An Economic Model for OECD Economies with Truncated M-Derivatives: Exact Solutions and Simulations

, , ,

, , ,

Abstract

:1. Introduction

2. Economics and Mathematical Fundamentals

2.1. Preliminaries

2.2. Inada Conditions

- (a)

- .

- (b)

- .

- (c)

- .

- (d)

- , for any constant .

- (e)

- If f is α-differentiable at , then .

- (f)

- .

- 1.

- It is increasing for both capital and labor force, that is, and .

- 2.

- It has constant returns to scaling, meaning that , for all .

- 3.

- It satisfies and .

- 4.

- Finally, and that .

- Since is satisfied, then . Likewise, holds in view of the fact that .

- This Inada condition readily follows letting .

- Ifthen is of order , for some . Consequently, . In similar fashion, implies . On the other hand, ifthen is of order , which implies that . Finally, we must point out that the case of is handled similarly.

- Observe that holds if and only if , which implied that . But , K and are positive, which yields that . Similarly, implies that , as desired.

3. Solow Model without Migration

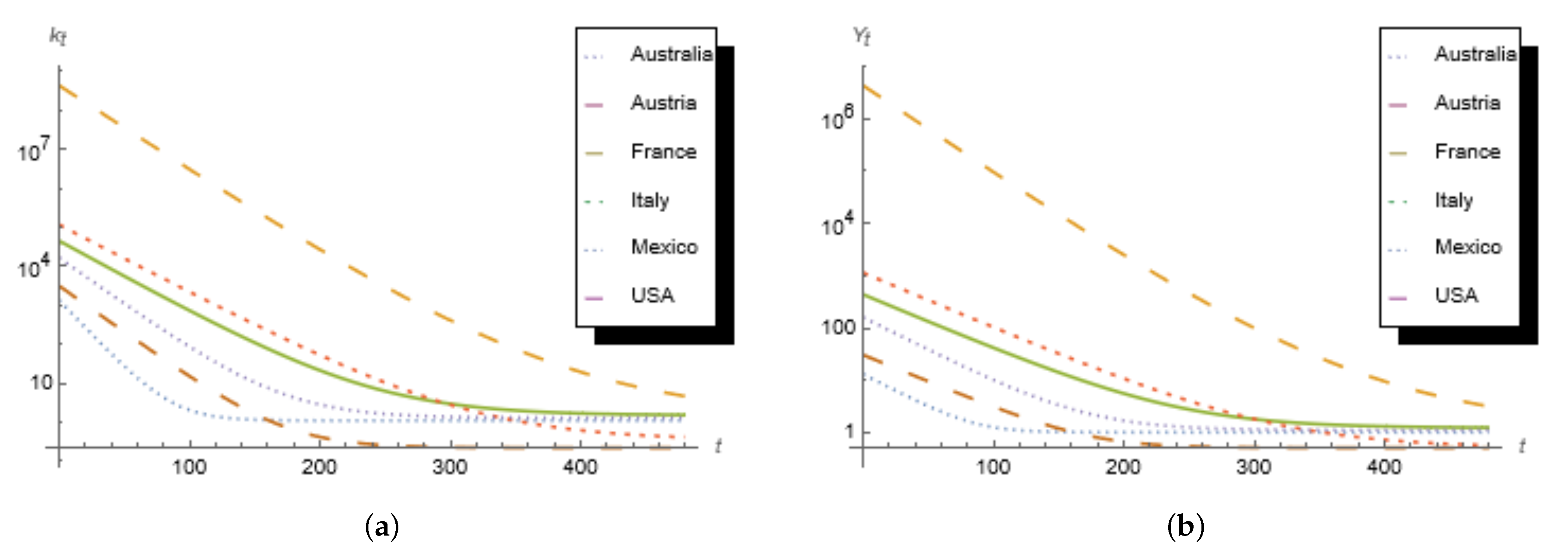

4. Solow Model with Migration

4.1. Closed Analytic Solutions

4.2. Analytical Results

- (i)

- If , then with .

- (ii)

- If and , then with .

- (i)

- Notice that , and are satisfied if and only if . In turn, this implies that .

- (ii)

- Observe now that , and hold if and only if . Moreover, observe that if and only if , where is as in the hypotheses. □

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Solow, R.M. A contribution to the theory of economic growth. Q. J. Econ. 1956, 70, 65–94. [Google Scholar] [CrossRef]

- Swan, T.W. Economic growth and capital accumulation. Econ. Rec. 1956, 32, 334–361. [Google Scholar] [CrossRef]

- Fernández-Anaya, G.; Quezada-Téllez, L.A.; Nuñez-Zavala, B.; Brun-Battistini, D. Katugampola Generalized Conformal Derivative Approach to Inada Conditions and Solow-Swan Economic Growth Model. arXiv 2019, arXiv:1907.00130. [Google Scholar]

- Neto, J.P.J.; Claeyssen, J.C.R.; Ritelli, D.; Scarpello, G.M. Closed-form solution to an economic growth logistic model with constant migration. Ciência E Nat. 2016, 38, 764–770. [Google Scholar] [CrossRef]

- Mankiw, N.G.; Romer, D.; Weil, D.N. A contribution to the empirics of economic growth. Q. J. Econ. 1992, 107, 407–437. [Google Scholar] [CrossRef]

- Barossi-Filho, M.; Silva, R.G.; Diniz, E.M. The empirics of the Solow growth model: Long-term evidence. J. Appl. Econ. 2005, 8, 31–51. [Google Scholar] [CrossRef] [Green Version]

- Brida, J.G.; Maldonado, E.L. Closed form solutions to a generalization of the Solow growth model. Appl. Math. Sci. 2007, 1, 1991–2000. [Google Scholar]

- Accinelli, E.; Brida, J.G. Re-Formulation of the Solow Economic Growth Model Whit the Richards Population Growth Law. GE, Growth, Math Methods 0508006, EconWPA. 2005. Available online: https://econpapers.repec.org/paper/wpawuwpge/0508006.htm (accessed on 22 July 2021).

- Grassetti, F.; Hunanyan, G. On the economic growth theory with Kadiyala production function. Commun. Nonlinear Sci. Numer. Simul. 2018, 58, 220–232. [Google Scholar] [CrossRef]

- Juchem Neto, J.P.; Claeyssen, J.C.R.; Ritelli, D.; Scarpello, G.M. Closed-form solution for the solow model with constant migration. TEMA 2015, 16, 147–159. [Google Scholar] [CrossRef] [Green Version]

- Hilfer, R. Applications of Fractional Calculus in Physics, 1st ed.; World Scientific: Singapore, 2000. [Google Scholar]

- Luo, D.; Wang, J.; Feckan, M. Applying fractional calculus to analyze economic growth modelling. J. Appl. Math. Stat. Inform. 2018, 14, 25–36. [Google Scholar] [CrossRef] [Green Version]

- Tejado, I.; Pérez, E.; Valério, D. Fractional derivatives for economic growth modelling of the Group of Twenty: Application to Prediction. Mathematics 2020, 8, 50. [Google Scholar] [CrossRef] [Green Version]

- Traore, A.; Sene, N. Model of economic growth in the context of fractional derivative. Alex. Eng. J. 2020, 59, 4843–4850. [Google Scholar] [CrossRef]

- Valentina, T.; Vasily, T. Fractional dynamics of natural growth and memory effect in economics. Eur. Res. 2016, 23, 12. [Google Scholar]

- Tenreiro Machado, J.; Duarte, F.B.; Duarte, G.M. Fractional dynamics in financial indices. Int. J. Bifurc. Chaos 2012, 22, 1250249. [Google Scholar] [CrossRef] [Green Version]

- Chaudhary, M.; Kumar, R.; Singh, M.K. Fractional convection-dispersion equation with conformable derivative approach. Chaos Solitons Fractals 2020, 141, 110426. [Google Scholar] [CrossRef]

- Mayo-Maldonado, J.C.; Fernandez-Anaya, G.; Ruiz-Martinez, O.F. Stability of conformable linear differential systems: A behavioural framework with applications in fractional-order control. IET Control Theory Appl. 2020, 14, 2900–2913. [Google Scholar] [CrossRef]

- Bas, E.; Acay, B.; Ozarslan, R. The price adjustment equation with different types of conformable derivatives in market equilibrium. AIMS Math. 2019, 4, 805–820. [Google Scholar] [CrossRef]

- Acay, B.; Bas, E.; Abdeljawad, T. Non-local fractional calculus from different viewpoint generated by truncated M-derivative. J. Comput. Appl. Math. 2020, 366, 112410. [Google Scholar] [CrossRef]

- Sousa, J.V.d.C.; de Oliveira, E.C. A New Truncated M-Fractional Derivative Type Unifying Some Fractional Derivative Types with Classical Properties. Int. J. Anal. Appl. 2018, 16, 83–96. [Google Scholar]

- Andrews, G.E.; Askey, R.; Roy, R. Special Functions; Cambridge University Press: Cambridge, MA, USA, 1999; Volume 71. [Google Scholar]

- Erdélyi, A. Higher transcendental functions. In Higher Transcendental Functions; McGraw-Hill Book Company: New York, NY, USA, 1953; p. 59. [Google Scholar]

{kind=link}

{kind=link}

| Country | s | ||||

|---|---|---|---|---|---|

| Australia | |||||

| Austria | |||||

| France | |||||

| Italy | |||||

| Mexico | |||||

| USA |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Quezada-Téllez, L.A.; Fernández-Anaya, G.; Brun-Battistini, D.; Nuñez-Zavala, B.; Macías-Díaz, J.E. An Economic Model for OECD Economies with Truncated M-Derivatives: Exact Solutions and Simulations. Mathematics 2021, 9, 1780. https://doi.org/10.3390/math9151780

Quezada-Téllez LA, Fernández-Anaya G, Brun-Battistini D, Nuñez-Zavala B, Macías-Díaz JE. An Economic Model for OECD Economies with Truncated M-Derivatives: Exact Solutions and Simulations. Mathematics. 2021; 9(15):1780. https://doi.org/10.3390/math9151780

Chicago/Turabian StyleQuezada-Téllez, Luis A., Guillermo Fernández-Anaya, Dominique Brun-Battistini, Benjamín Nuñez-Zavala, and Jorge E. Macías-Díaz. 2021. "An Economic Model for OECD Economies with Truncated M-Derivatives: Exact Solutions and Simulations" Mathematics 9, no. 15: 1780. https://doi.org/10.3390/math9151780