYS | 1323.63 | 376.218 | 0.893 *** | 2.161 # | 552.01 *** | 0.860 *** |

| INTERGLOBE | 1594.319 | 377.614 | 1.014 *** | 0.472 # | 566.67 *** | 0.853 *** |

| IOCL | 100.339 | 16.690 | 0.808 *** | 0.777 # | 470.05 *** | 0.863 *** |

| ITC | 205.913 | 19.466 | 0.509 *** | 0.597 # | 618.35 *** | 0.842 *** |

| SUN | 641.808 | 135.725 | 1.059 *** | 1.936 # | 468.18 *** | 0.867 *** |

| TATASTEEL | 833.685 | 401.376 | 1.529 *** | 1.265 # | 857.9 *** | 0.875 *** |

| Training Segment | Test Segment | |||||||

|---|---|---|---|---|---|---|---|---|

| NSE | TI | IA | DA | NSE | TI | IA | DA | |

| Spanish stocks | ||||||||

| ARCELORMITTAL | 0.9890 | 0.0187 | 0.9933 | 0.9664 | 0.9343 | 0.0474 | 0.9335 | 0.9054 |

| EBRO | 0.9694 | 0.0058 | 0.9860 | 0.9568 | 0.8769 | 0.0115 | 0.9438 | 0.9054 |

| GESTAMP | 0.9953 | 0.0082 | 0.9970 | 0.9688 | 0.8937 | 0.0400 | 0.9173 | 0.8649 |

| GRIFOLS | 0.9970 | 0.0046 | 0.9984 | 0.9856 | 0.8579 | 0.0387 | 0.9388 | 0.8784 |

| IAG | 0.9492 | 0.0221 | 0.9686 | 0.9401 | 0.5911 | 0.0562 | 0.7153 | 0.8649 |

| INDRA | 0.9554 | 0.0167 | 0.9788 | 0.9616 | 0.7588 | 0.0415 | 0.8135 | 0.9045 |

| REPSOL | 0.9974 | 0.0047 | 0.9985 | 0.9928 | 0.8997 | 0.0285 | 0.9153 | 0.9189 |

| ROVI | 0.9964 | 0.0094 | 0.9981 | 0.9736 | 0.9130 | 0.0489 | 0.9278 | 0.9054 |

| SIEMENS | 0.9853 | 0.0147 | 0.9916 | 0.9784 | 0.7029 | 0.0646 | 0.8489 | 0.8784 |

| TELEFONICA | 0.9463 | 0.0117 | 0.9649 | 0.9544 | 0.7407 | 0.0220 | 0.7591 | 0.8514 |

| Indian stocks | ||||||||

| APOLLO | 0.9992 | 0.0051 | 0.9997 | 0.9927 | 0.9617 | 0.0406 | 0.9850 | 0.9589 |

| BAJAJ | 0.9739 | 0.0117 | 0.9846 | 0.9709 | 0.8472 | 0.0280 | 0.9048 | 0.9041 |

| EXIDE | 0.9800 | 0.0068 | 0.9900 | 0.9563 | 0.6411 | 0.0309 | 0.8065 | 0.9178 |

| HAVELL | 0.9978 | 0.0068 | 0.9988 | 0.9879 | 0.9626 | 0.0300 | 0.9832 | 0.9589 |

| INFOSYS | 0.9985 | 0.0053 | 0.9991 | 0.9757 | 0.9724 | 0.0244 | 0.9867 | 0.9863 |

| INTERGLOBE | 0.9873 | 0.0126 | 0.9922 | 0.9612 | 0.9473 | 0.0308 | 0.9736 | 0.8767 |

| IOCL | 0.9942 | 0.0006 | 0.9974 | 0.9976 | 0.9352 | 0.0213 | 0.9720 | 0.9452 |

| ITC | 0.9532 | 0.0102 | 0.9708 | 0.9442 | 0.8167 | 0.0205 | 0.8986 | 0.9452 |

| SUN | 0.9968 | 0.0058 | 0.9984 | 0.9854 | 0.9433 | 0.0273 | 0.9747 | 0.9452 |

| TATASTEEL | 0.9984 | 0.0086 | 0.9991 | 0.9976 | 0.9483 | 0.0517 | 0.9788 | 0.9315 |

| Series | ARIMA | SARIMA | BATS | TBATS | ISOMAP-GBR |

|---|---|---|---|---|---|

| Spanish stocks | |||||

| ARCELORMITTAL | (4) | (5) | (3) | (2) | (1) |

| EBRO | (5) | (4) | (3) | (2) | (1) |

| GESTAMP | (5) | (4) | (3) | (2) | (1) |

| GRIFOLS | (5) | (4) | (3) | (2) | (1) |

| IAG | (5) | (4) | (3) | (2) | (1) |

| INDRA | (4) | (5) | (3) | (2) | (1) |

| REPSOL | (4) | (5) | (2) | (3) | (1) |

| ROVI | (5) | (4) | (3) | (2) | (1) |

| SIEMENS | (5) | (4) | (3) | (2) | (1) |

| TELEFONICA | (4) | (5) | (3) | (2) | (1) |

| Indian stocks | |||||

| APOLLO | (5) | (4) | (3) | (2) | (1) |

| BAJAJ | (5) | (4) | (3) | (2) | (1) |

| EXIDE | (4) | (5) | (2) | (3) | (1) |

| HAVELL | (5) | (4) | (2) | (3) | (1) |

| INFOSYS | (4) | (5) | (3) | (2) | (1) |

| INTERGLOBE | (4) | (5) | (3) | (2) | (1) |

| IOCL | (4) | (5) | (3) | (2) | (1) |

| ITC | (5) | (4) | (3) | (2) | (1) |

| SUN | (5) | (4) | (3) | (2) | (1) |

| TATASTEEL | (4) | (5) | (3) | (2) | (1) |

| Series | Global Level | Count of Media Chatter | Local Level | Count of Media Chatter |

|---|---|---|---|---|

| ARCELORMITTAL | OIL (1), BITCOIN (2), MEDIA_COVERAGE_INDEX_WW (3), IBEX35 (4), VIBEX, OAE (5), MEDIA_HYPE_INDEX_WW (6), SENTIMENT_INDEX_WW (7), GOLD (8), INFODEMIC_INDEX_WW (9), SENTIMENT_INDEX_SP (10). | 5 (4 worldwide and 1 local indicators) | MEDIA_COVERAGE_INDEX_WW (1), OIL (2), IBEX35 (3), VIBEX (4), PANIC_INDEX_WW (5), GOLD (6), FAKE_NEWS_INDEX_WW (7), FAKE_NEWS_INDEX_SP (8), BITCOIN (9), PANIC_INDEX_SP (10). | 5 (3 worldwide and 2 local indicators) |

| EBRO | OIL (1), BITCOIN (2), MEDIA_HYPE_INDEX_WW (3), GOLD (4), IBEX35 (5), OAE (6), VIBEX (7), INFODEMIC_INDEX_SP (8), MEDIA_COVERAGE_INDEX_WW (9), SENTIMENT_INDEX_SP (10). | 4 (2 worldwide and 2 local indicators) | OIL (1), BITCOIN (2), MEDIA_HYPE_INDEX_WW (3), GOLD (4), SENTIMENT_INDEX_SP (5), FAKE_NEWS_INDEX_SP (6), INFODEMIC_INDEX_WW (7), MEDIA_COVERAGE_INDEX_SP (8), PANIC_INDEX_WW (9), IBEX35 (10). | 6 (3 worldwide and 3 local indicators) |

| GESTAMP | BITCOIN (1), OIL (2), IBEX35 (3), MEDIA_HYPE_INDEX_WW (4), OAE (5), GOLD (6), MEDIA_COVERAGE_INDEX_SP (7), VIBEX (8), FAKE_NEWS_INDEX_WW (9), SENTIMENT_INDEX_WW (10). | 4 (3 worldwide and 1 local indicators) | OAE (1), OIL (2), BITCOIN (3), IBEX35 (4), VIBEX (5), MEDIA_HYPE_INDEX_WW (6), GOLD (7), SENTIMENT_INDEX_SP (8), FAKE_NEWS_INDEX_WW (9), SENTIMENT_INDEX_WW (10). | 4 (3 worldwide and 1 local indicators) |

| INDRA | BITCOIN (1), MEDIA_COVERAGE_INDEX_WW (2), GOLD (3), OIL (4), INFODEMIC_INDEX_WW (5), IBEX35 (6), MEDIA_HYPE_INDEX_WW, OAE (7), SENTIMENT_INDEX_WW (8), SENTIMENT_INDEX_SP (9), INFODEMIC_INDEX_SP (10). | 6 (4 worldwide and 2 local indicators) | IBEX35 (1), BITCOIN (2), MEDIA_COVERAGE_INDEX_WW (3), GOLD (4), OIL (5), INFODEMIC_INDEX_WW (6), MEDIA_HYPE_INDEX_WW (7), INFODEMIC_INDEX_SP (8), SENTIMENT_INDEX_WW (9), VIBEX (10). | 5 (4 worldwide and 1 local indicators) |

| REPSOL | OIL (1), IBEX35 (2), GOLD (3), BITCOIN (4), INFODEMC_INDEX_WW (5), VIBEX (6), SENTIMENT_INDEX_WW (7), OAE (8), MEDIA_COVERAGE_INDEX_SP (9), MEDIA_COVERAGE_INDEX_WW (10). | 4 (3 worldwide and 1 local indicators) | OIL (1), GOLD (2), BITCOIN (3), MEDIA_HYPE_INDEX_WW (4), OAE (5), VIBEX (6), FAKE_NEWS_INDEX_WW (7), INFODEMIC_INDEX_SP (8), MEDIA_COVERAGE_INDEX_WW (9), INFODEMIC_INDEX_WW (10). | 5 (4 worldwide and 1 local indicators) |

| ROVI | OIL (1), MEDIA_HYPE_INDEX_WW (2), MEDIA_COVERAGE_INDEX_WW (3), BITCOIN (4), OAE (5), GOLD (6), INFODEMIC_INDEX_WW (7), SENTIMENT_INDEX_WW (8), IBEX35 (9), MEDIA_COVERAGE_INDEX_SP (10). | 5 (4 worldwide and 1 local indicators) | OIL (1), MEDIA_HYPE_INDEX_WW (2), MEDIA_COVERAGE_INDEX_WW (3), BITCOIN (4), OAE (5), GOLD (6), INFODEMIC_INDEX_WW (7), SENTIMENT_INDEX_WW (8), IBEX35 (9), MEDIA_COVERAGE_INDEX_SP (10). | 5 (4 worldwide and 1 local indicators) |

| SIEMENS | BITCOIN (1), OAE (2), OIL (3), MEDIA_COVERAGE_INDEX_WW (4), INFODEMIC_INDEX_WW (5), GOLD (6), VIBEX (7), MEDIA_HYPE_INDEX_WW (8), SENTIMENT_INDEX_WW (9), IBEX35 (10). | 4 (4 worldwide indicators) | BITCOIN (1), MEDIA_COVERAGE_INDEX_WW (2), OAE (3), OIL (4), MEDIA_HYPE_INDEX_WW (5), VIBEX (6), MEDIA_COVERAGE_INDEX_SP (7), IBEX35 (8), INFODEMIC_INDEX_WW (9), GOLD (10). | 4 (3 worldwide and 1 local indicators) |

| TELEFONICA | GOLD (1), IBEX35 (2), BITCOIN (3), OIL (4), MEDIA_HYPE_INDEX_WW (5), INFODEMIC_INDEX_WW (6), MEDIA_COVERAGE_INDEX_WW (7), SENTIMENT_INDEX_WW (8), MEDIA_HYPE_INDEX_SP (9), FAKE_NEWS_INDEX_WW (10). | 6 (5 worldwide and 1 local indicators) | IBEX35 (1), OIL (2), GOLD (3), MEDIA_HYPE_INDEX_WW (4), FAKE_NEWS_INDEX_WW (5), INFODEMIC_INDEX_WW (6), MEDIA_HYPE_INDEX_SP (7), MEDIA_COVERAGE_INDEX_WW (8), FAKE_NEWS_INDEX_SP (9), BITCOIN (10). | 6 (5 worldwide and 1 local indicators) |

| Series | Global Level | Count of Media Chatter | Local Level | Count of Media Chatter |

|---|---|---|---|---|

| BAJAJ | NIFTY (1), OIL (2), EM (3), BITCOIN (4), SENTIMENT_INDEX_WW (5), IVIX (6), MEDIA_HYPE_INDEX_WW (7), MEDIA_HYPE_INDEX_IN (8), SENTIMENT_INDEX_IN (9), MEDIA_COVERAGE_INDEX_WW (10). | 5 (3 worldwide and 2 local indicators) | NIFTY (1), EM (2), OIL (3), BITCOIN (4), MEDIA_HYPE_INDEX_WW (5), IVIX (6), MEDIA_HYPE_INDEX_IN (7), MEDIA_COVERAGE_INDEX_IN (8), SENTIMENT_INDEX_IN (9), SENTIMENT_INDEX_WW (10). | 5 (2 worldwide and 3 local indicators) |

| EXIDE | EM (1), IVIX (2), NIFTY (3), MEDIA_COVERAGE_INDEX_WW (4), GOLD (5), OIL (6), MEDIA_HYPE_INDEX_IN (7), BITCOIN (8), SENTIMENT_INDEX_IN (9), MEDIA_COVERAGE_INDEX_IN (10). | 4 (1 worldwide and 3 local indicators) | EM (1), IVIX (2), GOLD (3), MEDIA_COVERAGE_INDEX_WW (4), SENTIMENT_INDEX_IN (5), NIFTY (6), FAKE_NEWS_INDEX_IN (7), INFODEMIC_INDEX_WW (8), MEDIA_HYPE_INDEX_WW (9), MEDIA_HYPE_INDEX_IN (10). | 6 (2 worldwide and 4 local indicators) |

| HAVELL | OIL (1), NIFTY (2), BITCOIN (3), INFODEMIC_INDEX_IN (4), MEDIA_HYPE_INDEX_IN (5), IVIX (6), MEDIA_HYPE_INDEX_WW (7), EM (8), SENTIMENT_INDEX_WW (9), INFODEMIC_INDEX_WW (10). | 5 (3 worldwide and 2 local indicators) | NIFTY (1), OIL (2), MEDIA_HYPE_INDEX_IN (3), INFODEMIC_INDEX_IN (4), PANIC_INDEX_WW, EM (5), FAKE_NEWS_INDEX_WW (6), SENTIMENT_INDEX_WW (7), MEDIA_COVERAGE_INDEX_IN (8), IVIX (9), MEDIA_COVERAGE_INDEX_WW (10). | 6 (3 worldwide and 3 local indicators) |

| INFOSYS | NIFTY (1), BITCOIN (2), OIL (3), EM (4), IVIX (5), MEDIA_COVERAGE_INDEX_WW (6), INFODEMIC_INDEX_IN (7), MEDIA_HYPE_INDEX_WW (8), GOLD, SENTIMENT_INDEX_WW (9), GOLD (10). | 4 (3 worldwide and 1 local indicators) | NIFTY (1), BITCOIN (2), OIL (3), SENTIMENT_INDEX_WW (4), FAKE_NEWS_INDEX_IN (5), MEDIA_HYPE_INDEX_WW (6), IVIX (7), GOLD (8), MEDIA_COVERAGE_INDEX_WW (9), MEDIA_HYPE_INDEX_IN (10). | 5 (3 worldwide and 2 local indicators) |

| IOCL | NIFTY (1), MEDIA_COVERAGE_INDEX_WW (2), OIL (3), MEDIA_HYPE_INDEX_WW (4), BITCOIN (5), IVIX (6), EM (7), SENTIMENT_INDEX_IN (8), SENTIMENT_INDEX_WW (9), GOLD (10). | 4 (3 worldwide and 1 local indicators) | NIFTY (1), OIL (2), MEDIA_COVERAGE_INDEX_WW (3), SENTIMENT_INDEX_IN (4), EM (5), BITCOIN (6), MEDIA_COVERAGE_INDEX_IN (7), IVIX (8), MEDIA_HYPE_INDEX_IN (9), MEDIA_HYPE_INDEX_WW (10). | 5 (2 worldwide and 3 local indicators) |

| ITC | NIFTY (1), OIL (2), MEDIA_HYPE_INDEX_WW (3), MEDIA_HYPE_INDEX_IN (4), IVIX (5), EM (6), SENTIMENT_INDEX_WW (7), GOLD (8), BITCOIN (9), SENTIMENT_INDEX_IN (10). | 4 (2 worldwide and 2 local indicators) | NIFTY (1), OIL (2), MEDIA_HYPE_INDEX_IN (3), MEDIA-HYPE_INDEX_WW (4), SENTIMENT_INDEX_IN (5), SENTIMENT_INDEX_WW (6), PANIC_INDEX_IN, IVIX (7), FAKE_NEWS_INDEX_WW (8), FAKE_NEWS_INDEX_IN (9), GOLD (10). | 7 (3 worldwide and 4 local indicators) |

| SUN | MEDIA_COVERAGE_INDEX_WW (1), NIFTY (2), OIL (3), BITCOIN (4), MEDIA_HYPE_INDEX_WW (5), IVIX (6), MEDIA_HYPE_INDEX_IN (7), EM (8), GOLD (9), PANIC_INDEX_WW (10). | 4 (3 worldwide and 1 local indicators) | MEDIA_COVERAGE_INDEX_WW (1), NIFTY (2), MEDIA_HYPE_INDEX_WW (3), MEDIA_HYPE_INDEX_IN (4), IVIX (5), EM (6), OIL (7), FAKE_NEWS_INDEX_WW (8), INFODEMIC_INDEX_WW (9), BITCOIN (10) | 5 (4 worldwide and 1 local indicators) |

| TATASTEEL | MEDIA_COVERAGE_INDEX_WW (1), MEDIA_HYPE_INDEX_WW (2), NIFTY (3), OIL (4), BITCOIN (5), IVIX (6), EM (7), MEDIA_HYPE_INDEX_IN (8), INFODEMIC_INDEX_IN (9), FAKE_NEWS_INDEX_IN (10). | 5 (2 worldwide and 3 local indicators) | MEDIA_COVERAGE_INDEX_WW (1), NIFTY (2), MEDIA_HYPE_INDEX_WW (3), OIL (4), BITCOIN (5), SENTIMENT_INDEX_IN (6), MEDIA_HYPE_INDEX_IN (7), FAKE_NEWS_INDEX_IN (8), EM (9), PANIC_INDEX_WW (10). | 6 (3 worldwide and 3 local indicators) |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ghosh, I.; Alfaro-Cortés, E.; Gámez, M.; García-Rubio, N. COVID-19 Media Chatter and Macroeconomic Reflectors on Black Swan: A Spanish and Indian Stock Markets Comparison. Risks 2023, 11, 94. https://doi.org/10.3390/risks11050094

Ghosh I, Alfaro-Cortés E, Gámez M, García-Rubio N. COVID-19 Media Chatter and Macroeconomic Reflectors on Black Swan: A Spanish and Indian Stock Markets Comparison. Risks. 2023; 11(5):94. https://doi.org/10.3390/risks11050094

Chicago/Turabian StyleGhosh, Indranil, Esteban Alfaro-Cortés, Matías Gámez, and Noelia García-Rubio. 2023. "COVID-19 Media Chatter and Macroeconomic Reflectors on Black Swan: A Spanish and Indian Stock Markets Comparison" Risks 11, no. 5: 94. https://doi.org/10.3390/risks11050094